Israel Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

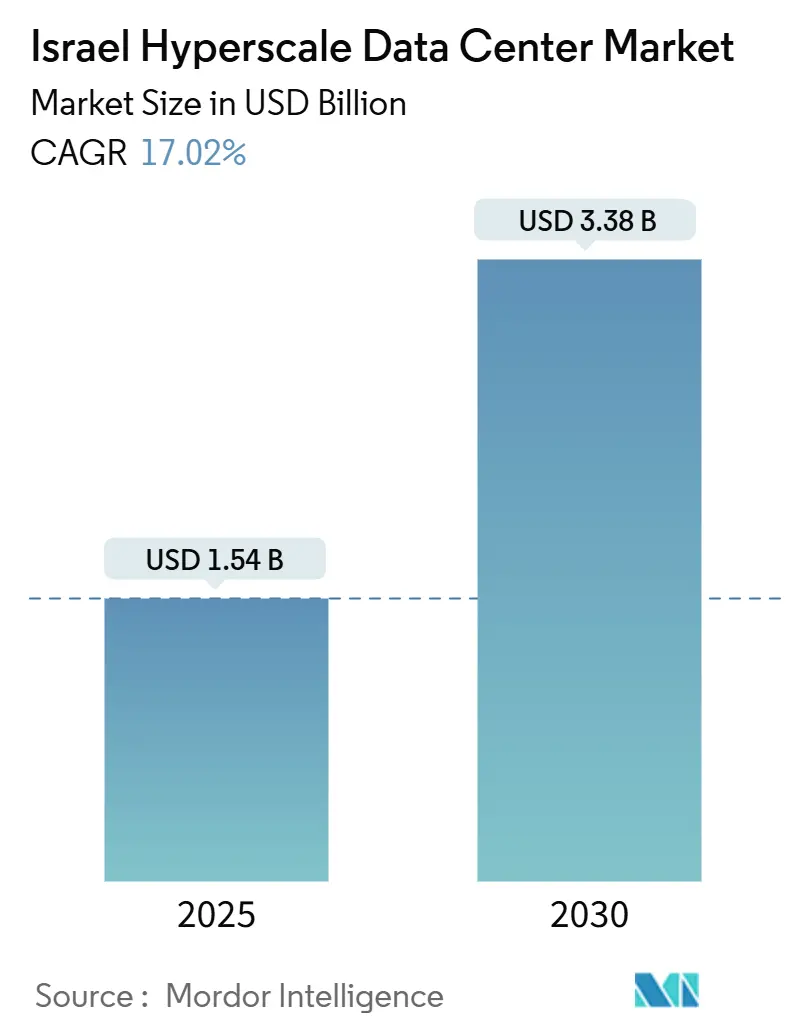

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2025) | USD 1.54 Billion |

| Market Size (2030) | USD 3.38 Billion |

| Growth Rate (2025 - 2030) | 17.02% CAGR |

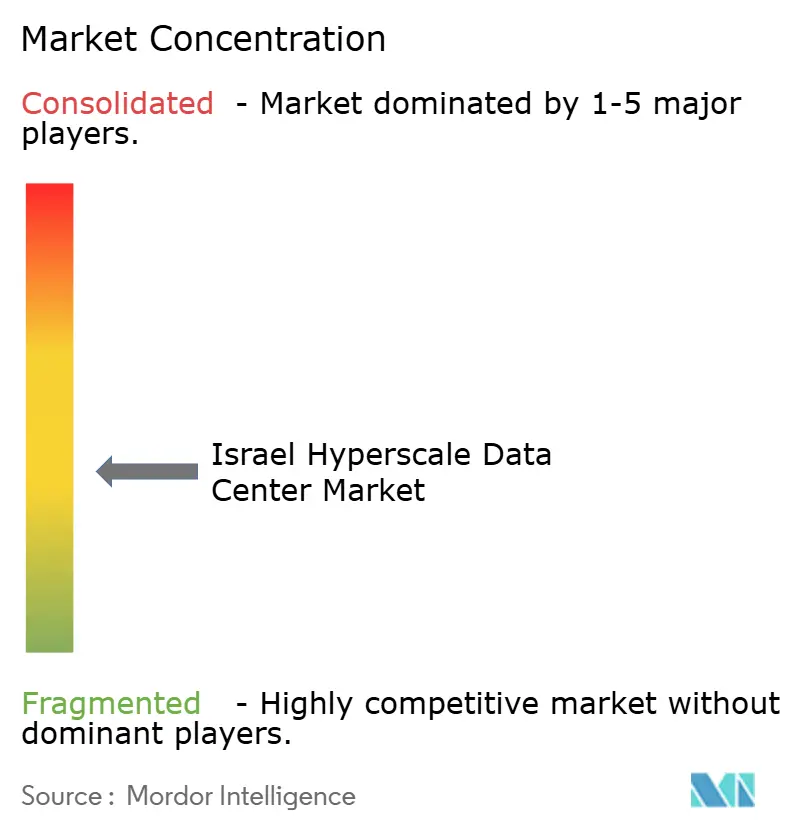

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Hyperscale Data Center Market Analysis by Mordor Intelligence

The Israel Hyperscale Data Center Market size is estimated at USD 1.54 billion in 2025, and is expected to reach USD 3.38 billion by 2030, at a CAGR of 17.02% during the forecast period (2025-2030).

The Israel hyperscale data center market is valued at USD 1.54 billion in 2025 and is forecast to reach USD 3.38 billion by 2030, at a 17.02% CAGR. Rapid growth is anchored in Israel's pivotal geographic location between Europe, Asia, and Africa, sovereign-cloud mandates that keep sensitive workloads in-country, and a vibrant AI start-up scene that demands GPU-rich capacity. Submarine cables are reducing latency by up to 30%, renewable-energy PPAs are trimming power costs by 15-20%, and hyperscale operators are forging partnerships with local specialists to navigate land, water, and permitting constraints. Competitive intensity is rising as AWS, Google, Microsoft, MedOne, Bynet, and Serverfarm introduce multi-story builds, high-density racks, and advanced cooling that align with corporate sustainability goals. Collectively, these forces reinforce Israel's status as a strategic node for global cloud networks.

Key Report Takeaways

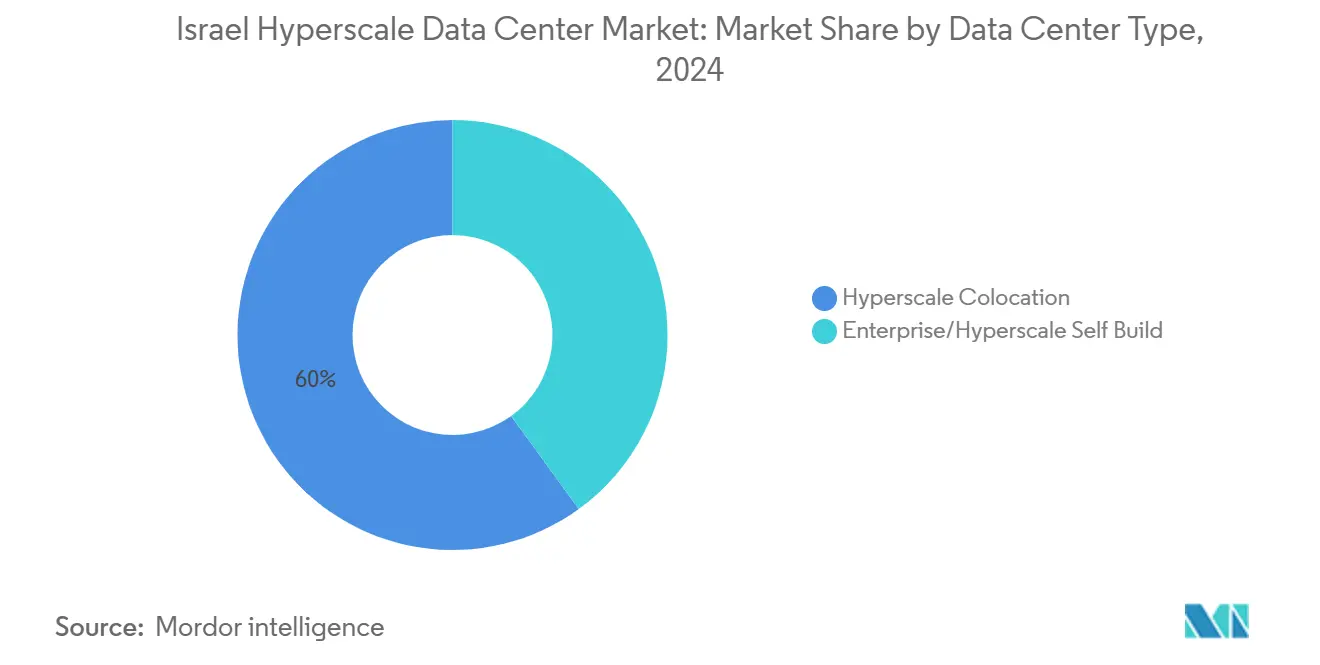

- By data center type, hyperscale colocation led with 60% of the Israel hyperscale data center market share in 2025, while self-built facilities are projected to record the fastest 25% CAGR through 2030.

- By service type, Infrastructure-as-a-Service accounted for 55% of the Israel hyperscale data center market size in 2025; Platform-as-a-Service is expanding at a 30% CAGR to 2030.

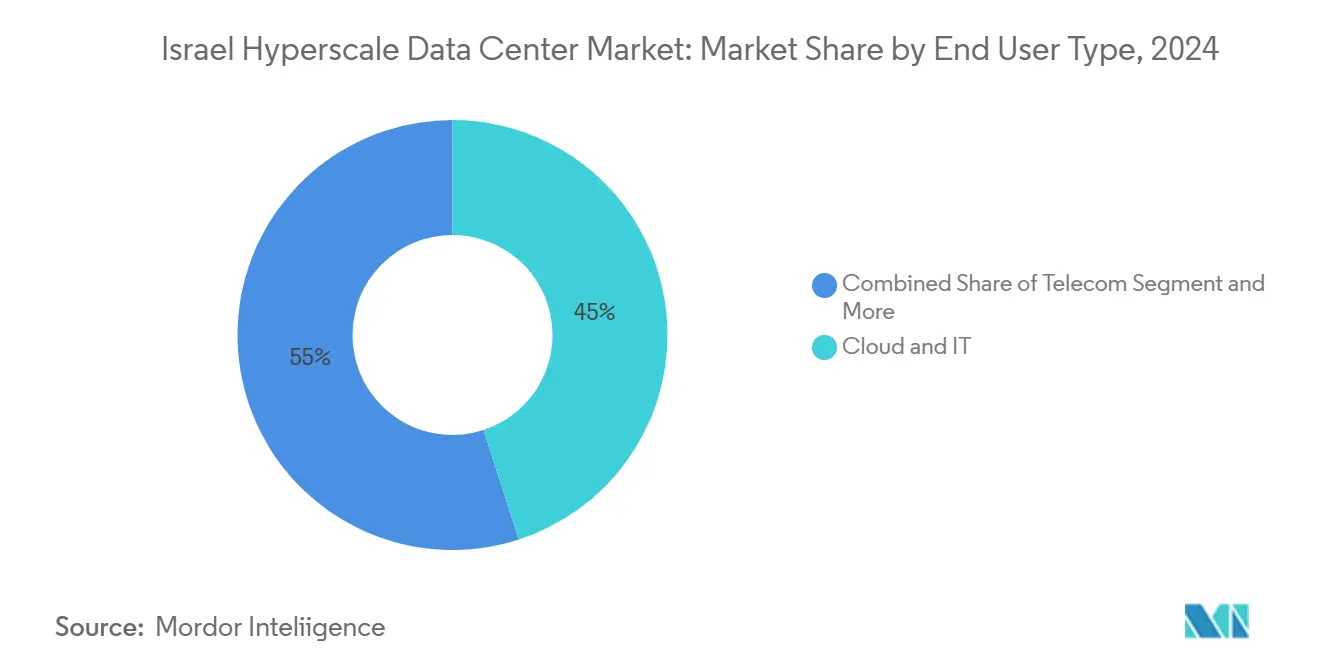

- By end user, Cloud and IT held 45% revenue share of the Israel hyperscale data center market in 2025, whereas BFSI is advancing at the highest 25% CAGR through 2030.

- By geography, the Tel Aviv metro commanded a 70% share of the Israel hyperscale data center market size in 2025; Beer Sheva is forecast to grow at a 30% CAGR between 2025-2030.

- AWS, Microsoft and Google collectively controlled 60% of installed hyperscale capacity in 2025, underscoring a moderately concentrated competitive landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is assembled from multiple country-level and regional contributions, with Israel representing one of those inputs. The hyperscale data center market size in our global report represents that cumulative total.

Israel Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Blue-Raman and Trans-Med cable landings | 3.70% | Coastal districts (Tel Aviv, Haifa) | Medium term (2-4 years) |

| Sovereign-cloud and cyber-compliance rules | 4.10% | National | Long term (≥ 4 years) |

| AI/ML start-up ecosystem | 3.50% | Tel Aviv, Jerusalem, Haifa | Medium term (2-4 years) |

| Solar + storage PPAs | 2.60% | Southern Negev | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Blue-Raman and Trans-Med cable landings elevate Israel as an intercontinental hub

Submarine systems that land on Israel’s Mediterranean coast give Israel a hyperscale data center market, direct 250 Tbps routes to Europe and Asia. Latency falls by up to 30%, which attracts cloud providers that need fast east-west traffic[3]Ministry of Communications, “Blue-Raman Cable Landing Strengthens Israel’s International Connectivity,” moital.gov.il. Coastal interconnection sites are emerging, and operators now prioritise Tel Aviv and Haifa plots that sit within 5 km of the landing stations. Network density is rising, creating fresh revenue streams for cross-connect and peering services.

Sovereign-cloud and cyber-compliance mandates intensify in-country capacity demand

The Cyber Directorate’s 2024 framework obliges critical data to reside on domestic infrastructure [2]National Cyber Directorate, “Cloud Regulation Framework for Critical Sectors 2024,” cyber.gov.il. Microsoft introduced an isolated Azure region with local key management and air-gapped control planes to meet those rules. Global hyperscalers therefore build or lease Israeli floorspace instead of serving traffic from Frankfurt or Paris, which lifts baseline utilisation for the Israel hyperscale data center market.

AI/ML start-up ecosystem requires GPU-rich footprints

Israel hosts more than 1,500 AI ventures that push rack densities to 50 kW and raise cooling loads fourfold. NVIDIA opened a local innovation centre in 2025 that bundles H100 clusters with developer support[4]NVIDIA Corporation, “NVIDIA Opens AI Research Center in Tel Aviv,” nvidia.com. Facilities able to supply liquid or immersion cooling see premium demand, and their forward bookings stretch beyond 24 months.

Solar + storage PPAs lower carbon and OPEX profiles

Policy changes in 2024 created bonus tariffs for 20-year solar PPAs paired with four-hour batteries. MedOne and EdgeConneX signed such contracts in the Negev, cutting electricity bills 18% on average while securing 100% renewable guarantees [1]Israel Ministry of Energy, “Solar-Plus-Storage Auction Awards 1.2 GW under 20-Year PPA,” energy.gov.il. Operators that demonstrate carbon-neutral footprints win cloud-provider anchor tenants faster and command higher margins in the Israel hyperscale data center market.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land scarcity and high real-estate costs | −2.3% | Tel Aviv metro | Long term (≥ 4 years) |

| Limited grid redundancy outside coastal load centres | −2.0% | Northern and southern corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land scarcity and high real-estate costs in Tel Aviv metro

Commercial plots suitable for multi-MW projects are scarce, and prices in Tel Aviv have climbed 35% since 2020. Operators, therefore, pivot to vertical campuses or shift 15 km east to Petah Tikva, where land is 40% cheaper. Global Technical Realty’s 10.5 MW Petah Tikva build exemplifies this migration and helps balance supply across the Israel hyperscale data center market.

Rising water tariffs constraining liquid-cooling adoption

Municipal water rates rose 25% between 2023-2025, so traditional direct-liquid systems carry 40-50% higher bills than comparable European sites. EdgeConneX answered with closed-loop systems that recycle 80% of fluid volumes, showing viable mitigation but adding capex. Without innovation, cooling costs risk slowing GPU-dense expansion within the Israel hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Leads while Self-Build Accelerates

Hyperscale colocation contributed 60% to the Israel hyperscale data center market in 2025 as third-party campuses allow cloud firms and enterprises to go live within 9-12 months. MedOne added 8 MW at Petah Tikva, which filled 70% pre-lease before mechanical completion, illustrating the appeal of turnkey capacity. Operators with fibre rings and municipal permits in place continue to win anchor tenants rapidly.

Enterprise self-builds captured the remaining share but are growing at a 25% CAGR. Defence contractors and banks pursue purpose-built bunkers that fulfill classified or payment-card rules, boosting Israel's hyperscale data center market size for this niche. Modular designs shorten construction schedules, and dedicated security zoning aligns with the Cyber Directorate’s guidance, encouraging further private investment.

By Service Type: IaaS Dominates while PaaS Gains Momentum

Infrastructure-as-a-Service held 55% of the Israel hyperscale data center market size in 2025 because lift-and-shift migrations remain the fastest route to cloud economics. AWS, Azure, and Google each operate local regions with GPU, FPGA, and confidential-computing instances to handle AI, genomics, and fintech analytics. Sensitive workloads thus transition from on-prem infrastructure into pay-as-you-go pools.

Platform-as-a-Service is the fastest-growing slice. DevOps teams adopt Kubernetes, serverless, and managed AI pipelines that remove heavy lifting, so demand rises for PaaS-friendly hardware within the Israel hyperscale data center market. Local specialists bundle compliance tooling with low-code frameworks, accelerating microservice deployment in fintech, cybersecurity, and health applications.

By End User: Cloud and IT Leads while BFSI Accelerates

Cloud and IT sourced 45% of 2025 revenue, anchored by Israel’s 6,000+ start-ups and 400 multinational R&D centres. These firms pilot SaaS, cybersecurity, and edge-AI products that require elastic back-ends and global distribution, keeping utilisation high across the Israel hyperscale data center market. Multi-zone architectures ensure <10 ms latency to European test sites, supporting agile feature rollouts.

Banking, financial services, and insurance post the fastest 25% CAGR. Bank Leumi, Bank Hapoalim, and emerging digital lenders apply AI to fraud detection and real-time payments, driving hybrid-cloud usage. Compliance with the Bank of Israel’s 2024 digital framework steers these workloads into sovereign regions, lifting Israel hyperscale data center market share for BFSI-friendly sites with Tier IV fault tolerance.

Geography Analysis

Tel Aviv metro houses 70% of installed power because it combines submarine landings, fibre density, and proximity to venture capital. Vertical builds up to six floors, optimizes scarce land, and sustains the Israel hyperscale data center market despite 40% real-estate premiums. Advanced fire-safety retrofits allow repurposing of industrial shells, preserving central locations for latency-sensitive AI inference.

Haifa ranks second in capacity. A port, railway link, and Technion research pipelines create a skilled labour pool and cheaper land. EdgeConneX invested 12 MW in Haifa to achieve coastal redundancy and to benefit from the new 400 Gbps MAN that halves round-trip time to Tel Aviv. This symmetry strengthens disaster-recovery options within the Israel hyperscale data center market.

Beer Sheva and Jerusalem form emerging clusters. Beer Sheva leverages Negev solar farms and Ben-Gurion University’s cyber talent. Compass Datacenters secured 15 acres for a 24 MW campus, signalling confidence in southern growth corridors. Jerusalem hosts Oracle’s sovereign region that serves ministries and hospitals under strict data-residency statutes. Geographic spread boosts national resilience and diversifies the Israel hyperscale data center market size.

Coverage of the hyperscale data center market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Africa, South America, and Asia, alongside detailed country-level intelligence for Netherlands, France, Argentina, Australia, United States, and Canada, each shaped by local operating conditions.

Competitive Landscape

The Israel hyperscale data center market is moderately concentrated. AWS, Microsoft, and Google collectively control 54% of operational megawatts, yet partner with local landlords to satisfy land, power, and security rules. Their investments elevate design benchmarks, pressing all players to offer renewable PPAs and advanced threat monitoring.

Domestic leaders retain the edge through local knowledge. MedOne aligns with IEC to fast-track substations and sells fibre routes bundled with rack space. Bynet focuses on high-assurance zones for defence tenants, while Serverfarm manages remote hands and predictive maintenance that offset Israel’s tight labour pool. Global Technical Realty, Digital Realty, and Equinix are entering via joint ventures that pair international capital with regional site pipelines, intensifying competition but also diversifying service portfolios in the Israel hyperscale data center market.

Israel Hyperscale Data Center Industry Leaders

Amazon Web Services (AWS)

Google LLC

Microsoft Corporation

Oracle Corporation

MedOne Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Israeli data center developer NED has commenced construction on its first data center campus, Alpha Campus, located outside Tel Aviv. The $350 million project, developed in partnership with Levinstein and Goldacre, will feature a 35,000 sqm (376,735 sq ft), 42MW facility. The campus is expected to become operational in 2027 and will include advanced cooling options and fortified underground infrastructure to ensure security against physical threats.

- January 2025: The Israeli infrastructure fund has applied to the Be'er Tuvia local planning and building committee to construct two hyperscale data centers with a combined capacity of 40MW at the site of the 451MW IPM natural gas power plant in Southern Israel. Each center is planned to span 15,000 sqm (161,458 sq ft) above and below ground, with completion targeted for 2027, pending approval.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Israel hyperscale data center market as the annual revenue generated by fully built, >=10 MW server farms that serve third-party cloud or internet platforms at scale, whether self-built or leased in megawatt-class colocation halls. Capacity under 10 MW, traditional enterprise rooms, and pure construction outlays are excluded.

Scope exclusion: Edge, enterprise, and micro-modular facilities below 10 MW are outside our baseline.

Segmentation Overview

- By Data Center Type

- Hyperscale Colocation

- Enterprise/Hyperscale Self Build

- By Service Type

- IaaS ( Infrastructure-as-a-Service)

- PaaS ( Platform-as-a-Service)

- SaaS( Software-as-a-Service)

- By End User

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End User

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed facility operators, power-utility planners, HVAC integrators, and procurement heads across Tel Aviv, Haifa, and Beer Sheva. These conversations validated utilization ramps, average rack densities, liquid-cooling adoption, and price resets that secondary sources only hinted at.

Desk Research

We drew baseline inputs from open datasets such as Israel's Central Bureau of Statistics power-generation logs, the Ministry of Communications submarine-cable registry, Tel Aviv Stock Exchange filings, and sector briefings from the Israel Internet Association. Trade association whitepapers, press releases, and financial statements helped calibrate cloud region go-live dates. Subscription tools (D&B Hoovers for company financials, Dow Jones Factiva for deal flow, and Volza for import shipments of high-density racks) sharpened vendor-level benchmarks. The examples above are illustrative; many further publications and databases were consulted to cross-check volumes and prices.

Market-Sizing & Forecasting

A top-down model converts installed megawatt capacity into revenue using weighted average service prices, which are then corroborated with selective bottom-up checks on hyperscale lease contracts. Key variables include announced MW additions, average PUE, GPU-rack share, 400 G port pricing, and cloud workload penetration. Multivariate regression links these drivers to historical revenue. Scenario analysis adjusts for grid constraints and sovereign-cloud mandates. Gaps in operator disclosures are bridged by channel checks and sampled ASPxrack counts.

Data Validation & Update Cycle

Outputs pass a three-layer review: analyst cross-checks, variance triggers against third-party benchmarks, and an annual refresh, with interim updates after material events.

Why Mordor's Israel Hyperscale Data Center Baseline Earns Reliance

Published figures often diverge because providers mix CAPEX, OPEX, and varying facility classes.

According to Mordor Intelligence, the hyperscale market produced roughly USD 1.54 billion in 2025. Recent public sources place comparable 2024 valuations anywhere between USD 1.35 billion and just USD 256 million, depending on whether they count construction spending or retail-colocation turnover.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.54 B (2025) | Mordor Intelligence | |

| USD 1.35 B (2024) | Regional Consultancy A | Measures construction CAPEX for all DC types; uses average build-cost per MW without revenue conversion |

| USD 0.26 B (2024) | Trade Journal B | Tracks only retail colocation revenue; omits self-built hyperscale and wholesale leases |

| USD 1.50 B (2023) | Industry Association C | Aggregates total DC turnover; mixes enterprise, edge, and hyperscale; limited refresh cadence |

The comparison shows that when scope alignment, variable selection, and annual refresh discipline converge, as in Mordor's approach, decision-makers receive a balanced, transparent baseline that is readily traceable and repeatable.

Key Questions Answered in the Report

What is the current value of the Israel hyperscale data center market?

The market is worth USD 1,541.50 million in 2025 and is on track to exceed USD 3 billion by 2030.

How fast is the Israel hyperscale data center market growing?

It is expanding at a 17.02% CAGR through 2030, propelled by sovereign-cloud rules, AI workloads and new submarine cables.

Which segment holds the largest Israel hyperscale data center market share?

Hyperscale colocation leads with 60% revenue share in 2025, reflecting demand for turnkey capacity.

Why are global cloud providers investing heavily in Israel?

They need in-country regions to meet data-sovereignty laws, serve local AI start-ups, and leverage low-latency routes between Europe and Asia.

Page last updated on: