Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.65 Billion |

| Market Size (2026) | USD 13.03 Billion |

| Market Size (2031) | USD 15.09 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Breakfast Cereals Market Analysis by Mordor Intelligence

Europe Breakfast Cereals market size in 2026 is estimated at USD 13.03 billion, growing from 2025 value of USD 12.65 billion with 2031 projections showing USD 15.09 billion, growing at 2.98% CAGR over 2026-2031. The market expansion is primarily driven by increasing consumer preference for convenient and nutritious breakfast options, supported by busy lifestyles and the growing trend of on-the-go breakfast consumption. Ready-to-eat cereals dominate the market share, while hot cereals maintain steady demand, particularly in colder regions. Manufacturers are adapting to significant market shifts by focusing on health-oriented formulations and addressing supply chain challenges. Regulatory scrutiny of sugar content and acrylamide levels has prompted established players to reformulate products, creating opportunities for competitors offering products with improved nutritional profiles. Major manufacturers are introducing organic, gluten-free, and high-fiber variants to meet evolving consumer preferences. The market also experiences increased demand for private-label products, particularly in Western European countries. Additionally, the rising adoption of premium breakfast cereals and growing consumer interest in ancient grains and superfoods are creating new market opportunities.

Key Report Takeaways

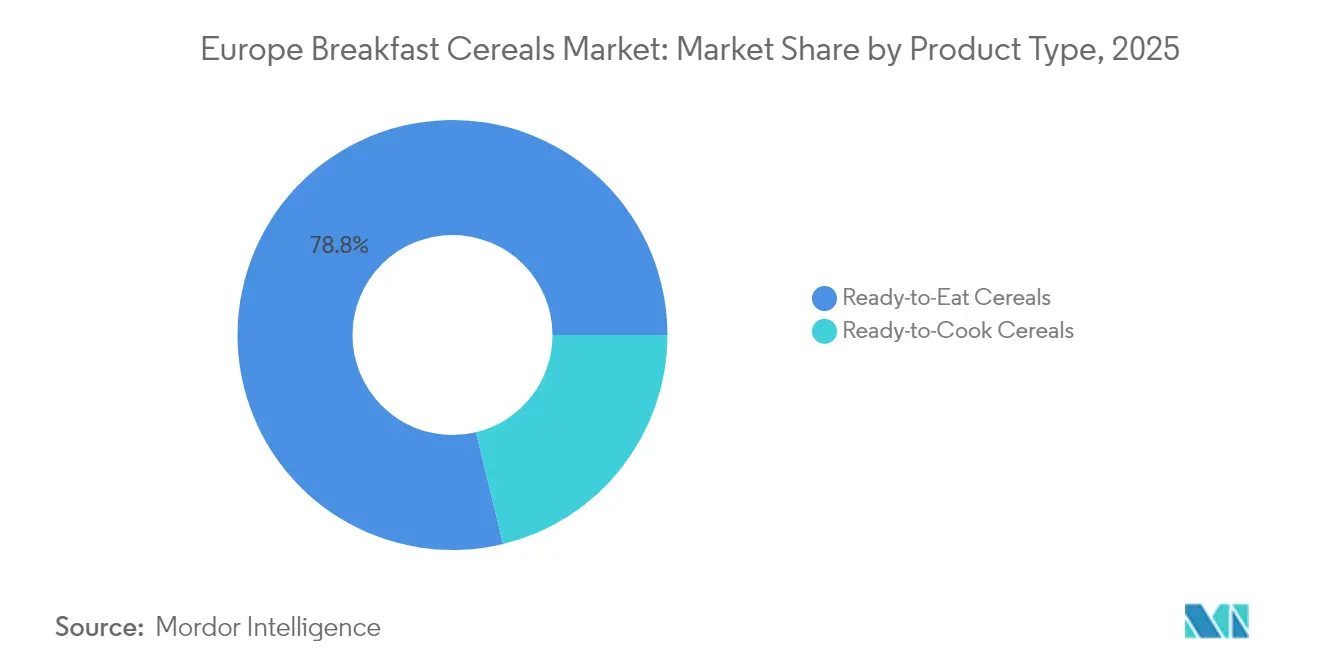

- By product type, ready-to-eat cereals dominated with 78.78% of European breakfast cereals market share in 2025, whereas ready-to-cook cereals are forecast to expand at a 5.02% CAGR through 2031.

- By ingredient source, oats commanded 34.31% share of the breakfast cereals market size in 2025; rice-based offerings are projected to grow at 4.28% CAGR to 2031.

- By packaging, traditional boxes led with 53.55% revenue share in 2025, while cups and single-serve formats are set to register an 5.21% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 60.72% of the breakfast cereals market in 2025; online retail is advancing at a 3.38% CAGR to 2031.

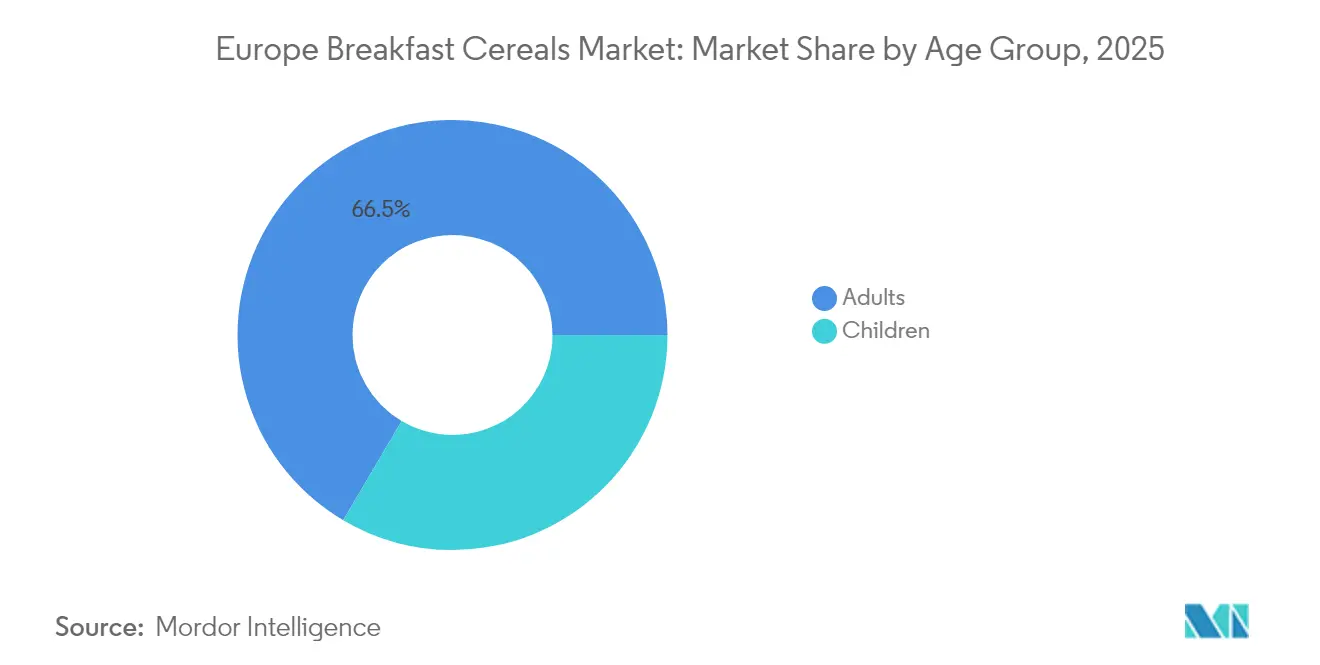

- By age group, adult-positioned products accounted for 66.51% of the European breakfast cereals market size in 2025, yet children’s cereals are poised for a 5.74% CAGR through 2031.

- By geography, the United Kingdom retained 28.18% share of the breakfast cereals market in 2025, whereas Poland is projected to record the fastest 4.78% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Breakfast Cereals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Rising demand for high-protein cereal variants among consumers | +1.5% | United Kingdom, Germany, France, Nordic countries (Denmark, Iceland, Norway, etc.) | Medium term (3-4 years) |

| Growing penetration of gluten-free grains expanding multi-grain cereals | +0.6% | Germany, United Kingdom, Italy, Spain | Medium term (3-4 years) |

| Working professionals seeking convenient and quick breakfast options | +0.5% | Pan-European, stronger in Southern and Eastern Europe | Long term (≥ 5 years) |

| Product innovation and variety cater to diverse dietary needs | +0.7% | United Kingdom, Germany, France, Nordic countries (Denmark, Finland, etc.) | Short term (≤ 2 years) |

| Surge in single-serve breakfast habits fueling on-the-go cereal cups | +0.8% | United Kingdom, France, Germany, urban centers | Short term (≤ 2 years) |

| Rise of online grocery platforms enhances accessibility and fuels demand | +0.4% | United Kingdom, Germany, France, Spain | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Protein Cereal Variants Among Consumers

Consumer preference for protein-enriched breakfast cereals is driving significant trans-formation in the European market. The trend has expanded beyond fitness enthusiasts to include mainstream consumers seeking sustained energy and satiety. The rising health consciousness among European consumers, combined with growing awareness of pro-tein's role in maintaining a balanced diet, has prompted manufacturers to develop pro-tein-enriched breakfast cereals. Consumers are increasingly selecting cereals fortified with protein sources such as quinoa, chia seeds, and various grains to support their fit-ness goals and maintain energy levels throughout the day. In response, major manufac-turers like Kellanova and Crispy Fantasy have expanded their product portfolios to include protein-rich options, incorporating ingredients such as nuts, seeds, and plant-based pro-teins. This shift aligns with the broader movement toward functional foods in the European market. The increasing focus on protein enrichment has intensified competition for quali-ty protein sources, driving manufacturers to invest in ingredient innovation and supply chain optimization.

Growing Penetration of Gluten-Free Grains Expanding Multi-Grain Cereals

The gluten-free breakfast cereals market has evolved beyond its initial focus on celiac disease patients. Consumer demand is driven by both medical requirements and lifestyle preferences, with a growing perception of gluten-free products as healthier options. Companies such as General Mills and Surreal are incorporating alternative grains like quinoa, amaranth, buckwheat, and millets into their products. For instance, General Mills offers Strawberry Vanilla Chex which is a gluten-free breakfast cereal. These cereals offer gluten-free content while maintaing unique textures and flavors. European dietitians recommend gluten-free oats and quinoa for their nutritional value and accessibility, though many alternative cereals remain unexplored despite their health benefits. The multi-grain breakfast cereals market is growing as consumers seek varied nutritional benefits from combined grain sources. The European Food Safety Authority reported in 2023 that celiac disease affects approximately 0.7% of the EU population[1]Source: European Food Safety Authority, “Safeguarding Celiac Disease Patients in Europe,” efsa.europa.eu. Manufacturers are focusing on research and development to enhance product quality while streamlining production processes to reduce costs, as gluten-free products currently sell at twice the price of traditional alternatives.

Working Professionals Seeking Convenient and Quick Breakfast Options

The resurgence of breakfast as a critical meal is fundamentally reshaping the Europe food landscape, particularly among working professionals where rising breakfast culture drives cereal consumption. According to Eurostat, employement rate in European countries in Q2 2024 was above 80% for Iceland, Netherlands, and Switzerland, above 75% for Nordic countries like denmark, sweden, Norway, among others. The increasing number of working professionals and dual-income households seek convenient and quick breakfast options, making cereals an attractive choice. This trend extends beyond traditional toast applications as consumers incorporate cereals into breakfast bowls, supported by the expansion of modern retail formats and e-commerce platforms that improve product accessibility. The growing awareness of nutritious breakfast options, coupled with manufacturers offering fortified cereals with added vitamins and minerals, contributes to market growth. According to a survey by the Agriculture and Horticulture Development Board (AHDB) in January 2025, 83% of consumers displayed positive attitudes toward healthy eating, viewing it as a form of self-care[2]Source: Agriculture and Horticulture Development Board, “Consumer Insight: Health Is All About Balance,” ahdb.org.uk. The breakfast trend's sustainability is reinforced by home-based consumption patterns established during pandemic lockdowns, which have continued even as work routines normalize.

Rise of Online Grocery Platforms Enhances Accessibility and Fuels Demand

The rapid expansion of online grocery platforms is widening access to breakfast cereals across Europe and stimulating incremental category demand. User-friendly mobile apps, subscription options, and next-day delivery services let consumers replenish pantry staples without visiting physical stores, a convenience that resonates with busy urban households. Algorithm-driven product recommendations often spotlight healthier or premium cereals, accelerating trial of high-protein, gluten-free, and multi-grain variants that might receive limited shelf space offline. Smaller brands leverage the low entry barriers of e-commerce marketplaces to reach geographically dispersed shoppers, intensifying assortment diversity and price competition. According to Eurostat, the percentage of online buyers in the European Union increased from 59% in 2014 to 77% in 2024, demonstrating the growing significance of e-commerce[3]Source: Eurostat, “E-Commerce Statistics for Individuals,” ec.europa.eu. This shift in retail dynamics has prompted established companies to adapt their strategies through direct-to-consumer initiatives, subscription models, and digital-first product launches.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Volatile oat and corn commodity prices compressing margins | -0.7% | Pan-European, stronger in Eastern Europe | Medium term (3-4 years) |

| Regulatory sugar scrutiny increasing reformulation costs | -0.5% | United Kingdom, France, Germany, Nordic countries | Medium term (3-4 years) |

| Consumer perception of processed foods | -0.4% | Pan-European, stronger in Southern Europe | Long term (≥ 5 years) |

| Competition from protein bars and RTD (Ready-to-Drink) breakfast beverages | -0.6% | United Kingdom, Germany, France, urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Oat and Corn Commodity Prices Compressing Margins

Price volatility in key cereal ingredients, particularly corn and oats, presents significant challenges. The interconnected nature of agricultural commodities means price fluctuations in one crop rapidly affect others, creating systemic pricing challenges. This volatility has intensified due to multiple factors, including geopolitical tensions, US (United States) tariffs on grains and oilseeds, and currency fluctuations, especially the dollar-euro exchange rate. Manufacturers face difficult decisions between absorbing additional costs or implementing price increases, which can affect consumer purchasing behavior. These challenges are particularly acute for premium and health-focused cereal producers, where maintaining high ingredient quality is essential. Supply chain disruptions and weather-related events, such as poor harvests and reduced crop yields in key European agricultural regions, further compound these issues, creating uncertainty in production planning and inventory management. Additionally, manufacturers struggle to maintain long-term contracts with suppliers at fixed prices during periods of high price volatility, directly impacting their production expenses and profit margins.

Regulatory Sugar Scrutiny Increasing Reformulation Costs

Regulatory pressures on sugar content present significant challenges in the European breakfast cereals market, particularly following the European Parliament's adoption of new rules for breakfast foods in April 2024 and the UK's implementation of restrictions on HFSS food promotions. These regulations require manufacturers to undertake costly reformulations while maintaining product taste, texture, and shelf stability. The challenge is particularly acute for smaller manufacturers who struggle with the financial burden of research and development costs for alternative sweeteners and new processing technologies. Beyond immediate reformulation challenges, manufacturers must also comply with stricter labeling requirements and nutritional guidelines, which add to operational expenses. The ongoing debate around sugar guidelines suggests that current regulatory approaches may oversimplify the issue, potentially leading to the use of less-studied sugar alternatives, while risking consumer rejection of altered taste profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready-to-Cook Gaining Nutritional Momentum

Ready-to-Eat (RTE) cereals maintain a 78.78% market share in Europe in 2025, driven by established consumer preferences and convenience. Ready-to-Cook (RTC) cereals demonstrate significant growth potential, with a projected CAGR of 5.02% through 2031, surpassing the market average by more than double. This expansion reflects consumers' increasing preference for hot breakfast options, which they perceive as less processed and more nutritious. Hot oatmeal dominates the RTC segment due to its recognized heart-health benefits and versatility with various toppings, including nuts, seeds, and fruits. Studies show that oat-based hot cereals provide sustained energy and improved satiety compared to RTE alternatives.

Muesli and porridge mixes show growth through premium variants and functional ingredients, while flakes constitute the largest RTE sub-segment due to production efficiency and established brand recognition. Puffed cereals and granola clusters expand their market presence through unique textures and versatile consumption occasions beyond breakfast. Manufacturers incorporate fruits and vegetables into cereal formulations to enhance nutritional content and taste profiles, addressing consumer demands for lower sugar content and improved nutritional value. This development highlights market opportunities for products that combine traditional cereal formats with enhanced nutritional benefits.

By Ingredient Source: Oats Lead While Rice Accelerates

Oat-based cereals dominate with a 34.31% market share in 2025, supported by their health benefits and versatility in ready-to-eat (RTE) and ready-to-cook (RTC) formats. The ingredient's benefits for heart health, energy provision, and digestive wellness match European consumer preferences. Rice-based cereals show the strongest growth trajectory, with a projected CAGR of 4.28% through 2031, driven by their gluten-free nature and neutral taste that accommodates diverse flavors and functional additives. Manufacturers are increasingly investing in oat and rice processing facilities to meet the rising demand and ensure consistent supply.

Wheat remains a core ingredient despite gluten concerns, while corn usage faces headwinds from price volatility and processed food perceptions. Barley's presence is growing due to its nutritional value and environmental benefits, though primarily in premium muesli and granola segments. Minor cereals, including quinoa, amaranth, and teff, are increasingly incorporated into multi-grain products. This ingredient diversification reflects both consumer interest in varied nutrition sources and manufacturers' efforts to strengthen supply chain resilience. The market is witnessing a surge in research and development activities focused on improving the nutritional profile and processing efficiency of alternative grains.

By Packaging Type: Single-Serve Disrupting Traditional Formats

Traditional boxes hold a dominant 53.55% market share in 2025, driven by efficient shelf utilization, consumer familiarity, and product protection capabilities. Cups and single-serve formats are experiencing rapid growth with an 5.21% CAGR through 2031, aligning with changing consumption habits and mobile lifestyles. These formats provide integrated solutions that eliminate the need for separate bowls and milk storage, offering true portability advantages over traditional packaging. The formats incorporate advanced barrier materials to maintain product crispness, particularly for moisture-sensitive ingredients.

Stand-up pouches combine enhanced freshness preservation with moderate portability benefits, though they do not match the convenience of single-serve options. The alternative formats, including plastic jars and bags, meet specific market requirements but encounter environmental challenges as the industry shifts toward recyclable materials. Current packaging development focuses on maintaining functionality while improving sustainability. The industry faces the challenge of balancing convenience with environmental responsibility, with emerging opportunities in compostable materials for single-serve packaging.

By Age Group: Children's Segment Outpaces Adult Market

Adult-targeted cereals hold a dominant 66.51% market share in 2025, as the category has evolved beyond its traditional positioning as children's food. The children's cereal segment is projected to grow at a 5.74% CAGR through 2031, supported by developments in nutritional content, product formats, and increased focus on breakfast quality. Manufacturers are adapting children's cereals in response to regulatory requirements and growing parental concerns about sugar content. The reformulation of children's cereals includes incorporating whole grains, reducing artificial ingredients, and introducing natural sweeteners. Market research indicates that parents are increasingly seeking cereals that balance taste appeal with nutritional benefits for their children.

The adult cereal segment is diversifying into specific categories, including weight management, active nutrition, digestive health, and indulgence. This diversification enables manufacturers to develop products that address specific health and lifestyle requirements. The distinction between adult and children's cereals continues to decrease, with products now designed to appeal across age groups while maintaining appropriate nutritional profiles. This trend indicates potential for family-oriented cereals that can meet various household preferences with a single product. Innovation in packaging formats and portion sizes has enhanced convenience for adult consumers. The integration of functional ingredients, such as protein and fiber, has strengthened the position of adult cereals as a nutritious breakfast option.

By Distribution Channel: Online Retail Disrupting Traditional Dominance

Supermarkets and hypermarkets maintain their dominance in cereal distribution, commanding a 60.72% market share in 2025. This leadership position stems from their comprehensive product selection, competitive pricing strategies, and substantial customer traffic. While convenience stores and grocery outlets continue serving as crucial distribution points due to their accessible locations and ability to capture impulse purchases, specialty stores have carved out a distinct niche by focusing on premium and health-oriented products. These traditional retail channels benefit from established consumer shopping habits and the immediate availability of products, which remains a significant advantage over online alternatives.

The online retail channel is witnessing remarkable growth at 3.38% CAGR through 2031, leveraging advantages such as extensive product ranges, subscription options, and personalized recommendations. Digital platforms effectively influence consumer behavior toward healthier choices through strategic product placement, particularly for high-fiber cereals in online listings. This digital transformation has enabled online retailers to successfully promote new brands and nutritious options that might have limited visibility in physical stores. Additionally, manufacturers are expanding into alternative distribution methods, including direct-to-consumer sales and food service, to diversify their distribution networks and strengthen customer relationships.

Geography Analysis

The United Kingdom maintains a 28.18% share of the European breakfast cereals market in 2025, supported by established consumption patterns and comprehensive retail infrastructure. The market exhibits intense competition across price segments, with private labels increasing their presence. Consumer purchasing behavior continues to shift in response to rising breakfast item prices, driving increased demand for value-based products. The UK's food security concerns are intensifying as domestic cereal production faces challenges from extreme weather conditions. These supply constraints present opportunities for manufacturers with diversified sourcing networks and robust supply chains.

Poland exhibits the highest growth potential in the European breakfast cereals market, with a projected CAGR of 4.78% through 2031, exceeding the regional average. This growth stems from increasing disposable incomes, higher urbanization rates, and changing breakfast consumption patterns. The country's domestic cereal production reached 35.2 million tonnes in 2023, constituting 13% of total EU production according to Euro Monitor data. This domestic production advantage is supporting the growth of local manufacturers like OBST S.A., which has expanded its breakfast cereal production capacity with a seventh production line, enabling the production of innovative cereal products including pillow-shaped cereals.

Germany, France, Italy, and Spain maintain stable growth trajectories with distinct consumption preferences. Germany demonstrates strength in organic and health-oriented segments, while France combines traditional breakfast options with increased cereal consumption. Italy and Spain report growing adoption rates, particularly in urban regions. Nordic countries emphasize premium products with health benefits, showing high demand for protein-enhanced and functional cereals. Russian and other European markets demonstrate varying development stages, influenced by economic conditions and retail infrastructure quality.

Regulatory Landscape

The European breakfast cereals market operates under EU food law and labeling requirements, anchored by Regulation (EU) No 1169/2011 for consumer information, including allergen declarations, and related rules on origin indications for primary ingredients. Contaminant-control rules tightened in 2024 with Commission Regulation (EU) 2024/1038 and Commission Regulation (EU) 2024/1756 updating maximum levels for key mycotoxins in cereal-based foods, effective July 1, 2024, increasing testing, supplier-qualification, and documentation needs across oats, wheat, corn, and multi-grain formulations. Updated microbiological criteria under Commission Regulation (EU) 2024/2895 set new Listeria monocytogenes limits in ready-to-eat foods with application starting July 1, 2026. Trade conditions for cereal-based preparations also evolve in 2026, as Council Regulations (EU) 2026/1455, 2026/1463, and 2026/1465 (effective July 1, 2026) adjust customs duties, autonomous tariff suspensions, and tariff quotas for certain agricultural products, influencing sourcing economics for imported inputs used in cereal preparations.

Competitive Landscape

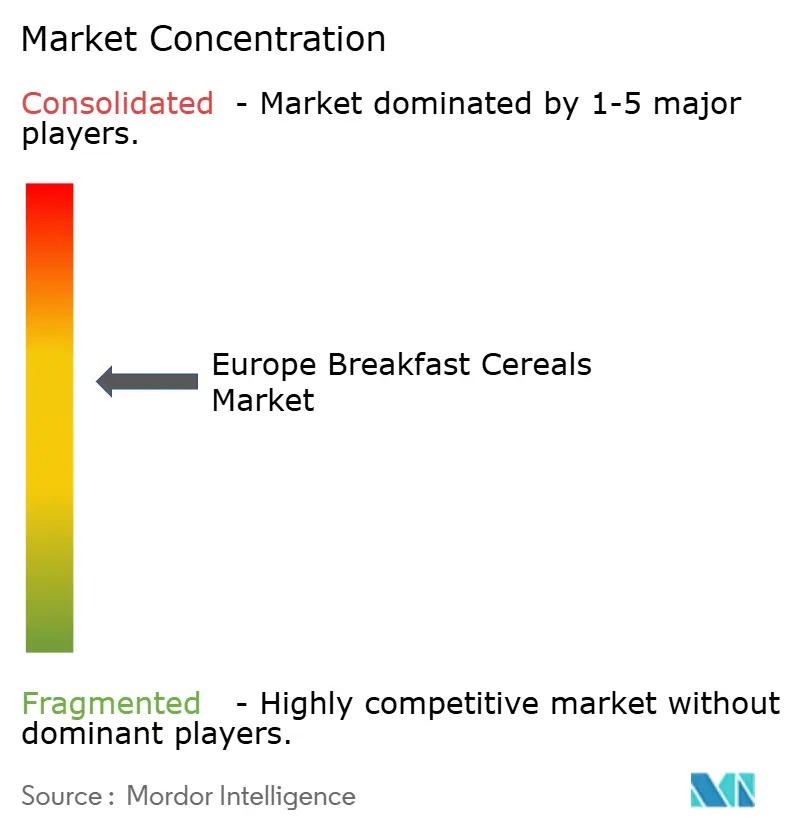

The European breakfast cereals market shows moderate concentration, with global companies like Mars, Incorporated, Nestle S.A., General Mills, Inc., and PepsiCo Inc. competing alongside regional players and growing private labels. This market structure creates margin challenges for established brands while presenting opportunities in premium segments where private labels traditionally lack market presence. The industry demonstrates a clear division between large global manufacturers and specialized companies targeting specific consumer segments.

Large manufacturers utilize their production capabilities and distribution networks while maintaining steady product development, whereas specialized companies focus on innovative formulations and direct-to-consumer sales channels. Companies are investing in expanding their production capabilities to meet consumer demand. For example, in October 2024, Kellanova invested EUR 75 million in British cereal production at its factory in Wrexham, North Wales. This investment trend reflects the industry's commitment to modernizing production facilities and meeting evolving consumer preferences.

Technology implementation centers on personalization, with the majority of consumers considering health impacts in their food choices and showing increased acceptance of AI-driven dietary recommendations. These technological developments indicate potential opportunities for breakfast cereals tailored to individual dietary requirements, which could transform the traditional mass-market model. The integration of digital technologies in product development and marketing strategies is becoming increasingly crucial for manufacturers to maintain a competitive advantage in the market.

Europe Breakfast Cereals Industry Leaders

Mars, Incorporated

Nestle S.A.

General Mills, Inc.

PepsiCo Inc,

Post Consumer Brands LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reformulation and fortification provide an innovation runway where policy pressure and retailer standards intersect with consumer demand for healthier cereals. Germany's National Reduction and Innovation Strategy (NRI) targets at least 20% sugar reduction in children's breakfast cereals by 2025, reinforcing product development programs around taste-preserving sugar reduction, whole-grain upgrades, and vitamin and mineral enrichment, while fortification remains mainstream across European cereal shelves to support differentiated claims (protein, fiber, micronutrients) that comply with EU labeling rules. Manufacturing consolidation and capacity modernization also open commercial whitespace in high-volume markets and faster-growing formats, supported by capacity investments such as Kellanova's GBP 75 million Wrexham plant upgrade announced in October 2024 and the GBP 66 million Staverton expansion approved in July 2026, which underpin deeper reformulation rollouts and broader private-label and branded portfolios across supermarkets and online channels.

Recent Industry Developments

- July 2026: Cereal Partners UK's GBP 66 million expansion at the Staverton factory receives planning approval, signaling continued investment in capacity and efficiency in UK cereal manufacturing network.

- December 2025: The European Commission granted final approval for Mars, Incorporated to acquire Kellanova in a deal reported at USD 35.9 billion, reshaping competitive dynamics in European breakfast cereals by pairing a large snacking and confectionery portfolio with established cereal brands.

- September 2024: Nestle introduced Trix cereal in Romania with fruit-shaped pieces and a formulation positioned around whole grains and added micronutrients, illustrating expansion of branded children's cereals into Central and Eastern Europe with nutrition messaging and differentiated shapes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of breakfast cereals sold for consumption across Europe, counted at the manufacturer or brand level across major cereal formats and common retail channels.

Scope exclusions: We do not count milk, yogurt, fruit, breakfast bars, or other non-cereal breakfast foods, and we exclude foodservice-only sales where they are not traceable as packaged cereals.

Segmentation Overview

- By Product Type

- Ready-to-Eat Cereals

- Flakes

- Puffed Cereals

- Granola and Clusters

- Others

- Ready-to-Cook Cereals

- Hot Oatmeal

- Muesli and Porridge Mixes

- Other Ready-to-Cook Cereals

- Ready-to-Eat Cereals

- By Ingredient Source

- Wheat

- Corn

- Oats

- Rice

- Barley

- Others

- By Packaging Type

- Boxes

- Stand-Up Pouches

- Cups and Bowls

- Others

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Specialty Stores

- Online Retailers

- Other Distribution Channels

- By Age Group

- Adults

- Children

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Sweden

- Norway

- Denmark

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on category sales, household food spending, and cross-border trade flows that influence cereal availability and pricing in Europe. We typically refer to public statistics and reference series such as Eurostat for household expenditure and trade, UN Comtrade for harmonized import-export patterns, and FAOSTAT for grain supply indicators. We also use EU level food information rules and guidance for labeling and nutrition claims to make sure category boundaries are interpreted consistently.

Next, we use company annual reports, investor presentations, and earnings call transcripts to understand revenue exposure to Europe and category-level mix shifts across key breakfast cereal formats. Trade association updates and reputable press coverage are used to sanity-check timing of pricing changes, promotions, and product launches. Select paid subscriptions are used only to speed up company financial screening, track news, and review patent activity related to ingredients and processing. These desk sources are illustrative, and additional public references are used as needed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions are used to confirm how cereal demand is moving across key European countries and to test assumptions around channel shares and price realization. We speak with manufacturers, ingredient suppliers, retailers and distributors, and category specialists so gaps from desk sources can be closed, and the final assumptions can be challenged from more than one angle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | |

| Mid tier: 44% | Functional/Unit leaders: 28% | |

| Smaller Players: 22% | Managers: 53% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where country-level packaged food consumption, household penetration for cereal eating occasions, and trade-adjusted supply signals are used to reconstruct the addressable cereal value pool. To keep totals realistic, we then corroborate the result with selective bottom-up checks such as sampled shelf pricing by format, typical weight per pack, and channel-level volume direction shared by retailers and distributors.

A few inputs that matter in this market include cereal price per kilogram movement, private label share shifts, promotions intensity in supermarkets, online grocery share for dry ambient foods, and grain cost pass-through timing, which often shows up with a lag in shelf prices. When data is thin for smaller countries, we use proxy indicators like population, retail sales index direction, and trade exposure to scale a defensible estimate, which is then challenged in interviews.

For forecasting, scenario analysis is applied around price and volume separately, and the final outlook is aligned to what industry respondents expect for household budgets and retailer pricing behavior. Assumptions are kept explicit so updates can be made quickly when inflation, promotions, or channel mix changes materially.

Data Validation & Update Cycle

Outputs are validated through triangulation across at least three angles, which usually include macro food spend signals, trade and supply direction, and company commentary on pricing and volumes. Where sharp jumps appear, we recheck the currency conversion timing, country weighting, and price per kilogram logic, then revisit the underlying assumption until the variance is explainable.

Before sign-off, the model goes through stepwise analyst reviews that focus on arithmetic checks, unit consistency, and country-level coherence with known category behavior. The report is refreshed annually, and interim updates are made when material events occur, such as tax changes, major pricing resets, or category disruption. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Europe Breakfast Cereals Market Size Measured Against Other Published Estimates

Published market values for breakfast cereals in Europe can look far apart because the scope and pricing basis are not always aligned, even when the market name sounds identical. Differences usually come from what gets counted as cereal, whether values are at retail or manufacturer level, and how countries outside the largest five are treated.

In practice, the gap also comes from how pack sizes and promotions are handled, how private label is estimated, and whether currency conversion uses an annual average or a point-in-time rate. Some publishers lean heavily on high-growth assumptions for online grocery or premiumization, while others keep a more conservative price progression, which changes the value forecast quickly when inflation is volatile.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.65 B (2025) | |

| Regional Consultancy A | USD 10.91 B (2025) | This figure appears to use a narrower value capture and may exclude parts of ready-to-cook cereals or smaller European markets, which pulls down the total even with a similar base year. |

| Industry Publisher B | USD 28.03 B (2024) | This estimate is much larger and is likely closer to retail value with broader inclusion rules across channels and end users, and it can also reflect a more aggressive price and volume growth stance. |

The table shows that the spread is mainly explained by whether pricing is counted at retail or at manufacturer level, plus how fully the Europe country set and cereal formats are included. By keeping the pricing basis consistent and checking pack-price behavior against trade and retailer inputs, the value pool stays tied to a repeatable demand logic used by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the European breakfast cereals market?

The market stands at USD 13.03 billion in 2026 and is projected to reach USD 15.09 billion by 2031.

Which is growing fastest within the product type segment of the breakfast cereals market?

Ready-to-cook hot cereals are forecast to grow 5.02% CAGR, more than double the overall category pace.

Why are single-serve cereal cups gaining popularity?

They cater to hybrid workers and commuters who need portable, no-bowl solutions, driving an 5.21% CAGR in cup formats.

How significant is online retail for breakfast cereals?

Online channels are expanding at 3.38% CAGR, leveraging personalized recommendations and broad assortments that bricks-and-mortar stores cannot match.

Which country contributes the largest share to European breakfast cereal sales?

The United Kingdom leads with a 28.18% share thanks to entrenched consumption habits and extensive retail infrastructure.

What are the major challenges confronting cereal manufacturers in Europe?

Key hurdles include volatile grain prices, stringent sugar-reformulation regulations, and competition from protein bars and ready-to-drink breakfast beverages.

Page last updated on: