IoT Infrastructure Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

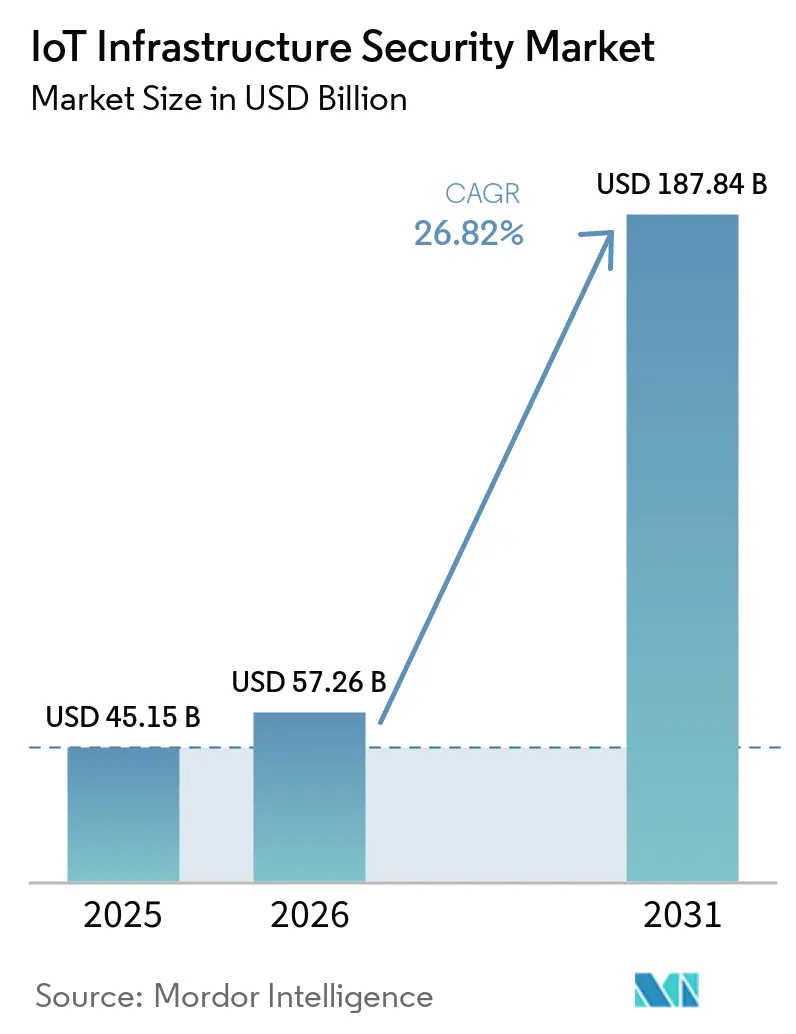

| Market Size (2026) | USD 57.26 Billion |

| Market Size (2031) | USD 187.84 Billion |

| Growth Rate (2026 - 2031) | 26.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Infrastructure Security Market Analysis by Mordor Intelligence

The IoT infrastructure security market size is expected to increase from USD 45.15 billion in 2025 to USD 57.26 billion in 2026 and reach USD 187.84 billion by 2031, growing at a CAGR of 26.82% over 2026-2031. This sharp rise follows a foundational period from 2019 to 2025, when enterprises were still moving through early IoT rollout cycles and building connected environments with a more limited security scope. The next phase is different because 21.1 billion active IoT endpoints were already operating globally in 2025, which widened exposure across devices, networks, platforms, and cloud environments and pushed security spending into board-level planning. The IoT infrastructure security market is also being shaped by a shift away from isolated tools, as buyers increasingly prefer integrated platforms that can discover assets, enforce device identity, manage risk, and support zero-trust controls across mixed IT and OT estates. Competitive activity remains strong because larger vendors are expanding platform breadth while specialist providers continue to win attention in industrial and cyber-physical settings where protocol depth and passive monitoring matter most. The pace of AI-enabled attack activity, together with persistent talent shortages, is further accelerating the move toward automation, managed services, and architecture-level security investments across the Internet of Things (IoT) infrastructure security market.

Key Report Takeaways

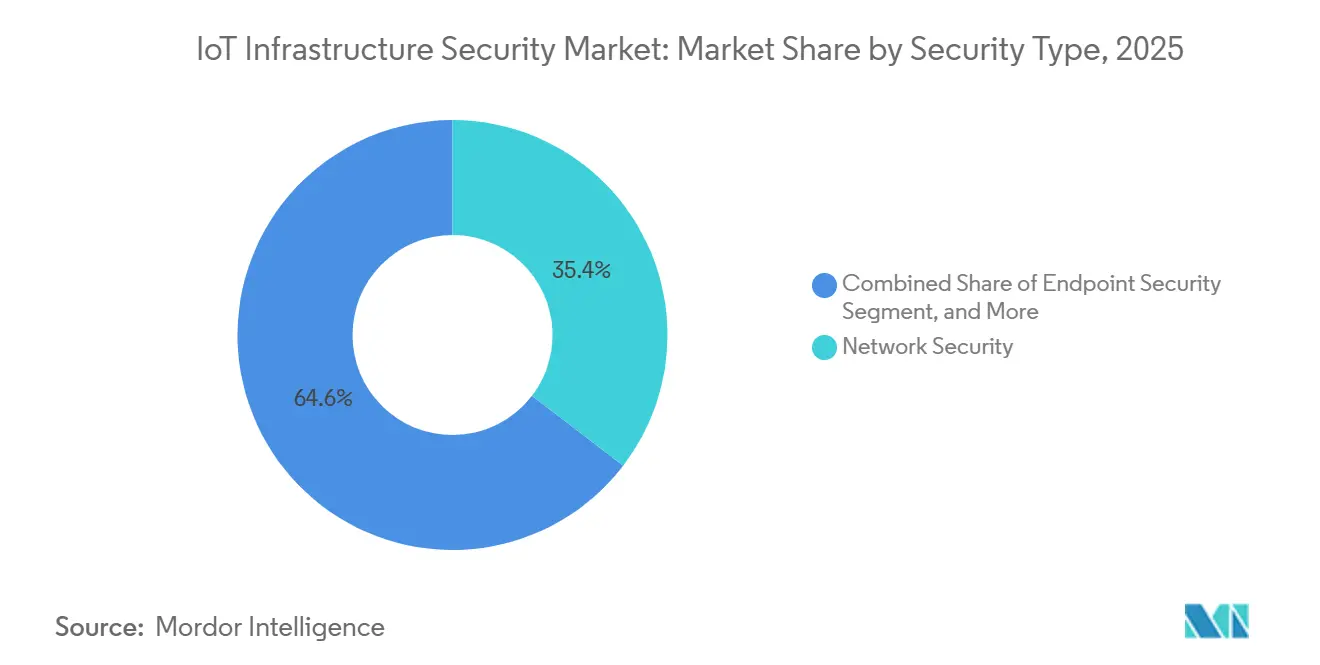

- By security type, network security led with 35.4% revenue share in 2025 for the IoT infrastructure security market, while cloud security is forecast to expand at a 31.2% CAGR through 2031.

- By deployment model, cloud-based solutions captured 57.2% of the Internet of Things (IoT) infrastructure security market in 2025, while hybrid deployments are forecast to grow at a 32.2% CAGR through 2031.

- By infrastructure layer, cloud and data centers accounted for 31.1% of the market share in 2025, while edge and fog are projected to grow at a 34.2% CAGR through 2031.

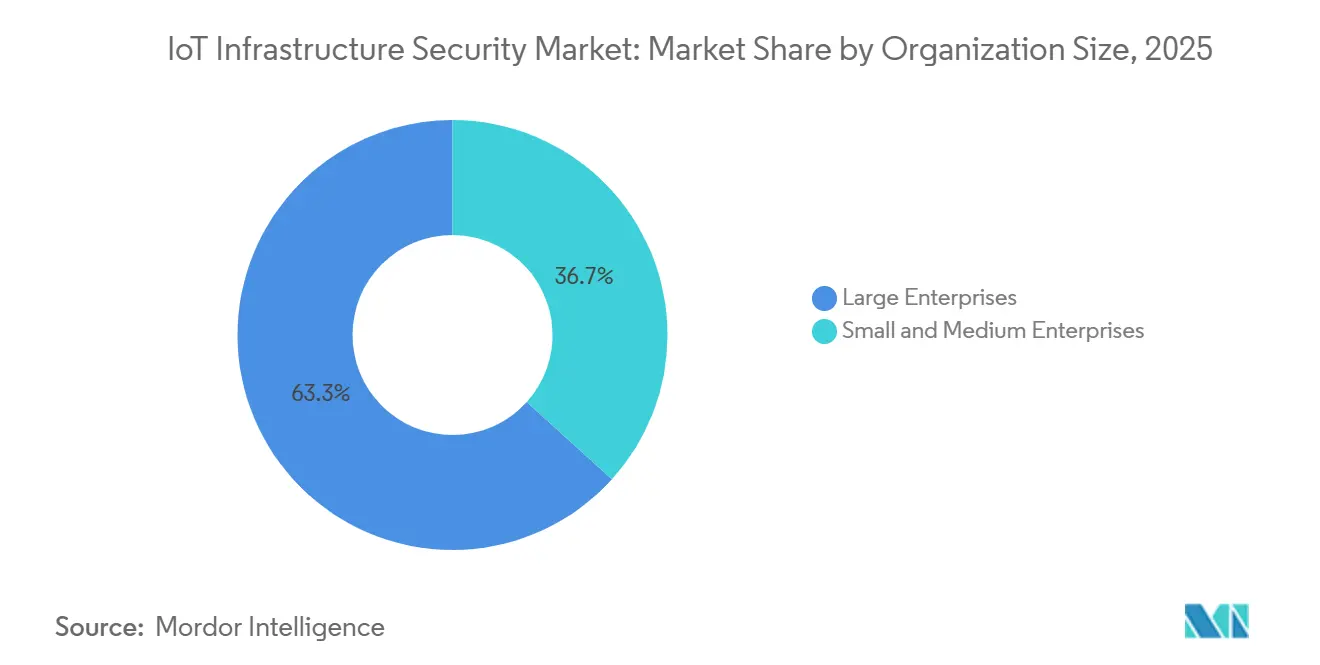

- By organization size, large enterprises represented 63.3% of spending in 2025, while small and medium enterprises are projected to grow at a 29.1% CAGR through 2031.

- By industry vertical, manufacturing accounted for 22.5% of the IoT infrastructure security market size in 2025, while smart cities and infrastructure are projected to expand at a 35.2% CAGR through 2031.

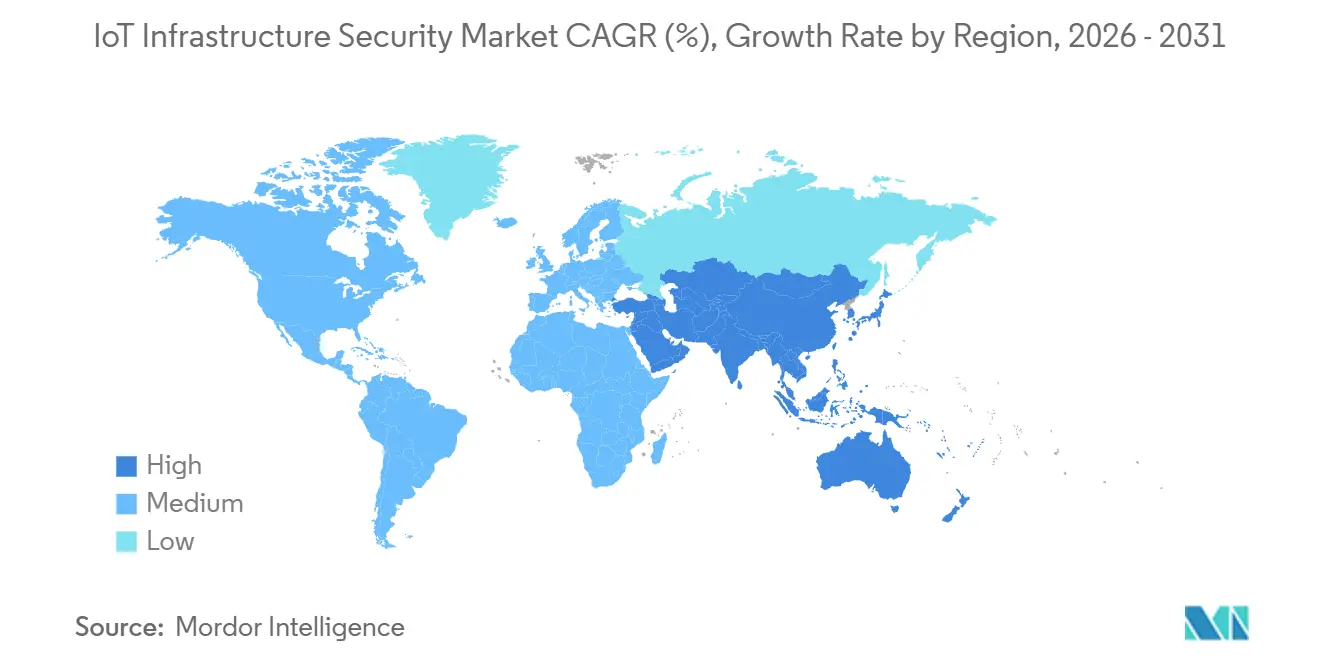

- By geography, North America held 38.6% of the IoT infrastructure security market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 32.2% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IoT Infrastructure Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Attack Surface Due to Massive IoT Adoption | +6.0% | Global, with concentrated exposure in North America, Asia-Pacific industrial zones, and Europe critical infrastructure | Short term (≤ 2 years) |

| Convergence of OT and IT Networks Elevating Security Needs | +4.5% | Global, particularly Germany, the United States, Japan, and energy-intensive Asia-Pacific economies | Medium term (2-4 years) |

| Regulatory Mandates Such as US IoT Cybersecurity Improvement Act | +4.0% | North America and Europe core, with spillover to the Asia-Pacific and the Middle East national cybersecurity frameworks | Medium term (2-4 years) |

| Integration of AI-Powered Anomaly Detection in IoT Endpoints | +3.5% | Global, with early gains in United States, United Kingdom, and Japan manufacturing clusters | Short term (≤ 2 years) |

| Emergence of 5G-Enabled IoT Driving Edge-Focus Security | +2.5% | Asia-Pacific core, especially China, South Korea, and Japan, with spillover to North America and Gulf states | Medium term (2-4 years) |

| Rapid Growth of IIoT Platforms in Developing Economies | +2.0% | Asia-Pacific, Middle East, and South America industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Attack Surface Due to Massive IoT Adoption

The scale of connected device growth is changing the economics of cyber defense across the IoT infrastructure security market. Vectra AI reported 13.6 billion IoT attacks between January and October 2025, and it also noted that more than 50% of connected devices ship with critical firmware vulnerabilities.[1]Vectra AI, “IoT Security in 2026: Threats, Risks, and Best Practices,” Vectra AI, vectra.aiThat mix of rising device counts and weak default security makes manual patching and manual inventory processes increasingly unworkable in enterprise environments. The result is a stronger demand for automated asset discovery, device identity controls, network segmentation, and zero-trust enforcement, especially in environments with large fleets of unmanaged or lightly managed devices. Palo Alto Networks also highlighted a 332% rise in exposed devices over the past year and stated that 70% of cyber incidents originated in IT environments through unprotected IoT entry points, which helps explain why this remains the strongest growth engine in the IoT infrastructure security market.[2]Palo Alto Networks, “Precision AI Pro, Now with Integrated Device Security,” Palo Alto Networks, paloaltonetworks.com

Convergence of OT and IT Networks Elevating Security Needs

The convergence of OT and IT networks is increasing risk in the IoT infrastructure security market, as events that begin on the corporate side can now spread directly into plant, utility, and infrastructure operations. SANS research found that 58% of initial ICS and OT attacks began as IT compromises, underscoring how deeply enterprise and operational environments are now linked.[3]SANS Research Program, “2025 ICS/OT Cybersecurity Budget: Spending Trends, Challenges, and the Future,” SANS Research Program, info.opswat.comShared credentials, connected communication paths, and centralized management tools improve efficiency, but they also create common entry points, such as phishing or weak remote access, that can compromise critical production systems. This forces OT and IT teams to share accountability for outcomes, and that change is supporting a move away from isolated tools toward unified platforms with broader visibility and policy control. As more operators build converged environments, the IoT infrastructure security market is seeing larger enterprise deals that bundle discovery, monitoring, segmentation, compliance reporting, and managed response into a single buying decision.

Regulatory Mandates such as US IoT Cybersecurity Improvement Act

Regulation is becoming a durable demand base for the IoT infrastructure security market because it turns security requirements into dated procurement obligations. NIST published the second public draft of NIST IR 8259r1 in September 2025, broadening its coverage to the full IoT product life cycle, including end-of-life management and supply chain transparency.[4]National Institute of Standards and Technology, “Foundational Cybersecurity Activities for IoT Product Manufacturers,” NIST, nvlpubs.nist.govExecutive Order 14306, signed in June 2025, requires federal vendors of consumer IoT products to carry the US Cyber Trust Mark by January 2027, which extends pressure across manufacturers and suppliers serving government-linked demand.[5]Office of the Federal Register, “Executive Order 14306, Sustaining Select Efforts to Strengthen the Nation’s Cybersecurity,” Federal Register, federalregister.gov These developments matter because threat awareness alone often delays action, while compliance deadlines usually force budgeting, product redesign, and audit preparation. The same pattern is emerging in other regions, where certification lead times and expanding product security expectations are turning regulatory frameworks into practical sales catalysts for the IoT infrastructure security market.

Integration of AI-Powered Anomaly Detection in IoT Endpoints

AI-enabled anomaly detection is moving into daily operations across the IoT infrastructure security market because it can analyze large device fleets without interrupting sensitive industrial processes. Passive monitoring now lets security teams build behavior baselines for connected assets and identify unusual traffic or command-and-control activity without the need for active scans that could disrupt production. AWS introduced multivariate anomaly detection in IoT SiteWise in July 2025, which made it easier to identify cross-variable equipment anomalies without requiring customers to build machine learning expertise first. Nozomi Networks launched Vantage IQ in January 2026 as a private, organization-trained AI assistant for OT and IoT security teams, reflecting growing demand for AI that stays within the customer environment rather than pushing sensitive telemetry into shared cloud models. The same technology race also keeps pressure high, as attackers use AI to accelerate reconnaissance and exploit development, leaving the IoT infrastructure security market with little room for a defensive pause.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Security Budgets for Legacy Industrial Assets | -1.8% | Global, concentrated in South America, lower-tier Middle East operators, and South and Southeast Asian SME manufacturers | Medium term (2-4 years) |

| Fragmented Standards Across IoT Ecosystem | -1.4% | Global, most acute for multi-market manufacturers exporting to the EU, the United States, and APAC simultaneously | Medium term (2-4 years) |

| Skill Shortage in IoT-Specific Cybersecurity Expertise | -1.2% | Global, with acute gaps in APAC manufacturing hubs and critical infrastructure sectors | Long term (≥ 4 years) |

| High Implementation Complexity for Multi-Layer Security | -0.9% | Global, most pronounced in multi-site industrial operators and mid-market enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Security Budgets for Legacy Industrial Assets

Legacy industrial assets slow the IoT infrastructure security market because the cost of replacement is still too high for many operators. TXOne Networks stated that replacing a single legacy industrial control system can cost USD 2.4 million in hardware alone, require 6 months of revalidation, and create 2 weeks of production downtime. SANS research also showed that 34% of respondents were unsure about their overall security budget allocations, while 41% allocated only 0-25% of their total budgets to ICS and OT security. Those conditions make full modernization difficult, even when leadership understands the risk exposure tied to older control systems and long asset life cycles. Compensating controls such as virtual patching, passive monitoring, and network microsegmentation can extend the secure operating life, but adoption still depends on proving operational returns, which tempers growth in the IoT infrastructure security market.

Fragmented Standards Across IoT Ecosystem

Fragmented standards remain a drag on the IoT infrastructure security market because manufacturers often need to comply with multiple security frameworks simultaneously. NIST IR 8259r1 shows how product manufacturers are being asked to document security activities across the full device life cycle, and those expectations add engineering and documentation work even before a product reaches the customer. Federal requirements such as the Cyber Trust Mark increase the need for traceability and demonstrable security controls, but other regions continue to apply their own certification models, update cycles, and conformity rules. The burden falls hardest on smaller vendors that lack large compliance teams, dedicated legal support, or additional engineering capacity for repeated documentation and testing. This slows product rollouts, increases certification cost, and limits trust when uncertified devices remain in circulation, all of which restrain the IoT infrastructure security market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Security Type: Network Leadership Holds While Cloud Security Advances Faster

Network security retained 35.4% of the IoT infrastructure security market in 2025, a position that reflects the continued exposure that begins at the connectivity layer. Routers, gateways, and other network-facing components remain the first point of control when enterprises try to identify unmanaged devices, isolate risky behavior, and contain lateral movement. For many buyers, the first wave of spending still goes to visibility, segmentation, and protocol-aware monitoring because those functions create immediate value across mixed device estates. Network security indicates that buyers still treat the network layer as the primary enforcement plane for large-scale IoT defense. The broader direction of the IoT Infrastructure Security Market also shows that organizations are shifting away from traditional perimeter tools toward network detection and response platforms that can analyze industrial traffic at wire speed.

Cloud security is the fastest-growing security type, with a projected CAGR of 31.2% through 2031, because enterprises increasingly want centralized operations, continuous updates, and managed support. This growth is closely tied to cloud-native zero-trust models, where policy management, device context, and automated response can be coordinated more efficiently across distributed sites. Palo Alto Networks moved its legacy IoT Security portal into Device Security within Strata Cloud Manager, setting August 2026 as the portal's shutdown date, demonstrating how leading vendors are consolidating discovery, classification, virtual patching, and compliance reporting into shared workflows. Endpoint security, application security, and other categories continue to drive meaningful demand, especially as AI-enabled applications, unmanaged devices, and regulated workloads expand. Across this mix, the IoT infrastructure security market is clearly moving toward unified platforms that share asset intelligence across network, endpoint, application, and cloud controls.

By Deployment Model: Cloud Scale Leads While Hybrid Adoption Speeds Up

Cloud-based deployments accounted for 57.2% of revenue in 2025, confirming that centralized visibility and subscription economics remain highly attractive in the IoT infrastructure security market. Cloud-based deployment that leads reflects the value buyers place on elastic analytics capacity, integrated threat intelligence, and faster feature delivery. This model is especially appealing to enterprises that do not want to build large in-house security teams for every site, plant, or branch. Cloud delivery also aligns with the growing role of AI-driven security tools, which benefit from continuous model updates and broad telemetry pooling within vendor-managed environments. AWS Security Hub Extended, launched in February 2026, supports that direction by combining findings from AWS security services and curated partner solutions into a single interface with standardized outputs and unified billing.

Hybrid deployment is the fastest-growing model, with a projected CAGR of 32.2% through 2031, because many operators still need air-gapped or tightly controlled OT environments. These buyers are not rejecting cloud economics; they are blending local control with centralized threat intelligence and policy management. In practice, a hybrid architecture helps enterprises keep safety-critical processes and sensitive workloads on-site while using off-site tools for analysis, orchestration, and reporting. On-premises deployment remains relevant in defense, utilities, and some healthcare environments where sovereignty, resilience, or internal policy still limit wider cloud use. The IoT infrastructure security market is therefore undergoing a blended transition rather than a simple shift from on-premises to the cloud.

By Infrastructure Layer: Centralized Security Is Mature While Edge Spending Rises

The cloud and data center layer held a 31.1% share in 2025, reflecting the maturity of centralized security operations, data aggregation, and policy enforcement in the IoT infrastructure security market. That layer has historically been the easiest place to concentrate logging, analytics, and threat intelligence because it sits close to shared compute resources and enterprise governance tools. It also benefits from well-established cloud security ecosystems, which give buyers access to bundled controls, partner integrations, and scalable incident workflows. The cloud and data center layer, therefore, remains a major anchor point for the IoT infrastructure security market, especially for enterprises seeking centralized oversight across a wide mix of sites and device types. At the same time, the old assumption that all relevant telemetry should flow back to centralized systems is weakening.

Edge and fog are the fastest-growing infrastructure layers, with a projected CAGR of 34.2% through 2031, as latency, sovereignty, and bandwidth concerns push more security functions closer to the device. This is especially important in industrial settings where real-time decisions matter and sending every data stream upstream incurs costs, delays, and exposure. Cisco stated that embedding Cyber Vision into switch and router ASICs can reduce total cost of ownership while limiting traffic overhead to 2-5%, compared with 50-80% for traditional SPAN-based approaches. Fortinet also expanded inspection to include MCP and agent-to-agent traffic with FortiOS 8.0, demonstrating how application and platform controls are evolving alongside AI-integrated IoT stacks. The IoT infrastructure security industry is now broadening from centralized cloud defense into a distributed model that links endpoint trust, network visibility, and local policy enforcement.

By Organization Size: Large Enterprises Set The Base, While SMEs Open New Demand

Large enterprises accounted for 63.3% of revenue in 2025, which makes them the spending anchor for the IoT Infrastructure Security Market. Their leadership comes from the scale and complexity of connected operations, including multi-site OT estates, global supplier networks, extensive compliance obligations, and the need for dedicated monitoring teams. These organizations also tend to buy broader platforms because the cost of integrating many isolated tools becomes difficult to justify over time. As a result, large accounts are helping shape vendor road maps around centralized management, unified asset context, and cross-domain policy enforcement. The Internet of Things (IoT) infrastructure security market still depends heavily on large enterprises for contract scale, long deployment cycles, and reference deployments in critical sectors.

Small and medium enterprises are the fastest-growing segment, with a projected CAGR of 29.1% through 2031, as regulations and service-based delivery are lowering entry barriers. Many smaller operators now face formal obligations that did not apply a few years ago, and they are also becoming more exposed as suppliers, manufacturing, logistics, and facility systems connect into wider digital ecosystems. The threshold cited in the input for NIS2 coverage, entities with more than 50 employees or EUR 10 million (USD 11.36 million) at 2025 average exchange rates, shows why mid-market buyers can no longer defer security decisions. Vendors are responding with starter frameworks, managed offerings, and simplified deployment paths that reduce the need for large internal teams. This is widening the buyer base of the IoT infrastructure security market beyond global enterprises and into earlier-stage adopters that still need practical, lower-friction controls.

By Industry Vertical: Manufacturing Leads While Smart City Programs Expand Faster

Manufacturing led all verticals with 22.5% revenue share in 2025, which keeps it at the center of the IoT infrastructure security market. The sector combines dense machine connectivity, old and new equipment in the same environment, strict uptime requirements, and high exposure to ransomware and operational disruption. Those conditions make manufacturing a difficult security environment because the devices are numerous, the operating windows are narrow, and change management is closely tied to production output. Security spending in this vertical is also influenced by a widening governance push across industrial economies, where manufacturers and their suppliers are under more pressure to show formal controls and incident readiness. For the IoT infrastructure security market, manufacturing remains the most established spending base because security failures can stop production, interrupt deliveries, and create visible financial loss in a short period.

Smart cities and infrastructure are the fastest-growing vertical, with a projected CAGR of 35.2% through 2031, because digitization programs are embedding security requirements from the start rather than treating them as later upgrades. Public surveillance, intelligent traffic systems, utilities, connected buildings, and citywide digital services create large multi-vendor environments where interoperability and continuous monitoring are essential. Gulf city programs are especially important in this context because they are building AI-enabled public safety and infrastructure systems with security written into the core architecture. Healthcare, energy and utilities, transportation and logistics, retail and consumer IoT, BFSI, and government and defense also contribute meaningful demand, although the mix of endpoint, network, cloud, and application priorities differs by operating environment. This broader vertical spread is helping the IoT infrastructure security market move from a mainly industrial base into a more diverse infrastructure and enterprise security landscape.

Geography Analysis

North America retained the largest regional position, with a 38.6% share in 2025, reflecting the region’s mature enterprise security budgets, regulatory density, and broad critical infrastructure exposure in the IoT Infrastructure Security Market. The region also benefits from substantial public cybersecurity spending that supports broader ecosystem demand. The US Department of Defense allocated USD 8.31 billion to cybersecurity programs in fiscal year 2026, while CISA set out fiscal year 2026 milestones for IoT and OT asset management within the Continuous Diagnostics and Mitigation program. Business 5G IoT connections in North America are expected to rise from 5 million in 2025 to 39 million by 2030, expanding both demand for secure edge connectivity and the attack surface for vendors and operators. Canada offers an opportunity of a different kind because more cautious OT and ICS budget allocation leaves room for managed service providers and lower-friction platform offerings.

Europe presents the most demanding compliance environment in the IoT Infrastructure Security Market, as several major digital and operational security frameworks are advancing simultaneously. NIS2, the Cyber Resilience Act, DORA, and the Radio Equipment Directive create a layered set of requirements that affect operators, manufacturers, and vendors selling connected products into the region. Germany adds another layer through KRITIS-related obligations that broaden accountability and push security deeper into essential infrastructure planning. This structure is making compliance timelines a direct buying trigger, especially for device manufacturers and operators that need vulnerability reporting, product hardening, and formal governance processes in place before deadlines arrive.

Asia-Pacific is projected to expand at a 32.2% CAGR in the Internet of Things (IoT) infrastructure security market through 2031, reflecting both the scale of deployment and the speed of new project formation in manufacturing and smart infrastructure. Japan remains important because telecom operators are positioning security as part of connectivity itself, as shown by NTT Docomo Business launching docomo business SIGN in December 2025, with built-in security features for IoT services. South America, the Middle East, and Africa represent a smaller base, but the direction is strong because industrial digitization and smart city programs are bringing security into new projects much earlier than before.

Competitive Landscape

The IoT Infrastructure Security Market is moderately consolidated. Cisco Systems, Palo Alto Networks, Fortinet, and Microsoft shape the platform layer, while Claroty, Armis, Nozomi Networks, Darktrace, and Forescout compete more directly in specialist OT and cyber-physical environments. Platform leaders are increasingly using AI-driven unification as their main strategy because customers want fewer consoles, shared asset context, and policy controls that work across IT, OT, IoT, and cloud environments. Cisco expanded AI Defense and AI-aware SASE in February 2026, adding an AI Bill of Materials, an MCP Catalog, and real-time guardrails for agentic use cases inside its broader security fabric. Fortinet reinforced this direction with FortiOS 8.0, which added secure AI controls, fabric-based AI agents, flexible SASE options, and support for sovereign deployments for customers with stricter data-residency requirements.

Specialist vendors are still relevant because many industrial buyers care deeply about passive monitoring fidelity, protocol coverage, and deployment flexibility in sensitive or air-gapped settings. Claroty’s January 2026 Series F round of USD 150 million showed that investor support for specialist critical infrastructure security remains strong even as the market matures. Zscaler’s acquisition of SquareX in February 2026 shows how adjacent controls are moving into the browser layer, which matters for IoT management interfaces and distributed access environments. This means the IoT Infrastructure Security Market is not just consolidating around firewalls or endpoint tools; it is reorganizing around broader trust, access, and operational visibility models.

Competitive differentiation is increasingly tied to the depth of industrial protocol, machine identity, and the ability to monitor devices without disrupting real-time operations. Cisco’s network-native Cyber Vision model and Palo Alto Networks’ integrated Device Security approach both show how large vendors are pulling OT and IoT security into broader enterprise platforms rather than leaving them as separate tools. OmniTrust’s launch of a unified trust lifecycle management platform in March 2026 points to another battleground, where vendors are trying to connect hardware trust, identity, firmware, device, cloud, and AI governance into a single continuous chain. The result is a market where specialist depth still matters, but switching costs are rising for buyers who adopt platform-led security fabrics across connected infrastructure.

IoT Infrastructure Security Industry Leaders

Cisco Systems, Inc.

Palo Alto Networks, Inc.

Fortinet, Inc.

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Device Authority and Xalient formed a strategic partnership to integrate Device Authority's KeyScaler identity management platform into Xalient's managed security service offering, targeting energy, utilities, manufacturing, and healthcare sectors with automated, zero-trust IoT device lifecycle management. The partnership responds directly to the rising EU Cyber Resilience Act and NIST compliance obligations for device identity governance.

- May 2026: Fortinet expanded its FortiGate G series portfolio with the FortiGate 3500G and 400G models, delivering ASIC-accelerated performance for AI-driven workloads at data center and enterprise edge scale, respectively. The 3500G provides 595.0 gigabits per second of firewall throughput, 3.4 times the competitive average, and extends the AI-driven Security Fabric with native shadow AI detection and FortiOS 8.0's MCP traffic inspection for IoT and agentic AI environments.

- April 2026: Corsha was awarded a USD 50 million sole-source Indefinite Delivery, Indefinite Quantity contract by the US Defense Logistics Agency to deliver machine-identity-driven zero-trust connectivity across DLA's critical operational systems, including building management, advanced manufacturing, and fuel distribution infrastructure.

- April 2026: Palo Alto Networks integrated Device Security, formerly IoT Security, into its Precision AI Pro Bundle with Strata Cloud Manager, unifying discovery and classification of over 3,600 device attributes across IT, IoT, OT, and IoMT assets, virtual patching enforcement, and auto-generated NIST, IEC, and HIPAA compliance reports, with the legacy IoT Security portal scheduled for shutdown in August 2026.

Global IoT Infrastructure Security Market Report Scope

IoT Infrastructure Security comprises a suite of technologies, policies, and practices designed to safeguard the entire Internet of Things ecosystem. This includes devices, networks, edge gateways, cloud platforms, and applications, all of which are vulnerable to cyber threats, unauthorized access, data breaches, and operational disruptions. Key measures include securing device identities and firmware, encrypting data both in transit and at rest, monitoring network traffic for anomalies, enforcing stringent access controls, and ensuring compliance across all layers of IoT deployment. These efforts are crucial to uphold the confidentiality, integrity, and availability of connected systems and the data they produce.

The IoT Infrastructure Security Market Report is Segmented by Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, and Other Security Types), Deployment (On-Premises, Cloud-Based, and Hybrid), Infrastructure Layer (Device/Endpoint Layer, Connectivity/Network Layer, Edge/Fog Layer, Cloud and Data Center Layer, and Application and Platform Layer), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Healthcare, Energy and Utilities, Transport and Logisitcs, Smart Cities and Infrastructure, Retail and Consumer IoT, BFSI, Government and Defense, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts Provided in Terms of Value (USD).

| Network Security |

| Endpoint Security |

| Application Security |

| Cloud Security |

| Other Security Types |

| On-Premises |

| Cloud-based |

| Hybrid |

| Device / Endpoint Layer |

| Connectivity / Network Layer |

| Edge / Fog Layer |

| Cloud and Data Center Layer |

| Application / Platform Layer |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Healthcare |

| Energy and Utilities |

| Transportation and Logistics |

| Smart Cities and Infrastructure |

| Retail and Consumer IoT |

| BFSI |

| Government and Defense |

| Others Industry Verticals |

| North America | United States |

| Canada | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Security Type | Network Security | |

| Endpoint Security | ||

| Application Security | ||

| Cloud Security | ||

| Other Security Types | ||

| By Deployment Model | On-Premises | |

| Cloud-based | ||

| Hybrid | ||

| By Infrastructure Layer | Device / Endpoint Layer | |

| Connectivity / Network Layer | ||

| Edge / Fog Layer | ||

| Cloud and Data Center Layer | ||

| Application / Platform Layer | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Industry Vertical | Manufacturing | |

| Healthcare | ||

| Energy and Utilities | ||

| Transportation and Logistics | ||

| Smart Cities and Infrastructure | ||

| Retail and Consumer IoT | ||

| BFSI | ||

| Government and Defense | ||

| Others Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the IoT Infrastructure Security Market in 2026?

The IoT Infrastructure Security Market is valued at USD 57.26 billion in 2026 and is projected to reach USD 187.84 billion by 2031 at a CAGR of 26.82%.

Which region leads global demand for IoT infrastructure security solutions?

North America held the largest regional share at 38.6% in 2025 because of mature enterprise budgets, heavy regulatory activity, and strong federal cybersecurity spending.

Why is Asia-Pacific the fastest-growing region?

Large-scale smart-city rollouts and industrial digitization initiatives in China, India, and Southeast Asia are driving a 32.2% CAGR.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 32.2%, supported by large-scale IoT adoption, industrial expansion, and smart infrastructure programs.

Which security type currently generates the most revenue?

Network security led with 35.4% share in 2025 because the connectivity layer remains the main control point for device visibility, segmentation, and early threat detection.

Why are cloud-based deployments so prominent in this space?

Cloud-based deployment held 57.2% of revenue in 2025 because buyers value centralized visibility, subscription economics, elastic analytics capacity, and faster feature delivery.

Page last updated on: