Agricultural Pyrethroids Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

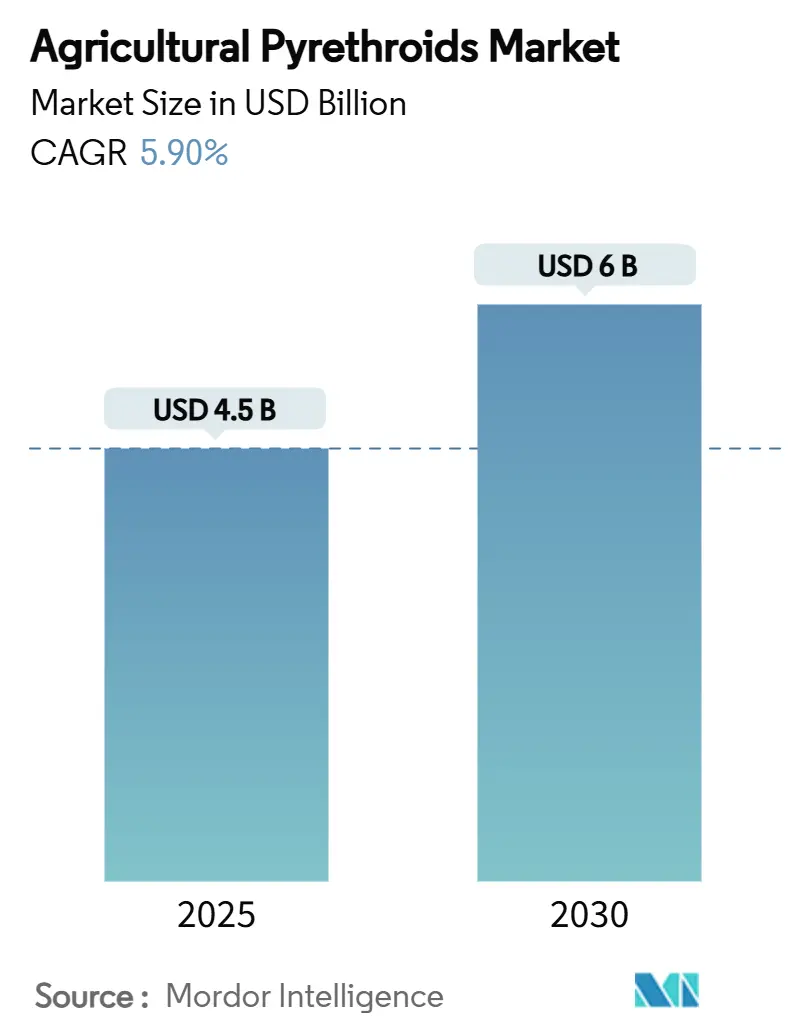

| Market Size (2025) | USD 4.5 Billion |

| Market Size (2030) | USD 6 Billion |

| Growth Rate (2025 - 2030) | 5.90% CAGR |

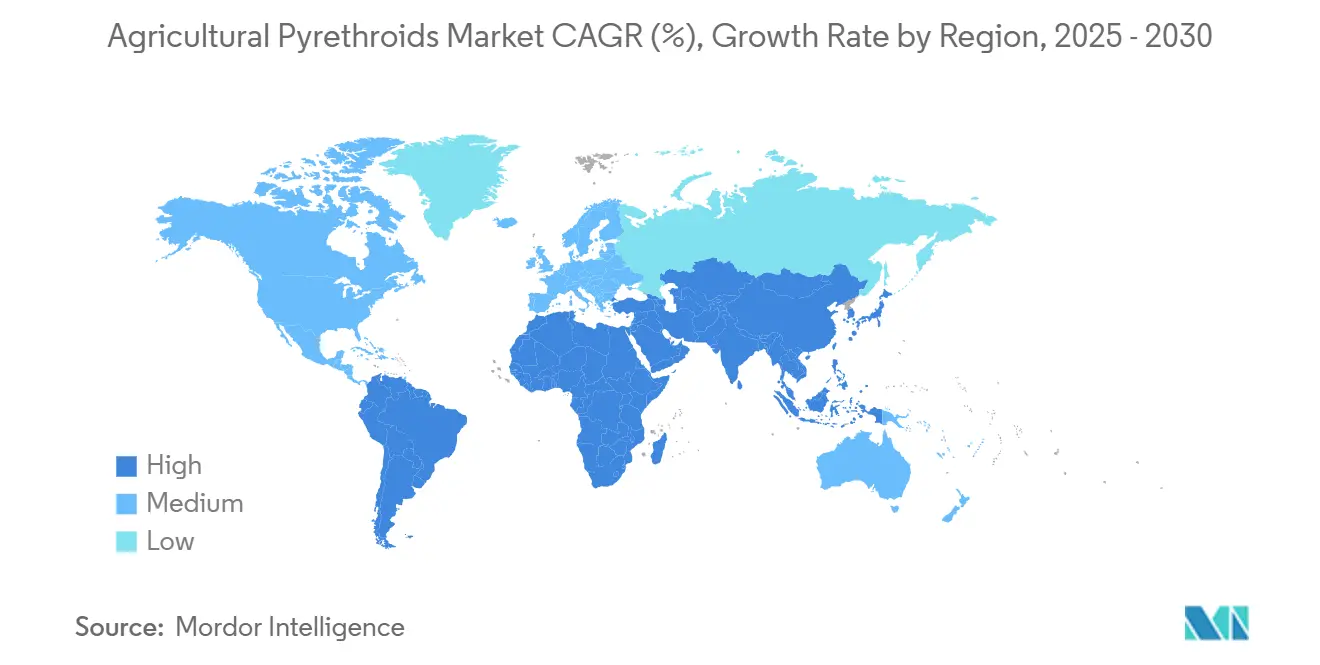

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

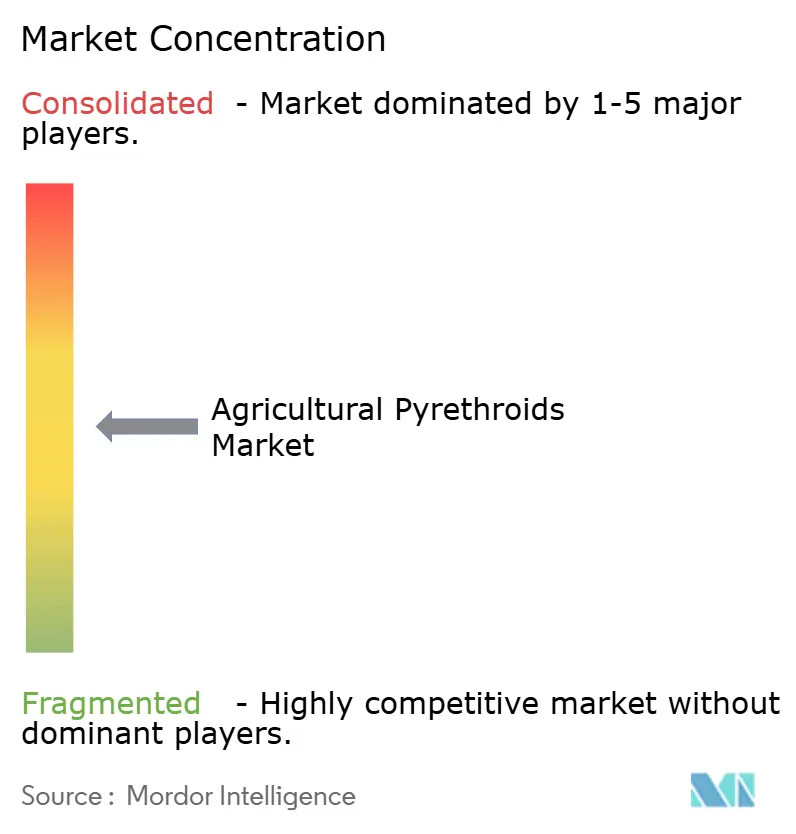

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Pyrethroids Market Analysis by Mordor Intelligence

The agricultural pyrethroids market size stood at USD 4.5 billion in 2025 and is forecast to reach USD 6.0 billion by 2030, expanding at a 5.9% CAGR. The anticipated growth reflects substitution demand created by neonicotinoid restrictions, continued expansion of soybean and cotton acreage, and rapid progress in microencapsulated low-drift formulations that satisfy tightening buffer-zone rules. Type II molecules continue to dominate the active-ingredient mix, yet dual-action blends pairing pyrethroids with complementary modes of action are expanding swiftly as resistance-management tools. Precision-spray drones and AI-guided application platforms are lowering per-acre costs and improving on-target delivery, elevating return on investment for growers who rely on pyrethroid chemistry. Finally, retailer-led pollinator-protection pledges are forcing suppliers to validate drift-reduction and residual-control claims, thereby accelerating the adoption of encapsulated products that balance efficacy and environmental compliance.

Key Report Takeaways

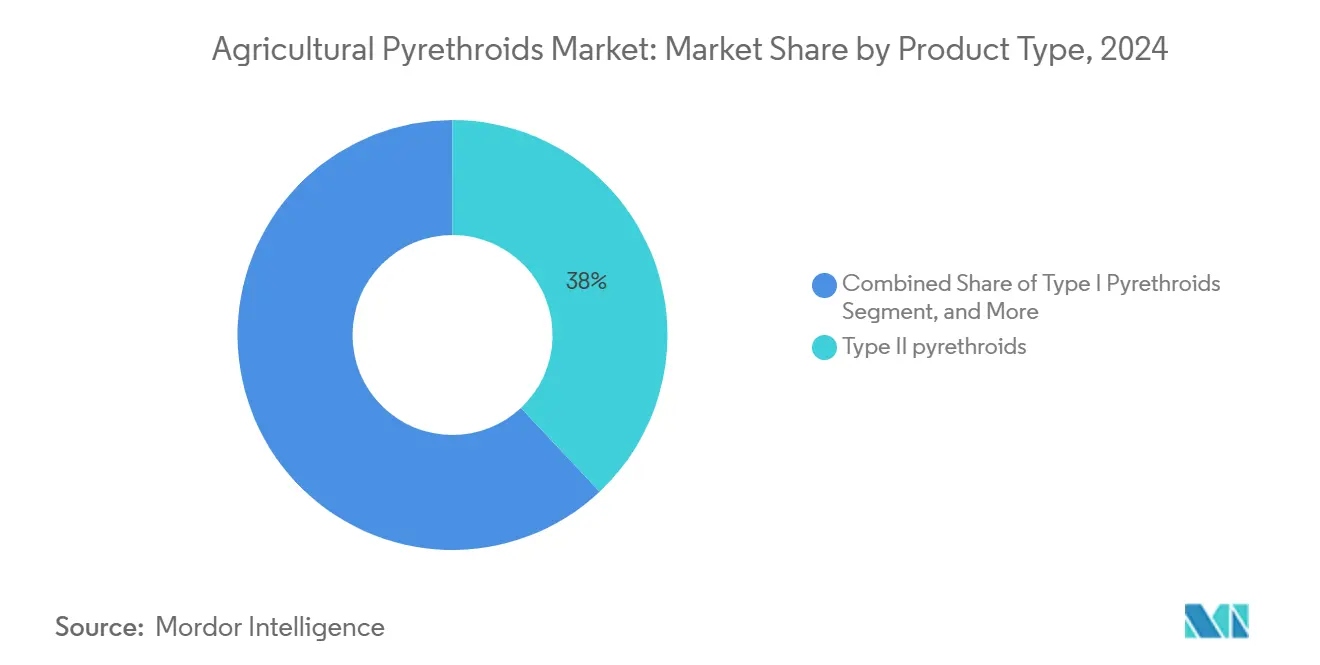

- By product type, Type II pyrethroids led with 38% agricultural pyrethroids market share in 2024, and dual-action formulations are projected to expand at an 11.8% CAGR through 2030, the fastest in the category.

- By crop type, oilseeds and pulses accounted for 46% of the agricultural pyrethroids market size in 2024, and fiber crops are forecast to grow at a 12.6% CAGR to 2030, the fastest among all crop groups.

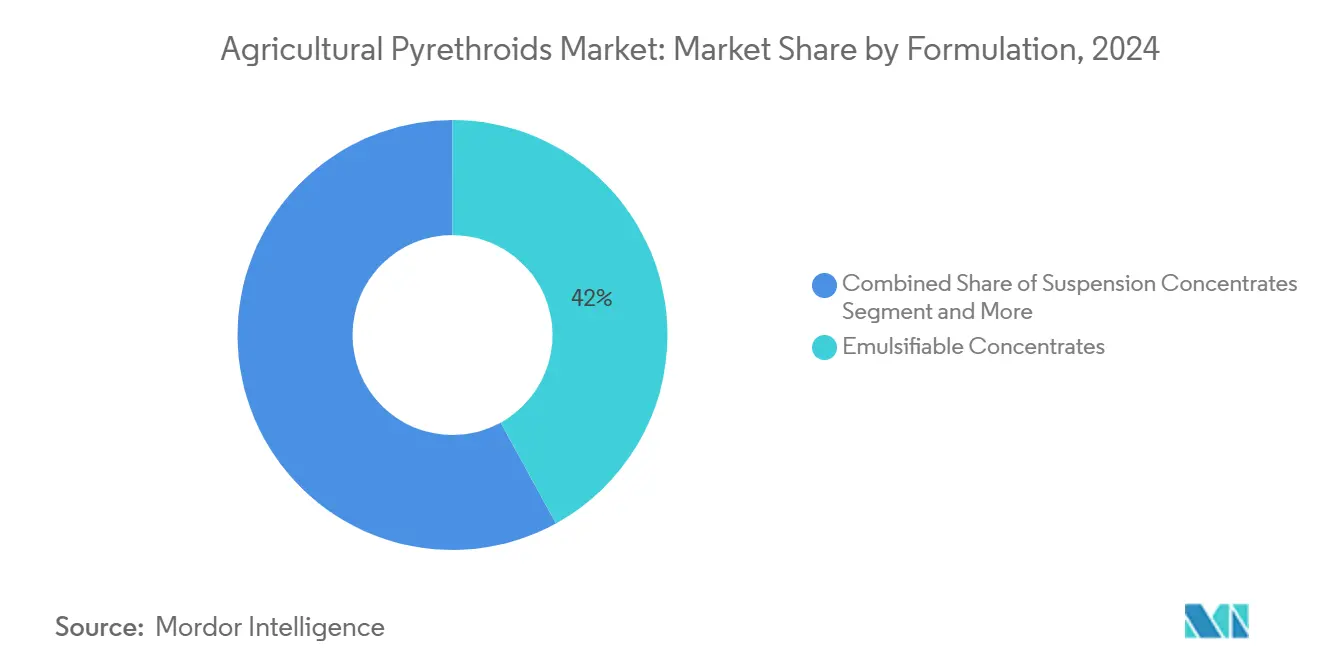

- By formulation, emulsifiable concentrates held 42% share of the agricultural pyrethroids market in 2024, and microencapsulated suspensions are advancing at a 13.2% CAGR between 2025-2030, the quickest in the formulation mix.

- By geography, Asia-Pacific dominated with 44% revenue share in 2024, and Africa is the fastest-growing region, projected at a 9.8% CAGR through 2030.

Global Agricultural Pyrethroids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating resistance to organophosphates and carbamates in major crop pests | +1.20% | Global most acute in India, Brazil, China | Medium term (2-4 years) |

| Neonicotinoid restrictions shifting acreage toward pyrethroid sprays and seed treatments | +1.80% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Expansion of soybean and cotton acreage | +1.10% | Brazil, Argentina, Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Microencapsulated low-drift formulations meeting buffer-zone rules | +0.90% | North America, Europe, Australia | Medium term (2-4 years) |

| Drone- and AI-guided precision-spray systems cutting application costs | +0.70% | Global, early uptake in developed markets | Long term (≥ 4 years) |

| Compatibility with biological tank mixes for Integrated Pest Management | +0.60% | Global, especially organic-transition regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating resistance to organophosphates and carbamates in major crop pests

Field monitoring confirms that Helicoverpa armigera in Tamil Nadu, India now shows 15-fold resistance to the organophosphate quinalphos and 8-fold resistance to the carbamate carbaryl, eliminating these chemistries as viable options in intensive cotton systems. Similar resistance ratios exceeding 100-fold have been reported in Brazil’s soybean belt and India’s central cotton zone, where decades of acetylcholinesterase-targeting sprays selected for both target-site mutations and P450-mediated metabolic detoxification. As efficacy collapses, growers are shifting rapidly to pyrethroid programs that exploit a different mode of action and retain high field-level knockdown, sustaining demand across soybean, cotton, and peanut rotations. The substitution trend is reinforced by extension-service advisories that remove organophosphate and carbamate active ingredients from local IPM guidelines, effectively redirecting procurement budgets to pyrethroid products. Because resistance mechanisms are polygenic and easily transferred across pest populations, agronomists forecast continued geographic spread of organophosphate and carbamate failure, locking in a durable demand for pyrethroid suppliers.

Neonicotinoid restrictions shifting acreage toward pyrethroid sprays and seed treatments

Californian retail bans enacted in January 2025 and the United Kingdom’s full phase-out of bee-hazardous neonicotinoids effective December 2024 have created immediate demand spikes for foliar and seed-treatment pyrethroids.[1]UCANR, “Neonicotinoid Pesticides No Longer Available,” ucanr.eduSimilar maximum residue limit thresholds in the European Union cap residues of banned neonics at 0.01 mg/kg, prompting growers to reformulate seed programs with pyrethroid chemistry that maintains plant-back flexibility. Universities tracking Midwestern corn and soybean systems find diamide–pyrethroid blends gaining share because they deliver broad-spectrum control while staying within residue guidelines. Rapid policy convergence across export-dependent economies suggests continued regulatory momentum favoring pyrethroid substitution through at least 2027.

Expansion of soybean and cotton acreage

Brazil, Argentina, and Paraguay are on track for record soybean output in 2025, enlarging the regional footprint of pyrethroid seed-treatment and foliar programs. In Sub-Saharan Africa, donor-funded agronomy projects are adding 1.6 million hectares of mechanized cotton and soybean area through 2028, translating into robust baseline demand for cost-effective insect control. Southeast Asian acreage gains in Vietnam and Myanmar further reinforce the volume outlook, ensuring the agricultural pyrethroids market continues to benefit from crop-mix shifts toward pest-susceptible broadleaf species.

Microencapsulated low-drift formulations meeting buffer-zone rules

Environmental Protection Agency revisions to Application Exclusion Zones mandate 100-foot setbacks for fine droplets, elevating drift-mitigation to compliance-critical status.[2]Federal Register, “Application Exclusion Zone Amendments,” federalregister.gov Encapsulated pyrethroids release actives slowly, lowering off-target movement by up to 57% while extending intervals between sprays. Milliken & Company’s 2023 acquisition of Encapsys strengthens the supply of biodegradable capsule walls that satisfy forthcoming EU microplastics limits. As retailers and certification bodies tighten pollinator-safety audits, encapsulated formats are rapidly becoming the preferred option for high-value fruit, vegetable, and cotton systems that must balance efficacy with environmental stewardship.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid evolution of pyrethroid-resistant Helicoverpa and Spodoptera species | -1.40% | Global, most severe in cotton belts | Short term (≤ 2 years) |

| Tighter maximum residue limits in key grain-importing regions | -0.80% | EU, Japan, South Korea | Medium term (2-4 years) |

| Accelerated uptake of GM Bt crops reducing foliar insecticide demand | -0.60% | India, Brazil, Argentina, expanding in Africa | Long term (≥ 4 years) |

| Heightened pollinator-safety scrutiny from food retailers and NGOs | -0.50% | North America, Europe, key export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid evolution of pyrethroid-resistant Helicoverpa and Spodoptera species

Intensive pyrethroid use has selected for kdr and metabolic resistance alleles in Helicoverpa and Spodoptera species, cutting field-level control and forcing growers into costly re-spray cycles. Short-season cotton in India now averages 4.5 additional sprays per hectare, raising input costs by USD 28 per hectare and accelerating resistance feedback loops. Industry consortia are funding on-farm monitoring and resistance-management education, yet adoption of rotational modes of action remains inconsistent, particularly in smallholder systems. Without widespread stewardship, resistance-driven yield losses threaten to outpace formulation gains.

Tighter maximum residue limits in key grain-importing regions

The European Food Safety Authority is reviewing deltamethrin limits in imported pulses, with provisional reductions from 0.1 mg/kg to 0.03 mg/kg under public consultation. Parallel reviews in Japan and South Korea signal a global shift toward lower tolerance thresholds. R&D pipelines now emphasize low-residue actives, synergists that degrade rapidly, and digital tools that calibrate dose to canopy density. Suppliers that can demonstrate sub-limit residue profiles stand to gain preferential procurement status with multinational grain traders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dual-action blends extend residual control

Type II pyrethroids held 38% agricultural pyrethroids market share in 2024, underpinned by broad-spectrum knockdown and established regulatory approvals. Dual-action blends are advancing at an 11.8% CAGR, leveraging complementary modes of action to mitigate resistance and widen the control window. Formulators pair lambda-cyhalothrin with diamides or spinosyns, creating premium products that command 18-25% price premiums over single-active benchmarks. Type I molecules retain relevance in specialty horticulture, where rapid knockdown during short pre-harvest intervals is critical. Ongoing patent filings indicate a robust innovation pipeline centered on synergist-enhanced capsules and rapid-breakdown ester chemistries that satisfy residue ceilings without sacrificing efficacy.

By Crop Type: Cotton drives fastest incremental volume

Oilseeds and pulses accounted for 46% of the agricultural pyrethroids market size in 2024, due to record soybean area in South America and expanding chickpea acreage in India.[3]Farmdoc Daily, “Record South American Soybean Harvest,” farmdocdaily.illinois.edu Fiber crops, primarily cotton, are forecast to post the highest 12.6% CAGR by 2030. The segment benefits from persistent lygus and bollworm pressure even in Bt-adopting regions, sustaining foliar spray frequency. Cereals and grains maintain steady demand as seed-treatment regulations tighten on neonicotinoids, while fruit and vegetable growers increasingly shift to encapsulated or dual-action pyrethroids that meet export-market residue limits and pollinator-safety protocols.

By Formulation: Encapsulated suspensions gain regulatory favor

Emulsifiable concentrates still dominate with a 42% share in 2024, favored by distributors for their price-to-performance ratio. Microencapsulated suspensions lead growth at a 13.2% CAGR as regulators, retailers, and auditors gravitate toward drift-reduction technology. Polymer-wall innovations extend residual activity, reduce photolysis losses, and enable flexible tank-mixing with biologicals. Suspension concentrates and wettable powders remain popular in price-sensitive smallholder markets, while ultra-low-volume aerosols cater to high-value orchard and greenhouse systems requiring precise droplet spectra.

Geography Analysis

Asia-Pacific dominated with 44% revenue share in 2024. Chinese policy incentives for low-toxicity formulations and India’s cotton-soybean acreage gains underpin demand. Southeast Asian rice and palm systems add incremental volume, while Australia’s strict drift standards accelerate substitution from emulsifiable concentrates to encapsulated suspensions.

Africa is the fastest-growing region, with a 9.8% CAGR, driven by donor-backed mechanization projects and government efforts to formalize agro-dealer channels. South Africa leads the adoption of precision-spray drones, and Nigeria’s private-sector warehousing reforms are improving product availability. East African horticulture exporters favor microencapsulated pyrethroids, which help meet European MRL (Maximum Residue Limit) thresholds without incurring price penalties for residue testing failures.

North America displays moderate growth, constrained by mature demand but supported by rapid uptake of AI-guided spot spraying that halves per-acre chemistry costs. The United States cotton and corn producers invest in digital scouting tools that trigger variable-rate pyrethroid applications, reducing overall load yet preserving acreage coverage. Europe remains compliance-driven, with suppliers channeling R&D toward fast-degrading esters that reconcile efficacy with forthcoming Sustainable Use Regulation targets.

Competitive Landscape

The agricultural pyrethroids market is moderately concentrated. BASF, Bayer, Syngenta, FMC, and UPL together hold the maximum market share, leaving meaningful headroom for regional specialists. Leaders leverage integrated supply chains, from technical-grade synthesis to digital farm-advisory platforms, to lock in distribution and price advantages. BASF’s capsule-suspension patents and Bayer’s AI-enabled Climate FieldView integrations exemplify bundling strategies that embed chemistry inside decision-support ecosystems.

Firms target white-space opportunities such as biodegradable wall materials and synergist combinations that address local resistance profiles. Meghmani Organics and PI Industries expand toll-manufacturing capacity in India to capture technical-grade outsourcing from multinationals seeking cost efficiency. Sumitomo and Mitsui Chemicals deepen R&D partnerships around lignin-based wall polymers that comply with Japan’s plastic-waste directives.

Strategic alliances with drone-manufacturing and farm-data startups are proliferating. Syngenta’s tie-up with Rantizo offers turnkey spray services, while FMC pilots API links between its Arc farm-decision platform and Precision AI’s long-duration drone fleet. These collaborations aim to secure product loyalty by embedding label-optimized application recipes directly into autonomous systems, strengthening brand differentiation at the point of use.

Agricultural Pyrethroids Industry Leaders

BASF SE

FMC Corporation

UPL Ltd

Bayer AG

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: FMC Corporation launched Ethos Elite LFR, a new insecticide/biofungicide premix crop protection product, for launch in the United States. The product combines bifenthrin, a proven pyrethroid insecticide, with two proprietary biological strains - Bacillus velezensis RTI301 and Bacillus subtilis RTI477. This combination provides broad-spectrum control against early-season diseases and soilborne pests.

- September 2022: FMC Corporation India expanded its portfolio by introducing three new products, including Talstar Plus insecticide, which contains Bifenthrin as a primary active ingredient. Talstar Plus protects against sucking and chewing pests that affect Indian farmers growing groundnut, cotton, and sugarcane crops.

Global Agricultural Pyrethroids Market Report Scope

| Type I Pyrethroids |

| Type II Pyrethroids |

| Dual-Action Formulations |

| Others |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Fiber Crops |

| Others |

| Emulsifiable Concentrates |

| Suspension Concentrates |

| Wettable Powders and Granules |

| Microencapsulated Suspensions |

| Aerosols and ULV |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Product Type | Type I Pyrethroids | |

| Type II Pyrethroids | ||

| Dual-Action Formulations | ||

| Others | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Fiber Crops | ||

| Others | ||

| By Formulation | Emulsifiable Concentrates | |

| Suspension Concentrates | ||

| Wettable Powders and Granules | ||

| Microencapsulated Suspensions | ||

| Aerosols and ULV | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the agricultural pyrethroids market?

The agricultural pyrethroids market size reached USD 4.5 billion in 2025 and is projected to hit USD 6.0 billion by 2030.

Which product type leads global revenue?

Type II pyrethroids lead with 38% market share in 2024, owing to broad-spectrum efficacy and longstanding registrations.

Which region is expanding fastest?

Africa is the fastest-growing region, forecast at 9.8% CAGR through 2030 as modernization programs and improved agro-dealer networks lift adoption.

How are regulations shaping product innovation?

Buffer-zone and drift-control mandates, along with tightening MRLs, are steering R&D toward microencapsulated formulations that limit off-target exposure yet sustain efficacy.

Page last updated on: