Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

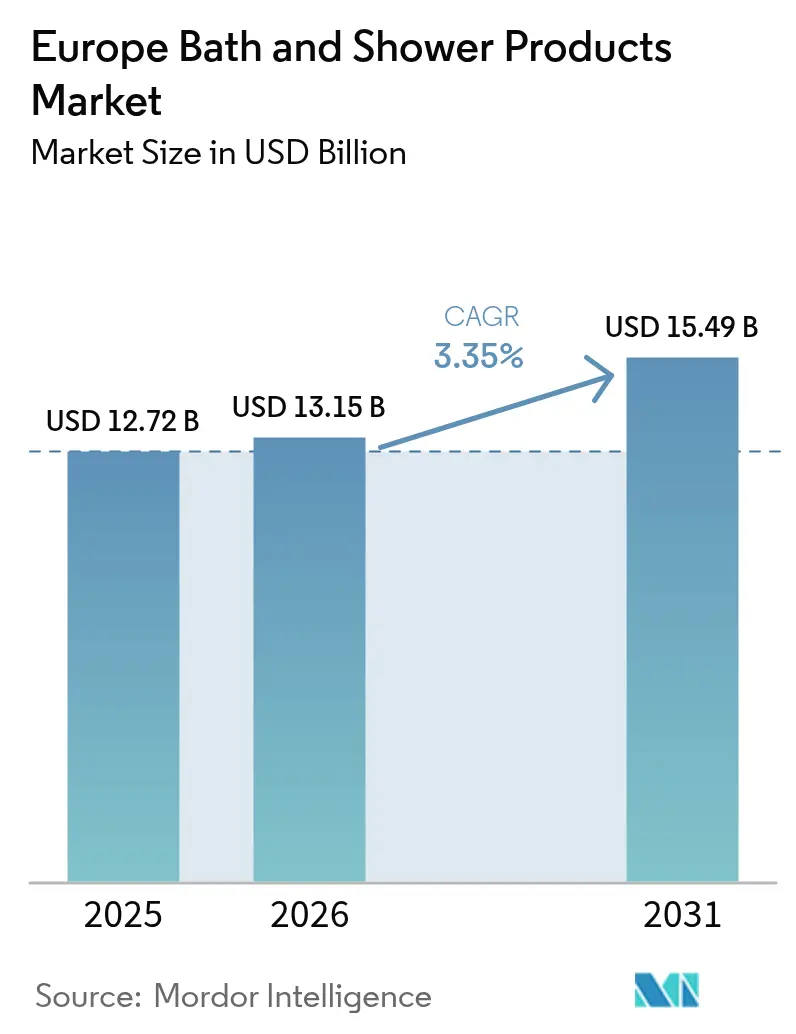

| Base Year Market Size (2025) | USD 12.72 Billion |

| Market Size (2026) | USD 13.15 Billion |

| Market Size (2031) | USD 15.49 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Bath And Shower Products Market Analysis by Mordor Intelligence

The Europe bath and shower products market size was valued at USD 12.72 billion in 2025 and estimated to grow from USD 13.15 billion in 2026 to reach USD 15.49 billion by 2031, at a CAGR of 3.35% during the forecast period (2026-2031). Regulatory mandates on packaging recyclability, ingredient transparency, and digital labeling are reshaping competitive priorities. Manufacturers are accelerating reformulation programs to phase out microplastics, PFAS, and contested preservatives, while simultaneously investing in refill stations and lightweight packaging. Supply-chain partnerships with biotechnology firms are rising as brands seek stable, bio-based inputs that de-risk palm-oil exposure. Channel fragmentation continues: brick-and-mortar drives volume, but e-commerce captures incremental value as digital discovery, subscription models, and D2C storefronts gain traction. Private-label scale-ups and discount retail expansion intensify price competition, pushing branded companies toward functional claims, sensorial upgrades, and verified sustainability data to defend shelf space.

Key Report Takeaways

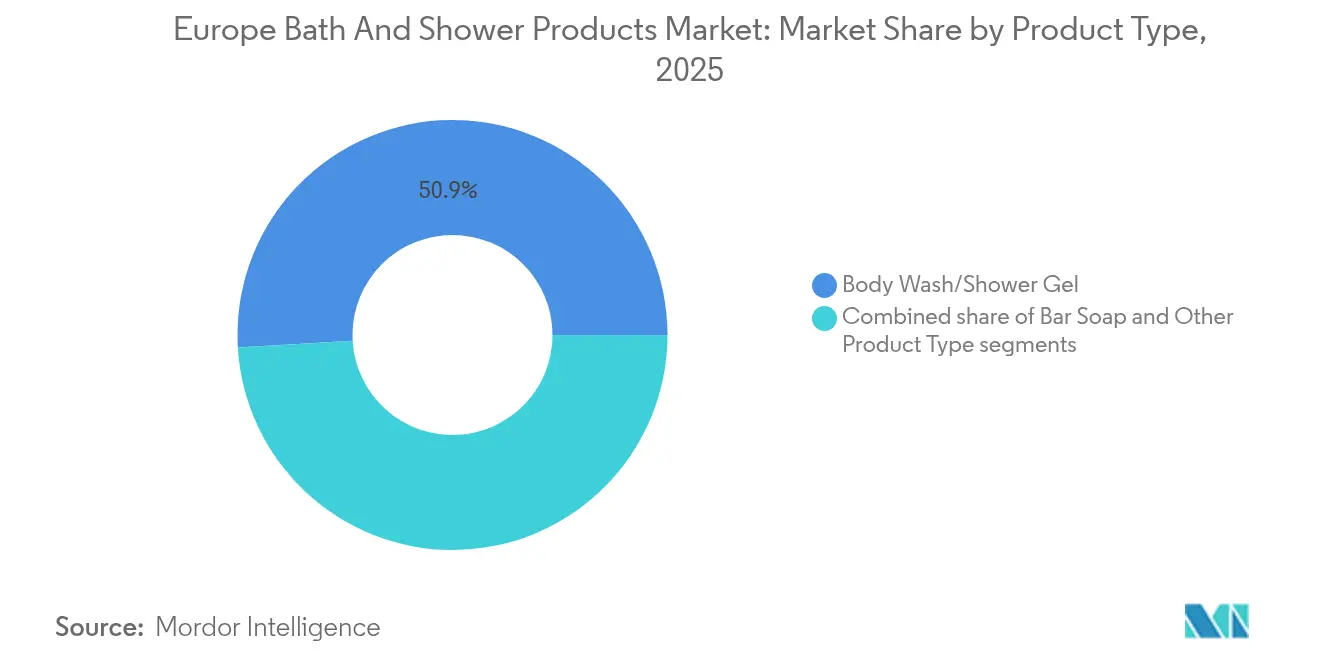

- By product type, body wash and shower gel commanded 50.92% revenue share in 2025, while bar soap is projected to advance at a 3.68% CAGR through 2031.

- By ingredient, conventional and synthetic formulations held 64.75% of the Europe bath and shower products market share in 2025; natural and organic ingredients are expanding at a 4.72% CAGR to 2031.

- By end user, adults accounted for 85.10% share of the Europe bath and shower products market size in 2025, and the kids and children segment is forecast to grow at a 5.31% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets led with 36.95% revenue share in 2025, whereas online retail stores exhibit the highest projected CAGR at 5.55% to 2031.

- By geography, Germany captured 21.20% of 2025 regional revenue; Poland is poised to record the fastest expansion at a 5.42% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Bath And Shower Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for natural and organic ingredients | +0.8% | Germany, France, United Kingdom, Netherlands, Sweden | Medium term (2-4 years) |

| Growing focus on wellness and self-care routines | +0.6% | Germany, United Kingdom, France, Italy, Spain | Short term (≤ 2 years) |

| Premiumization trends toward high-end, aromatic products | +0.5% | Germany, United Kingdom, France, Netherlands, Belgium | Medium term (2-4 years) |

| Increasing preference for sustainable and eco-friendly packaging | +0.7% | Regional (strongest in Germany, Netherlands, Sweden, France) | Long term (≥ 4 years) |

| Influence of social media and beauty influencers | +0.4% | United Kingdom, France, Spain, Italy, Poland | Short term (≤ 2 years) |

| Innovation in cruelty-free and vegan formulations | +0.3% | United Kingdom, Germany, Netherlands, Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer demand for natural and organic ingredients

Rising consumer demand for natural and organic ingredients significantly propels the Europe bath and shower products market, driven by heightened health consciousness, environmental awareness, and a shift toward clean beauty practices among millennials and Gen Z. According to the NSF 2024 survey, 74% of consumers consider organic ingredients important in personal care products, reflecting growing preference for skin-friendly, cruelty-free formulations featuring plant-based elements like aloe vera, shea butter, and essential oils [1]Source: NSF International, “Consumers Consider Personal Care Organic Ingredients Important,” nsf.org. Consumers are scrutinizing ingredient lists more carefully, with 65% seeking clear and transparent information to identify potentially harmful substances, which aligns with a broader demand for sustainable and hypoallergenic options. This trend is particularly pronounced in key markets such as Germany and Sweden, where natural labels strongly influence purchasing decisions.

Growing focus on wellness and self-care routines

Growing focus on wellness and self-care routines is a key driver of the Europe bath and shower products market, as consumers increasingly view bathing as a holistic experience that supports mental and physical well-being. This trend emphasizes products designed to relax, rejuvenate, and provide sensory pleasure, such as aromatherapy-infused gels, moisturizing creams, and exfoliating scrubs. The rise of self-care rituals, particularly among millennials and Gen Z, has led to greater demand for premium, spa-like bath products that offer therapeutic benefits. Brands are capitalizing on this by incorporating natural extracts, essential oils, and soothing ingredients to enhance the bathing experience. The UK's Office for National Statistics reported 14.69 million millennials in the United Kingdom in 2023, indicating this demographic's substantial market potential[2]Source: Office for National Statistics (UK), "Estimated population of Millennials in the United Kingdom in 2023, by single year of age and gender", ons.gov.uk . Additionally, wellness-focused consumers seek products that align with mindfulness and stress-relief practices. The market also reflects broader lifestyle shifts toward healthier habits and balanced living, reinforcing the role of bath and shower products in personal care.

Premiumization trends toward high-end, aromatic products

Premiumization trends significantly drive the Europe bath and shower products market, as consumers increasingly seek luxurious, high-quality experiences in personal care. Aromatic products, infused with exotic essential oils and natural fragrances, play a central role in this trend by offering sensory indulgence and emotional well-being benefits. This shift toward premium products reflects a growing willingness among consumers, especially affluent millennials and Gen Z, to invest in bath and shower items that provide superior textures, long-lasting scents, and sophisticated packaging. Brands respond with innovative formulations that combine efficacy with luxury, such as nourishing oils, aromatic blends, and ritualistic product lines. The premiumization trend also aligns with the rise of self-care culture, as consumers view bath time as a moment for relaxation and pampering. This movement supports higher price points and encourages differentiation within a competitive market landscape.

Influence of social media and beauty influencers

Social media and beauty influencers are powerful drivers in the Europe bath and shower products market by shaping consumer preferences and accelerating product discovery. According to a University of Portsmouth (2024) survey, 60% of consumers trust influencer recommendations, with nearly half of all purchasing decisions influenced by these endorsements [3]Source: University of Portsmouth, “New Research Unveils the "Dark Side" of Social Media Influencers and Their Impact on Marketing and Consumer Behaviour”, port.ac.uk . Influencers demonstrate product usage and share authentic reviews, creating trusted narratives that boost brand credibility and consumer engagement. Platforms like Instagram, TikTok, and YouTube amplify trends such as natural ingredients, wellness rituals, and premium fragrances, especially influencing millennials and Gen Z. These digital endorsements often generate viral product popularity, prompting brands to tailor marketing strategies to social media dynamics. The visual and interactive nature of social content enables consumers to explore sensory attributes virtually, heightening desire for innovative, aesthetically appealing bath and shower products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on chemical ingredients and safety | -0.4% | EU-wide (Germany, France, Netherlands, Sweden leading enforcement) | Long term (≥ 4 years) |

| Consumer concerns over harmful substances like parabens | -0.2% | Germany, United Kingdom, France, Netherlands, Sweden | Medium term (2-4 years) |

| Intense competition leading to price pressures | -0.5% | Poland, Spain, Italy, France (discount retail penetration) | Short term (≤ 2 years) |

| Rising manufacturing and raw material costs | -0.6% | Regional (supply-chain disruptions affecting Germany, Poland, France) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent regulations on chemical ingredients and safety

Stringent regulations on chemical ingredients and safety serve as a significant restraint in the Europe bath and shower products market, compelling manufacturers to navigate complex compliance landscapes under EU directives like REACH that restrict harmful substances such as parabens and microplastics. These mandates necessitate extensive reformulations, rigorous testing, and approval processes, which elevate production costs and delay product launches, particularly burdening smaller brands with limited resources. Frequent Safety Gate alerts result in bans and recalls of non-compliant items like shower gels and bath foams, disrupting supply chains and limiting market availability across Western Europe. Environmental requirements for biodegradable packaging and reduced plastics further intensify operational challenges, constraining innovation in synthetic-based formulations. In markets like Germany and France, multifunctional safety standards create disparities with price-sensitive Eastern regions, hindering overall affordability and market flexibility.

Consumer concerns over harmful substances like parabens

Consumer concerns over harmful substances like parabens significantly restrain the Europe bath and shower products market as awareness of potential health risks prompts demand for safer alternatives. Parabens, widely used as preservatives, face scrutiny due to associations with endocrine disruption and allergic reactions, leading consumers to avoid products containing them. This consumer caution drives brands to remove or replace parabens with natural or less controversial preservatives, increasing formulation complexity and costs. Additionally, negative perceptions around synthetic chemicals affect overall trust and slow market growth as consumers increasingly favor transparent ingredient disclosures. Regulatory bodies also impose restrictions on paraben use, reinforcing consumer apprehension and limiting product options. The rising preference for clean-label and organic bath products reflects this shift, but challenges remain in balancing safety, efficacy, and price.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Solid Formats Gain Momentum

Body wash and shower gel dominated the Europe bath and shower products market in 2025, capturing 50.92% of the revenue share. Their popularity stems from ease of use, versatility, and formulation benefits tailored for various skin types and preferences. Consumers appreciate the convenience of liquid formats in gel or creamy textures that offer moisturizing and aromatic experiences. Leading brands continuously innovate with new fragrances, natural ingredients, and dermatologist-tested formulas to maintain loyalty. Distribution through supermarkets, specialty shops, and e-commerce enhances accessibility across Europe. This segment’s large market share reflects established consumer habits and broad appeal across age groups.

Although body wash and shower gel hold the largest market share, bar soap is the fastest-growing segment, forecasted to expand at a compound annual growth rate of 3.68% through 2031. Resurgence in bar soap popularity is driven by growing consumer interest in sustainable, eco-friendly, and plastic-free personal care options. Bar soaps are perceived as natural, minimalistic, and effective cleansing alternatives aligning with environmental consciousness. Artisanal and organic varieties appeal particularly to niche consumers seeking premium and artisanal products. Additionally, bar soap manufacturing often involves simpler processes, enabling innovation in fragrances and formulations. This growth trajectory suggests bar soaps will increasingly complement and challenge liquid formats in the European market.

By Ingredient: Clean Labels Drive Reformulation

Conventional and synthetic formulations commanded the largest share of the Europe bath and shower products market in 2025, accounting for 64.75% of total revenue. Their dominance arises from widespread consumer familiarity, cost-effectiveness, and established performance in cleansing and fragrance delivery. Major brands leverage extensive distribution networks and marketing to sustain loyalty among price-sensitive and traditional users. These products benefit from advanced synthetic technologies that enhance lather, stability, and shelf life compared to natural alternatives. However, growing regulatory pressures on chemical ingredients and consumer concerns over irritants pose challenges to long-term positioning. Despite these headwinds, conventional formulations remain the market mainstay, supported by innovation in milder synthetic blends.

Natural and organic ingredients represent the fastest-growing segment, projected to expand at a compound annual growth rate of 4.72% through 2031, surpassing the overall market's 3.35% trajectory. This surge reflects heightened consumer demand for clean beauty, sustainability, and transparency in personal care routines. Brands emphasize plant-based, chemical-free profiles that appeal to health-conscious and eco-aware demographics across Europe. Certifications like ECOCERT and Soil Association bolster credibility, driving premium pricing and niche loyalty. Supply chain advancements in sourcing organic botanicals further enable scalability and formulation diversity. Ultimately, this segment's momentum signals a broader industry shift toward ethical, nature-derived products.

By End User: Kids Segment Accelerates on Safety Scrutiny

Adults accounted for the largest share of the Europe bath and shower products market in 2025, generating 85.10% of total revenue. This dominance is mainly driven by adults' substantial purchasing power and well-established personal care routines. Adult consumers show diverse product needs, ranging from basic cleansing to advanced wellness and mood-enhancing formulations. Their higher disposable incomes allow for premiumization and experimentation with multifunctional products. Additionally, product innovation focuses on addressing adult skin concerns, allergy risks, and ingredient transparency. This group remains the cornerstone of the market given their consistent consumption and broader product category reach.

The Kids and Children segment stands as the fastest-growing market category, forecasted to expand at a CAGR of 5.31% through 2031. Rising parental awareness around ingredient safety, allergen-free claims, and dermatological testing has heightened demand for specially formulated products designed for children’s sensitive skin. Brands are increasingly differentiating their offerings through premiumization and regulatory compliance to meet stringent safety standards. This focus has led to growth in hypoallergenic, gentle cleansing, and organic products tailored for younger users. The segment benefits from evolving consumer demands for transparency and trust in personal care, driving brand loyalty among families. As a result, the kids’ segment is rapidly gaining prominence alongside the dominant adult market.

By Distribution Channel: E-Commerce Reshapes Retail

Supermarkets and hypermarkets dominated the Europe bath and shower products market in 2025, capturing 36.95% of total revenue. These channels excel due to their extensive reach, offering consumers one-stop shopping for everyday personal care essentials alongside bulk purchase options. Competitive pricing, frequent promotions, and wide product assortments from leading brands reinforce their appeal to budget-conscious households. Strategic store placements across urban and suburban areas ensure high footfall and impulse buys in the bath and shower category. Shelf space dominance allows for prominent displays of new launches and seasonal variants. This segment's leadership stems from established consumer habits and unmatched distribution efficiency.

Online retail stores are poised for the strongest expansion, forecasted to achieve a compound annual growth rate of 5.55% through 2031, surpassing the overall market's 3.35% pace. Digital platforms thrive on convenience, personalized recommendations, and subscription models that lock in repeat purchases. Direct-to-consumer strategies enable brands to bypass traditional intermediaries, fostering deeper customer relationships and data-driven innovations. E-commerce growth accelerates with mobile shopping, fast delivery options, and virtual try-on features tailored for bath products. Younger demographics increasingly favor online discovery of niche, sustainable formulations unavailable in physical stores. This channel's momentum reshapes distribution dynamics, promising greater market penetration across Europe.

Geography Analysis

Germany commanded 21.20% of the European bath and shower products market revenue in 2025, leveraging its status as the region’s largest economy with a mature retail infrastructure. German consumers show strong preferences for premium and natural formulations, supported by robust environmental regulations and a well-established personal care ecosystem. The country’s emphasis on dermatologically tested and eco-friendly products contributes to sustained demand for gentle, high-quality bath items. Additionally, Germany’s demographic profile and rising awareness of health and sustainability trends further bolster market leadership. Environmental policies encouraging plastic-free and biodegradable packaging have also played a significant role in shaping consumer preferences.

Poland is forecast to grow at a 5.42% compound annual growth rate through 2031, making it the fastest-growing major market in Europe. This expansion is propelled by rising disposable incomes and increasing consumer spending on personal care products. Retail modernization, including the proliferation of modern retail formats and expanding distribution networks, fuels greater accessibility and variety. Aggressive private-label expansion by discount chains has enhanced value offerings and spurred volume growth. Poland’s evolving consumer preferences are beginning to align with broader European trends toward premiumization and natural ingredients.

The United Kingdom, France, Italy, and Spain collectively represent substantial revenue pools but face varying growth trajectories due to distinct economic and consumer dynamics. While these Western European countries maintain large, mature markets, growth rates differ due to regulatory, cultural, and competitive factors. Meanwhile, smaller but affluent markets like the Netherlands, Belgium, and Sweden exhibit strong sustainability expectations and regulatory compliance that foster niche premium segments. These countries tend to emphasize eco-conscious purchasing behaviors and strict product standards, reinforcing their roles as sophisticated, albeit smaller, contributors to the European market.

Regulatory Landscape

Bath and shower preparations in Europe are covered by Regulation (EC) No 1223/2009 on cosmetic products, which sets core obligations on product safety assessment, responsible-person requirements, and labeling and claims for products placed on the EU market. Ingredient use is governed through the Regulation annexes, including Annex II (prohibited substances) and Annex III (restricted substances), and the 2026 compliance perimeter has tightened further. Commission Regulation (EU) 2026/78, published January 2026, amended annex entries for substances classified as CMR, with application starting 1 May 2026.

Commission Regulation (EU) 2026/909, published April 2026, also amended Annexes II, III, V, and VI of the Cosmetics Regulation, including restrictions affecting substances such as Benzyl Salicylate and Triphenyl Phosphate. This reinforces the need for ongoing reformulation and stronger supplier documentation. Cosmetics makers also manage cross-cutting chemical rules, including REACH (EC) No 1907/2006 and CLP (EC) No 1272/2008, which affect classification, labeling, and the compliance status of inputs used in finished bath and shower products.

Competitive Landscape

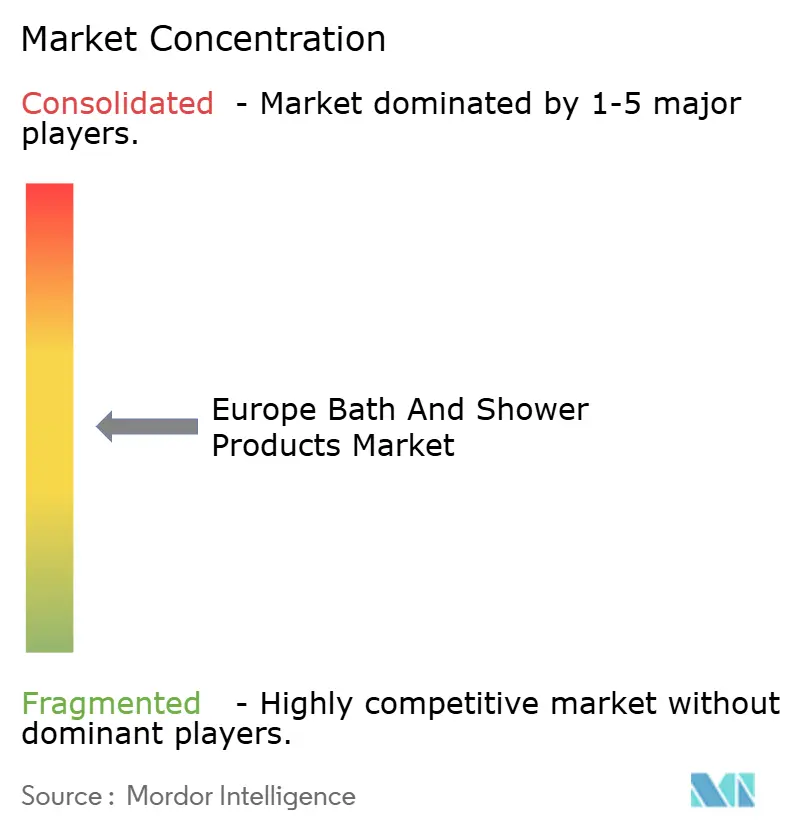

The Europe bath and shower products market displays moderate concentration, where the top five players Unilever PLC, L'Oréal S.A., The Procter & Gamble Company, Beiersdorf AG, and Henkel AG & Co. KGaA collectively command significant market share without achieving outright dominance. These multinational corporations leverage extensive brand portfolios, global supply chains, and robust marketing to maintain leadership across body washes, bar soaps, and gels. Unilever dominates with iconic brands like Dove and Lux, emphasizing skin health and sustainability initiatives. L'Oréal and Procter & Gamble counter with innovation in premium and natural formulations, capturing diverse consumer segments. Beiersdorf and Henkel focus on dermatological expertise through Nivea and Fa lines, appealing to everyday hygiene needs.

Leading firms sustain their positions through aggressive innovation, digital marketing, and sustainability commitments tailored to European consumer priorities. Unilever invests heavily in eco-friendly packaging and plant-based ingredients to align with regulatory demands and green preferences. L'Oréal utilizes social media for product launches, enhancing visibility among younger demographics seeking personalized care. Procter & Gamble emphasizes research and development for multifunctional products combining cleansing with moisturizing benefits. Beiersdorf and Henkel prioritize clinical testing and hypoallergenic claims to build trust in sensitive skin categories. These strategies foster brand loyalty amid moderate concentration, enabling top players to respond swiftly to trends like natural organics.

Moderate concentration creates fertile ground for private-label consolidation by retailers like supermarkets and discounters, which expand affordable alternatives mimicking premium features. Niche disruptors gain traction via artisanal, organic, and vegan offerings that target eco-conscious niches underserved by giants. Eastern European growth and e-commerce proliferation further fragment the landscape, allowing agile entrants to capture emerging demand. While top players hold sway through scale, challengers exploit gaps in sustainability and personalization. This dynamic balance drives overall market evolution, rewarding differentiation and adaptability. The interplay ensures vibrant competition benefiting consumers with variety and value.

Europe Bath And Shower Products Industry Leaders

-

L'Oréal S.A.

-

Beiersdorf AG

-

Unilever PLC

-

The Procter & Gamble Company

-

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory change and industry advocacy are creating room for compliant innovation in Europe, especially around ingredient substitution, digital-ready labeling content, and packaging circularity. In 2026, Commission Regulation (EU) 2026/78 (effective 1 May 2026) and Regulation (EU) 2026/909 (April 2026) updated Cosmetics Regulation annex restrictions, which in turn drives near-term demand for reformulation services, alternative preservative and fragrance systems, and more rigorous raw-material traceability that aligns with REACH and CLP requirements.

On packaging and sustainability, investment signals and policy debate indicate where companies are allocating resources and where suppliers can support commercialization. Cosmetics Europe issued multiple 2026 statements on simplifying the framework (Omnibus VI) and on the Urban Wastewater Treatment Directive (UWWTD) EPR debate, reflecting a compliance and cost-allocation agenda that feeds back into formulation choices and rinse-off product portfolios. At the same time, 2026 capacity moves such as Pierre Fabre's nearly EUR 50 million Avène plant expansion plan (to double capacity by 2029) and CHANEL's EUR 150 million fragrance manufacturing facility opening in France point to continued modernization of European production footprints, with opportunities for contract manufacturing, compliant ingredient supply, and low-impact packaging formats that fit retailer and regulatory expectations.

Recent Industry Developments

- March 2026: Dove expanded its Serum+ Oil Body Wash collection to the Canadian market, building on the earlier launch and broadening mass-retail availability. The rollout reinforces the shift toward serum-led, skincare-grade positioning in body wash, raising the competitive bar for sensorial performance and active-led formulations.

- June 2025: Procter & Gamble introduced the limited-edition Olay and Secret Summer Fizz Scent collection, including serum-infused body washes. The tie-up blends fragrance-led appeal with skincare cues, adding pressure on European bath and shower players to differentiate beyond basic cleansing through premium claims and novelty-led line extensions.

- July 2024: Dove introduced a new tiered portfolio led by Dove Advanced Care Body Wash, described as its most advanced body wash, following nearly a decade of R&D. The launch signaled a push to elevate performance credentials in mass body wash and intensified premiumization dynamics across core retail channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of bath and shower cleansing products sold across Europe, counted at the point of sale into retail and professional channels, and tracked in current US dollars for the stated years.

Scope exclusions: We exclude bath fittings and hardware, durable bathroom accessories, and services, and we also exclude hair-only and oral-care items even when sold in the same aisles.

Segmentation Overview

-

By Product Type

- Bar Soap

- Body Wash/Shower Gel

- Other Product Types

-

By Ingredient

- Conventional/Synthetic

- Natural/Organic

-

By End User

- Kids/Children

- Adult

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

-

By Country

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by setting a consistent fact base on consumption and trade flows for soaps and related personal cleansing preparations, and then aligning it with what is visible in the European retail environment. We refer to public sources such as Eurostat, national statistics offices (for example Germany and France), EU trade and customs tables, and relevant European Commission documentation tied to cosmetics rules.

To keep assumptions realistic, we also review company annual reports, investor presentations, and product label and claims guidance published by industry bodies, followed by reputed press coverage on pricing, promotions, and private-label expansion. Where needed, we use paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data to cross-check direction on volumes and mix. This desk source list is illustrative, and many other public and paid references were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what products are actually counted, how pricing changes by format, and how channel shares are moving across Europe. We speak with manufacturers, distributors, and retail-facing teams, and then cross-check with category managers and procurement respondents so the model assumptions on mix, price, and growth are not dependent on one viewpoint.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 18% | |

| Mid tier: 50% | Functional/Unit leaders: 36% | |

| Smaller Players: 19% | Managers: 46% |

Market-Sizing & Forecasting

We size Europe using a top-down model where country level personal cleansing consumption proxies, trade balances, and channel sell-through signals are reconstructed into a value pool for bath and shower products, and then split using observed format and channel mix. To keep the totals grounded, results are corroborated with selective bottom-up approximations like sampled price points by format, supplier and distributor channel checks, and a reasonability roll-up of visible category revenue pools.

Inputs that meaningfully move the model include bar-soap versus shower gel mix, private-label penetration, average selling price progression by pack size and claims, online share growth versus store-based sales, and reformulation or compliance-driven cost changes that can lift pricing. For forecasting, we lean on multivariate regression with scenario checks, where demand is tied to household consumption stability, inflation and promotion intensity, and the pace of premiumization toward natural and skin-sensitive products. Where bottom-up checks have gaps in smaller countries or niche formats, those are filled using neighboring country analogs and then normalized back to the Europe totals.

Data Validation & Update Cycle

Outputs are validated by comparing implied per-capita consumption and spend levels with independent signals like trade movements, category pricing trends, and channel share shifts discussed by interviewees. When a country shows an unusual jump in volume or price, we revisit the driver, re-check the desk inputs, and re-contact relevant respondents to confirm whether a real change occurred.

Before sign-off, the model goes through multi-step analyst reviews, where assumptions, formulas, and country splits are checked for internal consistency and for alignment with known market events. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, sharp inflation swings, or large channel disruptions. Before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Europe Bath Shower Products Market Size Measured Against Other Published Estimates

Published market numbers for Europe can look far apart because each publisher draws the market boundary differently and does not always apply the same year, currency timing, and channel coverage. Differences also show up when one study blends in adjacent personal-care categories, or when pricing is assumed to rise faster than what retail shelves and promotions suggest.

The biggest gaps typically come from what is counted as a bath and shower product, which channels are treated as in-scope, and how private-label pricing and mix are handled across countries. Some estimates also lean heavily on optimistic premiumization scenarios without re-checking the implied per-household spend, which can inflate the value pool when applied across all of Europe.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.72 B (2025) | |

| Regional Consultancy A | USD 11.48 B (2024) | Uses an earlier base year and a broader product basket that can mix in bath additives and adjacent cleansing items, and it may not normalize country pricing and channel mix to the same year currency timing. |

| Industry Publisher B | USD 18.70 B (2026) | Reported on a later year and appears to include wider wellness and professional-use demand pools, which can lift value if hotel, spa, and gym consumption is counted similarly to household retail sales. |

The table shows a clear spread that mainly follows year choice and what is included. In Mordor Intelligence's model, the Europe total is built for core bath and shower cleansing formats, with country splits tied back to mix and pricing checks so the final value can be traced to repeatable inputs. When scope and timing choices are kept consistent, it becomes easier to explain the number and to refresh it as pricing, channel shares, and product mix change.

Key Questions Answered in the Report

How large is the Europe bath and shower products market in 2026?

The market is valued at USD 13.15 billion in 2026.

What CAGR is projected for bath and shower products in Europe between 2026 and 2031?

The market is forecast to expand at a 3.35% CAGR during the period.

Which product sub-category is growing fastest in European bath and shower aisles?

Bar Soap leads growth with a 3.68% CAGR as solid formats gain sustainability favor.

Why is Poland the most dynamic national market for bath and shower products?

Rising disposable income, rapid retail modernization, and strong online uptake push Poland toward a 5.42% CAGR through 2031.

How are EU packaging rules affecting bath and shower brands?

Regulations mandate full recyclability and minimum recycled content by 2030, driving investment in refill systems and lightweight materials.

Page last updated on: