Canada Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.32 Billion |

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Heat Pump Market Analysis by Mordor Intelligence

The Canada heat pump market size is projected to be USD 2.32 billion in 2025, USD 2.44 billion in 2026, and reach USD 3.06 billion by 2031, growing at a CAGR of 4.63% from 2026 to 2031. Mounting federal and provincial decarbonization mandates are steering builders toward low-carbon electricity, making heat pumps the straightforward compliance option in new construction. More than 280,000 units have already been installed under national incentive programs, and Atlantic Canada now records penetration rates approaching one in three households. Technological advances keep full-capacity heating available down to −28 °C, easing long-standing performance concerns in prairie and northern climates. At the same time, hybrid configurations that blend electric heat pumps with gas furnaces are gaining favor among homeowners who want backup heat without breaching grid-capacity limits, especially in high-load provinces.

Key Report Takeaways

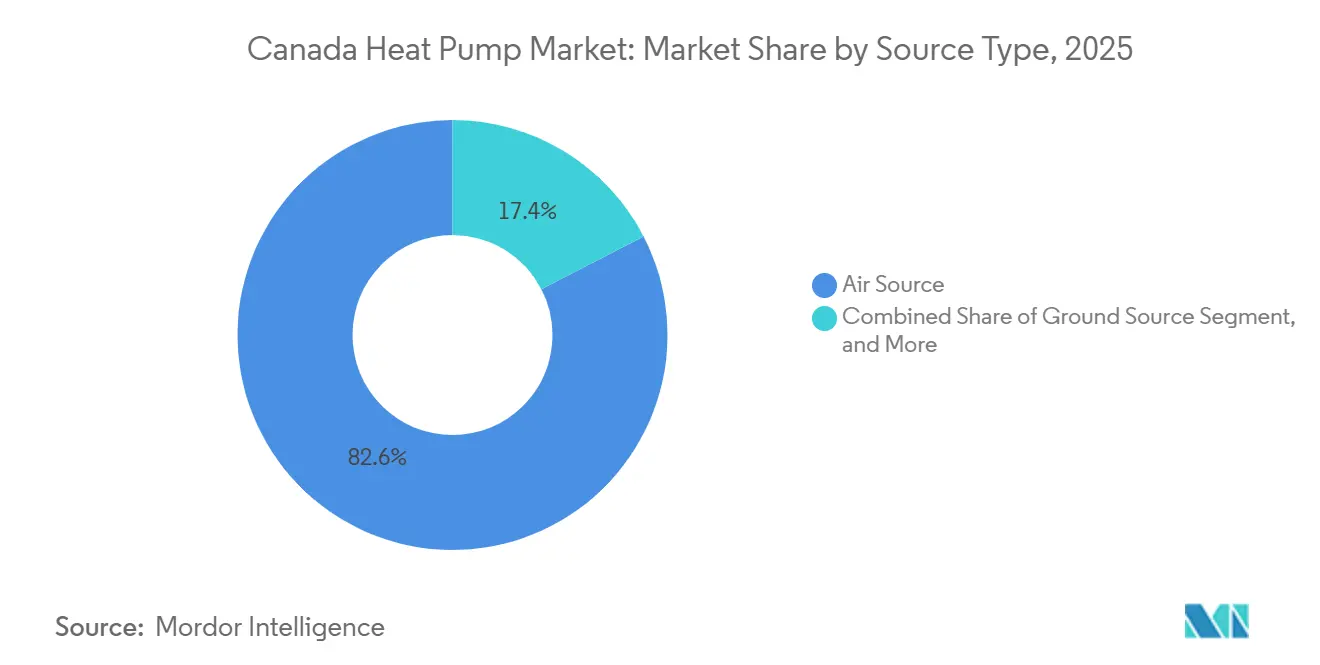

- By source type, air source systems led with 82.58% revenue share in 2025, while hybrid configurations are forecast to expand at a 5.17% CAGR through 2031.

- By technology, air-to-air solutions accounted for 58.12% of the Canada heat pump market share in 2025, whereas air-to-water systems are on track to grow at a 5.02% CAGR to 2031.

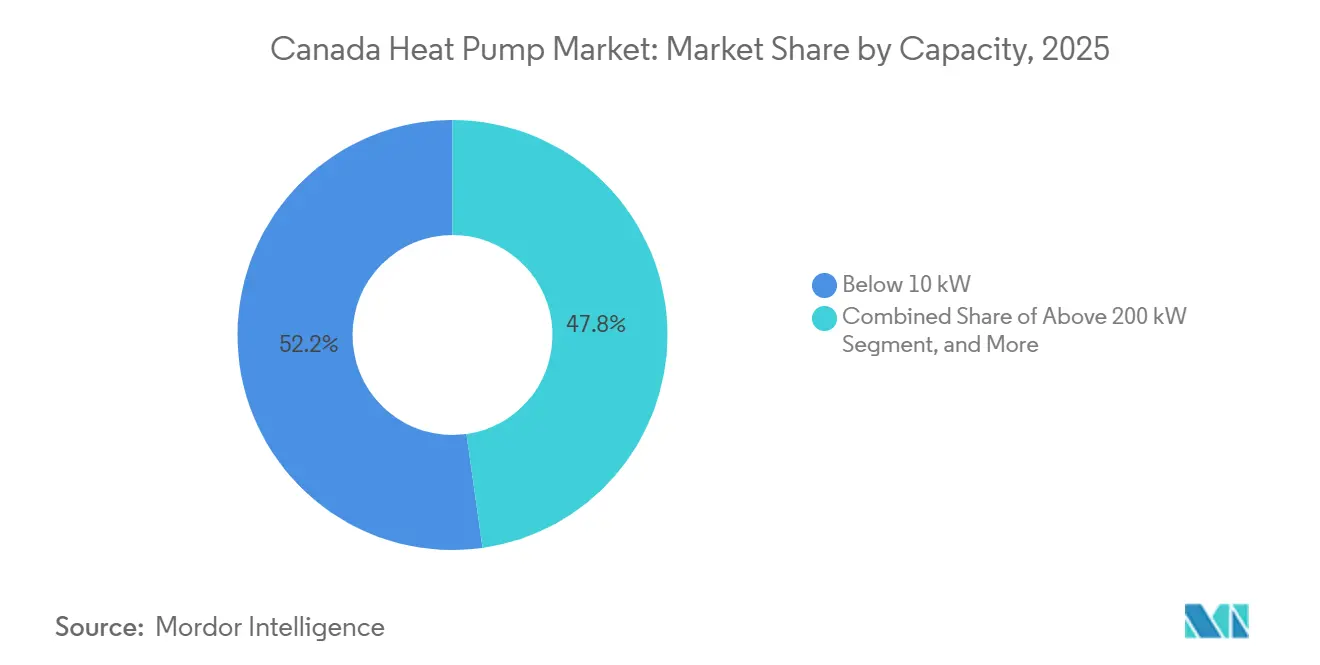

- By capacity, units below 10 kW captured 52.23% of the Canada heat pump market size in 2025, yet the mid-range 50-200 kW band is advancing at a 4.84% CAGR over 2026-2031.

- By application, space heating commanded 46.07% share in 2025 and domestic hot water is progressing at a 4.87% CAGR toward 2031.

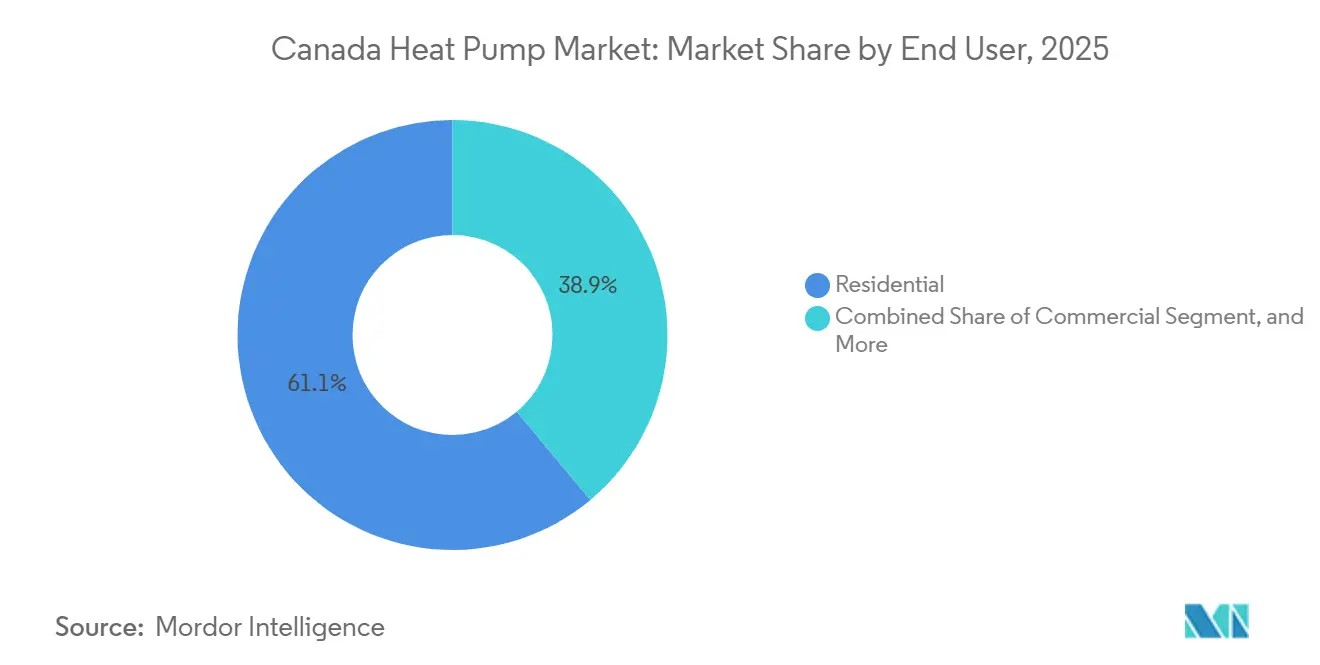

- By end user, the residential segment held 61.09% share in 2025, whereas commercial installations are forecast to rise at a 4.78% CAGR to 2031.

- By installation, retrofit activity covered 67.83% of 2025 deployments, and new-build installations are forecast at a 5.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives and Decarbonization Mandates | +1.2% | National, Highest in Atlantic Canada, British Columbia, Ontario, Quebec | Medium Term (2–4 Years) |

| Rising Energy Prices Driving Cost-Savings Adoption | +0.9% | Atlantic Provinces and Ontario | Short Term (≤ 2 Years) |

| Cold-Climate Heat Pump Performance Improvements | +0.8% | Prairie Provinces and Northern Territories | Long Term (≥ 4 Years) |

| Provincial Carbon Pricing Raising Fossil-Fuel Heating Costs | +0.7% | British Columbia, Quebec, Ontario, Alberta | Medium Term (2–4 Years) |

| Smart Grid Demand-Response Incentives for HVAC Loads | +0.4% | Ontario, British Columbia, Quebec | Long Term (≥ 4 Years) |

| Natural Refrigerant Adoption Ahead of 2025 HFC Phase-Down | +0.3% | National, Early Uptake in British Columbia and Ontario | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Government Incentives and Decarbonization Mandates

Rebates under the Canada Greener Homes programs have subsidized more than 280,000 units since 2020, and a recent survey shows 60% of buyers relied on at least one incentive. The 2025 National Building Code introduces six greenhouse-gas tiers, letting hydro-rich provinces meet Level A compliance simply by choosing electric heat pumps.[1]National Research Council Canada, “National Energy Code of Canada for Buildings: 2025,” publications-cnrc.canada.ca Provinces such as British Columbia and Quebec already signal intent to adopt higher tiers, giving the Canada heat pump market a predictable policy runway. Coupled with municipal bylaws that cap building emissions, the rules nudge developers toward pre-emptive electrification rather than retrofit later.

Rising Energy Prices Driving Cost-Savings Adoption

Atlantic households have migrated from heating oil to heat pumps as fuel surcharges and global oil volatility push annual operating costs above electric alternatives. Provincial utilities now top up federal rebates, pushing upfront savings to 50% in some cases. In Ontario, time-of-use rates and pilot demand-response payments shorten payback periods and help the Canada heat pump market penetrate gas-dominant suburbs.[2]Independent Electricity System Operator, “Demand Response Programs Overview,” ieso.ca

Cold-Climate Heat Pump Performance Improvements

Variable-speed compressors with enhanced vapor injection now sustain rated output to -15 °C and useful heating to -28 °C. Mitsubishi’s ecodan Pro delivers 60 °C water at -20 °C, opening retrofit opportunities in radiator-equipped buildings. The technology leap has lifted owner satisfaction to 91%, reflecting growing word-of-mouth credibility for the Canada heat pump market.[3]Clean Energy Canada, “Heat Pump Owners Have Their Say,” cleanenergycanada.org

Rising Energy Prices Driving Cost-Savings Adoption

British Columbia’s carbon tax climbed to CAD 80 (USD 62.4) per tonne in 2024, adding CAD 0.18 (USD 0.14) per m³ to gas bills and tipping cost parity toward electric systems. Quebec’s linked cap-and-trade scheme and Alberta’s emissions-intensity rules are producing similar price signals. As carbon levies escalate annually, the Canada heat pump market becomes the hedging strategy of choice for building owners facing uncertain fossil-fuel outlays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Equipment and Installation Costs | -0.6% | Prairie provinces and territories with limited rebates | Short term (≤ 2 years) |

| Skilled Labor Shortage for Certified Installers | -0.5% | National, acute in rural and remote areas | Medium term (2-4 years) |

| Electric-Grid Capacity Constraints During Peak Winter | -0.3% | Ontario, Alberta, Saskatchewan | Long term (≥ 4 years) |

| Consumer Misperceptions About Cold-Climate Performance | -0.2% | Prairie provinces and Northern territories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Equipment and Installation Costs

Installed prices range from CAD 5,000 to CAD 25,000 (USD 6,400 to USD 32,000) for air-source systems and rise to CAD 40,000 (USD 51,200) for ground-source projects, expenses that deterr many prairie households despite rebates.[4]Heating, Refrigeration and Air Conditioning Institute of Canada, “Installer Capacity Report,” hrai.caAir-to-water packages carry a further 20-40% premium because of buffer tanks and hydronic controls. A2L refrigerant safety features and technician certification add incremental material and labor cost, slowing Canada heat pump market momentum where subsidy stacks are thin.

Skilled Labor Shortage for Certified Installers

The national pool of A2L-qualified technicians lags demand, stretching urban lead times to 16 weeks and inflating rural project budgets by travel surcharges. Apprenticeship expansions and federal training grants are under way, yet most entrants will not reach field readiness until 2027. The bottleneck restricts rollout of advanced air-to-water and natural-refrigerant systems, putting a ceiling on near-term growth in the Canada heat pump market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Dominance With Hybrid Acceleration

Air source units commanded 82.58% share in 2025 thanks to lower cost and easier permitting. Hybrid air-source systems tied to gas furnaces are expected to grow at 5.17% CAGR because they hedge homeowners against extreme cold while still cutting emissions. Water source and ground source configurations remain niche yet attractive for district-energy sites like Toronto’s lake-loop integration, which underscores how the Canada heat pump market can scale in dense urban cores. Ground systems boasting seasonal COPs above 4.0 appeal to rural campuses and new subdivisions willing to finance borefields that last generations. Hybrid acceptance is strongest in Alberta and Saskatchewan, where dual-fuel switching near -10 °C meets cost-reduction goals without overloading carbon-intensive grids.

Regulatory tiers C and D under the new code recognize these compromises, creating a structured opening for hybrids inside the Canada heat pump market. The segment’s future hinges on grid decarbonization pace and carbon-price trajectories. If prairie utilities slash grid emissions by expanding wind and solar, full-electric air source may crowd out hybrids. Conversely, slow grid cleaning or high gas-price volatility would keep hybrid shipments buoyant. Either scenario sustains at least 20 appearances of air-source models on rebate eligibility lists each year, locking in visibility for the Canada heat pump market.

By Technology: Air-To-Water Gains In Commercial Retrofits

Air-to-air solutions supplied 58.12% of 2025 revenue, favored for ducted and ductless residential retrofits. Air-to-water designs, however, are advancing at 5.02% CAGR as commercial property owners chase 60-70 °C leaving water to retain radiator systems. Vancouver’s 575 V air-to-water district project and Johnson Controls’ condo developments exemplify how the Canada heat pump market size grows when hydronic flexibility merges with low-carbon goals.[5]Johnson Controls, “YORK 575 V Air-to-Water Brochure,” johnsoncontrols.com

Water-to-water ground loops suit institutional campuses, yet drilling logistics cap wider uptake. Future code tiers reward high leaving-water temperatures, and manufacturers now release cascade compressors rated to -20 °C at 60 °C supply. This evolution positions air-to-water as the premium retrofit path in provinces where carbon taxes and municipal bylaws penalize gas boilers. Continued refrigeration innovation, especially with R32 and R290, will likely narrow upfront cost gaps, reinforcing the Canada heat pump market share of hydronic systems.

By Capacity: Small Residential Units Lead, Mid-Range Commercial Accelerates

Below 10 kW models captured 52.23% of 2025 installations, covering single-family homes adopting ductless mini-splits. Mid-range 50-200 kW units, though only a 9% slice of shipments, are projected to rise at 4.84% CAGR because multi-unit housing and light-commercial buildings replace aging boilers to meet local emissions caps. Federal minimum COP rules effective 2026 force higher-efficiency designs, raising the Canada heat pump market size in the mid segment.

Viessmann and Bosch launches rated to -30 °C broaden addressable northern territory demand. Builders of new high-rise rentals can oversize shared 100 kW modules to exploit load diversity, trimming lifecycle cost against individual furnaces. Demand-response revenue stacking further sweetens payback, cementing mid-range capacity as the Canada heat pump market’s commercial workhorse through 2031.

By Application: Space Heating Dominates, Hot Water Gains Share

Space heating delivered 46.07% of 2025 revenue and remains core due to Canada’s climate severity. Domestic and sanitary hot-water units, however, post the fastest growth at 4.87% CAGR as air-to-water packages feed radiant loops and potable tanks from one outdoor unit. Samsung’s all-in-one model recycling cooling waste heat illustrates engineering strides that propel water-heating penetration inside the Canada heat pump market.

Industrial process projects such as Soteck’s 80 °C dairy line show COPs above 3.0, hinting at a budding high-temperature niche. Policy also shifts focus: building codes now count hot water toward operational greenhouse-gas limits, pushing developers to dual-purpose equipment. As utilities refine time-of-use rates, buffering hot water during off-peak hours lowers bills further, cementing the Canada heat pump market share growth of domestic hot water systems.

By End User: Residential Leads, Commercial Outpaces

The residential segment accounted for 61.09% of the Canada heat pump market share in 2025, reflecting the strong pull of federal and provincial rebates that target single-family retrofits. Homeowners are replacing aging furnaces with ductless mini-splits and cold-climate ducted systems able to hold full capacity to -25 °C, and smart-thermostat connectivity lets them join nascent demand-response programs that trim winter bills. Energy advisors also promote hybrid air-source solutions in prairie towns where low gas prices still appeal, but carbon charges keep full fossil heating from remaining cost-optimal. The commercial arena, however, posts the fastest expansion at a 4.78% CAGR as offices, schools and mixed-use towers prepare for municipal greenhouse-gas limits that lock out new gas boilers from 2026. Building owners favor modular 50-200 kW air-to-water packages that supply 60 °C water to existing radiators without ripping walls open, giving them a lower-risk path than deep envelope retrofits.

Mixed-use developments in Vancouver and Toronto prove that one central plant can meet residential, retail and institutional loads, improving asset utilization and project IRRs. Industrial demand is still modest, yet dairies, breweries and food processors now trial R1233zd units delivering 80 °C process water at coefficients of performance above 3.0, hinting at a future growth pocket. Across all end users, contractors report lead times lengthening to 10-16 weeks in peak season because of installer shortages, pushing some projects past rebate windows and nudging stakeholders to book equipment a full year in advance. Those dynamics together elevate lifecycle value propositions beyond the initial sticker price, reinforcing the long-run pull toward electrified heat in every customer class.

By Installation: Retrofit Dominates, New Construction Gains Momentum

Retrofit projects represented 67.83% of the Canada heat pump market size in 2025 because of the country’s vast legacy stock of oil and gas systems approaching end of life. Homeowners and facility managers tap stacked rebates that can offset up to half of upfront cost, and building-code amendments now classify major HVAC swaps as “alterations,” compelling emitters to meet higher efficiency tiers whenever they replace equipment. Contractors rely on ductless mini-splits for quick installs in older homes yet increasingly specify ducted cold-climate systems when owners want whole-home comfort paired with demand-response revenue. New-build applications, despite a smaller base, are forecast to rise at a 5.08% CAGR as developers treat heat pumps as the surest route to satisfy Level B or higher greenhouse-gas tiers without costly envelope upgrades. Prefabricated wall assemblies pre-wired for refrigerant lines and hydronic supply cut site labor, shortening schedules for modular and mid-rise projects.

In provinces with near-zero-carbon grids, code officials often recommend prescriptive compliance packages that award maximum points for an air-source or air-to-water unit, making alternative heating technologies less attractive. Builders also value the marketing edge of labeling homes “all electric and net-zero ready,” which commands selling-price premiums in fast-growing suburbs. Combined with utility time-of-use rates that reward off-peak water-heating, these factors set a clear glide path toward all-electric baselines in new housing subdivisions. Over the forecast window, analysts expect retrofit volumes to stay high as aging boilers phase out, yet the share of new-construction installs will climb steadily, creating a more balanced demand mix across the Canada heat pump market.

Geography Analysis

Atlantic Canada posts the country’s highest per-capita uptake thanks to heating-oil displacement, generous rebates and a greening grid that drops operating costs below oil burners. Nova Scotia alone installed 32,396 units under federal programs, translating customer savings into quick verbal referrals that sustain regional momentum. Ontario leads on absolute volume with 104,446 installs, yet widespread gas infrastructure tempers penetration; grid peak-demand concerns prompted the IESO to pilot winter load-shedding incentives that enhance the economics of smart-connected systems.

British Columbia combines an CAD 80 (USD 62.4)-per-tonne carbon tax with the Zero Carbon Step Code, steering builders toward electric systems even in areas already serviced by gas. Vancouver’s bylaw enforcing emissions caps on buildings larger than 50,000 ft² from 2025 tightens the commercial pipeline for the Canada heat pump market. Quebec added 69,321 units by 2025 and, owing to its near-zero-carbon hydro grid, now withholds single-family air-source rebates where gas lines exist, indirectly nudging multi-unit and ground-source uptake in dense suburbs.

Prairie provinces show mixed signals. Manitoba’s hydro grid supports electrification yet low gas prices slow adoption, keeping hybrids popular. Alberta and Saskatchewan struggle with high electricity carbon intensity, leading to the lowest heat-pump penetration in the country and framing the Canada heat pump market as a dual-fuel rather than full electrification play. Northern territories face severe cold and diesel-based power, limiting viability to special cold-climate units or community solar-plus-storage microgrids that could eventually electrify base heat loads.

Competitive Landscape

Global majors and regional specialists jostle in a moderately fragmented field. Daikin’s March 2026 launch of North America’s first residential R290 unit positions it as the refrigerant-transition front-runner, while Mitsubishi Electric’s ecodan Pro targets cold-climate hydronic retrofits with minus 28 °C ratings. Johnson Controls, Trane and Carrier invest in demand-response ready controls that speak OpenADR, enabling utilities to shave winter peaks and giving building owners a new revenue stream.

Geothermal suppliers such as WaterFurnace and ClimateMaster cater to campuses and rural estates requiring long-life underground loops, and local innovator Arctic Heat Pumps markets cost-efficient enhanced vapor injection products for -30 °C regions. Emerging CO₂ suppliers like Vitalis eye commercial refrigeration crossover, potentially disrupting the Canada heat pump market if commodity CO₂ prices remain stable.

Strategies converge on localization: Panasonic’s distribution deal with EMCO expands coast-to-coast service coverage; Bosch repackages U.S. AIM-Act compliant R-454B systems for Canadian codes; LG’s R32 monobloc simplifies hydronic installs by enclosing refrigerant circuits outdoors, a boon for installers facing A2L training gaps. Collectively, the top five vendors held nearly 55% of 2025 shipments, indicating moderate concentration yet vibrant room for niche challengers.

Canada Heat Pump Industry Leaders

Mitsubishi Electric Corporation

Daikin Industries Ltd.

Carrier Corporation

LG Electronics Inc.

Bosch Thermotechnology (GmbH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mitsubishi Electric debuted the ecodan Pro air-to-water series rated to -28 °C and 60 °C leaving water.

- March 2026: Daikin introduced a residential R290 heat pump ahead of federal efficiency rules.

- January 2026: Samsung released the EHS All-in-One unit integrating heating, cooling and domestic hot water for sub-25 °C climates.

- January 2026: The 2025 National Building Code and Energy Code took effect, embedding operational GHG tiers A-F.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canada heat pump market as all factory-built air-source, water-source, and ground-source heat pump units, expressed in U.S. dollars generated from their sale for residential, commercial, industrial, and institutional space-conditioning or sanitary-hot-water duties.

Scope exclusion: Window AC/heat-pump hybrids and portable electric space heaters are not counted.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Our analysts hold periodic interviews and brief surveys with manufacturer sales heads, installer networks active in Atlantic provinces and the Prairies, and officials administering rebate schemes in Ontario and British Columbia. These conversations ground truth rebate uptake, retrofit share, and cold-weather performance assumptions that underpin our model.

Desk Research

We draw on open datasets from Natural Resources Canada, Statistics Canada customs codes, Environment and Climate Change Canada rebate dashboards, and provincial utility filings to size unit inflows and average selling prices. International Energy Agency cold-climate performance tables and patent clusters captured through Questel signal future efficiency gains.

Company 10-Ks, IPO prospectuses, and investor presentations reveal pricing corridors, while news feeds accessed through Dow Jones Factiva flag subsidy launches and regulatory steps. The sources cited are illustrative; numerous additional public and subscription resources supported data capture, validation, and nuance gathering.

Market-Sizing & Forecasting

The 2024 base year revenue pool is rebuilt through a top-down merge of import statistics and federal rebate redemptions, which are then aligned with sampled supplier bookings to ensure coherence. Targeted bottom-up checks, installer volumes multiplied by prevailing ASPs, fine-tune provincial splits.

Model drivers include housing renovation permits, heating-degree-day trends, provincial electricity tariffs, average installed capacity per dwelling, and rebate uptake curves. We forecast through a multivariate regression, with scenario analysis framing upside tied to stricter carbon caps. Gaps in bottom-up granularity are bridged by interpolating adjacent provincial series and by expert opinion re-checks.

Data Validation & Update Cycle

Mordor analysts run automated anomaly scans, compare outputs with independent shipment trackers and utility electrification targets, and reconfirm outliers with sources before sign-off. Each study passes a two-stage peer review. We refresh figures annually, issuing interim updates when major policy or technology events occur.

Why Our Canada Heat Pump Baseline Stands Up to Scrutiny

Published estimates often diverge, largely because firms differ in scope choices, price ladders, and refresh timing.

Key gap drivers here include whether industrial installations are counted, how average selling prices are derived, currency-conversion dates, and the treatment of newly enhanced federal rebates that took effect in April 2025. Mordor's disciplined scope, live ASP tracking, and annual refresh cadence curb these variances.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.35 B (2025) | Mordor Intelligence | |

| USD 1.62 B (2024) | Global Consultancy A | Captures only air-source units and uses retail-chain ASPs |

| USD 1.59 B (2024) | Industry Association B | Omits industrial demand and applies fixed 1 CAD = 0.70 USD |

| USD 2.24 B (2024) | Regional Consultancy C | Relies on purchase intentions; excludes April 2025 rebate top-ups |

The comparison shows how narrower scopes, static pricing, or dated policy inputs compress other totals. Mordor Intelligence delivers a balanced, transparent baseline that ties every dollar to traceable variables and repeatable steps, giving decision-makers a dependable point of reference.

Key Questions Answered in the Report

What is the forecast value of the Canada heat pump market by 2031?

The market is projected to reach USD 3.06 billion by 2031.

How fast is the Canada heat pump market expected to grow between 2026 and 2031?

It is set to expand at a 4.63% CAGR over the forecast period.

Which heat pump technology is gaining traction in commercial retrofits?

Air-to-water systems are advancing at a 5.02% CAGR because they provide 60-70 °C water for legacy radiators.

Why are hybrid heat pumps popular in prairie provinces?

Dual-fuel systems balance cost and carbon savings by switching to gas during extreme cold, avoiding grid strain.

What policy change most directly supports new-build adoption?

The 2025 National Building Code introduces greenhouse-gas tiers that favor electric heat pumps as a compliant solution.

Which capacity band is rising fastest in commercial buildings?

The 50-200 kW segment is growing at a 4.84% CAGR as offices and condos replace boilers with centralized heat pumps.

Page last updated on: