Market Overview

| Study Period | 2021 - 2031 |

|---|---|

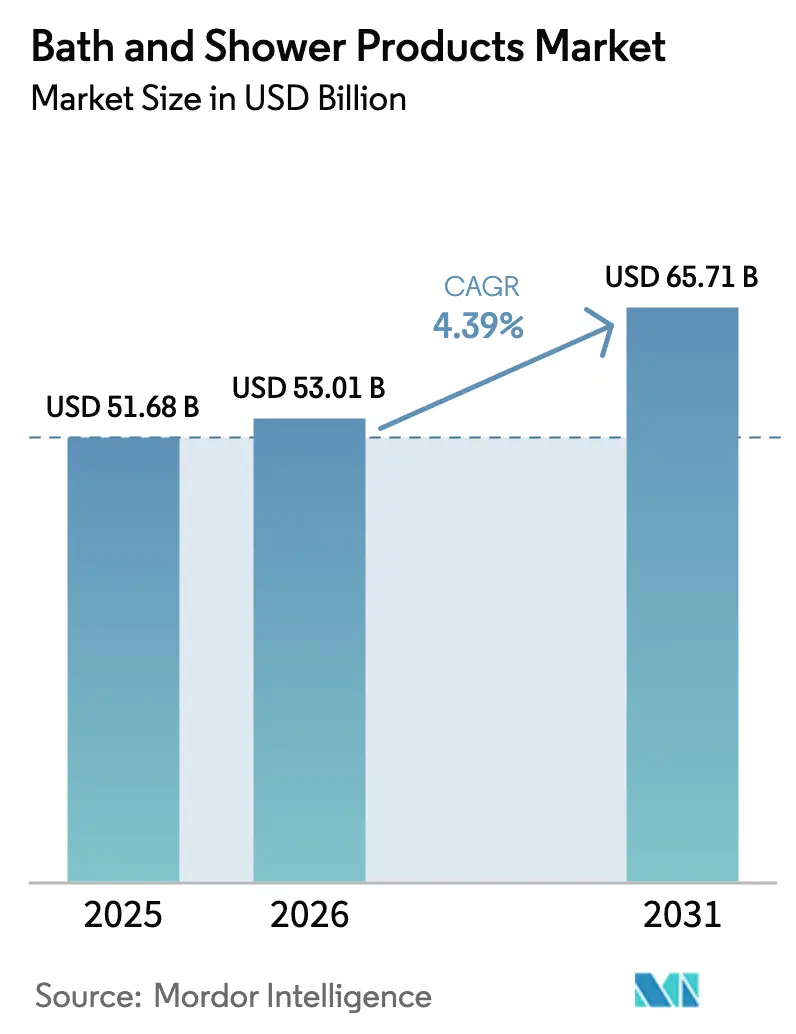

| Market Size (2026) | USD 53.01 Billion |

| Market Size (2031) | USD 65.71 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

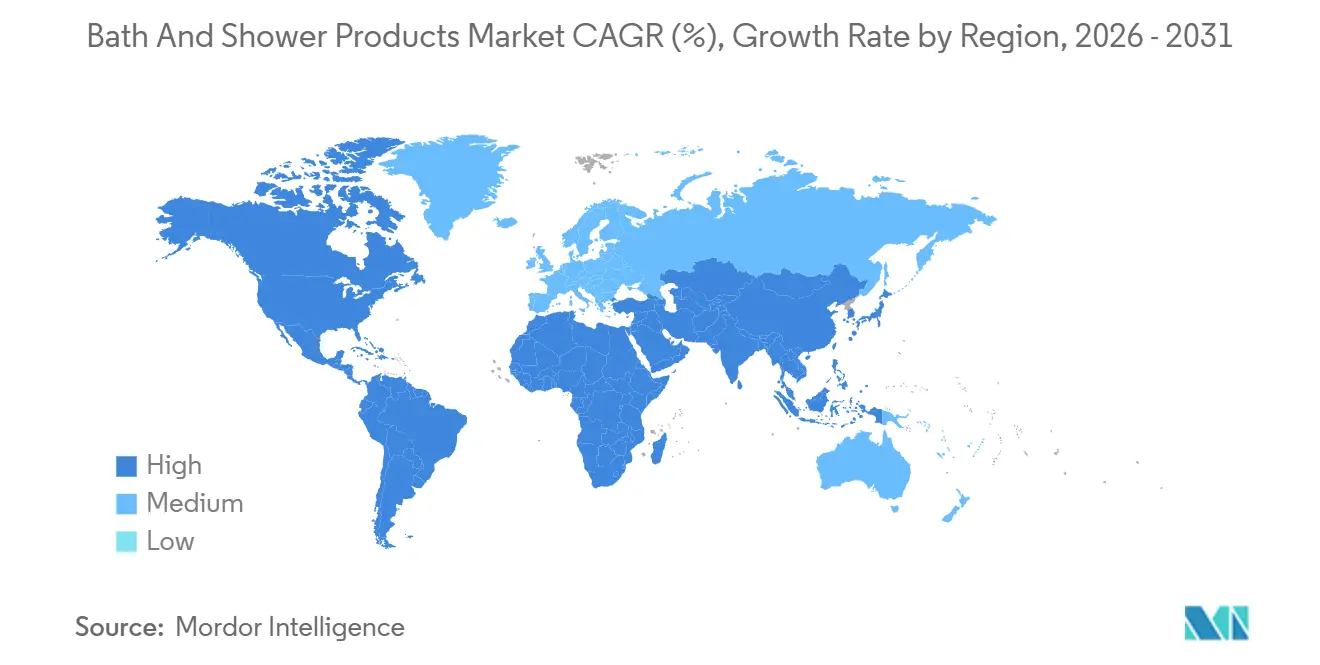

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bath And Shower Products Market Analysis by Mordor Intelligence

The bath and shower products market size is expected to grow from USD 51.68 billion in 2025 to USD 53.01 billion in 2026 and is forecast to reach USD 65.71 billion by 2031 at a 4.39% CAGR over 2026-2031. Factors such as premium positioning, ingredient transparency through certifications, and the digitization of sales channels are driving up average selling prices and broadening access in emerging urban areas. Consumers are leaning towards microbiome-friendly surfactants, pH-balanced products, and refillable packaging. This shift is steering research investments towards innovative chemistry and sustainable logistics. Industry leaders are adapting by accelerating their innovation cycles, utilizing skin-care ingredients like niacinamide and salicylic acid in body cleansing, and highlighting third-party safety audits to bolster consumer trust. Furthermore, the rise of digital discovery on social video platforms is streamlining the consumer journey, making top search visibility and endorsements from users crucial for market share. While increased regulatory scrutiny on persistent chemicals and certain preservatives is driving up reformulation costs, it simultaneously opens opportunities for nimble brands that prioritize clean-label claims from their inception.

Key Report Takeaways

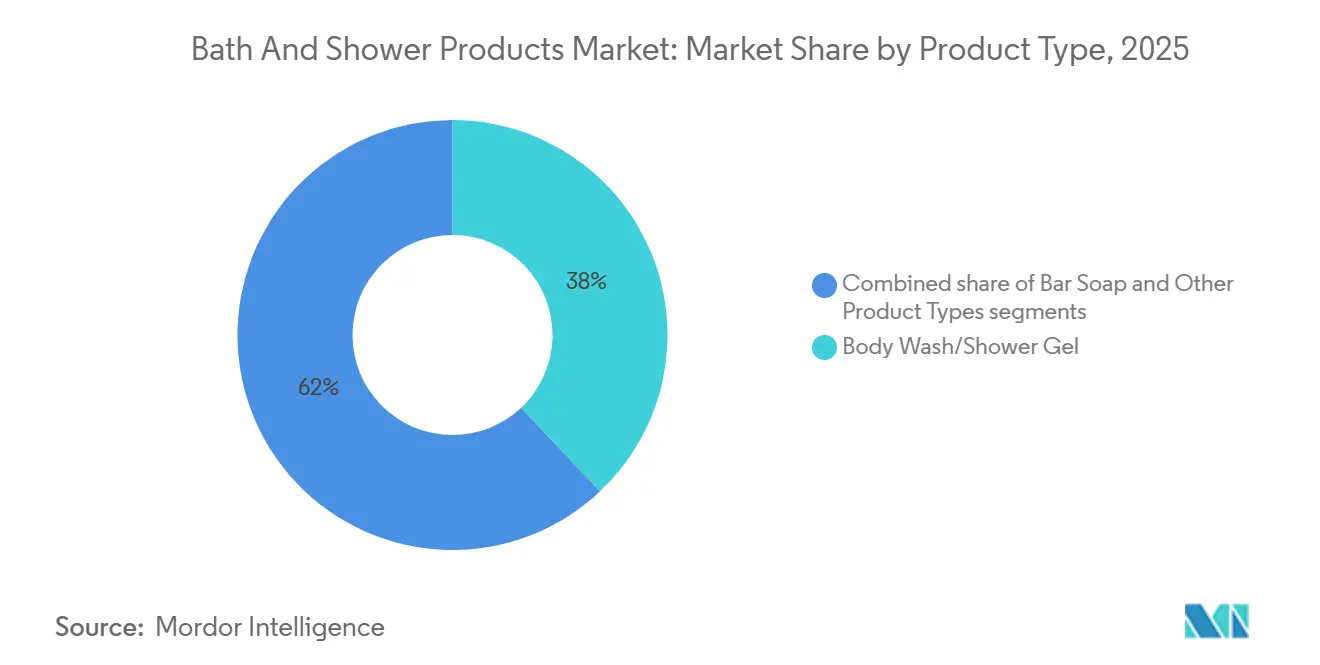

- By product type, Body Wash and Shower Gel held 37.96% of bath and shower products market share in 2025 and is forecast to advance at a 4.80% CAGR to 2031.

- By ingredient, Conventional and Synthetic inputs controlled 69.74% share of the bath and shower products market size in 2025, while Natural and Organic inputs are projected to expand at a 4.93% CAGR through 2031.

- By end user, Adults commanded 89.82% share of the bath and shower products market size in 2025, while Kids and Children lines are progressing at a 5.78% CAGR between 2026 and 2031.

- By distribution channel, Supermarkets and Hypermarkets contributed 36.57% revenue share in 2025, while Online Retail Stores are on track for a 5.96% CAGR to 2031.

- Regionally, Asia-Pacific generated 31.43% of 2025 turnover, while North America is expected to post a 5.96% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bath And Shower Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for pH-balanced, sulfate-free products | +0.8% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement | +0.6% | Global, strongest in North America, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Consumer inclination towards natural and organic products | +0.9% | Global, led by Europe and North America, is expanding in the Asia-Pacific | Long term (≥ 4 years) |

| Strong demand for products formulated with clean-label ingredients | +0.7% | North America and Europe, emerging in the Asia-Pacific tier-1 cities | Medium term (2-4 years) |

| Technological innovations in product formulations | +0.5% | Global, research and development concentrated in Japan, Germany, and the United States | Long term (≥ 4 years) |

| Increased consumer spending on self-care products | +0.4% | Global, resilient in high-income markets, volatile in emerging economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer inclination towards natural and organic products

As consumers increasingly scrutinize INCI lists with the same diligence once reserved for nutritional labels, certified organic and naturally derived ingredients have become central to differentiation strategies. Under COSMOS and Ecocert standards, rinse-off personal-care products must contain a minimum of 10% organic content by weight[1]Source: COSMOS Standard, “COSMOS v4.0 Cosmetic Organic Standard,” cosmos-standard.org. Meanwhile, the U.S. Department of Agriculture organic certification stipulates that 95% of plant-derived ingredients must adhere to organic farming protocols[2]Source: United States Department of Agriculture, “National Organic Program Handbook,” usda.gov. These regulatory benchmarks have birthed a two-tier market: brands meeting these certification standards enjoy premium shelf placements in specialty retail. In contrast, those leaning on ambiguous "natural" claims risk delisting as retailers intensify compliance audits. Unilever's Dove Naturally Good and Beiersdorf's Nivea Naturally Good showcase legacy players' commitment to certified formulations, aiming to fend off challengers like Ethique and Lush, who have carved a niche with their emphasis on naked packaging and zero-waste principles. This evolution isn't limited to ingredients; it's also about sourcing transparency. Brands revealing supplier geographies, fair-trade certifications, and biodiversity-impact assessments resonate with Gen Z and Millennial consumers, who view purchases as reflections of their values. However, the specter of greenwashing litigation, especially concerning "eco-friendly" surfactants, compels brands to back every marketing claim with third-party validation.

Growing demand for pH-balanced, sulfate-free products

Research has pinpointed the skin's optimal pH range at 5.4 to 5.9. This revelation has turned alkaline formulations, as typical body washes with a pH of 9 to 10, into a liability in premium markets, where preserving the microbiome influences buying choices. Sodium lauryl sulfate (SLS), a common sulfate surfactant, is known to disrupt the skin's lipid barrier and increase transepidermal water loss. In response, the European Medicines Agency has set concentration limits and mandated clear labeling for leave-on versus rinse-off products. Brands are now pivoting, opting for gentler amphoteric and non-ionic surfactants like cocamidopropyl betaine and decyl glucoside. These alternatives not only maintain foaming performance but also safeguard the skin's acid mantle. A testament to this industry shift is Kao Corporation's bio-IOS (isethionate) surfactant technology. It offers a sulfate-free cleansing experience with diminished irritation potential, a claim backed by clinical patch testing. While the Food and Drug Administration enforces rigorous safety substantiation under 21 CFR Part 347 for skin protectants and Part 720 for cosmetic facility registration, disclosures on pH and sulfate content remain voluntary. This oversight has created a transparency gap, which savvy consumers navigate by gravitating towards brands that openly share comprehensive formulation data. This trend is fueling a surge in premiumization: pH-balanced, sulfate-free body washes are priced 20% to 30% higher than their conventional counterparts. Yet, their growth rate outstrips mass-market products, thanks to endorsements from dermatologists and badges from clinical trials that turn skeptics into loyal customers.

Technological innovations in product formulations

Microbiome science, waterless formulations, and encapsulation technologies are reshaping the definition of "innovation" in a sector traditionally swayed by minor fragrance and packaging adjustments. Ingredients like Lactobacillus ferment lysate and Bifida ferment filtrate, both probiotic and postbiotic, are now featured in premium body washes. These ingredients, validated by peer-reviewed dermatology journals, enhance the skin's microbial ecosystem, bolstering barrier function and alleviating inflammation. Solid body-wash bars, first introduced by Lush and later expanded by Ethique, have completely removed water from their formulations. This shift not only slashes transportation emissions by up to 70% but also paves the way for plastic-free packaging, appealing to eco-conscious consumers. Encapsulation methods, such as liposomal delivery and cyclodextrin complexation, safeguard volatile actives like vitamin C and retinol from oxidation. This not only prolongs their shelf life but also supports time-release performance claims, justifying premium pricing. Unilever's innovative compressed deodorant aerosol technology, which halves the propellant volume, exemplifies how process advancements can yield both sustainability benefits and enhanced profit margins. However, navigating regulatory waters is crucial: the EU's Cosmetics Regulation (EC) No 1223/2009 mandates safety assessments for new ingredients, and Japan's Pharmaceutical and Medical Device Act necessitates pre-market notifications for quasi-drug claims. While these regulations may delay market entry, they ensure that only verified innovations reach consumers.

Influence of social media and celebrity endorsement

In 2024, academic research validated that influencers with follower counts between 100,000 and 500,000 can drive purchase intent more effectively than traditional mass-media campaigns. This is largely due to the perceived authenticity and emotional attachment audiences feel towards these influencers. Unilever's Dove Whole Body Deodorant, launched in 2024, harnessed the power of micro-influencers and user-generated content, amassing over 1 billion impressions in just 90 days and achieving an impressive USD 1 billion in annualized revenue. In China, live-streaming commerce is proving to be a game-changer. Hosts not only showcase product efficacy in real-time but also entice viewers with limited-time discounts, leading to conversion rates surpassing 20%. This starkly contrasts with the single-digit conversions seen in static e-commerce listings. Celebrity equity is also making waves: Rihanna's Fenty Skin and Pharrell Williams' Humanrace enjoy premium pricing, thanks to their personal brands' signals of inclusivity and innovation. These attributes resonate deeply with diverse consumer groups often overlooked by traditional brands. However, there's a looming challenge: as influencer marketing evolves, audiences are becoming wary of undisclosed sponsorships. This skepticism has led regulatory bodies, including the Federal Trade Commission, to mandate clear #ad disclosures and take action against misleading endorsements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.3% | Global, acute in Asia-Pacific, the Middle East, and Africa | Medium term (2-4 years) |

| Growing health concerns over product safety and ingredients | -0.5% | Global, regulatory pressure is strongest in North America and Europe | Long term (≥ 4 years) |

| Rising raw material and manufacturing costs | -0.6% | Global supply-chain dependencies in Asia-Pacific | Short term (≤ 2 years) |

| Intense market competition leading to price pressure | -0.7% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intense market competition leading to price pressure

Brand pricing power is being eroded by the growing penetration of private labels and intensified promotions across all distribution channels. In the United States and European markets, private-label bath and body products are capturing significant market share. Retailers, leveraging vertical integration and consumer price sensitivity, are extracting higher margins from branded suppliers. In response, manufacturers have streamlined product offerings to reduce complexity costs. Notably, 60% have adopted price-pack architecture changes, introducing smaller sizes and value bundles, to secure shelf space while minimizing consumer loss. This dynamic is tightening operating margins for mid-tier brands, caught between premium differentiation and mass-market scale economies. The rise of direct-to-consumer (DTC) brands is further fragmenting demand. Digital-first brands like Native and Dr. Squatch bypass traditional retail economics, investing savings into influencer marketing and subscription models for recurring revenue. Established players are countering by acquiring DTC newcomers, such as Procter & Gamble's USD 100 million acquisition of Native. However, integration challenges and cultural differences often dilute the agility that made these brands disruptive. E-commerce platforms and browser extensions like Honey and CamelCamelCamel have increased price transparency, enabling consumers to track historical pricing and optimize purchases. Consequently, brands must maintain consistent pricing to avoid reputational damage from perceived price gouging.

Growing health concerns over product safety and ingredients

Regulatory enforcement actions and consumer litigation have heightened scrutiny on ingredients, leading to reformulation cycles that strain research and development budgets and delay product launches. In November 2024, the Food and Drug Administration issued warning letters to Colgate-Palmolive's Tom's of Maine facility, citing water-system contamination with Pseudomonas aeruginosa and inadequate microbial testing protocols. This action triggered voluntary recalls and diminished consumer trust in the brand's "natural" positioning. California's PFAS ban, set to take effect in 2025, prohibits per- and polyfluoroalkyl substances in cosmetics[3]Source: California Department of Toxic Substances Control, “Safer Consumer Products Program PFAS Rulemaking,” dtsc.ca.gov. This has compelled brands to scrutinize their supply chains for hidden PFAS sources, especially in surfactants, emulsifiers, and packaging coatings. The European Union's Cosmetics Regulation (EC) No 1223/2009 lists over 1,300 prohibited substances, starkly contrasting with the fewer than 30 listed in the United States. This discrepancy presents both regulatory arbitrage opportunities and compliance challenges for global brands. Consumer advocacy groups, leveraging social media campaigns and petition drives, have amplified safety concerns. This was evident in the backlash against formaldehyde-releasing preservatives and synthetic musks associated with endocrine disruption. Brands that take the initiative to reformulate and publish safety dossiers, like Beautycounter's "Never List" of banned ingredients, can secure a competitive edge. However, the costs associated with maintaining ingredient databases, conducting clinical trials, and obtaining third-party certifications can surpass USD 500,000 per SKU, creating a significant barrier that tends to favor established players over newcomers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Formats Dominate Amid Sustainability Pressures

Waterless products are transforming the industry's environmental impact. Solid bars reduce transportation weight and eliminate plastic packaging. Brands like Lush and Ethique introduced 'naked' body-wash bars, cutting carbon emissions by 70% compared to liquids, a claim supported by lifecycle assessments. Mainstream brands now adopt these innovations to meet sustainability goals. Bar soap remains popular in price-sensitive markets and among minimal-packaging consumers, but its growth lags as younger users associate it with dryness and inconvenience. Niche products like shower oils and micellar waters lack scale to drive market growth. Body Wash/Shower Gel, with a 37.96% market share in 2025, is forecast to grow at a 4.80% CAGR through 2031, driven by refillable packaging and microbiome-friendly formulations. Unilever's Dove Body Love collection, launched in February 2024, targets body acne and stretch marks with salicylic acid and niacinamide, showcasing liquid formats' ability to incorporate complex ingredients. Kao Corporation's bio-IOS surfactant technology, used in Bioré and Jergens, offers sulfate-free cleansing with reduced irritation, appealing to dermatologically sensitive consumers.

Regulatory frameworks influence product innovation. The Food and Drug Administration's 21 CFR Part 347 governs skin-protectant claims, and Part 720 requires facility registration but imposes no format-specific restrictions, allowing brands to explore various formats. ISO 22716 ensures production hygiene, while solid bars' low water activity reduces microbial contamination, simplifying preservation and extending shelf life without synthetic preservatives. This makes solid formats viable in regions with unreliable cold-chain logistics, such as South Asia and Sub-Saharan Africa. Refillable packaging, pioneered by L'Occitane and scaled by Unilever's Love Beauty and Planet, addresses single-use plastic concerns while creating proprietary ecosystems that boost consumer lifetime value. However, reverse logistics for collection and redistribution requires significant capital, favoring large players and creating a competitive edge for refill models.

By Ingredient: Synthetic Dominance Erodes as Certification Standards Tighten

Natural and organic ingredients are projected to grow at a 4.93% CAGR through 2031, driven by certifications from COSMOS, Ecocert, and the U.S. Department of Agriculture that define "natural" and curb greenwashing. COSMOS requires 10% organic content in rinse-off products and 95% plant-derived ingredients, while the U.S. Department of Agriculture mandates that 95% of agricultural inputs meet organic standards, favoring vertically integrated suppliers. Conventional and synthetic ingredients, holding 69.74% market share in 2025, benefit from cost efficiency and performance stability but face slower growth due to regulatory scrutiny on sulfates, parabens, and synthetic fragrances. The EU's Cosmetics Regulation (EC) No 1223/2009 bans over 1,300 substances, and California's Proposition 65 enforces warnings for harmful chemicals, pressuring brands to reformulate or face restrictions.

Brands like Beiersdorf's Nivea Naturally Good and Unilever's Dove 0% Aluminum Deodorant invest in certified natural lines to compete with transparent, fair-trade-focused brands like Dr. Bronner's. Natural body washes command 20%-40% premiums over synthetic ones, with strong consumer demand driven by health and environmental concerns. However, scaling natural ingredients is challenging due to harvest variability, geopolitical risks, and limited suppliers, causing cost volatility. Brands like L'Occitane, with long-term agreements with certified organic farms, gain cost stability and values-driven marketing appeal. Bio-fermentation platforms, producing nature-identical molecules via microbial synthesis, offer a sustainable, scalable alternative that bridges synthetic and natural ingredients.

By End User: Adult Segment Dominates, Yet Pediatric Growth Signals Lifecycle Strategy

From 2026 to 2031, the kids/children's products segment is projected to grow at a 5.78% CAGR, outpacing all other end-user segments. This growth is driven by parents' focus on hypoallergenic and tear-free formulations certified under strict pediatric safety protocols. In 2025, adults held 89.82% of the market share, supported by daily routines and higher per-capita consumption. However, the pediatric segment's rapid growth highlights a shift toward lifecycle value capture. Brands securing dermatologist endorsements and hypoallergenic claims early often retain loyalty as children transition into adulthood, creating annuity-like revenue streams. Following its 2023 spin-off, Johnson & Johnson's legacy pediatric portfolio, now under Kenvue, faces competition from clean-label challengers like Pipette and Tubby Todd, emphasizing EWG-verified ingredients and transparent sourcing. While the Food and Drug Administration lacks specific pediatric personal-care standards, relying on general cosmetic safety under the Federal Food, Drug, and Cosmetic Act, industry self-regulation through the Personal Care Products Council imposes stricter limits on allergens, preservatives, and pH levels for products targeting children under three.

Legacy brands like Unilever's Dove Baby and Beiersdorf's Eucerin Baby extend brand equity into pediatric markets through dermatologist co-branding and clinical validation. The adult segment's slower growth reflects market saturation in developed regions, where consumption has plateaued. Growth now depends on premiumization rather than volume. In affluent markets, self-care spending supports the shift to premium body washes with active ingredients like retinol, vitamin C, and AHAs, blurring the line between cleansing and treatment. Gender-specific products, once a growth driver, face backlash as Gen Z consumers favor unisex or gender-neutral options. Brands focusing on benefit-driven messaging, such as "for dry skin" or "for sensitive skin", are gaining traction with younger consumers who prioritize functionality over identity-based marketing.

By Distribution Channel: Omnichannel Fulfillment Reshapes Retail Economics

Online retail stores are projected to grow at a CAGR of 5.96% through 2031, driven by China's live-streaming commerce and the U.S.'s subscription-model DTC platforms, which have shortened the discovery-to-purchase timeline from weeks to minutes. In 2025, supermarkets and hypermarkets held a 36.57% market share, leveraging basket-size economics and impulse purchases. However, their growth is hindered by rising private-label penetration, 19% in the U.S. and 38% in Europe, forcing branded suppliers to accept margin compression or risk delisting. Specialty stores, like Sephora and Ulta Beauty, along with independent natural-product retailers, offer curated premium assortments and experiential touchpoints, such as scent testing and personalized consultations, justifying higher price points but serving a narrower consumer base. Other distribution channels, including salons, spas, and direct sales, cater to niche demands but lack the scale to influence overall market dynamics. The shift to online channels accelerates as e-commerce platforms deploy AI-driven recommendation engines, augmented-reality try-on tools, and same-day delivery, replicating in-store convenience while offering broader assortments and price transparency.

Subscription models, introduced by Dollar Shave Club and scaled by brands like Native and Dr. Squatch, secure recurring revenue and reduce customer-acquisition costs by 40% to 60% compared to one-time purchases. However, managing churn remains a challenge, as subscription fatigue and economic downturns increase cancellation rates. Brands are investing in retention strategies, including personalized product recommendations, flexible delivery schedules, and loyalty rewards, which erode margin advantages. Hybrid fulfillment methods, such as click-and-collect and curbside pickup, gained traction during the COVID-19 pandemic by blending online discovery with in-store immediacy. Retailers integrating inventory visibility, real-time order tracking, and seamless returns across channels gain market share, while siloed operations lose ground to digitally native competitors.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 31.43% of total revenue, driven by rising disposable incomes, urbanization, and deepening e-commerce penetration. In China, live-streaming markets are turning product demonstrations into immediate sales boosts. Meanwhile, in India, rural strategies using sachets are cultivating brand familiarity, paving the way for future premium upsells. Japanese companies are leveraging their onsen mineral heritage and microbiome research to craft export-ready formulations, carving out prestigious niches overseas. While regulatory fragmentation across ASEAN nations increases compliance costs, digital cross-border logistics are easing market entry for smaller labels adept at navigating documentation.

North America is set to lead in value growth, projecting a 5.96% CAGR. This surge is largely attributed to stringent state-level chemical bans, prompting premium reformulations and bolstering clean-label innovators. Retail trends are shifting towards refill stations and aluminum containers, a move in sync with municipal plastic levies. Brands endorsed by dermatologists are claiming prime shelf space in pharmacies, while Gen Z is gravitating towards unisex fragrances and minimalist designs. The region's robust broadband penetration is fueling subscription services, solidifying consistent reorder cycles in the bath and shower products market. Europe, while mature in volume, is still witnessing a value uplift, thanks to sustainability premiums and narratives of clinical efficacy. The EU's ingredient blacklist has now surpassed 1,300 entries, making regulatory compliance a crucial capability that safeguards established players. In Germany, France, and the Nordics, pharmacies are amplifying therapeutic product positioning. In contrast, Southern European discounters are exerting downward pressure on unit price ceilings. Following Brexit, Britain has introduced parallel registration, adding to the paperwork but retaining its market significance, especially with its substantial prestige segment.

South America, along with the Middle East and Africa, presents a landscape of opportunities, albeit tempered by challenges in logistics and currency fluctuations. Brazilian multinationals are leveraging narratives of biodiversity and direct selling to outpace global competitors. In the Gulf Cooperation Council countries, there's a preference for fragrance-rich products and halal certifications, allowing for premium pricing despite smaller population sizes. However, in Nigeria and Egypt, the infiltration of counterfeit products is undermining brand equity. In response, brands are investing in QR-code authentication seals and rigorous distributor vetting programs.

Competitive Landscape

The Bath and Shower Products Market is moderately fragmented. The top five players, Procter & Gamble, Unilever, Colgate-Palmolive, Beiersdorf, and Kao Corporation, hold an estimated 35% to 40% market share. This leaves ample room for regional specialists and digitally native disruptors. Incumbents utilize multi-brand portfolios to cater to diverse demands. For instance, Unilever's Dove targets mass-premium consumers, Lux appeals to value-conscious buyers, and Love Beauty and Planet focuses on sustainability-minded customers. This strategy not only maximizes shelf presence but also shields the parent company from risks associated with any single brand. Technology-driven differentiation is evident in the industry's shift towards microbiome-friendly surfactants, waterless formulations, and refillable packaging systems. These innovations not only address regulatory pressures but also resonate with evolving consumer values. A case in point is Kao Corporation's bio-IOS surfactant, which offers sulfate-free cleansing with minimized skin irritation. This underscores how research and development investments can create competitive advantages that are challenging for private-label manufacturers to replicate. Meanwhile, emerging disruptors like Native, Dr. Squatch, and Ethique are sidestepping traditional retail economics. By adopting direct-to-consumer models, they're channeling savings into influencer marketing and subscription platforms, ensuring recurring revenue and reduced customer-acquisition costs.

Strategic maneuvers in the market highlight a focus on vertical integration and capturing lifecycle value. Procter & Gamble's acquisition of Native for over USD 100 million underscored the perspective that incumbents see DTC insurgents as potential acquisition targets rather than threats. However, the integration process often diminishes the very agility that made these brands disruptive. Unilever's acquisition strategy, which includes brands like Tatcha and Paula's Choice, is a move to penetrate ultra-premium segments. Here, the potential for margin expansion can counterbalance any volume declines in the mass-market tiers.

Patent filings shed light on innovation focal points: Beiersdorf is exploring encapsulation technologies for volatile actives, L'Oreal is delving into bio-fermentation platforms for nature-identical molecules, and Shiseido is advancing transdermal delivery systems, enabling body washes to double as treatment vehicles. While compliance with standards like ISO 22716 Good Manufacturing Practices and region-specific regulations, such as Food and Drug Administration's 21 CFR Part 720 facility registration in the U.S. and the EU's Cosmetics Regulation (EC) No 1223/2009, are essential, brands that surpass these minimums through third-party certifications like COSMOS, Leaping Bunny, and B Corp, carve out a competitive edge in segments driven by values.

Bath And Shower Products Industry Leaders

Procter & Gamble Company

Colgate-Palmolive Company

L’Oréal S.A.

Bath & Body Works, Inc.

Unilever Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Unilever announced a USD 150 million investment to expand its Dove body-wash production capacity in Mexico, targeting Latin American demand growth and nearshoring supply chains to reduce transportation emissions and tariff exposure. The facility will incorporate water-recycling systems and renewable-energy sourcing, aligning with Unilever's Ambition 2030 sustainability targets.

- January 2025: Beiersdorf launched Nivea Luminous630 Even Glow body wash across European markets, incorporating its patented Luminous630 ingredient that targets hyperpigmentation and uneven skin tone. The launch represents a USD 20 million R&D investment and positions the brand in the treatment-body-care segment.

- September 2024: Kao Corporation partnered with a Japanese biotechnology firm to commercialize bio-based surfactants derived from non-food biomass, targeting a 30% reduction in carbon footprint versus petroleum-derived alternatives. The partnership includes a USD 25 million joint investment in pilot-scale production.

- August 2024: L'Oreal acquired a minority stake in a French microbiome-science startup specializing in postbiotic ingredients for skin care, signaling its intent to integrate microbiome-friendly formulations across its Garnier and La Roche-Posay body-care portfolios. The investment totaled USD 15 million.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the bath and shower products market as finished consumer goods used on skin during bathing or showering, including bar soaps, liquid and gel body washes, bath additives, and specialty exfoliants and soakers. The definition aligns with the product taxonomy used in retail audits and customs codes, ensuring every value reflects sell-through to end users.

Items formulated chiefly for hair care, deodorizing sprays, oral hygiene, or disposable wipes sit outside this assessment.

Segmentation Overview

- Product Type

- Bar Soap

- Body Wash/ShowerGel

- Other Product Types

- Ingredient

- Conventional/Synthetic

- Natural/Organic

- End User

- Kids/Children

- Adult

- Distribution Channel

- Supermarkets and Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Peru

- Colombia

- Chile

- Rest of South America

- Middle East and Africa

- South Africa

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held interviews with formulation chemists, brand managers, contract manufacturers, and regional retail buyers across Asia-Pacific, North America, and Europe. These conversations tested early desk estimates, clarified emerging segments such as microbiome-friendly washes, and calibrated average selling prices in modern trade and e-commerce.

Desk Research

We begin with structured desk work that screens public sources such as UN Comtrade trade flows, Cosmetics Europe production statistics, U.S. FDA import alerts, and hygiene spend data from the World Bank. Company filings, investor decks, and labeled retail prices add channel realism. Select paid repositories, D&B Hoovers for brand financials and Dow Jones Factiva for deal tracking, supply deeper firm-level signals. Additional journals and trade magazines enrich trend context. The list above is illustrative, and many other materials were consulted to verify numbers and definitions.

Market-Sizing & Forecasting

The core model applies a top-down build that reconstructs retail demand from national production, net trade, and household spend on personal wash, which is then balanced against sampled bottom-up checks on leading supplier shipments and store-level ASP × volume snapshots. Key variables include population hygiene outlay per capita, urbanization, palm-oil feedstock prices, e-commerce share of FMCG, and premium-label penetration. Forecasts rely on multivariate regression supported by primary-research consensus for variable trajectories, with scenario analysis capturing regulatory or ingredient cost shocks.

Data Validation & Update Cycle

Outputs pass automated variance rules, peer review, and a senior sign-off. We refresh every twelve months and trigger interim updates when material events, such as sudden tariff changes or a major product recall, shift the baseline.

Why Mordor's Bath And Shower Products Baseline Earns Decision-Makers' Trust

Published estimates often diverge because firms vary product scope, selling price assumptions, and update cadence. By anchoring numbers to consistent product definitions and annually audited inputs, Mordor limits those drifts.

Key gap drivers include some publishers blending hair or deodorant lines into totals, others applying aggressive premium-price inflation, and a few projecting from pre-pandemic trends without fresh channel checks. Our model, refreshed each year, avoids such pitfalls and mirrors on-shelf realities in multiple regions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 51.78 Bn (2025) | Mordor Intelligence | - |

| USD 53.74 Bn (2025) | Global Consultancy A | Includes luxury body lotions and uses constant 2019 ASPs |

| USD 52.10 Bn (2024) | Trade Journal B | Excludes online-only private labels and uses 2020 trade ratios |

In sum, the disciplined scope choices, mixed-method validation, and clear refresh rhythm applied by Mordor Intelligence provide a balanced, transparent baseline that decision-makers can trace back to verifiable variables and reproducible steps.

Key Questions Answered in the Report

What is the projected value of the bath shower products market by 2031?

The bath and shower products market size is expected to grow from USD 51.68 billion in 2025 to USD 53.01 billion in 2026 and is forecast to reach USD 65.71 billion by 2031 at a 4.39% CAGR over 2026-2031.

Which product format leads revenue within bath and shower lines?

Body Wash and Shower Gel held 37.96% share in 2025 and retains the top position through 2031.

How quickly are natural and organic bath cleansers expanding?

Natural and organic formulations are advancing at a 4.93% CAGR thanks to rising certification uptake and ingredient transparency.

Why is North America expected to outpace global growth?

State-level chemical bans and strong clean-label adoption push North America to an anticipated 5.96% CAGR through 2031.

Which retail channel is gaining share the fastest?

Online Retail Stores are growing at a 5.96% CAGR as live-streaming and same-day delivery reshape purchase behavior.

Page last updated on: