IoT Identity Access Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

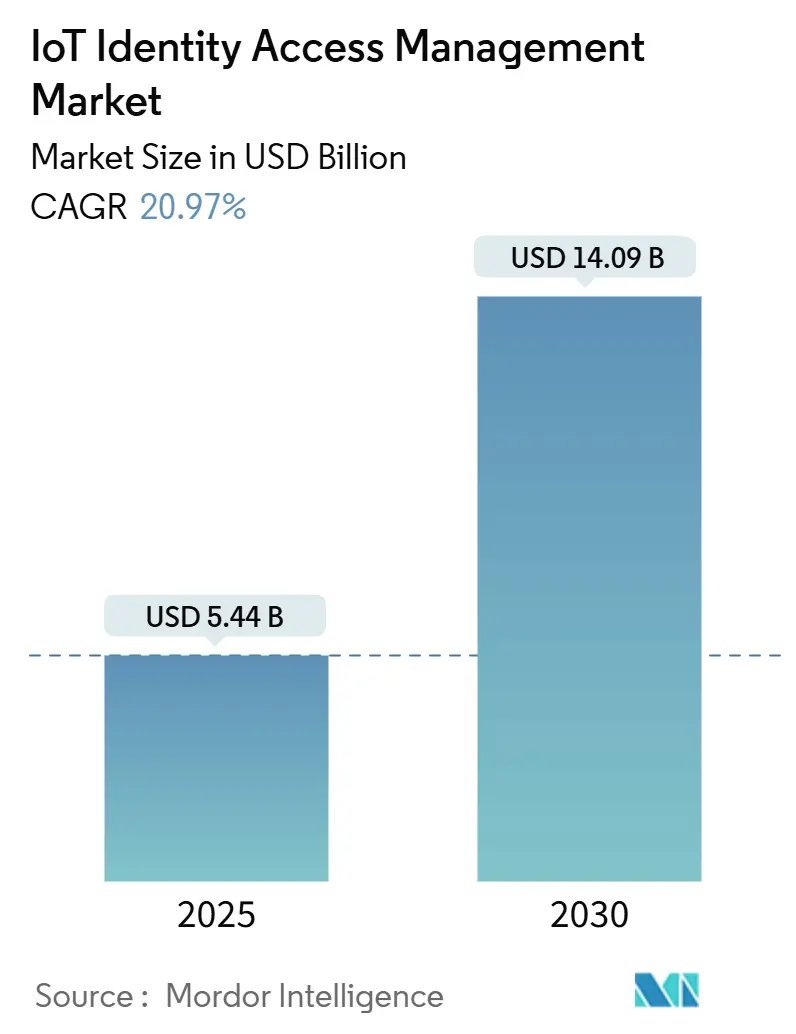

| Market Size (2025) | USD 5.44 Billion |

| Market Size (2030) | USD 14.09 Billion |

| Growth Rate (2025 - 2030) | 20.97% CAGR |

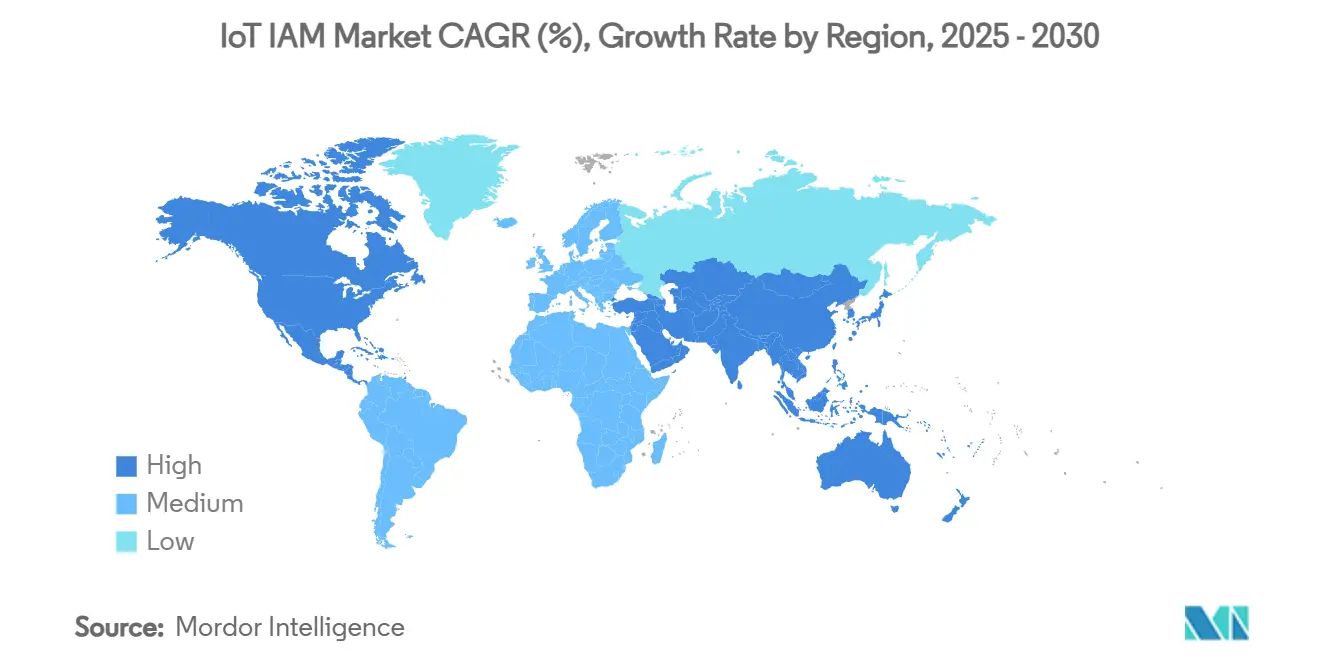

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Identity Access Management Market Analysis by Mordor Intelligence

The IoT Identity Access Management Market size is estimated at USD 5.44 billion in 2025, and is expected to reach USD 14.09 billion by 2030, at a CAGR of 20.97% during the forecast period (2025-2030).

Accelerated brown-field retrofits of operational technology, mandatory software bill of materials (SBOM) rules on both sides of the Atlantic, and the mainstreaming of passwordless authentication across industrial settings all reinforce the growth outlook. Manufacturers are building zero-trust controls into programmable logic controllers, healthcare suppliers are racing to meet FDA cybersecurity mandates, and cloud-delivered identity platforms are displacing on-premise tools as enterprises demand simpler scaling options, further driving the IoT identity access management market. Telco security-as-a-service bundles lower entry barriers for small firms, while soaring cyber-insurance premiums create an explicit financial upside for every organization that can document strong identity controls. Fragmentation persists, yet strategic acquisitions by incumbents and the arrival of chip-level zero-trust blueprints point to an eventual re-ordering of the competitive field.

Key Report Takeaways

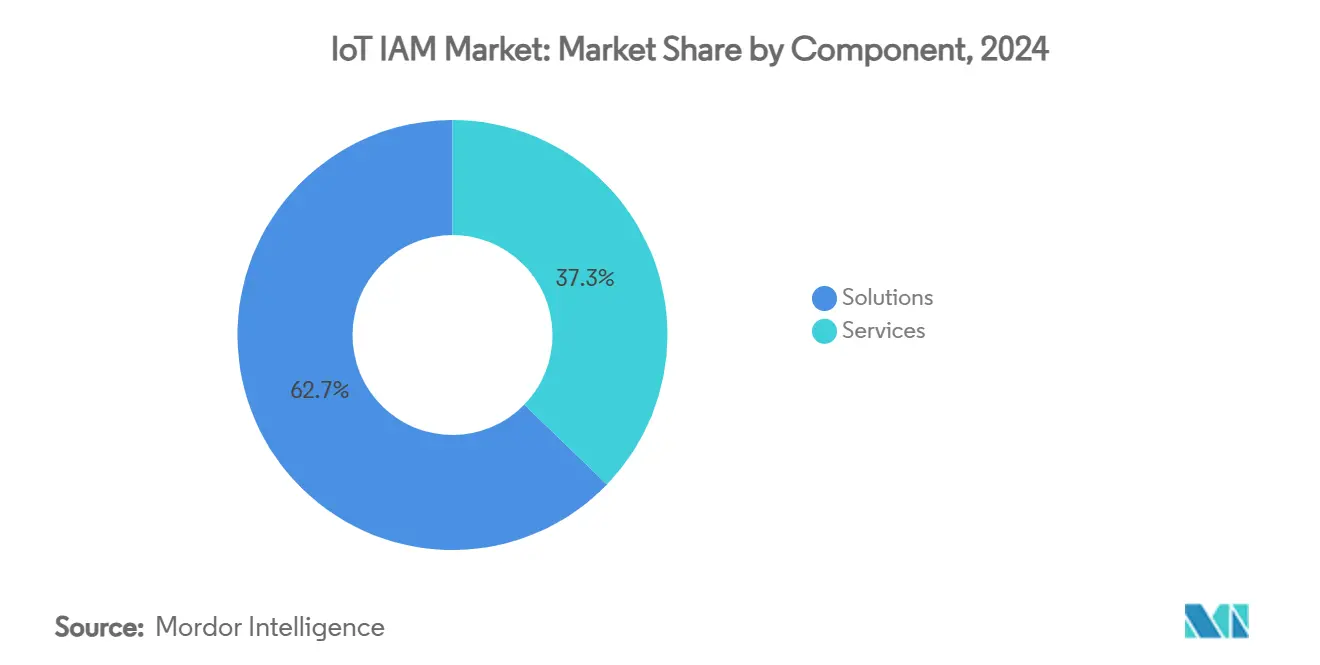

- By component, solutions accounted for 62.75% revenue share in 2024, whereas services within the IoT IAM market are advancing at a 21.54% CAGR through 2030

- By deployment mode, cloud captured 70.54% of the 2024 IoT IAM market share, while hybrid architectures are growing at a 22.67% CAGR to 2030.

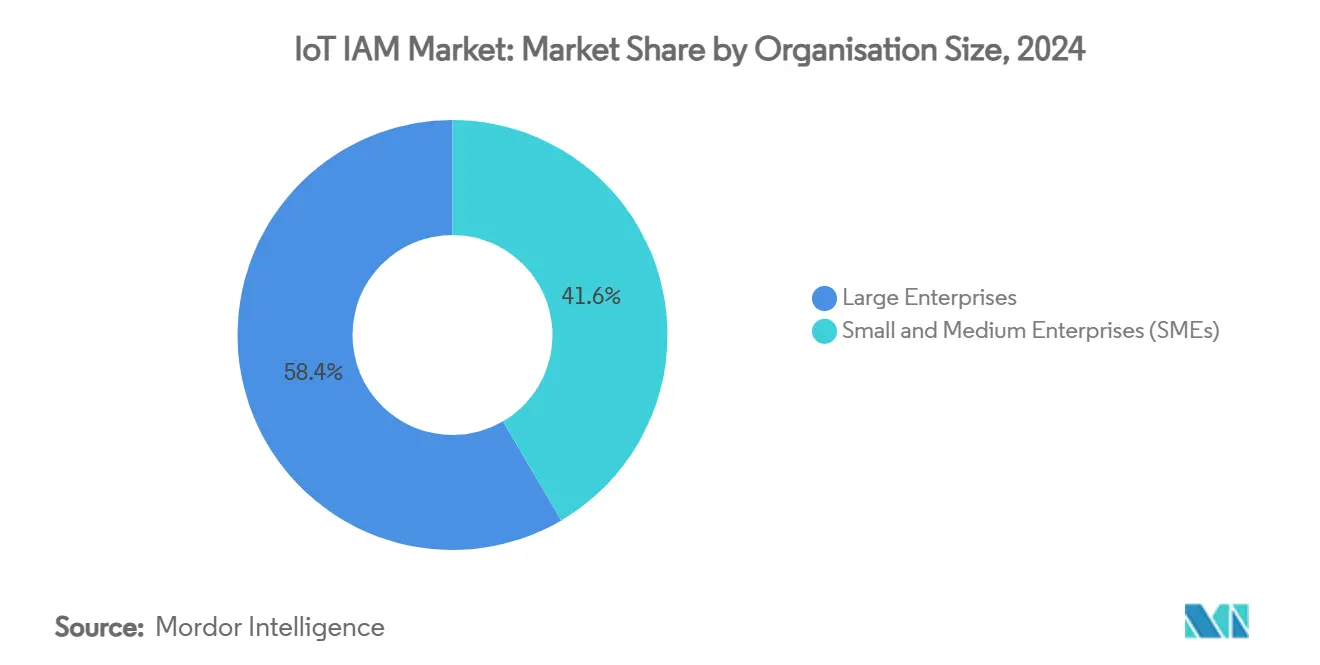

- By organization size, large enterprises held 58.43% share of the IoT IAM market size in 2024, yet SMEs record the fastest CAGR at 21.96% through 2030.

- By industry vertical, manufacturing led with 24.64% of IoT IAM market share in 2024; healthcare is projected to expand at a 24.01% CAGR to 2030.

- By geography, North America retained 38.54% share in 2024, while Asia-Pacific posts the highest CAGR of 24.65% over the forecast horizon of the IoT Identity access management market.

Global IoT Identity Access Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of connected OT assets in brown-field industrial plants | +4.2% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Mandatory SBOM disclosure rules in US and EU | +3.8% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| Edge-native zero-trust reference architectures from chip vendors | +3.5% | Global | Medium term (2-4 years) |

| Rising cyber-insurance premiums pushing IAM adoption | +2.9% | North America and EU core, expanding to APAC | Short term (≤ 2 years) |

| Mainstream shift to passwordless authentication for IoT endpoints | +3.1% | Global | Medium term (2-4 years) |

| Managed IoT security-as-a-service bundles from telcos | +2.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of Connected OT Assets in Brown-field Industrial Plants

Industrial firms keep attaching sensors and gateways to decades-old machinery, creating identity blind spots in once air-gapped networks. Nozomi Networks embedded a security sensor in Mitsubishi Electric PLCs to provide real-time process monitoring, illustrating how device visibility reaches deep into control loops. The ISA Global Cybersecurity Alliance notes that 62% of factories now demand SL2 capabilities such as user distinction and session management, features rarely baked into legacy hardware. Linking aging protocols with modern authentication pushes organizations toward hybrid identity frameworks able to reconcile Modbus, PROFINET, and MQTT traffic within the same trust fabric. Vendors gain traction by offering appliance-free discovery, micro-segmentation policies for PLC networks, and root-of-trust enforcement at the edge. As more brown-field sites upgrade, demand for interoperable identity mapping services soars, especially where downtime penalties are severe.

Mandatory SBOM Disclosure Rules in US and EU

NIST’s SBOM mandate and CISA’s companion guidance force every connected-device maker to catalog software components and disclose vulnerabilities, embedding identity thinking into the supply chain. [1]National Institute of Standards and Technology, “New NIST Errata Update – C-SCRM,” nist.gov The Defense Acquisition University codified SBOM templates in January 2024, turning procurement contracts into enforcement levers for authentication depth at both device and component levels. Europe’s Cyber Resilience Act mirrors this stance by imposing liability on vendors that lack continuous identity oversight across product life cycles. These rules prompt device makers to weave certificate hierarchies into build pipelines, automate signing of firmware packages, and expose real-time inventory feeds to customers. In parallel, auditing platforms able to map CVEs to identity attributes become essential for risk scoring and warranty claims. Compliance deadlines create an upfront cost spike, but the resulting transparency lowers mean-time-to-respond and builds confidence among insurers and regulators.

Edge-native Zero-trust Reference Architectures from Chip Vendors

Semiconductor designers now imprint zero-trust blueprints into silicon, bypassing perimeter-centric models. The Cloud Security Alliance outlines a five-step path for operational technology environments, cementing continuous verification as a design baseline.[2]Cloud Security Alliance, “Zero Trust for Critical Infrastructure Security,” cloudsecurityalliance.org Cisco’s Identity Services Engine 3.x adds cloud-enabled device profiling and agentless checks, proving that least-privilege enforcement can coexist with deterministic control loops. Hardware passkey readiness already exceeds 75% of connected devices, clearing the path for credential-free onboarding and mutual attestation. This integration lets OEMs market “trust-as-a-feature” SKUs, differentiating on cryptographic acceleration and secure enclave isolation. Consequently, board-room debates shift from whether to adopt zero-trust to which chipset roadmap delivers the deepest embedded controls at acceptable cost.

Rising Cyber-insurance Premiums Pushing IAM Adoption

Insurance carriers tighten underwriting criteria, demanding proof of privileged-access hygiene before issuing IoT coverage. Vodafone UK showed SMEs lose billions to lax security, a statistic insurers cite when pricing policies. Semiconductor fabs face state-sponsored threats, driving Deloitte to urge supply-chain grade IAM as a guardrail against IP theft. Sectigo reports a 243% ROI for automated certificate management, quantifying the benefit side of the security ledger. The premium differential between firms that present auditable identity controls and those that cannot widens yearly, effectively converting IAM expenditure into risk-financing savings. Boards increasingly require documentation of certificate rotation cadences, least-privilege roles, and zero-trust segmentation in renewal submissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy PLCs with hard-coded credentials | -2.1% | Global, manufacturing-heavy regions | Long term (≥ 4 years) |

| Inter-vendor certificate format incompatibility | -1.8% | Global | Medium term (2-4 years) |

| OPEX spike from X.509 lifecycle management at scale | -1.5% | North America and EU core | Short term (≤ 2 years) |

| Shortage of OT-security-skilled labour in emerging markets | -1.9% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy PLCs with Hard-coded Credentials

Millions of programmable logic controllers still carry factory-set passwords burnt into firmware, leaving no path for field updates. The ISA Global Cybersecurity Alliance published its top 20 secure PLC coding practices, but retrofitting guidance onto hardware built before 2015 often demands shutdowns that plants can ill afford. [3]ISA Global Cybersecurity Alliance, “Top 20 Secure PLC Coding Practices Available Now,” isa.org RF IDEAS advocates external credential readers to overlay logical access control without flashing firmware, yet physical install work disrupts production lines. Georgia Tech’s PLCHound algorithm hunts static credentials in traffic flows, but detection does not equate to remediation when hardware lacks root-of-trust anchors. The sheer installed base means replacement cycles stretch into decades, dragging down the addressable segment for advanced identity orchestration.

Inter-vendor Certificate Format Incompatibility

Although X.509 is the de-facto certificate standard, vendors implement proprietary field extensions, differing key lengths, and custom renewal hooks. Entrust warns that integrating heterogeneous certificate authorities becomes exponentially complex as device fleets scale. The SSL Store notes that misaligned trust chains often force operators to run parallel PKI stacks or rely on insecure manual enrolment. GlobalSign forecasts 55.7 billion devices needing certificate management by 2025, underscoring the scale mismatch facing current reconciliation tools. Keyfactor and Unikie offer an abstraction layer to bridge edge certificates into unified dashboards, yet uptake depends on supplier cooperation. Without concerted standardization, integration costs keep rising and slow down multi-vendor rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Anchor Enterprise Deployments

Solutions held a 62.75% stake of IoT IAM market share in 2024, confirming enterprise appetite for all-in-one platforms that bundle authentication, authorization, and device provisioning. Vendors enrich these suites with AI-driven anomaly scoring and connector libraries for OT protocols, allowing plants to secure Human Machine Interfaces and PLCs under a single policy grid. The IoT identity access management market size attached to services is forecast to expand at a 21.54% CAGR as organizations outsource configuration, policy tuning, and incident response to certified partners. Professional services gain momentum wherever certificate renewal backlogs threaten uptime, while managed service providers fold identity orchestration into connectivity contracts. As zero-trust maturity rises, many firms shift from DIY patchworks to subscription-based operations centres that guarantee compliance reporting.

Demand for solutions in the IoT IAM market persists because regulators and insurers prefer evidence of integrated policy engines over ad-hoc toolchains. Platform roadmaps emphasise Software Bill of Materials correlation, automated risk scoring, and out-of-the-box support for SBOM ingestion APIs. Meanwhile, service revenues track the widening skills gap; consultancies package readiness assessments, brown-field discovery exercises, and phased migration blueprints for legacy PLC clusters. Telecommunications operators exploit their network vantage point to resell overlay identity monitoring, converting bandwidth deals into recurring security bundles.

By Deployment Mode: Cloud Dominance Meets Hybrid Innovation

Cloud options represented 70.54% of 2024 deployments, validating the operational appeal of instant elasticity, built-in redundancy, and usage-based cost curves. Multitenant control planes push policy updates to millions of endpoints in near real-time, a capability on-premise stacks cannot match without hefty capex. The hybrid model, however, projects a 22.67% CAGR through 2030 because factories need local enforcement nodes to maintain determinism and air-gap isolation. The IoT IAM market size associated with hybrid rollouts widens as security architects deploy cloud dashboards above edge appliances that continue authorizing traffic during WAN disruptions.

Edge nodes host local policy caches, certificate authorities, and micro-segmentation engines, then replicate state to the cloud for analytics and governance. Chip-embedded secure elements further blur the line by pushing root-of-trust down to device silicon while streaming telemetry up to SaaS portals, reinforcing trends in the IoT identity access management market. On-premise footprints linger in defense, energy, and tightly regulated utilities that must meet data-sovereignty rules. Even here, the gravitational pull of cloud manifests through private-cloud instantiations of previously appliance-bound software.

By Organization Size: Enterprise Leadership Yields to SME Acceleration

Large enterprises commanded 58.43% of spending in 2024 as they possessed the integration bandwidth to retrofit identity to sprawling control networks. Their budgets cover red-team exercises, certificate automation, and zero-trust proofs-of-concept across global sites. Yet SMEs clock a 21.96% CAGR, signifying democratized access to enterprise-grade features via freemium SaaS tiers and telco bundles. Managed service subscriptions slash up-front costs, while pay-as-you-grow licensing aligns with variable production schedules. The IoT IAM market size attributed to SMEs rises sharply once connectivity providers merge data plans with embedded certificate rotation and compliance dashboards.

Research across US manufacturing SMEs shows the return on investment of secure IIoT projects exceeds initial outlay, turning IAM from cost centre to profit lever, boosting adoption in the IoT identity access management market. Public grants and industry clusters subsidize pilot projects, while sector associations publish playbooks containing template risk assessments. As a result, smaller firms no longer delay deployments on grounds of complexity; instead, they negotiate outcome-based contracts that transfer residual risk to service providers.

By Industry Vertical: Manufacturing Maturity Drives Healthcare Innovation

Manufacturing captured 24.64% of the IoT identity access management market share in 2024, backed by extensive zero-trust rollouts in programmable logic controllers. Machine builders integrate secure boot, signed firmware, and identity brokers into new generations of equipment, enabling continuous attestation during production shifts. Healthcare outpaces every other sector with a 24.01% CAGR because the FDA now requires pre-market cyber-risk documentation that hinges on robust device authentication. The IoT IAM market size dedicated to medical devices therefore expands as OEMs weave mutual TLS, signed SBOMs, and remote-revoke hooks into infusion pumps and imaging scanners.

Energy utilities embrace IAM to shield smart meters and substation gear, while logistics fleets deploy role-based APIs for telematics boxes, ensuring drivers access only vehicle-specific data. Smart home adoption spikes under the Matter framework, which mandates baseline encryption and passkey support for every certified device. Vertical use-cases converge on a common motif: mapping every asset to a unique, immutable identity, then enforcing least privilege in real time.

Geography Analysis

In 2024, North America accounted for 38.54% of the IoT identity access management market revenue, buoyed by mature zero-trust postures, NIST guidance, and favourable insurance discounts for verified identity frameworks. Enterprises in the United States typically pair cloud IAM back ends with on-premise industrial gateways, and federal procurement clauses ignite continuous demand in defense and healthcare. The region also hosts most venture-funded disruptors, accelerating feature velocity and M&A activity.

Asia-Pacific exhibits the steepest 24.65% CAGR, as Japanese conglomerates KDDI and NEC combine telco backbone assets with cybersecurity platforms to protect supply chains. Government programs such as Japan’s JC-STAR labeling system label consumer IoT security posture, nudging buyers toward certified identity-rich devices and further strengthening the IoT identity access management market. China’s build-out of AIoT solutions for the Osaka Expo 2025 demonstrates the region’s commitment to integrating machine learning with embedded security. Indian manufacturers sprint to retrofit plants under Industry 4.0 subsidies, leveraging local systems integrators that bundle connectivity and certificate rotation.

Europe posts steady gains anchored in regulatory harmonization under the Cyber Resilience Act, which makes SBOM and vulnerability disclosure mandatory, supporting growth in the IoT IAM market. Industrial hubs in Germany and the Nordics emphasize IEC 62443 alignment, translating into predictable IAM rollouts. Meanwhile, the Middle East and Africa capitalize on greenfield infrastructure, deploying 5G-enabled smart cities where identity protocols are embedded from day one. Latin America benefits from multilateral financing that stipulates cybersecurity milestones, yet limited OT-security talent tempers adoption curves. Altogether, regional patterns underscore that policy, telco strategy, and manufacturing maturity jointly steer IAM penetration.

Competitive Landscape

The marketplace in the IoT identity access management market remains unconcentrated; no vendor exceeds a single-digit share, giving rise to specialized niche providers. Xage Security joined forces with Darktrace to fuse zero-trust gateways and AI anomaly detection, targeting critical infrastructure operators that need hands-off tuning. DigiCert’s Device Trust Manager stretches certificate issuance from factory floor to retirement, bridging compliance with EU and US medical regulations. Platform differentiation leans on integrated SBOM analytics, post-quantum crypto readiness, and chipset-level secure elements.

Strategic acquisitions accelerate capability expansion in the IoT IAM market. Armis acquired Silk Security for USD 150 million to ingest risk prioritization algorithms into its asset-centric platform, aiming to move up-market into board-level reporting. Microsoft earlier absorbed CyberX to fortify Azure IoT security stacks, a precursor to its broader zero-trust ecosystem. SEALSQ builds a USD 93 million pipeline for quantum-safe microcontrollers, betting that regulators will mandate crypto-agility before the decade ends.

Network operators leverage their unique vantage point: Aeris delivers IoT Watchtower as an in-band security filter, while Verizon meshes 5G slices with identity postures. Cloud natives extend Secure Access Service Edge (SASE) to OT; Cato Networks’ first SASE-native IoT module exemplifies the trend. Over 2025-2030, winning vendors will likely pair hardware roots of trust with SaaS policy orchestration, backed by analytics pipelines able to map SBOM findings to compensating controls in minutes.

IoT Identity Access Management Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

International Business Machines Corporation

Oracle Corporation

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nozomi Networks delivered the first embedded security sensor for industrial PLCs, adding AI anomaly detection at the control layer.

- May 2025: KDDI and NEC launched a joint cybersecurity business to shield Japanese critical infrastructure and supply chains.

- March 2025: G+D and AWS deepened collaboration on cloud-based eSIM offerings, boosting identity provisioning capabilities for massive IoT.

- March 2025: Honeywell and Verizon Business integrated Verizon 5G into Honeywell smart meters to enable remote access and improved grid reliability

Global IoT Identity Access Management Market Report Scope

| Solutions |

| Services |

| Cloud |

| On-premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Manufacturing |

| Healthcare |

| Energy and Utilities |

| Transportation and Logistics |

| Smart Home and Consumer Electronics |

| Government and Defence |

| Other Industry Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-premise | |||

| Hybrid | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | Manufacturing | ||

| Healthcare | |||

| Energy and Utilities | |||

| Transportation and Logistics | |||

| Smart Home and Consumer Electronics | |||

| Government and Defence | |||

| Other Industry Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is driving the rapid growth of the IoT identity access management market?

Mandatory SBOM regulations, zero-trust adoption in industrial settings, and telco security-as-a-service bundles are accelerating spend, producing a 20.97% CAGR through 2030.

Which deployment model dominates IoT identity access management today?

Cloud accounts for 70.54% of deployments owing to scalability and lower capex, although hybrid architectures are expanding at a 22.67% CAGR as factories seek local enforcement.

Why is healthcare the fastest-growing vertical?

FDA cybersecurity guidance now requires device authentication and SBOM submission, pushing healthcare IAM spending to a 24.01% CAGR.

How do cyber-insurance premiums affect IAM adoption?

Insurers increasingly demand documented identity controls; firms that comply secure lower premiums, making IAM investment financially attractive.

What role do telcos play in the IoT IAM ecosystem?

Operators bundle managed identity services with connectivity, exemplified by Verizon’s Sensor Insights and Aeris’s IoT Watchtower, enabling SMEs to deploy secure IoT quickly.

Are legacy PLCs a barrier to IoT IAM rollouts?

Yes; hard-coded credentials in older PLCs create vulnerabilities and slow modernization, subtracting up to 2.1% from the forecast CAGR.

Page last updated on: