Germany Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

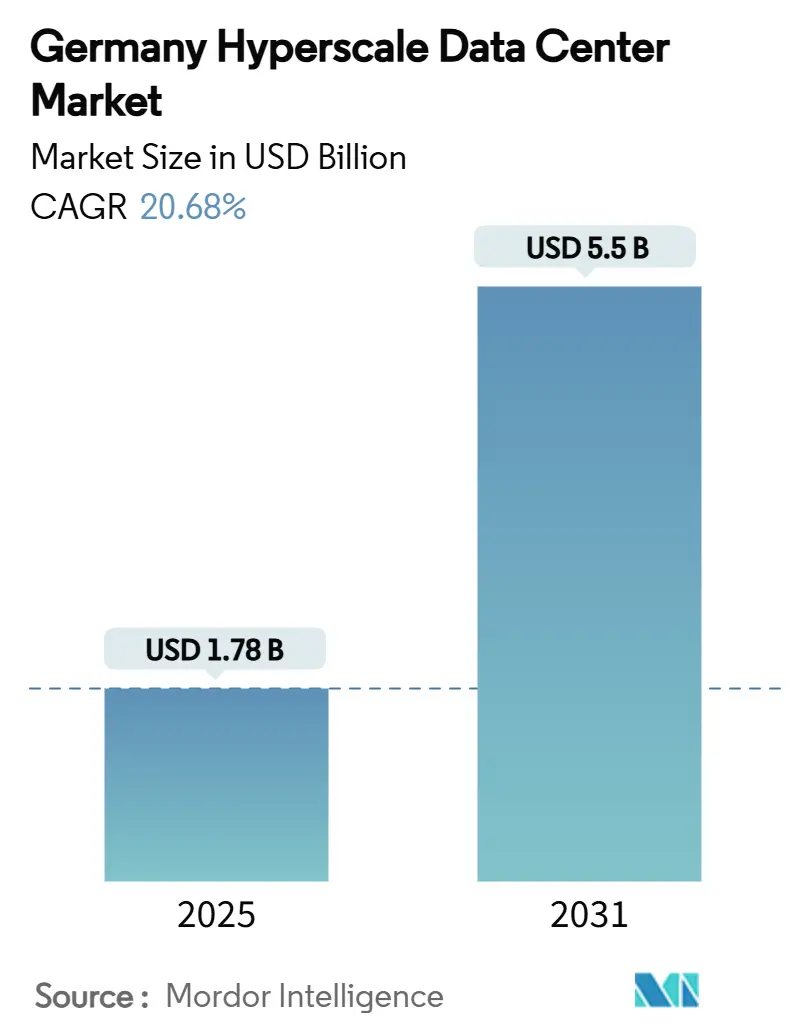

| Market Size (2025) | USD 1.78 Billion |

| Market Size (2030) | USD 5.5 Billion |

| Growth Rate (2025 - 2031) | 20.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Hyperscale Data Center Market Analysis by Mordor Intelligence

The Germany hyperscale data center market size stands at USD 1,781.51 million in 2025 and is projected to reach USD 5,503.28 million by 2031 at a 20.68% CAGR, while installed IT capacity is set to expand from 2,451.07 MW in 2025 to 3,942.78 MW by 2031 at an 8.24% CAGR. The rapid uptick reflects Germany’s dual role as Europe’s digital-sovereignty nucleus and an AI infrastructure hotspot, where sovereign-cloud mandates, AI/ML rack densities above 50 kW and renewable-energy targets converge to reshape build strategies. Operators are prioritizing higher-density, GPU-centric architectures that favor liquid cooling, 415 V three-phase distribution and renewable power purchase agreements. Grid constraints in tier-1 metros are shifting capacity toward Brandenburg and other secondary hubs, while sovereign-cloud compliance drives premium pricing for certified footprints. Competitive intensity is rising as hyperscalers expand direct builds, forcing colocation providers to add build-to-suit options, liquid-cooling expertise and renewable PPAs to retain share.

Key Report Takeaways

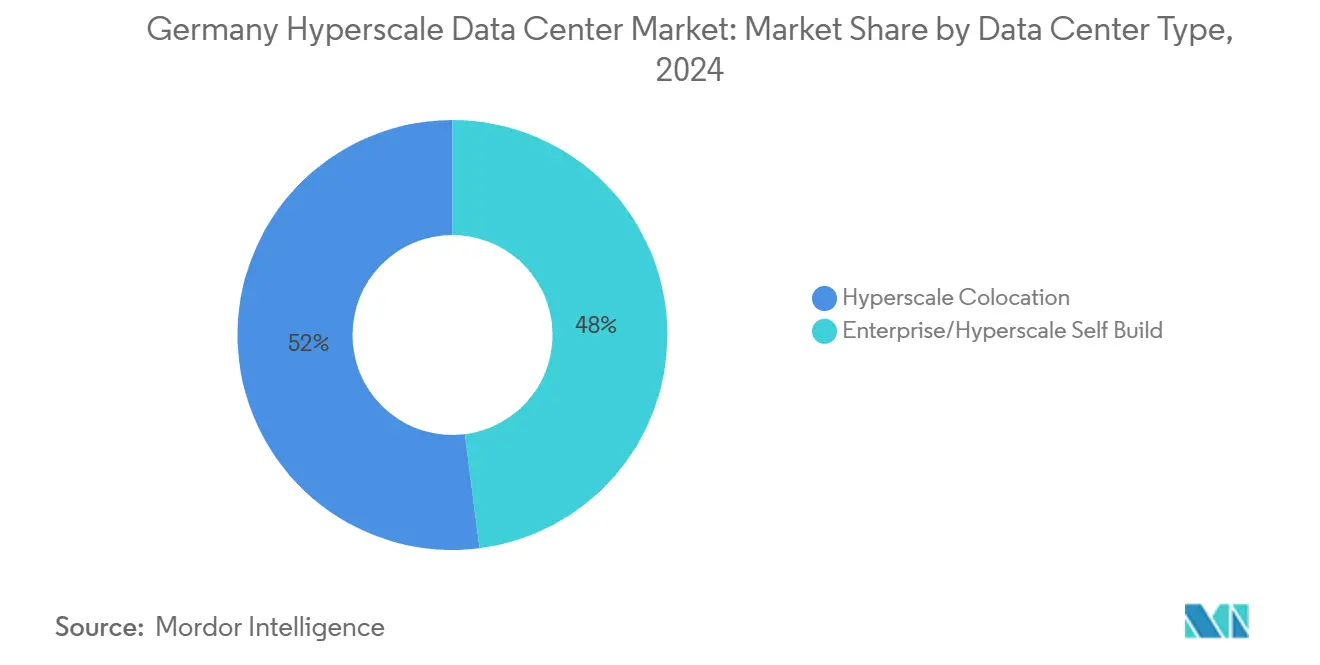

- By data center type, hyperscale colocation held 52% revenue share in 2024, while hyperscaler self-builds are projected to grow at a 12.8% CAGR to 2031.

- By component, IT infrastructure accounted for a 41.2% share of the Germany hyperscale data center market size in 2024 and is advancing at a 14.6% CAGR through 2031.

- By tier standard, Tier III sites commanded 60% share in 2024, whereas Tier IV facilities are rising at a 13.4% CAGR over 2025-2031.

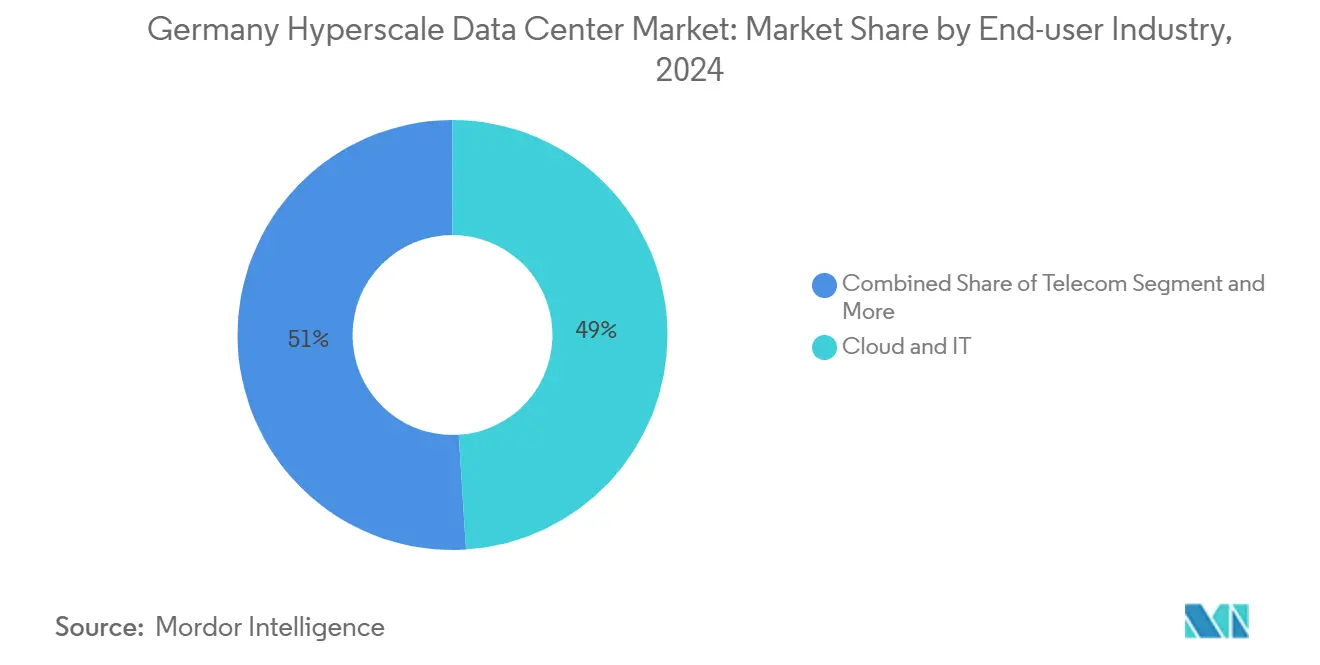

- By end-user industry, cloud and IT services held 49% share in 2024, and this segment leads growth at a 15.2% CAGR through 2031.

- By data center size, massive-scale sites captured 46% of the Germany hyperscale data center market size in 2024, while mega-scale campuses are projected to expand at a 16.0% CAGR between 2025-2031.

- By geography, Frankfurt/Rhein-Main led with 58% of the Germany hyperscale data center market share in 2024, whereas Berlin/Brandenburg is forecast to post the fastest 14.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Germany reflects both domestic market structures and the presence of firms operating internationally. The market landscape study of the global hyperscale data center industry shows how these players are arranged across regions.

Germany Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging GPU-centric AI/ML rack densities (>50 kW) | +4.20% | Frankfurt, Berlin, Munich metros | Medium term (2-4 years) |

| Sovereign-cloud compliance (GDPR, BSI C5) builds | +3.80% | National, weighted to Frankfurt/Berlin | Long term (≥4 years) |

| Real-time payment and CBDC latency mandates | +2.10% | Frankfurt financial district, nationwide rollout | Medium term (2-4 years) |

| 5G edge–core consolidation around metro hubs | +2.90% | Major metros and secondary cities | Long term (≥4 years) |

| GenAI inference clusters needing liquid cooling | +3.50% | Core markets with power headroom | Short term (≤2 years) |

| Availability-based renewable PPAs for capacity hedge | +2.70% | Northern Germany, offshore-wind corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging GPU-centric AI/ML rack densities ( Greater than 50 kW)

Rack power envelopes now exceed 50 kW in most AI training clusters, rendering air cooling impractical for NVIDIA H100 deployments. Microsoft’s EUR 3.2 billion (USD 3.73 billion) programme underscores the pivot from storage-heavy builds to compute-optimized halls that demand direct-to-chip or immersion cooling. Operators are retrofitting distribution to 415 V three-phase topologies, while UPS vendors introduce fast-response modules to manage GPU burst loads. Northern Data’s roll-out of 19,000 H100 GPUs exemplifies the capex premium attached to AI-ready halls [1].Northern Data Group, “Q3 2024 Results,” northerndata.de Source: IBM, “IBM Cloud C5 Germany Compliance,” ibm.com Premium price points and density gains widen gross-margin potential but raise engineering complexity across the Germany hyperscale data center market.

Sovereign-cloud compliance (GDPR, BSI C5) builds

Germany’s digital-sovereignty agenda makes BSI C5 attestation and data-residency guarantees compulsory for public-sector workloads. T-Systems’ Sovereign Cloud powered by Google Cloud shows how compliance capital spend turns into a competitive moat [2].T-Systems, “Sovereign Cloud Powered by Google Cloud,” t-systems.com NIS-2 implementation expands cyber-resilience obligations to thousands of operators, tightening operational checkpoints. Certification overheads lengthen project schedules but let compliant sites command higher yields, cementing compliance as a demand driver within the Germany hyperscale data center market.

Real-time payment and CBDC latency mandates

The ECB’s 2024 distributed-ledger tests cleared EUR 1.6 billion (USD 1.86 billion) in central-bank money and signalled permanent demand for sub-millisecond infrastructure [3]European Central Bank, “Exploratory Work on New Technologies,” ecb.europa.eu. Frankfurt’s financial core positions Frankfurt data centers within a few milliseconds’ round-trip of major trading engines, driving demand for low-latency infrastructure and edge deployments near exchanges and clearing venues. O2 Telefónica’s 5G core on AWS demonstrates telco alignment around ultra-low-latency compute. Low-latency finance broadens workload diversity and reinforces demand for fault-tolerant Tier IV space in the Germany hyperscale data center market.

5G edge–core consolidation around metro hubs

Allocations of private 5G spectrum to automotive OEMs are turning Munich, Stuttgart and Wolfsburg into micro-edge clusters serving factory automation. Deutsche Telekom plans 10,000 edge-cloud nodes by 2030, yet prefers metro aggregation sites for economy-of-scale management. Consolidated hubs lower TCO and streamline cyber controls, weaving 5G and AI into the Germany hyperscale data center market’s fabric.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-use caps on evaporative cooling | -2.80% | Water-stressed regions, urban cores | Short term (≤2 years) |

| GPU/optics supply-chain shortages | -3.20% | Nationwide, all major projects | Medium term (2-4 years) |

| Heat-reuse mandate increasing CapEx (draft law) | -2.10% | Urban zones with district heating | Medium term (2-4 years) |

| Grid-connection curtailment >30 MW in tier-2 cities | -1.90% | Secondary markets, emerging metros | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Water-use caps on evaporative cooling

EU sustainability rules now compel water-use disclosure, spotlighting daily consumption that can hit 5 million gallons at large sites [4].Business Insider, “Schneider Electric and NVIDIA Data Center Designs,” businessinsider.com DENEFF’s survey shows 56% of operators see weak demand for heat-reuse, limiting synergy between water and thermal efficiency. Urban water caps tighten allowable draw, pushing operators toward closed-loop adiabatic or liquid systems that cost more upfront and lift the operational hurdle in the Germany hyperscale data center market.

GPU/optics supply-chain shortages

Europe accounts for only 9% of global semiconductor output, exposing German builds to GPU bottlenecks and 12-month lead times. Geopolitical risks around Taiwanese production amplify uncertainty. Delays cascade from GPUs to high-speed optics, threatening project schedules and slowing capacity additions across the Germany hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Dominance Meets Self-Build Acceleration

Hyperscale colocation controlled 52% revenue in 2024, reflecting entrenched enterprise preference for turnkey resilience. However, the Germany hyperscale data center market now sees hyperscaler self-builds expanding at 12.8% CAGR as cloud majors seek architectural control for AI and sovereignty workloads. The accelerating pipeline lifts the Germany hyperscale data center market as AWS, Microsoft, and Oracle commit multibillion budgets to bespoke campuses.

Self-builds embed direct-to-chip cooling, 400 G fabric and custom power paths that colocation shells seldom pre-install. Colocation incumbents respond with build-to-suit modules, sovereign-cloud enclaves and flexible land banks. This two-track growth cushions demand volatility and broadens service menus across the Germany hyperscale data center industry.

By Component: IT Infrastructure Drives Transformation

IT infrastructure delivered 41.2% of 2024 revenue, leading segment growth at 14.6% CAGR as GPU server clusters displace storage-centric racks. The Germany hyperscale data center market size for server nodes outpaces chillers and generators as training workloads dominate capex.

Electrical gear follows closely: 415 V busways, fast-transfer switchgear and lithium-ion UPS units rise in tandem with rack density. Mechanical spend migrates toward liquid loops and rear-door exchangers, though legacy chilled-water plants still underpin lower-density halls. The evolving bill-of-materials lifts average project value in the Germany hyperscale data center market while deepening vendor specialization.

By Tier Standard: Tier IV Gains Momentum

Tier III installations hold 60% of operational floor space, the historical default for concurrent maintainability. Yet Tier IV footprints are climbing at 13.4% CAGR to satisfy AI and fintech uptime thresholds. The Germany hyperscale data center market size for Tier IV halls grows faster as operators chase premium rents that offset duplication costs.

Investors absorb higher capex because Tier IV contracts usually span 10-15 years. Additionally, energy-efficiency law incentives for heat reuse and PUE cutbacks dovetail with Tier IV’s modular-redundancy ethos. The design shift cements fault-tolerant architecture as a new benchmark within the Germany hyperscale data center market.

By End-User Industry: Cloud Services Dominate

Cloud and IT services captured 49% share in 2024 and will compound at 15.2% CAGR through 2031. Enterprise cloud-migration, SaaS adoption and AI platform demand feed ballooning footprints for hyperscalers and regional providers.

Telecom ranks next as 5G and edge architectures converge. BFSI workloads remain sticky in Frankfurt due to latency sensitivities, while manufacturing embraces Industry 4.0 digital twins that require real-time analytics. Government, e-commerce and media streams add diversity, reducing dependency on any one vertical and enriching the Germany hyperscale data center market.

By Data Center Size: Mega-Scale Facilities Emerge

Massive-scale campuses of 25-60 MW hold the largest slice at 46% in 2024, but mega-scale builds above 60 MW post a 16.0% CAGR as operators consolidate fleets. Mega sites exploit land and power economies, driving down unit opex across the Germany hyperscale data center market.

Projects such as NTT’s 500 MW campus and the Schwarz Group’s 200 MW Lübbenau build illustrate how retail, cloud and telco stakeholders converge on giga-campuses. Smaller facilities pivot to edge and specialised compliance niches, ensuring a balanced size mix that underpins the long-term health of the Germany hyperscale data center industry.

Geography Analysis

Frankfurt/Rhein-Main anchors 58% of installed capacity, underpinned by DE-CIX, dense fiber rings and proximity to the . Land scarcity and 100% renewable thresholds push expansion to remote parcels near Limburg and Hanau, yet the metro retains network gravity that secures long-term tenancy. Self-build announcements by AWS and Digital Realty elevate competitive stakes while sustaining the Germany hyperscale data center market.

Berlin/Brandenburg accelerates at a 14.0% CAGR, leveraging lower land prices and sovereign-cloud alignment with federal agencies. Maincubes’ Nauen campus and AWS’s European Sovereign Cloud region validate demand south of the capital Renewable wind supply and open grid capacity shorten permitting cycles, making the corridor the top challenger to Frankfurt in the Germany hyperscale data center market.

Munich/Bavaria and Hamburg/North contribute specialist pull. Munich’s auto OEM clusters drive private-5G and AI model-training demand, whereas Hamburg couples port logistics with offshore wind PPAs. NRW’s Düsseldorf-Cologne axis appeals to industrial IoT workloads. These secondary poles diversify regional risk and ensure the Germany hyperscale data center market size expands beyond historical strongholds.

Mordor Intelligence evaluates the hyperscale data center market across all key regional markets, including Europe, South America, and Asia, with deeper country-level insights covering Netherlands, France, Brazil, Hong Kong, Singapore, and Vietnam.

Competitive Landscape

Competition sits at a medium-high level as colocation majors, sovereign-cloud specialists and hyperscalers cross paths. Digital Realty and Equinix consolidate Frankfurt plots while integrating liquid cooling to host NVIDIA clusters. AWS budgets USD 9.44 billion for Frankfurt alone, signalling firm vertical-integration intent. Microsoft’s EUR 3.2 billion AI push and Oracle’s USD 3 billion regional build testify to escalating direct investments.

Sovereign-cloud specialists such as STACKIT and secunet take advantage of compliance niches, targeting public-sector tenders sidelined by hyperscaler data-export fears. Private-equity vehicles like BlackRock-Mainova and Aquila-Bain commit multibillion capital, indicating institutional appetite for long-duration contracted cash flows.

Technological differentiation intensifies: Schneider Electric’s liquid-cooling alliances, Westinghouse-Data4 nuclear power MOU and maincubes’ solar PPA illustrate race-to-net-zero positioning. As supply-chain risks raise project timeframes, incumbents with proven vendor networks maintain advantage, yet mega-scale entrants still erode concentration by adding fresh capacity to the Germany hyperscale data center market.

Germany Hyperscale Data Center Industry Leaders

Amazon Web Services (AWS)

Microsoft Corp.

Alphabet Inc. (Google Cloud)

Oracle Corp.

IBM Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: A consortium of SAP, Deutsche Telekom, Ionos, and Schwarz began scoping a sovereign AI data-processing centre expected to add 200 MW by 2028.

- April 2025: Colt Data Centre Services confirmed a USD 2.3 billion build-out for four German sites totalling 117 MW, each integrating waste-heat export systems.

- April 2025: Digital Realty inaugurated FRA18 inside Frankfurt’s historic Neckermann complex, adding 8,200 sqm of white space.

- April 2025: Data Center Partners acquired land in Mainz for a 40 MW campus; NorthC bought six sites from Colt Technology Services in Germany and the Netherlands.

- January 2025: CyrusOne received permits for its 54 MW FRA5 in Hanau, designed for a 1.27 PUE on 100% renewables.

- May 2025: Portus announced a 5.5 MW site in Munich aimed at high-density GPU colocation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every hyperscale facility in Germany that delivers at least 20 MW of IT load, whether self-built by a cloud provider or leased under a hyperscale colocation contract; the valuation reflects the fully fitted white space plus critical power, cooling, network, and DCIM systems.

Scope Exclusions: Edge modules below 5 MW, enterprise server rooms, and powered-shell real-estate projects are excluded.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-Build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Unit

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning

- Design and Engineering

- Fire Detection and Physical Security

- DCIM/BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT Services

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End User

- By Data Center Size

- Large (Less than equal to 25 MW)

- Massive (Greater than 25 MW and less than equal to 60 MW)

- Mega (Greater than 60 MW)

- By Geography

- Frankfurt / Rhein-Main

- Berlin / Brandenburg

- Munich / Bavaria

- Hamburg / North

- NRW (Dusseldorf-Cologne)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed data-center developers, switch-gear vendors, fiber carriers, and municipal energy officials spread across Frankfurt/Rhein-Main, Berlin, and Bavaria. Dialogues focused on live rack densities, liquid-cooling adoption, power-purchase contract lengths, and vacancy backlogs; insights refined utilization curves and validated growth assumptions captured from desk research.

Desk Research

We began with regulatory filings from the Federal Network Agency, location permits published by state planning offices, and power-grid expansion data from TransnetBW and Amprion. These were matched with deployment statistics from the German Datacenter Association, Eurostat ICT use surveys, and traffic peaks reported by DE-CIX, which together anchor installed and planned capacity. Company 10-Ks, investor decks, and press releases supply capex run-rates, while news archives in Dow Jones Factiva and balance-sheet snapshots in D&B Hoovers let us track operator finances. The sources cited above are illustrative; many additional open datasets and journals were reviewed to cross-check figures and narratives.

Market-Sizing & Forecasting

We start with a top-down reconstruction that multiplies live megawatts in 2024 by average build cost per MW and expected ramp-up timing. We then overlay demand-pool indicators such as cloud spending, GPU shipment growth, renewable-energy share, vacancy rates, and fiber route additions. Supplier roll-ups of announced campuses, channel checks on average selling prices, and sampled lease commitments provide a bottom-up sense-check before totals are finalized. A multivariate regression model, containing variables like national cloud-adoption index and Frankfurt grid headroom, projects value and capacity through 2031; scenario analysis adjusts for power-allocation moratoria or faster AI uptake.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst audits, and a senior-lead sign-off. Variance above five percent versus independent metrics triggers re-contact of field respondents. We refresh every twelve months and issue interim updates after material events such as energy-price shocks.

Why Mordor's Germany Hyperscale Data Center Baseline Commands Reliability

Published estimates vary because firms mix scopes, assume different rack-fill trajectories, or leave announced MW undiscounted.

Our work confines the scope to true hyperscale footprints, indexes costs to localized EPC surveys, and updates annually, while many studies refresh less often or blend enterprise halls with cloud blocks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.78 B (2025) | Mordor Intelligence | |

| USD 2.59 B (2024) | Regional Consultancy A | Includes smaller enterprise and wholesale colocation revenue |

| USD 11.79 B (2023) | Trade Journal B | Uses announced capex without phasing or utilization adjustments |

| USD 8.17 B (2023) | Market Database C | Reports total data-center revenue, not filtered to >=20 MW sites |

Taken together, the comparison shows that once differing scopes and phasing assumptions are stripped away, our disciplined, annually refreshed model offers investors and policy planners a balanced, transparent baseline they can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the projected value of the Germany hyperscale data center market by 2031?

The market is forecast to reach USD 5,503.28 million by 2031, growing at a 20.68% CAGR.

Which region leads the market today, and which is growing fastest?

Frankfurt/Rhein-Main leads with 58% share, while Berlin/Brandenburg records the highest 14.0% CAGR through 2031.

Why are hyperscalers building their own German facilities instead of relying on colocation?

Self-builds allow hyperscalers to integrate liquid cooling, customised power paths and sovereign-cloud controls that shared halls cannot easily match, supporting AI and compliance workloads.

How will Germany’s Energy Efficiency Act affect data center operations?

It mandates 100% renewable sourcing by 2027 and escalating heat-reuse quotas, pushing operators toward renewable PPAs and heat-recovery systems.

What technologies are crucial for handling AI rack densities above 50 kW?

Direct-to-chip or immersion liquid cooling, 415 V three-phase distribution and fast-response UPS modules are essential for managing thermal and load spikes.

Are supply-chain constraints still a major hurdle for new builds?

Yes. Limited European GPU and optics capacity means lead times can exceed 12 months, delaying AI-focused expansions and impacting project timelines.

Page last updated on: