Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

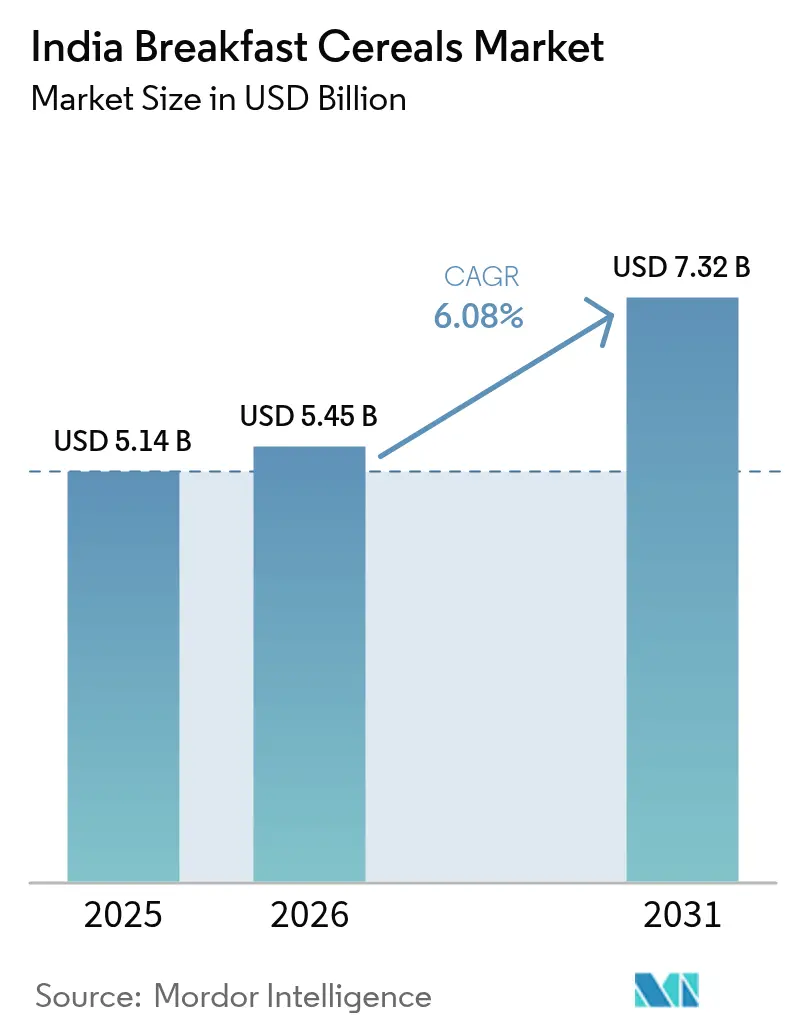

| Base Year Market Size (2025) | USD 5.14 Billion |

| Market Size (2026) | USD 5.45 Billion |

| Market Size (2031) | USD 7.32 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Breakfast Cereals Market Analysis by Mordor Intelligence

The Indian breakfast cereal market size was valued at USD 5.14 billion in 2025 and estimated to grow from USD 5.45 billion in 2026 to reach USD 7.32 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031). With increasing health awareness, consumers are opting for nutritious, low-sugar, fortified, and whole-grain cereals. Urbanization, the growth of dual-income households, government incentives, and record domestic grain production are driving a shift from traditional home-cooked breakfasts to convenient packaged options. While ready-to-eat (RTE) products dominate the market, premium offerings such as protein-fortified, organic, and millet-based cereals are expanding the market's scope. Supply-chain improvements under the PM Kisan Sampada Yojana have reduced logistics costs, and the rise of 10-to-30-minute quick-commerce deliveries is influencing impulse purchases among urban households. Additionally, record wheat and corn harvests have stabilized raw material costs, enabling manufacturers to maintain entry-level pricing while introducing higher-margin products.

Key Report Takeaways

- Ready-to-Eat cereals captured 73.82% of the Indian breakfast cereal market share in 2025, whereas Ready-to-Cook cereals are on track to expand at a 6.62% CAGR through 2031.

- Corn-based varieties accounted for a 40.75% share of the Indian breakfast cereal market size in 2025, but oat-based cereals are projected to grow at a 6.93% CAGR to 2031.

- Conventional products retained 76.15% of the Indian breakfast cereal market size in 2025, yet organic lines are advancing at a 7.35% CAGR through 2031.

- Boxes dominated packaging with 64.55% revenue share in 2025; cups and bowls are the fastest growers at 7.16% CAGR to 2031.

- Supermarkets and hypermarkets controlled 60.98% of India's breakfast cereal market share in 2025, while online retail is surging at an 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Breakfast Cereals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health-conscious consumer base | +1.2% | National, with early gains in metros, Bangalore, Mumbai, Delhi | Medium term (2-4 years) |

| Premiumization via protein-fortified SKUs | +1.0% | Urban centers, Tier-1 cities with high disposable income | Short term (≤ 2 years) |

| Rising demand for Ready-to-Eat cereals | +0.8% | National, accelerated in dual-income household clusters | Medium term (2-4 years) |

| Increasing dual-income households | +0.9% | Metro cities, emerging Tier-2 urban centers | Long term (≥ 4 years) |

| Shift in consumer preferences toward clean-label products | +0.7% | Urban markets, health-conscious demographics nationwide | Medium term (2-4 years) |

| Govt. Millet Mission accelerating millet cereals | +0.6% | National, with focus on tribal and rural nutrition programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health-conscious consumer base

India's health-conscious demographic is driving significant changes in breakfast consumption patterns, reflecting a shift beyond basic nutritional awareness. With increasing incomes, consumers are focusing more on health and wellness, allocating higher spending toward nutritious foods, gym memberships, preventive healthcare, and wellness products. According to the Department of Economic Affairs, India's per capita national income reached INR 184.21 thousand in 2024[1]Source: Department of Economic Affairs (India), "Economic survey FY 2025 statistical appendix", www.indiabudget.gov.in. Government programs like the Anemia Mukt Bharat initiative, which provided Iron-Folic Acid supplements to 15.4 crore children and adolescents in Q2 FY 2024-25[2]Source: Ministry of Health and Family Welfare, "India’s Fight Against Anemia", www.pib.gov.in, highlight the role of breakfast cereals in addressing micronutrient deficiencies, as reported by the Ministry of Health and Family Welfare. Additionally, the Economic Survey 2025's call for stricter regulations on ultra-processed foods, including sweetened breakfast cereals, emphasizes the opportunity for reformulated, health-compliant alternatives. This regulatory focus is expected to drive innovation, encouraging the development of products with reduced sugar, increased protein, and fortified formulations that align with government nutrition goals.

Premiumization via protein-fortified SKUs

India faces a significant protein deficiency due to limited dietary diversity and a predominantly vegetarian population. To combat this issue, the government has implemented a large-scale staple food fortification program, which now distributes fortified rice to 80 crore people. This initiative not only addresses nutritional gaps but also familiarizes consumers with nutrient-enhanced food products. In response to this growing awareness, companies are introducing innovative offerings to meet consumer demand. For instance, in April 2025, PepsiCo launched its "Life" multigrain cereal, specifically designed for health-conscious individuals seeking nutritious options. Similarly, emerging brands like Troo Good have raised USD 9 million in funding to develop protein-rich breakfast solutions, catering to the increasing need for fortified food products. Furthermore, the Production Linked Incentive scheme is playing a pivotal role in supporting this trend. By providing targeted financial assistance to innovative and organic small and medium enterprises (SMEs) under Category II, the scheme facilitates the development of protein-fortified products. This support significantly reduces barriers to market entry, enabling the creation and availability of specialized formulations to address India's protein deficiency effectively.

Rising demand for ready-to-eat cereals

The adoption of Ready-to-Eat (RTE) cereals in Indian households highlights a shift driven by more than just convenience. With rising female workforce participation, dual-income households are growing, facing time limitations that make traditional breakfast preparation less practical. In February 2025, the government, under the PM Kisan Sampada Yojana, approved 1,608 projects, including 41 Mega Food Parks and 394 cold chain projects[3]Source: Ministry of Food Processing Industries, "From Farm to Retail: Make in India’s push for Food Processing Excellence", www.pib.gov.in, according to the Ministry of Food Processing Industries. These initiatives aim to enhance supply chain efficiency, reducing the previously high costs of RTE products. Urban Indians increasingly rely on quick commerce platforms, which are addressing distribution challenges and improving RTE cereal availability in smaller cities. The segment's growth indicates that convenience is becoming a major purchasing factor, particularly for Gen Z consumers. By 2035, this group is expected to account for half of India's spending, driving a shift in breakfast habits from labor-intensive preparations to quick, grab-and-go options.

Increasing dual-income households

The rise of dual-income households is driving a demand shift that goes beyond simple time-saving preferences, leading to a fundamental reorganization of lifestyles. Female workforce participation continues to grow significantly each year. According to the World Bank, India's female labor force participation rate increased from 31.24% in 2023 to 32.8% in 2024[4]Source: World Bank, "Labor force participation rate, female", www.worldbank.com. This growth is reshaping households by increasing disposable incomes while reducing the time available for meal preparation. These households are changing their consumption patterns by prioritizing branded, convenient products and showing a willingness to pay premiums for time-saving solutions. This shift reflects an increase in working-age individuals per household, boosting both earning potential and the demand for breakfast convenience. These demographic changes are creating distinct consumer segments with specific needs, emphasizing the importance of targeted product positioning over mass-market strategies. The sustainability of this trend is supported by structural economic changes: nuclear family trends are driving household formation at a faster rate than population growth, resulting in more individual household units with dual-income potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity | -0.9% | National, particularly acute in rural and Tier-3+ cities | Short term (≤ 2 years) |

| Cultural preference for hot savoury breakfasts | -0.7% | National, strongest in North and East India traditional regions | Long term (≥ 4 years) |

| Volatile specialty-grain input costs | -0.5% | National, supply chain dependent regions | Medium term (2-4 years) |

| Challenges in product reformulation | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High price sensitivity

Inflationary pressures are driving consumers toward value-seeking behaviors, creating challenges for premium breakfast cereal brands. FMCG companies raised prices by 3-5% in 2024 due to rising commodity costs. To maintain price points, many adopted "shrinkflation" strategies. However, elevated food inflation has reduced discretionary spending, particularly among the lower-middle and middle classes. This price sensitivity is especially evident in rural markets, where 92% of retail trade occurs through kirana stores, which have limited shelf space for premium products. Price-sensitive consumers often switch brands based on discounts, promotions, or cheaper alternatives, leading to reduced brand loyalty and tighter margins for manufacturers. The competition is further heightened as breakfast cereals face subsidized alternatives. Government programs, such as Bharat Atta and Bharat Rice, provide heavily subsidized staples, establishing price benchmarks that challenge commercial breakfast options.

Cultural preference for hot savoury breakfasts

Breakfast choices in India go beyond mere taste preferences, reflecting cultural identity and regional pride. Although the Green Revolution led to a decline in traditional grains and created nutritional gaps, many Indians continue to favor hot, freshly prepared breakfast staples such as parathas, idlis, dosas, and poha. Through initiatives like Poshan Pakhwada 2025, the Indian government is actively promoting these traditional foods. Supported by the Ministry of Women and Child Development, this program encourages community-level preparation of these dishes at Anganwadi centers, reinforcing their cultural importance. However, regional differences add complexity: North and East Indian states exhibit a stronger preference for hot, savory breakfasts, while South Indian markets show a slightly higher adoption of ready-to-eat options. Even health-conscious consumers, who often perceive cold cereals as less nutritious, remain attached to traditional breakfast choices. Nonetheless, the government's Millet Mission and the promotion of 'Shree Anna' offer a promising opportunity. Millet-based hot cereals could address both cultural preferences and the growing need for convenience, potentially leading to innovative product categories that balance tradition with modernity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready-to-Cook Gains Despite RTE Dominance

Ready-to-Eat cereals hold a dominant 73.82% market share in 2025, despite Ready-to-Cook cereals growing rapidly, with a projected CAGR of 6.62% through 2031. This growth highlights a balance between traditional Indian breakfast preferences for hot, freshly prepared meals and the increasing demand for convenience. Government initiatives promoting traditional grains have significantly contributed to this expansion. For instance, the coarse grain procurement program reached a 10-year high of 1.255 million metric tons in 2023-24, as per the Ministry of Consumer Affairs. This milestone ensures a steady supply and stable pricing for essential RTC ingredients like oats and millet.

In the Ready-to-Eat segment, flakes continue to dominate due to strong consumer trust. However, granola and clusters are gaining popularity, particularly among health-conscious urban consumers willing to pay a premium for added nutritional benefits. Puffed cereals maintain consistent demand, driven by their affordability and appeal to children. The segment's growth is further shaped by the FSSAI's updated standards, which now include categories such as vegan and organic products. These regulations encourage product innovation while maintaining safety standards. To adapt to evolving consumer preferences, companies are introducing hybrid products that bridge the gap between RTE and RTC. For example, instant hot cereals combine the convenience of modern products with the traditional flavors consumers value, addressing both cultural preferences and modern lifestyle needs.

By Ingredient Source: Oat Innovation Challenges Corn Supremacy

Corn maintains the largest market share at 40.75% in 2025. Corn-based cereals, such as corn flakes, are highly favored by Indian consumers for their taste and versatility. These cereals are typically consumed at breakfast, often accompanied by milk, fruits, or sweeteners. Meanwhile, oat-based cereals are experiencing the fastest growth, with a strong CAGR of 6.93% projected through 2031. This growth highlights a significant shift toward healthier grain alternatives. The increasing demand for oats is driven by their beta-glucan content and cholesterol-lowering benefits, which are widely promoted through health campaigns and medical endorsements. Supporting this trend, the government has significantly increased its procurement of coarse grains, particularly oats and millet. This initiative ensures supply stability and enables manufacturers to expand their oat-based product lines without concerns about input cost fluctuations.

Wheat-based cereals continue to see steady demand due to their cultural familiarity and affordability. Rice-based cereals address specific dietary needs and regional preferences. Barley remains a niche segment but maintains stability in health-focused formulations. The "Others" category, which includes millets and ancient grains, is benefiting from the government's Millet Mission and the 'Shree Anna' promotion. The Production Linked Incentive scheme specifically targets millet-based Ready-to-Cook (RTC) and Ready-to-Eat (RTE) products. In 2023, the FSSAI introduced millet standards, which were later shared with Codex Alimentarius, providing manufacturers with a clearer regulatory framework. This clarity reduces formulation risks, particularly for those exploring ancient grain applications. Combined with government procurement preferences for millet-based products, this regulatory support gives companies investing in traditional grain innovations, such as millets, a competitive edge over those focusing on conventional corn and wheat formulations.

By Product Nature: Organic Acceleration Amid Conventional Stability

Conventional cereals held 76.15% of the Indian breakfast cereal market size in 2025, driven by their affordability, widespread availability, and strong consumer trust. However, organic SKUs are growing at a notable 7.35% CAGR. This trend highlights a divided market: price-conscious consumers continue to prefer conventional cereals, while affluent households increasingly opt for organic alternatives. The growth of the organic segment is supported by the FSSAI's introduction of clear standards for organic products, reducing compliance risks for manufacturers.

Urban families, particularly those with young children, are more inclined to pay a premium for organic products due to rising health awareness and concerns about pesticide residues. On the other hand, the conventional segment remains resilient because of its cost advantages and extensive distribution network, especially through traditional kirana stores. Nonetheless, the Economic Survey 2025's proposal for health taxes on ultra-processed foods could create regulatory incentives favoring organic and minimally processed options. Additionally, the government's Production Linked Incentive scheme, specifically Category II, supports innovative and organic SMEs by providing financial incentives that facilitate organic product development and scaling. With FSSAI's enhanced organic standards and expanded testing infrastructure, the organic segment is well-positioned for growth. Meanwhile, conventional products face increasing regulatory scrutiny regarding health claims and processing methods.

By Packaging Type: Convenience Formats Disrupt Traditional Boxes

Boxes retained a 64.55% revenue share in 2025. These boxes, often featuring inner linings or pouches, provide superior protection against moisture, pests, and contamination, ensuring cereals remain fresh for extended periods. Their large printable surfaces enable brands to effectively highlight product features, nutritional details, and visually appealing designs, increasing visibility on supermarket shelves and enhancing consumer engagement. Meanwhile, cups and bowls are experiencing steady growth, with a 7.16% CAGR projected through 2031. These single-serve formats cater to a mobile workforce that frequently consumes breakfast in cars, trains, or offices. Furthermore, quick-commerce algorithms favor smaller, high-velocity SKUs, improving their ranking in in-app search results and boosting their visibility.

Stand-up pouches offer dual benefits: they appeal to cost-conscious first-time buyers and provide resealability for families with diverse breakfast routines. However, proposed uniform labeling regulations by Legal Metrology could increase compliance costs per SKU, potentially driving pack-size rationalization in India's breakfast cereal market. Simultaneously, sustainability goals are steering research and development efforts toward recyclable PET cups and bio-based liners, all while maintaining microwave safety—a critical innovation frontier that could serve as a key market differentiator in the future.

By Distribution Channel: E-Commerce Surge Reshapes Market Access

Supermarkets and hypermarkets maintain a 60.98% share in 2025, concentrated in major urban centers. These organized retailers cater to the highest breakfast cereal consumption. Their vast networks ensure easy access for a broad consumer base. Online retail stores, expanding at a robust 7.78% CAGR through 2031, lead all distribution channels. This shift is especially evident in quick commerce, where platforms offer 10-30 minute delivery windows, turning breakfast cereal purchases into impulse buys rather than planned events.

While convenience and specialist stores hold steady, catering to specific geographic and demographic niches, traditional kirana stores still reign supreme in rural and semi-urban markets, even if not distinctly recognized in formal distribution metrics. In 2024, FSSAI's reactivation of draft e-commerce regulations clarifies compliance for online food sales, alleviating the regulatory uncertainties that once hampered digital growth. This evolving distribution landscape mandates manufacturers to adapt: brands must now navigate an omnichannel presence, balancing traditional retail, modern trade, e-commerce marketplaces, and direct-to-consumer platforms, each demanding unique product positioning, pricing, and promotional tactics.

Geography Analysis

India's breakfast cereal market showcases distinct regional variations, shaped by the subcontinent's economic development, cultural nuances, and infrastructure accessibility. Urban markets, accounting for about 60% of consumer spending, are at the forefront of adopting breakfast cereals. This trend is fueled by higher disposable incomes, evolving lifestyles, and a growing exposure to global food trends. Major cities like Mumbai, Delhi, Bangalore, and Chennai lead in per-capita consumption, a result of their dual-income households, international exposure, and a lifestyle that prioritizes convenience. Thanks to government initiatives like Mega Food Parks and cold chain projects, product availability is on the rise in Tier-2 and Tier-3 cities. While these areas have seen limited organized retail penetration, it's expanding swiftly. Regional breakfast traditions play a pivotal role in shaping these adoption patterns: South Indian markets are leaning towards ready-to-eat options, whereas North Indian consumers still favor traditional hot dishes like parathas and dal-chawal.

Rural markets, witnessing a faster growth in FMCG consumption than their urban counterparts, present a mixed bag of opportunities and challenges for breakfast cereal brands. While there's a keen interest, adoption is hindered by price sensitivity and a cultural inclination towards traditional meals. However, the government's fortified rice program, primarily targeting rural populations, is introducing them to processed, nutrient-enhanced foods, potentially paving the way for greater acceptance of breakfast cereals. Furthermore, initiatives like the PM Formalisation of Micro Food Processing Enterprises are bolstering local processing capabilities. This could lead to the development of region-specific products that cater to local tastes while retaining modern convenience.

Digital penetration is reshaping geographic distribution strategies, allowing brands to directly reach consumers in previously hard-to-access markets. The expansion of quick commerce beyond metropolitan areas is opening up fresh distribution avenues. Additionally, the government's route optimization efforts, which have slashed transport costs by Rs 250 crore annually, are enhancing product availability and pricing in remote regions, as highlighted by the Ministry of Consumer Affairs. State-level nutrition programs, like Haryana's fortified atta initiative that benefitted 3.3 million individuals, underscore the impact of localized policy implementations in driving demand for fortified breakfast items. Given this geographic intricacy, manufacturers face the challenge of maintaining brand consistency on a national scale while also customizing offerings regionally. This is especially crucial in areas like flavor profiles, packaging sizes, and distribution methods, ensuring they resonate with local tastes while aligning with contemporary convenience trends.

Competitive Landscape

The Indian breakfast cereal market is fragmented, with intense competition among multinational corporations, established Indian FMCG companies, and emerging health-focused startups. Global players like Kellanova, Nestlé, and PepsiCo utilize substantial advertising budgets and nationwide distribution networks to maintain their leadership in core flakes. On the other hand, domestic brands such as Marico and Patanjali aggressively focus on ayurvedic positioning and millet-based products, appealing to tradition-oriented consumers.

Direct-to-consumer brands like YogaBar, True Elements, and Troo Good leverage social media micro-influencers to effectively target niche segments, including keto, vegan, and high-protein diets. Major players in the Indian breakfast cereals market include Kellanova, Nestle SA, PepsiCo Inc, Bagrry's India Ltd, and Marico Ltd. These companies prioritize strategies such as new product launches, market expansions, partnerships, and acquisitions. Additionally, they are heavily investing in research and development to introduce innovative variants that address the growing demand for healthy and clean-label food products.

Global conglomerates are increasingly pursuing mergers and acquisitions to strengthen their presence in organic and millet sub-segments. Regulatory advancements are driving innovation, with FSSAI's expanded 286-member scientific panels now issuing grain-specific norms within six months, significantly reducing product-launch timelines. However, heightened competition has triggered price wars in supermarkets; during the summer of 2025, promotional discounts averaged 23% off the listed price, compressing gross margins despite revenue growth in the Indian breakfast cereal market.

India Breakfast Cereals Industry Leaders

-

Bagrry's India Ltd

-

PepsiCo Inc

-

Kellanova

-

Nestle SA

-

Marico Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: PepsiCo's Life unveiled a multigrain cereal, focusing on family wellness. This healthier introduction, aimed at bolstering immunity and promoting healthy bones, arrives amidst declining sales in the category.

- February 2025: Nestlé India has unveiled Munch Choco Fills, adding a new dimension to its breakfast cereal lineup. With a crunchy exterior and a rich chocolate filling, this cereal promises to elevate breakfast moments

- July 2024: Kellanova India has relaunched its flagship breakfast cereal, Kellogg’s Chocos, under the new name Multigrain Chocos. This aligns with the packaged food major’s strategy to expand household penetration of its breakfast cereals portfolio in the country.

- June 2023: Nestlé has bolstered its breakfast cereals lineup in India, unveiled two new offerings: KOKO KRUNCH Millet-Jowar and MUNCH Breakfast Cereals. These additions aim to diversify the breakfast choices for Indian consumers.

India Breakfast Cereals Market Report Scope

Breakfast cereal is made from processed grains or multiple grains, such as corn, oats, wheat, and others, that are considered the day's first meal. India's breakfast cereals market is segmented by type and distribution channel. Based on type, it is segmented as ready-to-eat and ready-to-cook. By distribution channel, the market is segmented into supermarkets/hypermarkets, independent retailers, online retail stores, specialty stores, convenience stores, and other distribution channels. For each segment, the market sizing and forecasts have been done based on the value in USD million.

Product Type

| Ready-to-Eat Cereals | Flakes |

| Puffed Cereals | |

| Granola and Clusters | |

| Others (Coated/Sugar-Frosted Cereals, Shredded and Threaded) | |

| Ready-to-Cook Cereals | Hot Oatmeal |

| Muesli and Porridge Mixes | |

| Other Ready-to-Cook Cereals |

Ingredient Source

| Wheat |

| Corn |

| Oats |

| Rice |

| Barley |

| Others |

Product Nature

| Conventional |

| Organic |

Packaging Type

| Boxes |

| Stand-up Pouches |

| Cups and Bowls |

| Others |

Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Specialist Stores |

| Online Retail Stores |

| Other Distribution Channels |

| Product Type | Ready-to-Eat Cereals | Flakes |

| Puffed Cereals | ||

| Granola and Clusters | ||

| Others (Coated/Sugar-Frosted Cereals, Shredded and Threaded) | ||

| Ready-to-Cook Cereals | Hot Oatmeal | |

| Muesli and Porridge Mixes | ||

| Other Ready-to-Cook Cereals | ||

| Ingredient Source | Wheat | |

| Corn | ||

| Oats | ||

| Rice | ||

| Barley | ||

| Others | ||

| Product Nature | Conventional | |

| Organic | ||

| Packaging Type | Boxes | |

| Stand-up Pouches | ||

| Cups and Bowls | ||

| Others | ||

| Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Specialist Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

How large is the India breakfast cereal market in 2026?

The category is valued at USD 5.45 billion in 2026 and is projected to reach USD 7.32 billion by 2031.

Which segment is growing fastest within breakfast cereals?

Ready-to-Cook cereals are expanding at a 6.62% CAGR, outpacing other product types.

Why are oats gaining popularity over corn?

Medical endorsements for beta-glucan heart benefits and stronger government support for coarse grains are boosting oat-based launches.

What role does e-commerce play in cereal sales?

Online retail is the fastest-growing channel, projected at an 7.78% CAGR as quick-commerce boosts impulse purchases.

Page last updated on: