Vietnam Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

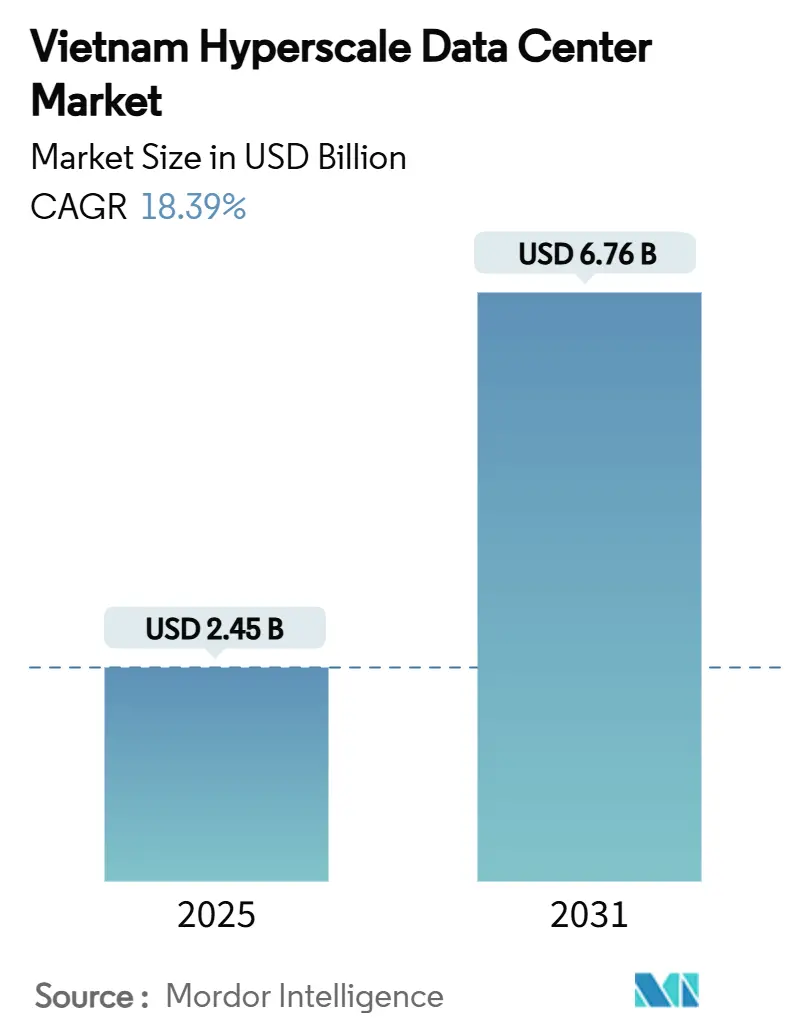

| Market Size (2025) | USD 2.45 Billion |

| Market Size (2031) | USD 6.76 Billion |

| Growth Rate (2025 - 2031) | 18.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Hyperscale Data Center Market Analysis by Mordor Intelligence

Vietnam hyperscale data center market size stands at USD 2.45 billion in 2025 and is forecast to climb to USD 6.76 billion by 2031, reflecting a 18.39% CAGR over 2025-2031. The market’s volume is set to expand from 477.64 MW in 2025 to 2,302.09 MW by 2031, underlining the pronounced infrastructure build-out required to meet surging digital demand. Government cloud-first mandates, 5G roll-outs, and record foreign direct investment combine to anchor Vietnam’s status as a rising regional hub. Local telecommunications majors dominate installed capacity but face fast-escalating competition from global hyperscalers now permitted 100% ownership. Infrastructure spending is skewing toward liquid-cooling technologies and renewable-backed power solutions as operators mitigate grid bottlenecks. Southern Vietnam retains the largest installed base thanks to superior subsea cable access, while Northern Vietnam offers the fastest growth on the back of policy proximity and early government adoption.

Key Report Takeaways

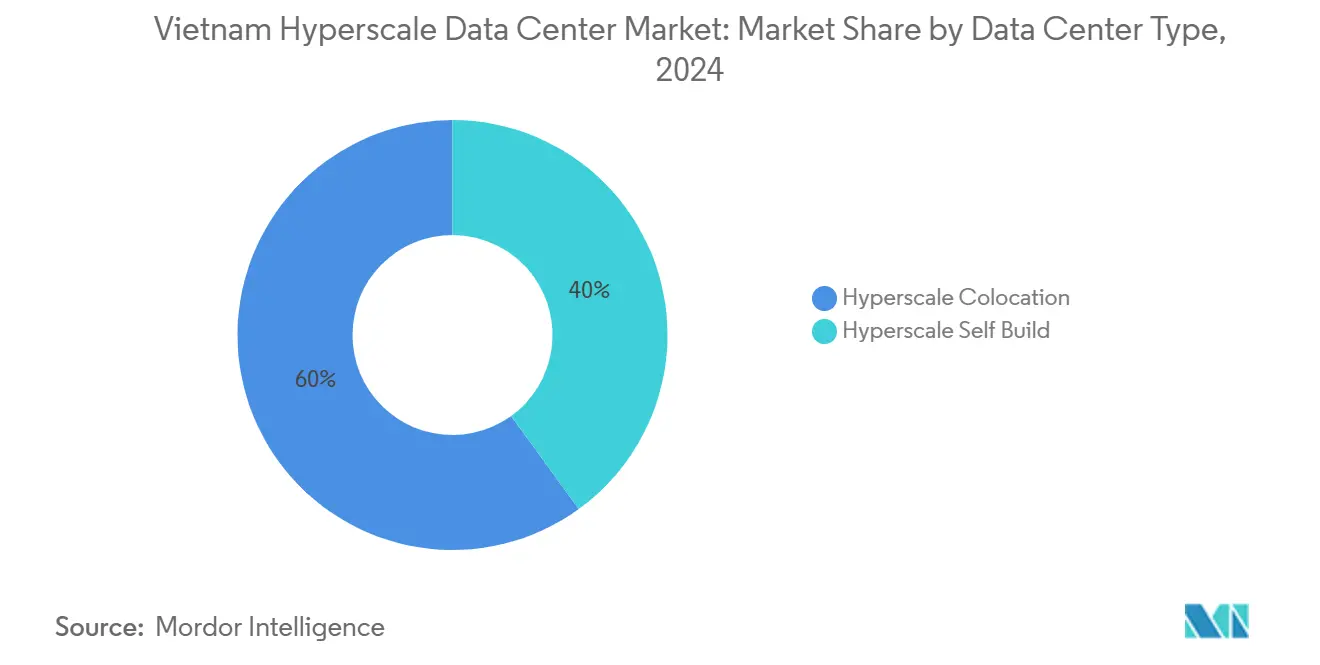

- By data center type, hyperscale colocation led with 60% revenue share in 2024; hyperscaler self-build facilities are projected to expand at 20.5% CAGR through 2030.

- By component, IT infrastructure accounted for a 43% share of the Vietnam hyperscale data center market size in 2024, and mechanical infrastructure is advancing at a 19.5% CAGR through 2030.

- By tier standard, Tier III facilities held 75% of the Vietnam hyperscale data center market share in 2024, whereas Tier IV is forecast to register a 20.1% CAGR to 2030.

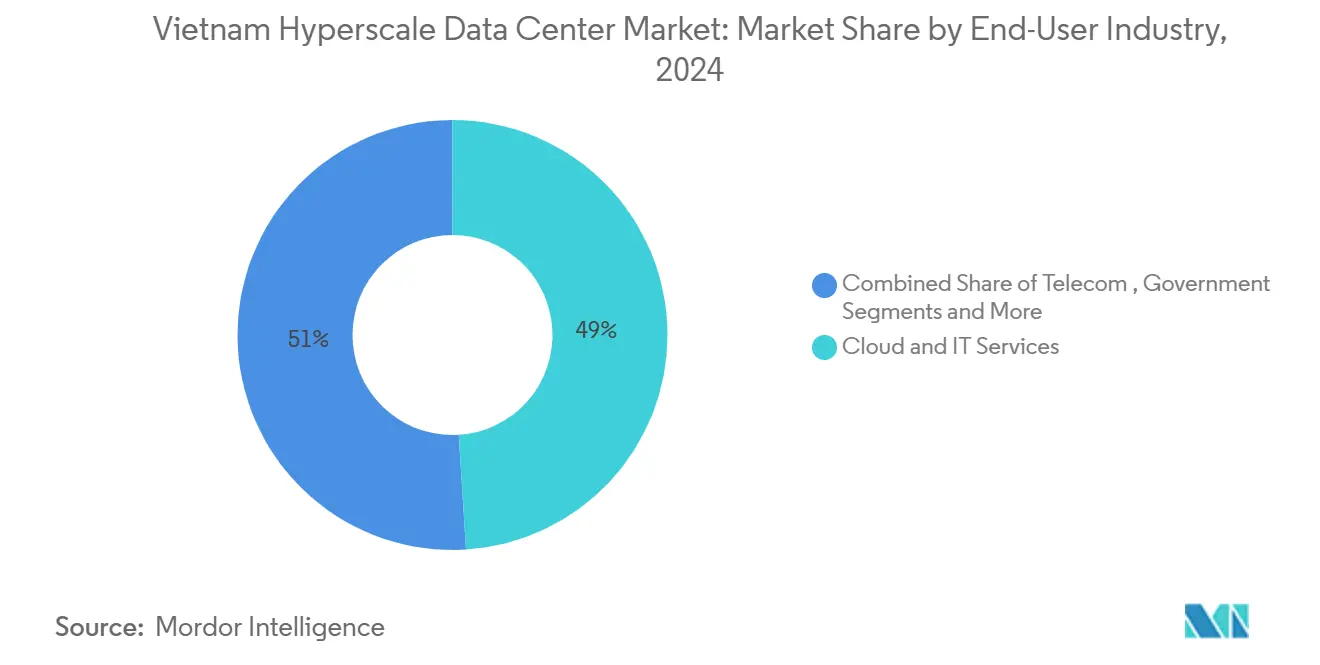

- By end-user industry, cloud and IT made up 49% of revenue in 2024, and BFSI is expected to grow at an 18.7% CAGR between 2025-2030.

- By data center size, large facilities (≤25 MW) captured a 53% share in 2024, while mega-scale (greater than 60 MW) deployments are on track for a 20.7% CAGR through 2030.

The conditions observed in Vietnam are shaped as much by international forces as by domestic ones. Mordor Intelligence’s hyperscale data center market research places those conditions within the broader global frame.

Vietnam Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis Table*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cloud-first mandates by Vietnamese enterprises and e-Government programs | 4.2% | National, with early gains in Hanoi, Ho Chi Minh City | Medium term (2-4 years) |

| E-commerce and fintech transaction surge demanding low-latency compute | 3.8% | Southern Vietnam, Ho Chi Minh City cluster dominance | Short term (≤ 2 years) |

| 5G roll-outs and edge–core consolidation accelerating core DC capacity | 3.1% | National, priority in industrial zones | Medium term (2-4 years) |

| FDI incentives and tax holidays for data-center investments | 2.9% | National, concentrated in high-tech zones | Long term (≥ 4 years) |

| Vietnam-Singapore cable redundancy enabling multi-AZ architectures | 2.2% | Southern Vietnam, international connectivity hubs | Medium term (2-4 years) |

| Spill-over of China AI-compute export controls driving GPU clusters to Vietnam | 1.7% | National, emphasis on Hanoi and Da Nang tech parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising cloud-first mandates by Vietnamese enterprises and e-Government programs

Vietnam’s National Digital Transformation Program requires every state agency to run on cloud by 2030, guaranteeing persistent demand for new hyperscale halls.[1]Bao Chinh Phu, “Chương trình hành động quốc gia phát triển và chuyển đổi sang sử dụng nền tảng điện toán đám mây,” baochinhphu.vn The Ministry of Public Security’s national data center, live since February 2025, anchors a single citizen database and sets performance benchmarks that domestic providers must emulate. VNPT’s “xa lộ số” backbone upgrade to 10 Gbps inter-DC links further underlines rising core traffic. By 2030, 70% of enterprises are expected to adopt domestic cloud, effectively locking hyperscale utilisation rates at high double digits.

E-commerce and fintech transaction surge demanding low-latency compute

Banking and payments workloads have become latency-sensitive as mobile commerce scales. VIB recorded 35% quicker product roll-outs and 23% cost savings after shifting to AWS. Techcombank’s LinuxONE migration boosted peak transaction capacity four-fold, illustrating why BFSI workloads gravitate toward hyperscale cores.[2]IBM, “Techcombank,” ibm.com Rising cardless payments and real-time settlement fuel dense server deployments in Ho Chi Minh City to guarantee sub-millisecond response.

5G roll-outs and edge–core consolidation accelerating core DC capacity

Viettel manufactures 80% of its own 5G gear, pushing massive edge footprints that back-haul traffic to national cores.[3]South China Morning Post, “Vietnam races to launch 5G network,” scmp.com Provinces lobbying for blanket 5G coverage amplify demand for regional zones that aggregate thousands of micro-cells. Edge-to-core architecture is shifting power density targets upward and reinforcing the need for ≥N+1 electrical designs.

FDI incentives and tax holidays for data-center investments

Revised investment rules now allow foreign investors to break ground before full licensing and grant tax holidays for up to 15 years. Land-use rights were extended to 70 years, and the 2024 telecommunications law abolished ownership caps, tilting the competitive field in favour of deep-pocketed hyperscalers.

Restraints Impact Analysis Table*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-grid congestion in key industrial zones | -3.4% | Northern Vietnam, industrial concentrations | Short term (≤ 2 years) |

| Lengthy land-acquisition and permitting cycles | -2.1% | National, acute in urban centers | Medium term (2-4 years) |

| Water-scarcity risks limiting evaporative cooling in Mekong Delta | -1.8% | Southern Vietnam, Mekong Delta regions | Long term (≥ 4 years) |

| Hyperscale-grade talent gap in operations engineering | -1.6% | National, concentrated in technical hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power-grid congestion in key industrial zones

Peak-hour shortages cost the economy USD 1.4 billion annually and force operators to oversize back-up diesel and battery systems. Only half of Vietnam’s 80,555 MW installed capacity is effectively dispatched because of grid constraints, and USD 128.3 billion must be invested by 2030 to modernise transmission. The resulting opex drag tempers near-term margin expansion.

Hyperscale-grade talent gap in operations engineering

Vietnam will require 500,000 technology workers by 2025 but still lacks deep data-center operations and cybersecurity skill sets. Enterprises now run in-house cloud-bootcamps with AWS and Cisco curricula, adding indirect costs that can elongate ramp-up schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Dominates Despite Self-Build Acceleration

Hyperscale colocation captured 60% of the Vietnam hyperscale data center market in 2024, mirroring a domestic preference for capital-light entry models. Self-build hyperscale projects, however, are forecast to post a 20.5% CAGR through 2030 as Google considers a USD 300-650 million site near Ho Chi Minh City and Viettel erects a 140 MW campus. The shift from multi-tenant footprints toward dedicated campuses signals a maturing customer base that values tighter control over security, network latency, and sustainability targets. Colocation providers are therefore scaling hall sizes, evidenced by SAM DigitalHub’s planned 150 MW Binh Duong complex, to retain hyperscale tenants who might otherwise migrate to proprietary builds. Over the forecast horizon, the Vietnam hyperscale data center market will increasingly feature hybrid structures where anchor cloud tenants dictate power densities and environmental parameters, blurring the traditional colocation-versus-self-build divide.

By Component: IT Infrastructure Leads While Mechanical Systems Surge

IT compute, storage, and networking hardware represented 43% of revenue in 2024 as operators raced to provision x86 and GPU clusters. Mechanical infrastructure is expected to grow the fastest at 19.5% CAGR as immersion and refrigerant-based liquid cooling cut PUE to sub-1.4 levels. Given Vietnam’s tropical humidity, chilled-water loops and rear-door heat exchangers are becoming standard, nudging the Vietnam hyperscale data center market size allocation toward mechanical line items. Electrical systems, from ring bus switch-gear to 2N UPS strings, continue to draw investment because grid instability necessitates oversizing. Intelligent DCIM layers are gaining traction as operators chase real-time visibility into temperature gradients and energy KPIs, setting the scene for predictive maintenance regimes.

By Tier Standard: Tier III Dominance with Tier IV Acceleration

Tier III made up 75% of capacity in 2024 because it balances reliability and capital cost. Tier IV footprints are predicted to expand at 20.1% CAGR as multinational cloud platforms impose strict ≥99.995% uptime contracts. Viettel’s 140 MW campus has already earned Tier III credentials with a target PUE below 1.4, while VNPT’s Hoa Lac site runs on N+1 electrical topologies. These templates are catalysing a market-wide shift where redundancy metrics become a marketing differentiator, propelling the Vietnam hyperscale data center market toward globally harmonised benchmarks.

By End-User Industry: Cloud Dominance with BFSI Surge

Cloud and IT workloads consumed 49% of installed capacity in 2024 on account of state-mandated migration. BFSI is forecast to log the quickest 18.7% CAGR, propelled by digital banking platforms, real-time payment rails, and reg-tech analytics that demand deterministic latency. Techcombank’s four-times throughput boost post LinuxONE adoption exemplifies how banking cores are re-platforming to hyperscale architecture. Manufacturing, telecom, and e-commerce workloads round out demand, ensuring the Vietnam hyperscale data center industry remains diversified across verticals.

By Data Center Size: Large Leads While Mega-Scale Emerges

Large sites (≤25 MW) held 53% share in 2024 but mega campuses (>60 MW) are on a 20.7% CAGR trajectory. Viettel’s 10,000-rack, 140 MW plant and SAM DigitalHub’s 150 MW blueprint exemplify a scaling logic that aims to land global AI workloads and reserve expansion parcels up front. The Vietnam hyperscale data center market size captured by mega assets is therefore projected to multiply, aligning domestic capacity profiles with mature hubs such as Singapore and Jakarta.

Geography Analysis

Southern Vietnam commands the largest slice of the Vietnam hyperscale data center market on the back of Ho Chi Minh City’s established carrier hotels and subsea cable knots. The new Asia Direct Cable’s 50 Tbps berth at Vũng Tàu cuts round-trip latency to major ASEAN peers, prompting hyperscalers to co-locate compute clusters near landing stations. Mega builds such as Viettel’s 140 MW campus and Google’s proposed 650 million-USD complex cement the region’s primacy for cross-border workloads. Demand is anchored by e-commerce, fintech, and export-oriented manufacturing firms that value proximity to financial exchanges and last-mile logistics nodes.

Northern Vietnam, centred on Hanoi, delivers the fastest growth rate as ministries mandate sovereign-cloud hosting. The Ministry of Public Security’s national data center underscores government commitment and signals to enterprises that latency advantages accrue to deployments in the capital corridor. VNPT’s 23,000 sqm Tier III hub in Hoa Lac, paired with Viettel’s 30 MW green site, illustrates how state-linked operators act as first movers. Private investors are following suit, seeking compliance certainty and closer oversight of cybersecurity protocols.

Central Vietnam’s Da Nang corridor emerges as a strategic alternative balancing seismic redundancy and land cost efficiency. A newly approved 1,881 hectare Free Trade Zone and 341 hectare IT Park attract FPT, CMC, and VNPT build plans. Connectivity is ensured by dual-route terrestrial fiber and 90 Tbps subsea capacity, positioning Da Nang as a disaster recovery node for national cloud platforms. Combined, these geographic dynamics guarantee that the Vietnam hyperscale data center market will not be constrained to a single urban wedge, safeguarding resilience and seat-of-government linkages.

The hyperscale data center market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as North America, Middle East, and Africa, along with detailed country-level analysis for China, Australia, Canada, Israel, South Africa, and Norway.

Competitive Landscape

Domestic telecommunications leaders Viettel, VNPT, and FPT still control around 97% of installed megawatts, but deregulation is redrawing the field. Full foreign ownership rights awarded in July 2024 opened the door for Google, Alibaba, and Meta, whose potential investments exceed USD 1 billion. Viettel is setting technology pace via AI-assisted cooling that pushes PUE below 1.4, while VNPT banks on government contracts and sovereign-cloud certifications. New-age colocation developers such as SAM DigitalHub prefer modular halls and immersion cooling to leapfrog legacy designs. The collision of domestic regulatory leverage with multinational scale economics is likely to trigger alliances rather than full-blown price wars—witness ST Telemedia’s tie-up with VNG on a 60 MW hybrid facility. Overall, the competitive fabric is moving from oligopolistic to contestable as capital barriers fall and technology standardisation accelerates.

Vietnam Hyperscale Data Center Industry Leaders

Viettel IDC

FPT Telecom International

VNPT Net Corporation

CMC Telecom

Amazon Web Services (AWS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CMC wins approval for a USD 250 million hyperscale data center, reinforcing private-sector confidence in Vietnam’s digital infrastructure trajectory.

- June 2025: Government ratifies national cloud action plan mandating 100% agency adoption by 2030.

- June 2025: Da Nang Free Trade Zone was officially established, offering tax holidays for data-center operators.

- May 2025: Meta unveils AI investment programme including Vietnamese language models.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Vietnam's hyperscale data center market as all newly commissioned or fully built facilities in the country that provide >=4 MW of contiguous IT load for cloud, AI, and large-scale content workloads. The model captures capital value and operating revenue streams linked to hyperscale self-build as well as wholesale colocation halls rated Tier III or higher.

Edge pods below 4 MW, enterprise on-premise rooms, and pure shell and core construction contracts are not counted.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-Build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- PDUs

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning

- Design Engineering

- Fire, Security and Safety Systems

- DCIM / BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End Users

- By Data Center Size

- Large ( Less than or equal to 25 MW)

- Massive (Greater than 25 MW and Less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

Multiple conversations were held with data center planners, power engineers, real estate advisers, and cloud capacity managers in Ho Chi Minh City, Hanoi, and Singapore. These exchanges clarified build timeline slippages, average rack power envelopes, and likely take-up rates by hyperscalers, which helped us adjust utilization curves and pricing spreads.

Desk Research

Mordor analysts first mapped the universe using open statistics from Vietnam's Ministry of Information and Communications, national power utility EVN, customs shipment records, and trade association reports such as the Vietnam Internet Association. We also screened English and Vietnamese press carried on Dow Jones Factiva for project start dates, rack densities, and land costs. Capacity benchmarks were validated with Uptime Institute certifications, APNIC IPv6 traffic data, and project filings available through the Planning and Investment Ministry. Paid intelligence from D&B Hoovers supplied financials for key developers. The sources mentioned illustrate the evidence base and are not exhaustive.

Market-Sizing and Forecasting

Mordor's model begins with a top down reconstruction of installed IT load using official power connection approvals, subsea cable landings, and declared foreign direct investment. Results are cross checked through selective bottom up roll ups of announced megawatt blocks and sampled average selling price per kW. Key drivers, foreign ownership liberalization, subsea cable redundancy, average PUE progress, rack power densification, land lease cost, and fiber backhaul growth, feed a multivariate regression that projects value and capacity to 2031. Gaps in individual site data are bridged by peer averages and then re validated through channel checks.

Data Validation and Update Cycle

All interim outputs undergo variance checks against historical energy sales and import statistics. An internal reviewer signs off after anomalies are resolved, and reports are refreshed annually, with ad hoc updates when material policy or project announcements emerge.

Why Our Vietnam Hyperscale Data Center Baseline Earns Trust

Published estimates often diverge because firms pick different inclusion rules, adjust currencies on separate dates, or roll capacity into construction spending.

Key gap drivers include some studies that treat only capital expenditure while Mordor reports economic value in use; others fold enterprise and edge rooms into totals; a few apply a uniform utilization factor that ignores Vietnam's rapid rack density shift and preferential tax incentives that compress payback periods.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.45 B (2025) | Mordor Intelligence | - |

| USD 654 M (2024) | Regional Consultancy A | Tracks investment outlays, excludes recurring revenue |

| USD 2.20 B (2025) | Trade Journal B | Reports total data center revenue, not hyperscale only, and mixes edge nodes |

| USD 1.20 B (2023) | Industry Portal C | Uses historical spend, applies flat 15 % CAGR without project level adjustments |

These comparisons show that when scope alignment, utilization realism, and dual modeling are applied, Mordor Intelligence delivers a balanced baseline that decision makers can trace to transparent variables and reproducible steps.

Key Questions Answered in the Report

What is the current size of the Vietnam hyperscale data center market?

The Vietnam hyperscale data center market size is USD 2.45 billion in 2025 and is projected to reach USD 6.76 billion by 2031.

Which region hosts the most hyperscale capacity in Vietnam?

Southern Vietnam, led by Ho Chi Minh City and Bà Rịa-Vũng Tàu clusters, holds the largest installed capacity due to superior subsea cable connectivity.

What segment is growing the fastest by tier standard?

Tier IV facilities, driven by global uptime requirements, are forecast to grow at a 20.1% CAGR through 2030.

How are power-grid constraints being mitigated?

Operators are investing in 2N electrical topologies, on-site renewables, and liquid-cooling to counteract grid congestion that currently costs Vietnam USD 1.4 billion each year.

Which end-user segment is growing fastest?

BFSI workloads are advancing at a 25% CAGR between 2025-2030 as banks and fintechs migrate to cloud-enabled platforms that require in-country hyperscale hosting.

What ownership rules apply to foreign hyperscalers?

Since July 2024, foreign investors can own 100% of Vietnamese data center entities, eliminating earlier minority-stake restrictions and spurring billion-dollar project pipelines.

Page last updated on: