Smart Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

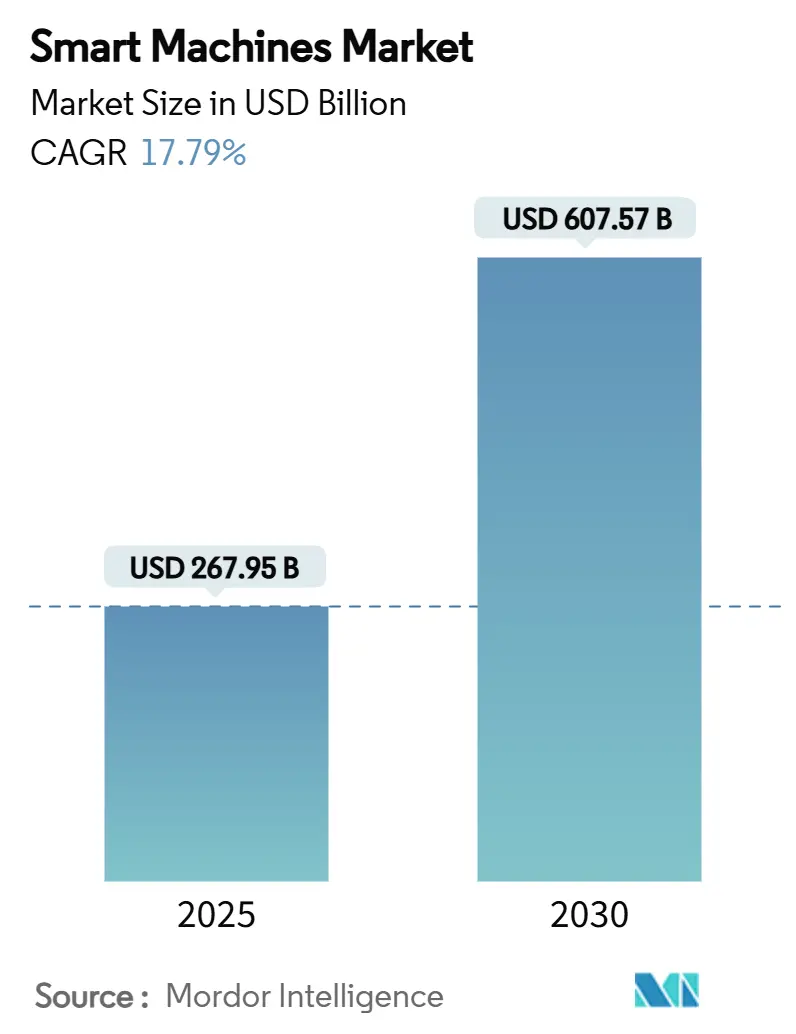

| Market Size (2025) | USD 267.95 Billion |

| Market Size (2030) | USD 607.57 Billion |

| Growth Rate (2025 - 2030) | 17.79% CAGR |

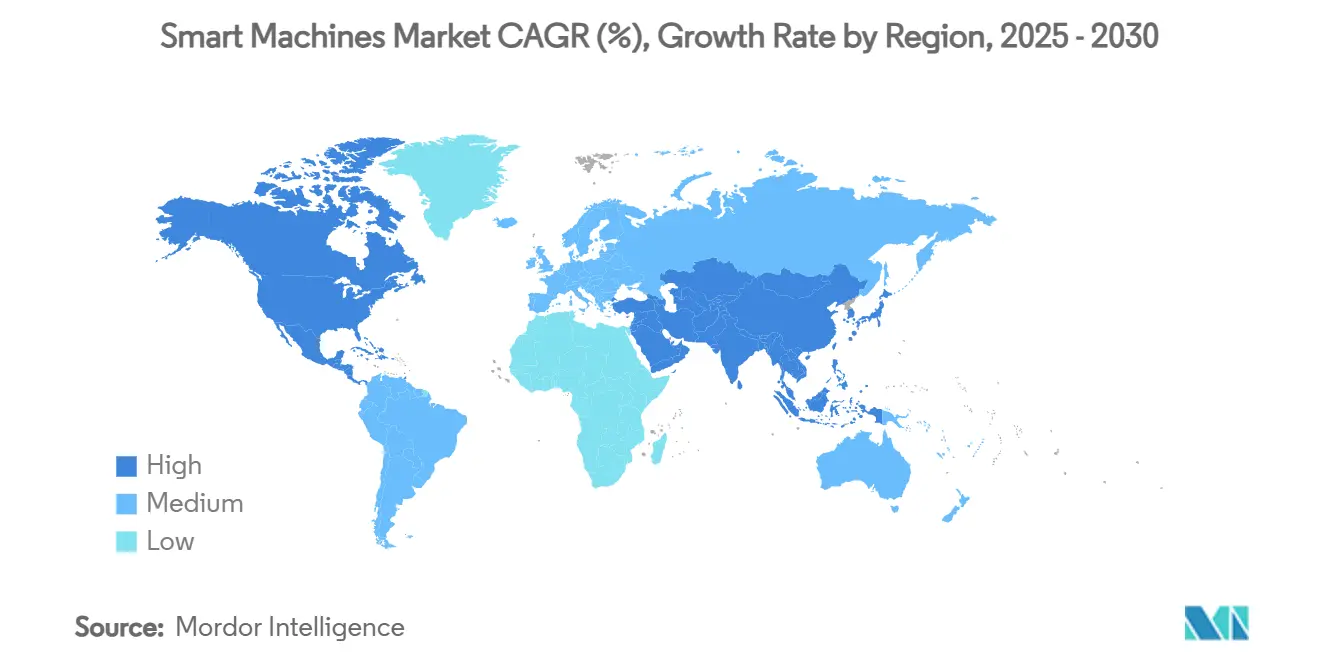

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Machines Market Analysis by Mordor Intelligence

The smart machines market size is estimated at USD 267.95 billion in 2025 and is projected to reach USD 607.57 billion by 2030, advancing at a 17.79% CAGR. Momentum comes from the commercialization of neuromorphic processors, the rapid digitalization of factories, and the spread of edge-to-cloud architectures. Hardware retains a majority revenue share as robotics, sensors, and AI accelerators remain essential, yet software expands the total addressable pool by turning machines into continuously upgradable platforms. Asia-Pacific leads on both share and growth thanks to China’s semiconductor capacity, Japan’s robotic know-how, and India’s large-scale AI infrastructure build-out. Competitive intensity is moderate because domain specialists still hold proprietary process knowledge even as hyperscalers standardize AI stacks. Cyber-security risks and capital-expenditure hurdles temper adoption, but commercialization of affective computing and autonomous mobility keeps the long-term trajectory firmly expansionary.

Key Report Takeaways

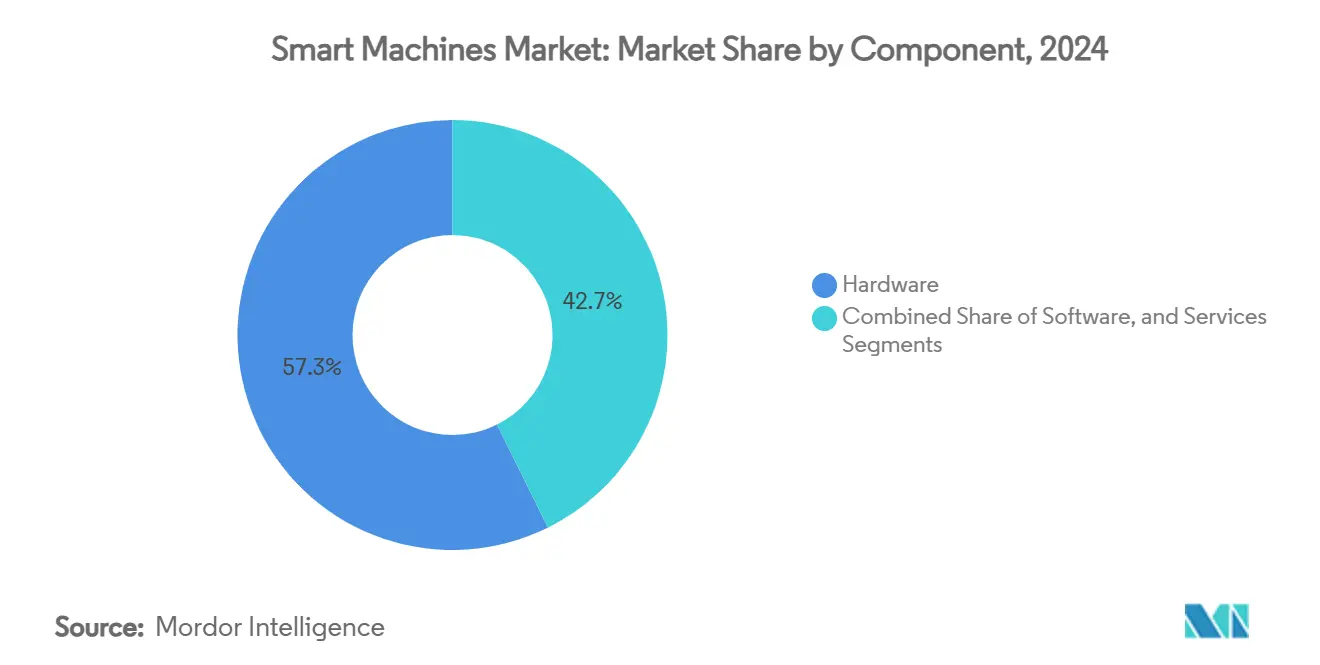

- By component, hardware held 57.32% of the smart machines market share in 2024, while software is forecast to clock the fastest 17.89% CAGR through 2030.

- By type, robots accounted for 38.31% share of the smart machines market size in 2024 and autonomous cars are set to accelerate at a 17.77% CAGR to 2030.

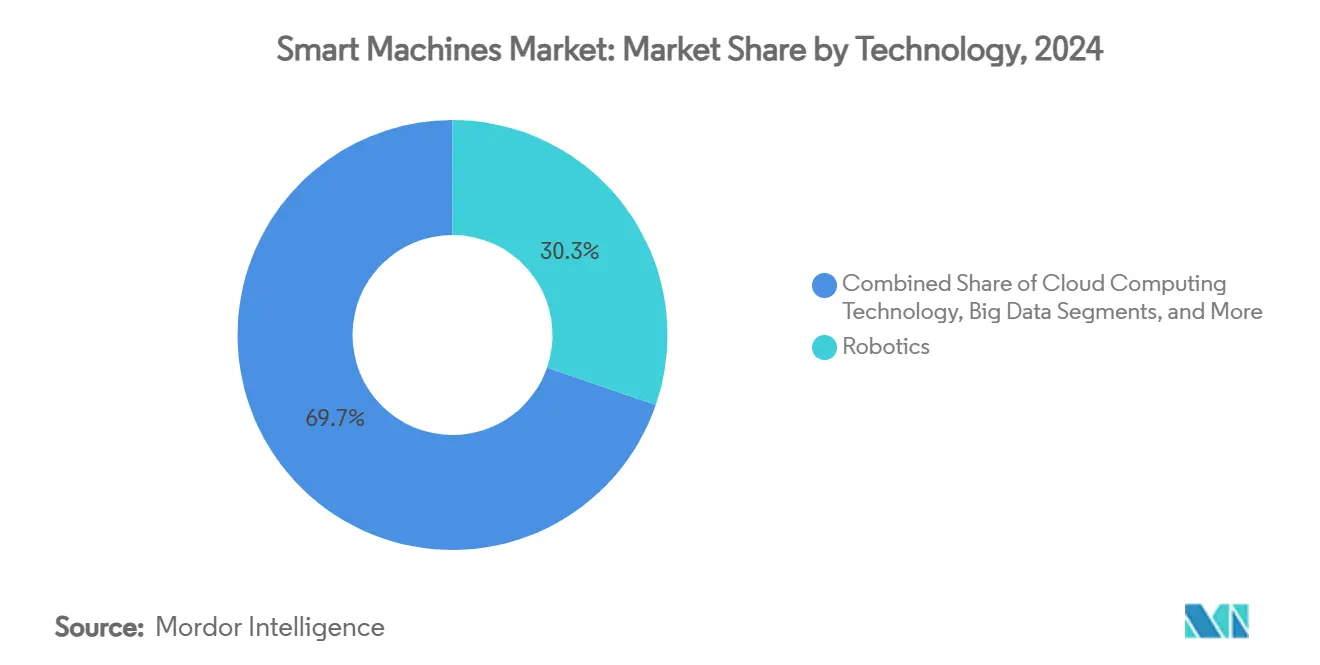

- By technology, robotics captured 30.28% share of the smart machines market in 2024; affective computing is poised to expand at a 17.96% CAGR between 2025-2030.

- By application, industrial deployments led with 27.42% of the smart machines market share in 2024, while healthcare applications are on track for a 17.88% CAGR to 2030.

- By geography, Asia-Pacific commanded 36.19% share in 2024 and is projected to compound at an 18.21% CAGR through 2030.

Global Smart Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrial-automation drive | +4.2% | Global, led by Asia-Pacific and Europe | Medium term (2-4 years) |

| AI and ML algorithmic breakthroughs | +3.8% | North America and EU leadership, Asia-Pacific acceleration | Short term (≤2 years) |

| Surging autonomy demand in mobility | +3.5% | Global, early roll-out in North America and China | Long term (≥4 years) |

| Edge-to-cloud IoT integration boom | +3.1% | Global, clusters in Germany and Japan | Medium term (2-4 years) |

| Neuromorphic processors commercialize | +2.8% | Asia-Pacific core, spill-over to North America | Long term (≥4 years) |

| Swarm-robotics adoption in intralogistics | +2.2% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid industrial-automation drive

Factories worldwide confront mounting labor gaps and quality targets. Germany deployed record robot volumes in 2024, while BMW’s Regensburg plant used AI-enabled predictive maintenance to avert 500 minutes of yearly line downtime. [1]BMW Group, “Smart maintenance using artificial intelligence,” press.bmwgroup.com Automotive lines now run more than 1,500 robots per 10,000 workers, cutting assembly defects by 70% and compressing payback to under two years. Beyond welding and painting, smart machines orchestrate quality control, material handling, and energy optimization, enabling mass-customized output at scale. The shift from stand-alone robots to self-optimizing work-cells underpins steady demand for high-precision actuators, advanced vision systems, and low-latency industrial networks. Regionally, Asia-Pacific scales fastest as manufacturers accelerate automation to offset wage inflation and demographic pressure.

AI and ML algorithmic breakthroughs

Advances in transformer-based vision and natural-language models allow smart machines to function in unstructured environments. Siemens and Microsoft trained an Industrial Foundation Model enabling natural-language queries to production assets. [2]Microsoft, “Siemens and Microsoft scale industrial AI,” news.microsoft.com NVIDIA’s Isaac platform supports cross-domain transfer learning so warehouse robots reuse autonomous-vehicle datasets, slashing annotation costs. Algorithmic progress reduces data requirements, lets machines manage edge-case scenarios, and widens the pool of addressable tasks stretching from surgical suturing to subterranean mining. Early adopters report sub-12-month model-retraining cycles, half the time needed in 2023, speeding ROI realization.

Surging autonomy demand in mobility

Transport electrification and autonomy agendas boost machine intelligence across manufacturing, fleet operation, and maintenance. Mobileye posted double-digit 2025 revenue growth on advanced driver-assist demand. [3]Mobileye, “Mobileye Releases Second Quarter 2025 Results,” ir.mobileye.comScania’s fully autonomous yard trucks and delivery robots automate last-mile logistics, compress loading times, and cut fuel burn. Governments finalizing safety frameworks add regulatory clarity, which unlocks investment in lidar, high-performance compute, and redundant actuation. Resulting learning cycles flow back into industrial robotics and drone systems, reinforcing overall smart machines market expansion.

Edge-to-cloud IoT integration boom

Hybrid architectures let devices act locally yet learn globally. Amazon saved USD 37.83 million annually by linking fulfillment-center equipment to predictive models running on AWS IoT, cutting unplanned downtime 69%. BrainChip’s Akida Pico consumes microwatts yet executes vision inference, eliminating latency faced when streaming to distant clouds. Plants employing federated learning report 20-30% jumps in overall-equipment-effectiveness as machines share insights securely through private 5G links.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and ROI ambiguity | -2.4% | Global, sharper in emerging markets | Short term (≤2 years) |

| Cyber-security and data-privacy concerns | -1.8% | Global, highest in EU and North America | Medium term (2-4 years) |

| Global talent gap in AI/robotics engineering | -1.5% | Worldwide, severe in developed economies | Long term (≥4 years) |

| Growing carbon footprint of AI compute | -1.1% | Global, with EU regulatory pressure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX and ROI ambiguity

Neuromorphic chips trim operating costs but initial outlays for robots, sensors, and connectivity remain high. ASML lithography tools face U.S. tariff hikes of 25%, exacerbating semiconductor equipment budgets. SMEs temper adoption until Robots-as-a-Service contracts prove payback. Phased rollouts, pilot cells, and performance-based financing models are gaining traction yet broad commercialization still hinges on lower entry pricing and clearer life-cycle value metrics.

Cyber-security and data-privacy concerns

Industrial robots generate multi-petabyte data streams that open novel attack surfaces. The Association for Advancing Automation warns that insufficient segmentation exposes motion-control systems to ransomware, causing months-long commissioning delays. Siemens’ Defense-in-Depth program mandates zero-trust architectures, but many brownfield plants lack monitoring tools and trained staff. Resulting risk assessments frequently defer smart-machine investment schedules by up to a year, slowing near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware foundation drives software innovation

Hardware contributed USD 153.7 billion, equal to 57.32% of the smart machines market in 2024, reflecting necessity for precision mechanics, power electronics, and domain-specific processors. Software, while smaller, is rising at 17.89% CAGR as edge-AI frameworks and low-code orchestration layers create platform stickiness. Integrated stacks mean each incremental software license multiplies performance of installed hardware, forging a virtuous upgrade loop. Service providers capture steady revenue by integrating gear across operational technology and IT domains, a role expected to widen once legacy PLCs converge with AI co-processors.

Cloud-native delivery models further compress deployment cycles. NVIDIA bundles its Jetson boards with Isaac SDK, and Siemens rolls out Industrial Copilot within its Xcelerator marketplace. This dual monetization of silicon plus code is reshaping partner ecosystems and redistributing bargaining power. As a result, hardware vendors seek software margins, and software houses co-design silicon, blurring traditional boundaries.

By Type: Robots lead while autonomous cars accelerate

Industrial, collaborative, and service robots aggregated 38.31% share of the smart machines market size in 2024, cementing leadership derived from mature supply chains and proven ROI. Autonomous cars, although nascent, headline the growth chart with a 17.77% CAGR outlook. Warehouse drones and AMRs occupy a middle ground, serving retail and logistics operators pushing same-day delivery promises.

Function consolidation is visible: Yaskawa’s MOTOMAN NEXT series combines vision, route planning, and adaptive grippers inside one envelope, eliminating external controllers. Meanwhile, automotive OEMs deploy unified compute platforms that power both plant robots and their own vehicles, symbolizing technology spill-overs. Over the forecast period, cross-domain code reuse will keep lowering autonomy costs, reinforcing demand momentum in both categories.

By Technology: Robotics dominance challenged by affective computing

Robotics technology supplied 30.28% revenue share in 2024, but affective computing, predicted to compound at 17.96% CAGR, is reshaping human-machine interaction norms. Emotion-sensing algorithms fine-tune hospital robots’ voice tone to patient anxiety levels, enhancing care outcomes. Cloud-edge orchestration, big-data analytics, and cognitive reasoning round out the stack, each layering value on basic motion control.

Edge inference boards now feature embedded accelerators for sentiment analysis, and hospitals integrating these devices report higher patient-satisfaction scores. Concurrently, cognitive technology merges symbolic reasoning with deep learning, letting smart machines justify decisions to regulators, an emerging compliance advantage in sectors such as aviation maintenance.

By Application: Industrial strength meets healthcare innovation

Industrial plants accounted for 27.42% of the smart machines market share in 2024, leveraging decades of automation investment and established KPIs. Healthcare, exhibiting a 17.88% CAGR, rides demographic change and precision-medicine mandates. Hospitals procure AI-assisted diagnostics that flag anomalies on imaging scans, and surgical suites adopt robotic arms delivering sub-millimeter accuracy.

Automotive factories integrate smart machines from stamping to final assembly, compressing takt time. Consumer-electronics makers embed AI co-processors and haptic feedback into home appliances, making everyday items participants in broader IoT ecosystems. Logistics operators deploy autonomous mobile robots that slash picker walking distances, and defense agencies test unmanned ground vehicles for perimeter patrols, widening addressable volume.

Geography Analysis

Asia-Pacific owned 36.19% of 2024 revenue and is projected to grow at 18.21% CAGR through 2030. China alone is expected to install 400,000 new industrial robots in 2025, more than 70% of East Asian demand. Japan supplies high-precision actuators and controllers to global OEMs, while India’s USD 100 billion AI-ready data-center pipeline accelerates local smart-machine uptake. South Korea’s robot density, topping 1,900 units per 10,000 workers, creates a vibrant domestic retrofit market.

Europe follows through an innovation-led posture. Germany’s factories posted record robot orders in 2024, supported by EU’s EUR 200 billion AI program that subsidizes digital twins and collaborative robotics deployments. Siemens funnels multi-billion-dollar outlays into smart-battery production and AI R&D centers, anchoring regional supply chains. France and the UK harness research institutes for surgical robotics and emotion-AI respectively, positioning the bloc as a rule-setter on ethical AI and sustainability.

North America contributes algorithmic leadership and high-value manufacturing. U.S. plants receive USD 10 billion of fresh Siemens investment to double electrical-equipment output and embed AI-driven quality analytics. Canada leverages generous tax incentives to cultivate battery-manufacturing clusters that adopt autonomous material handling. The region balances growth opportunities with stringent data-privacy and cyber-security regulations that elevate compliance costs but also raise adoption barriers for foreign vendors.

Competitive Landscape

Competition is balanced between platform leaders and domain incumbents. NVIDIA, Microsoft, and Google monetize AI toolchains that underpin many third-party robotics stacks, while Siemens, ABB, and FANUC differentiate through decades of process engineering knowledge. Moderate market fragmentation persists: the top five vendors control about 45% of global revenue, leaving room for specialists offering neuromorphic chips, swarm-robotics software, or verticalized service bundles.

Strategic moves skew toward ecosystem expansion. ABB will spin off its Robotics business after registering USD 2.3 billion revenue in 2024, aiming for sharper capital allocation and targeted M&A. Siemens collaborates with Microsoft to launch Industrial Copilot, embedding generative AI agents across the factory stack. NVIDIA aligns with Dell and IBM to create AI-native data platforms that optimize inference cost per watt.

Niche innovators capture green-field domains. BrainChip supplies ultra-low-power NPUs for battery devices, Verity deploys drones for warehouse inventory, and Innok Robotics’ INDUROS automates factory intralogistics paths. Partnership models prevail: OEMs embed startups’ technology via revenue-sharing agreements, accelerating time to market and distributing risk across the value chain.

Smart Machines Industry Leaders

International Business Machines Corporation

Alphabet Inc. (Google LLC)

Microsoft Corporation

Apple Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ABB posts record USD 9.8 billion Q2 orders and discloses intent to spin off Robotics division.

- May 2025: Siemens unveils AI agents for industrial automation within its Xcelerator platform at Automate 2025.

- April 2025: BMW commits USD 4.3 million to retrofit Munich plant for EV production using next-gen robots and AI energy optimization.

- March 2025: Siemens announces USD 10 billion investment to expand U.S. manufacturing and AI infrastructure, adding 900 jobs.

Global Smart Machines Market Report Scope

| Hardware |

| Software |

| Service |

| Robots |

| Autonomous Cars |

| Drones |

| Wearable Devices |

| Other Types |

| Cloud Computing Technology |

| Big Data |

| Internet of Everything |

| Robotics |

| Cognitive Technology |

| Affective Technology |

| Automotive |

| Consumer Electronics |

| Healthcare |

| Industrial |

| Logistics and Transportation |

| Military, Aerospace and Defense |

| Security |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Service | |||

| By Type | Robots | ||

| Autonomous Cars | |||

| Drones | |||

| Wearable Devices | |||

| Other Types | |||

| By Technology | Cloud Computing Technology | ||

| Big Data | |||

| Internet of Everything | |||

| Robotics | |||

| Cognitive Technology | |||

| Affective Technology | |||

| By Application | Automotive | ||

| Consumer Electronics | |||

| Healthcare | |||

| Industrial | |||

| Logistics and Transportation | |||

| Military, Aerospace and Defense | |||

| Security | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the smart machines market?

The smart machines market size is USD 267.95 billion in 2025.

How fast is global demand for smart machines growing?

Revenue is forecast to rise at a 17.79% CAGR between 2025 and 2030.

Which region leads adoption of smart machines?

Asia-Pacific holds 36.19% share and is also the fastest-growing region through 2030.

Which segment grows quickest within smart machines?

Software expands fastest at 17.89% CAGR as AI platforms scale across assets.

Why are manufacturers investing in smart machines?

Deployments cut defects up to 70% and enable predictive maintenance that prevents costly downtime.

What is a key risk when rolling out smart machines?

Cyber-security exposure rises as machines generate large data volumes, necessitating zero-trust defenses.

Page last updated on: