Industrial Internet Of Things (IIoT) Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.36 Billion |

| Market Size (2031) | USD 33.26 Billion |

| Growth Rate (2026 - 2031) | 18.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Internet Of Things (IIoT) Security Market Analysis by Mordor Intelligence

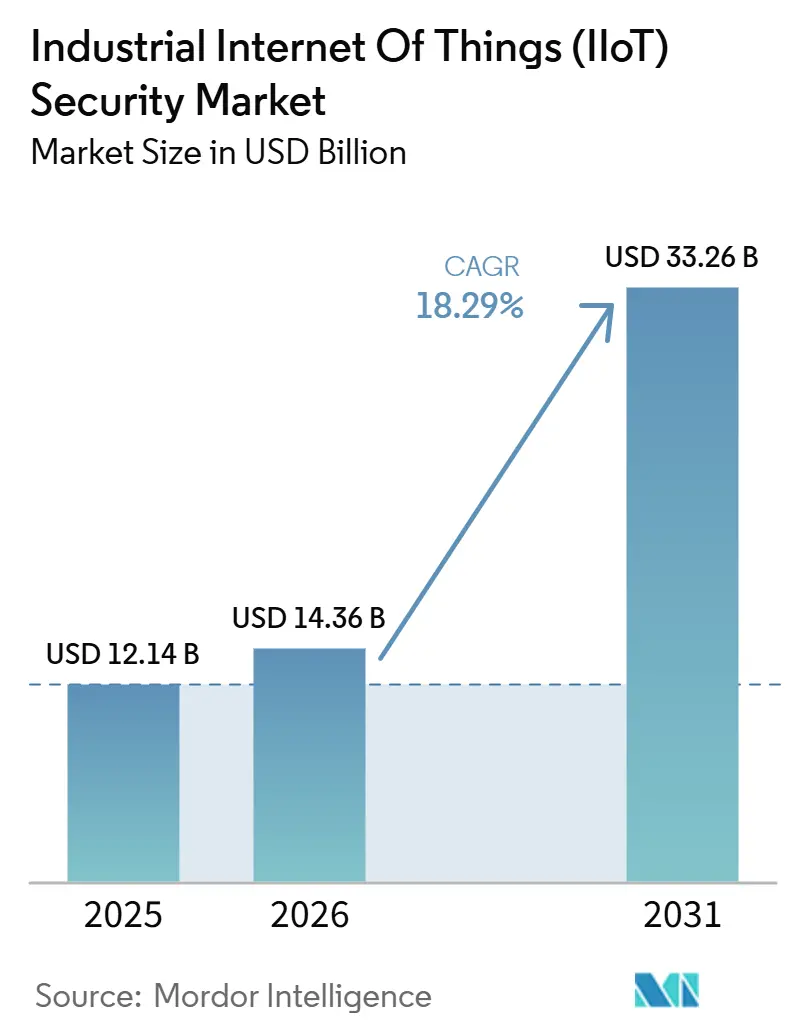

The industrial internet of things (IIoT) security market size is projected to be USD 12.14 billion in 2025, USD 14.36 billion in 2026, and reach USD 33.26 billion by 2031, growing at a CAGR of 18.29% from 2026 to 2031. The cybersecurity for industrial IoT market is moving higher because industrial operators are connecting more plant assets, remote access points, and cloud-linked control layers than they did even a year ago. Ransomware pressure on manufacturers, utilities, and transport operators has made cyber risk a direct operations issue, which is pushing boards to treat protection spending as part of resilience planning rather than only an IT budget line. Regulatory pressure in North America, Europe, and parts of Asia is also making monitoring, segmentation, and incident readiness harder to defer, especially for critical infrastructure owners. At the same time, the cybersecurity for the industrial IoT market is shifting from product-led buying toward broader platform and service contracts because many operators want continuous visibility, threat detection, and response support in one model. This leaves the strongest opening with vendors that can connect OT intelligence, compliance support, and managed protection into a single offering that fits both legacy sites and newer digital plants.

Key Report Takeaways

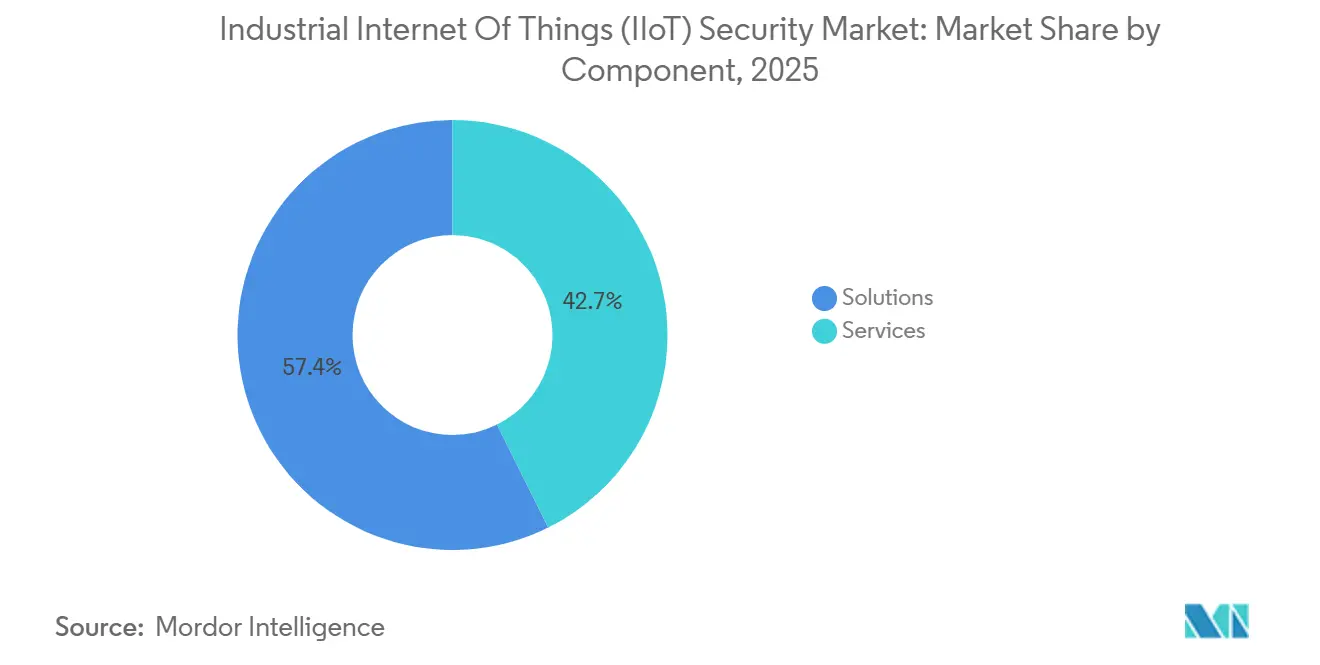

- By component, solutions held 57.35% of revenue in 2025 in the industrial internet of things (IIoT) security market, while services are projected to expand at a 20.21% CAGR through 2031.

- By security type, network security led with 41.69% share in 2025, while cloud security is projected to grow at a 21.26% CAGR through 2031.

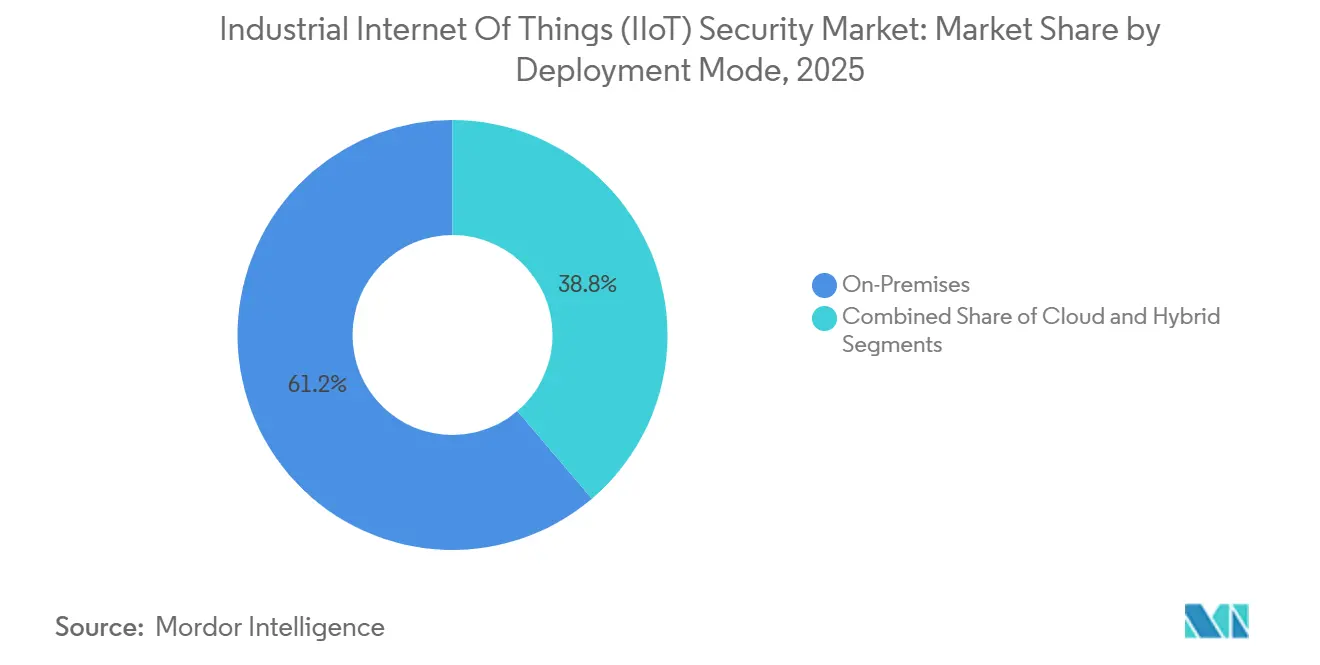

- By deployment mode, on-premises accounted for 61.23% of revenue in 2025, while cloud deployments are expected to expand at a 22.63% CAGR through 2031.

- By end-user industry, industrial manufacturing held 31.64% share in 2025, while healthcare and life sciences are projected to record the fastest CAGR at 21.37% through 2031.

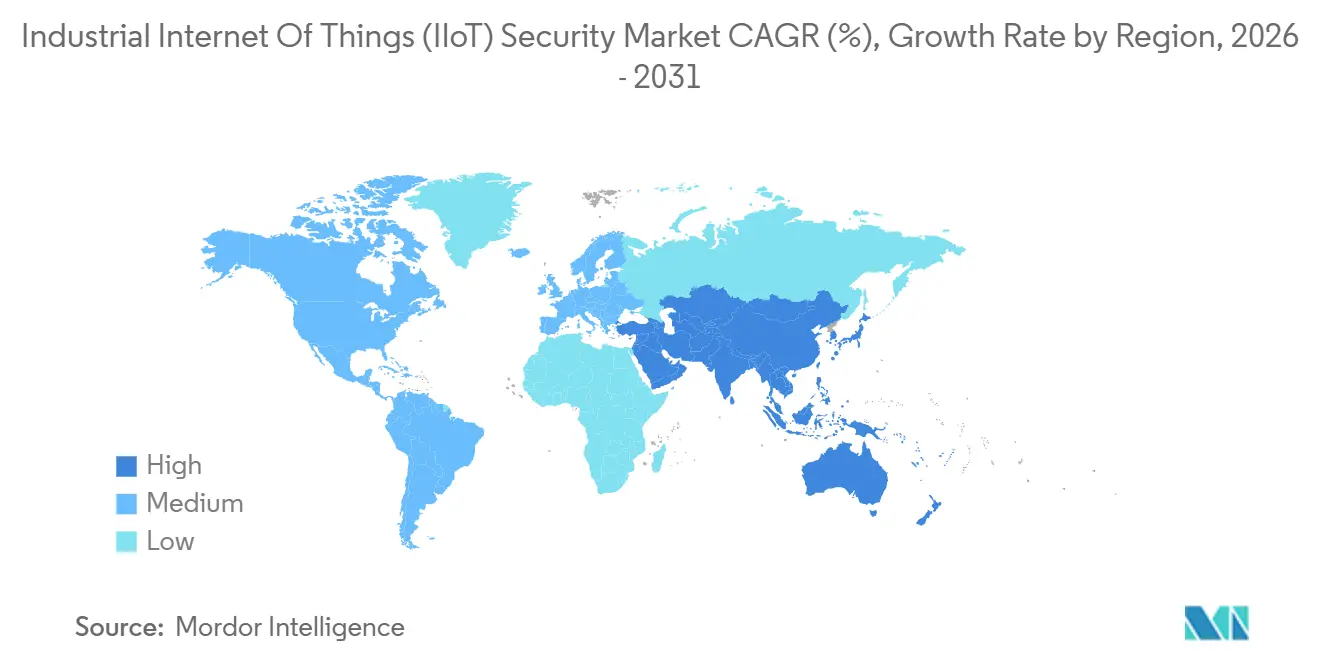

- By geography, North America held 38.25% of the industrial internet of things (IIoT) security market in 2025, while Asia-Pacific is projected to record the fastest CAGR at 23.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Internet Of Things (IIoT) Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IT and OT Convergence Expanding the Attack Surface | +5.2% | Global | Short term (≤ 2 years) |

| Rising IIoT Device Density Across Connected Plants | +4.5% | Global, with highest concentration in China, India, and ASEAN | Medium term (2-4 years) |

| Regulatory Pressure on Critical Infrastructure Security | +3.8% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Cyber Insurance Underwriting Requiring Stronger OT Controls | +2.1% | North America, EU | Short term (≤ 2 years) |

| Securing Vendor Remote Access to Industrial Assets | +1.6% | Global | Short term (≤ 2 years) |

| Asset Discovery Gaps Created by Unmanaged Edge Sensors | +1.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IT and OT Convergence Expanding the Attack Surface

The industrial internet of things (IIoT) security market is being pushed higher by the simple fact that most industrial environments no longer keep enterprise systems and plant systems fully separate. Palo Alto Networks, Siemens, and Idaho National Laboratory documented 20 million unique industrial devices exposed to the public internet in 2024, which shows how much of the operating environment is now reachable from outside the plant boundary.[1]Palo Alto Networks, “The Cartography Of Risk, Operational Technology And The Public Internet,” Palo Alto Networks, PALOALTONETWORKS.COM. The same research found that adversaries often remained in view for extended periods before active exploitation, which means monitoring gaps now matter as much as perimeter controls in the industrial internet of things (IIoT) security market. Buyers are therefore putting more weight on cross-domain visibility, identity controls, and segmentation policies that can follow assets across IT systems, OT zones, and hybrid cloud links. This is also changing purchase logic because operators increasingly prefer unified protection layers that can track movement from office networks into engineering workstations and then toward control assets. As a result, the industrial internet of things (IIoT) security market is favoring vendors that can show protocol awareness, rapid asset mapping, and continuous threat monitoring in one operating model.

Rising IIoT Device Density Across Connected Plants

The industrial internet of things (IIoT) security market is also benefiting from the fast spread of sensors, gateways, and connected edge devices across production environments. Palo Alto Networks and Idaho National Laboratory recorded more than 110 million observations of OT devices exposed to the internet in 2024, which reflected how quickly connected assets were accumulating across manufacturing, energy, and utilities. This growing device base creates persistent inventory gaps because many assets are added close to operations, while central IT and security teams may not update visibility tools at the same pace. TXOne Networks reported that 60% of organizations experienced at least 1 OT security incident in 2025, and 88% increased OT security spending by more than 10%, which shows how device sprawl is turning directly into buying urgency for the industrial internet of things (IIoT) security market. Rockwell Automation also found in 2025 that 38% of manufacturers planned to use existing operational data to improve cybersecurity, which suggests that asset intelligence is becoming a starting point for defense design rather than a later improvement step. The result is that the industrial internet of things (IIoT) security market is moving beyond isolated point products and toward broader discovery, monitoring, and response tools that can keep pace with changing plant asset maps.

Regulatory Pressure on Critical Infrastructure Security

Regulatory change is becoming a more direct spending trigger for the industrial internet of things (IIoT) security market, especially where industrial downtime can affect public safety, energy reliability, or essential services. In the United States, FERC approved Reliability Standard CIP-015-1 in July 2025, which extended mandatory internal network security monitoring requirements to additional access and control systems outside earlier perimeter assumptions.[2]U.S. Federal Energy Regulatory Commission, “Approval Of CIP-015-1, Cyber Security, Internal Network Security Monitoring,” Federal Register, GOVINFO.GOV. FERC also moved in September 2025 to expand supply chain-related security obligations to a broader class of cyber assets, which enlarged the compliance perimeter for bulk electric system operators. In Japan, METI published OT Security Guidelines for semiconductor device factories in 2025, linking plant security practice more closely to recognized frameworks and procurement expectations. SANS reported in 2025 that regulated sites suffered fewer financial and safety impacts from cyber incidents than unregulated peers, which helps explain why compliance is now being treated as a practical risk reduction tool inside the industrial internet of things (IIoT) security market. This makes regulatory alignment a commercial driver because industrial owners are no longer only buying to satisfy audits; they are buying to reduce operational disruption and recovery costs.

Cyber Insurance Underwriting Requiring Stronger OT Controls

Cyber insurance is adding another financial reason for asset owners to strengthen OT protections, and that is lifting activity in the industrial internet of things (IIoT) security market. Dragos and Marsh McLennan estimated potential global OT cyber risk exposure at USD 329.5 billion in 2025, and they noted that indirect costs made up 70% of OT cybersecurity breach impacts, which reinforces why insurers are focusing on resilience measures rather than only post-event claims. When business interruption and supply chain effects dominate loss severity, operators have a stronger incentive to prove that they can map assets, separate networks, and respond quickly to abnormal activity. That is shifting discussions with finance teams because stronger controls can now be justified through both security outcomes and insurance readiness. It is also raising the minimum standard for documentation, since underwriters increasingly want asset visibility, incident response procedures, and evidence that remote connections are governed. In practice, this has helped the industrial internet of things (IIoT) security market move closer to the center of operating risk decisions rather than leaving it as a narrow technical procurement topic.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Retrofit Costs for Legacy Controllers and Field Devices | -3.2% | Global, pronounced in South America, Middle East, and Africa | Long term (≥ 4 years) |

| OT Cybersecurity Skills Shortage | -2.4% | Global, severe in Asia-Pacific and South America | Long term (≥ 4 years) |

| Downtime Risk During Security Deployment | -1.9% | Global, highest impact in energy and industrial manufacturing | Medium term (2-4 years) |

| Fragmented Ownership Between Operations, IT, and Engineering | -1.4% | Global, particularly North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs for Legacy Controllers and Field Devices

The industrial internet of things (IIoT) security market still faces a basic obstacle because many industrial sites continue to rely on equipment designed for long service lives and limited native security. TXOne Networks found in 2026 that 54% of industrial organizations cited compatibility with legacy equipment as the leading barrier to security adoption, while 38% still pointed to high replacement costs as a constraint. This helps explain why many operators prefer protection-in-place strategies instead of full controller replacement, especially where production lines cannot tolerate prolonged shutdowns. The input data also showed full PLC replacement costs of EUR 30,000 to EUR 150,000 (USD 33,000 to USD 165,000) and complete production line retrofits at EUR 3 million (USD 3.3 million) per line, so cost pressure remains substantial even before downtime is factored in. TXOne also noted in 2025 that strategic life extension can avoid USD 2 million to USD 5 million in costs per legacy system, which is why buyers in the industrial internet of things (IIoT) security market often choose virtual patching, network controls, and isolation tools before they choose hardware renewal. The result is slower adoption in brownfield facilities, even when management recognizes that legacy exposure is widening relative to newer, security-by-design sites.

OT Cybersecurity Skills Shortage

The industrial internet of things (IIoT) security market is also constrained by a shortage of people who understand plant operations and modern cyber defense at the same time. Fortinet stated in its 2026 skills gap research that the lack of cybersecurity skills remained a leading cause of breaches, and that pressure is especially acute in environments where specialized OT expertise is required. When industrial owners cannot staff round-the-clock monitoring, incident triage, and engineering-aware response teams, they often delay deployments or narrow project scope. This shortage also shifts buying toward managed service providers because outsourced monitoring can close capability gaps faster than internal hiring can. The effect is uneven because larger operators can absorb higher service costs more easily, while smaller facilities may postpone upgrades even when risk is visible. That means the industrial internet of things (IIoT) security market continues to expand, but the path is slower, where talent scarcity limits how quickly operators can operationalize the tools they purchase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Hold the Base While Services Gain Speed

Solutions held 57.35% of revenue in 2025, which kept this segment at the center of the industrial internet of things (IIoT) security market because most programs still begin with visibility, segmentation, detection, and vulnerability management tools. Buyers usually start with core controls because brownfield facilities need an immediate view of what is connected before they can set policy, tune alerts, or isolate risky paths between enterprise networks and plant systems. In the cybersecurity for industrial IoT industry, early spend continues to favor asset-discovery platforms, protocol-aware monitoring, and industrial intrusion detection because these tools establish the operating picture that later services depend on. The solutions base also remains important because many regulated operators still want direct control over architecture decisions and tool placement inside critical facilities.

Services are projected to expand at a 20.21% CAGR through 2031, and that stronger pace reflects the growing need for managed detection, incident response, compliance support, and remote SOC coverage. Dragos reported in 2026 that comprehensive OT visibility reduced incident dwell time from an industry average of 42 days to 5 days, which gives service-led models a clear performance argument when operators need faster outcomes.[3]Dragos, “Dragos 2026 Year In Review, New OT Threats And Ransomware,” Dragos, DRAGOS.COM. This is why the industrial internet of things (IIoT) security market is steadily moving toward contracts that combine technology, monitoring, and response into a recurring service relationship. In the cybersecurity for industrial IoT industry, that shift also puts pressure on product-only vendors because buyers increasingly want proof that controls can be operated effectively, not just installed. Over time, solutions should remain the larger revenue base, but services are likely to capture a rising share of new spending because staffing pressure and accountability demands continue to grow.

By Security Type: Network Controls Lead While Cloud Protection Grows Fastest

Network security held 41.69% share in 2025, and it accounted for 41.69% of the industrial internet of things (IIoT) security market share because industrial operators still prioritize segmentation, firewalling, and internal traffic visibility before many other control layers. That position reflects the structure of legacy OT environments, where separating zones and monitoring east-west traffic remains essential to limit movement from IT systems into control networks. Palo Alto Networks and its research partners showed that public internet exposure across industrial devices remained large in 2024, which supports continued spending on network-aware defenses in the industrial internet of things (IIoT) security market. Network security also retains budget priority because it can reduce risk across many asset classes at once, from engineering workstations to remote access paths and edge gateways.

Cloud security is projected to grow at a 21.26% CAGR through 2031, which shows how much the industrial internet of things (IIoT) security market is shifting toward cloud-connected SCADA, remote monitoring, identity services, and hosted analytics. As operators move more monitoring and management functions into hybrid environments, they need controls that can protect data flows, credentials, and application links outside the plant boundary. Dragos noted in 2026 that adversaries were actively targeting deeper operational layers, including engineering workstations and configuration data, which supports a stronger demand for controls that can follow identities and workloads across connected environments. Application security, identity and access management, data security, and continuous threat monitoring are also gaining ground because buyers increasingly want layered control rather than single-point defenses. The industrial internet of things (IIoT) security market, therefore, continues to favor network security in the base year, while faster cloud adoption is pulling newer spending toward distributed defense models.

By Deployment Mode: On-Premises Remains Dominant While Cloud Models Advance

On-premises deployments accounted for 61.23% of the industrial internet of things (IIoT) security market in 2025, reflecting the installed base of legacy environments, low-latency operational needs, and data control requirements at critical facilities. Many industrial owners still kept security tools close to production assets because older architectures were designed around site-level control and tight network boundaries. This also meant that deployment choice was often driven by system constraints rather than by a pure preference for local infrastructure. In the cybersecurity for industrial IoT industry, on-premises systems therefore remained common, as process continuity, regulatory sensitivity, and older plant design limited the speed of cloud migration.

Cloud deployments are projected to expand at a 22.63% CAGR through 2031, which makes them the fastest-growing mode in the industrial internet of things (IIoT) security market. That growth reflects the appeal of managed SOC services, vendor-hosted intelligence, and analytics environments that can scale without the need for repeated on-site hardware refreshes. Cisco stated in 2026 that embedded zero-trust remote access in industrial switches and routers can simplify plant-floor security operations, demonstrating how cloud-enforced policy is increasingly tied to industrial network infrastructure itself.[4]Cisco Systems, “Layered Defense For The Plant Floor, Simplifying OT Security,” Cisco, CISCO.COM. Hybrid deployment is likely to remain especially important, as many operators want local sensors and control, with cloud-based analysis and policy coordination. The industrial internet of things (IIoT) security market is therefore moving toward consistent protection across on-premises, edge, and cloud environments rather than toward a single deployment model replacing all others.

By End-User Industry: Manufacturing Leads While Healthcare and Life Sciences Accelerates

Industrial manufacturing held 31.64% share in 2025, and it remained the largest end-user block in the industrial internet of things (IIoT) security market because factories continue to face intense ransomware pressure and broad exposure across PLCs, DCS, SCADA, and edge assets. Dragos stated in 2026 that manufacturing accounted for more than 66% of ransomware victims among industrial organizations in 2025, which helps explain why this vertical kept the largest revenue share. The focus in manufacturing remains practical and immediate, with spending centered on visibility, segmentation, protocol monitoring, and incident response readiness across production lines. In the cybersecurity for industrial IoT industry, manufacturing also sets buying patterns for other verticals because it combines high asset density, long equipment life, and direct revenue loss when operations stop.

Healthcare and life sciences is projected to grow at a 21.37% CAGR through 2031, which makes it the fastest-expanding end-user segment in the industrial internet of things (IIoT) security market. That pace reflects the spread of connected medical devices, hospital operational systems, and building technologies that now sit closer to enterprise networks than they once did. Energy and utilities also remain a major demand pool because Dragos documented in 2026 that threat actors were mapping control loops and targeting HMIs, VFDs, and cellular gateways in U.S. infrastructure environments. Transportation and logistics is gaining relevance as ports, fleets, and intermodal operations connect more operational systems to digital management layers. Water, wastewater, chemicals, and food operations should also keep adding demand because they face many of the same visibility, remote access, and resilience requirements seen across the broader industrial internet of things (IIoT) security market.

Geography Analysis

North America held 38.25% of the industrial internet of things (IIoT) security market share in 2025, which kept it as the largest regional contributor. The region benefits from a dense installed base of critical infrastructure and a procurement environment where industrial owners are already familiar with OT-specific tools and managed security services. FERC approval of CIP-015-1 in July 2025 widened mandatory internal monitoring requirements, which strengthened the compliance case for continued spending across electricity and related critical systems. FERC also pushed for broader supply chain protections in September 2025, which added to the need for stronger control across a wider set of cyber assets. Dragos also identified North America as carrying the highest concentration of industrial OT cyber financial exposure, which helps explain why buyers in the industrial internet of things (IIoT) security market often prioritize detection depth, response support, and vendor consolidation.

Asia-Pacific is projected to expand at a 23.87% CAGR through 2031, which makes it the fastest-growing regional block in the industrial internet of things (IIoT) security market size. Growth is being supported by rapid industrial digitalization, a large manufacturing base, and an operating environment where many plants are increasing connectivity faster than they can build specialized OT security teams. In Japan, METI published OT Security Guidelines for semiconductor device factories in 2025, which tied plant security more closely to recognized standards and raised the profile of OT cyber requirements in a strategic manufacturing sector.[5]Ministry of Economy, Trade and Industry, “Semiconductor Device Factory OT Security Guidelines,” Ministry of Economy, Trade and Industry, METI.GO.JP. This kind of sector-specific rulemaking matters because it influences procurement language, audit expectations, and supplier readiness across wider production networks. The result is that Asia-Pacific is becoming a high-growth part of the industrial internet of things (IIoT) security market, not only because of rising exposure, but also because operators are formalizing security requirements while managed service demand continues to increase.

Europe remains another major demand center in the industrial internet of things (IIoT) security market because energy, manufacturing, transport, and digital infrastructure operators face broad security and reporting obligations. Germany continues to stand out within Europe because its industrial base creates sustained demand for OT visibility, segmentation, and control-system-aware monitoring. The United Kingdom is also relevant because OT security guidance has moved closer to internationally recognized control frameworks, which supports more standardized buying criteria across industrial operators. South America, the Middle East, and Africa still represented smaller revenue pools, but they remained important growth areas where state-owned energy and utilities operators often carry high exposure with limited internal specialist capacity. That pattern keeps the industrial internet of things (IIoT) security market open to managed service models in those regions, especially where brownfield facilities need practical protection without full infrastructure replacement.

Competitive Landscape

The industrial internet of things (IIoT) security market shows moderate concentration, with specialist OT security vendors competing alongside industrial automation companies and large enterprise security providers. Claroty, Nozomi Networks, and Dragos remain central names because they built offerings around industrial asset visibility, protocol depth, and OT-specific threat intelligence, while Honeywell, Siemens, ABB, Schneider Electric, Cisco, Fortinet, and Palo Alto Networks bring broader portfolios into the same buying process. This mix keeps competition active because buyers can choose between purpose-built OT platforms and wider cyber or automation stacks that include OT security as part of a larger operating model. The result is an industrial internet of things (IIoT) security market where product quality still matters, but service depth, integration reach, and the ability to support mixed environments matter just as much.

Strategic moves in 2025 and 2026 show where vendors are trying to differentiate. Claroty raised USD 150 million in Series F funding in January 2026, which gave it more room for expansion and acquisition-led platform development. Honeywell expanded its OT Cybersecurity Suite in June 2026 with 5 new capabilities, including AI-driven defense and managed OT Security Operations Center support, which strengthened its position across manufacturing, energy, and critical infrastructure accounts. Dragos acquired Phosphorus in June 2026 to extend protection across billions of connected devices in operational networks, which pushed its platform further into device-centric security coverage. Nozomi Networks also became part of a larger automation strategy after Mitsubishi Electric signed a definitive agreement to acquire it in September 2025, which reflected growing interest in combining OT security software with industrial automation reach. These moves show that the industrial internet of things (IIoT) security market is rewarding vendors that can broaden their scope without losing OT depth.

Another important competitive shift is the move from tool sales toward outcome-based contracts. Buyers increasingly want fewer vendors, easier integration with SIEM, SOAR, and identity platforms, and stronger proof that providers can reduce dwell time or improve response readiness. Cisco highlighted embedded zero-trust remote access within industrial networking equipment in 2026, which is one example of vendors trying to simplify deployment by building security into the infrastructure layer. Honeywell and other large industrial providers are also using managed services and AI-enabled analytics to compete more directly with OT specialists for long-term operating contracts. That keeps the industrial internet of things (IIoT) security market open to multiple vendor types, but it also raises the bar for smaller firms that do not yet have deep protocol libraries, service coverage, or strong ecosystem links.

Industrial Internet Of Things (IIoT) Security Industry Leaders

Claroty Ltd.

Nozomi Networks Inc.

Dragos Inc.

Cisco Systems, Inc.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Dragos acquired Phosphorus, extending the Dragos Platform to protect billions of connected devices embedded in operational networks. The acquisition follows Dragos' October 2024 acquisition of Network Perception and expands its total addressable market to more than USD 50 billion, per the company's own estimate.

- June 2026: Honeywell expanded its OT Cybersecurity Suite with five new capabilities, Secure Media Exchange portable scanner, AI-powered Cyber Proactive Defense, Cyber Governance Risk and Compliance automation, a unidirectional Data Diode, and a managed 24/7 OT Security Operations Center, covering manufacturing, energy, and critical infrastructure sectors.

- February 2026: Palo Alto Networks, Siemens, and Idaho National Laboratory published the Intelligence-Driven Active Defense Report 2026, documenting a 332% surge in internet-exposed OT devices, from 6 million in 2023 to 20 million in 2024, and providing a structured OT-SOC implementation roadmap for asset owners.

- October 2025: Japan's Ministry of Economy, Trade and Industry published OT Security Guidelines for semiconductor device factories, aligned with SEMI E187/E188 standards and NIST CSF 2.0, establishing a sector-specific security baseline that is expected to influence procurement requirements for Japan's semiconductor supply chain globally.

- September 2025: Mitsubishi Electric signed a definitive agreement to acquire Nozomi Networks, initially announced at a combined enterprise value undisclosed but reported as part of Mitsubishi Electric's strategic push to embed OT security into its industrial automation portfolio. The deal marked a significant inflection in the consolidation of the OT cybersecurity pure-play segment.

Global Industrial Internet Of Things (IIoT) Security Market Report Scope

The Industrial Internet of Things (IIoT) Security is the practice of protecting connected devices, sensors, control systems, and communication networks that support industrial operations across sectors such as manufacturing, energy, transportation, and utilities. It safeguards the confidentiality, integrity, and availability of industrial data and processes by preventing, detecting, and responding to cyber threats that could disrupt production, compromise safety, or cause financial and operational losses. Cybersecurity for IIoT helps protect both digital and physical assets across highly connected industrial environments.

The Industrial Internet Of Things (IIoT) Security Market Report is Segmented by Component (Solutions and Services), Security Type (Network Security, Device and Endpoint Security, Application and API Security, Identity and Access Security, Data Security and Privacy, and Security Monitoring and Threat Detection), Deployment Mode (On-Premises, Cloud, and Hybrid), End-User Industry (Industrial Manufacturing, Energy and Utilities, Oil and Gas, Transportation and Logistics, Healthcare and Life Sciences, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Network Security |

| Device and Endpoint Security |

| Application and API Security |

| Identity and Access Security |

| Data Security and Privacy |

| Security Monitoring and Threat Detection |

| On-Premises |

| Cloud |

| Hybrid |

| Industrial Manufacturing |

| Energy and Utilities |

| Oil and Gas |

| Transportation and Logistics |

| Healthcare and Life Sciences |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of the Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Solutions | |

| Services | ||

| By Security Type | Network Security | |

| Device and Endpoint Security | ||

| Application and API Security | ||

| Identity and Access Security | ||

| Data Security and Privacy | ||

| Security Monitoring and Threat Detection | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By End-User Industry | Industrial Manufacturing | |

| Energy and Utilities | ||

| Oil and Gas | ||

| Transportation and Logistics | ||

| Healthcare and Life Sciences | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the industrial internet of things (iiot) security market?

The industrial internet of things (iiot) security market was valued at USD 12.14 billion in 2025, stood at USD 14.36 billion in 2026, and is projected to reach USD 33.26 billion by 2031 at an 18.29% CAGR.

Which region leads revenue in cybersecurity for industrial IoT?

North America led with 38.25% share in 2025, supported by critical infrastructure density and stricter compliance requirements.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to post the fastest CAGR at 23.87% through 2031, helped by rapid industrial digitalization and tighter OT security requirements.

Which component is driving the most spending today?

Solutions led the revenue mix with 57.35% share in 2025 because operators still begin with visibility, segmentation, and monitoring tools.

Which deployment model is expanding the fastest?

Cloud deployments are expected to grow at a 22.63% CAGR through 2031 as more operators adopt managed SOC services and cloud-linked analytics.

Which end-user segment shows the strongest future growth?

Healthcare and life sciences is projected to expand at a 21.37% CAGR through 2031 as connected medical devices and hospital operational systems face higher cyber exposure.

Page last updated on: