Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.28 Billion |

| Market Size (2026) | USD 17.79 Billion |

| Market Size (2031) | USD 27.72 Billion |

| Growth Rate (2026 - 2031) | 9.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand ICT Market Analysis by Mordor Intelligence

The New Zealand ICT market size is expected to grow from USD 16.28 billion in 2025 to USD 17.79 billion in 2026 and is forecast to reach USD 27.72 billion by 2031 at 9.29% CAGR over 2026-2031. Continuous public-sector digitization, rapid cloud-region rollouts and accelerating enterprise demand for artificial intelligence are the primary engines behind this expansion. Large-scale infrastructure investments by Microsoft, AWS and Google have materially lowered latency and data-residency concerns, spurring organizations to migrate complex workloads. Enterprises are simultaneously adopting renewable-powered data-center capacity to satisfy environmental targets, while Māori data-sovereignty requirements encourage hybrid deployment models that keep sensitive datasets onshore. Skills shortages and escalating cyber threats temper the growth outlook, yet sustained government funding for e-government, digital health and rural connectivity keeps the New Zealand ICT market firmly on an upward trajectory.[1]Digital.govt.nz, “Māori, Pacific Peoples, Ethnic Communities and GenAI,” digital.govt.nz

Key Report Takeaways

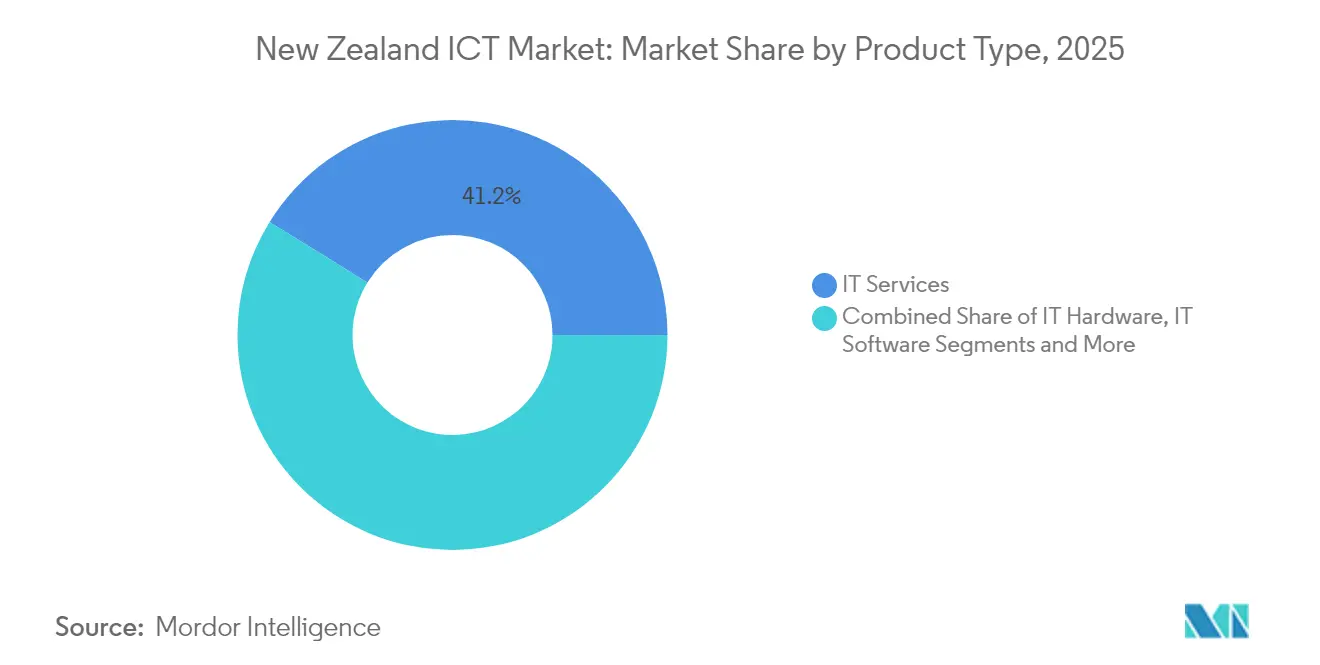

- By product type, IT Services led with 41.19% revenue share in 2025, whereas IT Security is on track for the fastest 9.55% CAGR through 2031.

- By enterprise size, Large Enterprises captured 61.94% of the New Zealand ICT market share in 2025; SMEs are expanding at a 10.05% CAGR through 2031.

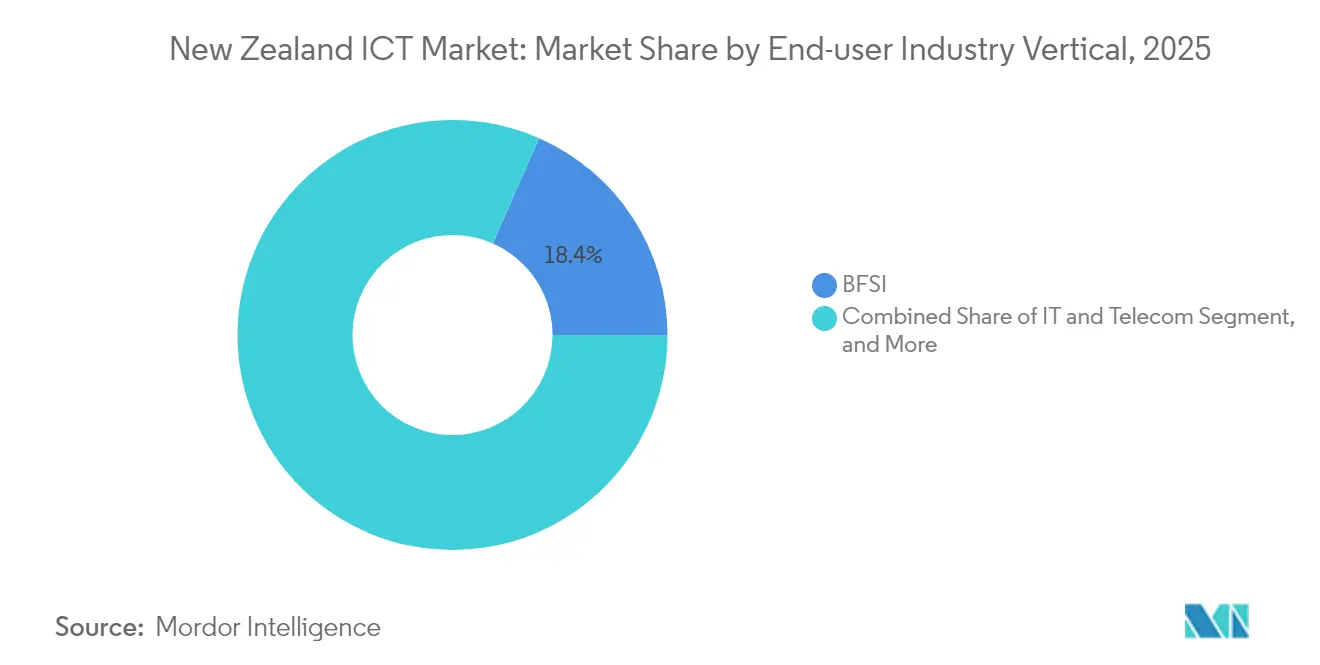

- By end-user industry, BFSI accounted for 18.40% of 2025 revenue, yet healthcare and life sciences are advancing at a 10.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

New Zealand ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust growth of technology exports | +1.8% | National – Auckland and Wellington clusters | Medium term (2-4 years) |

| Hyperscale cloud-region investments | +2.1% | National – primary DCs in Auckland | Short term (≤ 2 years) |

| Government spending on e-health and e-gov | +1.5% | National – early rollouts in urban centers | Medium term (2-4 years) |

| Rapid adoption of AI-ML solutions | +1.9% | National – BFSI and manufacturing leaders | Short term (≤ 2 years) |

| Renewable-powered data centers | +1.2% | National – renewables-rich regions | Long term (≥ 4 years) |

| Māori data-sovereignty initiatives | +0.9% | National – government and research sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Investments Drive Digital Infrastructure Modernization

Public-sector digital programs continue to steer capital toward cloud, cybersecurity and digital-health platforms. The Ministry of Business, Innovation and Employment allocated NZD 50 million (USD 29.23 million) over four years to reinforce national cyber-defense and to modernize e-government services. Simpler vendor-qualification pathways now allow SME tech providers faster entry into public contracts, boosting competitive intensity across the New Zealand ICT market.[2]MinterEllisonRuddWatts, “Cyber Risk and Cyber Insurance: Themes and Predictions,” minterellison.co.nz In parallel, Treaty of Waitangi-aligned procurement policies stimulate demand for culturally appropriate technology solutions, differentiating this landscape from other developed economies. Government endorsements also catalyze private investment: Te Tumu Paeroa’s role as anchor tenant for Microsoft’s local cloud region validated hyperscale commitments and encouraged further data-center builds.[3]Data Center Dynamics, “Te Tumu Paeroa to Be Anchor Tenant in Microsoft’s New Zealand Cloud Region,” datacenterdynamics.com

Hyperscale Cloud Investments Accelerate Enterprise Adoption

Combined deployments by Microsoft, AWS and Google are redefining infrastructure baselines, enabling enterprises to decommission legacy on-premise hardware. Local availability zones slash latency, satisfy privacy legislation and support the New Zealand ICT market’s migration to software-as-a-service. Satellite connectivity via AWS Project Kuiper expands broadband reach to rural enterprises, promoting inclusive cloud uptake. Submarine-cable partnerships such as Google-Vocus reinforce trans-Tasman bandwidth, ensuring that the virtuous cycle of adoption and reinvestment continues.

AI-ML Adoption Transforms Sector Operations

Enterprises are mainstreaming artificial intelligence, moving from experimental pilots to production-grade deployments that deliver measurable returns. Spark New Zealand and Infosys co-developed AI tools for network optimization and customer-service automation, while the operator’s IoT platform surpassed 2 million connected devices, driving 53.3% high-tech revenue growth. Financial institutions rely on machine learning for fraud detection; manufacturers adopt predictive-maintenance algorithms to minimize downtime; and the gaming sector leverages AI to personalize player experiences, underpinning its NZD 548 million (USD 320.38 million) export ambition. Government guidelines on responsible AI cap compliance risk and shape vendor choice, reinforcing best-practice standards across the New Zealand ICT market.

Renewable Energy Integration Attracts ESG-Focused Workloads

Eco-conscious enterprises prefer colocating workloads in data centers powered by clean energy. Spark New Zealand signed a 10-year power-purchase agreement for 63 MW of solar output that will cover roughly 60% of its electricity needs from 2025, while One New Zealand pledged 100% renewable supply. NEXTDC and T4 Group market green-data-center footprints to international clients pursuing scope-3 emissions cuts. These commitments bolster New Zealand’s appeal as an ESG-compliant digital hub and enrich the New Zealand ICT market with premium, sustainability-aligned demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills gap for ICT professionals | −1.4% | National – acute in Auckland and Wellington | Short term (≤ 2 years) |

| Escalating cybersecurity threats | −1.1% | National – heavier burden on SMEs | Short term (≤ 2 years) |

| Power-grid capacity constraints | −0.8% | Regional – Auckland and Canterbury | Medium term (2-4 years) |

| Complex public-procurement cycles | −0.6% | National – gradual improvement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ICT Skills Shortage Constrains Expansion

Persistent shortages in cloud-architecture, cybersecurity and AI engineering talent limit the pace at which enterprises can implement new platforms. Kordia’s 2025 security survey showed 67% of firms had not conducted penetration testing in the previous year, revealing both capability and resourcing gaps. Spark responded by launching Te Awe, an internal academy for AI and data-analytics upskilling, illustrating how large employers must build talent pipelines in-house. Government migration pathways intend to ease pressures, yet domestic training remains critical for the New Zealand ICT market to sustain projected growth.

Cybersecurity Threats Escalate Compliance Requirements

Financial losses from cybercrime climbed to NZD 6.8 million (USD 3.97 million) in Q4 2024, a 91% year-on-year spike, with 17 major incidents surpassing NZD 100,000 (USD 58,477.) each. Cyber-insurance underwriting tightened, leading to higher premiums and stricter prerequisites such as multi-factor authentication and annual red-teaming. For SMEs, the added cost diverts funds from innovation to compliance tools, curbing their uptake of advanced solutions within the New Zealand ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Hold Commanding Lead as Security Demand Surges

IT Services captured a dominant 41.19% of 2025 revenue, mirroring corporate preference for managed solutions during economic uncertainty. Elevated demand for network modernization, cloud migration and application maintenance keeps managed-service contracts stable, although margin pressure intensifies from competitive bidding and public-sector austerity. IT Security, while smaller, registers a brisk 9.55% CAGR as board-level awareness of cyber risk compels proactive spending; the segment’s momentum translates into the fastest expansion across the New Zealand ICT market. In contrast, IT Hardware shipments decelerate because enterprises extend refresh cycles and embrace software-defined infrastructure, although peripheral demand persists for hybrid-work deployments.

Heightened regulatory expectations including mandatory breach notifications and privacy-impact assessments elevate security’s strategic importance, embedding cyber controls into every sourcing conversation. Spark’s security unit now exceeds 150 full-time specialists, exemplifying how service providers embed specialized practices to meet this demand. Meanwhile, AI-enabled monitoring blurs the traditional lines between infrastructure, software and security, spawning integrated platform offerings that set new performance benchmarks within the New Zealand ICT industry.

By Enterprise Size: SMEs Deliver Faster Growth Momentum

Large Enterprises maintained 61.94% control of 2025 spending owing to established IT budgets, cross-border digital ambitions and ongoing data-center investments. However, SMEs outpace them at a 10.05% CAGR to 2031 as cloud subscriptions, SaaS models and streamlined public-procurement frameworks democratize access to sophisticated tools. The revised All-of-Government marketplace reduces administrative burden for small suppliers, enabling them to compete for contracts historically awarded to incumbents. Subsidized rural broadband and simplified tax depreciation on ICT assets further enhance SME purchasing power.

For large organizations, near-term headwinds include public-sector budget freezes and private-sector cost controls that delay transformational projects. Spark’s IT-services revenue fell 14.9% in FY 2024 after customers postponed modernization programs. Yet capital-heavy initiatives such as AI super-clusters and green data-centers remain largely a large-enterprise domain, sustaining volume across the broader New Zealand ICT market.

By End-user Industry: Healthcare Rises as Post-Pandemic Priorities Endure

BFSI organizations topped spending with 18.40% of 2025 revenue, driven by core-bank upgrades, digital wallets and regulatory mandates. Nevertheless, healthcare and life sciences record the highest 10.55% CAGR amid telemedicine rollouts, electronic medical-record consolidation and AI-assisted diagnostic tools. Public funding for rural telehealth accelerates demand for secure connectivity, while private providers integrate wearable-device analytics into chronic-care programs, deepening technology dependence.

Manufacturing capitalizes on IoT sensors and predictive maintenance to boost efficiency, aligning with Industry 4.0 objectives. In entertainment, the gaming and esports sub-segment leverages cloud-rendering and AI-driven personalization to target NZD 1 billion (USD 0.58 billion) in export revenue. Energy utilities deploy smart-grid telemetry, and retail chains integrate omnichannel logistics to reduce delivery times. Collectively these verticals diversify revenue sources and reinforce resilience within the New Zealand ICT market.

Geography Analysis

Auckland and Wellington anchor demand, fueled by proximity to hyperscale data centers, dense fiber networks and headquarters of leading corporates and government ministries. The two cities account for most high-value contracts, yet regional centers increasingly benefit from ultrafast broadband and rural-connectivity schemes. Chorus’s 2025 free-speed upgrade, for instance, elevated 700,000 households from 50/10 Mbps to 100/20 Mbps service tiers, closing the digital-inclusion gap.

Christchurch’s rebuilt infrastructure, post-earthquake, incorporates resilient fiber rings and modern data hubs, attracting disaster-recovery-as-a-service deployments. Hamilton and Tauranga see rising demand from agritech ventures leveraging IoT for precision farming. On the South Island, power-rich regions such as Otago draw interest for renewable-backed edge facilities. Nevertheless, grid-capacity constraints in Auckland and Canterbury create planning uncertainty for new hyperscale builds, highlighting the need for accelerated transmission upgrades.

Cross-Tasman subsea cable expansions lower latency between Auckland and Sydney to sub-23 milliseconds, positioning New Zealand as a redundancy node within Asia-Pacific traffic routes. Local privacy statutes, including the Privacy Act 2020, and Māori data-governance principles compel enterprises to store and process sensitive workloads in-country, boosting domestic service uptake. Consequently the New Zealand ICT market leverages geographic isolation as a trust advantage while deploying global interconnectivity to serve outward-facing digital exporters.

Competitive Landscape

Market concentration sits at a moderate level: traditional telecom incumbents Spark New Zealand, One New Zealand and Chorus control backbone infrastructure, but hyperscalers and a long tail of specialist MSPs intensify rivalry. Spark’s margins compressed in FY 2025 as aggressive business-mobile pricing and public-sector austerity pressured earnings. In response, the operator divested select tower assets to fund data-center expansion and signed a 5G-standalone pact with Nokia to unlock edge-compute use cases.

International clouds differentiate through localized compliance, such as Microsoft’s inclusion of Te Tumu Paeroa as anchor tenant to demonstrate Treaty alignment. Domestic challengers like Team IM and Datacom deliver sovereign-cloud services, targeting public agencies sensitive to offshore data flows. Meanwhile, niche providers exploit gaps in AI consulting, zero-trust security and managed Kubernetes, prompting a wave of partnership-driven go-to-market strategies.

ESG credentials now factor heavily into contract awards: NEXTDC’s renewables-powered Auckland facility competes head-to-head with Spark’s green-energy pledge, compelling incumbents to publish detailed sustainability roadmaps. Overall, price-based competition in legacy connectivity coexists with value-based differentiation in managed services, AI and compliance-first offerings, reshaping the revenue mix within the New Zealand ICT market.

New Zealand ICT Industry Leaders

IBM New Zealand Ltd

Amazon New Zealand Pty Ltd

Microsoft New Zealand Limited

Spark New Zealand Limited

Datacom Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Spark New Zealand announced a multiyear partnership with Nokia to enhance 5G standalone capabilities and automate network operations.

- May 2025: Vocus completed its acquisition of Stuff Fibre, adding 20,000 broadband customers to its 200,000-strong base.

- April 2025: Spark New Zealand formed a strategic IT collaboration with Infosys to accelerate digital-transformation delivery.

- February 2025: Chorus revealed free wholesale fiber speed upgrades benefiting 700,000 households, effective June 2025.

New Zealand ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form.

New Zealand ICT market tracks revenue accrued through the sale of ICT offerings including IT hardware, IT software, IT services, IT infrastructure and communication services that are being used in various end-user industry across the Country.

The New Zealand ICT market is segmented by type (IT hardware (computer hardware, networking equipment, peripherals), IT software, IT services (managed services, business process services, business consulting services, cloud services), IT infrastructure/data centers (colocation data centers, data center storage, data center servers, data center compute), IT security/ cybersecurity (application security, cloud security, data security, identity and access management, infrastructure protection, integrated risk management, network security equipment, endpoint security), communication services), by enterprise size (small and medium enterprises, large enterprises), by industry vertical (BFSI, IT & Telecom, government, retail & e-commerce, manufacturing, energy & utilities, others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Verticals | ||

Key Questions Answered in the Report

What is the projected value of the New Zealand ICT market by 2031?

The market is forecast to reach USD 27.72 billion by 2031, expanding at a 9.29% CAGR.

Which segment will grow fastest through 2031?

IT Security leads with a 9.55% CAGR as firms prioritize cyber-resilience.

How are Maori data-sovereignty principles impacting technology procurement?

They drive adoption of hybrid and sovereign-cloud architectures that keep sensitive data onshore.

Why are hybrid cloud models gaining popularity?

Enterprises balance regulatory data-residency with public-cloud flexibility, pushing hybrid strategies to a 10.42% CAGR.

What skills shortage most affects the sector?

Shortages in cloud architects, AI engineers and cybersecurity professionals constrain implementation timelines.

How significant are renewable-energy commitments for data-center investments?

Green-energy deals, like Spark’s 63 MW solar PPA, are now decisive factors for ESG-minded customers selecting local facilities.

Page last updated on: