Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.16 Billion |

| Market Size (2031) | USD 22.33 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

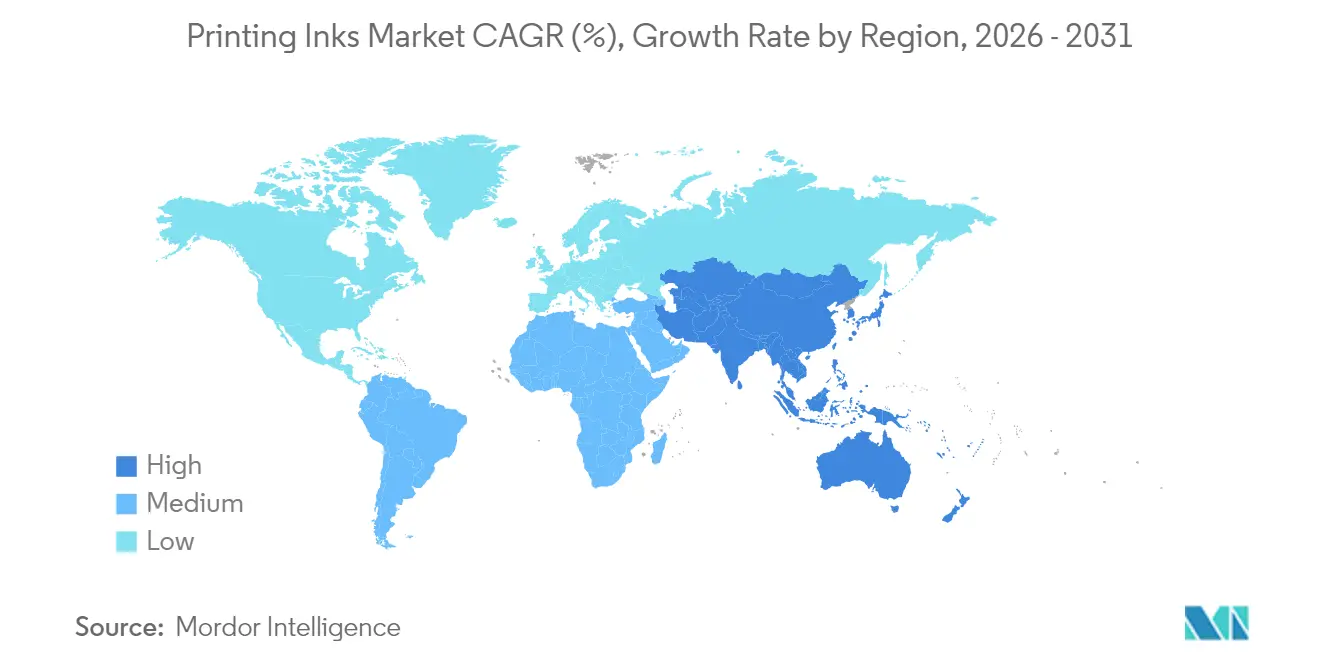

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Printing Inks Market Analysis by Mordor Intelligence

The Printing Inks Market size was valued at USD 18.58 billion in 2025 and estimated to grow from USD 19.16 billion in 2026 to reach USD 22.33 billion by 2031, at a CAGR of 3.11% during the forecast period (2026-2031). Packaging, digitalization, and sustainability together shape demand patterns, capital investment, and regional shifts. Packaging already commands 55.94% of the printing inks market and remains the fastest-expanding application at 4.37% CAGR through 2030. Oil-based formulations keep a major share, but UV-LED inks post the highest 7.59% CAGR as converters pursue instant curing and lower energy use. The printing inks market, therefore, balances legacy strengths with emerging eco-friendly and digital capabilities.

Key Report Takeaways

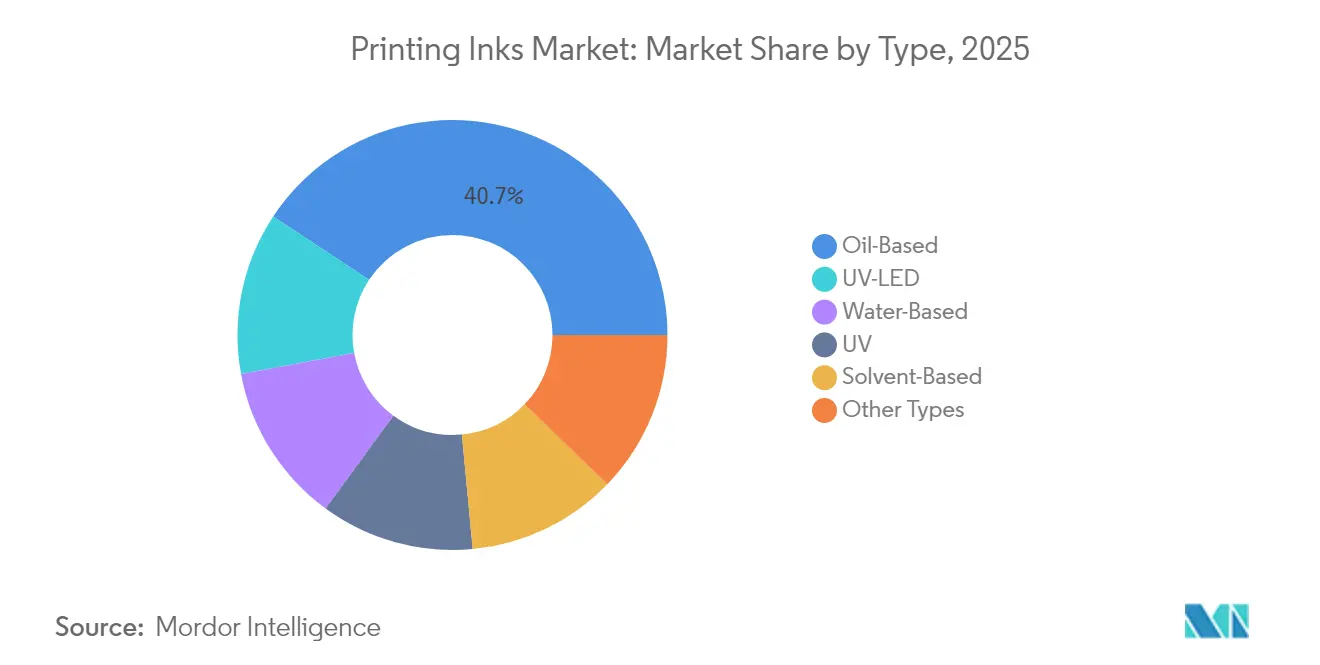

- By type, oil-based inks accounted for 40.70% share of the printing inks market size in 2025, and UV-LED formulations are advancing at a 7.47% CAGR through 2031.

- By process, lithographic printing held 32.95% of the printing inks market share in 2025, while digital printing records the highest projected CAGR at 8.15% through 2031.

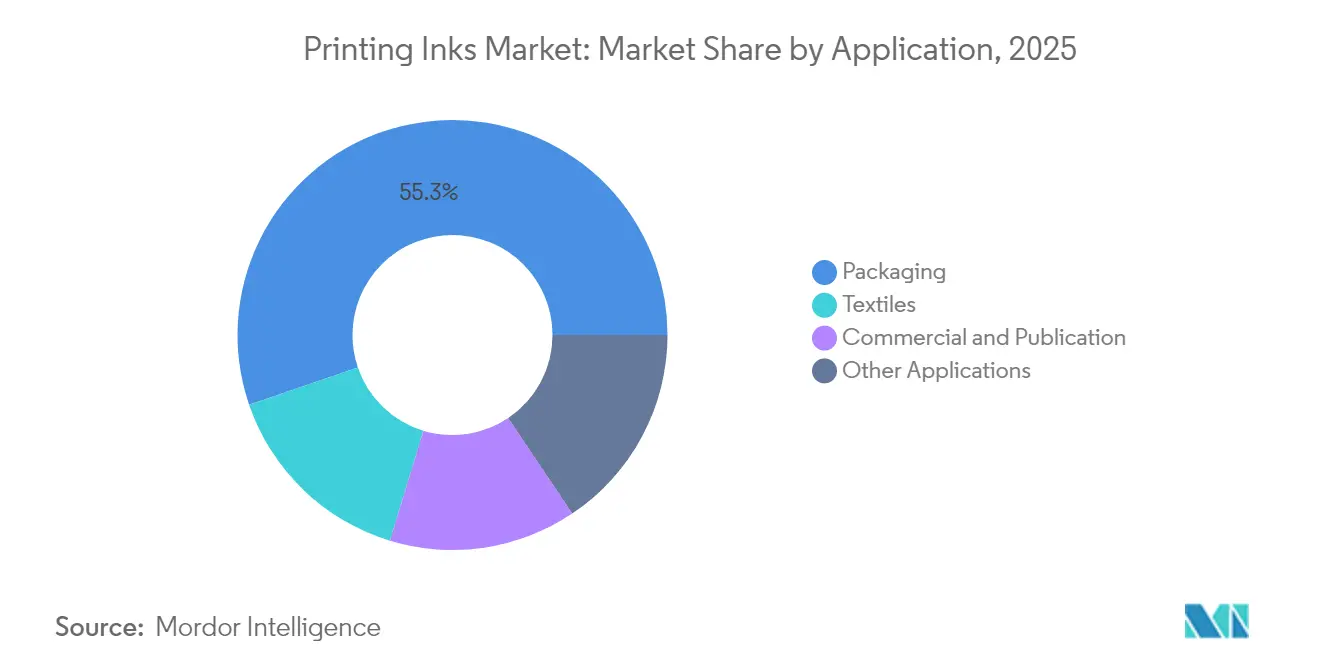

- By application, packaging led with 55.25% revenue share in 2025 and is forecast to expand at a 4.29% CAGR to 2031.

- By geography, Asia-Pacific captured 40.10% share of the printing inks market size in 2025 and is forecast to rise at a 3.96% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Printing Inks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in digital printing industry | +0.8% | Global, with APAC and North America leading adoption | Medium term (2-4 years) |

| Expansion of packaging and labels demand | +0.7% | Global, strongest in APAC and emerging markets | Long term (≥ 4 years) |

| Shift toward water-based eco-friendly inks | +0.6% | Europe and North America core, expanding to APAC | Medium term (2-4 years) |

| Emergence of UV/energy-curable technologies | +0.5% | North America and EU, with APAC adoption accelerating | Long term (≥ 4 years) |

| Adoption of functional conductive inks for electronics | +0.4% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Digital Printing Industry

Digital printing has moved from a niche concept to a mainstream production platform that reshapes the printing inks market. Continuous drops in equipment cost and head improvements allow converters to migrate short and medium runs toward inkjet, improving job turnaround and reducing inventory risk. Ink manufacturers respond with low-viscosity, high-optical-density pigment packages that maintain color consistency at high jetting speeds. Digital fabric printing already approaches 15 billion meters annually, stimulated by on-demand apparel and décor customization. Packaging converters exploit variable data to address seasonal promotions and localized languages, compressing lead times from weeks to days.

Expansion of Packaging and Labels Demand

Global demand for packaged goods expands steadily as rising urbanization, smaller household sizes, and e-commerce fulfillment change consumption habits. Corrugated boxes, paperboard sleeves, and flexible pouches all require durable, food-safe inks that withstand mechanical stress and logistics humidity. Brands rely on high-fidelity graphics and tactile finishes to stand out on crowded shelves, which boosts the value of specialty coatings and metallic pigments. Emerging economies in Asia-Pacific and parts of Africa see double-digit growth in packaged food and personal care, underpinning volume gains for water-based flexo and gravure inks. Label applications become more data-rich, integrating QR codes and anti-counterfeiting features that demand precise registration and robust color stability. The net result is sustained volume expansion even during macro-economic slowdowns, reinforcing packaging’s role as the primary growth engine for the printing inks market.

Shift Toward Water-Based Eco-Friendly Inks

Regulatory pressures and brand sustainability goals accelerate the migration from solvent-borne to water-based chemistries. France has mandated the phase-out of mineral-oil inks for many consumer applications by 2025, while Germany already accounts for 15.3% of eco-ink usage within Europe. The new formulations achieve lower volatile organic compound levels, improved recyclability, and favorable food-contact profiles, making them attractive for corrugated packaging and publication insert printing. Advancements in pigment dispersion and surfactant technology deliver equivalent gloss and rub resistance compared with solvent systems, dissolving historical performance barriers. Early movers gain a marketing advantage and reduce compliance costs, nudging laggards to accelerate research and development spending. Water-based adoption therefore reinforces the overall sustainability narrative that increasingly guides procurement choices in the printing inks market.

Emergence of UV/Energy-Curable Technologies

UV-LED curing provides instant hardening, allowing printers to eliminate extended drying tunnels and print on heat-sensitive films. Energy consumption drops significantly because LED arrays emit in specific wavelengths and require no warm-up cycle. Field data from commercial sheet-fed presses show ink savings near 20% and turnaround-time improvements near 40%. INX International has expanded its energy-curable portfolio across flexographic and electron-beam platforms, demonstrating versatile performance on plastics and metalized substrates. Luxury packaging buyers appreciate the high gloss, chemical resistance, and odor-neutral profiles that UV-LED delivers. As capital costs fall, medium-sized converters in Asia-Pacific accelerate adoption, lifting the segment’s 7.59% CAGR within the printing inks market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decline in conventional commercial printing | -0.4% | Global, most pronounced in North America and Europe | Medium term (2-4 years) |

| Stringent VOC and waste-disposal regulations | -0.3% | Europe and North America core, expanding globally | Long term (≥ 4 years) |

| Nitrocellulose raw-material shortages | -0.2% | Global, with acute impact on specialty ink manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Decline in Conventional Commercial Printing

Newspaper and magazine circulations shrink every quarter as advertisers reallocate budgets to digital channels. In January 2024, shipments of U.S. printing-writing paper fell 9% year on year. Offset ink consumption therefore declines, leaving surplus blending capacity and intensifying price competition. Print houses retire older presses, which trims aftermarket demand for replacement inks and dampens revenue for maintenance services. Some suppliers respond by refitting mixing facilities to produce water-based flexo systems, but pay-back periods stretch when demand for commercial print remains soft. The secular downturn subtracts 0.4 percentage points from the forecast CAGR, partially offset by new digital and packaging volumes.

Stringent VOC and Waste-Disposal Regulations

Environmental agencies tighten permissible solvent limits and broaden chemical substance restrictions. The U.S. Environmental Protection Agency published updated National VOC Emission Standards for aerosol coatings with compliance milestones extending to January 2027[1]Environmental Protection Agency, “National Volatile Organic Compound Emission Standards for Aerosol Coatings: Interim Final Rule,” federalregister.gov . Europe’s REACH framework added carcinogenic and mutagenic substances to Annex XVII effective September 2025. Reformulation efforts raise raw-material costs and extend development cycles, particularly for smaller producers lacking deep research and development budgets. Waste management rules also demand closed-loop cleaning systems, adding capital expenditure on recovery units. While the regulations push the printing inks market toward greener chemistries, they temporarily squeeze margins and lengthen time-to-market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Oil-Based Dominance Faces Technology Disruption

Oil-based inks secured 40.70% of 2025 revenue due to cost efficiency and broad compatibility, yet their growth remains subdued under tightening VOC rules. UV-LED products post a 7.47% CAGR, reflecting converter preference for instant curing and energy savings. Water-based packages gain traction in corrugated cartons and paper cups, especially inside the European Union where food-contact and recyclability requirements grow stricter. Solvent systems persist in specialized industrial decals that need extreme adhesion, though volume gradually migrates toward less volatile alternatives.

Conversion logistics shape purchasing behavior. UV-LED presses avoid extended maintenance shut-downs because lamp life often exceeds 20,000 hours. Reduced scrap and lower energy bills tilt the total cost of ownership advantage toward energy-curable chemistries. In parallel, bio-based oil replacements gain interest as feedstock volatility and disclosure requirements under corporate sustainability reporting standards increase. Early adopters secure marketing premiums for plant-derived content, although supply chains for bio-solvents remain nascent. The combined trend signals a gradual, though definitive, reweighting of the printing inks market toward low-VOC, quick-cure platforms.

By Process: Lithographic Leadership Challenged by Digital Innovation

Lithographic presses remain the workhorse for many large-volume catalogs and folding cartons, holding a 32.95% share of 2025 output. However, their share edge narrows as inkjet lines deliver higher uptime and require no plate inventory. Digital presses clock the fastest 8.15% CAGR thanks to variable data capabilities and on-the-fly job changes that enable micro-targeted promotions. Flexographic units increase color gamut with expanded-spectrum anilox rolls and low-migration water-based inks, strengthening their role in flexible packaging. Gravure retains importance for very long runs and metallic finish control, especially in Asia, where integrated packaging complexes seek consistent film thickness across millions of impressions.

Technology choices now depend on run length, substrate mix, and sustainability goals rather than historic plant layouts. ISO 2846 colorimetric standards help printers switch between process paths without brand color drift, easing mixed-technology fast launches. As digital consumable prices fall, the printing inks market evolves away from purely volume-based cost curves toward value-based service models such as pay-per-print. Ink suppliers deepen partnerships with press OEMs to fine-tune rheology and thermal stability, protecting nozzle health and reducing downtime. These alliances anchor future revenue streams even as the installed base of analog presses declines.

By Application: Packaging Supremacy Accelerates Market Evolution

Packaging commands both scale and momentum. Its 55.25% share in 2025, together with a 4.29% CAGR, reinforces its status as the fulcrum of the printing inks market. Corrugated shippers accommodate the surge in e-commerce parcel traffic, whereas premium folding cartons and rigid boxes support beauty and spirits categories that prize shelf impact. Flexible pouches gain share because lightweight structures lower freight costs and increase retailer facings. Water-based and UV-LED inks excel in these applications by offering low odor, excellent bond strength, and rapid post-print handling.

Textiles emerge as a promising diversification path. Direct-to-garment and dye-sublimation systems facilitate on-demand fashion, reducing unsold inventory and environmental waste. Ink chemistries must deliver wash resistance and fabric hand softness, prompting suppliers to blend pigment nanosizing with polymeric binders. Security printing, encompassing tamper-evident seals and track-and-trace labels, gains relevance as regulators tackle counterfeit pharmaceuticals and high-value electronics. Although commercial and publication segments shrink, specialized book runs such as photo albums and children’s titles persist by leveraging digital color personalization. The multifaceted application mix cushions the printing inks market against single-segment volatility.

Geography Analysis

Asia-Pacific holds 40.10% of global 2025 revenue and grows at 3.96% CAGR, reflecting robust manufacturing ecosystems in China, India, and Southeast Asia. Domestic consumption rises alongside expanding middle classes, boosting demand for packaged snacks, personal care, and pharmaceuticals. Local converters invest in high-speed flexo lines and adopt UV-LED retrofits to conserve energy and meet export customer audits. Governments in China and India support electronics and solar module supply chains, indirectly stimulating conductive ink opportunities for sensors and busbars. Regional raw material access, notably pigments and resin intermediates, supports competitive pricing that feeds into global trade flows of printing inks.

Europe enforces some of the most stringent environmental rules, accelerating migration to water-based and energy-curable platforms. Germany’s leadership in eco-ink adoption and France’s mineral-oil ban drive regional suppliers to overhaul formulations and invest in closed-loop solvent recovery. Luxury brand clusters in Italy and France pursue premium finishing, elevating the demand for metallic, pearlescent, and tactile varnish systems. Eastern European converters adopt modular flexo lines to serve cross-continent retail groups, often specifying the same low-migration inks required by Western buyers.

North America combines technological maturity with tight VOC oversight. The EPA’s TSCA evaluations push formulators to validate raw-material toxicology and invest in safer alternatives. Major converters implement predictive maintenance platforms; INX International reported a 13% bump in asset availability after deploying AI analytics on production lines. Mexico gains share as a near-shoring hub for packaged food and personal care goods destined for the United States and Canada, lifting regional ink volumes. Brand owners push for recycling-ready inks that do not impair paper repulping or polyolefin reclamation, fostering collaboration across the packaging value chain. The region exemplifies how automation, sustainability, and regulatory stringency intersect to shape the future trajectory of the printing inks market.

Competitive Landscape

The printing inks market shows moderate fragmentation. Global leaders such as Siegwerk and ALTANA optimize scale synergies in procurement and cross-border logistics. Meanwhile, regional champions tailor portfolios to local taste profiles and regulatory nuances, building loyalty through agile technical support. They often partner with OEMs for co-development of niche systems like high-opacity white inks for recycled PET labels. Supply risks remain. Nitrocellulose shortages elevate lead times for solvent flexo and gravure inks, prompting some converters to prequalify alternative binders. Pigment price volatility, especially for key azo shades, forces formulators to evaluate high-gamut hybrid systems. Regulatory scrutiny over PFAS compounds and photo-initiator residues drives rapid raw-material re-screening. Market participants who integrate sustainability certifications, digital color management, and agile sourcing thus secure a strategic edge in the printing inks market.

Printing Inks Industry Leaders

DIC Corporation

Flint Group

hubergroup

Sakata INX Corporation

Siegwerk Druckfarben AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: DuPont premiered Artistri PN1000 low-viscosity pigment inks at drupa 2024, citing enhanced optical density and food-contact compliance.

- March 2024: DIC India inaugurated an INR 1.1 billion (~USD 0.013 billion) toluene-free liquid-ink plant in Gujarat with 10,000-ton yearly capacity.

Global Printing Inks Market Report Scope

Printing inks consist of a pigment or pigments of the required color mixed with oil or varnish, majorly a black ink made from carbon blacks and thick linseed oil added. The printing ink market is segmented by type, process, application, and geography. By type, the market is segmented into solvent-based, water-based, oil-based, UV, UV-LED, and other types of inks. By process, the market is segmented into lithographic printing, flexographic printing, gravure printing, digital printing, and other processes. By application, the market is segmented into packaging, commercial and publication, textiles, and other applications. The report also covers the market size and forecasts for the printing inks market in 19 countries across major regions. The report offers market size and forecasts for printing inks in volume (metric tons) for all the above segments.

By Type

| Solvent-Based |

| Water-Based |

| Oil-Based |

| UV |

| UV-LED |

| Other Types |

By Process

| Lithographic Printing |

| Flexographic Printing |

| Gravure Printing |

| Digital Printing |

| Other Processes |

By Application

| Packaging | Rigid Packaging | Paperboard Containers |

| Corrugated Boxes | ||

| Rigid Plastic Containers | ||

| Metal Cans | ||

| Other Rigid Packaging | ||

| Flexible Packaging | ||

| Labels | ||

| Other Packaging | ||

| Commercial and Publication | ||

| Textiles | ||

| Other Applications |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Solvent-Based | ||

| Water-Based | |||

| Oil-Based | |||

| UV | |||

| UV-LED | |||

| Other Types | |||

| By Process | Lithographic Printing | ||

| Flexographic Printing | |||

| Gravure Printing | |||

| Digital Printing | |||

| Other Processes | |||

| By Application | Packaging | Rigid Packaging | Paperboard Containers |

| Corrugated Boxes | |||

| Rigid Plastic Containers | |||

| Metal Cans | |||

| Other Rigid Packaging | |||

| Flexible Packaging | |||

| Labels | |||

| Other Packaging | |||

| Commercial and Publication | |||

| Textiles | |||

| Other Applications | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Key Questions Answered in the Report

How large is the printing inks market in 2026?

The printing inks market size is USD 19.16 billion in 2026 with a 3.11% CAGR forecast to 2031.

Which segment is growing fastest within printing inks?

Digital printing inks expand at an 8.15% CAGR as converters pursue short runs and customization.

Why does packaging dominate printing-ink demand?

Packaging captures 55.25% share because e-commerce, premium branding, and food safety rules all demand high-performance, often eco-friendly inks.

What technology shift is most disruptive for ink suppliers?

UV-LED curing reshapes process economics by delivering instant drying, lower energy use, and compatibility with heat-sensitive films.

How are regulations influencing ink formulation?

Stricter VOC limits and REACH substance bans accelerate the move toward water-based and energy-curable chemistries that cut emissions and improve recyclability.

Page last updated on: