Artificial Intelligence Of Things (AIoT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

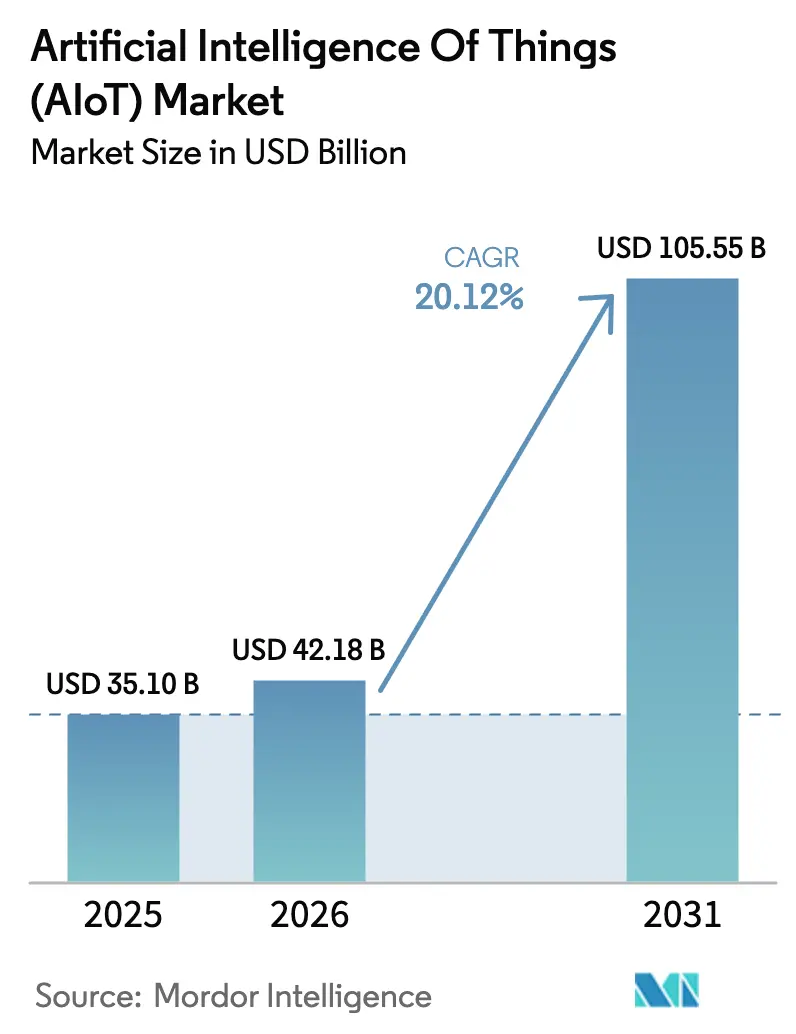

| Market Size (2026) | USD 42.18 Billion |

| Market Size (2031) | USD 105.55 Billion |

| Growth Rate (2026 - 2031) | 20.12% CAGR |

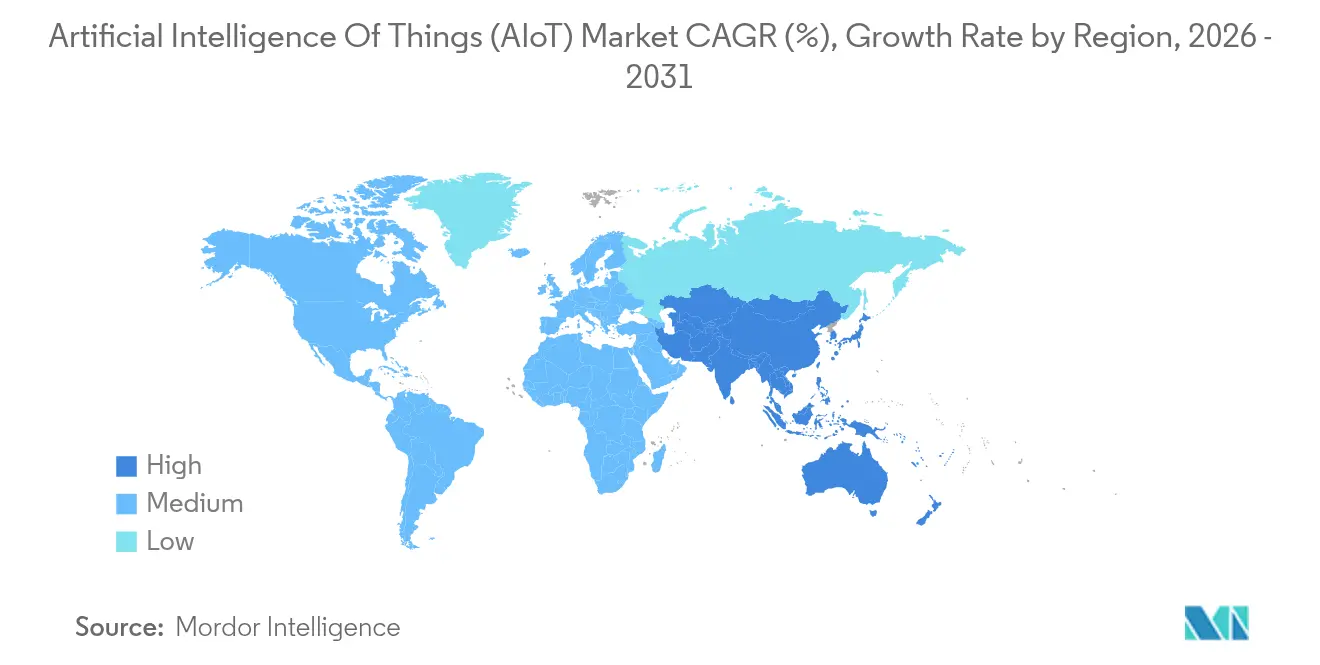

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

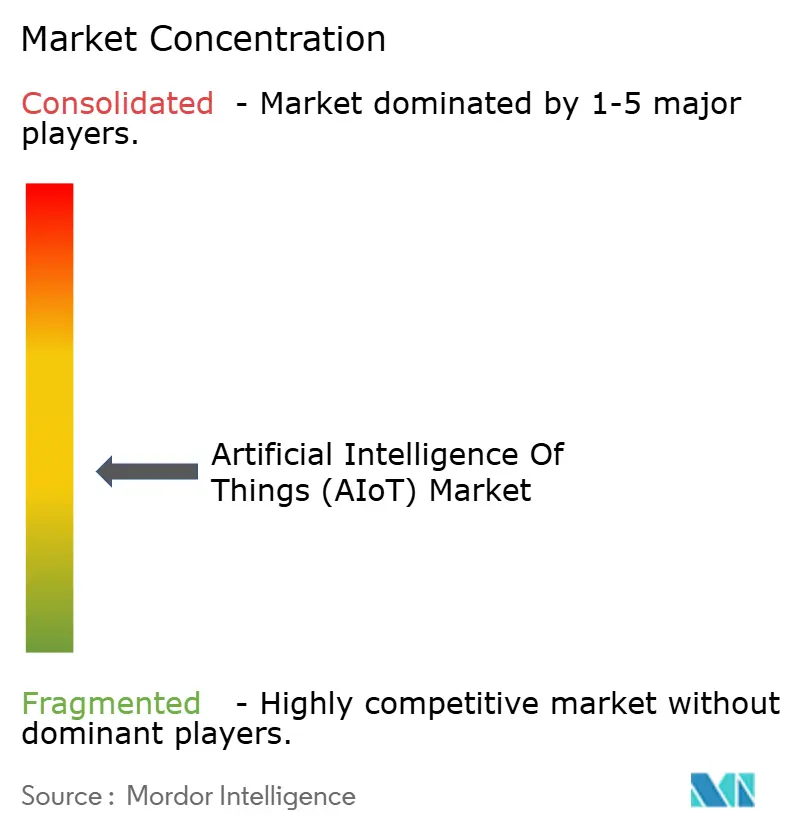

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence Of Things (AIoT) Market Analysis by Mordor Intelligence

Artificial Intelligence of Things market size in 2026 is estimated at USD 42.18 billion, growing from 2025 value of USD 35.10 billion with 2031 projections showing USD 105.55 billion, growing at 20.12% CAGR over 2026-2031. Rapid convergence of AI models with sensor-rich IoT endpoints is shifting deployments from reactive monitoring to autonomous, edge-native intelligence. Volume manufacturing of low-cost AI chipsets, hyperscaler investment in AI-centric cloud services, and rising enterprise demand for predictive operations continue to expand addressable use cases. Semiconductor leaders such as NVIDIA recorded 78% year-over-year revenue growth to USD 39.3 billion in Q4 2025 on the back of AI infrastructure demand. Integration complexity is simultaneously creating a sizable services opportunity as organizations seek specialist partners to knit AI algorithms, networking, and domain workflows into unified solutions. Regulatory frameworks such as the EU AI Act are driving “privacy-by-design” architectures that favor distributed processing and standards-based interoperability.

Key Report Takeaways

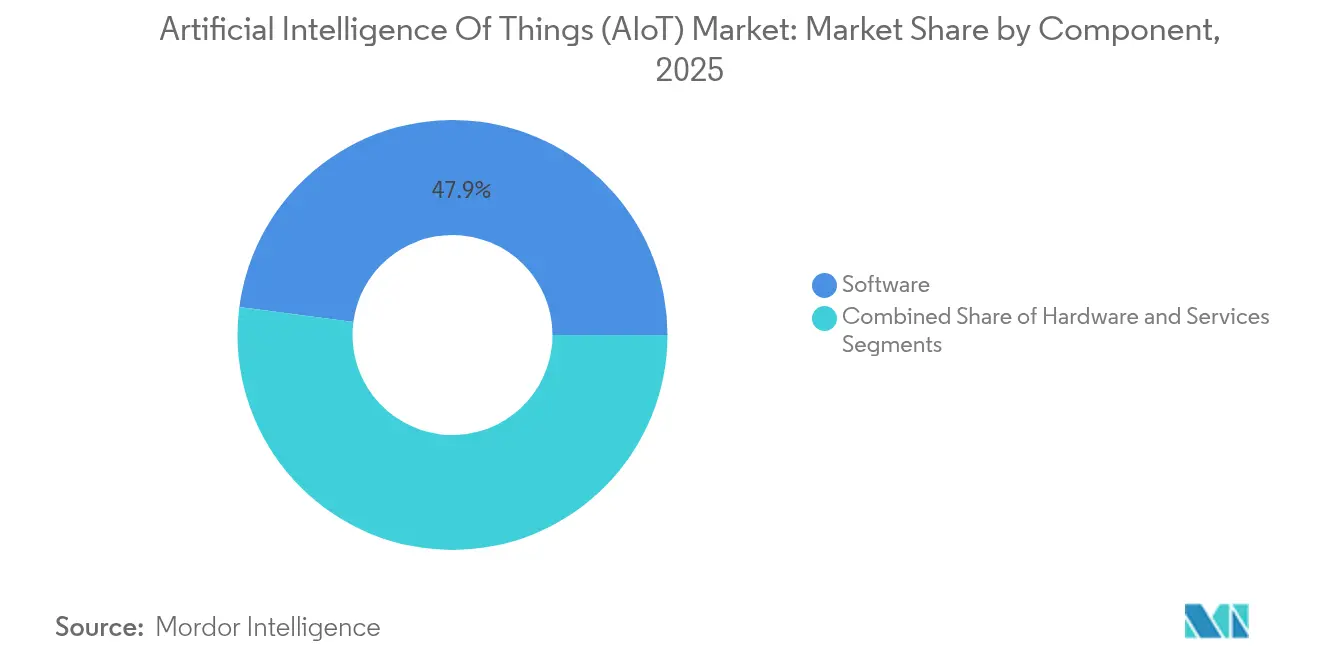

- By component, software platforms led with 47.92% revenue share in 2025; services are projected to expand at a 31.60% CAGR to 2031.

- By deployment model, cloud-based solutions held 56.84% of the Artificial Intelligence of Things market share in 2025, while edge implementations are forecast to grow at 37.45% CAGR through 2031.

- By application, video surveillance maintained 24.10% share of the Artificial Intelligence of Things market size in 2025; autonomous mobility is advancing at a 42.60% CAGR to 2031.

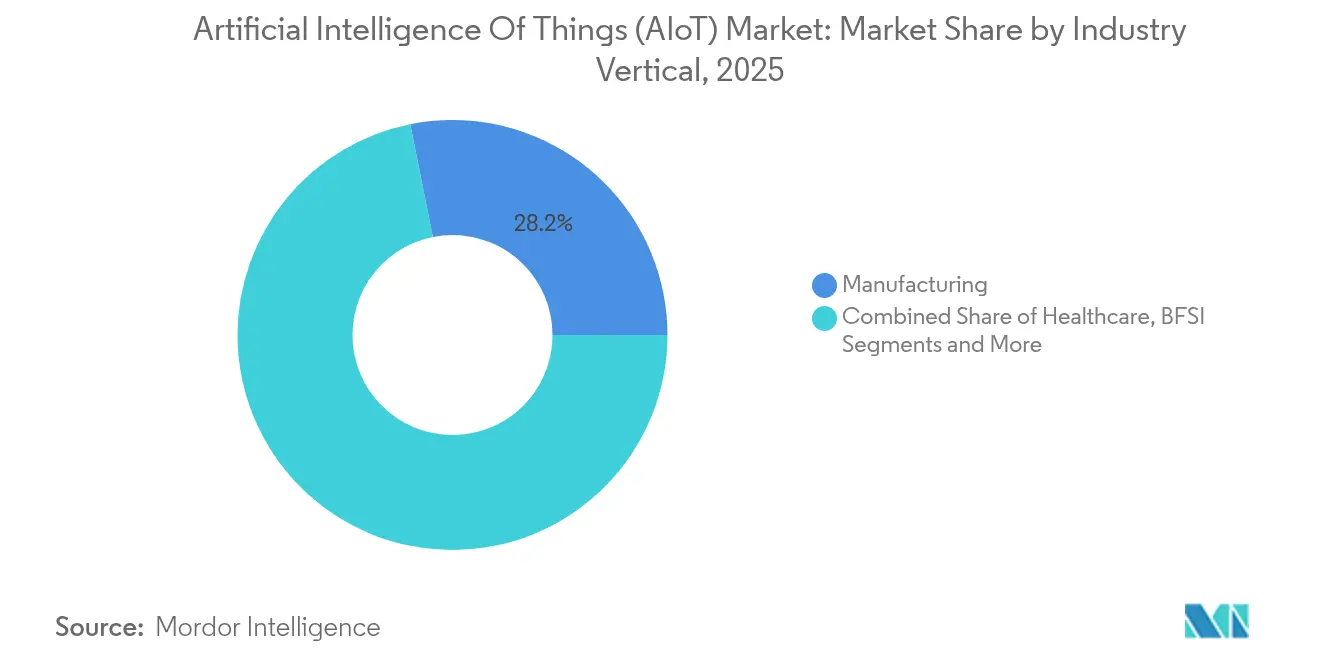

- By industry vertical, manufacturing accounted for 28.15% of 2025 revenue, whereas healthcare is the fastest-growing segment at 35.40% CAGR.

- By technology stack, machine learning represented 40.72% share in 2025; natural language processing records the strongest growth at 28.95% CAGR.

- By geography, North America commanded 42.10% revenue share in 2025; APAC is projected to rise at a 27.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Intelligence Of Things (AIoT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge-AI hardware cost declines accelerate adoption | +4.2% | Global, Asia-Pacific manufacturing leads | Medium term (2-4 years) |

| Roll-out of 5G / 6G networks enabling ultra-low latency | +3.8% | North America and EU early, Asia-Pacific mass | Long term (≥ 4 years) |

| Growing enterprise spend on predictive-maintenance AIoT suites | +3.1% | Germany, China, United States | Short term (≤ 2 years) |

| AIoT-ready chipsets embedded in consumer devices | +2.9% | North America, China | Medium term (2-4 years) |

| Low-Earth-Orbit satellite IoT links unlock remote assets | +1.8% | Australia, Canada, Brazil | Long term (≥ 4 years) |

| Government-backed smart-city programs fuel infrastructure modernisation | +1.5% | China, India, GCC states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Edge-AI hardware cost declines accelerate adoption

Ongoing price reductions in edge inference silicon are reshaping cost–benefit equations across industrial and consumer deployments. Intel’s 2024 partnership with Qualcomm to co-engineer wireless AI modules exemplifies cross-vendor moves that compress bill-of-materials while boosting on-device processing efficiency.[1]Qualcomm Incorporated, “Qualcomm–Intel Wireless AI Collaboration,” qualcomm.com Manufacturers are now able to execute complex predictive algorithms locally, lowering cloud compute fees and avoiding latency-induced downtime.

Roll-out of 5G / 6G networks enabling ultra-low latency

Telecom operators are layering AI-optimized transport slices onto 5G cores and launching initial 6G research beds, creating the bandwidth and deterministic latency critical for autonomous mobility and remote robotics. Cisco’s AI-powered predictive network automation roadmap underscores how transport upgrades and network intelligence combine to support real-time AIoT workloads.[2]Cisco Systems, “Cisco Networking Cloud and Nexus HyperFabric,” cisco.com

Growing enterprise spend on predictive-maintenance AIoT suites

Industrial majors are scaling sensor networks and analytics bundles to cut unplanned shutdowns. Honeywell’s collaboration with Google Cloud to build autonomous plant agents demonstrates the ROI narrative now driving board-level funding for AI-enabled maintenance programs.[3]Honeywell International, “Honeywell and Google Cloud Expand AI Partnership,” honeywell.com

AIoT-ready chipsets embedded in consumer devices

Device makers increasingly integrate dedicated inference engines into wearables, smart appliances, and in-vehicle infotainment. Qualcomm and Palantir extended their edge analytics partnership in March 2025 to deliver lightweight, on-device AI pipelines that reduce backhaul traffic and preserve user privacy.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of AIoT-skilled systems integrators | –2.8% | Emerging markets, mid-tier cities | Short term (≤ 2 years) |

| Fragmented edge-cloud standards hinder interoperability | –2.1% | Global multi-vendor sites | Medium term (2-4 years) |

| Rising privacy-preserving-AI compliance costs | –1.9% | EU first, extending to APAC | Long term (≥ 4 years) |

| EU AI Act compliance raises documentation overhead | –1.5% | Europe, exporters to EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of AIoT-skilled systems integrators

Deployments require rare combinations of ML engineering, industrial protocols, and domain know-how. Limited talent pools inflate project costs and elongate roll-outs, especially for mid-market manufacturers outside major tech hubs.

Fragmented edge-cloud standards hinder interoperability

ISO/IEC 27402 offers baseline security rules, yet comprehensive interoperability guidance remains patchy. Enterprises often lock into single-vendor stacks early, increasing switching costs and dampening ecosystem experimentation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software platforms drive integration complexity

Software accounted for 47.92% revenue in 2025, underpinning orchestration, AI model management, and data integration across distributed assets. Services are tracking a 31.60% CAGR as enterprises outsource end-to-end solution design to bridge IT-OT silos. Hardware price deflation is commoditizing edge nodes, pushing differentiation up-stack into software value layers. The Artificial Intelligence of Things market size for software is expected to widen as algorithm marketplaces and domain-specific model libraries scale commercially. Services growth mirrors client demand for bespoke connectors, security hardening, and lifecycle governance.

By Deployment Model: Edge computing gains strategic priority

Cloud architectures retained 56.84% of 2025 spending, yet edge deployments lead growth at 37.45% CAGR as latency-sensitive workloads migrate nearer to machines. Enterprises are adopting hybrid blueprints that dynamically split inference between local and central compute based on bandwidth, privacy, and energy constraints. Cisco’s Nexus HyperFabric clusters exemplify converged designs that house GPUs and high-speed Ethernet in the same rack, giving customers optionality to shift workloads without re-architecting estates. This flexibility is steering procurement roadmaps toward composable, vendor-agnostic stacks that decouple data gravity from algorithm performance.

By Application: Autonomous mobility reshapes transportation intelligence

Video surveillance held 24.10% revenue in 2025, benefiting from mature camera ecosystems and incremental AI add-ons. Autonomous mobility posts the fastest expansion at 42.60% CAGR, propelled by regulatory pilots and falling LiDAR costs. Waymo’s scaled robo-taxi operations and Tesla’s in-house full-self-driving stack reveal how mileage accumulation accelerates model refinement. Logistics fleets and municipal transit agencies are extending proof-of-concepts into full production, embedding edge inference units that fuse sensor data for sub-millisecond path planning.

By Industry Vertical: Healthcare digitization accelerates AIoT adoption

Manufacturing contributed 28.15% of 2025 turnover through predictive maintenance, quality analytics, and adaptive robotics. Healthcare, advancing at 35.40% CAGR, is leveraging remote patient monitoring, AI-augmented diagnostics, and hospital asset tracking to alleviate clinician workloads and improve outcomes. Regulatory approvals for software-as-a-medical-device (SaMD) and reimbursement for tele-cardiology services are reinforcing capital allocation into connected care platforms across the Artificial Intelligence of Things market. Energy, utilities, and agriculture sectors continue to introduce sensor-driven optimisation but trail healthcare in relative growth momentum.

By Technology Stack: Natural language processing enables human-centric interfaces

Machine learning dominated 40.72% of the 2025 stack, underpinning anomaly detection and optimisation logic. Natural language processing now registers the strongest CAGR at 28.95% as conversational interfaces and voice-activated controls democratise access to complex industrial systems. Cisco embedded NLP into network management consoles to simplify policy configuration, allowing operations staff to pose plain-English queries rather than scripting CLI commands. Computer vision and reinforcement learning also deepen penetration in autonomous inspection drones and adaptive supply-chain routing respectively.

Geography Analysis

North America led with 42.10% revenue in 2025, supported by advanced connectivity, a dense venture capital base, and federal AI research incentives. United States manufacturers deploy factory-floor analytics to offset labour shortages, while Canada’s privacy regulations drive early adoption of federated-learning frameworks in healthcare. Mexico’s maquila segment is integrating edge AI nodes to streamline cross-border logistics flows.

APAC is the fastest-growing region at 27.85% CAGR to 2031. China’s extensive industrial parks and Belt and Road trade corridors require predictive visibility across multimodal freight networks, spurring bulk procurement of embedded AI gateways. Japan scales service-robot fleets to assist an ageing population, pairing computer vision with dexterous manipulators in elder-care facilities. India’s Digital India program fast-tracks smart-city tenders that bundle AI traffic management, solid-waste analytics, and e-health kiosks under unified command platforms.

Europe balances innovation with stringent governance. The EU AI Act imposes transparency and risk-management mandates that encourage secure-by-design tooling. Germany’s automotive OEMs deploy GPU-rich edge clusters on shop floors for real-time welding inspection, while the United Kingdom channels industrial strategy funds into AIoT cyber-resilience hubs. Middle East oil producers digitalise upstream assets using satellite backhaul and edge vision processing to improve worker safety and trim carbon footprints.

Competitive Landscape

Competitive intensity remains moderate. Cloud hyperscalers—AWS, Microsoft, Google—bundle AI, device orchestration, and ingestion pipelines into subscription packages, driving platform stickiness. NVIDIA dominates accelerator silicon, prompting alliance strategies among networking and server vendors; Cisco’s Ethernet-based Spectrum-X fabric integrates NVIDIA’s Silicon One ASICs to deliver deterministic AI cluster throughput. Industrial incumbents such as Siemens and GE Digital embed vertical expertise into domain-focused offerings that compete less on raw compute and more on workflow optimisation.

Partnership ecosystems are replacing bilateral vendor lock-ins. SAP embedded generative AI into 50% of 2024 cloud orders, using its ERP install base to propagate AIoT features like asset-centric digital twins and predictive spare-parts logistics. Semiconductor players court software partners to differentiate beyond frames-per-second benchmarks, as shown by STMicroelectronics and Qualcomm co-developing wireless AI reference designs for battery-constrained endpoints. Start-ups target niche gaps: edge-native privacy engines, ultra-low-power inference kernels, or vertical-specific compliance tooling. ISO/IEC 42001 governance certification creates an on-ramp for specialist auditors that help suppliers align lifecycle processes with regulatory expectations.

Artificial Intelligence Of Things (AIoT) Industry Leaders

Amazon Web Services

Microsoft Corp.

Google LLC

IBM Corp.

Cisco Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Qualcomm and Palantir extended their collaboration to fuse ontology-based analytics with edge System-on-Chip platforms for factory automation.

- June 2025: Cisco launched AI Canvas and Nexus Dashboard upgrades to streamline secure AIoT fabric deployment across retail and healthcare campuses.

- October 2024: STMicroelectronics and Qualcomm entered a wireless IoT alliance integrating Qualcomm RF IP with ST’s STM32 microcontrollers for industrial and consumer devices.

- August 2024: Advantech and Momenta’s AIoT Ecosystem Fund invested in Axiom Cloud to scale refrigeration digital twins that lower energy consumption in grocery chains.

Global Artificial Intelligence Of Things (AIoT) Market Report Scope

AIoT integrates the connectivity offered by the Internet of Things (IoT) with the insights derived from Artificial Intelligence (AI). This innovative technology relies on incorporating Artificial Intelligence within the IoT framework.

The study tracks the revenue accrued through the sale of Artificial Intelligence of Things (AIoT) solutions and services by various players in the global market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. It further analyses the macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The Artificial Intelligence of Things (AIoT) Market is segmented by component (software, services), by application (video surveillance, inventory management, predictive maintenance, supply chain management, others), by deployment (cloud-based AIoT, edge AIoT), by industry vertical (retail, BFSI, agriculture, healthcare, manufacturing, transportation & logistics, government & defense, others), and by geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments

| Hardware |

| Software |

| Services |

| Cloud-based AIoT |

| Edge AIoT |

| Hybrid AI-Edge |

| Video Surveillance and Security |

| Predictive Maintenance |

| Inventory and Warehouse Management |

| Supply-Chain and Fleet Optimization |

| Energy and Utilities Management |

| Smart Buildings and Cities |

| Customer Experience and Personalization |

| Autonomous Mobility |

| Manufacturing |

| Healthcare |

| Retail and E-commerce |

| BFSI |

| Transportation and Logistics |

| Agriculture |

| Energy and Utilities |

| Smart Cities and Government |

| Aerospace and Defense |

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Computer Vision |

| Reinforcement Learning |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Model | Cloud-based AIoT | ||

| Edge AIoT | |||

| Hybrid AI-Edge | |||

| By Application | Video Surveillance and Security | ||

| Predictive Maintenance | |||

| Inventory and Warehouse Management | |||

| Supply-Chain and Fleet Optimization | |||

| Energy and Utilities Management | |||

| Smart Buildings and Cities | |||

| Customer Experience and Personalization | |||

| Autonomous Mobility | |||

| By Industry Vertical | Manufacturing | ||

| Healthcare | |||

| Retail and E-commerce | |||

| BFSI | |||

| Transportation and Logistics | |||

| Agriculture | |||

| Energy and Utilities | |||

| Smart Cities and Government | |||

| Aerospace and Defense | |||

| By Technology Stack | Machine Learning | ||

| Deep Learning | |||

| Natural Language Processing | |||

| Computer Vision | |||

| Reinforcement Learning | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Artificial Intelligence of Things market?

The market is valued at USD 42.18 billion in 2026 and is projected to reach USD 105.55 billion by 2031, reflecting a 20.12% CAGR.

Which component segment is growing fastest?

Services are expanding at 31.60% CAGR through 2031 as enterprises seek expert partners for complex integration work.

Why is edge deployment gaining traction over cloud-only models?

Edge implementations reduce latency, address data-sovereignty mandates, and cut bandwidth fees, resulting in a 37.45% CAGR outlook for edge architectures.

Which application area shows the highest growth potential?

Autonomous mobility leads with 42.60% CAGR due to rapid advances in computer vision, sensor fusion, and regulatory pilots in urban transport.

Page last updated on: