France Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

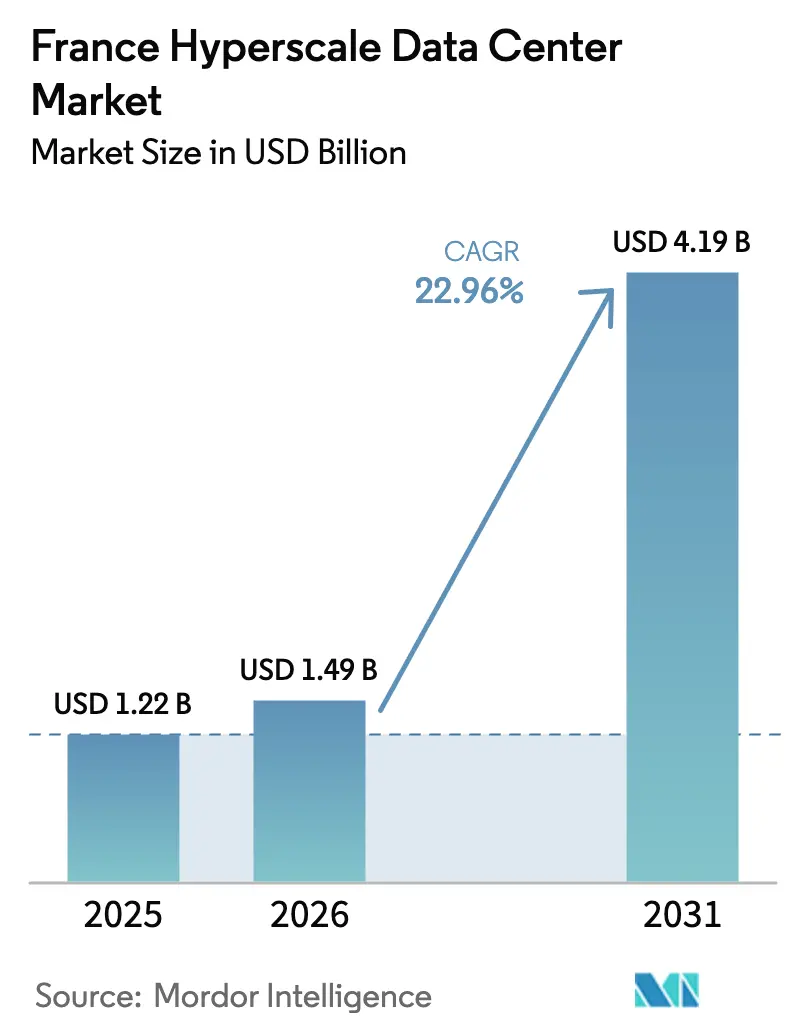

| Base Year Market Size (2025) | USD 1.22 Billion |

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 22.96% CAGR |

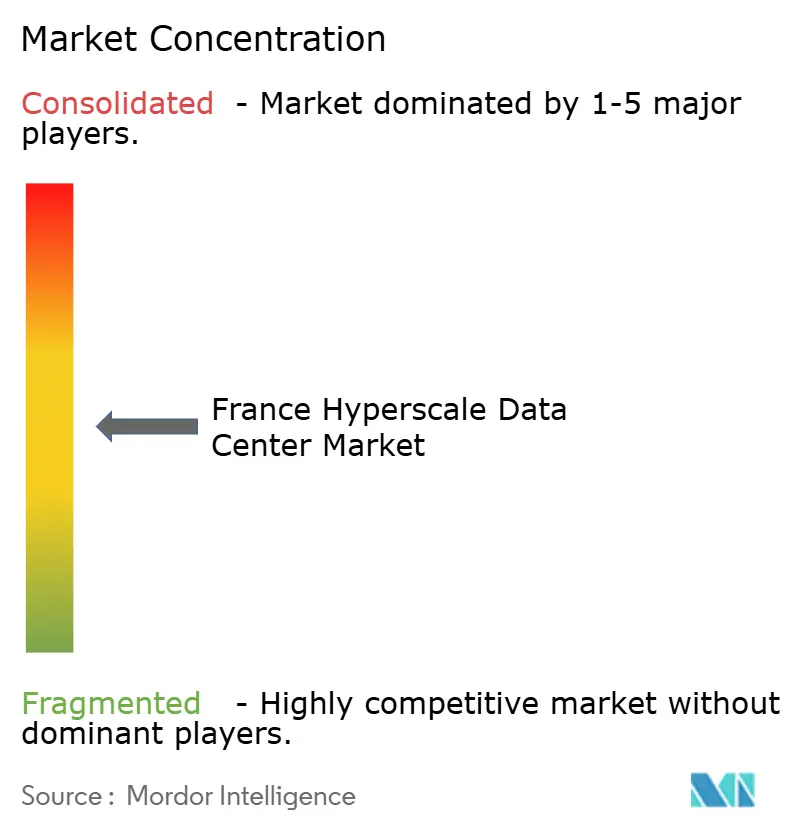

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Hyperscale Data Center Market Analysis by Mordor Intelligence

The France hyperscale data center market size is expected to increase from USD 1.22 billion in 2025 to USD 1.49 billion in 2026 and reach USD 4.19 billion by 2031, growing at a CAGR of 22.96% over 2026-2031. The France hyperscale data center market is being propelled by three structural pivots: the siting of NVIDIA’s 1.4 GW Paris campus, the French government’s program to add six EPR2 nuclear reactors, and the European Sovereign Cloud framework that funnels U.S. and Chinese cloud tenants toward in-country capacity. Operators are capitalizing on France’s nuclear-based power mix to host GPU-dense clusters that satisfy low-carbon procurement rules while meeting data-residency mandates. Rapid uptake of liquid-cooling retrofits, the ability to secure long-duration nuclear or offshore-wind power-purchase agreements, and edge-to-core consolidation along the Paris-Marseille fiber corridor together shorten commissioning cycles and lower unit operating costs for the France hyperscale data center market. As hyperscalers replicate sovereign-cloud footprints across EU member states, they must now duplicate availability zones inside France, which inflates regional capex but lifts national installed capacity.

Key Report Takeaways

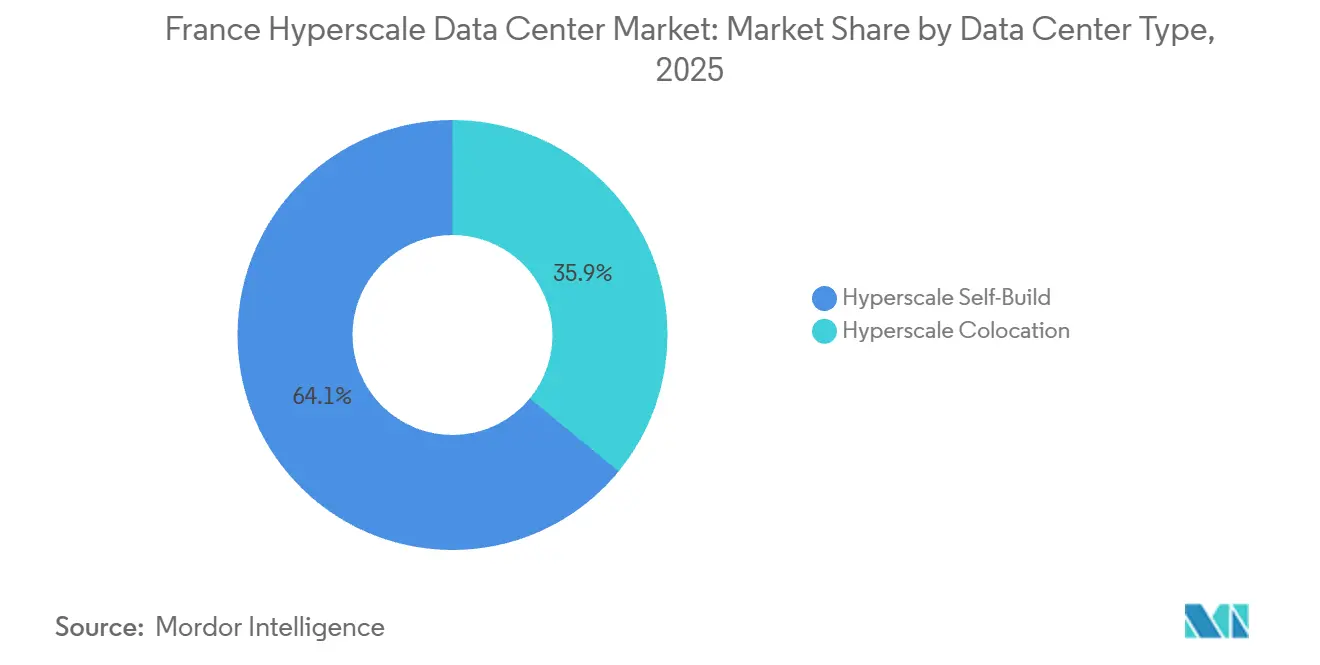

- By data center type, self-build deployments held 64.06% of the France hyperscale data center market share in 2025, while hyperscale colocation is projected to clock the highest 23.43% CAGR through 2031.

- By component, IT infrastructure captured 45.18% of the France hyperscale data center market size in 2025, whereas mechanical infrastructure is forecast to post the fastest 23.83% CAGR on accelerating liquid-cooling retrofits.

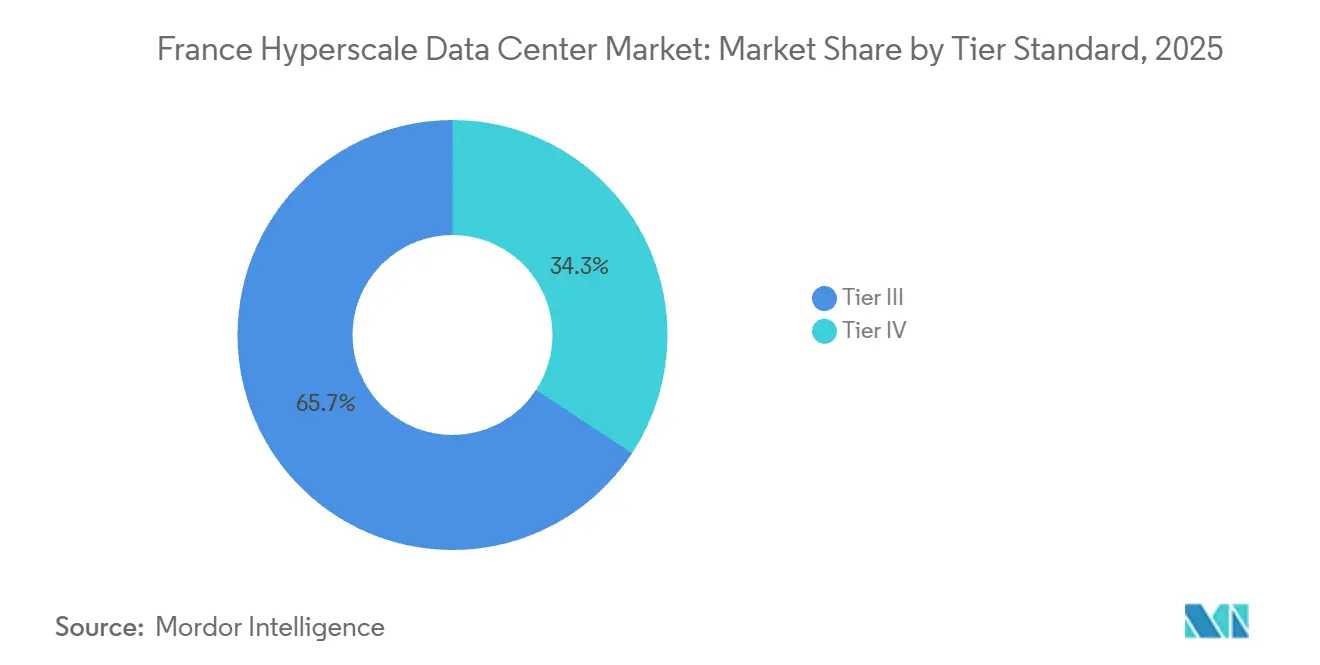

- By tier standard, Tier III sites accounted for 65.73% of share in 2025, yet Tier IV facilities are expected to expand at a 23.56% CAGR as real-time payments and GenAI inference eliminate downtime tolerance.

- By data center size, campuses ranging from 25 MW to 60 MW represented 43.42% of share in 2025, but mega-scale sites above 60 MW are anticipated to grow at a leading 23.68% CAGR as hyperscalers consolidate regional hubs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

National developments in France connect differently with activity unfolding across other parts of the world. In the global hyperscale data center market coverage, Mordor Intelligence integrates these into a single analytical framework.

France Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding GPU-Centric AI/ML Workloads from US and China Cloud Tenants | +6.8% | National, concentrated in Paris and Marseille metro areas | Short term (≤ 2 years) |

| Sovereign-Cloud Roll-Outs by Hyperscalers In Europe | +5.2% | National, with spillover to broader EU compliance zones | Medium term (2-4 years) |

| Real-Time Payment Mandates Boosting Tier IV Builds in Paris | +3.1% | Paris metro, with secondary impact in Lyon and Marseille | Medium term (2-4 years) |

| 5G Edge-Core Consolidation Along Paris-Marseille Fiber Corridors | +2.9% | Paris-Marseille corridor, extending to Toulouse and Bordeaux | Long term (≥ 4 years) |

| GenAI Inference Build-Outs Demanding Liquid-Cooling Campuses | +4.6% | National, with early adoption in Paris and Normandy | Short term (≤ 2 years) |

| Renewable PPAs Tied to New EPR2 and Offshore-Wind Projects | +3.7% | National, with concentration in Normandy and Brittany coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding GPU-Centric AI/ML Workloads from U.S. and China Cloud Tenants

French campuses are absorbing GPU-dense inference clusters that overseas hyperscalers cannot deploy domestically amid power-grid constraints. NVIDIA’s 1.4 GW Paris site will house more than 100,000 Blackwell GPUs configured in liquid-cooled designs, making it the largest single-location AI deployment in Europe. A similar 1 GW campus being built in northern France targets Chinese AI labs that require EU data residency. As a result, average rack loads climbed from 8 kW in 2024 to 22 kW in 2025, and operators now specify 40-60 kW cabinets as standard. France’s dense network of nuclear plants, permissive AI regulation, and proximity to multiple subsea cables collectively place the France hyperscale data center market at the center of Europe’s GPU supply chain.

Sovereign-Cloud Roll-Outs by Hyperscalers in Europe

AWS launched a physically and logically isolated European Sovereign Cloud in January 2026 to ensure that customer data remain exclusively inside the EU and that only EU-resident staff have administrative access. Microsoft added three availability zones in Paris and Marseille in April 2025 to expand its sovereign footprint. Domestic challenger Scaleway obtained SecNumCloud certification in December 2025, allowing French government workloads to reside on its DGX Cloud Lepton platform. These parallel deployments force leading hyperscalers to duplicate infrastructure in multiple member states rather than consolidating in a single low-cost hub, thereby accelerating the France hyperscale data center market while lifting per-unit costs.

5G Edge-Core Consolidation Along Paris-Marseille Fiber Corridors

Mobile operators are collapsing distributed edge sites into higher-capacity cores. Exa Infrastructure added 400 Gbps wavelengths along the Paris-Marseille route in 2025, and Infinera supplied 800 Gbps coherent optics to Orange, enabling mobile backhaul aggregation at fewer handoff points. The Medusa submarine cable, which landed in Marseille in 2025, offers direct connectivity to Egypt, Saudi Arabia, and India. This reconfiguration reinforces the Paris-Marseille axis as the region’s primary Southeast-Europe traffic gateway and positions the France hyperscale data center market to shoulder expanding low-latency transport demand.

Renewable PPAs Tied to New EPR2 and Offshore-Wind Projects

France’s PPE3 program will add six EPR2 reactors, unlocking roughly 9.9 GW of new baseload capacity by 2030. Data4 signed a 40 MW, 12-year nuclear PPA at EUR 50 per megawatt-hour in September 2025, half the winter spot rate.[1]Data4 Group, “Escaudain Campus Overview,” data4group.com RTE is also reserving grid headroom for datacenter off-take in coastal Normandy and Brittany where 18 GW of offshore wind will come online by 2035. Long-duration PPAs hedge electricity volatility and are fast becoming a procurement prerequisite for hyperscalers entering the France hyperscale data center market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-Usage Restrictions on Evaporative Cooling | -2.8% | National, with acute enforcement in Île-de-France and Provence-Alpes-Côte d'Azur | Short term (≤ 2 years) |

| GPU And Optic Supply-Chain Bottlenecks | -3.4% | Global, with localized impact on French campus commissioning timelines | Medium term (2-4 years) |

| Rising Heat-Tax and Carbon Levies | -1.9% | National, with higher rates in urban zones subject to air-quality mandates | Medium term (2-4 years) |

| Local-Grid Curtailment Rules Capping Draw More Than 30 MW | -2.1% | Regional, concentrated in Paris metro and Lyon where grid headroom is constrained | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Water-Usage Restrictions on Evaporative Cooling

In 2025, prefectures in Île-de-France capped evaporative-cooling consumption at 0.4 liters per kilowatt-hour, pushing new builds toward closed-loop or dry-cooler designs that cost 30-40% more upfront.[2]ADEME, “Cooling Water Restrictions in Datacenters,” ademe.fr OVHcloud demonstrated a water usage effectiveness of 0.3 liters per kilowatt-hour in 2024 by employing adiabatic towers fed by rainwater. While the benchmark proves compliance is possible, land-use and capex barriers lengthen project timelines and reduce near-term additions to the France hyperscale data center market.

GPU and Optic Supply-Chain Bottlenecks

Lead times for NVIDIA H100 series GPUs stretched to 9-12 months in 2025, and 800 Gbps optical transceivers moved into chronic shortage as global AI clusters competed for components. French campuses consequently face commissioning delays of 6-9 months, which suppresses realized capacity growth during the 2026-2028 window. Sovereign-cloud operators with smaller procurement volumes suffer the greatest setback, widening the competitive gap inside the France hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Paris and Marseille together hosted roughly 60% of installed hyperscale capacity in 2025, leveraging dense subsea cable landings and the presence of major internet exchanges. The Medusa cable’s 2025 landing in Marseille brings direct optical paths to the Middle East and South Asia, reinforcing Marseille’s status as Europe’s southern gateway. Exa Infrastructure’s addition of 400 Gbps wavelengths along the axis shrinks latency for mobile backhaul and high-frequency trading traffic.

Normandy and Brittany have emerged as preferred alternatives for greenfield development, buoyed by offshore-wind pipelines and pre-reserved grid capacity. Thesee DataCenter’s EUR 60 million 50 MW expansion in Normandy taps this advantage, while Scaleway’s planned 300 MW Montereau campus secures proximity to nuclear-powered baseload. The shift decentralizes capacity out of Paris, but added round-trip propagation of 5-10 milliseconds to the capital limits the relocation of latency-sensitive banking and gaming workloads.

Île-de-France now enforces stricter water-usage caps and grid-curtailment rules, prioritizing projects committing to over 400 MW draw and sidelining smaller entrants. Consequently, the France hyperscale data center market has developed a two-tier structure. Paris-Marseille hubs are priced at a premium for sub-10 millisecond latency, while coastal or eastern sites are optimized for energy-intensive AI training, prioritizing Renewable PPA access over proximity.

Mordor Intelligence's coverage of the hyperscale data center market extends across other regions including Europe, Africa, and South America, while country-specific intelligence is also available for Sweden, Poland, South Africa, Chile, Australia, and Taiwan, each offering a view on the jurisdiction-level dynamics as applicable.

Segment Analysis

By Data Center Type: Colocation Gains as Speed Trumps Ownership

Hyperscale self-build captured 64.06% of the France hyperscale data center market share in 2025, underscoring the weight that AWS, Microsoft, and Google place on architectural control. Yet colocation is forecast to expand at a 23.43% CAGR, outpacing the overall France hyperscale data center market by 47 basis points. Data4’s EUR 5 billion Escaudain campus delivers turnkey shells that shrink commissioning cycles from 36 months to under 18. Vantage Data Centers and Altarea are investing EUR 400 million in a 400 MW Bordeaux campus tailored to sovereign-cloud tenants constrained by balance-sheet limits.[3]Vantage Data Centers, “Bordeaux Campus Fact Sheet,” vantage-dc.com

Self-build will remain the method of choice for workloads that demand deterministic performance across global availability zones. AWS’s sovereign-cloud regions employ identical rack layouts from Paris to Milan, a standardization not guaranteed in multi-tenant shells. As a result, the France hyperscale data center market is bifurcating; U.S. hyperscalers extend self-builds for latency-critical zones, while mid-tier and sovereign providers gravitate to colocation that prioritizes speed-to-market over full asset control.

By Component: Mechanical Spend Surges on Liquid-Cooling Retrofits

IT hardware accounted for 45.18% of the share in 2025. Mechanical systems are on track to post the fastest growth, with a 23.83% CAGR, as liquid cooling has become mandatory for racks exceeding 40 kW. France’s DDADUE law obliges new builds above 500 kW to recover waste heat, driving demand for heat exchangers and district-heating tie-ins that add 15-20% to baseline construction cost.

Electrical gear such as UPS and switchgear scales with total megawatts but benefits from modularization, keeping its growth near the headline France hyperscale data center market rate. Network and storage equipment see slower growth as hyperscalers increase server densities and shift to NVMe flash. The result is that mechanical capex now represents the primary bottleneck, absorbing an estimated 30% of total additions to the French hyperscale data center market through 2027.

By Tier Standard: Tier IV Builds Accelerate for Mission-Critical Workloads

Tier III sites constituted 65.73% of share in 2025, a legacy of banking and telecom workloads able to tolerate planned outages. Tier IV facilities are forecast to rise at a 23.56% CAGR as instant payment rails and GenAI inference clusters eliminate downtime tolerance. The European Central Bank’s TARGET settlement system requires Tier IV infrastructure for member banks, compelling French institutions to migrate from Tier III colocation.

Tier III will remain relevant for content delivery, batch analytics, and development sandboxes, particularly in regional metros where cost sensitivity is significant. In contrast, Tier IV builds in Paris now command a premium, justified by revenue-at-risk calculations. This ensures a steady pipeline, boosting the France hyperscale data center market size for ultra-resilient campuses.

By Data Center Size: Mega-Scale Campuses Consolidate Regional Hubs

Campuses rated between 25 MW and 60 MW owned 43.42% of the share in 2025, striking a balance between risk and scale economies. Yet sites above 60 MW are expected to grow at a 23.68% CAGR, as hyperscalers consolidate traffic into a handful of regional hubs. Data4’s 500 MW Escaudain project reduces per-megawatt build cost by up to 25% versus distributed builds thanks to on-site substations and dedicated fiber routes.

Smaller facilities below 25 MW continue to serve edge caching and enterprise colocation. However, they face challenges such as limited grid headroom and longer permitting timelines. As a result, the France hyperscale data center market is consolidating into mega-hubs for sovereign-cloud regions and massive-scale campuses for colocation tenants, leaving small-scale developers to focus on niche workloads or exit the market.

Competitive Landscape

The France hyperscale data center market is fragmented, with no single operator exceeding 15% share. Data4 leads domestic players, with EUR 15 billion in projects and a pioneering 40 MW nuclear PPA that locks power pricing at EUR 50 per MWh. OVHcloud operates 45 datacenters featuring a 1.29 power usage effectiveness and a record low water usage effectiveness of 0.3 liters per kilowatt-hour, setting a sustainability bar competitors must meet. Equinix maintains 11 French facilities linked to its global interconnection fabric, yet faces margin pressure as hyperscalers shift traffic onto private backbones.

Scaleway, having secured SecNumCloud certification, markets itself as the sovereign alternative for state buyers and is negotiating a 300 MW build with EDF. Thesee DataCenter’s Normandy expansion taps offshore wind curves to woo AI tenants seeking fixed-price green energy. Vantage Data Centers teams with property developer Altarea on a 400 MW Bordeaux campus designed for turnkey hyperscale shells. Technology differentiation centers on liquid-cooling density and AI-driven datacenter-infrastructure management; one northern-France campus reports 85% of racks using direct-to-chip cold plates at densities exceeding 120 kW. Competitive advantage is therefore rotating from mere scale to regulatory compliance and guaranteed low-carbon power.

Domestic providers are increasingly leveraging regulatory certifications, power-purchase agreements, and advanced cooling technologies to differentiate in a field where pure scale no longer guarantees advantage. Scaleway’s SecNumCloud accreditation positions it as the go-to sovereign option for public-sector workloads that must remain under French jurisdiction, while Thesee DataCenter’s Normandy campus targets latency-sensitive AI inference clusters just outside the congested Paris grid. Liquid-cooling champions such as Verne Global and Nscale are partnering with municipalities to channel waste heat into district networks, thereby reducing local carbon levies and strengthening community relations. Meanwhile, mid-tier operators that lack access to long-duration nuclear PPAs face widening cost gaps during winter spot-price spikes, prompting a wave of consolidation talks reported in early 2026 among operators controlling sub-5% market shares. The strategic outlook suggests that successful players will marry secure data-sovereignty architectures with fixed-price low-carbon energy, leaving asset-light resellers and legacy air-cooled facilities increasingly marginalized.

France Hyperscale Data Center Industry Leaders

Amazon Web Services (AWS)

Microsoft Corporation (Azure)

OVHcloud

Meta Platforms, Inc.

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Vantage Data Centers and Altarea confirmed a EUR 400 million partnership to build a 400 MW campus in Bordeaux, designed around modular blocks that commission in under 18 months.

- January 2026: Data4 unveiled a EUR 5 billion Escaudain campus that will deliver 500 MW across eight buildings, marking France’s largest single-site deployment.

- January 2026: AWS launched its European Sovereign Cloud, storing all customer data exclusively within EU borders and staffing operations solely with EU residents.

- January 2026: OVHcloud partnered with OpenNebula to supply open-source sovereign-cloud stacks for European public-sector clients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the France hyperscale data center market as every new or expanded facility on French soil engineered for single-tenant or multi-tenant halls that together host at least 5,000 servers and draw an aggregated IT load above 20 MW, enabling cloud, social media, AI/ML, and high-growth platform workloads.

Scope Exclusions: Micro-edge sites below 5 MW, legacy enterprise server rooms, carrier hotels devoted solely to network interconnect, and any facility outside metropolitan France are excluded.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-Build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Units

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning Services

- Design Engineering

- Fire Detection, Suppression and Physical Security

- DCIM/BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By Data Center Size

- Large ( Less than or equal to 25 MW)

- Massive (Greater than 25 MW and Less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured calls with facility design engineers, power-purchase brokers, and operations heads at hyperscale self-builds and Paris-area colocations, supplemented by short surveys of GPU integrators in Lyon and HVAC specialists in Marseille. The conversations validated price-per-MW assumptions, commissioning delays, and sustainable-cooling adoption timelines that secondary sources only hinted at.

Desk Research

We began with publicly available datasets from CRE (energy mix and tariffs), ARCEP (fiber backbone and 5G roll-out), INSEE (enterprise cloud adoption), Eurostat (cross-border power flows), and the French Ministry of Ecological Transition (building permits and water guidelines). Trade associations such as France Datacenter and the European Cloud Alliance provided project trackers, while Uptime Institute papers clarified Tier conversion costs. To size supplier revenue trails, we tapped D&B Hoovers and Dow Jones Factiva for company filings and tender wins. These sources illustrate, rather than exhaust, the secondary evidence pool that fed our baseline.

Market-Sizing & Forecasting

A top-down model converts national data-center electricity demand into hyperscale value by isolating facilities above 20 MW, applying capacity-utilization curves, then multiplying by blended average service pricing. Select bottom-up checks, supplier roll-ups, sample rack counts, and ASP × volume spot checks fine-tune totals. Key variables tracked include megawatt additions cleared by grid operators, average GPU density per rack, sovereign-cloud contract volumes, liquid-cooling penetration, and EUR/kWh trajectories. Forecasts rely on a multivariate regression against those drivers, with scenario bounds cross-verified by interview insights. Gaps in site counts are bridged using building-permit lags and Volza shipment logs.

Data Validation & Update Cycle

Outputs pass a three-layer review: peer analyst audit, senior consultant sign-off, and automated variance flags against external capacity trackers. Models refresh annually, with mid-cycle revisions triggered by >=50 MW announcements or price shocks. A last-mile check is run before client delivery, so numbers always reflect the latest reality.

Why Mordor's France Hyperscale Data Center Baseline Stands Firm

Published figures often differ because firms widen the scope to include edge halls, quote build-cost rather than service revenue, or freeze exchange rates months in advance. Our disciplined focus on in-service IT load, current-year pricing, and yearly refresh cadence keeps our baseline anchored, even when others oscillate on definition or update rhythm.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 1.22 B (2025) | Mordor Intelligence | - |

| 5.80 B (2024) | Regional Consultancy A | Includes smaller edge sites and on-premise upgrades; uses announced capex rather than operational revenue |

| 1.88 B (2023) | Trade Journal B | Tracks hyperscale computing hardware spend, not data-center services; earlier base year and global ASP assumption |

The comparison shows that once scope creep and metric mismatches are stripped away, Mordor offers a balanced middle ground, grounded in verifiable operational data, refreshed annually, and backed by transparent assumptions clients can retrace with ease.

Key Questions Answered in the Report

What is the projected value of the France hyperscale data center market in 2031?

The market is forecast to reach USD 4.19 billion by 2031.

How fast is the France hyperscale data center market expected to grow?

It is projected to expand at a 22.96% CAGR between 2026 and 2031.

Which deployment model is growing fastest inside France?

Hyperscale colocation is advancing at a 23.43% CAGR through 2031, making it the quickest-growing segment.

Why are liquid-cooling investments rising so sharply?

GenAI inference racks exceed 40 kW per cabinet, and French regulations mandate waste-heat recovery, both of which require liquid-cooling systems.

How do nuclear PPAs influence datacenter site selection?

Long-duration nuclear PPAs fix electricity prices at levels well below winter spot peaks, giving campuses near EPR2 reactors a decisive cost edge.

Which regions outside Paris are drawing significant hyperscale builds?

Normandy and Brittany attract projects thanks to offshore-wind pipelines and pre-reserved grid capacity.

Page last updated on: