Finland Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

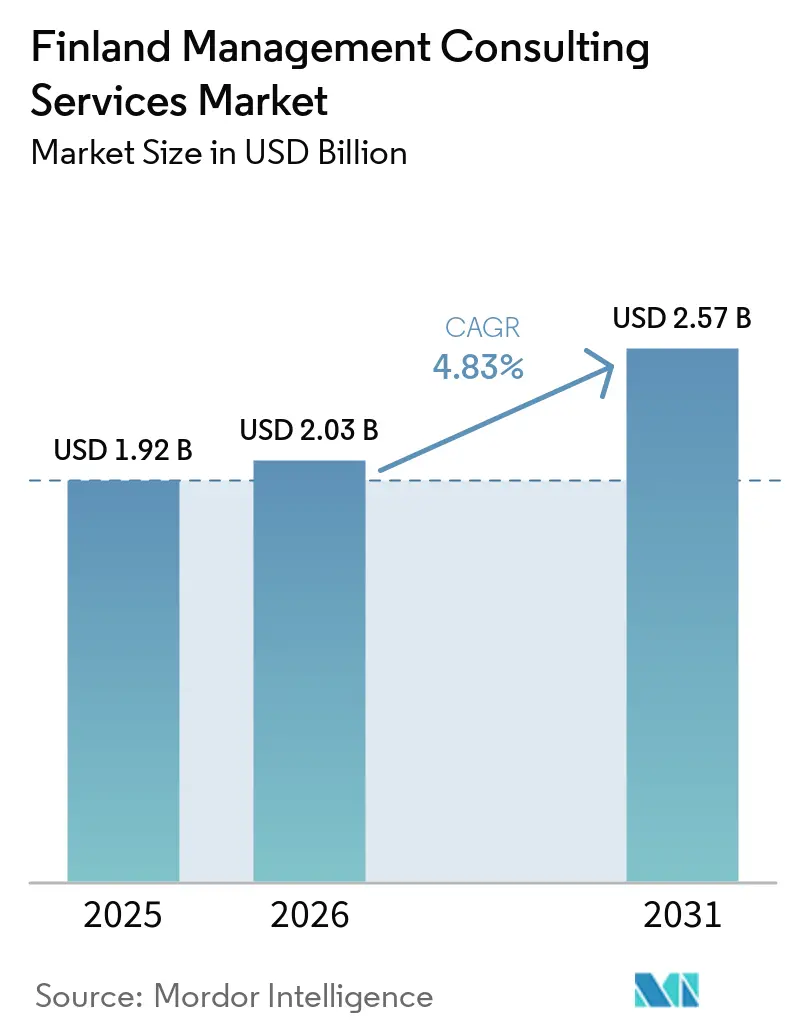

| Base Year Market Size (2025) | USD 1.92 Billion |

| Market Size (2026) | USD 2.03 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland Management Consulting Services Market Analysis by Mordor Intelligence

The Finland management consulting services market size is expected to increase from USD 1.92 billion in 2025 to USD 2.03 billion in 2026 and reach USD 2.57 billion by 2031, growing at a CAGR of 4.83% over 2026-2031. The Finland management consulting services market is benefiting from the government’s Digital Compass program, an ambitious climate-neutrality deadline of 2035, and defense-modernization road-maps tied to NATO membership. Demand is strongest where digital transformation, regulatory compliance, and sustainability intersect with sector-specific needs in energy, banking, and manufacturing. Advisory firms are also capitalizing on an early national pivot toward generative AI, which is reshaping cost structures and delivery models. At the same time, rising wage inflation, free EU-backed advisory schemes for SMEs, and self-service AI platforms are squeezing margins, pushing incumbents toward outcome-based pricing and AI-augmented delivery.

Key Report Takeaways

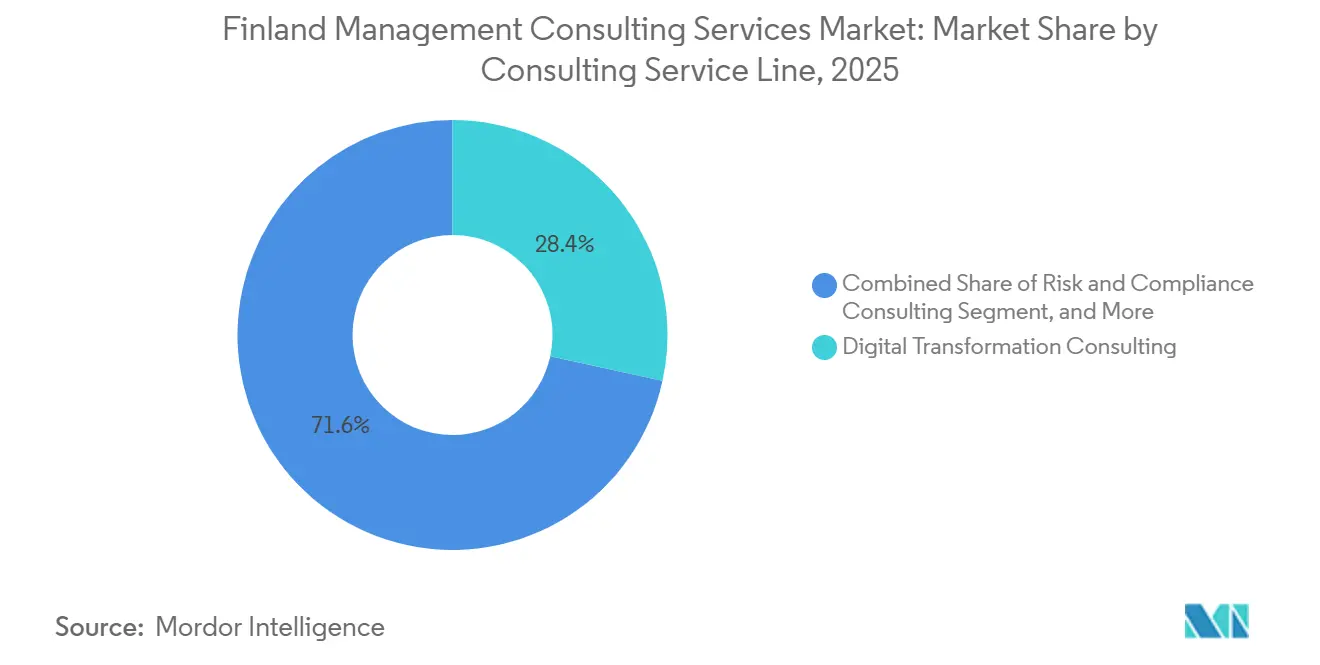

- By consulting service line, Digital Transformation Consulting led with 28.42% revenue share in 2025, while Risk and Compliance Consulting is projected to advance at a 5.19% CAGR through 2031.

- By organization size, Large Enterprises accounted for 63.24% of 2025 spending, whereas the SME segment is forecast to grow at 4.89% over 2026-2031.

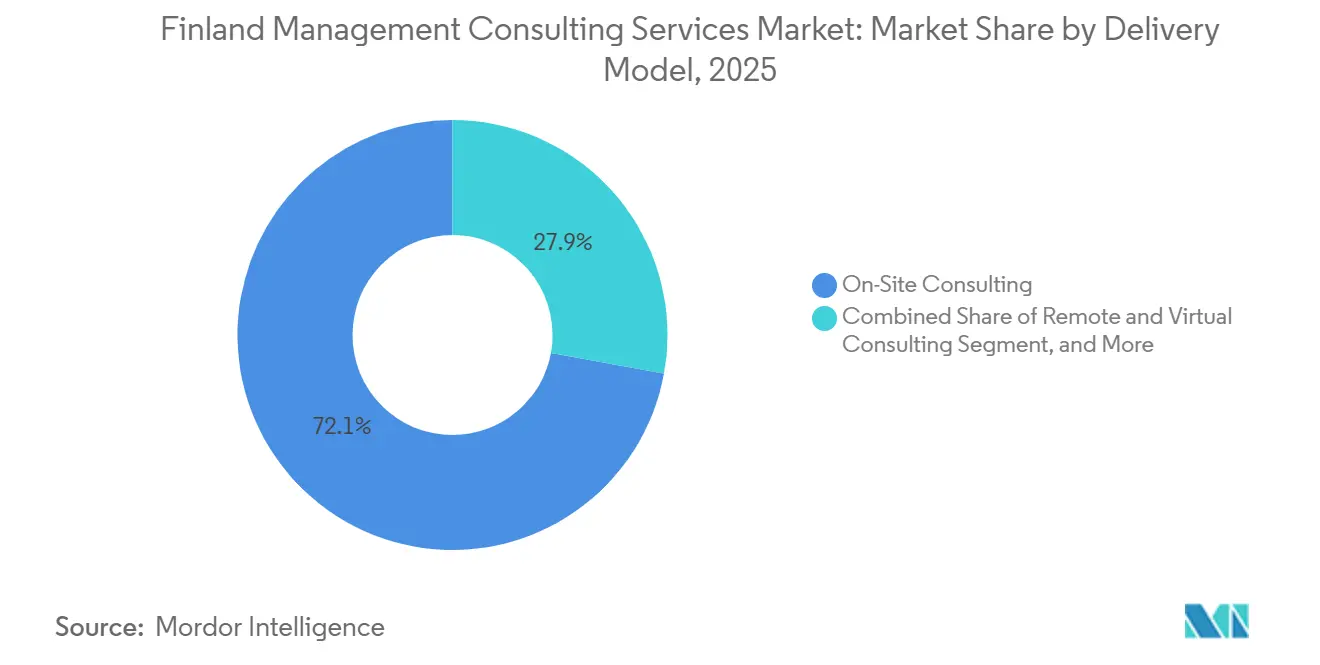

- By delivery model, On-Site Consulting dominated with 72.13% share in 2025, although Remote and Virtual Consulting is set to expand at a 5.23% CAGR to 2031.

- By end-user industry, IT and Telecommunications captured 20.04% of 2025 revenue, while Energy and Resources is expected to post the fastest growth at a 4.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Finland Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-Transformation Spending Boom Across Public and Private Sectors | +1.2% | National, concentrated in Helsinki, Espoo, Tampere | Medium term (2-4 years) |

| Sustainability and Net-Zero Consulting Mandates | +0.9% | National, spillover to Nordic cross-border projects | Long term (≥ 4 years) |

| Generative-AI Readiness and Adoption Programs | +0.8% | National, early adoption in financial services and public sector | Short term (≤ 2 years) |

| EU Chips Act-Linked Semiconductor Ecosystem Build-out | +0.6% | Oulu, Espoo, Tampere semiconductor clusters | Long term (≥ 4 years) |

| NATO Accession Modernization Road-Mapping for Defense and Cybersecurity | +0.5% | National, defense hubs in Helsinki, Tampere | Medium term (2-4 years) |

| Circular Bioeconomy Transitions in Forestry and Packaging Value Chains | +0.4% | Central and eastern Finland forestry regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Spending Boom Across Public and Private Sectors

Large multiyear frameworks from agencies such as DVV and Kela are accelerating cloud-native replacements of legacy platforms, keeping the Finland management consulting services market anchored in high-value enterprise-architecture and change-management work.[1]Gofore Plc, “Gofore Corporate Announcements,” gofore.com Private-sector demand mirrors the public push, with banks, insurers, and manufacturers migrating to SAP S/4HANA and modern supply-chain suites. Vendors are opening innovation centers in Finland to capture this surge, deepening local skills pools while lifting project complexity.[2]CGI, “CGI SAP SCM Innovation Center,” cgi.com As digital public services must be 100% online by 2030, consulting pipelines remain visible well into the next decade. The driver’s influence is amplified by Finland’s cultural preference for trust-based, on-site engagement, which raises average contract values.

Sustainability and Net-Zero Consulting Mandates

Finland’s legally binding 2035 carbon-neutral deadline brings a wave of ESG reporting, Scope 3 emissions mapping, and low-carbon technology deployments. The Corporate Sustainability Reporting Directive alone pulls roughly 500 Finnish companies into audited non-financial disclosures, elevating demand for data-management platforms, assurance frameworks, and carbon-credit monetization advice. High-profile projects such as the Varanto seasonal thermal storage facility demonstrate the capital scale and multidisciplinary consulting needs tied to decarbonizing district heating. Forestry and packaging clients are simultaneously transitioning to circular-bioeconomy models, opening advisory opportunities in life-cycle assessment and compostable-material certification.[3]Bio-Packaging, “Bio-Packaging Horizon Europe Project,” biopackaging.eu Together, these trends keep sustainability workstreams front and center for both global and Finnish-owned consultancies.

Generative-AI Readiness and Adoption Programs

Finland leads the EU in enterprise AI adoption rates yet lags in extracting measurable business impact, creating a strategic-execution gap ripe for consulting support. Government funds, venture grants, and vendor labs are catalyzing pilot projects in financial services, public administration, and health tech. C-suite workshops now emphasize governance, risk management, and ROI modeling to translate sandbox experiments into production-grade solutions. Demand is strongest for operating-model redesigns, use-case prioritization, and systems integration of agentic AI platforms that span SAP, Salesforce, and ServiceNow. As clients push for productivity gains and fixed-price outcomes, firms that embed AI into their own delivery gain a competitive edge in the Finland management consulting services market.

EU Chips Act-Linked Semiconductor Ecosystem Build-out

The national “Chips from the North” strategy targets up to EUR 6 billion (USD 6.78 billion) in investments and 15,000 new jobs by 2035, positioning Finland as a hub for compound-semiconductor R&D and advanced packaging. Consulting demand ranges from subsidy application support and cluster governance to talent-pipeline design and IP strategy. Research institutes in Oulu and Espoo provide pilot-line capacity that startups leverage through consulting-led commercialization road-maps. This ecosystem driver injects fresh revenue pools into the Finland management consulting services market, especially for firms with deep-tech fluency and EU grant-writing expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Consultant-Talent Shortage and Wage Inflation | -0.7% | Helsinki, Espoo, Tampere | Short term (≤ 2 years) |

| Private-Sector Cost-Cutting Amid Slow Domestic Growth | -0.5% | Construction, retail, telecom nationwide | Short term (≤ 2 years) |

| Free EU-Backed Advisory Schemes for SMEs Compress Fee Pools | -0.3% | SME-dense regions nationwide | Medium term (2-4 years) |

| Rise of AI-Driven Self-Service Strategy Platforms | -0.2% | Legal, finance, HR functions nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Consultant-Talent Shortage and Wage Inflation

Vacancies for cloud architects, AI engineers, and cybersecurity specialists far outstrip supply, driving salary premiums that erode project margins. Tampere’s ICT cluster listed 1,340 open consulting roles and 1,800 vacancies needing over six months of training in 2025, reflecting acute scarcity of cloud and AI specialists.[4]Tampere ICT, “Tampere ICT Talent Shortage Report,” tampereict.fi Senior data engineers now command monthly pay up to EUR 8,000 (USD 9,040) above baseline, while hybrid-work consultants average annual income of USD 80,100. Mid-tier firms face a dilemma: absorb costs, pass them to clients, or pivot toward AI-augmented delivery that reduces reliance on scarce talent. The shortage is most severe in engagements requiring security clearances, such as NATO-aligned cyber programs, creating delivery risks and bid delays across the Finland management consulting services market.

Private-Sector Cost-Cutting Amid Slow Domestic Growth

GDP growth forecasts below 1.5% and unemployment near 9% are putting pressure on discretionary spending in telecom, retail, and construction. Elisa’s EUR 40 million (USD 45.2 million) savings plan, including cuts to outsourced services, exemplifies how large clients are tightening external-consulting budgets. High energy prices following the Strait of Hormuz crisis compound the squeeze on industrial margins, leading to deferred or downsized transformation projects. These conditions shorten sales cycles and favor outcome-based or risk-sharing contracts, challenging traditional billable-hour models that still dominate parts of the Finland management consulting services market. Cinode’s Q4 2025 snapshot flags weak construction and real-estate spending as higher interest rates bite.[5]Cinode, “The Nordic Consulting Industry Stabilizes in Q4,” cinode.com BearingPoint’s AI-powered cost-take-out platform shows how consultancies pivot to serve clients prioritizing margin protection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Risk and Compliance Momentum Reshapes Portfolio

Risk and Compliance Consulting is forecast to grow at a 5.19% CAGR through 2031, the fastest pace among service lines in the Finland management consulting services market. Digital Transformation Consulting retained a 28.42% Finland management consulting services market share in 2025, reflecting deep public-sector frameworks and large SAP migration waves. The Finland management consulting services market size for Digital Transformation is moderating in growth as cloud playbooks mature and price competition rises. Operations Consulting remains a steady contributor by linking Industry 4.0 sensors with lean production for metals and machinery clients. HR and Financial Advisory practices feel cyclical swings yet secure niche work in hybrid-work design and complex bank divestments.

Compliance specialists now lead RFP shortlists as firms race to meet CSRD, NIS2, and AI Act milestones that turn fully binding in 2026. Cybersecurity, ESG data management, and supply-chain due diligence projects feed bundled mandates that spill into technology selection and change-management tracks. Strategy houses monetize early thought leadership by packaging modular offerings that align governance frameworks with AI readiness. Sustainability workstreams, circular-economy design, and carbon-credit monetization intersect with core risk mandates, tightening integration across service lines in the Finland management consulting services market. Vendors that cross-staff regulatory lawyers, data engineers, and sector experts win larger transformation bundles.

By Organization Size: Subsidies Accelerate SME Digital Uptake

Large Enterprises captured 63.24% of 2025 spending, anchoring the Finland management consulting services market size with multi-year projects in banking, telecom, and public utilities. Their demand profile centers on core-system replacement, cloud-native modernization, and global process harmonization, often within outcome-based or gain-share contracts. The segment is also the first to insource commodity skills, pressuring vendors to supply senior talent and value-added AI accelerators. Even so, defense, energy, and regulated-sector frameworks keep the large-enterprise pipeline resilient through 2031.

SMEs expand at a 4.89% CAGR on the back of Business Finland Sprint grants, ELY Centre vouchers, and EU Chips Act incentives that offset advisory fees. Lightweight sprints in ERP cloudification, e-invoicing compliance, and export-readiness remain the norm, but chip-cluster startups now request deeper support in IP strategy and talent scaling. Local language service, flexible commercials, and rapid prototypes give mid-tier Finnish consultancies a strong edge in this arena of the Finland management consulting services industry. As procurement reform forces large frameworks to split into lots, boutique players gain new routes to prime positions. Overall, SMEs inject diversity and faster cycle times into the Finland management consulting services market.

By Delivery Model: Hybrid Approach Gains Ground

On-Site Consulting held a dominant 72.13% share in 2025, underscoring cultural norms that prize high-trust face-to-face work and tacit knowledge transfer within the Finland management consulting services market. The physical presence of senior advisors remains a buying criterion for public agencies that manage sensitive citizen data and defense workloads. Yet remote delivery is climbing at a 5.23% CAGR to 2031 as energy shocks raise travel costs and clients normalize AI-augmented collaboration suites. Provider margins benefit because virtual benches can flex across accounts and geographies without per-diem outlays.

Hybrid engagement models mix scheduled site visits with digital whiteboards, speaker-tracking cameras, and agentic meeting archives that mitigate information loss. Consultancies replicate lab environments in client cloud sandboxes, accelerating prototype loops without extending on-site rotations. The Finland management consulting services market now treats pure remote work as viable for code drops and data modeling, while complex change management still commands periodic workshops in Helsinki, Tampere, or Oulu. Firms that master seamless hand-offs between physical and virtual teams boost utilization rates and client satisfaction. Whitelane survey feedback suggests senior-led hybrid crews challenge client thinking more effectively than off-site-only teams.

By End User Industry: Energy and Resources Outpaces IT Spend

IT and Telecommunications supplied 20.04% of 2025 revenue, maintaining the largest vertical slice of the Finland management consulting services market. Telecom clients pivot from 5G rollouts to cost-takeout mandates as competitive pressure mounts, compressing new project pipelines. Banking and insurance groups continue core-system overhauls tied to shifting payment rails and open-banking APIs. Manufacturing accounts focus on edge-AI maintenance and circular-economy retrofits to stay globally competitive.

Energy and Resources posts the highest 4.96% CAGR through 2031 as the national climate strategy enforces carbon-neutrality deadlines. Thermal storage, offshore wind, and hydrogen pilots trigger advisory work in permitting, project finance, and grid integration. Forestry and packaging majors add bio-refinery trials and compostable-material R&D to the mix, broadening sustainability mandates. Public-sector digitalization remains a steady engine given frameworks that run beyond 2030 and reinforce the Finland management consulting services market. Healthcare, transport, and logistics join growth ranks as AI decision support, digital twins, and agentic compliance platforms mature.

Geography Analysis

Helsinki metropolitan area accounts for a majority of the Finland management consulting services market due to the concentration of ministries, Fortune 500 subsidiaries, and venture funding. Framework agreements with DVV, Kela, and municipal ICT offices secure predictable revenue for both global firms and Finnish specialists. Local buyers prioritize providers with Finnish-language fluency and demonstrated success in citizen-facing portals, pushing vendors to retain on-shore leadership teams. The capital region also hosts most innovation centers launched by hyperscalers and consulting-tech alliances, reinforcing its dominance.

Tampere builds critical mass around its ICT cluster, which reported 1,340 open consulting roles in 2025, highlighting labor-market tension that shapes project staffing and rate cards. The city serves as a sandbox for hybrid-work advisory, influencing delivery-model innovation within the Finland management consulting services market. Oulu positions itself as a semiconductor and 5G design hub, attracting chip-ecosystem consulting tied to EU Chips Act funds and advanced-packaging pilot lines. Each regional niche sustains differentiated demand mixes that diversify vendor portfolios while preserving national scale benefits.

Secondary cities such as Turku, Kuopio, and Kajaani inherit health-tech consulting capacity from the recently concluded HealthHub Finland program. Forestry-heavy central and eastern regions fuel circular-bioeconomy advisory, anchored by biorefinery pilots and compostable-packaging projects. Cross-border delivery is rising as Finnish consultancies win frameworks in Germany and Liechtenstein, exporting expertise in digital government and ESG compliance. Procurement reform effective in October 2026 levels the playing field for regional boutiques, signaling gradual diffusion of the Finland management consulting services market beyond the capital corridor.

Competitive Landscape

Global majors, among them Accenture, Deloitte, PwC, KPMG, EY, McKinsey, BCG, and Bain, anchor complex transformation deals and retain the largest billable benches in the Finland management consulting services market. They defend share by pairing regulatory fluency with alliance ecosystems that feature SAP, Microsoft, and NVIDIA accelerators. Finnish-listed players such as Gofore, Tietoevry, Sitowise, and Vincit differentiate through local language delivery, agile pricing, and municipal framework depth. Mid-tier import BearingPoint doubled its Finnish practice from 2021 to 2024 by bundling EU compliance know-how with GenXplore AI cost-takeout tools.

Competitive intensity is rising as generative AI compresses billable-hour models and clients demand outcome guarantees. Vendors respond by building proprietary accelerators, reskilling benches in prompt engineering, and spinning new labs for physical AI, digital twins, and agentic risk management. Talent scarcity drives cross-border acquisitions, evidenced by Gofore’s Esentri deal that secures German public-sector exposure while fortifying on-shore capacity. Price pressure and subcontract-splitting clauses in new procurement rules open headroom for niche specialists focused on quantum, chips, or circular-economy transitions.

Disruption also arrives from AI-driven self-service platforms that allow in-house teams to automate legal review, finance close, and compliance mapping. Consultancies hedge by embedding orchestration layers on top of IBM, ServiceNow, and SAP BTP stacks, offering managed AgentOps that scale beyond traditional staffing pyramids. Early movers protect margins and sustain relevance across all tiers of the Finland management consulting services market.

Finland Management Consulting Services Industry Leaders

Accenture Oy

Deloitte Oy

PricewaterhouseCoopers Oy

KPMG Oy Ab

Ernst and Young Oy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: EY was recognized by NVIDIA as Partner Network GSI Tech Innovation Partner of the Year and rolled out the EY.ai Physical AI platform, an agentic Third-Party Risk Management solution adopted by nearly 20 Finnish clients.

- March 2026: Sitowise appointed a Chief Technology Officer to accelerate digital-infrastructure consulting after winning a EUR 2.7 million-to-EUR 4.5 million railway information-systems contract and a EUR 1 million Digiroad renewal mandate.

- February 2026: Gofore posted February net sales of EUR 19.3 million, reflecting momentum from its EUR 250 million DVV framework, a EUR 44 million Espoo ICT award, and the January acquisition of German consultancy Esentri.

- February 2026: Capgemini divested its Government Solutions unit to focus on private-sector digital transformation, following the May 2025 launch of a generative-AI mainframe-modernization offering and resilient full-year 2025 results.

Finland Management Consulting Services Market Report Scope

The Finland Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Finland management consulting services market?

The market is valued at USD 1.92 billion in 2025 and is forecast to reach USD 2.57 billion by 2031.

Which service line is growing the fastest?

Risk and Compliance Consulting is projected to expand at a 5.19% CAGR through 2031 as firms meet CSRD, NIS2, and AI Act requirements.

Why are SMEs increasing their consulting spend?

EU Chips Act incentives, Business Finland grants, and ELY Centre vouchers lower advisory costs, helping SMEs fund digitalization and circular-economy projects.

How is delivery shifting between on-site and remote models?

On-site work still dominates, but remote and virtual consulting is growing at a 5.23% CAGR as energy costs and AI collaboration tools drive acceptance of hybrid models.

Which industry vertical will generate the quickest growth?

Energy and Resources leads with a 4.96% CAGR, propelled by the 2035 carbon-neutrality mandate and large-scale renewable-energy projects.

What competitive strategies are consulting firms adopting?

Firms combine Finnish-language delivery, AI accelerators, and outcome-based pricing to offset talent scarcity and rising price pressure.

Page last updated on: