Ireland ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

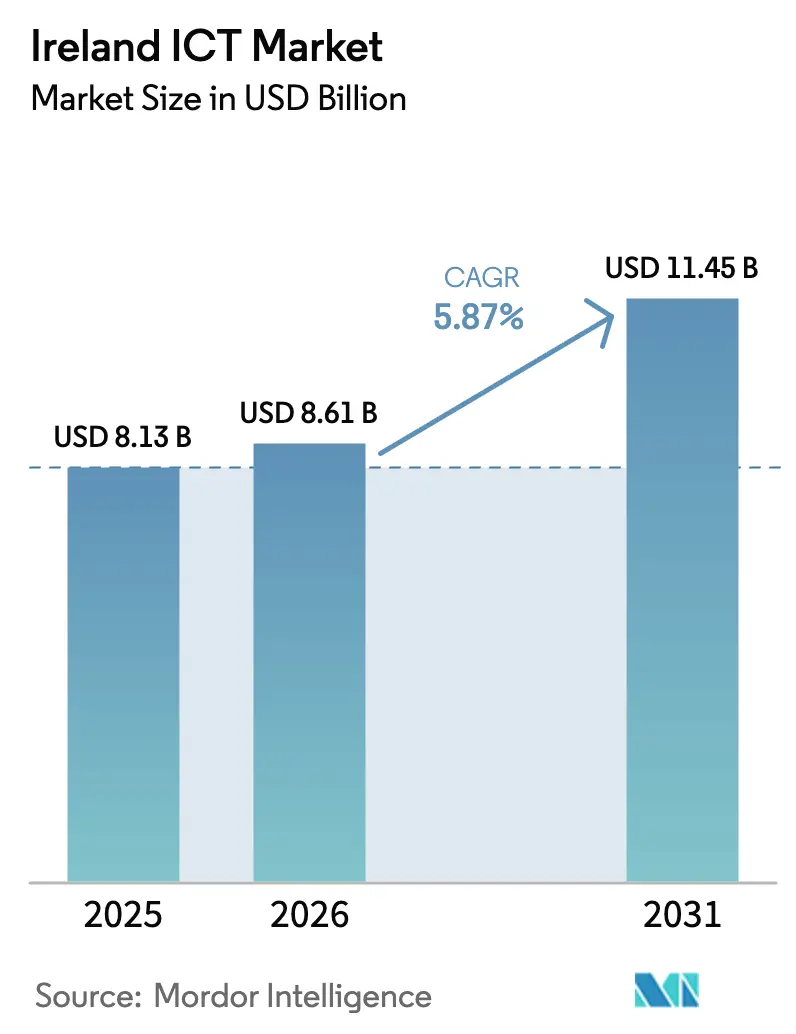

| Base Year Market Size (2025) | USD 8.13 Billion |

| Market Size (2026) | USD 8.61 Billion |

| Market Size (2031) | USD 11.45 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

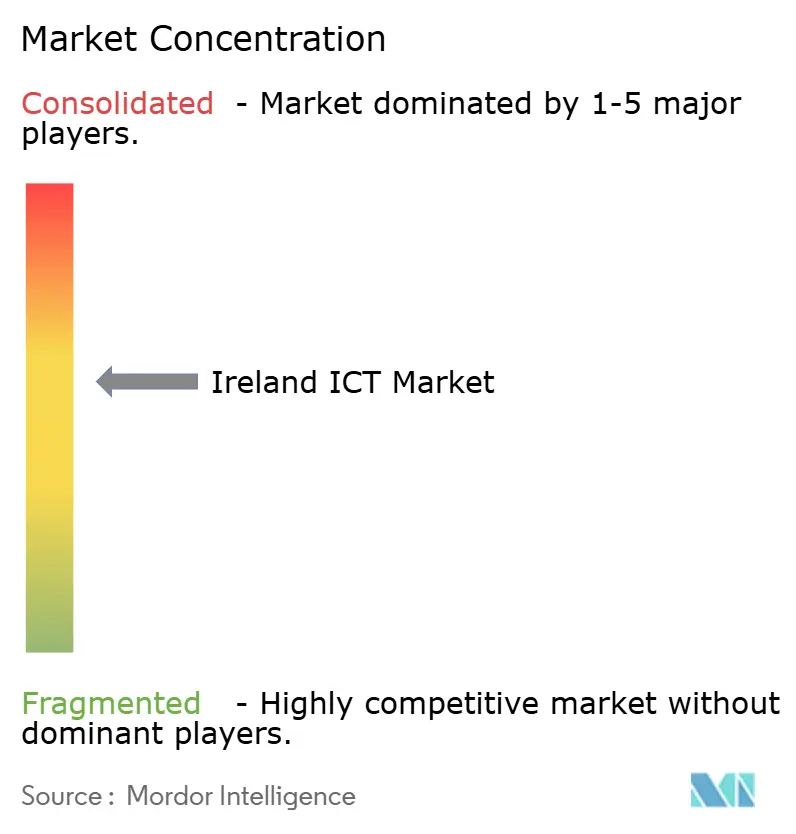

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland ICT Market Analysis by Mordor Intelligence

The Ireland ICT market size is expected to grow from USD 8.13 billion in 2025 to USD 8.61 billion in 2026 and is forecast to reach USD 11.45 billion by 2031 at 5.87% CAGR over 2026-2031. Robust foreign direct investment (FDI), hyperscale data-center construction, and targeted government incentives for digital skills are driving sustained growth. Post-Brexit re-routing of technology capital positions Ireland as Europe’s second-largest exporter of computer and IT services, while the National Digital Strategy 2030 accelerates cloud adoption among smaller businesses. Multinational clusters in Dublin and Cork strengthen the innovation ecosystem, and ongoing 5G/fiber rollouts lower latency barriers that once limited nationwide digital service delivery. Nonetheless, grid capacity limits, cybersecurity talent shortages, and hardware import risks temper the growth outlook. Balancing these forces, Ireland ICT market participants continue to capitalize on tax efficiency, deep research linkages, and a dense network of European-focused regulatory expertise.

Key Report Takeaways

- By type, IT services led with 40.55% of Ireland ICT market share in 2025; cloud services is forecast to expand at a 5.98% CAGR to 2031.

- By enterprise size, the large-enterprise segment held 61.20% of the Ireland ICT market share in 2025, while SMEs record the highest projected CAGR at 5.93% through 2031.

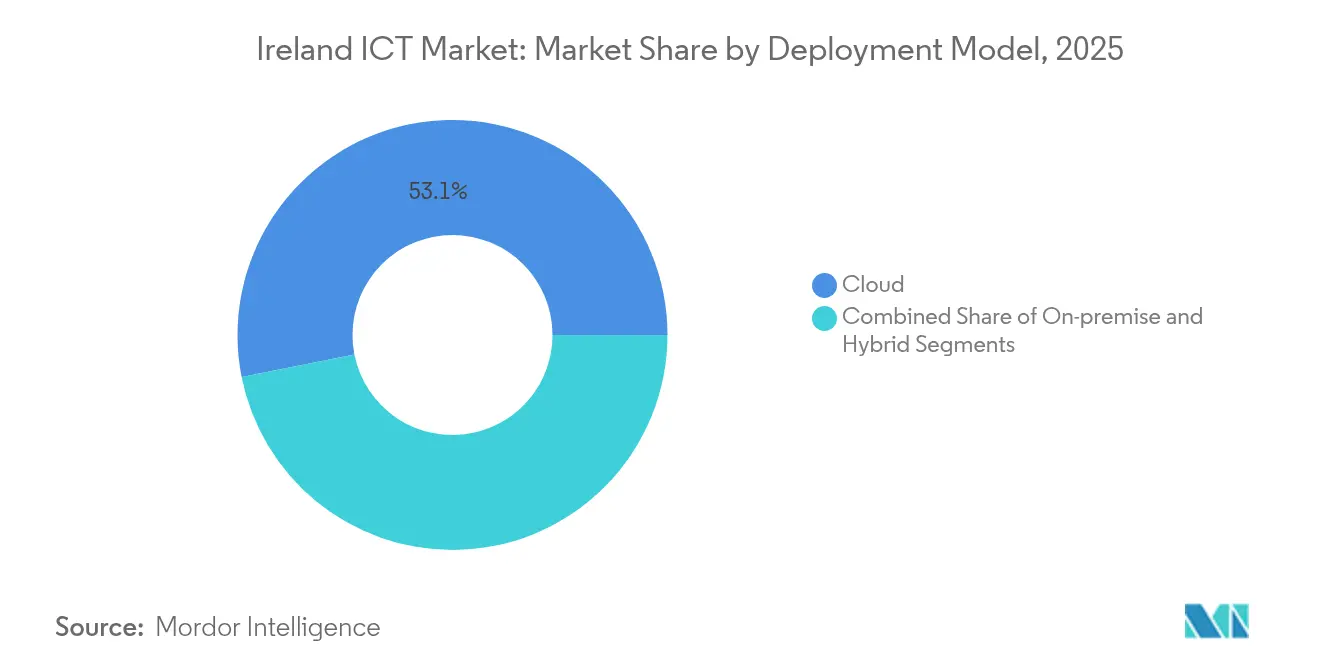

- By deployment model, cloud accounted for 53.12% share of the Ireland ICT market size in 2025 and hybrid is advancing at a 6.22% CAGR through 2031.

- By end-user industry, BFSI commanded 17.52% of the Ireland ICT market size in 2025, whereas gaming and esports is poised for a 6.47% CAGR between 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ireland ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU post-Brexit tech FDI inflows | +1.20% | National, Dublin and Cork | Medium term (2-4 years) |

| National Digital Strategy 2030 subsidies for SMEs | +0.80% | National, rural emphasis | Long term (≥ 4 years) |

| Expansion of hyperscale data centers | +1.50% | National, Dublin-centric | Short term (≤ 2 years) |

| Nationwide gigabit fiber-5G rollout | +0.90% | National, underserved areas | Medium term (2-4 years) |

| AI language localization demand | +0.60% | National tech clusters | Long term (≥ 4 years) |

| Edge computing tax incentives for MedTech | +0.40% | Cork and Galway | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Post-Brexit Tech FDI Inflows

Brexit accelerated a migration of technology investments into Ireland, with over EUR 17 billion in Amazon commitments since 2020 supporting 6,500 local employees and generating EUR 11.4 billion in gross value added. Intel’s Fab 34, Europe’s first EUV mass-production site, extends the hardware base that anchors many ICT service contracts. Employment-permit data show 6,500 new ICT visas in 2024, up 24% year-over-year, underscoring continued labor inflows. Compliance-driven software and consulting projects rise in tandem, as freshly relocated financial institutions align operations with EU directives.

National Digital Strategy 2030 Subsidies for SMEs

The strategy deploys EUR 67 million for infrastructure and skills, targeting 80% basic digital proficiency by 2030 versus 72.9% in 2024. A EUR 1.5 billion National Training Fund earmarked for digital upskilling fuels demand for e-learning platforms and professional-services engagements. Direct supports such as the Grow Digital Voucher lower onboarding costs for cloud, cybersecurity, and automation tools, giving SMEs latitude to contract managed-service providers and accelerate platform migration.

Expansion of Hyperscale Data Centers

Dublin ranks as the world’s third-largest hyperscale cluster outside the United States. Vantage Data Centers alone committed USD 1 billion to new capacity, and Microsoft’s multi-site footprint raises data-center power draw to 21% of Ireland’s electricity use. Knock-on opportunities emerge for cooling, power management, and predictive-maintenance software, while colocation scarcity supports premium pricing. Grid constraints, however, pushed EirGrid to freeze roughly 30 proposals, enhancing the value of current assets.

Nationwide Gigabit Fiber – 5G Rollout

Fiber-to-the-home coverage reached 71% of premises by Q3 2024, with gains of 29% in County Leitrim year-over-year. Virgin Media’s 5 Gbps residential debut and expanding small-cell footprints unlock low-latency use cases in IoT and private networks. Operators require network-orchestration, slicing, and monitoring solutions to optimize traffic and monetize new service tiers, creating additional revenue lanes for software vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of advanced cloud security talent | -0.70% | National, Dublin corridor | Short term (≤ 2 years) |

| Grid constraints on new data centers | -0.90% | National, Dublin region | Medium term (2-4 years) |

| Hardware import supply-chain risks | -0.50% | National | Short term (≤ 2 years) |

| Sustainability-reporting compliance burden | -0.30% | National, large enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Advanced Cloud Security Talent

Demand for cloud-security professionals meets only 9% of open roles, elevating project lead times and inflating salaries by 40% above standard IT positions. Although Technology Ireland ICT Skillnet has trained 2,500 specialists since 2005, industry still needs roughly 10,000 more workers. Limited capacity slows zero-trust and AI-driven defense rollouts, prompting some firms to delay ambitious cloud migrations or rely on offshore managed-security centers.

Grid Constraints on New Data Centers

EirGrid’s moratorium on fresh hyperscale discussions stems from supply-demand imbalance as data centers already consume one-fifth of national electricity. Companies now explore on-site generation or provincial locations, adding capital intensity and operational complexity. High-density AI workloads face the greatest bottlenecks, potentially diverting inward investment to countries with surplus renewable capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Dominance Drives Digital Transformation

IT services generated 40.55% of the Ireland ICT market size in 2025, reflecting entrenched multinational outsourcing and an ecosystem of nearly 900 software firms. Hardware revenues remain steady as hyperscale builders source servers, power infrastructure, and network gear for Dublin campuses. Cloud services lead expansion at a 5.98% CAGR, propelled by AI workloads and compliance requirements that favor scalable, audited environments.

Recurring revenue from managed platforms strengthens resilience against currency swings, while localized software engineering exemplified by Microsoft and SAP development hubs anchors intellectual property creation. Communication services profit from back-haul upgrades and enterprise 5G pilots, and security offerings see double-digit growth as firms adopt zero-trust architectures to meet GDPR and emerging EU AI Act mandates.

By Enterprise Size: Large-Enterprise Leadership with SME Acceleration

Large enterprises held 61.20% of Ireland ICT market share in 2025 on the strength of U.S. multinationals that choose Ireland for EU headquarters and enjoy a 12.5% corporate tax rate. These firms drive deep professional-services engagements spanning compliance, analytics, and DevSecOps.

SMEs, buoyed by voucher schemes and training grants, chart the fastest path at 5.93% CAGR. Reduced up-front outlays and modular cloud applications let smaller firms automate finance, customer engagement, and logistics workflows, narrowing digital-maturity gaps with larger peers.

By Deployment Model: Cloud Leadership with Hybrid Momentum

Cloud deployment represented 53.12% of the Ireland ICT market share in 2025, fueled by hyperscaler presence and low-latency transatlantic routes. Financial-services and life-sciences stakeholders increasingly mix on-premise safeguards with cloud elasticity, propelling the hybrid model to a 6.22% CAGR.

Scarce grid allotments raise demand for workload portability, while edge nodes in Cork and Galway handle real-time MedTech data under recently announced tax incentives. On-premise estates persist for sovereign-data workloads and latency-critical trading applications, sustained by fiber penetration that now reaches 71% of national premises.

By End-user Industry Vertical: BFSI Leadership with Gaming Disruption

BFSI accounted for 17.52% of 2025 spending as banks deploy AI-driven risk tools and fintechs exploit passporting certainty within the EU . Cloud-native core-banking overhauls, open-banking APIs, and RegTech services provide steady contract flows.

Gaming and esports accelerates at 6.47% CAGR, underpinned by a 32% refundable Digital Games Tax Credit and the launch of the National Esports Centre in Cork. Energy, utilities, and manufacturing verticals adopt smart-grid analytics and Industry 4.0 platforms, while public-sector agencies digitize citizen services using Recovery and Resilience Facility funds.

Geography Analysis

Dublin contributes 42% of national GDP and hosts eight of the world’s top-10 technology companies, producing network effects that reduce procurement friction and foster cross-vendor innovation . The city’s data-center corridor benefits from robust subsea-cable connectivity to North America, bolstering low-latency cloud services.

Cork ranks second, specializing in semiconductor R&D and advanced manufacturing around Apple and Intel affiliates. IDA Ireland’s semiconductor initiative and EUR 65 million National Grand Challenges Programme funnel resources into quantum computing prototypes and photonics startups, diluting Dublin’s historical dominance.

Provincial diversification gains traction as National Broadband Ireland pushes FTTH beyond 70% coverage and employment-permit data show Dublin sourcing less than half of new ICT hires for the first time in 2024. Rural hubs exploit lower real-estate costs and renewable-energy availability to attract edge-computing and AI-inference nodes, mitigating grid stress in the capital.

Competitive Landscape

Global incumbents and nimble indigenous players shape a moderately concentrated field. Amazon, Microsoft, and Google leverage hyperscale footprints to bundle infrastructure, AI platforms, and industry clouds, while Dell, Cisco, and Intel supply core hardware and edge devices.[1]Cisco Systems, “2024 Cisco Full Annual Report,” Cisco.com Irish-grown firms such as FINEOS and Workhuman compete in HRTech and InsurTech niches, exploiting local data-privacy expertise to win EU contracts.

Strategic moves center on ecosystem lock-in Microsoft’s regional campus delivers Azure, Dynamics 365, and GitHub services, while AWS adds Outposts racks to align with hybrid demand. Cisco’s USD 28 billion acquisition of Splunk intensifies observability competition and spurs channel partners to offer integrated security analytics.

White-space opportunities persist in AI localization, quantum-ready encryption, and CSRD-compliant sustainability reporting. Service providers able to stitch compliance, edge orchestration, and multi-cloud cost governance into cohesive offerings are positioned to outperform.

Ireland ICT Industry Leaders

Microsoft Corporation, Inc.

Oracle Corporation

Intel Corporation

Amazon Web Services Inc.

Alphabet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Technology Ireland ICT Skillnet expanded cloud-security and AI training.

- March 2025: Virgin Media launched 5 Gbps residential broadband in Dublin.

- March 2025: Ericsson committed EUR 200 million to Athlone R&D, adding 200 engineering roles.

- February 2025: Dell Technologies posted USD 95.6 billion revenue, with Infrastructure Solutions Group up 29% YoY.

Ireland ICT Market Report Scope

Information and communication technologies, or ICT, is a broader term for information technology (IT). It refers to all communication technologies, such as wireless networks, the Internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services, that enable users to store, access, transmit, retrieve, and manipulate information in digital form.

The Irish ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of enterprise (small and medium enterprise and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail, and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market size and forecasts are provided in value (USD) for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

How large is the Ireland ICT market in 2026?

It is valued at USD 8.61 billion with a projected 5.87% CAGR through 2031.

Which segment grows fastest between 2026-2031?

Cloud services expand at 5.98% CAGR, driven by compliance and AI workloads.

What share do large enterprises hold?

They command 61.20% of total spending, reflecting multinational concentration.

Where does Ireland rank for hyperscale data centers?

Dublin is the world’s third-largest hyperscale hub outside the United States.

What is the main growth restraint?

Grid capacity limits that delay new data-center projects reduce near-term expansion.

Page last updated on: