Fortified Breakfast Cereals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

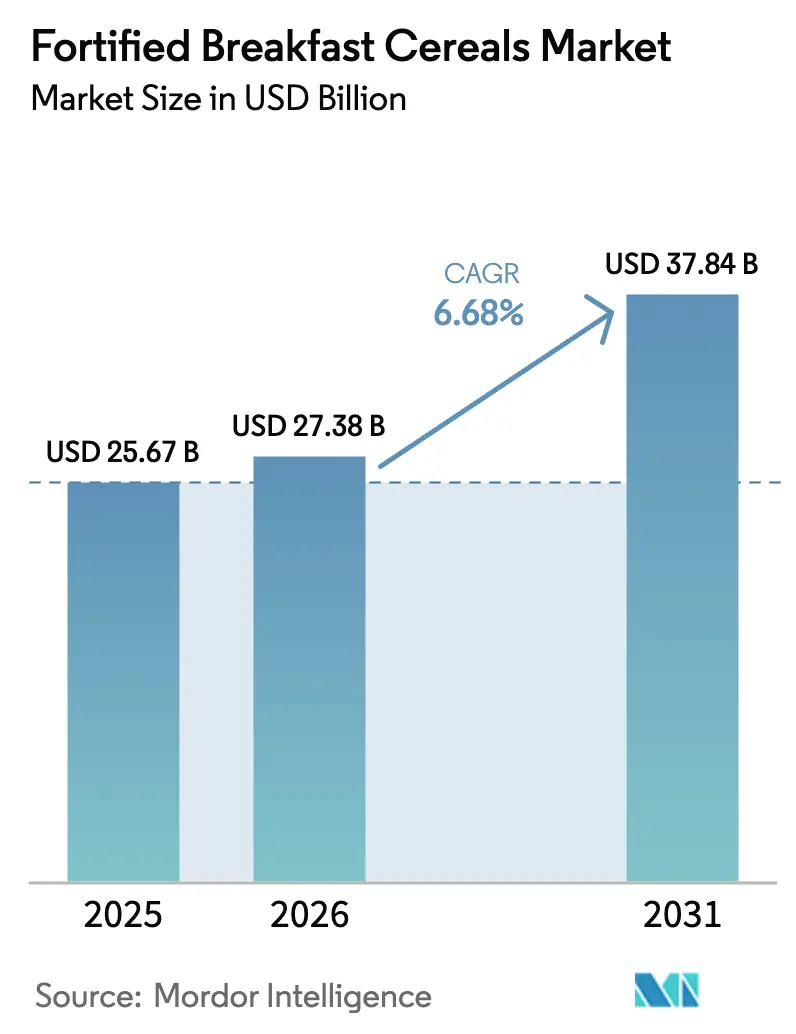

| Market Size (2026) | USD 27.38 Billion |

| Market Size (2031) | USD 37.84 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fortified Breakfast Cereals Market Analysis by Mordor Intelligence

In 2025, the fortified breakfast cereals market size was valued at USD 25.67 billion. Fortified breakfast cereals market size in 2026 is estimated at USD 27.38 billion, growing from 2025 value of USD 25.67 billion with 2031 projections showing USD 37.84 billion, growing at 6.68% CAGR over 2026-2031. This growth is primarily attributed to increasing consumer interest in preventive health measures, regulatory updates that allow broader fortification practices, and advancements in nutrient delivery technologies. Manufacturers are responding to evolving consumer preferences by reformulating products to comply with lower sugar mandates while ensuring taste appeal, particularly in children's product lines. On the supply side, challenges such as fluctuations in commodity prices and rising packaging costs have been effectively countered through premium pricing strategies, brand consolidation, and the growing popularity of fiber-rich oat-based options. These factors have enabled the market to maintain resilience and drive innovation. As a result, the fortified breakfast cereals market continues to evolve at the intersection of nutritional science and shifting consumer lifestyles, positioning itself as a key player in the broader health and wellness industry.

Key Report Takeaways

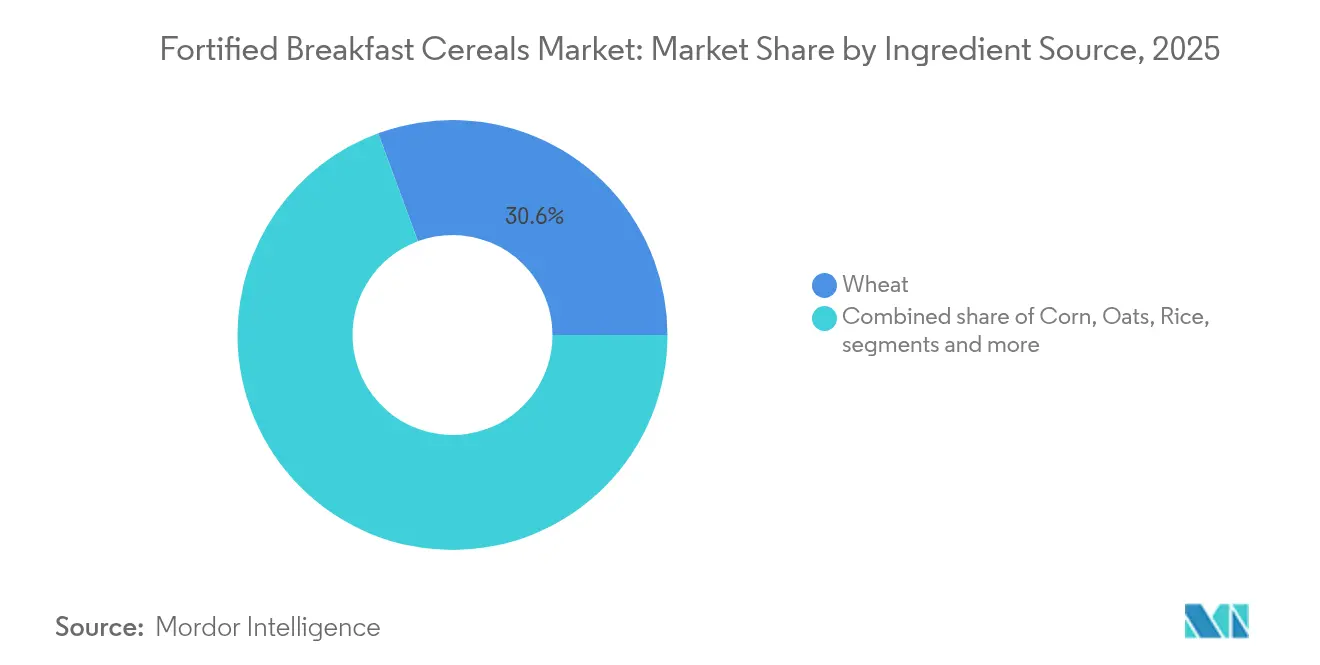

- By ingredient source, wheat-based cereals led with 30.62% of fortified breakfast cereals market share in 2025, while oat-based products are projected to post the fastest 6.86% CAGR through 2031.

- By age group, adults accounted for 47.71% of the fortified breakfast cereals market size in 2025, and children’s cereals are expected to grow at a 6.84% CAGR through 2031.

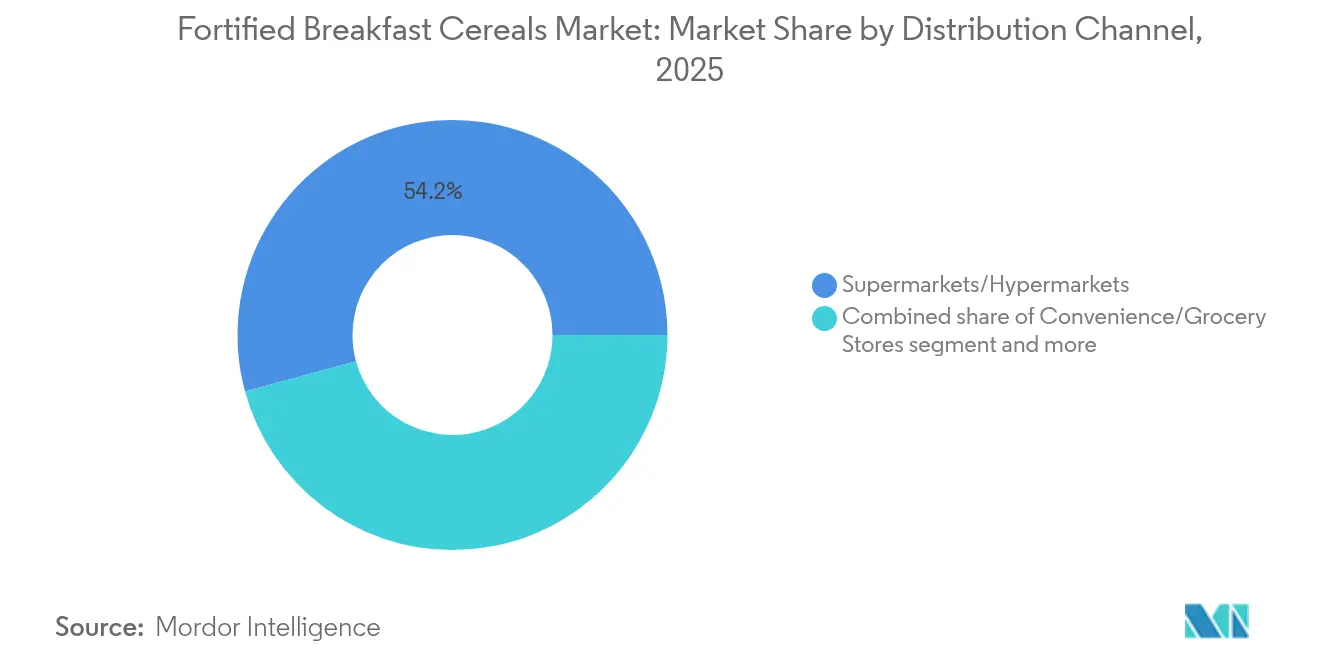

- By distribution channel, supermarkets/hypermarkets retained 54.23% revenue share in 2025, whereas online retailers are forecast to expand at 10.21% CAGR to 2031.

- By packaging type, boxed formats captured 60.55% share of the fortified breakfast cereals market in 2025, while stand-up pouches are set to register a 7.55% CAGR through 2031.

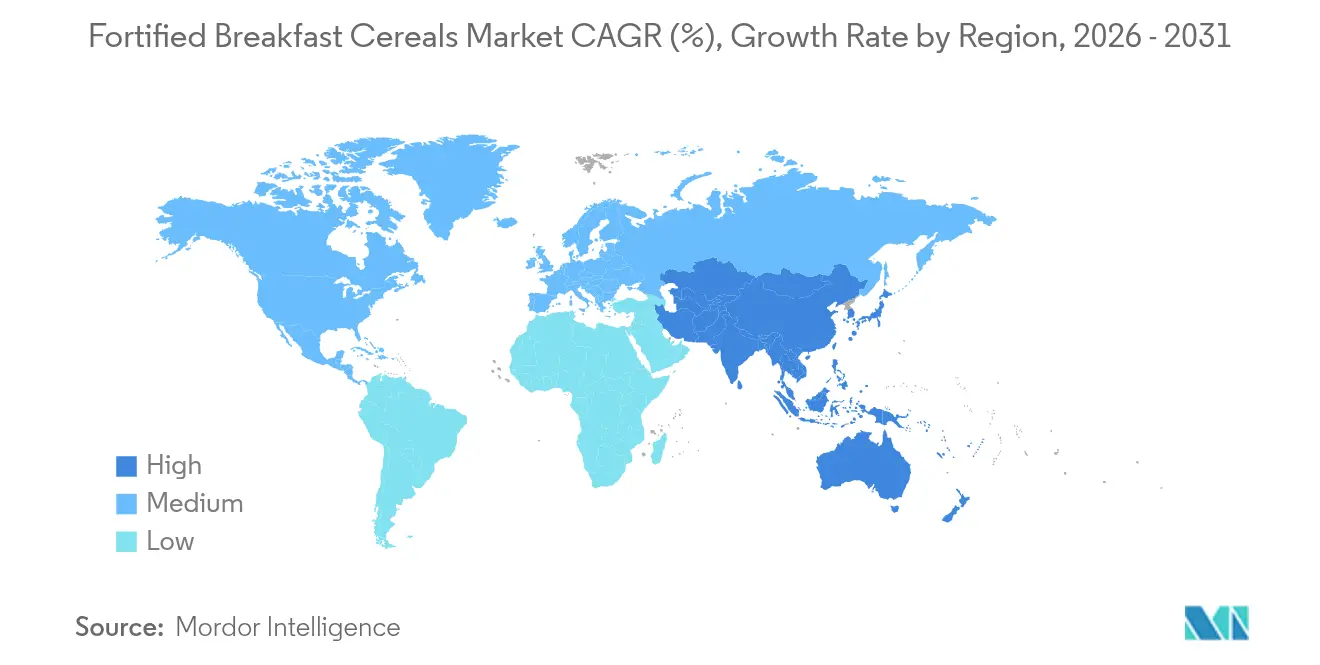

- By geography, North America commanded a 39.58% share in 2025, but Asia-Pacific is on track for the highest 6.92% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fortified Breakfast Cereals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health awareness drives demand for fortified breakfast cereals | +1.1% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Premiumization driving value growth | +0.9% | North America, Europe, Urban Asia-Pacific | Long term (≥ 4 years) |

| Strategic investments by market players | +0.7% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Urbanization of megacities boosting convenience-oriented fortified breakfast choices | +0.6% | Asia-Pacific, Latin America, Middle East | Long term (≥ 4 years) |

| Weight-management focus among aging consumers fueling high-fiber, fortified oat cereals | +0.5% | North America, Europe, Japan | Medium term (2-4 years) |

| E-commerce growth is making fortified cereals more accessible | +0.4% | Global, accelerated in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising health awareness drives demand for fortified breakfast cereals

Research highlights a growing consumer focus on preventive nutrition, significantly influencing cereal purchasing decisions. Consumers now seek products enriched not only with traditional vitamins and omega-3 fatty acids but also with functional ingredients like probiotics and prebiotics, driven by increased awareness of gut health, especially post-pandemic. Reflecting this trend, the FDA has approved the fortification of breakfast cereals with up to 560 IU of vitamin D3 per 100 grams, aligning regulatory measures with evolving health priorities and enabling manufacturers to make impactful nutritional claims [1]U.S. Food and Drug Administration, "FDA ups vitamin D fortification in cereals and grain-based bars", www.fda.gov. Fortified ready-to-eat cereals have become a key source of daily micronutrient intake, particularly for children and adolescents, often delivering at least 15% of the recommended daily values for essential nutrients such as iron, calcium, and B vitamins. This shift underscores the growing role of cereals in addressing nutritional gaps and supporting overall health.

Premiumization driving value growth

Manufacturers are increasingly adopting premium positioning strategies to cater to sophisticated consumer demands for clean-label ingredients and specialized nutritional profiles while achieving higher profit margins. For instance, in 2024, General Mills launched Wheaties Protein at USD 8.99 per box, offering over 20 grams of protein per serving. This product targets health-conscious consumers who are willing to pay a premium for functional benefits. The protein cereal segment, in particular, exhibits significant potential for premiumization. Brands like Magic Spoon capitalize on this trend by leveraging direct-to-consumer channels and forming partnerships with specialized retailers to justify premium pricing. In Europe, consumer preferences are evolving, with a growing emphasis on taste alongside health benefits. This shift creates opportunities for premium formulations that combine indulgence with nutrition. The success of artisanal granola brands and organic cereal variants highlights this trend. Additionally, premiumization extends beyond product formulations to packaging innovations. The use of sustainable materials and convenient formats, such as stand-up pouches, not only supports higher price points but also appeals to environmentally conscious consumers, further driving the premiumization trend in the market.

Strategic investments by market players

Manufacturers are accelerating capital deployment across the value chain by modernizing production facilities and expanding capacities to meet the increasing demand for specialized formulations. General Mills, as part of its Accelerate strategy, is advancing regenerative agricultural practices on 1 million acres by 2030 while significantly increasing investments in product innovation, particularly in the cereals segment. Similarly, in 2024, Post Holdings reported a USD 436.4 million contribution to net sales in Q3 2024 through strategic acquisitions. The Weetabix segment achieved a 35% profit increase, driven partly by the acquisition of Deeside Cereals, highlighting how targeted investments can effectively enhance market share. Besides, investments in manufacturing infrastructure prioritize fortification capabilities and flexible production lines designed to meet diverse nutritional needs and accommodate various packaging formats. Kellanova, through its Better Days Promise, is committed to responsibly sourcing 12 priority ingredients, including corn, wheat, and sugar cane, by 2030. Manufacturers are also leveraging advancements in encapsulation techniques and nutrient stability systems to address technical challenges. These technologies enable the delivery of consistent nutritional profiles, maintain product quality, and extend shelf life, thereby overcoming previous limitations in fortification options.

Urbanization of megacities boosting convenience-oriented fortified breakfast choices

Rapid urbanization in developing markets is driving the emergence of concentrated consumer bases that demand convenient and nutritious breakfast solutions tailored to their fast-paced lifestyles. Megacities, characterized by dense populations and busy schedules, are fostering demand for products that combine portability, nutritional value, and extended shelf life. This transition creates significant opportunities for international brands to penetrate these markets by offering localized formulations that cater to regional tastes and preferences. Additionally, ready-to-eat cereals are increasingly positioned as versatile snack options, expanding their consumption beyond the traditional breakfast setting. This trend is particularly evident in urban environments, where consumers prioritize flexibility in meal timing. Urban consumers' growing exposure to diverse food cultures, facilitated by digital platforms and the presence of international retail outlets, has further enhanced the acceptance of fortified cereals. These products are increasingly perceived as legitimate nutritional solutions, especially when marketed as premium health offerings rather than processed convenience foods. This strategic positioning not only addresses the nutritional needs of urban populations but also aligns with their evolving preferences for high-quality, health-focused products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent sugar-reduction regulations limiting formulation flexibility | -0.4% | Global, strictest in North America and Europe | Short term (≤ 2 years) |

| Volatile oat and corn commodity prices compressing margins | -0.3% | Global, acute in grain-dependent regions | Medium term (2-4 years) |

| Competition from traditional breakfast staples | -0.3% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Supply chain disruptions affecting availability | -0.2% | Global, concentrated in import-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent sugar-reduction regulations limiting formulation flexibility

Manufacturers are increasingly constrained by regulatory requirements that complicate the balance between taste and nutrition, particularly in children's cereals, where flavor significantly influences consumption patterns. The Child and Adult Care Food Program's upcoming regulation, effective October 2025, limits added sugars to a maximum of 6 grams per dry ounce [2]USDA Food and Nutrition Service, "Calculating the Added Sugars Limit for Breakfast Cereals in the Child and Adult Care Food Program", www.fns.usda.gov. This policy necessitates the reformulation of many popular cereal brands that currently exceed these limits. Additionally, the FDA's updated "healthy" labeling criteria exclude highly sweetened cereals, potentially altering market positioning and consumer perceptions of traditional products. To address these challenges, manufacturers are exploring alternative sweetening methods using natural ingredients such as honey, maple syrup, and fruit concentrates. However, these solutions introduce higher costs and supply chain complexities, further compressing profit margins. As regulatory landscapes grow more complex and vary across jurisdictions, manufacturers must allocate significant resources to research and development for developing flavor enhancement technologies and conducting consumer acceptance testing. These efforts are critical to maintaining sensory appeal while adhering to evolving nutritional mandates.

Volatile oat and corn commodity prices compressing margins

Manufacturers face mounting margin pressures as raw material cost fluctuations challenge their ability to implement price increases without risking market share in price-sensitive segments. In 2024, oat prices reached a five-month high, significantly impacting the fastest-growing ingredient segment, where premium positioning relies heavily on stable cost structures. The Producer Price Index by Commodity data released by the Federal Reserve Economic Data (FRED) showed oats trading at USD 277.48 in May 2024 [3]Source: Federal Reserve Economic Data (FRED), “Producer Price Index by Commodity: Farm Products: Oats”, fred.stlouisfed.org. However, price volatility persists as demand growth continues to outstrip supply expansion in key markets, exacerbating cost pressures. Meanwhile, corn futures for 2025 crops are trading at discounts, providing some relief for corn-based formulations. Despite this, manufacturers struggle to develop effective hedging strategies that balance cost stability with inventory management needs. The heightened sensitivity to commodity price fluctuations is particularly pronounced in private label and value-tier products, where limited margin flexibility forces manufacturers to optimize formulations and explore alternative ingredient sources. These measures are critical to maintaining profitability in an increasingly volatile market environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Source: Wheat Dominance Meets Oat Innovation

In 2025, wheat secures its position as the leading ingredient source, commanding a 30.62% market share. This dominance is bolstered by established supply chains, cost efficiencies, and the ingredient's adaptability in processing, catering to varied fortification needs. Wheat's gluten content not only lends structural integrity to cereals but also boasts a neutral flavor, seamlessly integrating diverse fortification additives without altering taste. According to USDA data, US winter wheat production in 2024 reached 1.35 billion bushels, marking a 9% increase from 2023, with yields standing at 51.7 bushels per acre. This ensures a steady supply for cereal producers. Familiarity with wheat-based cereals and established fortification methods guarantees consistent nutrient delivery. Furthermore, wheat's processing versatility enables manufacturers to craft varied textures and formats, all while remaining competitively priced in value-tier segments.

Oat-based cereals are on the rise, projected to grow at a 6.86% CAGR through 2031. This surge is attributed to their superior nutritional benefits and a heart-health focus, appealing to health-conscious consumers. USDA data highlights a 23% jump in oat production in 2024, reaching 67.8 million bushels, with record yields of 76.5 bushels per acre, paving the way for broader cereal applications. General Mills' Cheerios stands as a testament to oats' market promise, spotlighting whole grain oats as the main ingredient, all while proudly holding a gluten-free certification and promoting a heart-healthy image. Bob's Red Mill has introduced innovative high-protein oats, tackling the traditional protein shortfall in oat-based products, which could spur wider acceptance across various cereal segments. Additionally, the beta-glucan fiber in oats not only offers scientifically backed health advantages but also bolsters premium market positioning and supports regulatory health claims.

By Packaging Type: Traditional Boxes Versus Sustainable Pouches

In 2025, box packaging commands a dominant 60.55% market share, leveraging established consumer shopping habits, optimal retail display characteristics, and brand recognition to bolster premium positioning strategies. Traditional cardboard boxes not only shield products during transport and storage but also provide ample space for nutritional information, marketing messages, and brand imagery, all of which sway purchase decisions. For instance, Kellogg's shift to 97% timber-based packaging, sourced from recycled or certified-sustainable content, underscores the adaptability of traditional formats to sustainability mandates without compromising their functional benefits. Box packaging not only offers visibility for portion control but also safeguards cereal texture and nutritional integrity throughout distribution. Its standardized dimensions maximize retail shelf space and streamline inventory management across various retail channels.

Stand-up pouches emerge as the fastest-growing packaging format, boasting a 7.55% CAGR through 2031. Their rise is fueled by sustainability benefits, cost savings, and a knack for keeping products fresh, all of which resonate with eco-conscious consumers. Post Consumer Brands' foray into bagged Malt-O-Meal cereals underscores this trend, reaping a 29% surge in operating profits and a 4.2% uptick in consumption, even as traditional boxed cereals wane. Flexible packaging trumps rigid containers by slashing material use by up to 75%, all while boasting superior barrier properties that prolong shelf life and safeguard nutritional content. Coveris steps into the spotlight with its launch of recyclable 100% polyethylene cereal liners, presenting a mono-material solution that not only protects products but also champions the circular economy. Plus, the resealable nature of this format caters to consumer convenience and curbs food waste by enhancing product preservation.

By Distribution Channel: Supermarket Stability Versus E-commerce Acceleration

In 2025, supermarkets/hypermarkets hold a commanding 54.23% market share, driven by their ability to offer extensive product assortments, competitive pricing, and a shopping experience tailored to consumer preferences for in-person cereal selection. These large-format retailers maximize product visibility through dedicated cereal aisles and strategically placed promotional end-cap displays, which encourage impulse purchases and foster brand discovery. Their dominance highlights the importance of tactile product evaluation, immediate product availability, and the convenience of combining cereal purchases with other grocery needs. Additionally, traditional retail formats benefit from well-established partnerships with major manufacturers, ensuring consistent product availability and robust promotional support. The scale of these retailers enables them to implement competitive pricing strategies that attract price-sensitive consumers while maintaining profitability for both retailers and manufacturers.

Online retailers are emerging as the fastest-growing distribution channel, with a projected CAGR of 10.21% through 2031. This growth is propelled by increasing consumer demand for convenience, the popularity of subscription models, and enhanced product discovery capabilities that particularly benefit specialty and premium cereal brands. E-commerce platforms offer subscription services that guarantee consistent product availability while leveraging customer data to enable personalized marketing and product innovation. These digital channels excel in facilitating the discovery of niche products and providing consumer education, areas where traditional retail formats often fall short. The rapid growth of online retail reflects broader trends in grocery digitization, which have been accelerated by pandemic-driven behavioral shifts and advancements in last-mile delivery infrastructure, making online cereal shopping more practical, efficient, and cost-effective.

By Age Group: Adult Market Leadership Versus Children's Innovation

In 2025, adults account for the largest demographic segment, holding a 47.71% market share. This dominance is driven by a growing preference for health-conscious purchasing decisions, increased adoption of premium products, and a shift in consumption patterns that extend beyond traditional breakfast hours. Adult consumers increasingly seek cereals with functional benefits, such as high protein content, fiber density, and micronutrient fortification, which align with their active lifestyles and focus on preventive health strategies. The segment also benefits from higher disposable income levels, enabling consumers to invest in premium-priced specialized formulations and organic variants. Furthermore, adult cereal consumption is evolving to reflect snacking behaviors, with products designed for multiple consumption occasions throughout the day. Ready-to-eat cereals have become a preferred choice for time-constrained professionals, offering convenient, portable, and shelf-stable nutrition solutions that deliver meaningful health benefits without requiring extensive preparation.

Children's cereals represent the fastest-growing demographic segment, with a projected CAGR of 6.84% through 2031. This growth is fueled by successful reformulation efforts aimed at reducing sugar content while maintaining taste appeal and incorporating functional benefits such as enhanced protein and fiber content. For instance, innovations like Kellogg's High Protein Bites cereal, which contains 21% plant-based protein and high fiber content, exemplify the industry's ability to address parental concerns about nutrition while ensuring the products remain appealing to children. These advancements highlight the segment's focus on balancing health benefits with taste to meet evolving consumer demands.

Geography Analysis

In 2025, North America commands a dominant 39.58% market share, leveraging its sophisticated regulatory frameworks that clarify fortification claims and health positioning strategies. The region's well-established retail infrastructure not only supports premium product launches but also offers a diverse product range, catering to everything from traditional family brands to specialized functional formulations. Recent regulatory shifts, such as the FDA's revised "healthy" claim criteria and the CACFP's sugar reduction mandates, are reshaping product formulations. These changes present competitive advantages for manufacturers adept at navigating compliance. Instead of merely expanding in volume, the region's growth is driven by premiumization trends and the adoption of functional ingredients. Consumers are increasingly willing to pay a premium for cereals that offer significant nutritional benefits. Furthermore, strategic consolidations, like Mars' USD 35.9 billion acquisition of Kellanova in 2024, not only bolster market concentration but also enhance international capabilities, fueling global growth ambitions.

Europe is charting a steady growth path, championing sustainability and harmonizing regulations to bolster cross-border product development and marketing. Regional preferences play a pivotal role in shaping product offerings. For instance, Italy's strong inclination towards supplements and Spain's focus on balancing taste with health present avenues for localized formulations. Cereal Partners Worldwide, a joint venture between Nestlé and General Mills, showcases the scale needed for effective penetration, operating in 130 countries and producing over 100 cereal varieties. Europe's commitment to sustainable packaging and responsible sourcing resonates with the growing environmental consciousness among consumers, offering brands a chance to stand out through genuine sustainability efforts.

Asia-Pacific is on track to be the fastest-growing region, boasting a projected CAGR of 6.92% through 2031. This growth is largely fueled by urbanization, leading to concentrated consumer bases in search of convenient and nutritious breakfast options. A clear illustration of this trend is seen in China, where urban consumers are shifting from traditional breakfast staples to Western-style convenience foods, adapting to their fast-paced lifestyles. The region's varied stages of economic development pave the way for both value-tier and premium strategies. Established markets like Japan and Australia are at the forefront of functional ingredient innovation, while emerging markets are more focused on accessibility and enhancing basic nutrition. The region's growth hinges on adept localization strategies, balancing global nutrition standards with local tastes and cultural dietary habits.

Competitive Landscape

The fortified breakfast cereals market is characterized by moderate consolidation, with a few international and regional players competing for market share by offering a range of products that include added vitamins, minerals, and other nutrients. Major global companies, including Nestle S.A., General Mills Inc., Post Holdings Inc., PepsiCo Inc., and Bob’s Red Mill Natural Foods, command a substantial market share. These key players are not only launching new products with healthier, often organic, ingredients but are also pursuing acquisitions, mergers, partnerships, and expansions as central to their marketing strategy.

Established manufacturers harness their scale advantages and brand equity to solidify their market positions. They're also channeling investments into functional ingredient innovations and premium product positioning. Meanwhile, emerging brands like Magic Spoon, with a focus on protein, and those emphasizing gut health, are applying pressure. They utilize direct-to-consumer channels and a targeted health-centric approach, challenging the traditional marketing methods of their established counterparts.

Strategic trends highlight the integration of functional ingredients, initiatives for sustainable sourcing, and innovative packaging solutions. These innovations not only address environmental concerns but also ensure product quality and longevity. Technological advancements are being harnessed to enhance fortification stability, incorporate alternative proteins, and employ processing methods that safeguard nutritional value while streamlining costs. A testament to the industry's shift, General Mills has pledged to promote regenerative agricultural practices across 1 million acres by 2030, underscoring the competitive edge sustainability offers while bolstering supply chain resilience.

Fortified Breakfast Cereals Industry Leaders

-

Nestle S.A

-

General Mills Inc,

-

Post Holdings Inc

-

Bob’s Red Mill Natural Foods

-

PepsiCo Inc,

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kellogg's introduced Oaties, a high-fiber, oat-based cereal in two variants - Original Crunch and Choco Crunch. The cereal maintained its crispiness in milk and targeted health-conscious consumers. Both variants were non-HFSS products fortified with B vitamins, iron, and vitamin D, featuring a multilayered texture.

- December 2024: General Mills, Inc. expanded its product portfolio through the introduction of Wheaties Protein cereal with Cheerios Protein. The product offered 8 grams of protein per serving and was available in cinnamon and strawberry varieties, featuring a multilayered texture.

- March 2024: The Sidemen entered into a strategic partnership with Mornflake to introduce "Best Cereal" in the UK market. The initial product line comprised two HFSS-compliant varieties: Choco Crunch and Caramel Gold. The cereals, manufactured from wheat and oat puffs, were fortified with vitamins B12, D, and E. The products are launched exclusively through Tesco's retail network, with planned distribution expansion to Morrisons and Iceland.

- January 2024: WK Kellogg Co. developed a new cereal brand, Eat Your Mouth Off, to address the Millennial and Generation Z consumer segments. The product incorporated puff cereal containing 22 grams of protein and zero sugar per serving.

Global Fortified Breakfast Cereals Market Report Scope

Fortified breakfast cereals are products that have been enriched with additional vitamins and minerals that are not naturally present in the grains. Common nutrients added include iron, B vitamins, and vitamin D. Some of the popular breakfast cereals based on type include wheat, corn, oats and others. Fortified breakfast cereals market is segmented by product type, demographic, distribution channel, and geography. Based on product type, the market is segmented into wheat, rice, barley, oat, corn, and other product types. By demographic, the market is segmented into children, adults and seniors. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. The report is also segmented by Geography into North America, Europe, Asia-Pacific, South America, and, Middle East and Africa. The report offers the market size in value terms in USD for all the above-mentioned segments.

| Wheat |

| Corn |

| Oats |

| Rice |

| Barley |

| Others |

| Boxes |

| Stand-Up Pouches |

| Others (Cups, and bags, etc.) |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Specialty Stores |

| Online Retailers |

| Other Distribution Channels |

| Adults |

| Children |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| Sweden | |

| Netherlands | |

| Belgium | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Morocco | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Australia | |

| Rest of Asia-Pacific |

| By Ingredient Source | Wheat | |

| Corn | ||

| Oats | ||

| Rice | ||

| Barley | ||

| Others | ||

| By Packaging Type | Boxes | |

| Stand-Up Pouches | ||

| Others (Cups, and bags, etc.) | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| By Age Group | Adults | |

| Children | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Sweden | ||

| Netherlands | ||

| Belgium | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Morocco | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current size of the fortified breakfast cereals market?

The fortified breakfast cereals market size stood at USD 27.38 billion in 2026 and is projected to reach USD 37.84 billion by 2031.

Which ingredient source is growing the fastest?

Oat-based cereals are forecast to expand at a 6.86% CAGR through 2031, outpacing wheat, corn, and rice varieties.

Why are stand-up pouches gaining popularity?

Pouches reduce material usage, improve resealability, and offer recyclability advantages, driving a 7.55% CAGR for flexible packaging formats.

What regions offer the highest growth potential?

Asia-Pacific, led by China and India, is expected to post a 6.92% CAGR as urbanization and rising incomes boost demand for convenient, nutrient-rich breakfasts.

Page last updated on: