Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

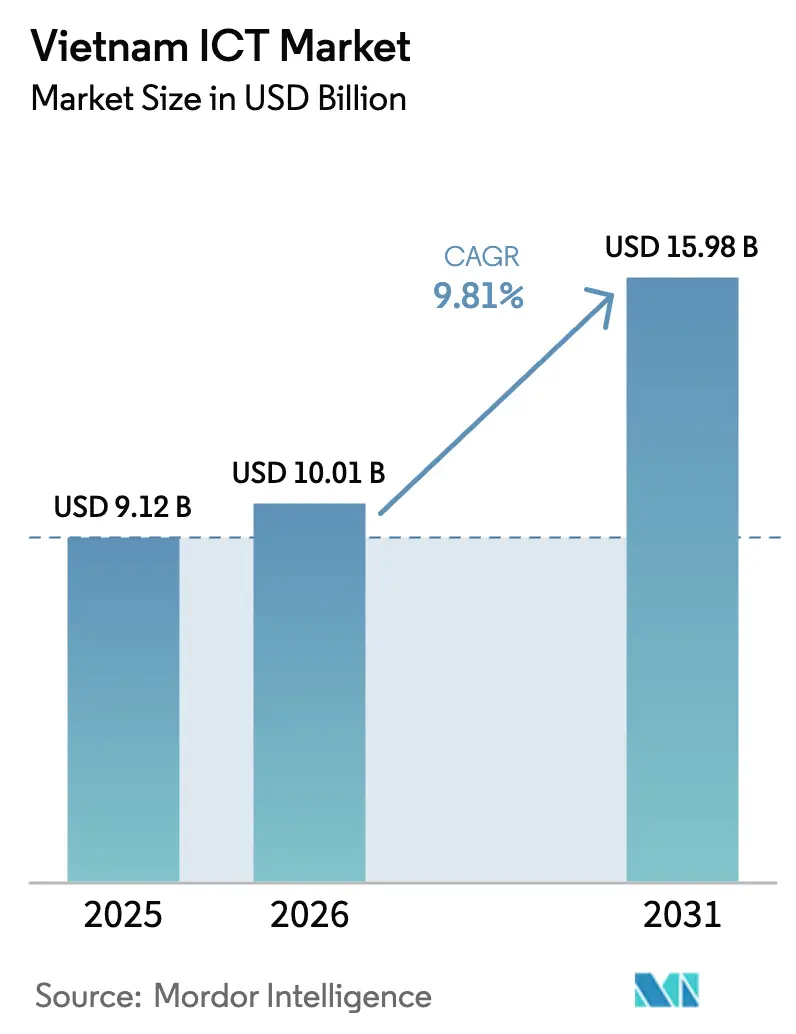

| Base Year Market Size (2025) | USD 9.12 Billion |

| Market Size (2026) | USD 10.01 Billion |

| Market Size (2031) | USD 15.98 Billion |

| Growth Rate (2026 - 2031) | 9.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam ICT Market Analysis by Mordor Intelligence

The Vietnam ICT market size was valued at USD 9.12 billion in 2025 and estimated to grow from USD 10.01 billion in 2026 to reach USD 15.98 billion by 2031, at a CAGR of 9.81% during the forecast period (2026-2031). Government-led digitalization programs, sizable foreign direct investment, and the push to localize semiconductor production continue to accelerate adoption across hardware, software, and services. Large-scale 5G rollouts, paired with expanding cloud and data-center capacity, are fueling new revenue streams for telecommunications operators and global hyperscalers. At the same time, smart-city initiatives in 48 municipalities are driving demand for integrated connectivity, analytics, and cybersecurity solutions. The competitive dynamic remains balanced between state-owned carriers and multinational technology vendors that are deepening local partnerships to address industry-specific digital-transformation mandates. Although funding constraints in secondary cities and a shortage of advanced engineering talent pose headwinds, the Vietnam ICT market is expected to maintain double-digit momentum through 2030 as enterprises modernize operations and new digital-services models scale.

Key Report Takeaways

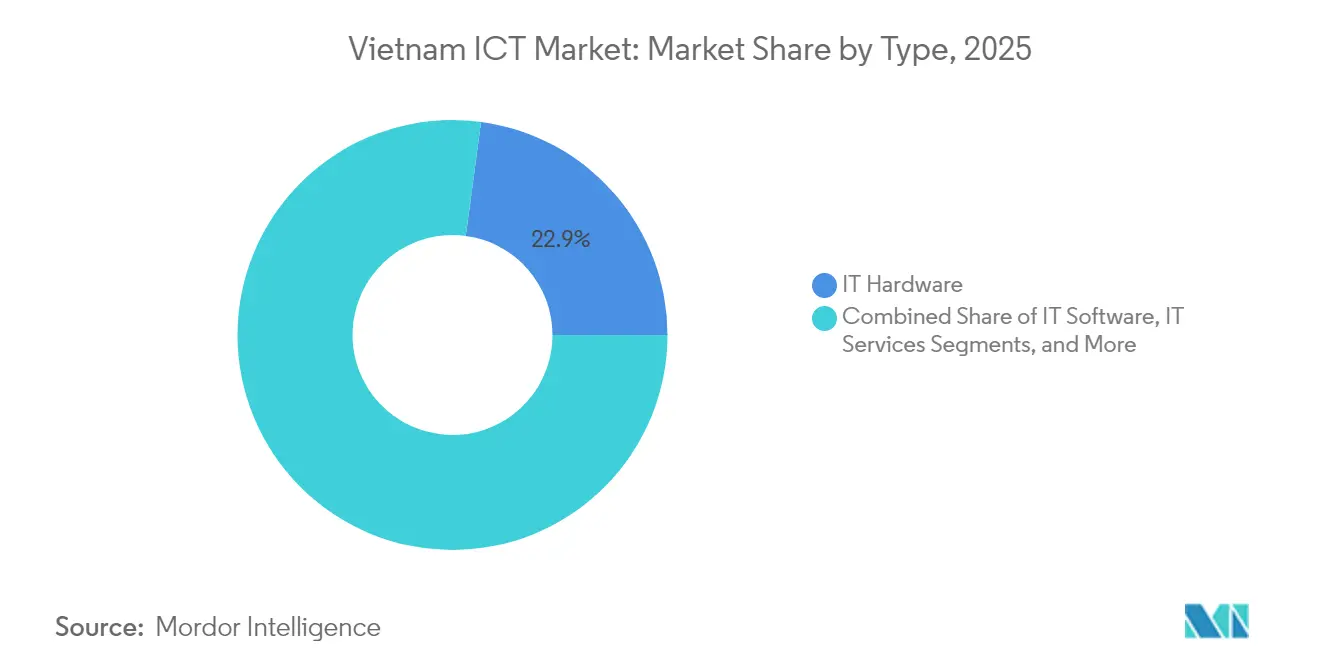

- By type, IT Hardware led with a 22.88% share of the Vietnam ICT market share in 2025; IT Services is advancing at a 12.07% CAGR through 2031.

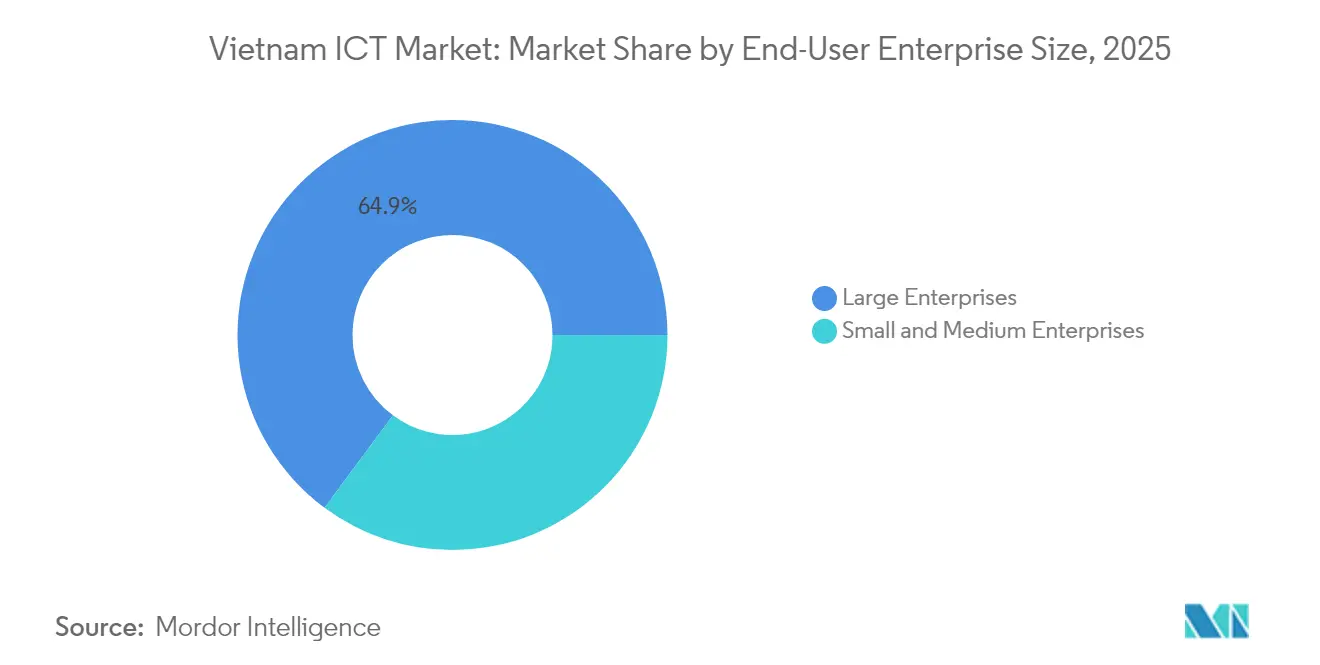

- By enterprise size, Large Enterprises accounted for 64.85% of the Vietnam ICT market size in 2025, while Small and Medium Enterprises are expanding at an 11.62% CAGR to 2031.

- By industry vertical, BFSI held 17.55% of 2025 spending; Healthcare and Life Sciences is poised for 11.88% CAGR growth to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-city infrastructure programmes | +2.1% | National, with early gains in Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Digital transformation across Industry 4.0 value-chains | +2.8% | National, concentrated in manufacturing hubs | Long term (≥ 4 years) |

| Surging cloud- and AI-linked capex | +1.9% | National, with focus on major urban centers | Short term (≤ 2 years) |

| Government "Make-in-Vietnam" digital-economy roadmap | +1.7% | National policy with regional implementation | Long term (≥ 4 years) |

| Semiconductor self-sufficiency incentives | +1.2% | National, with focus on northern provinces | Long term (≥ 4 years) |

| Hyperscale and regional IDC hub build-out | +1.8% | National, concentrated in Ho Chi Minh City and Hanoi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart-City Infrastructure Programs

Government approval of 48 municipal digitalization roadmaps has created a USD 2 billion pipeline for connectivity, sensor networks, and cybersecurity platforms. Ho Chi Minh City’s flood-management upgrade and Da Nang’s sustainable-city plan both require real-time data analytics, strengthening demand for edge computing and IoT gateways. [1]U.S. International Trade Administration, “Vietnam – Information and Communication Technologies,” trade.gov Mandatory allocation of at least 10% of public-sector IT budgets to cybersecurity further expands the addressable market for threat-detection vendors. The national VNeID digital-identity roll-out already serves millions of citizens and is scaling authentication services for e-government portals. These projects generate multiplier effects for telecom carriers, cloud providers, and systems integrators while positioning Vietnam as a testbed for regional smart-city solutions.

Digital Transformation Across Industry 4.0 Value Chains

Manufacturing plants adopting AI-driven predictive-maintenance systems report production-efficiency gains of 30-50%. Textile exporters such as Vinatex have boosted consolidated revenue by 6.1% after deploying IoT-enabled supply-chain analytics. Samsung’s USD 920 million expansion underscores rising capital inflows devoted to machine-learning-based quality control and automated logistics. Decree 109, which lowered registration taxes for locally produced vehicles, has accelerated automotive digitalization through robotics and connected-factory platforms. Blockchain-powered provenance tracking and AI-enhanced demand forecasting are helping Vietnamese manufacturers capture higher-margin global orders while shortening time-to-market.

Surging Cloud- and AI-Linked Capex

Sixty-eight percent of enterprises now invest in cloud and AI to optimize logistics and customer engagement, triggering sharp growth in hybrid-cloud deployments. Microsoft has added local data-center capacity, and Google is evaluating a greenfield cloud region, signaling long-term confidence in the Vietnam ICT market. The national cloud-computing program’s data-sovereignty rules favor enterprise-grade platforms with built-in compliance controls. NVIDIA’s planned AI R&D hub will bolster semiconductor-design capabilities and enrich the talent ecosystem for machine-learning engineers. Banks lead the shift, migrating core workloads and layering AI customer-service bots to defend share against fintech entrants.

“Make-in-Vietnam” Digital-Economy Roadmap

The strategy seeks a 20% GDP contribution from digital activities by 2025 and 30% by 2030, supported by 80,000 registered digital enterprises and R&D tax credits that reduce the cost of innovation. [2]FPT Corporation, “Annual Report 2024: Growth Strategy,” fpt.com.vn Foreign investors are projected to channel USD 25 billion into Vietnamese tech ventures by 2025 on the back of streamlined licensing and preferential tax regimes. Semiconductor self-sufficiency plans include training 50,000 engineers by 2030, closing critical skills gaps while reducing reliance on imported chips. Regulatory sandboxes in fintech and blockchain offer controlled test beds for new products, balancing innovation with financial-stability safeguards. Strengthened IP protection further encourages multinationals to locate design centers and transfer advanced know-how to local partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front network and data-centre build costs | -1.4% | National, particularly affecting secondary cities | Medium term (2-4 years) |

| Shortage of specialised ICT talent | -1.8% | National, most acute in emerging technology sectors | Short term (≤ 2 years) |

| Heavy reliance on imported core components | -0.9% | National, affecting hardware and infrastructure segments | Long term (≥ 4 years) |

| Fragmented cyber-regulatory compliance burden | -0.7% | National, with varying provincial implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Network and Data-Center Build Costs

The capital intensity of 5G spectrum, fiber backhaul, and Tier III data-center construction strains operator balance sheets, especially outside the two largest metros. Secondary cities often lack the demand density to hit utilization thresholds, extending payback periods for investors. Currency fluctuation risk and rising interest rates elevate funding costs, while land-use approvals add administrative delays. Although public-private-partnership models are emerging, financing gaps persist for small regional carriers and neutral-host tower companies. These constraints could defer rural broadband timelines and limit edge-computing coverage that many Industry 4.0 use cases require.

Shortage of Specialized ICT Talent

Demand for advanced engineers continues to outrun supply, particularly in cybersecurity, AI, and semiconductor design. Rising salary premiums - monthly pay for experienced AI developers exceeds USD 2,000 - squeeze SME budgets and encourage job-hopping among specialists. Although the government is expanding scholarships and joint curricula with global universities, the lead time to cultivate deep expertise remains long. Companies increasingly build in-house academies and form university partnerships, yet the near-term gap threatens project-delivery schedules for large cloud-migration and analytics engagements. Persistent scarcity could slow the Vietnam ICT market’s move up the value chain in design-intensive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Drive Technology Modernization

IT Hardware maintained a 22.88% share of the Vietnam ICT market in 2025 as operators upgraded base-station and data-center equipment to support nationwide 5G backbones. However, the Vietnam ICT market size for hardware is expected to expand more slowly than that for services as infrastructure build-outs mature. In contrast, IT Services is on track for a 12.07% CAGR through 2031, propelled by consulting, systems integration, and managed-security projects that require specialized know-how. Hybrid cloud, ERP modernization, and AI implementation demand continuous professional-services support, creating sticky revenue streams for vendors and integrators.

Cloud-services adoption is escalating as enterprises pursue pay-as-you-go scalability; this, in turn, lifts demand for connectivity and cybersecurity offerings bundled by telecom carriers. Software revenue is also climbing as firms migrate from perpetual licenses to subscription-based SaaS, lowering up-front costs. Communication services benefit from growing mobile-data consumption and enterprise 5G use cases. Managed-services contracts, especially for cybersecurity monitoring, allow SMEs to outsource complex functions and keep headcount lean while meeting regulatory mandates.

By End-User Enterprise Size: SME Digitalization Accelerates

Large Enterprises still command 64.85% of the Vietnam ICT market size owing to multi-year ERP, analytics, and compliance investments that require substantial capital. Yet Small and Medium Enterprises are racing ahead at an 11.62% CAGR thanks to cloud-based accounting, e-commerce, and CRM applications that eliminate hardware purchases and simplify upgrades. Government programs such as VNPT’s OneSME portal bundle connectivity, software, and training, lowering adoption barriers.

Large Enterprises prioritize integrated risk-management and data-protection systems to comply with the 2025 Data Law, stimulating demand for advanced security analytics and audit trails. Manufacturers and banks lead spend on AI-enhanced quality control and fraud detection. Meanwhile, SMEs leverage SaaS to compete on customer experience without matching large-enterprise budgets. As subscription models mature, the Vietnam ICT market will likely see a convergence in digital capability between company sizes, intensifying competition across industries.

By End-User Industry: Healthcare Leads Digital Innovation

Healthcare and Life Sciences is forecast to post a 11.88% CAGR as all public hospitals adopt electronic health records and virtual-hospital platforms expand remote-care coverage. Smart-hospital pilots integrate IoT sensors, automated dispensing, and AI-assisted diagnostics, driving demand for low-latency networks and high-performance computing. The Vietnam ICT market share for healthcare-related solutions is therefore set to climb steadily through 2031.

BFSI retained the largest vertical spend at 17.55% in 2025, enabled by biometric authentication, blockchain-based settlement, and AI fraud analytics. Banks are modernizing mobile platforms and migrating core systems to cloud environments to compete with agile fintech challengers. Regulatory sandboxes permit controlled trials of new digital-asset products while safeguarding systemic stability. Other high-growth segments include Manufacturing and Industry 4.0, which deploys predictive-maintenance analytics, and Retail E-commerce and Logistics, where automated fulfillment and last-mile optimization software address booming online sales.

Geography Analysis

Ho Chi Minh City and Hanoi together generated roughly 59.20% of the Vietnam ICT market in 2025, buoyed by dense clusters of multinational firms, banks, and tech startups that demand sophisticated connectivity and cloud services. The southern commercial hub leads e-commerce adoption, with online retail sales surpassing USD 25 billion in 2024, creating sizable requirements for payment gateways, warehouse-management systems, and customer-analytics platforms.

Da Nang is emerging as a secondary tech nucleus, aided by smart-city pilot programs that showcase integrated flood-monitoring, traffic-optimization, and e-government solutions. Forty-eight municipal digital-transformation projects are spreading demand to secondary and tertiary cities, prompting telecom carriers to extend fiber backbones and edge-computing nodes. Provincial administrations are standardizing citizen-service portals, creating repeatable opportunities for systems integrators to deploy secure cloud architectures across jurisdictions.

Northern provinces benefit from proximity to China and established electronics supply chains, making them prime locations for semiconductor design centers and Industry 4.0 factories. Logistics technology adoption is rising as automated customs and cargo-tracking platforms support cross-border trade. Meanwhile, the Mekong Delta applies IoT crop-monitoring and smart-irrigation platforms to bolster agricultural productivity, demonstrating the Vietnam ICT market’s reach beyond urban areas.

Competitive Landscape

Vietnam’s ICT ecosystem combines strong domestic incumbents with deepening participation from global leaders. State-owned operators Viettel, VNPT, and MobiFone account for more than 95% of communications infrastructure, using this scale to extend into cloud hosting, cybersecurity, and digital-services bundles. FPT Corporation leverages a nationwide systems-integration footprint to win offshore software projects, recording USD 500 million in Japanese revenue while reinforcing its domestic leadership.

Multinationals including Microsoft, Cisco, Google, and Oracle are investing directly in local data-center capacity and joint ventures, transferring advanced cloud and security capabilities to Vietnamese partners. The looming rollout of O-RAN 5G by Viettel highlights increasing openness to multi-vendor ecosystems, reducing vendor lock-in and spurring innovation. Start-ups such as VNG and TMA Solutions are disrupting traditional models with AI-enabled platforms for finance, gaming, and e-commerce, supported by venture funding and government innovation grants.

Regulatory frameworks encourage foreign capital yet mandate data localization and cybersecurity compliance, favoring providers with robust risk-management practices. As enterprise clients consolidate workloads onto hybrid clouds, competition is shifting toward end-to-end digital-transformation contracts that bundle connectivity, infrastructure, and managed services. Overall, the Vietnam ICT industry exhibits moderate concentration, with domestic telcos dominant in networks but a fragmented landscape across software and services segments.

Vietnam ICT Industry Leaders

Microsoft Corporation

Cisco Systems Inc.

Viettel Group

VNPT Group

FPT Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Qualcomm Technologies acquired VinAI’s Movian AI division to enhance autonomous-vehicle and smart-city capabilities, establishing Vietnam as a key AI R&D hub.

- March 2025: M1 Limited purchased 70% of ADG Group for USD 15 million, expanding telecommunications services and infrastructure capacity.

- February 2025: FPT Corporation formed USD 50 million partnerships with Sumitomo Corporation and SBI Holdings to co-develop fintech platforms for Southeast Asia.

- January 2025: KT Corporation and Viettel Group launched a strategic alliance to co-deploy 5G and edge-computing solutions in Vietnam.

Vietnam ICT Market Report Scope

Information and communication technology (ICT) is an extensional term for information technology (IT) that stresses the role of unified communications and the integration of telecommunications (telephone lines and wireless signals) and computers, as well as necessary enterprise software, middleware, storage, and audiovisual, enabling users to access, store, transmit, understand, and manipulate information.

The Vietnamese ICT market is segmented by type (hardware [network switches, routers and WLAN, servers and storage, and other hardware], software, IT services, and telecommunication services) and industry vertical (BFSI, IT and telecom, government, retail, and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| Communication Services |

By End-User Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Other Verticals |

| By Industry Vertical (Value) |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| Communication Services | ||

| By End-User Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas (Up-, Mid-, Down-stream) | ||

| Gaming and Esports | ||

| Other Verticals | ||

| By Industry Vertical (Value) | ||

Key Questions Answered in the Report

How fast is the Vietnam ICT market expected to grow through 2031?

The Vietnam ICT market is projected to record a 9.81% CAGR, rising from USD 10.01 billion in 2026 to USD 15.98 billion by 2031.

Which segment is expanding the quickest?

IT Services leads with a forecast 12.07% CAGR as enterprises demand cloud migration, cybersecurity, and digital-transformation support through 2031.

What factors are driving investment in cloud and AI infrastructure?

Data-sovereignty regulations, surging e-commerce traffic, and multinational cloud-region commitments from firms like Microsoft and Google are propelling new data-center and AI spending.

Why are SMEs adopting digital tools more rapidly?

Cloud-based subscription models lower up-front costs, while government programs such as VNPT’s OneSME bundle connectivity and software tailored for smaller firms.

Where are smart-city deployments most advanced?

Ho Chi Minh City, Hanoi, and Da Nang host large-scale pilots integrating IoT sensors, real-time analytics, and digital-identity platforms, setting templates for other municipalities.

What is the biggest near-term challenge for the sector?

A shortage of specialized talent in cybersecurity, AI, and semiconductor design is tightening labor supply and could delay complex project rollouts.

Page last updated on: