Insider Threat Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.03 Billion |

| Market Size (2030) | USD 6.32 Billion |

| Growth Rate (2025 - 2030) | 15.80% CAGR |

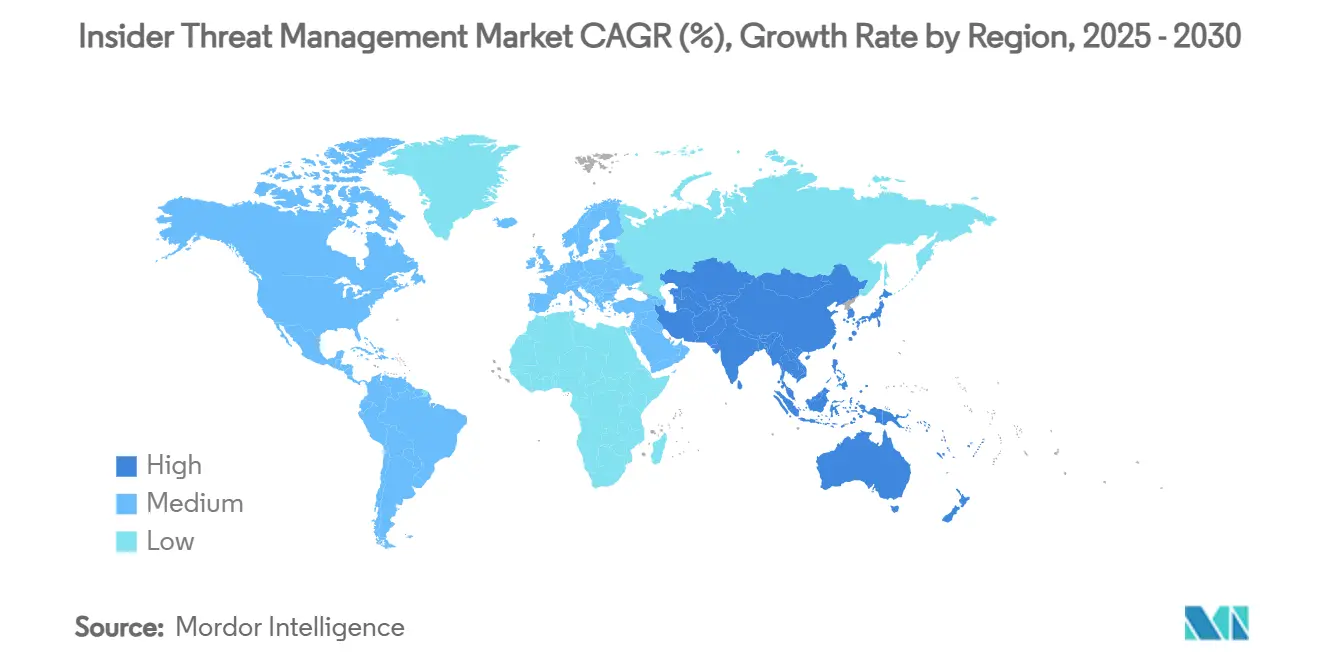

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

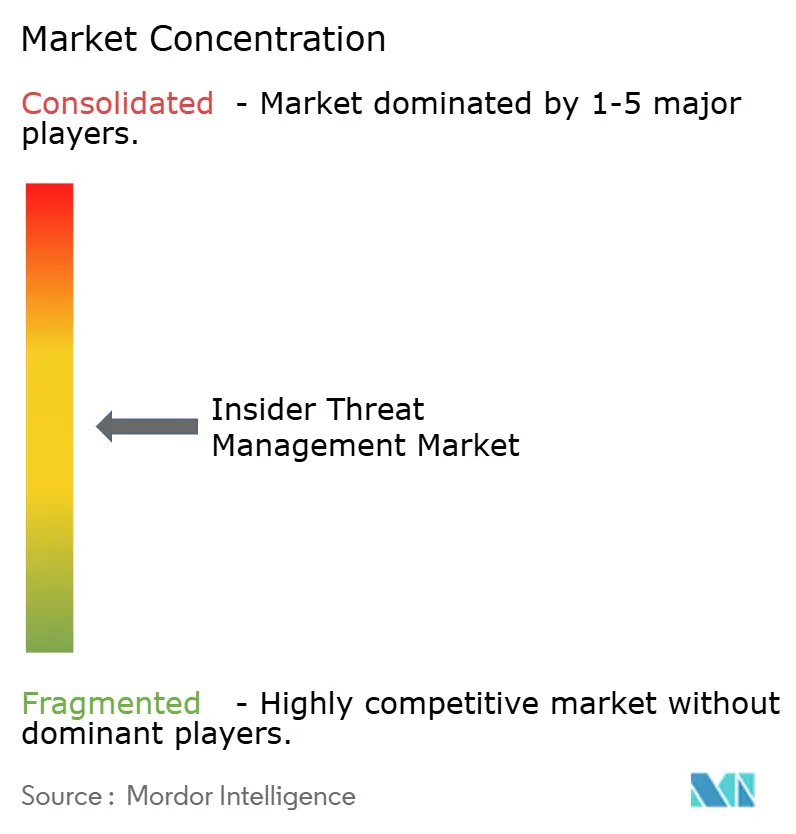

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insider Threat Management Market Analysis by Mordor Intelligence

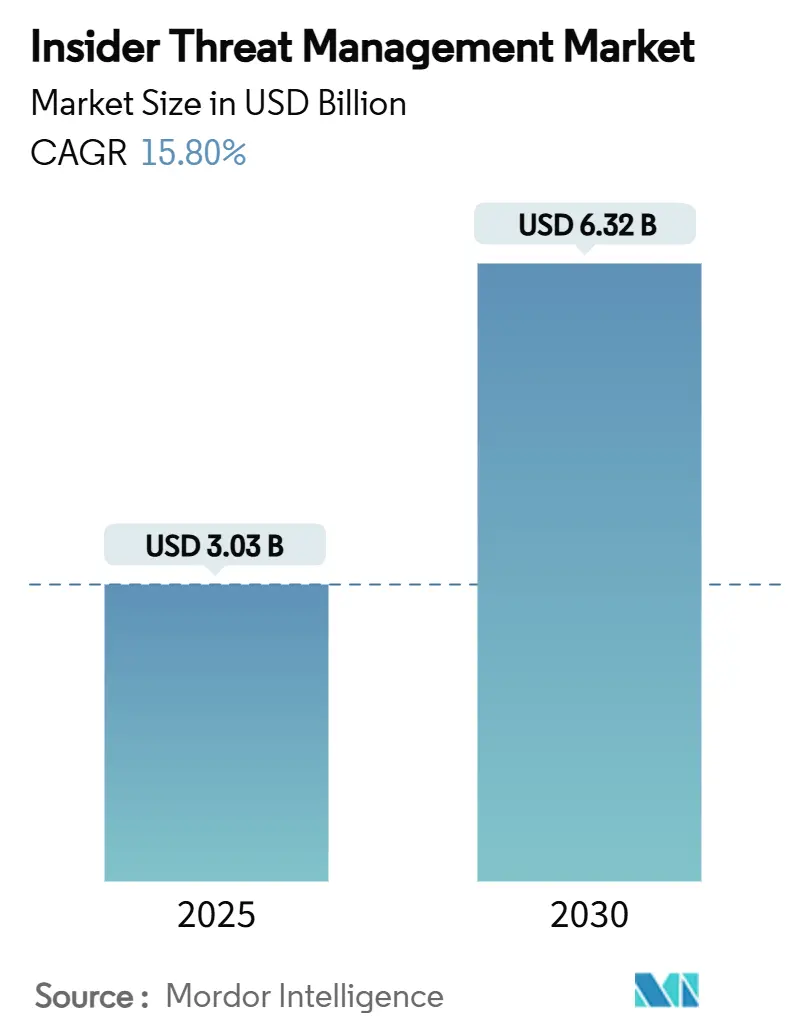

The Insider Threat Management Market size is estimated at USD 3.03 billion in 2025, and is expected to reach USD 6.32 billion by 2030, at a CAGR of 15.80% during the forecast period (2025-2030). Demand accelerates as enterprises recognize that perimeter-centric defenses cannot stop credential misuse, data exfiltration, and sabotage originating from trusted users. Growth is reinforced by stringent privacy legislation, increased board-level focus on risk, and rising cyber-insurance requirements for user-centric controls. Investment in AI-based behavioral analytics is lifting detection accuracy while lowering analyst workload. Venture funding and public-sector zero-trust mandates are further expanding the insider threat management market by widening adoption beyond highly regulated sectors.

Key Report Takeaways

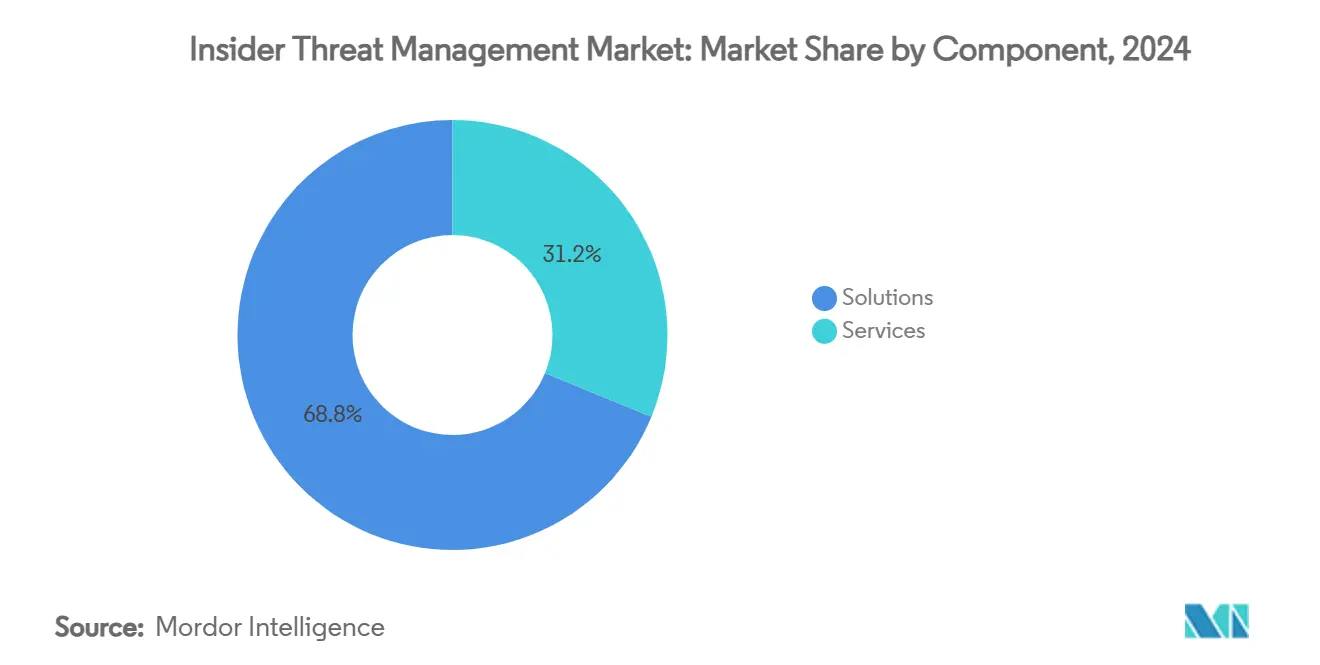

- By component, solutions accounted for 68.8 of % insider threat management market share in 2024, while services are advancing at a 17.6% CAGR through 2030.

- By deployment mode, cloud captured 71.7% of the insider threat management market size in 2024 and is projected to grow at a 16.5% CAGR to 2030.

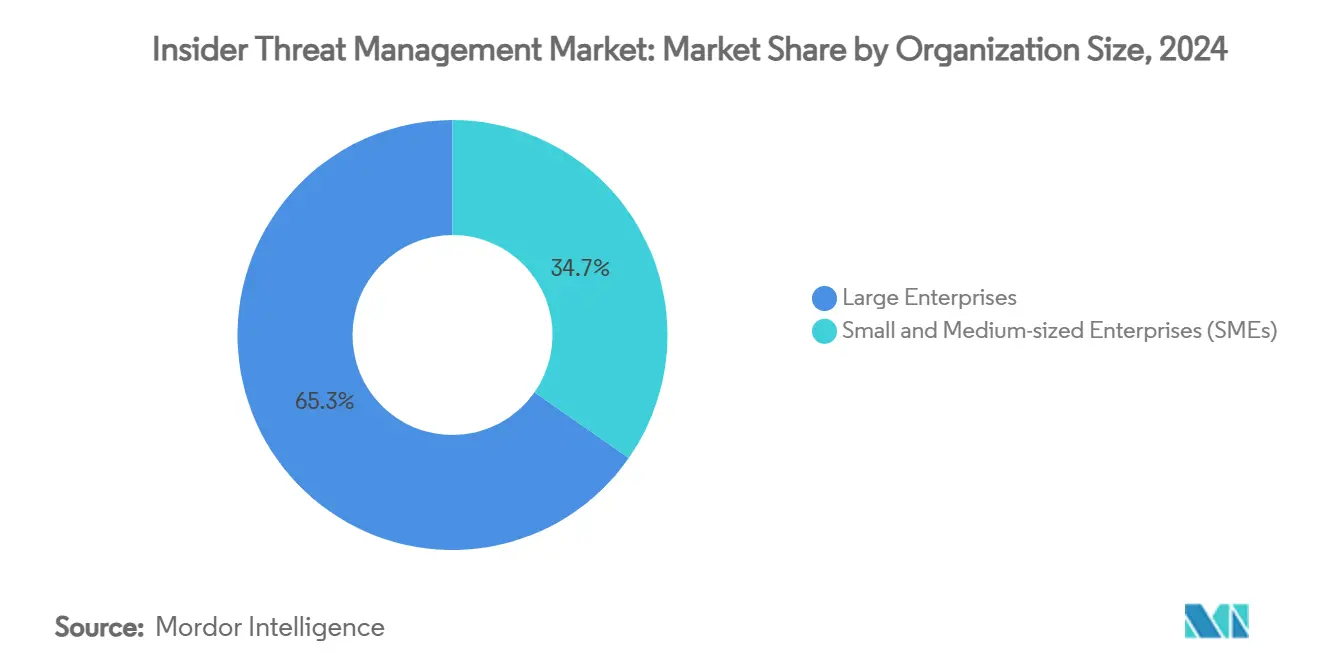

- By organization size, large enterprises held 65.3% revenue share of the insider threat management market size in 2024, whereas small and medium-sized enterprises are expanding at a 17.8% CAGR during the forecast window.

- By end-use industry, BFSI led with 29.1% market share of the insider threat management market size in 2024; healthcare and life sciences are forecast to record the fastest 16.9% CAGR through 2030.

- By geography, North America commanded 38.2% of 2024 revenues, while Asia-Pacific is expected to post a 17.1% CAGR to 2030.

Global Insider Threat Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of hybrid/remote work expanding threat surface | +3.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Stringent data-privacy regulations (GDPR, CCPA, DPDP Act India) driving compliance spend | +2.8% | Global, with early adoption in EU, North America, India | Long term (≥ 4 years) |

| Rising cloud and SaaS adoption demanding inside-out visibility | +2.5% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| AI-powered behavioral analytics improving detection accuracy | +2.1% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Cyber-insurance underwriting now mandates insider-risk controls | +1.8% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Venture funding spike for pure-play insider-risk vendors | +1.4% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosion of hybrid/remote work expanding threat surface

Pandemic-era work patterns normalised long-term hybrid arrangements, leaving security teams with limited line-of-sight into unmanaged devices and home networks. Federal Bureau of Investigation data show a steep rise in remote-linked cybercrime since 2022, with insider incidents tracking the overall surge. Zero-trust network access is becoming the default for new remote connections, and behavioral telemetry now extends to collaboration suites and file-sync tools. Average breach costs tied to remote work are rising, especially in healthcare, where off-site access to patient records brings HIPAA scrutiny. [1]U.S. Department of Health & Human Services, “Healthcare Cybersecurity Bulletin,” hhs.gov As a result, investments in analytics that profile user baselines regardless of location continue to swell.

Stringent data-privacy regulations driving compliance spend

The EU General Data Protection Regulation, California Consumer Privacy Act, and India’s Digital Personal Data Protection Act impose heavy fines for mishandling personal information. Enterprises, therefore, raise privacy budgets to fund continuous monitoring, access governance, and incident audit trails. Eight in ten global organisations have appointed an internal Data Protection Officer to oversee compliance. Firms are swapping legacy solutions for identity-centric data loss prevention that traces data lineage. Multinationals expect further spend as jurisdictions in Latin America, the Middle East, and Southeast Asia draft similar laws.

Rising cloud and SaaS adoption demanding inside-out visibility

Workloads in Microsoft 365, Salesforce, AWS, and other SaaS platforms now store sensitive intellectual property outside the corporate firewall. The insider threat management market sees cloud deployment preferred for elasticity, real-time model tuning, and unified telemetry across multiple tenants. Security vendors increasingly integrate cloud APIs to ingest activity logs and apply anomaly scoring. Edge deployments that combine local processing with cloud inference help heavily regulated entities meet data-residency rules while still benefiting from AI engines hosted in hyperscale clouds.

AI-powered behavioral analytics improving detection accuracy

Machine-learning models evaluate keystrokes, file movements, and sentiment in user communications to flag subtle deviations earlier than rule sets can. Leading platforms cite 94.7% detection accuracy and 38% fewer false positives after adopting adaptive models. [2]DTEX Systems, “AI³ Launch Press Release,” dtexsystems.com Generative AI now summarises events for analyst review and suggests remediation, cutting mean time to resolution. Small businesses access these capabilities through pay-as-you-go offerings, broadening the addressable insider threat management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute cybersecurity skills shortage hampers program maturity | -2.3% | Global, most severe in North America and Europe | Long term (≥ 4 years) |

| User-privacy regulations limit monitoring depth | -1.8% | EU and California leading, expanding globally | Medium term (2-4 years) |

| Budget prioritization toward perimeter controls over insider tools | -1.2% | Global, with emphasis in cost-conscious SME segment | Short term (≤ 2 years) |

| Legacy SIEM/DLP overlap causing buyer confusion | -0.9% | North America and Europe, mature security markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute cybersecurity skills shortage hampers program maturity

The global talent gap is projected to exceed 3.4 million unfilled roles in 2025. Specialised analysts who interpret behavioural data and lead discreet investigations are especially scarce. Japanese surveys show three-quarters of firms are unable to recruit sufficient staff, driving demand for managed detection and response. Automation eases workload, but complex cases still rely on human judgment that AI cannot yet match.

User-privacy regulations limit monitoring depth

GDPR and similar statutes require data minimisation, purpose limitation, and employee transparency. Enterprises must balance granular monitoring with legal and cultural expectations of privacy. Some adopt privacy-preserving federated learning to analyse patterns without centralising raw personal data, though this can trim accuracy. Compliance teams, therefore, coordinate closely with security to craft proportional controls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Market Foundation

Solutions dominated 2024 revenue, owning 68.8% share of the insider threat management market. Enterprises prize platforms merging user and entity behaviour analytics, insider risk scoring, and identity-centric data loss prevention in one console. Scalability is critical; leading tools process up to 10 million log events daily, delivering near-real-time alerts. The insider threat management market size for services is smaller today, yet expanding briskly as firms lacking in-house expertise outsource 24/7 monitoring. Managed detection and response providers bundle behavioural analytics, legal guidance, and HR coordination, filling the widening skills void.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments captured 71.7% revenue in 2024 and will continue to outpace on-premise at 16.5% CAGR. This reflects the migration of IP and regulated data into SaaS and the appetite for elastic compute to train AI models. The insider threat management market size attributable to on-premise remains steady among defence and critical-infrastructure operators bound by sovereignty rules. Hybrid patterns are emerging, with agents collecting events locally and forwarding metadata to cloud engines for correlation.

By Organization Size: SMEs Emerge as Growth Engine

Large enterprises controlled 65.3% of 2024 spend, underpinned by deep budgets and complex compliance mandates. Program maturity is high; several Fortune 500 companies now align executive compensation to insider risk metrics. Yet SMEs are the fastest-rising cohort, expanding at 17.8% CAGR. Consumption-based licences and simplified dashboards allow companies with lean teams to deploy enterprise-grade analytics in days. The insider threat management industry now tailors pre-configured playbooks for common SME use-cases such as departing employee data grabs.

By End-use Industry: BFSI Leads, Healthcare Accelerates

BFSI retained a 29.1% share of the insider threat management market in 2024 due to high transaction volumes and stringent audit obligations. Financial firms log every privileged action, seeking to pinpoint anomalous money movement or customer record access. In contrast, healthcare and life sciences forecast the strongest 16.9% CAGR. High-value patient data and the surge in telemedicine create fertile ground for credential abuse. Device proliferation in research labs also adds visibility challenges addressed by user-centric analytics.

Geography Analysis

North America generated 38.2% of 2024 revenues, buoyed by early behavioural analytics adoption, a proactive regulatory stance, and venture capital that accelerates product innovation. Federal agencies operate mature insider programs that influence private-sector standards, while zero-trust roadmaps set technology benchmarks for suppliers.

Europe follows, shaped by GDPR enforcement that obliges continuous monitoring and rich audit trails. Vendors emphasise privacy-by-design, offering flexible data-masking and local processing options to satisfy varied member-state requirements.

Asia-Pacific is the fastest-expanding regional opportunity at 17.1% CAGR. Japan’s government highlights insider risk among its top three cyber concerns, spurring investment across manufacturing, telecom, and aerospace. In parallel, organisations in India, Australia, and Singapore boost spending as new data-protection bills come online. These forces collectively stimulate the insider threat management market across the region.

Competitive Landscape

The insider threat management market remains moderately fragmented, though consolidation is accelerating. Strategic deals such as Palo Alto Networks' acquiring Protect AI for USD 500 million and Thoma Bravo’s USD 5.3 billion bid for Darktrace enlarge platform breadth and compress standalone vendor space. [3]Palo Alto Networks, “Protect AI Acquisition Announcement,” paloaltonetworks.com AI performance is the main differentiator: DTEX Systems’ AI³ engine cuts false positives by 59% while analysing tens of millions of daily events, helping the firm secure a USD 50 million growth round from Alphabet’s CapitalG. [4]DTEX Systems, “AI³ Launch Press Release,” dtexsystems.com

Partnerships also shape positioning. Proofpoint’s alliance with Microsoft embeds data-loss prevention hooks into Azure, and CyberArk integrates privileged-identity telemetry to enrich anomaly scoring. Vendors explore quantum-safe cipher detection, edge analytics for operational technology, and sentiment analysis within collaboration tools.

New entrants focus on generative-AI-driven triage, offering plain-language explanations of risk and automated policy recommendations. Funding momentum suggests continued innovation, although heightened due diligence by investors will test lesser differentiated offerings.

Insider Threat Management Industry Leaders

Dtex Systems Inc.

Proofpoint Inc.

Forcepoint LLC

Securonix Inc.

Varonis Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: DTEX Systems launched AI³ technology that applies generative AI to accelerate insider-risk investigations.

- May 2025: Tenable acquired Apex to expand AI-driven risk analytics for insider threat use cases.

- May 2025: Impart Security closed a USD 12 million Series A round to build adaptive detection models.

- April 2025: Palo Alto Networks finalised the USD 500 million takeover of Protect AI, enhancing its insider analytics stack.

- March 2025: Microsoft added 11 AI agents to Security Copilot, automating phishing analysis and regulatory alert handling.

- March 2025: Proofpoint and Microsoft formed a global alliance to fortify human-centric security controls in Microsoft 365.

Global Insider Threat Management Market Report Scope

| Solutions | User and Entity Behavior Analytics (UEBA) |

| Insider Risk Management Platforms | |

| User Activity Monitoring and Session Recording | |

| Identity-Centric Data Loss Prevention (IDLP) | |

| Services | Professional Services |

| Managed Detection and Response (MDR) for Insider Risk |

| Cloud |

| On-premise |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Government and Defense |

| Retail and eCommerce |

| IT and Telecom |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | User and Entity Behavior Analytics (UEBA) | |

| Insider Risk Management Platforms | |||

| User Activity Monitoring and Session Recording | |||

| Identity-Centric Data Loss Prevention (IDLP) | |||

| Services | Professional Services | ||

| Managed Detection and Response (MDR) for Insider Risk | |||

| By Deployment Mode | Cloud | ||

| On-premise | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-sized Enterprises (SMEs) | |||

| By End-use Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Manufacturing and Industrial | |||

| Government and Defense | |||

| Retail and eCommerce | |||

| IT and Telecom | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current insider threat management market size?

The insider threat management market size stands at USD 3.03 billion in 2025 and is projected to climb to USD 6.32 billion by 2030.

Which deployment model is growing fastest?

Cloud-based solutions are expanding at a 16.5% CAGR, reflecting enterprise migration to SaaS and the need for elastic AI analytics.

Why is BFSI the largest end-user industry?

Stringent financial regulations and high transaction volumes make BFSI organisations prioritize behavioural monitoring, giving the sector 29.1% 2024 market share.

How are privacy laws affecting adoption?

Regulations such as GDPR require robust audit trails yet constrain excessive monitoring, prompting vendors to build privacy-preserving analytics that satisfy both compliance and security.

What role does AI play in insider threat management?

AI improves detection accuracy to approximately 95% while cutting false positives, automating triage, and helping firms overcome cybersecurity staff shortages.

Which region offers the highest growth potential?

Asia-Pacific is forecast to grow at a 17.1% CAGR as countries tighten data-protection rules and invest in zero-trust architectures.

Page last updated on: