United Kingdom Heat Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

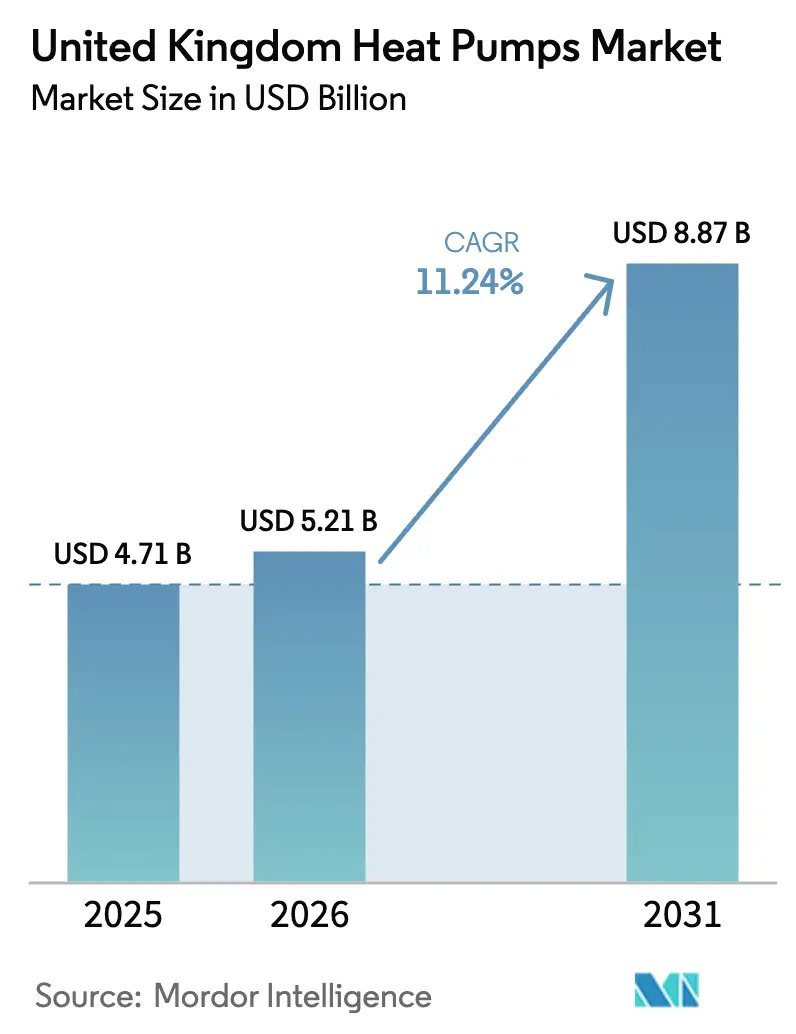

| Base Year Market Size (2025) | USD 4.71 Billion |

| Market Size (2026) | USD 5.21 Billion |

| Market Size (2031) | USD 8.87 Billion |

| Growth Rate (2026 - 2031) | 11.24% CAGR |

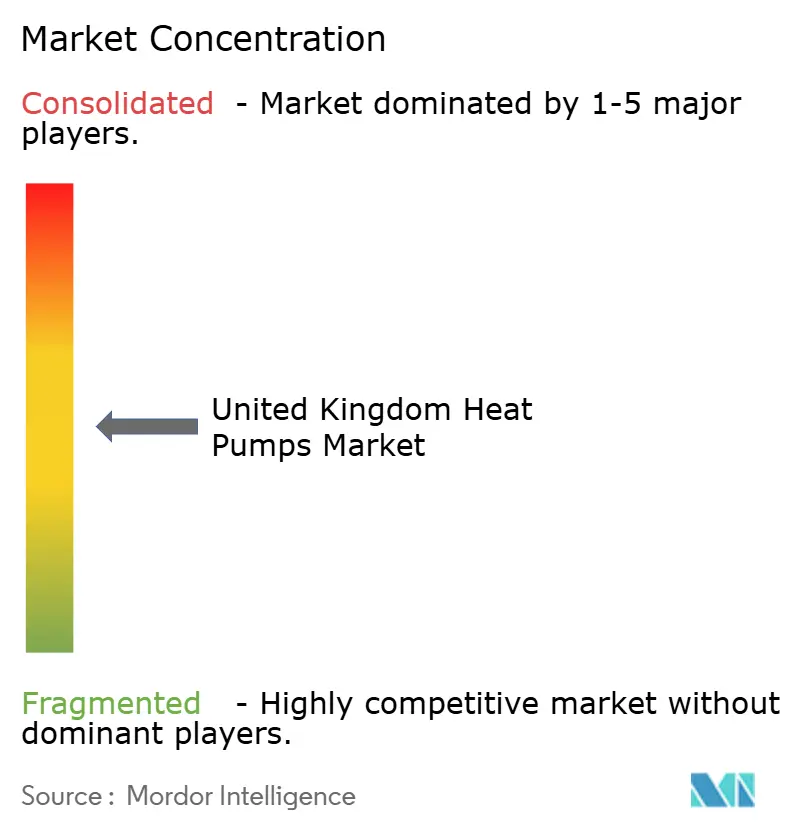

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Heat Pumps Market Analysis by Mordor Intelligence

The United Kingdom heat pumps market size is expected to increase from USD 4.71 billion in 2025 to USD 5.21 billion in 2026 and reach USD 8.87 billion by 2031, growing at a CAGR of 11.24% over 2026-2031. Elevated carbon-reduction mandates, richer installation subsidies, and rapid domestic production expansion underpin this outlook. The United Kingdom heat pumps market is benefiting from the Boiler Upgrade Scheme’s higher GBP 7,500 grant ceiling, a falling electricity-to-gas price ratio that improves running-cost parity, and accelerating investment in local manufacturing lines that shorten delivery cycles. Integrated energy-service platforms are entering the value chain, signaling a shift from a fragmented installer model toward vertically integrated offerings. Execution risks do persist, chiefly the installer skills gap, localized grid congestion, and rising consumer interest in hybrid solutions that retain gas back-up capacity.

Key Report Takeaways

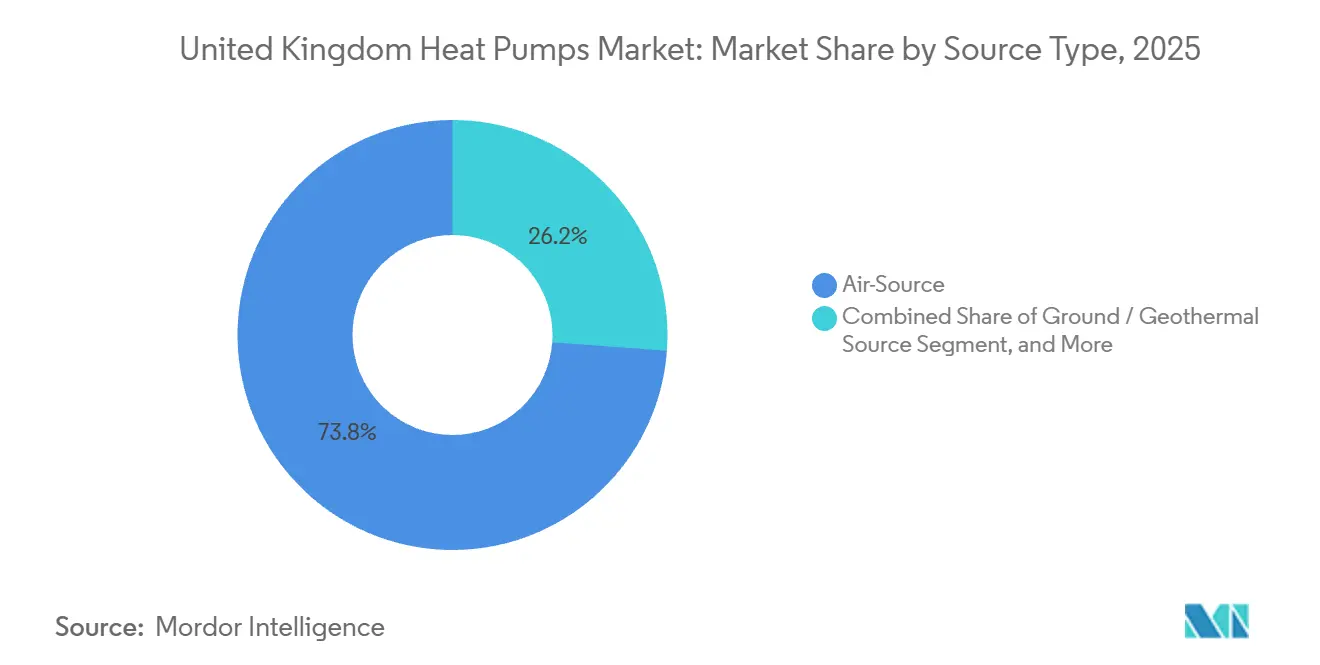

- By source type, air-source systems led with 73.83% revenue share in 2025, while ground-source units are projected to post a 12.31% CAGR through 2031.

- By rated capacity, units up to 10 kW accounted for 44.26% of 2025 demand, whereas systems above 30 kW are forecast to grow at 12.78% CAGR to 2031.

- By system design, split configurations commanded 61.14% of installations in 2025, with hybrid heat pumps expected to register a 12.16% CAGR over the outlook period.

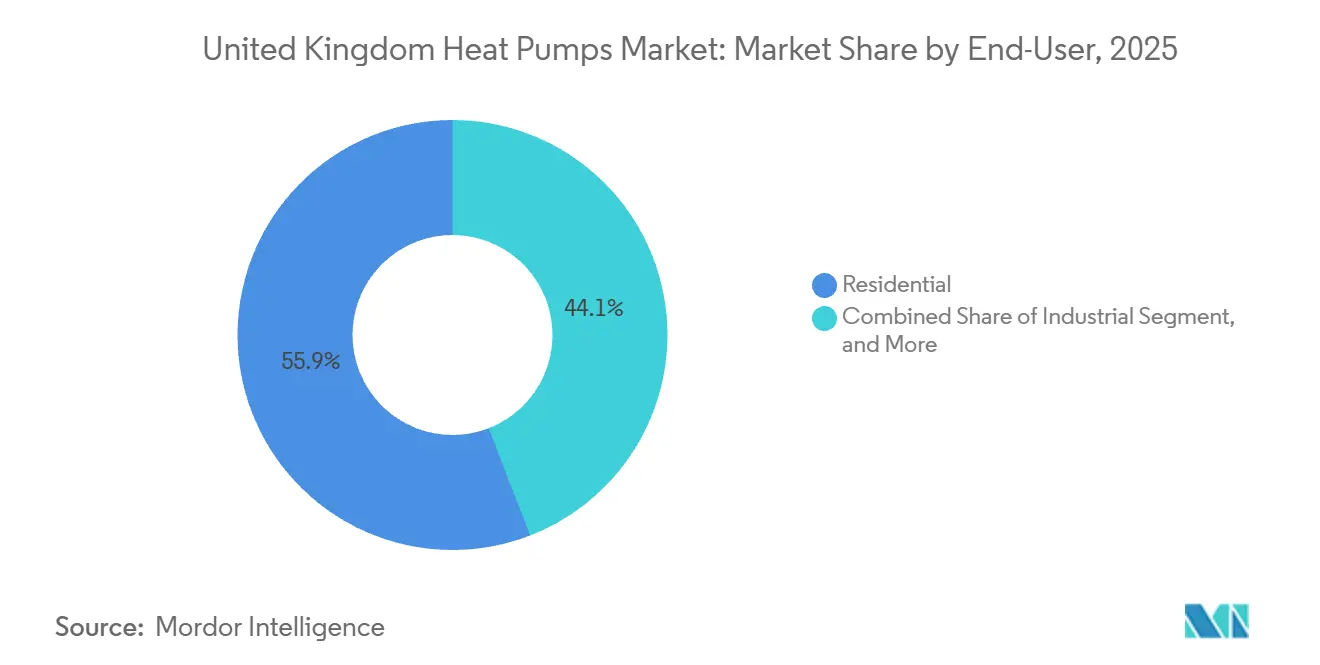

- By end-user, residential customers generated 55.88% of 2025 revenue, and industrial deployments are anticipated to expand at 12.82% CAGR through 2031.

- By application, space-heating and cooling captured 63.54% of 2025 turnover, while district-heating networks are set to record a 12.47% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Heat Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Regulations and Net-Zero Targets | +3.2% | National, strongest in England and Wales | Long term (≥ 4 years) |

| Boiler Upgrade Scheme Grants and Other Financial Incentives | +2.8% | National, with higher uptake in Scotland | Medium term (2-4 years) |

| Rising Electricity-Gas Price Differential Favouring Heat Pumps | +1.9% | National, acute in off-grid areas | Medium term (2-4 years) |

| Domestic Manufacturing Scale-up via Heat Pump Investment Accelerator | +1.5% | National, concentrated in Midlands and North | Long term (≥ 4 years) |

| Recovering Office-Space Demand and HVAC Retrofits | +0.7% | London, Manchester, Birmingham, Edinburgh | Short term (≤ 2 years) |

| Flexible Tariff and Demand-Side Response Integration | +0.6% | National, early adopters in smart-meter households | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Regulations and Net-Zero Targets

Legally binding 2050 net-zero legislation places heat decarbonization at the center of the United Kingdom's climate strategy, as space and water heating account for 37% of national emissions. The Clean Heat Market Mechanism, introduced in 2024, obliges boiler brands to ensure heat pumps represent at least 8% of annual sales, embedding a compliance cost on gas-only portfolios.[1]Department for Energy Security and Net Zero, “Clean Heat Market Mechanism Year 2 Guidance,” gov.uk The Future Homes Standard, implemented in 2025, requires new houses to cut carbon emissions by up to 80% relative to 2013 baselines, effectively locking heat pumps into all future residential constructions. Combined with the government’s 600,000-unit annual installation target for 2028, these policy levers push manufacturers to redirect R&D away from condensing boilers toward advanced heat-pump platforms. The result is a durable, long-horizon demand signal that anchors the United Kingdom heat pumps market.

Boiler Upgrade Scheme Grants and Other Financial Incentives

The Boiler Upgrade Scheme lifted its air-source grant to GBP 7,500 (USD 9,500) in October 2024, slashing the upfront premium over a gas boiler to GBP 3,000-5,000 for a typical home.[2]Ofgem, “Boiler Upgrade Scheme Grant Increase Announcement,” ofgem.gov.uk Monthly applications rose 88% year-on-year by March 2025, yet the cumulative total still covers less than 7% of the 600,000-unit annual target, underscoring the runway for growth.[3]Department for Energy Security and Net Zero, “Boiler Upgrade Scheme Statistics,” gov.uk Additional regional incentives, such as Scotland’s rural grant of up to GBP 9,000, create a north-south uptake gradient, while the Heat Training Grant helps defray installer accreditation costs. Although funding pools have been expanded, grant awareness and installer throughput remain gating factors, suggesting financial sweeteners should continue to stimulate volume in the medium term.

Rising Electricity-Gas Price Differential Favouring Heat Pumps

Wholesale gas eased from its 2022 spike, yet electricity tariffs stayed buoyant due to network levies, compressing the electricity-to-gas unit-price ratio toward 3:1 by late 2024. At coefficients of performance near 3.0, heat pumps achieve operating-cost parity with gas boilers around this 3:1 threshold, a milestone many households are now approaching. Innovative time-of-use tariffs, such as Cosy Octopus, offer overnight electricity at 9 p/kWh, enabling pre-heating strategies that save roughly GBP 96 per year. Ofgem’s consultation on shifting environmental levies from electricity to gas could further shave 10-15% off electric unit rates, structurally improving lifetime economics for heat pumps. Off-grid homes running on heating oil already enjoy 30-50% lower running costs after switching, which magnifies their appeal in rural markets.

Domestic Manufacturing Scale-up via Heat Pump Investment Accelerator

The Heat Pump Investment Accelerator has unlocked GBP 30 million in matched funding, spurring marquee commitments from Vaillant and Baxi to produce 400,000 and 200,000 units per year respectively inside the United Kingdom by 2027. Local lines cut lead times that stretched to 12-16 weeks in 2023 and buffer exchange-rate and tariff risk post-Brexit. They also nurture a specialized labor pool, improving service quality and accelerating product iteration for United Kingdom climate conditions. While key components such as compressors still rely on imports from Asia, a rising domestic content share enhances supply-chain resilience and supports the United Kingdom heat pumps market’s long-term expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of Cheaper Gas-Boiler Replacements | -1.8% | National, strongest in urban areas with gas grid access | Medium term (2-4 years) |

| Shortage of Qualified Heat-Pump Installers | -1.5% | National, acute in rural and northern regions | Medium term (2-4 years) |

| Local Distribution-Grid Capacity Constraints | -0.9% | Rural areas and older suburban networks | Long term (≥ 4 years) |

| Semiconductor and Rare-Earth Magnet Supply Risks | -0.6% | Global, affecting all manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prevalence of Cheaper Gas-Boiler Replacements

Replacing a gas boiler costs GBP 2,000-3,500 versus GBP 10,000-14,000 for an air-source heat pump, even after subsidies, keeping a sizeable upfront premium that deters cash-constrained households. Behavioural inertia reinforces like-for-like boiler swaps, as many owners act only when a unit fails in winter. Hybrid heat pumps, priced between GBP 6,000-9,000 yet ineligible for grants, further complicate pure electrification by offering an incremental pathway. Because the Clean Heat Market Mechanism targets only manufacturers, installer businesses can still focus on boiler replacements without penalty, limiting near-term conversion in the United Kingdom heat pump market.

Shortage of Qualified Heat-Pump Installers

The country employs as few as 4,000 certified heat-pump installers, but reaching 600,000 annual installations demands at least 27,000 technicians by 2028. Roughly 39% of trainees exit the trade before their first installation, citing low early-career volumes and high compliance overhead. Rural customers have reported six-to-twelve-month waits for quotations, throttling market momentum in 2024 and 2025. Although the Heat Training Grant offsets course fees, income volatility and administrative burden still curtail workforce expansion, creating a material drag on the United Kingdom heat pumps market through mid-decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air-Source Scale And Ground-Source Upside

In 2025, air-source systems commanded a dominant 73.83% share of the revenue. Meanwhile, ground-source units are on track to achieve a notable 12.31% CAGR through 2031. Air-source units captured the lion's share of 2025's revenue, because they fit typical U.K. retrofits and qualify for the largest subsidy. Residential customers prize the compact split-system form factor, while light-commercial buyers value inverter compressors that modulate to partial loads. Nevertheless, lifecycle economics increasingly favor ground-source designs in schools, offices, and logistics centers that operate for 20-plus years. Seasonal performance factors above 4.0 shave operating costs by up to 30%. Closed-loop vertical borehole systems overcome urban space limits, and government guidance has simplified planning approval, boosting tender volumes for projects above 200 kW. As heat-network developers bundle shared ground arrays into regeneration sites, the United Kingdom heat pumps market is expected to see ground-source penetration rise steadily through 2031.

Air-to-air technology remains a gray-area niche, with roughly 225,000 units installed by early 2025 but excluded from the Clean Heat Market Mechanism. Removal of that exclusion could accelerate growth, especially in flats where hydronic retrofits are impractical. Meanwhile, the emerging deep-geothermal roadmap identifies Cornwall and the Midlands as long-term hot spots, offering baseload heat for district grids beyond 2030. Investors will watch pilot outcomes closely, as successful demonstrators could open a new vertical within the United Kingdom heat pumps market.

By Rated Capacity: Small Units Dominate, Large Arrays Accelerate

In 2025, units up to 10 kW made up 44.26% of the demand, while systems exceeding 30 kW are projected to expand at a CAGR of 12.78% through 2031. Equipment in the residential scale, particularly those up to 10 kW, underscores the gradual decarbonization trend in detached houses and small terrace homes. In suburban infill projects, 10-20 kW systems are now catering to multi-family blocks, eliminating the need for central plant rooms. This is made possible by using low-profile outdoor units that adhere to noise limits set by permitted developments. The 20-30 kW range is ideal for primary schools, care homes, and convenience retail outlets. Here, the simultaneous demands for space heating and domestic hot water necessitate buffers to prevent short cycling.

Growth is shifting toward systems above 30 kW, especially arrays for district-heating substations and industrial process loops. Daikin’s five-year Greater Manchester framework, covering 64,000 systems, exemplifies volume procurement aligned with local-authority climate plans. High-temperature platforms that deliver 80-100 °C water are displacing gas boilers in food manufacture and paper mills, and the Industrial Heat Recovery Support program co-funds feasibility studies that derisk corporate capital budgets. As a result, the large-capacity slice of the United Kingdom heat pumps market is forecast to outpace the aggregate growth rate through 2031, reinforcing supply-chain moves toward modular, containerized designs.

By System Design: Split Convenience Versus Hybrid Transition

Split configurations captured 61.14% of 2025 installations, benefiting from widespread installer familiarity and superior acoustic performance. Manufacturers continuously refine refrigerant charge to meet F-gas quotas, with R290 propane emerging as a low-GWP frontrunner. Monobloc units, produced at Vaillant’s new Derby plant, avoid F-gas handling on-site and reduce installation time by up to one day, an advantage in the constrained installer landscape.

Hybrid heat pumps appeal to households reluctant to upgrade radiators or electrical service heads. The technology’s 12.16% CAGR through 2031 reflects a cost-effective bridge toward full electrification, the electric compressor addresses the baseload and the retained gas boiler covers peak demand. Critics warn of lock-in effects if hybrids remain in place beyond 2035, yet payback dynamics are compelling today for the 15 million homes below EPC Band C. Smart-switching controls that default to the compressor when electricity prices fall under time-of-use tariffs can halve gas consumption without compromising comfort.

By End User: Homeowners Lead, Factories Follow

Residential customers generated 55.88% of 2025 sales, propelled by grant support and consumer marketing campaigns. Penetration is still under 1% of the 29 million-unit housing stock, leaving vast upside for the United Kingdom heat pumps market. Commercial retrofits are climbing as landlords race to satisfy Minimum Energy Efficiency Standards that tighten to EPC B by 2030. Pilot projects from Arup and British Land show 50-60% HVAC energy savings and enhanced tenant retention.

Industrial adoption, advancing at 12.82% CAGR, now targets process-heating segments below 150 °C, where high-temperature pumps replace steam boilers and recover waste heat from refrigeration cycles. Firms tapping the Industrial Heat Recovery Support scheme report three-year paybacks when paired with dynamic tariffs that value flexible load. Public-sector institutions, led by the NHS Net Zero Strategy, are procuring standardized heat-pump packages via national frameworks, bringing predictable volume to suppliers.

By Application: Space Heating Commands, District Networks Surge

Space-heating and cooling functions held 63.54% of 2025 revenue, a natural outcome in a heating-dominated climate. Modern inverter compressors deliver year-round comfort and trim shoulder-season gas consumption in mixed-fuel buildings. Domestic-hot-water use cases demand outlet temperatures above 55 °C to manage Legionella risk, and manufacturers meet this threshold either via cascade refrigeration cycles or electric immersion boosters.

District-heating applications, advancing at 12.47% CAGR, bundle utility-scale heat pumps with thermal stores and secondary loops serving dense urban quarters. Greater Manchester’s GBP 400 million pipeline targets 90 GWh per year by 2030, leveraging largescale arrays to unlock economies of scale. South Kilburn and Bristol Temple Quarter are additional proof points showing how municipal clients de-risk bankability for private operators. Over the outlook period, the United Kingdom heat pumps market is likely to see district schemes transition from pilot phase to mainstream capital-market asset class.

Geography Analysis

Installations in England contributed roughly three-quarters of 2025 unit volume, anchored by dense housing and the strongest installer base. Scotland punches above its population share thanks to richer Home Energy Scotland grants that cover up to GBP 9,000, fostering higher per-capita uptake. Wales benefits from robust retrofits in off-grid rural areas where heating oil remains expensive, and Northern Ireland shows early momentum after Octopus Energy’s acquisition of a local manufacturer.

Regional electricity pricing and grid capacity shape adoption patterns. Rural counties in southwest England and the Highlands face transformer congestion that can delay connections, while urban centers leverage stronger distribution networks and shorter installer travel times. London boroughs witness rising commercial demand driven by air-quality zones that penalize fossil-fuel boilers, whereas the Midlands gain manufacturing-linked employment as Vaillant and Baxi expand local lines.

Policy delivery differs across devolved administrations. Scotland’s heat-in-buildings strategy sets steeper interim targets, Wales emphasizes social-housing retrofits, and Northern Ireland prioritizes installer-training subsidies to boost local capacity. Despite these nuances, the United Kingdom heat pumps market demonstrates coherent national momentum, with each geography contributing distinct growth levers that collectively sustain double-digit expansion through 2031.

Competitive Landscape

The market is moderately fragmented. Boiler incumbents leverage legacy installer networks to cross-sell heat pumps, while pure-play brands such as NIBE and Kensa focus on technical performance and deep installer training. Octopus Energy’s 2024 acquisition of Renewable Energy Devices illustrates vertical integration that captures margin from the factory floor to the energy tariff.

Technology competition centers on variable-speed inverters, low-GWP refrigerants, and cloud-linked smart controls that align consumption with time-of-use tariffs. Several manufacturers have filed patents for machine-learning algorithms that anticipate weather and occupancy patterns, raising performance while easing user interaction. Subscription business models that bundle hardware, installation, and electricity supply at a flat monthly fee are emerging, potentially rewriting revenue streams in the United Kingdom heat pumps market.

New entrants target white-space opportunities. Hybrid systems appeal to gas-grid homes wary of full electrification. High-temperature units serve industrial process heat below 100 °C, and shared ground-loop arrays unlock dense urban sites. Component shortages, notably semiconductors and rare-earth magnets, remain a watch-list risk, but domestic assembly investments improve resilience and shorten order lead times.

United Kingdom Heat Pumps Industry Leaders

IMS Heat pumps

Vaillant Group

Baxi Heating UK

Worcestor Bosch Group

Viessmann Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Daikin and Copeland formed a joint venture to expand compressor production in the United Kingdom, ensuring supply for the Greater Manchester framework.

- November 2025: The government launched Round 2 of the Heat Pump Investment Accelerator, allocating GBP 90 million to boost domestic manufacturing capacity.

- September 2025: Octopus Energy and LG announced a partnership to co-develop Kraken-enabled heat pumps optimized for the Cosy tariff, targeting 50,000 units by 2027.

- March 2025: Vaillant opened its GBP 40 million Derby plant producing monobloc R290 units, creating 200 jobs.

United Kingdom Heat Pumps Market Report Scope

Heat pumps are machines that transfer heat energy from a heat source to a thermal reservoir, moving it in the opposite direction of spontaneous heat transfer by absorbing heat from a cold space and releasing it into a warmer one. The market for the study is defined as the revenues generated from the sale of Heat Pumps. Moreover, various end-user industries tracked for market estimations include industrial, commercial, and residential, among others. The market also covers the major factors impacting the heat pumps market, including drivers and restraints.

The United Kingdom Heat Pumps Market Report is Segmented by Source Type (Air-Source, Water-Source, and Ground/Geothermal Source), Rated Capacity (Up to 10 kW, 10-20 kW, 20-30 kW, and Above 30 kW), System Design (Split System, Monobloc, and Hybrid Heat Pump), End-User (Residential, Commercial, Industrial, and Institutional), Application (Space Heating and Cooling, Water Heating, District Heating, and Process and Industrial Heating). The Market Forecasts are Provided in Terms of Value (USD).

| Air-Source | Air-to-Air |

| Air-to-Water | |

| Water-Source | Surface Water |

| Open Loop | |

| Ground / Geothermal Source | Closed Loop Vertical |

| Closed Loop Horizontal | |

| Direct Expansion |

| Up to 10 kW |

| 10-20 kW |

| 20-30 kW |

| Above 30 kW |

| Split System |

| Monobloc |

| Hybrid Heat Pump |

| Residential |

| Commercial |

| Industrial |

| Institutional |

| Space Heating and Cooling |

| Water Heating |

| District Heating |

| Process and Industrial Heating |

| By Source Type | Air-Source | Air-to-Air |

| Air-to-Water | ||

| Water-Source | Surface Water | |

| Open Loop | ||

| Ground / Geothermal Source | Closed Loop Vertical | |

| Closed Loop Horizontal | ||

| Direct Expansion | ||

| By Rated Capacity | Up to 10 kW | |

| 10-20 kW | ||

| 20-30 kW | ||

| Above 30 kW | ||

| By System Design | Split System | |

| Monobloc | ||

| Hybrid Heat Pump | ||

| By End-User | Residential | |

| Commercial | ||

| Industrial | ||

| Institutional | ||

| By Application | Space Heating and Cooling | |

| Water Heating | ||

| District Heating | ||

| Process and Industrial Heating | ||

Key Questions Answered in the Report

How large is the United Kingdom heat pumps market in 2026?

The United Kingdom heat pumps market size is USD 5.21 billion in 2026, rising toward USD 8.87 billion by 2031.

What CAGR is expected for heat pumps in the United Kingdom to 2031?

Revenue is projected to expand at an 11.24% CAGR over the 2026-2031 period.

Which heat-pump source type is growing fastest?

Ground-source systems are forecast to post a 12.31% CAGR through 2031 as commercial and institutional buyers prioritize lifecycle efficiency.

Why are hybrid heat pumps gaining interest despite limited subsidies?

Hybrids let households cut gas use 50-70% without major radiator or insulation upgrades and benefit from smart tariffs that lower running costs.

What policy incentives support adoption today?

Key levers include the GBP 7,500 Boiler Upgrade Scheme grant, the Clean Heat Market Mechanism, and region-specific top-ups such as London's Warmer Homes program.

How severe is the installer capacity gap?

As few as 4,000 installers currently hold the required certification, while at least 27,000 technicians will be needed by 2028 to meet the 600,000-unit installation target.

Page last updated on: