Inkjet Colorants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

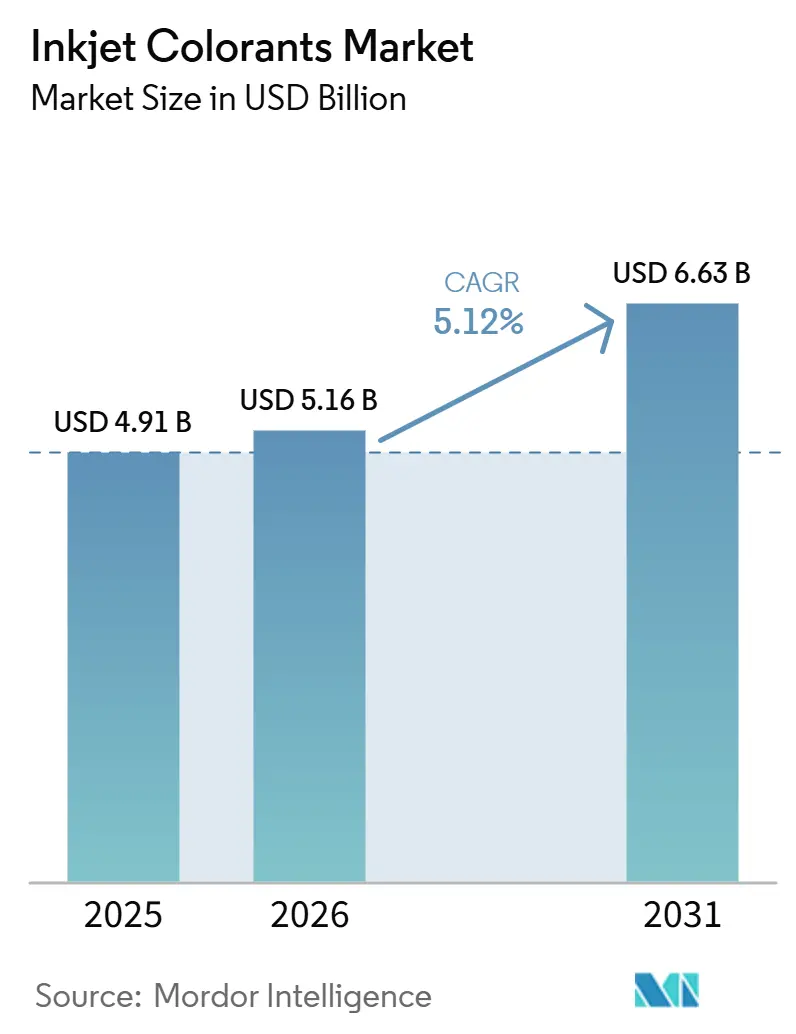

| Market Size (2026) | USD 5.16 Billion |

| Market Size (2031) | USD 6.63 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inkjet Colorants Market Analysis by Mordor Intelligence

The Inkjet Colorants Market size is expected to increase from USD 4.91 billion in 2025 to USD 5.16 billion in 2026 and reach USD 6.63 billion by 2031, growing at a CAGR of 5.12% over 2026-2031. The increasing demand for low-VOC printing on corrugated boxes, flexible films, and labels is driving packaging converters to adopt water-based and UV-curable chemistries. In the Asia-Pacific region, textile mills are moving toward digital inkjet lines, which reduce setup times and enable mass customization. Industrial users are utilizing high-resolution systems for applications such as coding, marking, and direct decoration on electronic housings. Nano-pigment dispersions, measuring below 15 nanometers, are gaining preference over traditional dyes by preventing nozzle clogging and expanding the color spectrum. Additionally, UV-curable formulations are capturing market share from solvent-based options, as their instant curing reduces energy consumption and supports heat-sensitive substrates.

Key Report Takeaways

- By colorant type, pigments led with 55.11% revenue share in 2025; nano-pigments are projected to expand at a 5.57% CAGR from 2026 to 2031.

- By formulation type, water-based systems accounted for 60.33% of 2025 sales, while UV-curable chemistries are advancing at a 5.89% CAGR from 2026 to 2031.

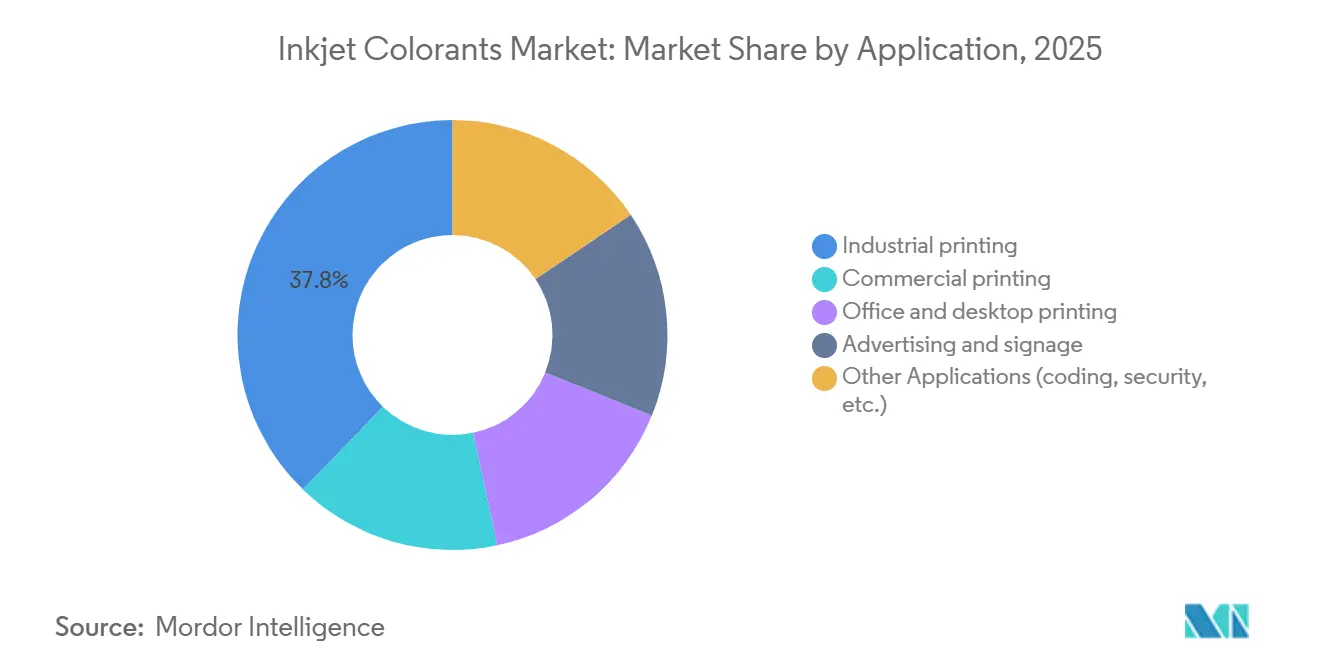

- By application, industrial printing commanded 37.77% of the inkjet colorants market share in 2025, and is growing fastest at a 6.11% CAGR from 2026 to 2031.

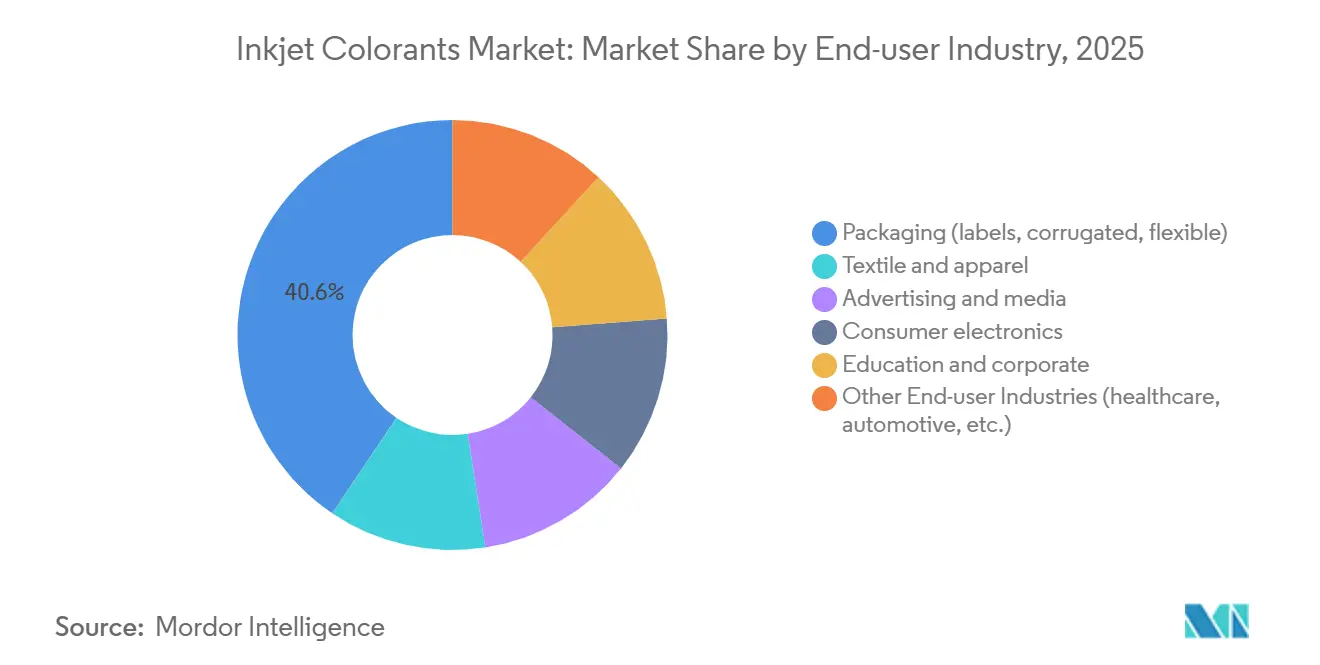

- By end-user industry, packaging retained leadership with 40.55% of 2025 value; textile and apparel is set to post a 6.18% CAGR from 2026 to 2031.

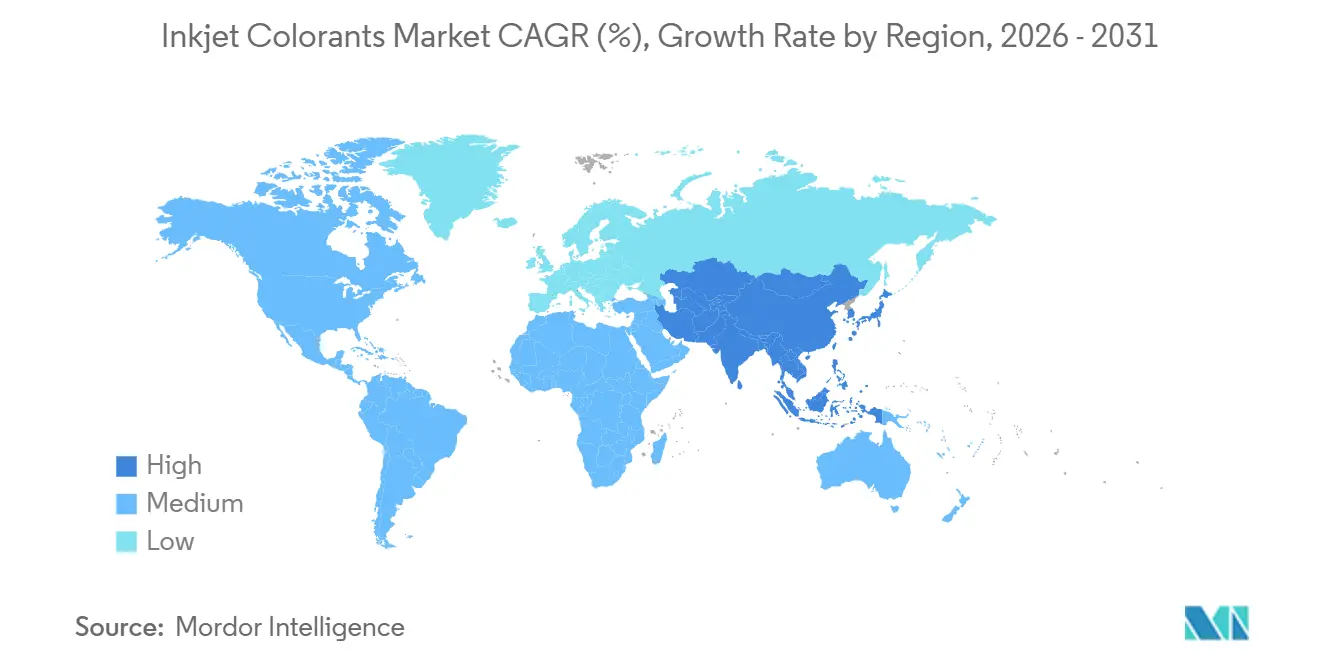

- By geography, Asia-Pacific captured 46.23% of 2025 revenue and is poised to expand at a 5.9% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Inkjet Colorants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of digital textile printing and packaging | + 1.8% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Advancements in high-resolution inkjet technology | + 1.3% | Global, with early adoption in Japan, Germany, United States | Short term (≤ 2 years) |

| Shift toward water-based and eco-friendly formulations | + 1.5% | Europe and North America regulatory-driven, Asia-Pacific brand-driven | Medium term (2-4 years) |

| Rise of on-demand additive-manufacturing inks | + 0.7% | North America and Europe industrial hubs, emerging in China | Long term (≥ 4 years) |

| Integration of colorants for printed electronics | + 0.6% | Japan and South Korea core, expanding to China and Taiwan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Digital Textile Printing and Packaging

Textile mills are shifting from traditional screen lines to inkjet systems, reducing break-even volumes from thousands of meters to just hundreds. This change allows brands to align production with actual demand. In 2025, Monster Digital expanded its operations with ten Kornit Apollo units, enabling same-day fulfillment for apparel pre-orders[1]Monster Digital, “Kornit Apollo Installation,” monsterdigital.com. Erreà Sport increased its production efficiency by incorporating seven Mimaki Tiger-1800B MkIII printers, achieving a production rate of 150 m² per hour on polyester blends. Corrugated and flexible converters are adopting water-based presses, such as Fujifilm’s Jet Press FP790, which bonds to polyolefin films without requiring corona treatment. Asia-Pacific remains a key region, with China's digital ink expenditure in textiles reaching CNY 4.417 billion in 2025, representing approximately 20% of the global total.

Advancements in High-Resolution Inkjet Technology

Pharmaceutical serialization and security labels now benefit from nano-pigments, achieving an impressive 1,200 dpi output. Kodak’s KODACOLOR platform boasts an 11 nm mean particle size, achieving a remarkable 99% first-pass yield[2]Kodak Inc., “KODACOLOR Nano-Pigment Dispersions,” kodak.com. This efficiency translates to reduced waste, especially on production lines exceeding 100 m/min. In a notable advancement, Kobe University showcased structural-color printing using silver nanoparticles. These nanoparticles shift hue based on the viewing angle, bolstering anti-counterfeiting measures. In a collaborative effort, Epson and Manz Asia are pioneering inkjet deposition techniques tailored for semiconductor photoresist patterning. This innovation paves the way for expanded opportunities in printed electronics. Additionally, hyperdispersants like Evonik’s TEGO Dispers 695 play a crucial role, stabilizing pigment loads exceeding 25 wt% while ensuring viscosity remains within optimal jetting parameters.

Shift Toward Water-Based and Eco-Friendly Formulations

Stricter VOC limits under the EU Industrial Emissions Directive and U.S. NESHAP are influencing the shift toward water-based solutions. Sun Chemical introduced AquaHeat, a product designed to withstand temperatures of 220 °C in a retort while containing 60% bio-renewable content. Kao Collins developed LUNAJET, which delivers VOC-free performance on polyolefins without requiring primers. Nazdar paired high-viscosity water inks with NIR dryers, achieving a 40% reduction in energy consumption compared to hot air methods. Toyo Ink Europe introduced GIO-compliant UV inks ahead of Germany's January 2027 mineral-oil ban, reflecting the industry's adjustment to compressed compliance timelines.

Rise of On-Demand Additive-Manufacturing Inks

Functional colorants that either conduct electricity or manage heat are becoming increasingly important in additive manufacturing. Silver nanoparticle inks provide more than 10% bulk silver conductivity for PCB traces. BASF’s QDYES quantum-dot dispersions contribute to a 10% improvement in electroluminescent efficiency. UV-curable ceramic inks, which can endure sintering temperatures above 600 °C, enable the production of full-color graphics on automotive glazing. North America and Europe currently hold a significant position, while Chinese contract manufacturers are adopting inkjet technology to enhance customization capabilities.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC and wastewater regulations | -0.9% | Europe and North America primary, China secondary | Short term (≤ 2 years) |

| Competition from laser, UV-offset and hybrid presses | -0.5% | Global, most acute in commercial printing and office segments | Medium term (2-4 years) |

| Nozzle clogging and dispersion-stability issues | -0.6% | Global, acute in nano-pigment and high-solids formulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and Wastewater Regulations

New EU caps of 50 mg/m³ VOC for printing installations, along with similar U.S. limits, are increasing reformulation costs. By January 2027, Germany's food-contact ink regulations will require the removal of mineral-oil resins, necessitating technological adjustments. Minnesota's wastewater directives, which limit copper and chromium to under 1 ppm, are contributing to higher filtration expenses. China's updated Water Pollution Control Law, with fines up to CNY 1 million for violations, is encouraging the replacement of heavy-metal driers. While large multinationals can allocate testing costs across global volumes, regional suppliers are experiencing pressure on their margins.

Nozzle Clogging and Dispersion-Stability Issues

Printhead orifices, sized between 10-50 µm, encounter clogging issues when agglomerates exceed design thresholds. High dispersant loads can prevent flocculation but may increase viscosity levels beyond the 10 cP mark. Evonik’s AERODISP additives are designed to adjust rheology in UV-curable inks, helping to reduce settling during pauses in the production line. Sun Chemical’s Microlith solid dispersions provide an 18-month shelf life at 50 °C without any drift. Kodak reports achieving a 99% first-pass yield by maintaining particle distribution within a 2 nm range. However, the requirement for head cleaning can reduce the cost advantages of digital printing, particularly on packaging lines that aim for over 90% uptime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Colorant Type: Nano-Pigments Drive Performance Gains

In 2025, pigments accounted for 55.11% of total revenue, indicating their higher lightfastness compared to dyes. Nano-pigments, the fastest-growing sub-segment, are projected to grow at a 5.57% CAGR. Their particle sizes, kept below 15 nm, reduce nozzle clogging risks and improve the color gamut. Kodak’s 11 nm dispersions enhance print quality to 1,200 dpi on glossy substrates. In November 2025, Sun Chemical increased its perylene pigment production by 200 tons, focusing on packaging inks that require Blue Wool 7 lightfastness. Disperse dyes continue to hold a share in cost-sensitive textiles, although brands are shifting to pigments to comply with Oeko-Tex standards.

In security printing, carbon black and TiO₂ pigments meet barcode contrast standards above 1.5:1 under NIR light. Japan and Germany are key adopters of nano-pigments for food-contact compliance. Specialty variants are being developed for sublimation and ceramic decoration, where stability beyond 200 °C is critical.

By Formulation Type: UV-Curable Gains on Instant Cure

In 2025, water-based systems represented 60.33% of the demand, while UV-curable inks exhibited a higher growth rate with a 5.89% CAGR. INX International’s MDLM inks cure in 0.5 seconds at a rate of 2,000 cans per minute, supporting metal-can decoration without requiring ovens. Toyo Ink Europe’s GIO series has addressed the removal of mineral oil in preparation for the 2027 regulations. UV-LED arrays reduce energy consumption by 70% and maintain surface temperatures below 50 °C, making them suitable for foam and film substrates.

Solvent lines continue to be used in outdoor signage, particularly where plasticizer migration necessitates strong carriers. Roland’s ECO-SOL MAX reduces odor through the use of glycol ethers. Latex and eco-solvent inks provide a balance between performance and regulatory compliance. Near-infrared dryers, when used with high-viscosity water inks, achieve a 40% reduction in energy consumption.

By Application: Industrial Printing Leads Volume and Growth

Industrial printing, which constituted 37.77% of the 2025 application revenue, is anticipated to grow at a 6.11% CAGR through 2031. This growth is attributed to developments in coding, marking, and direct-to-shape technologies. Videojet’s 2380 thermal printer, offering a 600 dpi resolution, addresses EU and U.S. pharmaceutical serialization requirements. KEYENCE MK-G operates at a speed of 120 pieces per minute and is designed for printing on curved parts within the cosmetics packaging segment. The adoption of digital solutions is increasing due to the benefits of variable data and tooling-free production, which are gradually replacing analog methods.

In the commercial printing segment, the focus is on producing photo books and mailers with quick turnaround times. The office desktop segment is experiencing a decline as enterprises shift towards managed services, with a preference for laser printing. The signage segment is moving towards latex and UV LED technologies. For instance, Mimaki’s UJ330H-160 printer supports printing on 10 cm-thick boards, catering to the POS display market. Additionally, niche applications in security, ceramics, and biomedicine are contributing to the segment's growth.

By End-User Industry: Textile Outpaces Packaging Growth

In 2025, the packaging segment accounted for 40.55% of the revenue share, while the textile and apparel segment is expected to grow at the fastest rate, with a 6.18% CAGR through 2031. Kornit’s Apollo lines, in collaboration with Monster Digital, support same-day apparel sales for items pre-sold online. Erreà Sport utilizes a Mimaki fleet with a throughput of 150 m²/h. Fujifilm’s Jet Press FP790 introduces plate-free customization for flexible pouches.

Within the advertising segment, UV-curable and latex inks are used for vehicle wraps, offering a three-year outdoor lifespan. The consumer electronics segment employs instant-cure inks, particularly on polycarbonate cases. Segments such as healthcare, automotive interiors, and ceramics are increasingly adopting digital workflows due to the design flexibility they provide. Growth in the textile segment is influenced by the demand for on-demand fashion and efforts to reduce inventory levels.

Geography Analysis

Asia-Pacific, which accounted for 46.23% of 2025 revenue, is projected to grow at a 5.90% CAGR through 2031. In China, textile digital-ink expenditure reached CNY 4.417 billion, driven by mills in Guangdong and Zhejiang adopting Kornit and Mimaki systems. Siegwerk's acquisition of Hi-Tech Inks in 2026 is expected to secure 20% of India's flexible-packaging market, strengthening clusters in Gujarat and Tamil Nadu. In Japan, OEMs are advancing 1,200 dpi heads operating beyond 50 kHz. South Korea is transitioning its beverage-label lines to UV inks. Across ASEAN nations, relocations are increasing the demand for compliant water-based and UV-curable solutions.

In North America and Europe, growth is moderating as markets focus on replacements rather than new developments. The U.S. NESHAP and Germany's mineral-oil ban are driving faster adoption of eco-formulations. Flint Group's establishment of a plant in India highlights the Asian focus of European suppliers. In Canada and Mexico, near-shoring trends are increasing digital press installations, particularly in Ontario and Jalisco.

In South America and the Middle East & Africa, Brazil's sportswear printers are shifting to inkjet technology. In Saudi Arabia, the Vision 2030 initiative is directing funds toward packaging expansions, with a preference for UV and water-based inks. In South Africa, high-odor solvent lines in commercial buildings are being replaced.

Competitive Landscape

The inkjet colorants market is moderately fragmented. Key suppliers include DIC Corporation / Sun Chemical, known for their expertise in pigment dispersion. DuPont (Artistri) focuses on high-performance inks for textiles and packaging. FUJIFILM Corporation (under Sericol and Inkjet) specializes in UV-curable and wide-format inks. Huntsman International Inc. provides solutions in textile reactive and disperse dye platforms, while TOYO INK CO., LTD. operates across the pigment-to-ink value chain. Vertical integration is becoming more prevalent as companies like Sun Chemical and DIC expand into formulated inks, and OEMs such as Fujifilm develop proprietary colorants. Siegwerk's acquisitions of Allinova in 2025 and Hi-Tech Inks in 2026 enhance its eco-friendly capabilities and presence in South Asia. Additionally, Sudarshan Chemical's acquisition of Heubach for over EUR 1 billion expands its pigment offerings.

Growth opportunities are emerging in nano-silver and copper inks for printed electronics, as well as in bio-derived dispersants that align with circular economy requirements. Evonik's TEGO Dispers 695 stabilizes 25 wt% pigment loads without affecting viscosity. Patent activity is focused on multi-functional additives that reduce the number of ink components. Competitors are differentiating based on total cost of ownership, emphasizing factors such as nozzle uptime, shelf stability, and regulatory compliance, rather than solely competing on price.

Inkjet Colorants Industry Leaders

DIC CORPORATION

FUJIFILM Corporation

Huntsman International. Inc.

DuPont

Toyo Ink Co., Ltd. (artience Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Siegwerk announced a definitive agreement to acquire Hi-Tech Inks, a leading Indian producer of flexographic and gravure printing inks. This acquisition strengthens Siegwerk's position in India's flexible packaging sector, making it the market leader with over 20 percent share.

- August 2025: Siegwerk signed a deal to acquire Allinova, a specialty chemicals firm in Hengelo, Netherlands, known for its expertise in water-based dispersions.

Global Inkjet Colorants Market Report Scope

Inkjet colorants are the specialized pigments or dyes that provide color to inkjet inks, enabling the marking, coding, or printing of images and text. They are key raw materials designed to meet stringent requirements, such as low viscosity, high surface tension, and superior stability to pass through tiny printhead nozzles.

The market is segmented by colorant type, formulation type, application, end-user industry and geography. By colorant type, the market is segmented into dyes, pigments, nano-pigments, and disperse dyes and other types. By formulation type, the market is segmented into water-based, solvent-based, UV-curable, and eco-solvent and latex. By application, the market is segmented into commercial printing, industrial printing, office and desktop printing, advertising and signage, and other applications (including coding and security). By end-user industry, the market is segmented into textile and apparel, packaging (including labels, corrugated, and flexible), advertising and media, consumer electronics, education and corporate, and other end-user industries (including healthcare and automotive). The report also covers the market size and forecasts for Inkjet Colorants in 19 countries across the world. For each segment market sizing and forecasts are provided in terms of value (USD).

| Dyes |

| Pigments |

| Nano-pigments |

| Disperse dyes and others |

| Water-based |

| Solvent-based |

| UV-curable |

| Eco-solvent and latex |

| Commercial printing |

| Industrial printing |

| Office and desktop printing |

| Advertising and signage |

| Other Applications (coding, security, etc.) |

| Textile and apparel |

| Packaging (labels, corrugated, flexible) |

| Advertising and media |

| Consumer electronics |

| Education and corporate |

| Other End-user Industries (healthcare, automotive, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Colorant Type | Dyes | |

| Pigments | ||

| Nano-pigments | ||

| Disperse dyes and others | ||

| By Formulation Type | Water-based | |

| Solvent-based | ||

| UV-curable | ||

| Eco-solvent and latex | ||

| By Application | Commercial printing | |

| Industrial printing | ||

| Office and desktop printing | ||

| Advertising and signage | ||

| Other Applications (coding, security, etc.) | ||

| By End-user Industry | Textile and apparel | |

| Packaging (labels, corrugated, flexible) | ||

| Advertising and media | ||

| Consumer electronics | ||

| Education and corporate | ||

| Other End-user Industries (healthcare, automotive, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the inkjet colorants market?

The Inkjet Colorants Market size was valued at USD 4.91 billion in 2025 and is estimated to grow from USD 5.16 billion in 2026 to reach USD 6.63 billion by 2031, at a CAGR of 5.12% during the forecast period (2026-2031).

Which segment shows the fastest growth within the inkjet colorants space?

Textile and apparel leads growth, advancing at a 6.18% CAGR between 2026 and 2031.

What segment is the main growth driver?

Industrial printing is the fastest-growing application, increasing at a 6.11% CAGR as manufacturers adopt on-demand coding and direct-to-object graphics.

How quickly are UV-curable formulations growing?

UV-curable inks register a 5.89% CAGR through 2031, the highest among formulation types.

Which region generates the most revenue for inkjet colorants?

Asia-Pacific contributes 46.23% of global revenue and is growing at a 5.90% CAGR.

Page last updated on: