Central And Eastern Europe Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

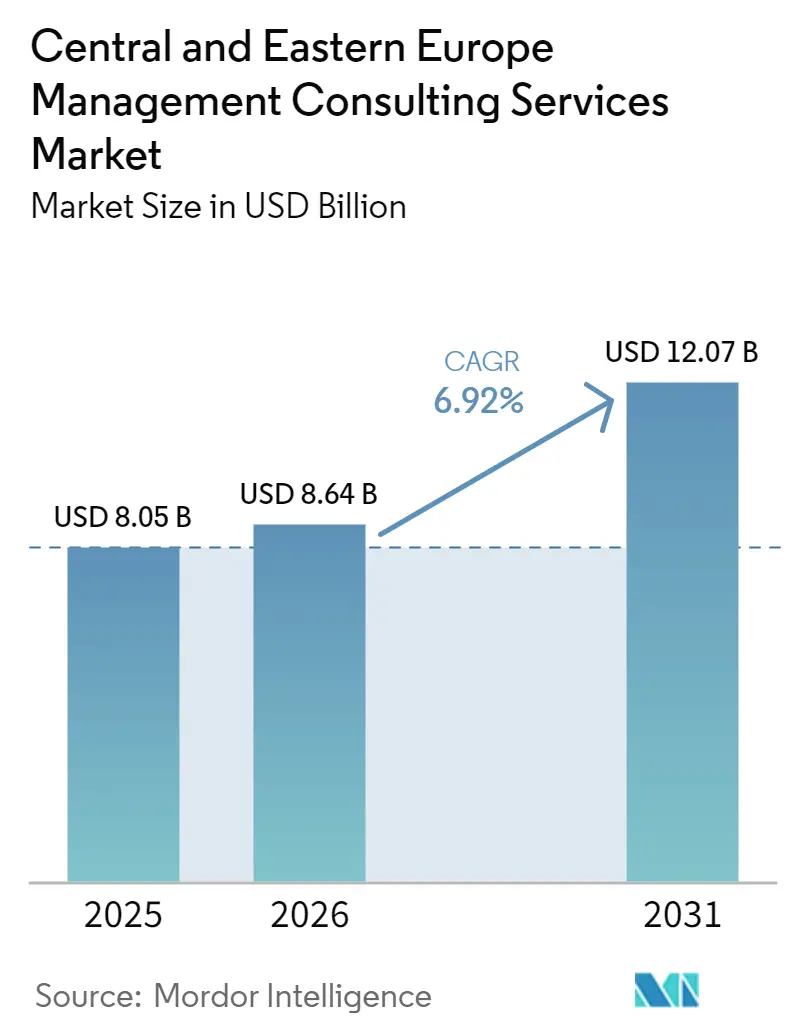

| Base Year Market Size (2025) | USD 8.05 Billion |

| Market Size (2026) | USD 8.64 Billion |

| Market Size (2031) | USD 12.07 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central And Eastern Europe Management Consulting Services Market Analysis by Mordor Intelligence

The Central and Eastern Europe management consulting services market size is projected to expand from USD 8.05 billion in 2025 and USD 8.64 billion in 2026 to USD 12.07 billion by 2031, registering a CAGR of 6.92% between 2026 and 2031. The upward trajectory is anchored in EU-funded digitalization programs, near-shoring from Western Europe, and the enforcement of the Carbon Border Adjustment Mechanism in 2026. Poland captured a 42.13% Central and Eastern Europe management consulting services market share in 2025, while Croatia is set to grow the fastest at a 9.04% CAGR to 2031. Digital transformation engagements dominate thanks to enterprise-wide generative-AI road-maps and cloud migrations, yet risk-and-compliance work is accelerating as the Digital Operational Resilience Act and NIS2 Directive impose new controls. Near-term growth is further lifted by record regional M&A volumes, strong hyperscaler investment into data-center infrastructure, and the spill-over of Ukraine’s reconstruction planning.

Key Report Takeaways

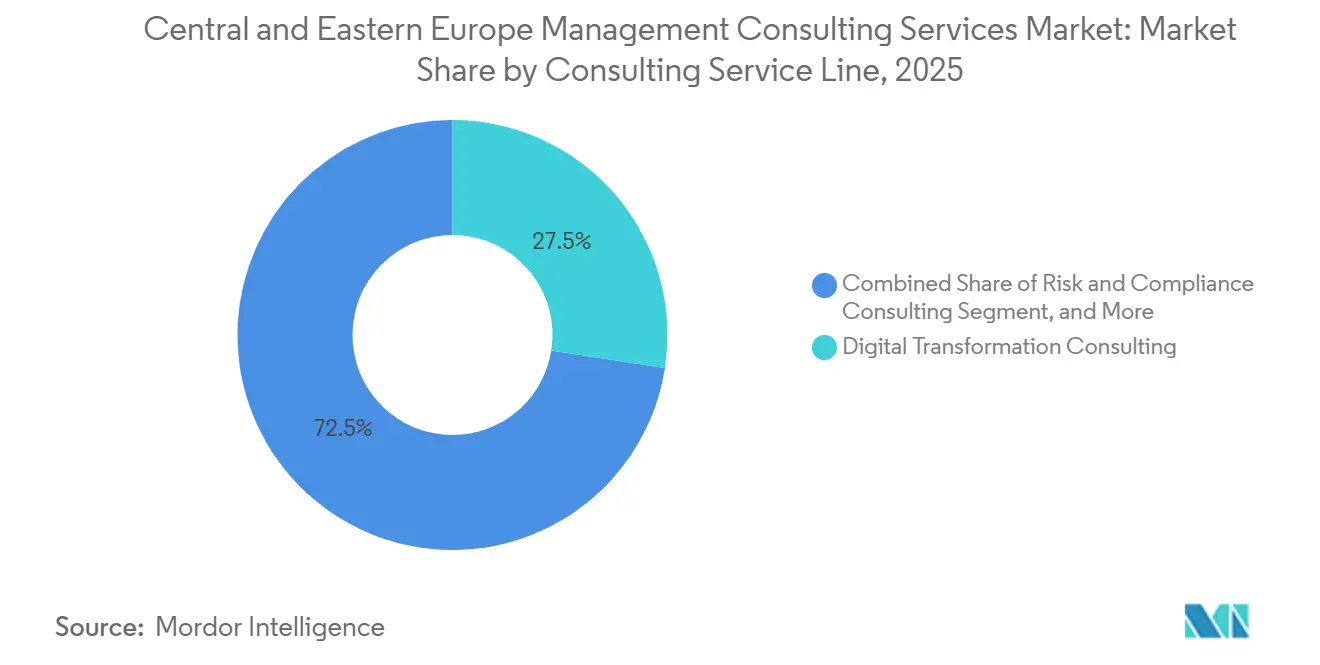

- By consulting service line, digital transformation led with 27.46% revenue share in 2025; risk and compliance is forecast to expand at an 8.09% CAGR through 2031.

- By organization size, large enterprises held 65.84% of 2025 spend, while small and medium-sized enterprises are projected to advance 7.18% annually to 2031.

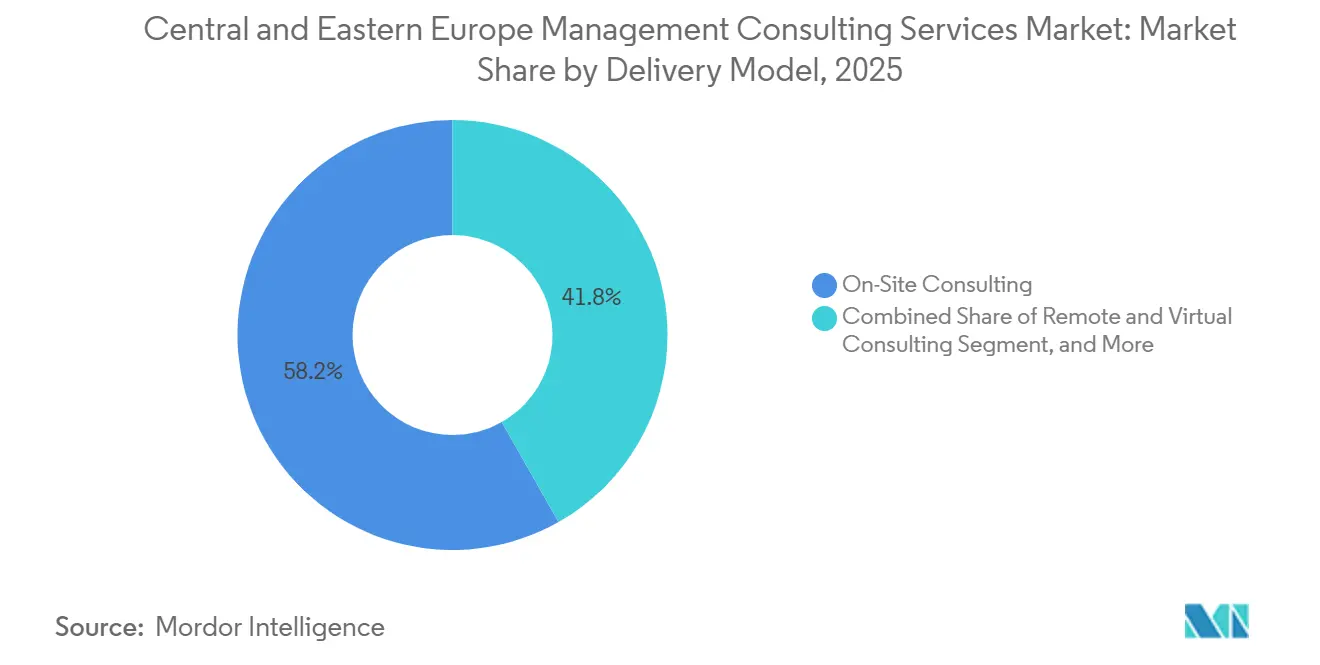

- By delivery model, on-site engagements commanded 58.21% share in 2025 and remote consulting is poised for a 7.32% CAGR through 2031.

- By end-user industry, IT and telecommunications accounted for 22.43% of the Central and Eastern Europe management consulting services market size in 2025, whereas energy and resources is advancing at a 7.48% CAGR to 2031.

- By geography, Poland dominated with 42.13% share of 2025 revenue; Croatia records the highest projected CAGR at 9.04% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Central And Eastern Europe Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EU-Funded Digitalization and Green-Transition Grants | +1.8% | Poland, Czech Republic, Hungary, Croatia, Romania | Medium term (2-4 years) |

| Accelerating Regional M&A Activity Among Mid-Market Firms | +1.5% | Poland, Czech Republic, Romania, Serbia | Short term (≤2 years) |

| Near-Shoring of Western European Corporate Functions to CEE | +1.2% | Poland, Czech Republic, Hungary, Bulgaria | Medium term (2-4 years) |

| Escalating Demand for Generative AI Implementation Road-maps | +1.0% | Poland, Czech Republic, Hungary | Short term (≤2 years) |

| Carbon Border Adjustment Mechanism Compliance Advisory Needs | +0.7% | Manufacturing-intensive regions in Poland, Czech Republic, Hungary | Medium term (2-4 years) |

| Post-War Infrastructure Reconstruction Planning in Ukraine Spill-Over | +0.5% | Poland, Romania, Slovakia, border regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in EU-Funded Digitalization and Green-Transition Grants

NextGenerationEU and the Modernisation Fund together injected more than EUR 3.66 billion (USD 4.03 billion) into Central and Eastern Europe by 2025, immediately triggering advisory mandates for grant structuring, disbursement compliance, and results reporting.[1]European Commission, “Modernisation Fund,” climate.ec.europa.eu Poland collected EUR 1.33 billion (USD 1.46 billion), the Czech Republic EUR 1.05 billion (USD 1.16 billion), and Croatia EUR 170 million (USD 187 million), redirecting consultant focus toward milestone-based engagements that align with EU audit standards. A further EUR 6.2 billion (USD 6.82 billion) earmarked for Poland under NextGenerationEU widens the pipeline of compliance-oriented projects. In parallel, the Digital Europe Programme’s EUR 1.3 billion (USD 1.43 billion) 2025-2027 budget stresses sovereign-cloud, AI, and cyber-security skills, compelling consultancies to build new competency centers. Poland’s DIG.IT grant of PLN 140 million (USD 35 million) aimed at SMEs lowers entry barriers for mid-market advisory firms, reshaping competition.

Accelerating Regional M&A Activity Among Mid-Market Firms

Central and Eastern Europe logged over 1,500 transactions worth EUR 36 billion (USD 40.7 billion) in 2025, a 42% jump from 2024, with Poland leading on 331 deals totaling EUR 13.76 billion (USD 15.5 billion).[2]Forvis Mazars, “Central and Eastern Europe M&A Report 2025,” forvismazars.com Private-equity deal flow climbed 18-24%, reflecting investors’ appetite for 40-50% cost arbitrage relative to Germany and Switzerland. This surge generates consulting needs across every transaction phase, from buy-side diligence to post-merger integration. The EUR 3.8 billion (USD 4.10 billion) Czech-Polish AI gigafactory illustrates cross-border industrial consolidation that requires multi-disciplinary advisory teams for regulatory, supply-chain, and workforce planning.[3]Czech Ministry of Industry and Trade, “Czech-Polish AI Gigafactory,” mpo.cz Clients also demand operational synergies in manufacturing and IT outsourcing, further broadening mandate volume.

Near-Shoring of Western European Corporate Functions to CEE

Western European companies relocated more than 2,081 service centers hosting over 480,000 professionals to Central and Eastern Europe by 2025, chasing 40-50% labor-cost savings and EU regulatory alignment.[4]European Business Services Association, “Accenture Expands Krakow Center,” europeanbusinessservices.com Massive hyperscaler bets, including Microsoft’s USD 1 billion Azure region, Google’s USD 2 billion cloud facility, and Amazon’s USD 2.3 billion investment, validate the region as a digital-infrastructure hub. Visa’s 1,500-seat tech hub and Siemens’ 1,000 new Polish roles back similar moves. As a result, consultancies see rising demand for site selection, workforce design, and change-management services that guide smooth transitions from high-cost Western bases. A 2026 KPMG survey shows 63% of German corporates expect greater CEE revenue contributions within five years, reinforcing the outlook.[5]KPMG AG, “German CEE Business Outlook 2026,” kpmg.com

Escalating Demand for Generative AI Implementation Road-Maps

Generative AI promises EUR 90-100 billion (USD 101-113 billion) of economic value in the region by 2025, with Poland alone contributing up to EUR 40 billion (USD 45 billion).[6]Implement Consulting Group, “Generative AI Economic Potential in CEE,” implementconsultinggroup.com Enterprises need guidance to map use cases, manage data governance, and meet the EU AI Act’s risk-based rules that begin phased enforcement from 2025. BearingPoint’s BeMind platform, claiming 20-30% productivity gains on SAP projects, underscores how firms are productizing AI-augmented delivery. McKinsey’s promotion of Warsaw-based generative-AI specialists echoes the skills priority. Consultancies must, however, balance rapid AI deployment with DORA-imposed resilience standards for financial clients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Consulting Talent Migration to Western Europe | -0.9% | Poland, Czech Republic, Hungary, Romania, Bulgaria | Medium term (2-4 years) |

| Price Pressure From On-Demand Freelance Consultant Platforms | -0.6% | Poland, Czech Republic, Hungary | Short term (≤2 years) |

| Prolonged Public-Sector Procurement Cycles | -0.4% | Poland, Czech Republic, Hungary, Bulgaria | Medium term (2-4 years) |

| Client Budget Volatility Amid Regional Geopolitical Risks | -0.3% | Poland, Romania, Slovakia, border regions | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Chronic Consulting Talent Migration to Western Europe

Eurostat data confirm sustained east-to-west migration, forcing CEE consultancies to pay 30-40% salary premiums to retain senior staff. The Czech Republic and Romania face acute brain-drain pressure, amplified by Romania’s 2025 withdrawal of IT tax break. Global integrators add capacity, Accenture will add 500 Krakow roles by end-2026, intensifying competition for experienced advisors.[7]European Business Services Association, “Accenture Expands Krakow Center,” europeanbusinessservices.com Mid-tier and boutique firms often stretch delivery teams or open offshore centers, but language skills and domain depth remain scarce, extending project timelines and weighing on margins.

Price Pressure From On-Demand Freelance Consultant Platforms

Freelancehunt alone processed 144,000 Polish projects in 2024 at hourly rates EUR 40-150 (USD 45-170), cutting traditional fee bands by up to 60%. SMEs, the fastest-growing client group at 7.18% CAGR, increasingly prefer pay-as-you-go expertise, fragmenting demand. Incumbent firms respond with outcome-based pricing and proprietary IP bundles, but these pivots require up-front investment in data-tracking infrastructure and risk-sharing models. Remote delivery’s rise, slated for a 7.32% CAGR, widens the talent pool and heightens price transparency, sustaining pressure on legacy billing practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Risk and Compliance Leads Expansion

Risk and compliance generated the fastest 8.09% CAGR to 2031, even though digital transformation retained the largest 27.46% 2025 revenue share of the Central and Eastern Europe management consulting services market. The Central and Eastern Europe management consulting services market size for digital transformation held first place because enterprises funded cloud migrations and generative-AI pilots, but growth momentum now tilts toward services that address DORA, NIS2, and CBAM rules.

Rising regulation means banks, utilities, and manufacturers request end-to-end incident-response road maps, vendor audits, and emissions accounting. Strategy work linked to a EUR 36 billion (USD 40.70 billion) M&A pipeline supplies steady engagements, while operations teams standardize processes for 2,081 relocated business-service centers. HR specialists focus on retention programs that counter brain drain, and small sustainability boutiques win niche mandates in green-transition reporting. Altogether, service-line diversity cushions revenue against single-theme slowdowns inside the Central and Eastern Europe management consulting services market.

By Organization Size: SMEs Narrow the Gap

Large enterprises commanded 65.84% of 2025 spending, maintaining scale advantages in multi-year transformations across finance, utilities, and telecom. Yet SMEs are projected to post a sharper 7.18% annual rise, adding fresh clients to the Central and Eastern Europe management consulting services market. Poland’s PLN 140 million (USD 35 million) DIG.IT fund and similar EU grants make advisory costs affordable for mid-market firms.

Modular, fixed-price packages help consultancies win SME deals without extensive proposal cycles. Hybrid delivery lowers travel overhead, and freelance platforms open wider specialist pools. Large corporations, meanwhile, negotiate outcome-based fees, pressing firms to embed analytics that track realized value. That dynamic keeps pricing innovative across every tier of the Central and Eastern Europe management consulting services industry.

By Delivery Model: Remote Work Captures Share

On-site projects still brought 58.21% of 2025 revenue, but remote and virtual engagements are rising at a 7.32% CAGR through 2031. Senior consultants now fly in only for high-stakes workshops, then manage execution from lower-cost hubs, protecting margins inside the Central and Eastern Europe management consulting services market. Secure collaboration suites and AI-powered project trackers reduce concerns about quality control.

Hybrid models spread talent across Poland, Hungary, and Bulgaria to counter Western Europe attrition. Regulated sectors keep some activities on premises, especially data-sensitive testing. Even so, remote capacity expansions in Krakow and Katowice signal permanent preference changes. Clients accept the blended approach because it can trim total advisory bills by 40-50% against Western benchmarks.

By End-User Industry: Energy and Resources Drives Future Demand

IT and telecommunications contributed a leading 22.43% share of 2025 revenue, fueled by USD 5.3 billion in hyperscaler data-center builds. Energy and resources, however, is projected to log the fastest 7.48% CAGR, giving it the strongest growth lane inside the Central and Eastern Europe management consulting services market size. Poland’s 18 GW offshore-wind pipeline, nuclear programs, and Hungary’s Paks II plant require feasibility, supply-chain, and stakeholder advisory.

Manufacturing contracts flow from near-shoring, while banking seeks cyber-resilience playbooks that satisfy DORA. Public agencies purchase grant-absorption guidance but sometimes delay awards. Retailers and logistics players digitize storefronts and warehouses, rounding out a broad vertical mix that shields the Central and Eastern Europe management consulting services market from single-sector cyclicality.

Geography Analysis

Poland retained 42.13% of Central and Eastern Europe management consulting services market share in 2025, anchored by a USD 25.73 billion ICT base, 525,000 tech workers, and 331 M&A deals worth EUR 13.76 billion (USD 15.50 billion). Ongoing EUR 6.2 billion (USD 6.82 billion) NextGenerationEU funds and multiple hyperscaler campuses extend multi-year advisory pipelines. GDP is forecast to grow 3.5% in 2026, keeping corporate budgets healthy.

The Czech Republic benefits from EUR 1.05 billion (USD 1.16 billion) in Modernisation Fund money and a CZK 90 billion AI gigafactory, pushing demand for compliance and automation guidance. Hungary’s 3.8% 2026 GDP expansion and EUR 7.2 billion (USD 8.10 billion) in 2024 FDI reinforce Budapest’s role as a shared-services hub inside the Central and Eastern Europe management consulting services market. Romania rides spill-over work tied to Ukraine reconstruction and growing private-equity interest despite the 2025 loss of IT tax breaks.

Croatia shows the fastest 9.04% CAGR to 2031, aided by tourism digitalization and EUR 170 million (USD 187 million) in green-transition grants. Bulgaria and Slovakia gain from near-shoring projects that relocate finance, HR, and analytics functions. A 2026 KPMG survey of 115 German firms found 56% plan new Polish investments and 35% each in Romania and the Czech Republic, confirming enduring Western interest. Combined, these country trends highlight a heterogeneous but expanding Central and Eastern Europe management consulting services market size that rewards localized go-to-market models.

Competitive Landscape

Global integrators, Accenture, Deloitte, PwC, and McKinsey, hold the largest revenue blocks, yet the market remains moderately fragmented. BearingPoint booked EUR 1.026 billion (USD 1.10 billion) 2025 revenue and unveiled BeMind, an AI platform that can cut SAP project effort by up to 30%, sharpening its edge in outcome-based billing. Deloitte merged its European and Middle East entities into a EUR 22.6 billion (USD 24.90 billion) super-firm, promising seamless cross-border talent pools for the Central and Eastern Europe management consulting services market.

Roland Berger’s March 2026 acquisition of 30-staff Alexec Consulting deepened battery and EV knowledge, aligning with the region’s clean-energy shift. Local technologists such as Asseco, Tietoevry, Sii Poland, and Ciklum leverage cultural fit and modest fee structures to win cloud and custom-software mandates. Ciklum’s USD 10 million GoSolve deal broadened Go-language and DevOps capacity.

Freelancehunt and similar platforms processed six-figure project volumes in 2024, undercutting headline rates yet lacking integrated delivery scope. Competitive pressure compels incumbent firms to invest in remote centers, proprietary accelerators, and specialist training, sustaining healthy rivalry across the Central and Eastern Europe management consulting services market.

Central And Eastern Europe Management Consulting Services Industry Leaders

Accenture PLC

Deloitte Touche Tohmatsu Limited (DTTL)

PricewaterhouseCoopers (PWC)

Ernst & Young Global Limited

KPMG International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Roland Berger purchased Wrocław-based Alexec Consulting to expand battery and EV expertise.

- March 2026: BearingPoint posted EUR 1.026 billion (USD 1.12 billion) 2025 revenue and launched its BeMind AI-powered SAP delivery platform.

- February 2026: EY Global Delivery Services opened a 150-employee center in Katowice, Poland.

- February 2026: McKinsey promoted two Warsaw partners specializing in generative AI and restructuring.

Central And Eastern Europe Management Consulting Services Market Report Scope

The Central and Eastern Europe Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| Bulgaria |

| Czech Republic |

| Hungary |

| Poland |

| Croatia |

| Rest of Central and Eastern Europe |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries | |

| By Geography | Bulgaria |

| Czech Republic | |

| Hungary | |

| Poland | |

| Croatia | |

| Rest of Central and Eastern Europe |

Key Questions Answered in the Report

How large will the Central and Eastern Europe management consulting services market be in 2031?

It is projected to reach USD 12.07 billion by 2031, growing at a 6.92% CAGR from 2026.

Which segment will expand the fastest?

Risk and compliance consulting is forecast to grow at 8.09% CAGR as new EU regulations drive mandatory audits and reporting.

Why are SMEs boosting consulting demand?

EU grant programs subsidize digital projects, letting SMEs access advisory expertise and fueling a 7.18% CAGR in their spending.

What makes Poland the regional consulting leader?

A USD 25.73 billion ICT sector, large talent base, and substantial EU funding give Poland 42.13% 2025 market share and sustained project flow.

How are delivery models evolving?

Hybrid setups combine limited on-site workshops with remote execution teams, cutting costs by up to 50% and expanding talent access.

What competitive strategies stand out among leading firms?

Global integrators launch AI platforms and merge regional entities, while mid-tier and local players pursue targeted acquisitions to deepen domain expertise.

Page last updated on: