Dublin Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

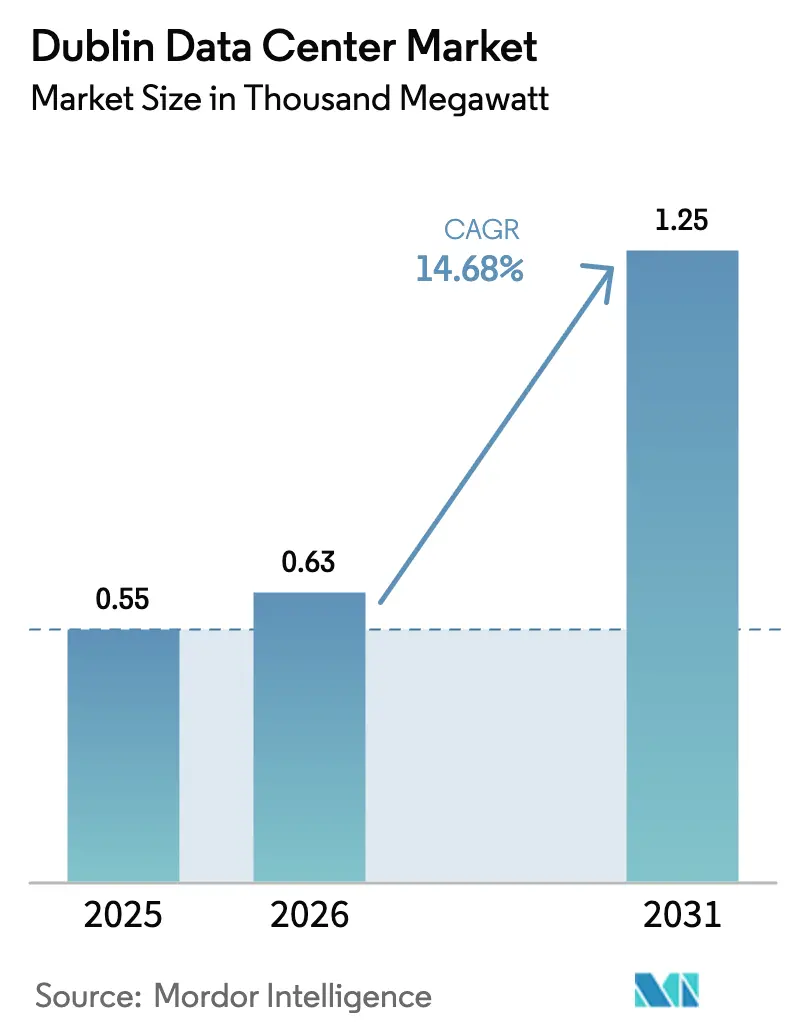

| Base Year Market Size (2025) | 0.55 Thousand megawatt |

| Market Volume (2026) | 0.63 Thousand megawatt |

| Market Volume (2031) | 1.25 Thousand megawatt |

| Growth Rate (2026 - 2031) | 14.68% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dublin Data Center Market Analysis by Mordor Intelligence

Dublin data center market size in 2026 is estimated at 0.63 thousand MW, growing from 2025 value of 0.55 thousand MW with 2031 projections showing 1.25 thousand MW, growing at 14.68% CAGR over 2026-2031. Consistent tax incentives, dense submarine-cable landings, and Ireland’s naturally cool climate underpin sustained demand from hyperscale cloud platforms, artificial-intelligence (AI) clusters, and latency-sensitive enterprises. Recent grid-connection limits have tilted market power toward incumbents that already hold capacity rights, spurring investment in on-site generation, liquid-cooling retrofits, and waste-heat recovery systems that improve power usage effectiveness (PUE). Meanwhile, data-sovereignty mandates such as the EU Data Boundary initiative channel continental workloads into Irish facilities, driving premium pricing for compliance-ready space. Intensifying competition among AWS, Microsoft, Google, and Meta is prompting record capital-raising by wholesale colocation operators and provoking a wave of mergers and asset swaps as newcomers race to secure land, talent, and remaining grid allotments.

Key Report Takeaways

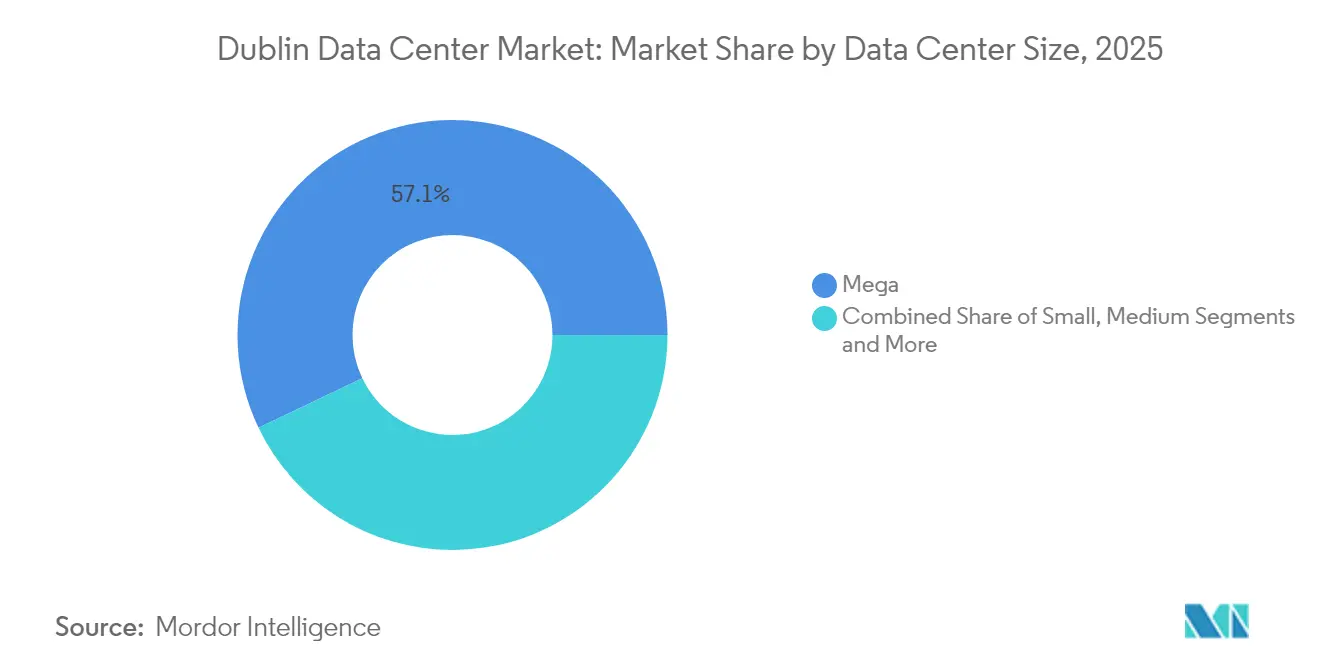

- By data-center size, mega facilities led with 57.10% of Dublin data center market share in 2025; massive campuses are forecast to expand at a 16.55% CAGR through 2031.

- By tier classification, Tier 3 sites accounted for 64.10% of the Dublin data center market size in 2025, while Tier 4 is projected to advance at a 15.90% CAGR through 2031.

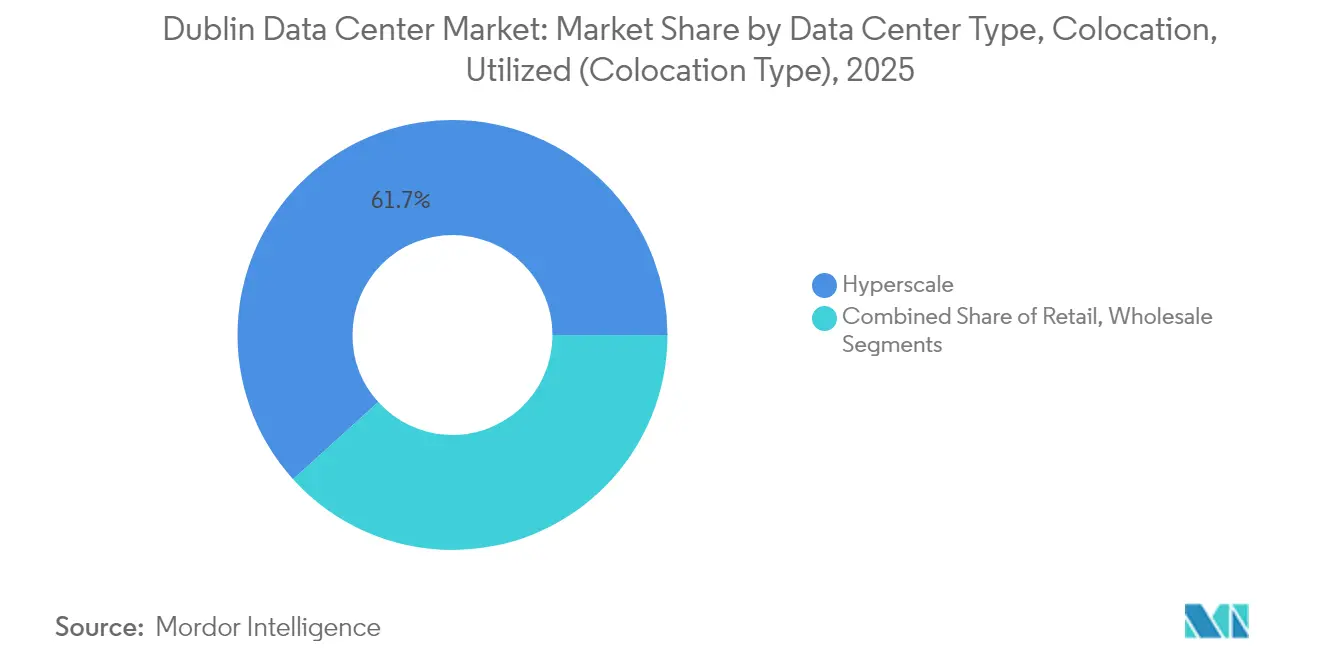

- By colocation model, the hyperscale segment captured 61.70% of the Dublin data center market size in 2025 and is growing at 15.20% through 2031.

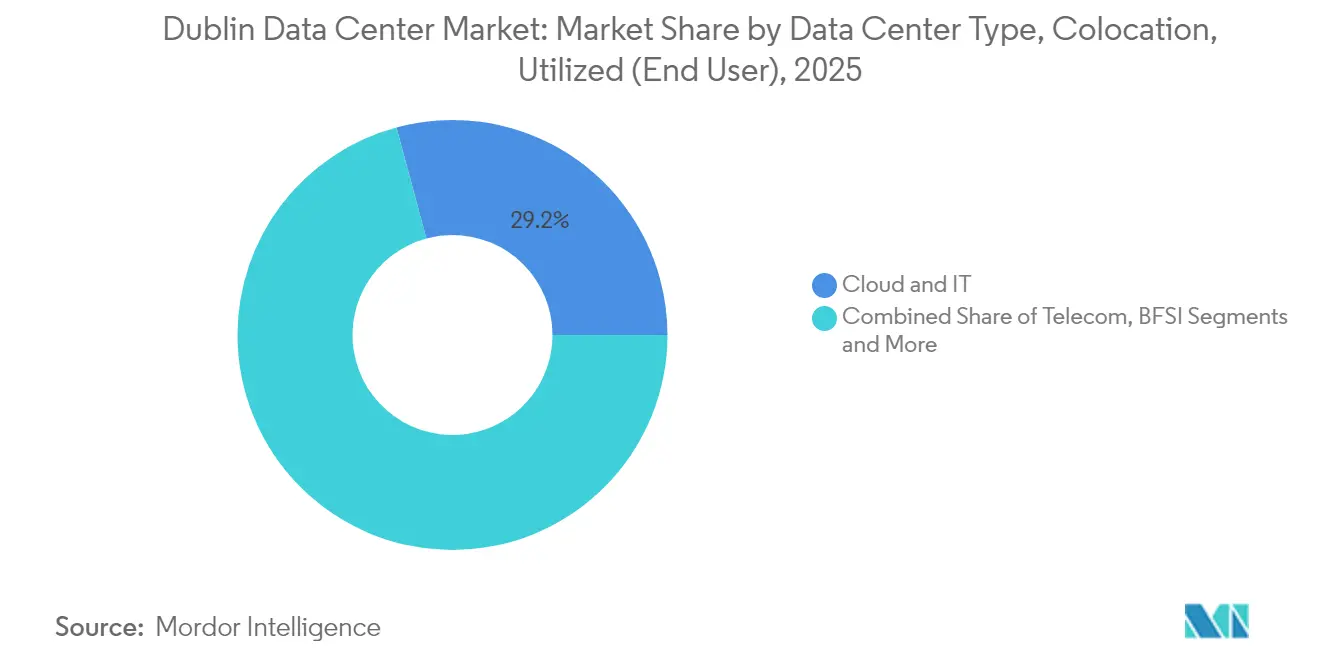

- By end user, cloud and IT services represented 29.20% of demand in 2025 and are tracking a 16.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Dublin Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud expansion by US tech majors | +4.2% | Dublin metro; spillover to Cork and Galway | Medium term (2-4 years) |

| Strategic FLAPD network-latency advantage | +2.8% | Global; benefits N. America–Europe routes | Long term (≥ 4 years) |

| Favourable Irish tax and EU data sovereignty regime | +3.1% | EU-wide; concentrated in Dublin | Long term (≥ 4 years) |

| New submarine-cable landings boost bandwidth | +1.9% | National; initial gains in Dublin, Cork, Galway | Medium term (2-4 years) |

| Grid-decarbonisation commitments lure green tenants | +2.3% | National; renewable-energy zones | Long term (≥ 4 years) |

| AI clusters driving high-density liquid-cooling demand | +3.7% | Global; concentrated in hyperscale hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud Expansion by US Tech Majors

Amazon’s USD 150 billion global data-center program reserves significant power blocks in Dublin, while Microsoft’s USD 500 million campus extension underscores confidence despite a grid-connection freeze.[1]Bloomberg News, “Amazon’s USD 150 Billion Expansion,” bloomberg.com Google’s newly filed EUR 200 million (USD 234.54 million) application signals commitment even after a separate site was denied for sustainability gaps. These investments amplify network effects that attract multi-cloud enterprise migrations, deepen supplier ecosystems, and elevate baseline design specifications such as 400 V power distribution and liquid-cooling loops. Irish component manufacturers, notably Danann Air, now export customized air-handling units worldwide, illustrating how local supply chains scale alongside hyperscaler footprints.

Strategic FLAPD Network Latency Advantage

Situated on the Frankfurt-London-Amsterdam-Paris-Dublin spine, the city leverages the Hibernia Express cable’s 59.5 ms New York-to-London round trip—six milliseconds faster than rivals—to entice algorithmic-trading, gaming, and AI-inference workloads. AEConnect’s 5,536 km transatlantic span delivers five-nines availability and 100 Gb/s wavelengths that feed Dublin’s interconnection campuses. Looking ahead, the EUR 1.1 billion (USD 1.29 billIon) Far North Fiber route via the Arctic Circle will anchor Galway into Asian networks, extending the nation’s reach beyond legacy UK pivot points.[2]Marine Ireland, “Far North Fiber Route Announcement,” marine.ie

Favourable Irish Tax and EU-Data-Sovereignty Regime

A 12.5% corporate tax rate combines with GDPR-aligned processing rules to draw US platforms seeking seamless EU market access. Microsoft’s February 2025 activation of its EU Data Boundary makes Dublin the default locus for European tenant data, turning compliance into a moat against less-certified peers.[3]Microsoft Blogs, “EU Data Boundary Completion,” blogs.microsoft.com Brexit uncertainty accelerates transfers from UK to Irish sites, while forthcoming AI-Act obligations position Dublin operators as turnkey partners for governance-intensive sectors.

New Submarine-Cable Landings Boost Bandwidth

The IRIS link between Galway and Iceland adds route diversity that lowers latency and hedges against UK landfall outages. Ireland’s first direct mainland-Europe cable, bypassing British territory, further secures continental trading paths, and legacy assets such as Virgin Media’s Sirius South continue to supply redundant capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-connection moratorium and power-availability limits | -3.8% | Dublin metro; secondary in Cork and Galway | Medium term (2-4 years) |

| Rising electricity costs from EU carbon pricing | -1.9% | EU-wide; acute for high-consumption sites | Long term (≥ 4 years) |

| Community opposition over water-consumption spikes | -1.2% | Local; Dublin suburbs and rural zones | Short term (≤ 2 years) |

| Specialised-talent shortage in Irish DC operations | -2.1% | National; acute in Dublin and Cork | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Moratorium and Power-Availability Limits

EirGrid’s 2028 freeze on new metropolitan hookups forces operators either to self-generate or to site builds in lesser-loaded counties. Vantage’s 52 MW Dublin campus now runs hydrotreated-vegetable-oil (HVO) generators that satisfy power-purchase-agreement (PPA) carbon thresholds and circumvent queue delays. The policy entrenches incumbents, inflates land valuations, and shifts expansion capital toward Galway, Offaly, and Cork.

Rising Electricity Costs from EU Carbon Pricing

EU-ETS allowances push wholesale Irish rates toward EUR 60/MWh, magnifying cost exposure for legacy diesel spin-ups and making fixed-price renewable PPAs vital for margin defense. Operators are accelerating battery-energy storage and hydrogen-ready turbines, while AI-driven power-management software shaves peaks that coincide with maximum carbon-intensity hours.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Mega Facilities Drive Hyperscale Consolidation

Mega campuses controlled 57.10% of Dublin data center market share in 2025. The Dublin data center market size for massive sites is projected to compound at 16.55% through 2031 as AI GPUs and liquid tanks raise per-rack densities. Incumbents exploit economies in substation build-outs, security, and talent pools that are hard for smaller designs to replicate.

Large and medium footprints retain vital roles for regulated industries and disaster-recovery nodes, yet growth tilts unmistakably toward installations exceeding 50 MW blocks. Edge-tier micro-sites emerge near Cork and Athlone to trim latency for fintech and 5G core slicing, but their aggregate megawatts remain modest relative to hyperscale clusters.

By Tier Type: Tier 3 Dominance Faces Tier 4 Disruption

Tier 3 remained the default with 64.10% of the Dublin data center market size in 2025, translating to roughly 353 MW at 1.6 PUE averages. As machine-learning pipelines migrate from research to mission-critical inference, Tier 4’s error-budget premiums become justifiable, moving its segment CAGR to 15.90%.

Operators retrofit secondary feeds, 2N+1 switchgear, and concurrently maintainable cooling loops that shrink fail-over intervals to microseconds. The tier schema itself may evolve: hybrid power designs now integrate curtailed wind, behind-the-meter batteries, and grid-interactive response that standard Uptime classifications fail to capture.

By Colocation Type: Hyperscale Segment Sustains Growth Leadership

The hyperscale colocation slice held 61.70% of Dublin data center market share in 2025. Multi-tenant wholesale suites give cloud providers turnkey scalability with lower stranded-capacity risk than self-builds.

Retail cages still court fintech start-ups and SaaS vendors, while interconnection-dense carrier hotels remain essential for peering and neutral-cloud exchanges. Take-or-pay power blocks embedded in recent hyperscale contracts protect facility cash-flows, helping operators raise low-cost debt such as Vantage’s record USD 13 billion round in January 2025.

By End User: Cloud and IT Dominance Reflects Digital Transformation

Cloud and IT firms consumed 29.20% of 2025 and will rise at 16.90% CAGR, underpinning the Dublin data center market’s expansion curve. Telecom groups leverage the same campuses for 5G core functions, while media CDNs pre-position high-bitrate libraries, reinforcing East-coast US to EU content flows.

Financial-services tenants seek Dublin’s sub-60 ms New York hops for pricing engines, and the public sector is consolidating legacy server rooms into “cloud-first” zones that must meet sovereign-hosted criteria. Because these user profiles value certified uptime and interconnection density over raw square footage, the city’s existing elastic ecosystem remains hard for challenger sites to replicate.

Geography Analysis

Ireland’s only Tier 1 metropolitan hub clusters along west Dublin’s fiber spine, where high-count conduits ride ESB Telecoms’ power easements to terrestrial landing stations . That corridor hosts 21% of national electricity draw, compelling EirGrid to cap incremental capacity until 2028. Despite the freeze, the Dublin data center market continues to aggregate European AI inference loads due to the city’s unique convergence of low-latency transatlantic paths and EU jurisdiction.

Cork is emerging as a secondary pole; new IRIS and Sirius South cables land there, and municipal authorities offer expedited permitting if operators integrate tidal-energy PPAs. Galway’s developing fiber rings, funded partly by the Far North Fiber consortium, are courting latency-sensitive science collaborations with Boston and Montreal. Rural Offaly and Longford advertise wind-co-location zones with sub-5 c/km grid-connection costs, enticing operators willing to pioneer remote operational models with autonomous-robot maintenance.

Competitive Landscape

Digital Realty operates nine local facilities totaling 485,000 sq ft and hosts more than 170 clients spanning pharma, fintech, and social-media workloads. AWS, Google, Meta, and Microsoft each run dedicated hyperscale campuses yet also lease wholesale suites when launch schedules outpace owned construction. This dual role blurs traditional supplier–customer lines and raises bar-entry requirements for newer firms. Vantage’s greenfield build brings 52 MW plus HVO-backed generation and district-heating export, illustrating how sustainability narratives now differentiate bids.

Supporting-chain specialists—from Vertiv’s cold-plate patents to John Sisk’s modular-shed techniques—are embedding themselves in project design charrettes to shave months off commissioning times and to navigate overlapping planning, water-use, and power conditions. Competitive intensity therefore migrates beyond mere megawatt delivery toward holistic compliance, ESG scoring, and speed-to-GPU-ready-rack outcomes.

Dublin Data Center Industry Leaders

Amazon Web Services

Microsoft Corporation

Google LLC

Meta Platforms Inc.

Digital Realty Trust Inc. (Interxion)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Vantage Data Centers announced a EUR 1.4 billion (USD 1.64 billion) EMEA expansion with Dublin as a focal site featuring waste-heat recovery and on-site HVO generators.

- February 2025: Microsoft finalized its EU Data Boundary, cementing Dublin as the default processing hub for EU customer data.

- January 2025: Vantage secured USD 13 billion in incremental funding to accelerate AI-oriented construction, including its first Dublin campus.

- December 2024: Equinix acquired BT’s Irish data centers for EUR 59 million (USD 69.19 million), broadening its local footprint.

Dublin Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Dublin data center market is segmented by DC size (small, medium, large, massive, and mega), tier type (tier 1 & 2, tier 3, and tier 4), absorption (utilized (colocation type (retail, wholesale, and hyperscale), end user (cloud and IT, telecom, media and entertainment, government, BFSI, manufacturing, and e-commerce)) and non-utilized).

The market sizes and forecasts are provided in terms of volume (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Massive |

| Mega |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Cloud Service Providers (CSPs) | |||

| Enterprise, Modular and Edge | |||

| Colocation | Utilized | Colocation Type | Retail |

| Wholesale | |||

| Hyperscale | |||

| End User | Cloud and IT | ||

| Telecom | |||

| Media and Entertainment | |||

| Government | |||

| BFSI | |||

| Manufacturing | |||

| E-Commerce | |||

| Other End User | |||

| Non-Utilized | |||

| By Data Center Size | Small | |||

| Medium | ||||

| Large | ||||

| Massive | ||||

| Mega | ||||

| By Tier Type | Tier 1 and 2 | |||

| Tier 3 | ||||

| Tier 4 | ||||

| By Data Center Type | Cloud Service Providers (CSPs) | |||

| Enterprise, Modular and Edge | ||||

| Colocation | Utilized | Colocation Type | Retail | |

| Wholesale | ||||

| Hyperscale | ||||

| End User | Cloud and IT | |||

| Telecom | ||||

| Media and Entertainment | ||||

| Government | ||||

| BFSI | ||||

| Manufacturing | ||||

| E-Commerce | ||||

| Other End User | ||||

| Non-Utilized | ||||

Key Questions Answered in the Report

What is the current Dublin data center market size?

The Dublin data center market size is 0.63 thousand MW in 2026 and is tracking toward 1.25 thousand MW by 2031.

How fast is the Dublin data center market growing?

Capacity is expanding at a 14.68% CAGR through 2031, driven by hyperscale cloud demand, AI workloads, and low-latency connectivity.

Why did EirGrid impose a grid-connection moratorium?

EirGrid paused new metropolitan hookups until 2028 to protect system reliability, prioritizing projects with on-site generation or proven grid support.

Which colocation segment leads in Dublin?

Hyperscale colocation leads with 61.70% share and continues to expand at 15.20% CAGR as cloud providers seek rapid, large-scale deployments.

Page last updated on: