Ireland Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

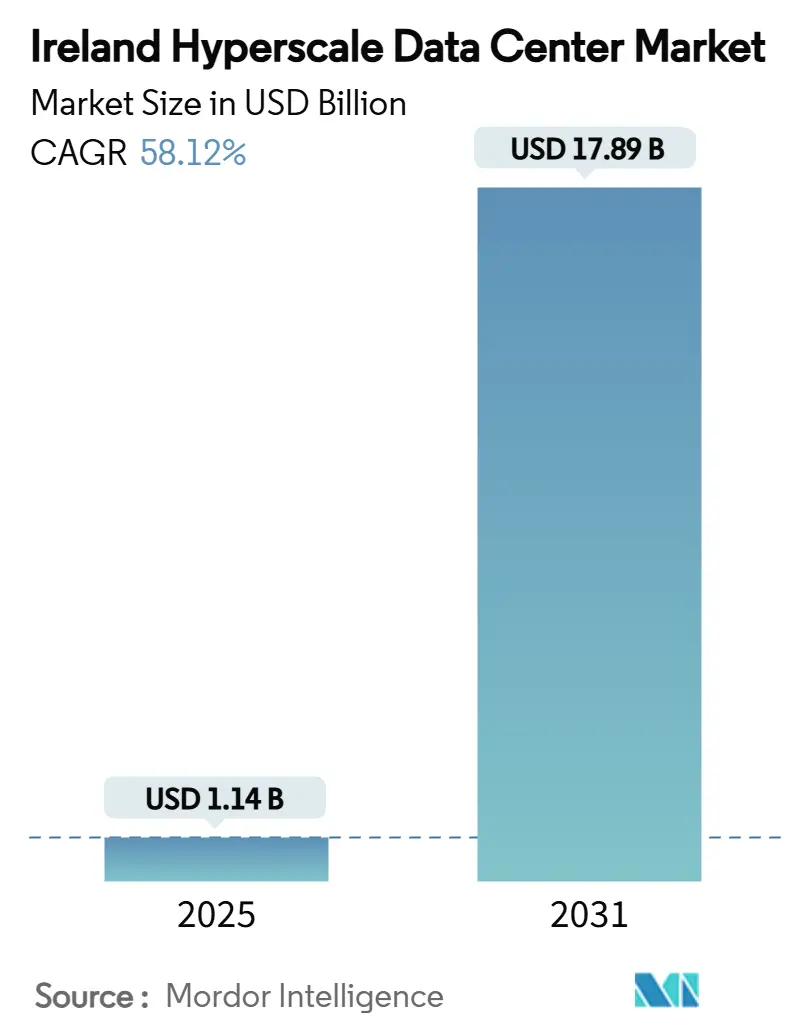

| Market Size (2025) | USD 1.14 Billion |

| Market Size (2031) | USD 17.89 Billion |

| Growth Rate (2025 - 2031) | 58.12% CAGR |

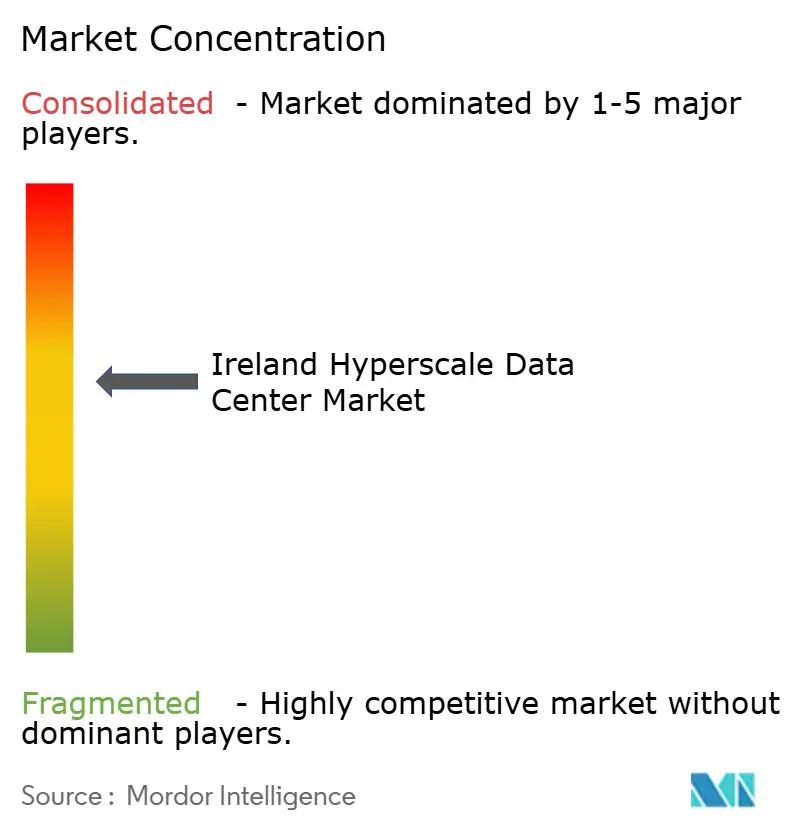

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland Hyperscale Data Center Market Analysis by Mordor Intelligence

Driving Forces Behind Ireland's Hyperscale Data Center Market Growth

The Ireland hyperscale data center market size is valued at USD 1.14 billion in 2025 and is forecast to reach USD 17.89 billion by 2031, expanding at a 58.12% CAGR through the period. Sustained capital inflows, surging artificial-intelligence workloads, and Ireland’s geographic bridge between Europe and North America jointly accelerate this trajectory. Installed IT load capacity rises from 0.946 thousand MW in 2025 to 2.621 thousand MW by 2031, reflecting an 18.51% CAGR that underscores aggressive infrastructure scaling. Dublin already hosts nearly 5% of global hyperscale sites, and its climatic advantage lowers cooling costs, reinforcing operator preference. Strategic Development Zones, dark-fiber landings, and EU-taxonomy-aligned financing compress project timelines and reduce weighted average cost of capital, sharpening competitive advantages. Conversely, a moratorium on grid connections above 50 MW, rising carbon-budget pressure, and constrained water abstraction introduce supply risk that encourages on-site generation, battery storage, and liquid-cooling retrofits.

Key Report Takeaways

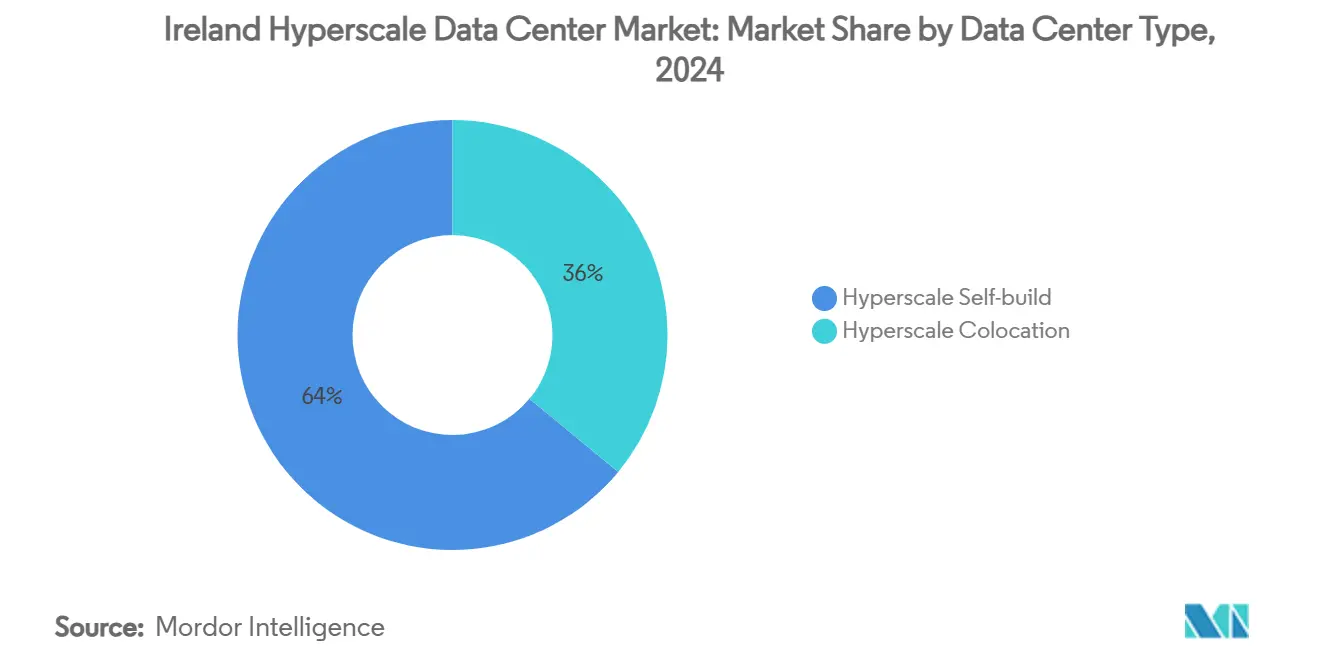

- By data center type, Hyperscale Self-Build held 64% of the Ireland hyperscale data center market share in 2024, while Hyperscale Colocation posted the highest projected CAGR at 11.20% through 2031.

- By component, IT Infrastructure accounted for 48% of the Ireland hyperscale data center market size in 2024; Cooling Systems is advancing at an 18.50% CAGR to 2031.

- By tier standard, Tier III dominated with 71% revenue share in 2024, whereas Tier IV facilities are forecast to expand at a 10.40% CAGR over 2025-2031.

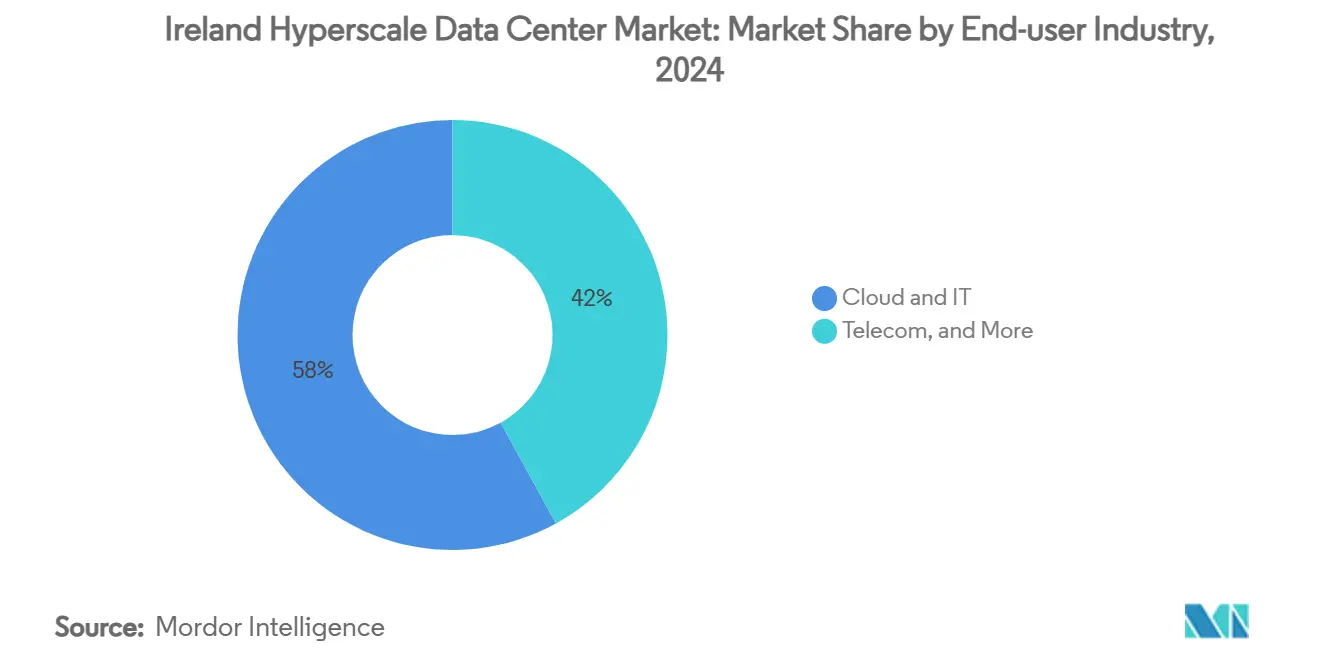

- By end-user industry, Cloud and IT captured 58% share in 2024 and is projected to rise at 19.10% CAGR between 2025-2031.

- By data center size, Massive sites led with 46% share in 2024; the Mega shows the fastest 13.60% CAGR through 2031.

Ireland Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating rack power densities >70 kW/rack | +12.50% | Greater Dublin Area; regional spillover | Medium term (2-4 years) |

| Fast-track Strategic Development Zones | +8.20% | Dublin metropolitan; satellite locations | Short term (≤2 years) |

| Grid-connected battery storage | +6.80% | National; high-renewable regions | Medium term (2-4 years) |

| Maritime dark-fiber landings | +5.40% | Dublin and Cork coastal corridors | Long term (≥4 years) |

| On-site waste-heat reuse | +3.70% | Dublin and Cork urban centers | Long term (≥4 years) |

| EU-taxonomy-aligned green financing | +4.90% | National; renewable-rich areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Rack Power Densities Drive Infrastructure Transformation

Rack densities that exceed 70 kW have become common in generative-AI clusters, forcing operators to replace traditional air systems with immersion and direct-to-chip liquid cooling[1].Data Center Frontier, “Cooling the AI Revolution in Data Centers,” datacenterfrontier.com The thermal burden also requires upgraded switchgear and higher-capacity busways, which in turn push power-usage-effectiveness targets below 1.2 in new builds. Facilities redesigned for AI workloads now specify 24-32 times the east-west network bandwidth that legacy cloud racks used, reshaping white-space layout and cable-management practices. Lead-time reductions of nearly 20% on GPU docks achieved through supply-chain rationalization illustrate how infrastructure refinement translates into faster model deployment. Collectively, these changes elevate capital intensity yet boost computational throughput per square meter, sustaining hyperscaler appetite for Irish capacity even under grid constraints.

Fast-Track Strategic Development Zones Accelerate Planning Approvals

The Planning and Development Act 2024 introduced statutory decision deadlines that compress approval cycles from several years to a few months, provided a project resides inside a designated Strategic Development Zone [2]A&L Goodbody, “The new Planning Act: a fresh start?” algoodbody.com. Land values inside the zones rose as scarcity increased, but the regulatory certainty outweighed the premium for most operators. Vantage Data Centers’ 52 MW Dublin project combines SDZ fast-tracking with on-site power generation, demonstrating how developers neutralize grid connection risk while meeting construction milestones. The zones also simplify community-consultation requirements, enabling earlier procurement of prefabricated electrical rooms and modular cooling pods. These features collectively bring forward revenue realization for investors and reinforce Ireland’s position despite Nordic competition.

Grid-Connected Battery Storage Transforms Energy Economics

Large-scale lithium-ion arrays now accompany hyperscale campuses, allowing operators to absorb curtailed wind output and dispatch into EirGrid’s ancillary-services markets. This flexibility yields revenue streams that trim effective power costs and offsets carbon-budget pressure. Amazon’s Project Eire leverages 100 MWh batteries to shave peak grid draw and provide fast-frequency response, positioning the facility as a stability asset rather than a burden. Co-located batteries also unlock higher renewable penetration by reducing spinning-reserve requirements, indirectly improving Ireland’s climate-action targets. Financial modeling shows that battery revenue can cut weighted-average power prices by up to 14% over a project’s life, lifting internal rates of return on hyperscale builds.

Maritime Fiber Infrastructure Enhances Connectivity Advantages

The Aqua Comms Iris trans-Atlantic cable lowers round-trip latency to New York under 60 milliseconds, strengthening Ireland’s appeal for latency-sensitive trading, gaming, and edge-AI workloads. Additional landings in Cork diversify entry points and provide route redundancy, elevating service-level guarantees for multinational clients. Enhanced backbone capacity encourages content-delivery networks to aggregate European traffic in Dublin, creating network-effect stickiness that deters relocations to continental hubs. Sub-1 ms inter-Dublin cross-connects enable multi-region cloud architectures within the metro, optimizing disaster-recovery topologies without leaving Irish jurisdiction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EirGrid moratorium on >50 MW connections | -15.30% | National; acute in Greater Dublin | Short term (≤2 years) |

| Tightened water-abstraction licences | -8.70% | Dublin metro and surrounding counties | Medium term (2-4 years) |

| Carbon-budget ceilings | -6.40% | National; varies with renewable supply | Long term (≥4 years) |

| High-voltage engineering talent shortage | -4.20% | National; technical specialties | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transmission System Constraints Create Development Bottlenecks

EirGrid’s cap on new connections above 50 MW forces operators to fragment capacity or invest in private substations, adding months to build schedules and inflating capital budgets [3].Pinsent Masons, “New Irish data centre policy,” pinsentmasons.comThe policy emerged after data centers consumed 21% of national electricity in 2023, with projections of 31% by 2026 without checks. Hyperscalers now submit designs featuring dual 49 MW feeds or autonomous gas turbines that maintain compliance yet sacrifice economies of scale. Amazon warned that prolonged restrictions threaten Ireland’s competitiveness against the Netherlands and Sweden, where grid headroom remains available. Although battery-storage integration partially mitigates the shortfall, the moratorium remains the single largest drag on the Ireland hyperscale data center market CAGR.

Carbon Budget Ceilings Constrain Long-Term Growth

The Climate Action Plan 2024 sets a 51% national greenhouse-gas reduction target by 2030, binding data center additions to demonstrable reductions in grid-carbon intensity. Operators must now secure renewable power-purchase agreements or build co-located wind and solar farms to obtain planning consent. Compliance costs rise further under the EU sustainability-rating scheme that mandates public reporting of energy reuse, water efficiency, and waste-heat recovery by September 2024. Smaller developers face disproportionate burdens, accelerating market consolidation as capital-rich hyperscalers dominate permitting races. Unless offshore-wind rollout meets its 37 GW by 2050 ambition, carbon-budget ceilings could cap the long-run capacity envelope of the Ireland hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Self-Build Scale Versus Colocation Agility

The Ireland hyperscale data center market size for Hyperscale Self-Build stood at USD 732 million in 2024 and commanded 64% market share. Amazon, Microsoft, Google, and Meta prefer self-build models because proprietary designs optimize GPU fabric efficiency and security posture. Vertical integration also minimizes latency between design iterations and deployment. However, Hyperscale Colocation is forecast to clock an 11.20% CAGR through 2030 as power caps make shared power blocks more attractive. Equinix’s EUR 59 million (USD 68.31 million) purchase of BT’s Irish assets brought carrier-neutral interconnection capability to hyperscale customers unwilling to wait for new builds. Colocation contracts with power-reservation clauses increasingly mirror cloud availability-zone standards, narrowing the feature gap between self-build and lease models.

Self-build projects confront grid-access hurdles most acutely, prompting creative architectures such as 49 MW dual blocks connected by private medium-voltage rings. Colocation providers, meanwhile, aggregate multi-tenant demand and lobby collectively for sub-50 MW exemptions, accelerating time-to-capacity for AI startups and sovereign-cloud workloads. As Ireland’s power-allocation regime intensifies, a blended strategy—leasing near-term blocks while constructing long-term campuses—emerges among hyperscalers aiming to sustain growth.

By Component: Compute Core Prevails, Cooling Outpaces

IT Infrastructure accounted for 48% of the Ireland hyperscale data center market size in 2024, driven by accelerated refresh cycles to NVIDIA H200 and AMD MI300 GPU clusters. Each rack now supports upwards of 4 PFLOPS, swelling average capex per white-space square meter. However, Cooling Systems record the highest 18.50% CAGR through 2030 as liquid-cooling adoption accelerates. Immersion tanks and CDU loops demand higher upfront spend yet cut operational energy costs by up to 30%. Electrical Infrastructure—spanning UPS, switchgear, and busways—sees steady upgrades due to higher instantaneous power draws, though growth remains moderate because operators reuse existing electrical rooms where feasible.

Component convergence also rises: rear-door heat-exchanger vendors partner with power-distribution manufacturers to co-optimize airflow-plus-power pathways, shortening commissioning timelines. General Construction benefits from modular steel frames that support 36-rack pods, enabling phased capacity additions aligned to AI demand curves. While mechanical systems such as chillers decline in share, pumps and heat-rejection towers for liquid loops compensate, ensuring the segment’s revenue base remains robust.

By Tier Standard: Reliability Trade-Offs Evolve

Tier III facilities contributed 71% of 2024 revenue as concurrent maintainability satisfies most cloud-native redundancy requirements without incurring Tier IV premiums. Multi-availability-zone architectures replicate data at the software layer, letting operators allocate capital toward GPU density rather than duplicate power feeds. Nonetheless, Tier IV grows at 10.40% CAGR because training outages on 100-billion-parameter models incur significant opportunity cost. Financial-services clients and sovereign AI labs increasingly stipulate fault-tolerant pathways under tightened operational-resilience rules. Mixed-tier campuses appear, where modules within the same compound offer different service-level agreements, optimizing land use and capital allocation.

By End-User Industry: Cloud Dominance Deepens

Cloud and IT applications absorbed 58% of 2024 demand and expand at 19.10% CAGR, indicating ongoing consolidation of global workloads into hyperscale nodes. Multicloud disaster-recovery strategies funnel incremental traffic toward Ireland as an offset to Frankfurt and Amsterdam capacity crunches. Telecom remains a secondary but strategic user as 5G standalone cores and Open-RAN vDU pools migrate to edge-inside-hyperscale hosts. The Government vertical gains momentum as the Connecting Government 2030 plan pushes 90% of local authority services online, lifting public-cloud consumption. Media, BFSI, Manufacturing, and E-Commerce maintain single-digit shares yet innovate with AI inference jobs that prefer proximal GPU availability, reinforcing baseline utilization for operators.

By Data Center Size: Massive Lead, Mega Momentum

Massive facilities between 25 MW and 60 MW retained 46% revenue share in 2024, conforming neatly to the 50 MW grid limit while retaining scale economics. Operators configure these campuses with expansion bays that allow step-ups once policy relaxes. Mega sites above 60 MW, though challenged by grid constraints, register a 13.60% CAGR due to on-site generation innovations such as hydrogen-ready gas turbines and 150 MWh batteries. Power-purchase agreements with upcoming offshore-wind clusters further unlock approvals for Mega footprints. Large sites below 25 MW slow as latency-sensitive edge functions shift toward metropolitan micro-data centers instead of traditional colocation rooms.

Geography Analysis

Ireland’s trans-Atlantic cables and temperate climate create strategic advantages that keep the Ireland hyperscale data center market competitive despite tight electricity margins. Greater Dublin hosts more than 75% of capacity, favored for fiber density and skilled talent. Land scarcity and rising grid curtailment drive operators to Kildare, Wicklow, and Meath, where new 110 kV lines add incremental headroom. Cork emerges as a secondary cluster riding submarine-cable landings and university talent pools. The Midlands attract energy-park models that pair wind farms with privately wired campuses, as seen in AWS’s co-located turbines project.

Competitive Landscape

The top four hyperscalers Amazon Web Services, Microsoft, Google, and Meta—collectively operate most capacity and continue multi-billion-dollar expansions. Their procurement scale secures long-lead GPUs and switchgear, creating cost advantages over smaller peers. Efficiency races center on liquid-cooling breakthroughs and machine-learning-driven workload orchestration. Amazon’s USD 150 billion global capex plan underscores long-run commitment to hyperscale dominance. Microsoft’s Dublin expansion of USD 230 million integrates battery-energy-storage and recycled-heat networks, aligning sustainability with capacity.

Colocation incumbents Equinix and Digital Realty differentiate via carrier-neutral ecosystems and renewable certificates that satisfy enterprise compliance. Vantage Data Centers and Kao Data enter with purpose-built high-density halls, promising sub-1.15 PUE and rack loads over 100 kW. Market entry barriers rise as power allocations shrink, spurring mergers such as Equinix’s acquisition of BT’s sites. Suppliers like Vertiv and Anord Mardix ramp local manufacturing to shorten delivery cycles for switchgear and cooling kits, reinforcing Ireland’s specialist supply chain.

Ireland Hyperscale Data Center Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Meta Platforms, Inc.

Equinix, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: IDA Ireland approved 179 FDI projects in H1 2025, many focused on data-centric R and D.

- June 2025: IREN Limited lifted mining capacity to 40 EH/s and announced Horizon 1 AI data center with liquid cooling.

- May 2025: BSO launched DataOne in France, a giga-scale AI center with 100% renewables, signaling continental competition.

- April 2025: Vertiv posted USD 2.036 billion Q1 sales, up 24% YoY, driven by AI-tied power solutions.

- February 2025: Vantage pledged EUR 1.4 billion (USD 1.61 billion) for EMEA expansion, including Irish campuses.

Ireland Hyperscale Data Center Market Report Scope

Hyperscale data centers, also known as Enterprise Hyperscale facilities, are large-scale infrastructures owned and managed by the companies they support. These centers deliver a wide range of scalable applications and storage services to meet the needs of individuals and businesses. Designed for efficiency, they house thousands of servers alongside critical hardware like routers, switches, and storage disks. To ensure seamless operations, these facilities are equipped with advanced support systems, including power and cooling solutions, uninterruptible power supplies (UPS), and air distribution networks.

The Ireland Hyperscale Datacenter Market is Segmented by Data Center Type (Hyperscale Colocation, Enterprise/Hyperscale Self Build), By Service Type (IaaS ( Infrastructure-as-a-Service), PaaS ( Platform-as-a-Service), SaaS( Software-as-a-Service)), By End User (Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, E-Commerce, Other End User). The Report Offers the Market Size and Forecasts for all the Above Segments in Terms of USD (millions).

| Hyperscale Self-Build |

| Hyperscale Colocation |

| IT Infrastructure | Server Infrastructure |

| Storage Infrastructure | |

| Network Infrastructure | |

| Electrical Infrastructure | Power Distribution Unit |

| Transfer Switches and Switchgears | |

| UPS Systems | |

| Generators | |

| Other Electrical Infrastructure | |

| Mechanical Infrastructure | Cooling Systems |

| Racks | |

| Other Mechanical Infrastructure | |

| General Construction | Core and Shell Development |

| Installation and Commissioning | |

| Design Engineering | |

| Fire, Security and Safety Systems | |

| DCIM/BMS Solutions |

| Tier III |

| Tier IV |

| Cloud and IT |

| Telecom |

| Media and Entertainment |

| Government |

| BFSI |

| Manufacturing |

| E-Commerce |

| Other End Users |

| Large (Less than equal to 25 MW) |

| Massive (Greater than 25 MW and less than equal to 60 MW) |

| Mega (Greater than 60 MW) |

| By Data Center Type | Hyperscale Self-Build | |

| Hyperscale Colocation | ||

| By Component | IT Infrastructure | Server Infrastructure |

| Storage Infrastructure | ||

| Network Infrastructure | ||

| Electrical Infrastructure | Power Distribution Unit | |

| Transfer Switches and Switchgears | ||

| UPS Systems | ||

| Generators | ||

| Other Electrical Infrastructure | ||

| Mechanical Infrastructure | Cooling Systems | |

| Racks | ||

| Other Mechanical Infrastructure | ||

| General Construction | Core and Shell Development | |

| Installation and Commissioning | ||

| Design Engineering | ||

| Fire, Security and Safety Systems | ||

| DCIM/BMS Solutions | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-User Industry | Cloud and IT | |

| Telecom | ||

| Media and Entertainment | ||

| Government | ||

| BFSI | ||

| Manufacturing | ||

| E-Commerce | ||

| Other End Users | ||

| By Data Center Size | Large (Less than equal to 25 MW) | |

| Massive (Greater than 25 MW and less than equal to 60 MW) | ||

| Mega (Greater than 60 MW) | ||

Key Questions Answered in the Report

What is the current value of the Ireland hyperscale data center market?

The market stands at USD 1.14 billion in 2025 and is projected to reach USD 17.88 billion by 2031.

Which segment grows fastest within the Ireland hyperscale data center market?

Cooling Systems lead component growth, advancing at an 18.50% CAGR as liquid-cooling adoption accelerates.

How does the EirGrid 50 MW moratorium affect new data centers?

It compels developers to design smaller blocks, add on-site generation, or adopt battery storage to secure grid access, cutting market CAGR by an estimated 15.3%.

Why is Dublin attractive for hyperscale operators?

Low-latency trans-Atlantic cables, a cool climate, and high fiber density lower operating costs and enhance global connectivity.

What role does offshore wind play in future capacity?

Ireland’s goal of 37 GW offshore wind by 2050 aims to supply clean electricity that can unlock Mega-scale data centers beyond current grid constraints.

Who are the leading players in the Ireland hyperscale data center industry?

Amazon Web Services, Microsoft, Google, Meta, Equinix, and Digital Realty dominate through self-build campuses and strategic acquisitions.

Page last updated on: