Iceland Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

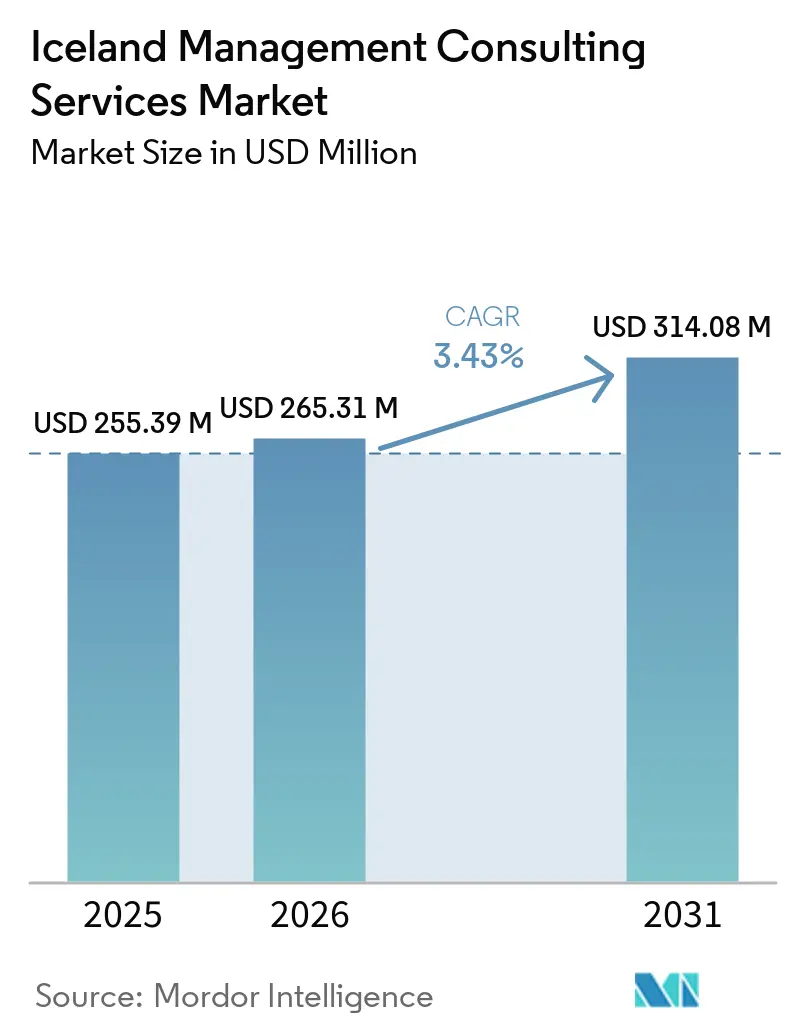

| Base Year Market Size (2025) | USD 255.39 Million |

| Market Size (2026) | USD 265.31 Million |

| Market Size (2031) | USD 314.08 Million |

| Growth Rate (2026 - 2031) | 3.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iceland Management Consulting Services Market Analysis by Mordor Intelligence

The Iceland management consulting services market size is expected to increase from USD 255.39 million in 2025 to USD 265.31 million in 2026 and reach USD 314.08 million by 2031, growing at a CAGR of 3.43% over 2026-2031. Iceland’s gradual shift from pandemic-era emergency digitization toward systematic modernization of public services is widening the advisory opportunity set, while persistent labor shortages continue to push both public and private organizations toward external expertise. Consulting demand now originates less from discretionary expansion projects and more from mandatory compliance with fast-evolving European regulations, government-funded AI programs, and workforce optimization requirements. Banks and insurers are overhauling digital-resilience frameworks, ministries are rolling out Icelandic-language AI applications, and tourism operators are battling margin compression, collectively sustaining fee pools across service lines. Competitive intensity remains moderate as the Big Four leverage Nordic talent networks, yet Icelandic boutiques retain an edge in local-language delivery and municipal procurement. Hybrid project models that blend Reykjavík workshops with remote Nordic specialists are emerging as the default engagement structure because they address cost, talent, and geographic constraints simultaneously.

Key Report Takeaways

- By consulting service line, Strategy Consulting led with 34.47% of revenue in 2025, whereas Digital Transformation Consulting is forecast to advance at a 3.63% CAGR through 2031.

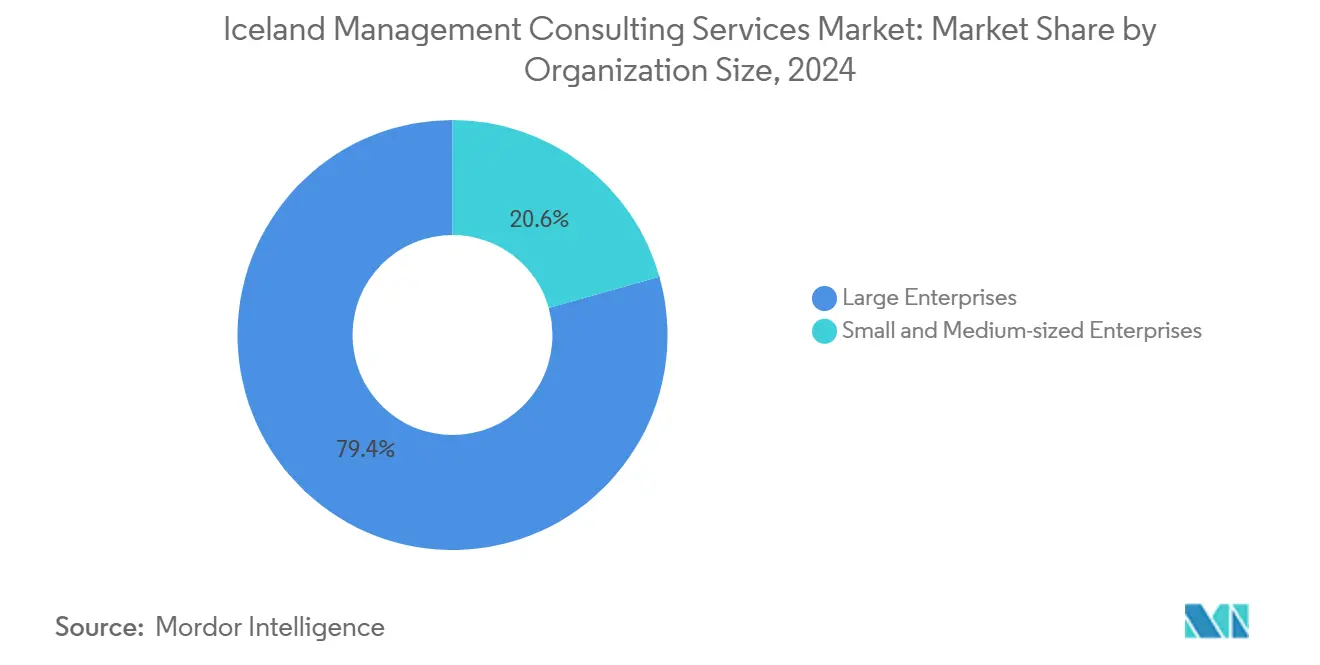

- By organization size, Large Enterprises commanded 68.34% of 2025 spending, while Small and Medium-Sized Enterprises are projected to grow at a 3.51% CAGR through 2031.

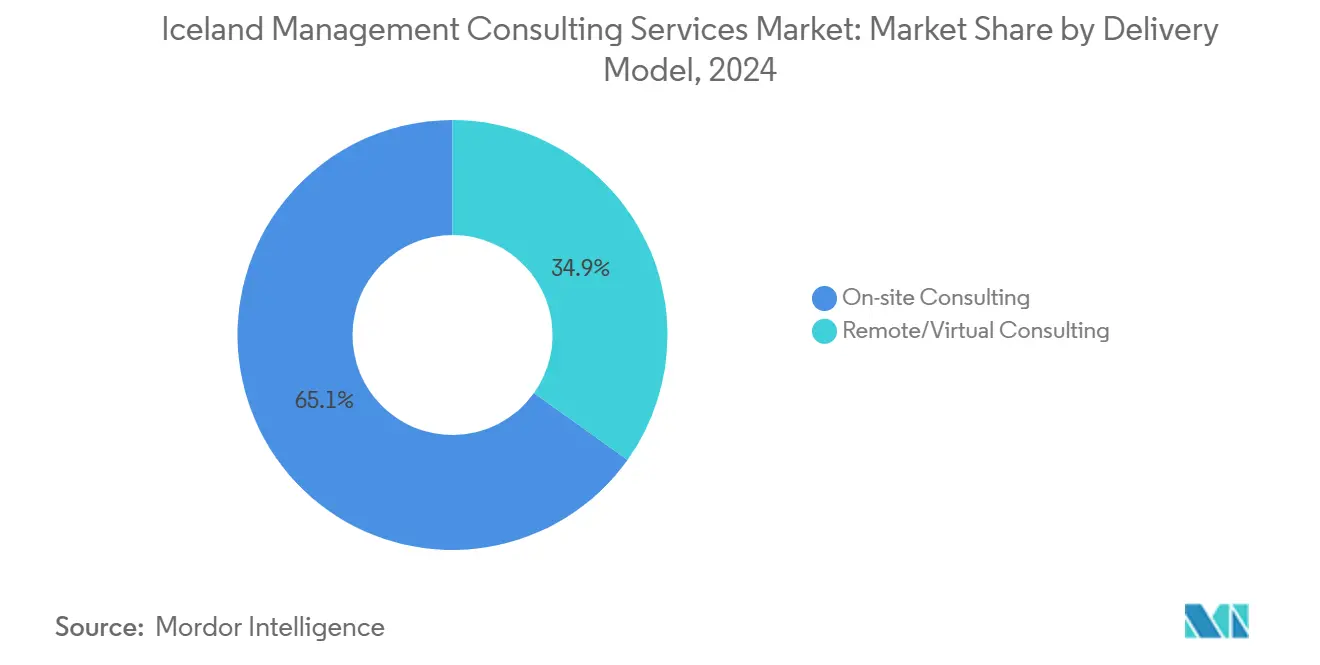

- By delivery model, On-Site Consulting captured 63.97% share in 2025, yet Remote and Virtual Consulting is rising fastest at a 3.72% CAGR to 2031.

- By end user industry, Banking and Insurance contributed 21.39% of 2025 revenue, whereas Public Sector engagements are set to climb at a 3.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Iceland Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Transformation of Icelandic Public Services | +0.9% | National, concentrated in Reykjavík | Medium term (2-4 years) |

| Tourism Rebound Fueling Strategy and Operations Consulting Demand | +0.6% | National, spillover to tourism hubs | Short term (≤ 2 years) |

| Tight Labor Market Accelerating HR-Outsourcing Advisory | +0.7% | National, acute in Reykjavík | Long term (≥ 4 years) |

| EU-Aligned ESG Disclosure Mandates for Icelandic Corporates | +0.5% | National, listed and large private firms | Medium term (2-4 years) |

| Cloud-Native SME Platforms Requiring Local Implementation Partners | +0.3% | National, urban SMEs | Long term (≥ 4 years) |

| Government-Backed AI-Enabled Icelandic Language Tech-Stack Funding 2024-2026 | +0.4% | National, public sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-First Transformation of Icelandic Public Services

Digital Iceland’s third framework tender selected 12 companies across 20 teams in 2024 to redesign citizen-facing portals, retire legacy systems, and integrate ministries through Straumurinn, Iceland’s X-Road interoperability layer.[1]Digital Iceland, “Framework Tender,” DIGITALICELAND.IS The work stream requires continuous API engineering, change management, and cybersecurity governance, locking in multi-year revenue for firms with public-sector credentials. Deloitte Iceland’s co-leadership of the Samrómur speech-corpus project under the 2024-2026 AI Action Plan further cements demand for Icelandic-language natural-language processing expertise. Municipalities are simultaneously digitizing permitting, taxation, and social-service workflows, creating fresh consulting pipelines outside central government. Because implementation deadlines span several budget cycles, this driver underpins both the 3.58% CAGR in public-sector spending and the 3.63% growth expected in the digital transformation service line. The capital region captures the bulk of contract value, yet remote teams in Copenhagen or Oslo are increasingly embedded to fill specialist gaps.

Tourism Rebound Fueling Strategy and Operations Consulting Demand

Iceland welcomed a record number of visitors in 2024, yet the sector’s real GDP contribution was flat because inflation and shorter average stays eroded margins.[2]OECD, “OECD Economic Surveys: Iceland 2024,” OECD.ORG Hotel operators, tour providers, and regional development agencies now hire consultants to fine-tune dynamic pricing, redesign itineraries around visitor-volume caps, and certify sustainability practices that differentiate them from Nordic rivals. Projects tend to be short, data-driven, and focused on yield management, which favors agile boutiques over large, multi-year transformation programs. As operators chase new revenue sources, advisors are embedding digital booking platforms, AI-enabled demand forecasting, and workforce-scheduling tools that stretch limited labor pools. Consulting demand clusters in Reykjavík and the Golden Circle corridor where most hospitality revenues originate, but it is beginning to spill over to secondary hubs as remote delivery lowers engagement costs. Although the tourism driver is cyclical, it boosts near-term advisory pipelines as firms battle cost pressure and regulatory scrutiny tied to sustainability rules.

Tight Labor Market Accelerating HR-Outsourcing Advisory

Iceland’s unemployment rate stood at 4.4% in December 2025, and a record 15,745 residents left the country in 2024, including 5,132 Icelandic citizens, draining mid-career talent from finance, IT, and professional services.[3]Statistics Iceland, “Migration and Citizenship 2024,” STATICE.IS Employers now compete on flexible work design, upskilling, and employer-brand positioning, areas where HR consultants deliver quantifiable returns. Big Four payroll-outsourcing packages targeting SMEs bundle compliance, benefits, and HR analytics, while the AI Action Plan allocates funding for reskilling programs that public agencies outsource to advisory firms. Given slow labor-force growth, this demand is structurally long-lived, making HR outsourcing one of the most resilient fee pools in the Iceland management consulting services market.

EU-Aligned ESG Disclosure Mandates for Icelandic Corporates

Iceland’s slow adoption of the EU Corporate Sustainability Reporting Directive has left listed and large private companies scrambling to build data-collection systems, double-materiality assessments, and assurance processes before phased enforcement begins in 2026.[4]European Commission, “Corporate Sustainability Reporting,” EUROPA.EU Fewer than half of Icelandic executives report having a formal ESG framework, creating a broad readiness gap that consultants are filling with bundled strategy, accounting, and technology services. Demand is strongest among Reykjavík-based banks and utilities that must disclose first, but mid-market exporters are also engaging advisors to align supply-chain metrics with European buyers. Projects typically start with materiality mapping, then expand into software selection, data-governance workflows, and board-level training, producing multi-year revenues. Because disclosures carry regulatory penalties and investor pressure, ESG consulting spend is considered non-discretionary, sheltering fee pools from economic swings. As Icelandic companies file their first CSRD-compliant reports, advisory focus is expected to shift toward assurance and digital-audit automation, extending growth through 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consulting Talent Drain to Mainland Nordics | -0.5% | National, most acute in Reykjavík | Long term (≥ 4 years) |

| Volatile Tourism-Linked GDP Compressing Advisory Budgets | -0.4% | National, outside capital | Short term (≤ 2 years) |

| High Client Price-Sensitivity Outside Reykjavík | -0.2% | Regional, rural municipalities | Medium term (2-4 years) |

| Limited Domestic Scale for Specialized Vertical Practices | -0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consulting Talent Drain to Mainland Nordics

In 2024, 5,132 Icelandic citizens, many of them mid-career professionals, relocated to Norway, Denmark, or Sweden, chasing salaries up to 30% higher than Reykjavík benchmarks and access to larger project pipelines. Local firms lose hard-won expertise, then pay premium rates to import Nordic specialists or rely on remote delivery that can weaken client intimacy. Wage inflation further compresses margins, especially for boutiques that cannot match Big Four compensation structures. Staffing volatility forces project delays and narrower bid pipelines, undermining Iceland’s capacity to meet rising demand in digital government and ESG compliance. The constraint is most acute in the capital region, but its ripple effects touch regional clients who already face thin consultant supply. With demographic growth muted, talent scarcity will remain a persistent brake on consulting expansion through 2031.

Volatile Tourism-Linked GDP Compressing Advisory Budgets

Tourism accounts for roughly 8.8% of Iceland’s GDP, yet its real growth turned negative in 2024 despite record arrivals as higher costs and shorter stays hit operator profitability. When cash flow tightens, hospitality companies and regional governments postpone discretionary strategy work, trimming consulting budgets on everything from brand refreshes to market-entry studies. The effect is felt most outside Reykjavík, where municipal revenues depend heavily on visitor taxes and where advisory spend already faces steep price sensitivity. Firms respond by shortening contract duration and switching to milestone-based fees, but these adjustments rarely offset the abrupt revenue dips caused by a soft tourist season. Because external shocks, volcanic activity, fuel costs, or shifts in European travel sentiment, can swing visitor numbers within a single quarter, advisory demand in tourism regions remains erratic. This volatility adds a -0.4% drag to the market’s overall CAGR forecast as consultancies hedge exposure to discretionary travel spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Strategy Revenue Strong, Digital Transformation Rising

Strategy Consulting accounted for 34.47% of 2025 revenue in the Iceland management consulting services market, reflecting its historic role in anchoring client relationships before expanding into adjacent services. Yet the Iceland management consulting services market share for Strategy Consulting is slowly eroding as ministries and banks shift budgets toward cloud migrations, cybersecurity upgrades, and Icelandic-language AI projects that fall under Digital Transformation Consulting. Digital Transformation engagements are forecast to compound at 3.63% annually because Straumurinn integration, data-governance overhauls, and AI Action Plan milestones require hands-on technical support.

Continued tourism volatility supports Operations Consulting, while HR Consulting benefits from workforce scarcity and record emigration. Risk and compliance projects, especially CSRD readiness and DORA gap assessments, keep growing even in down cycles. Given these cross-currents, the Iceland management consulting services market size allocated to digital transformation is likely to overtake strategy work by 2029, whereas financial advisory and sustainability niches will remain opportunistic, tied to M&A cycles and regulatory rollout timetables..

By Organization Size: Enterprise Wallets Dominate, SME Momentum Builds

Large Enterprises directed 68.34% of consulting spending in 2025, as Iceland’s listed banks, energy majors, and telecom operators pursue multi-year modernization programs. They continue to consume premium strategy, risk, and M&A advisory, and their volume sustains the Iceland management consulting services market size even in muted GDP years.

SMEs, representing 99% of Icelandic businesses, are scaling faster from a smaller base, helped by AI Action Plan grants that cover half of project fees and by SaaS platforms that cut the complexity of cloud adoption. Fixed-fee payroll-outsourcing subscriptions from PwC Iceland illustrate how advisors are productizing services to meet SME budget realities. As these turnkey packages proliferate, the Iceland management consulting services market will see a progressive shift toward higher-volume, lower-ticket SME engagements, balancing the historic dependence on large-enterprise accounts.

By Delivery Model: On-Site Still Leads, Remote Delivery Expands Fast

On-Site Consulting retained 63.97% share in 2025 because C-suite decision-making in Reykjavík favors face-to-face interaction, and certain due-diligence data must remain on-premises. That said, Remote and Virtual Consulting is climbing fastest at a 3.72% CAGR as Icelandic firms normalize video collaboration and increasingly accept Nordic experts working from Copenhagen or Oslo. Hybrid models now dominate multi-month projects, beginning with Reykjavík workshops and segueing into remote sprints.

Clients recognize travel savings and push for outcome-based pricing, compressing daily rates but broadening access to niche expertise that the domestic talent pool lacks. Consequently, the Iceland management consulting services market share attached to purely on-site work is expected to fall below 55% by 2031 as hybrid becomes standard practice.

By End User Industry: Banks Lead, Public Sector Growth Outpaces

Banks and insurers contributed 21.39% of 2025 fees, driven by overlapping DORA, ESG, and anti-money-laundering mandates that demand integrated compliance, data, and cyber-resilience roadmap. The Iceland management consulting services market size tied to banking remains stable because each regulatory wave triggers fresh gap analyses and technology spend.

Public-sector engagements, however, are expanding at a 3.58% CAGR as ministries digitize citizen services and municipalities chase AI Action Plan subsidies. Because these projects are budget-protected and multiyear, they inject predictability into the advisory pipeline. Tourism, fisheries, and retail remain sensitive to visitor flows and disposable income, relegating their consulting demand to short-cycle operations and cost-containment projects that swing with GDP.

Geography Analysis

Reykjavík hosts 64% of Iceland’s population and the headquarters of all major banks, government ministries, and listed companies, concentrating more than 60% of consulting revenue inside the capital region. Proximity to decision-makers lowers sales cycles and favors firms with permanent downtown offices.

Outside the capital, municipalities face thinner budgets and higher price sensitivity, deferring digital transformation unless covered by national grants. Tourism-heavy South Coast and Westfjords exhibit boom-bust consulting demand, while industrial hubs anchored by fisheries and aluminum smelters maintain steadier operations work. Straumurinn and AI Action Plan grants include regional components, but local capacity constraints hamper rapid uptake, reinforcing Reykjavík dominance.

EU-level directives apply nationwide, yet their practical workload concentrates in Reykjavík where legal, finance, and IT staff sit. As remote delivery acceptance rises, boutiques can address regional opportunities without brick-and-mortar expansion, but contract values remain smaller. The geography mix therefore continues to skew heavily toward the capital through 2031, even as remote workflows modestly broaden provincial reach.

Competitive Landscape

The market is moderately concentrated: Deloitte, PwC, KPMG, and EY together capture a majority of fees by pairing audit relationships with advisory cross-sell. Deloitte Iceland leverages its USD 43.5 billion global brand value and Samrómur AI involvement to win language-specific government work. KPMG has pivoted hard into sustainability and risk, while EY and PwC aggressively market payroll-outsourcing to SMEs.

Capacent’s 150-consultant expansion via the RGP Nordic acquisition illustrates how employee-owned boutiques scale quickly to contest mid-market tenders. Nordic specialists such as Implement Consulting Group and Sopra Steria import deep digital-government credentials, challenging Big Four generalists on technical depth. Talent drain remains a battlefield advantage for firms with pan-Nordic staffing pools, while purely domestic players grapple with wage inflation.

Technology alliances, Deloitte’s 2025 partnership with Legora or BCG’s AI analytics for offshore wind, signal a strategic shift toward proprietary platforms that lock in sticky, IP-driven engagements. Overall rivalry is expected to tighten as boutiques exploit remote delivery to reach Reykjavík clients without heavy fixed costs.

Iceland Management Consulting Services Industry Leaders

Accenture plc

Deloitte ehf. (Deloitte Iceland)

PricewaterhouseCoopers hf. (PwC Iceland)

KPMG ehf.

EY Ísland ehf.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Boston Consulting Group published its Nordic AI Inflection Point report covering enterprise AI adoption trends across the region, including Iceland.

- February 2026: Deloitte Iceland showcased graduate recruitment and sustainability advisory offerings at UTmessan, Iceland’s largest tech fair.

- January 2026: Boston Consulting Group partnered with a Nordic offshore-wind developer to deploy AI-driven turbine monitoring.

- November 2025: Boston Consulting Group released a global salmon-demand report highlighting supply-chain resilience priorities for Icelandic fisheries.

Iceland Management Consulting Services Market Report Scope

The Iceland Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

How large is the Iceland management consulting services market today and where is it headed?

The market stands at USD 265.31 million in 2026 and is projected to reach USD 314.08 million by 2031 at a 3.43% CAGR.

Which service line is growing fastest in Iceland's consulting sector?

Digital Transformation Consulting is advancing at 3.63% annually because public-sector digitization and AI programs dominate new spending.

What is driving advisory demand among Iceland's SMEs?

Cloud-native platforms, AI Action Plan grants that subsidize consulting fees, and turnkey payroll-outsourcing packages are lowering adoption barriers for smaller firms.

How are consulting delivery models changing in Iceland?

Hybrid engagements combining Reykjavík workshops with remote Nordic specialists are gaining traction, pushing remote and virtual consulting to a 3.72% CAGR.

Which industries provide the steadiest consulting pipelines?

Banking and Insurance remain the largest spenders due to overlapping compliance mandates, while the Public Sector is the fastest-growing segment thanks to multi-year digital-government programs.

What competitive strategies distinguish emerging Icelandic boutiques?

Local firms focus on Icelandic-language expertise, regional municipal relationships, and price-flexible remote delivery to counter Big Four scale advantages.

Page last updated on: