Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.69 Billion |

| Market Size (2026) | USD 4.84 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Printing Inks Market Analysis by Mordor Intelligence

The United States Printing Inks Market size is projected to expand from USD 4.69 billion in 2025 and USD 4.84 billion in 2026 to USD 5.64 billion by 2031, registering a CAGR of 3.11% between 2026 to 2031. Healthy e-commerce volumes, book-on-demand workflows, and brand-owner sustainability mandates are widening the customer base for low-migration ultraviolet (UV) LED, water-based flexographic, and electron-beam chemistries. Domestic-content preferences under the Buy American Act are encouraging formulators to shift pigment and resin sourcing to US suppliers, while tariffs on Chinese titanium dioxide are accelerating diversification into algae-derived and soy-based alternatives. At the same time, tightening federal and state volatile-organic-compound (VOC) caps are hastening the retreat of solvent-heavy gravure inks in favor of water-based and UV technologies. Capital spending from the top five suppliers, DIC (Sun Chemical), Flint Group, Siegwerk, Hubergroup, and Sakata INX, continues to target UV LED capacity, bio-based resins, and conductive‐ink dispersions that serve printed-electronics opportunities. These converging forces are expected to keep the United States printing inks market on a steady expansion path through 2031.

Key Report Takeaways

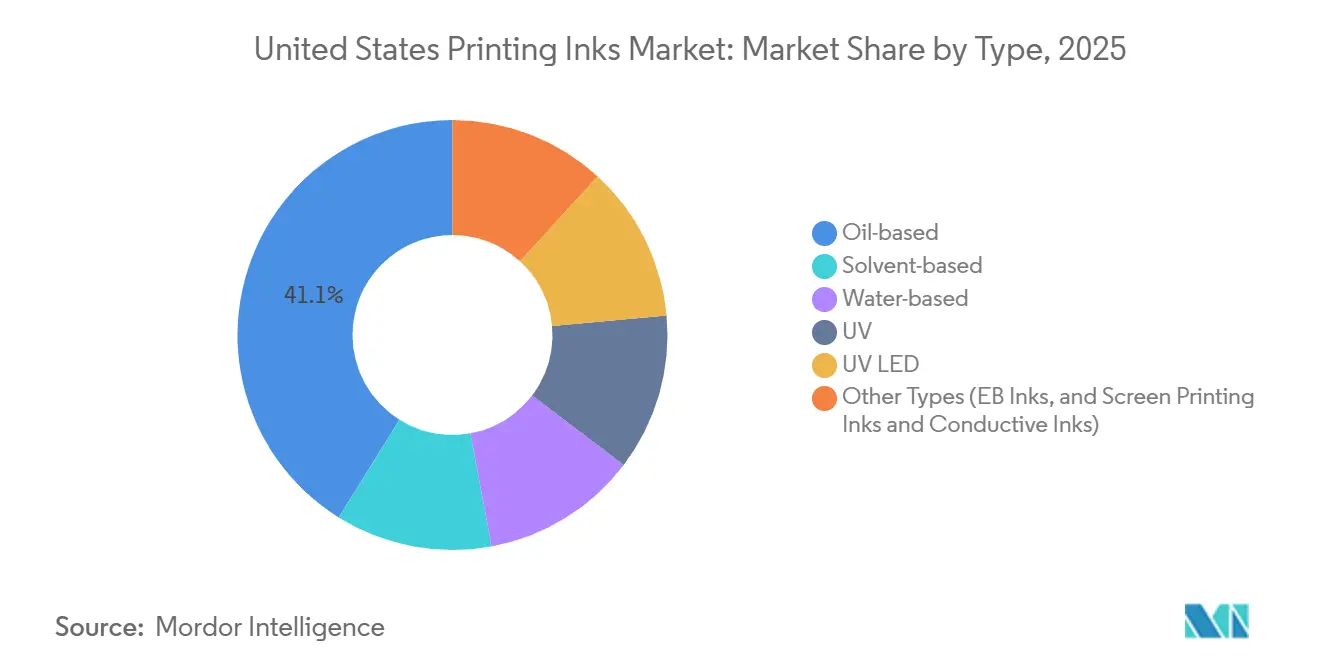

- By type, oil-based inks held the largest 41.12% share of the United States Printing Inks market in 2025, while Other Types advanced the fastest at a 5.11% CAGR during the forecast period (2026-2031).

- By printing process, lithographic sheetfed maintained the top 27.22% share during 2025; digital printing is projected to expand at the segment-leading 4.92% CAGR during the forecast period (2026-2031).

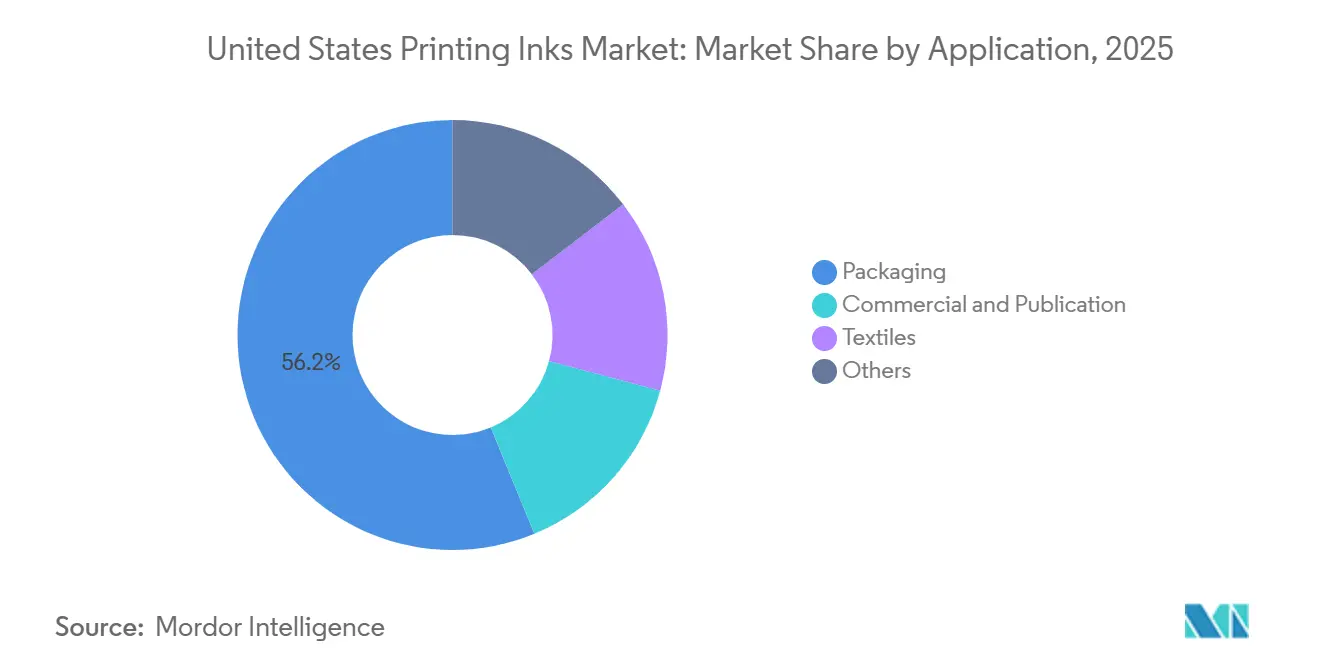

- By application, packaging commanded 56.23% of the United States Printing Inks market share in 2025 and is also forecast to post the quickest 3.93% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Printing Inks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-driven corrugated packaging growth | +0.8% | National, logistics hubs in Texas, California, Illinois | Medium term (2-4 years) |

| Resurgent on-demand book printing | +0.3% | National, education publishing centers in Northeast and Midwest | Short term (≤ 2 years) |

| Brand-owner migration to low-migration UV/LED curables | +0.6% | National, food-contact packaging converters | Medium term (2-4 years) |

| Federal “Buy American” preferences for sustainable inks | +0.4% | National, defense and infrastructure contracts | Long term (≥ 4 years) |

| Algae-derived pigment pilot plants achieving cost parity | +0.2% | National, specialty packaging and textiles | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Driven Corrugated Packaging Growth

Corrugated-box shipments topped USD 4.9 billion in 2024 as fulfillment centers handled smaller, more frequent parcels for direct-to-consumer brands[1]PRINTING United Alliance, “State of the Industry Report 2025,” printing.org. Water-based flexographic inks dominate because they dry quickly on recycled linerboard and comply with the Environmental Protection Agency’s National Emission Standards for Hazardous Air Pollutants (NESHAP) VOC (Volatile Organic Compound) limit of 0.04 kg/kg solids. Variable-data inkjet systems are gaining share by printing QR codes and promotional graphics without plate changes, and suppliers such as INX International report double-digit growth for digital corrugated inks. Amazon’s 2024 pledge to remove plastic air pillows heightened linerboard demand and spurred printers to adopt aqueous dispersions that hold density on lighter substrates. Together, sustainability mandates and throughput needs are set to keep packaging volumes ahead of overall United States printing inks market growth through 2031.

Resurgent On-Demand Book Printing

Print-on-demand bounced back in 2024-2025 as publishers trimmed warehousing costs and met niche-title demand via high-speed pigment-inkjet webs. An industry survey cited 10%-20% annual growth in educational print-on-demand orders, reflecting rapid curriculum updates. PRINTING United Alliance forecasts 2.1%-6.4% annual expansion for commercial printing through 2028, contingent on digital-inkjet uptake. Toner remains standard for monochrome blocks, yet aqueous inkjet now captures color inserts below 500 copies and runs at 150 m/min. Book manufacturers such as Walsworth added inkjet lines to serve self-publishing authors, while ink formulators refined aqueous dispersions to match offset image quality and satisfy OSHA (Occupational Safety and Health Administration)’s updated Hazard Communication Standard.

Brand-Owner Migration to Low-Migration UV/LED Curables

Food and pharmaceutical brands increasingly specify inks that meet US FDA and EU 10/2011 migration limits. Flint Group’s USD 150 million UV LED expansion equips narrow-web label converters to cure at 40-60°C, cutting energy use up to 70%. Siegwerk’s Michigan plant now formulates low-migration UV products that pass Nestlé and Unilever protocols without post-cure odor. Electron-beam inks, commercialized by Energy Sciences Inc., eliminate photoinitiators altogether and comply with FDA (Food and Drug Administration) direct-food-contact rules[2]Energy Sciences Inc., “EB Curing for Food Packaging,” ebeam.com. Hubergroup further strengthened the value proposition in 2025 by launching a bio-based UV resin with 70% renewable carbon. Strong brand-owner audits are therefore tilting run lengths from solvent gravure toward UV LED and EB technologies.

Federal “Buy American” Preferences for Sustainable Inks

The 2024 Federal Acquisition Regulation update raised domestic-content minima to 55% in 2026, climbing to 75% by 2030. Contracting officers apply a 20% price preference to compliant bids, and parallel Build America, Buy America rules stretch into infrastructure programs at the Department of Energy. With Section 301 tariffs placing a 25% duty on Chinese titanium dioxide, pigment producers such as DIC have announced US debottlenecking projects to localize supply. Living Ink Technologies’ algae black, cultivated in Colorado, already qualifies as 100% domestic, allowing converters to meet both tariff and sustainability scorecards. These procurement preferences are expected to channel incremental federal volumes toward domestically sourced, low-VOC systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OSHA and state VOC-caps tightening solvent use | −0.4% | National, strictest in California and Northeast | Short term (≤ 2 years) |

| Pigment supply-chain risk from China-US trade tensions | −0.5% | National, acute for TiO₂ and organics | Medium term (2-4 years) |

| Prospective California microplastics additive ban | −0.3% | California, potential Oregon–Washington spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OSHA and State VOC-Caps Tightening Solvent Use

The 2024 Hazard Communication Standard revision obliges updated safety data sheets for inks exceeding VOC thresholds. North Carolina capped flexographic ink VOC content at 25 wt%, and the South Coast AQMD Rule 1171 enforces even lower limits, although 2024 amendments allow maximum incremental reactivity averaging for compliance. Rising compliance costs have trimmed solvent gravure’s mid-single-digit share as printers switch to water-based flexo that now equals solvent adhesion on polyolefins. EPA’s NESHAP standard further restricts new publication-rotogravure installations to 0.04 kg VOC per kg solids. Collectively, these regulations squeeze margins for solvent systems and accelerate UV LED and aqueous adoption across the United States printing inks market.

Pigment Supply-Chain Risk from China-US Trade Tensions

Section 301 tariffs that jumped to 10%-60% in February 2025 put a 25% duty on Chinese titanium dioxide, lifting pigment prices 10%-15% across 2024. DIC, Sun Chemical, and smaller formulators are diversifying to Indian TiO₂ and European organics, but qualifying new grades lengthens lead times and raises inventory risk. Specialty quinacridone and phthalocyanine pigments remain China-centric, exposing high-performance packaging inks to sudden shortages. Sun Chemical’s minority stake in a non-Chinese TiO₂ producer reflects an industry rush to secure alternative supply bases. Until localization projects ramp up, cost volatility may delay product launches and compress margins, especially for pigment-dense gravure formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Oil-Based Formulations Sustain Lithographic Dominance

Oil-based inks, with a 41.12% share of 2025 volume, anchor the United States printing inks market size in lithographic offset, where emulsification control and oxidative curing assure color fidelity on coated cartons and labels. Linseed, soybean, and mineral-oil carriers provide the tack and dry-back that more than 15,000 installed sheetfed presses demand. Water-based grades, now in the mid-20% range, outpace overall growth as adhesion on polyethylene and polypropylene matches historical solvent benchmarks. Solvent gravure continues to erode due to VOC limits and digital displacement, while UV and UV LED inks, currently in the high-teen share, expand hand-in-hand with brand-owner low-migration audits.

The Other Types cluster, electron-beam, screen, and conductive formulas, accounts for a modest base yet is set to rise at a 5.11% CAGR during the forecast period (2026-2031), the swiftest in the portfolio. EB inks avoid photoinitiators and reach FDA direct-food-contact approval without costly migration testing. Conductive silver dispersions from DuPont and Henkel enable roll-to-roll sensor production, linking the United States printing inks market size to the USD 5.8 billion printed-electronics arena in 2024. Screen-print textiles also benefit as hybrid rotary-screen-inkjet lines marry throughput with variable data, stimulating incremental ink tonnage.

By Printing Process: Digital Inkjet Outpaces Legacy Lithographic Growth

Sheetfed lithography, with a 27.22% market share in 2025, remains entrenched owing to large installed capital and unmatched Pantone accuracy for premium folding cartons and brochures. Flexography enjoys e-commerce momentum as water-based liners print efficiently on recycled corrugated, while gravure shrinks under regulatory pressure and long-run catalog declines. Specialty processes, including textile screen and industrial graphics, round out demand with emerging conductive and functional applications that lift the United States printing inks market share for advanced inks.

Digital platforms are forecast to post a 4.92% CAGR during the forecast period (2026-2031), comfortably exceeding the broader United States printing inks market. Label converters value plate-free changeovers that serve craft-beverage SKUs under 10,000 linear feet, pushing digital inks to 15% of label volume by 2025. Aqueous pigment-inkjet dominates for its zero-VOC profile and offset-comparable resolution on coated stocks, gaining traction in on-demand book lines that drop warehouse costs.

By Application: Packaging Leads Volume and Growth Amid E-Commerce Surge

Packaging captured 56.23% of 2025 demand and is slated to rise at a 3.93% CAGR during the forecast period (2026-2031), outpacing publication and commercial segments. Rigid corrugated and paperboard formats absorb water-based flexographic inks that meet EPA (Environmental Protection Agency) VOC ceilings, while UV LED grades penetrate folding cartons destined for direct-food-contact situations. Flexible pouches and flow wraps import water-based and UV chemistries that now equal solvent gravure’s seal strength, driving substitution over the forecast window.

Commercial print, including books and catalogs, trails growth, but pockets of resilience remain in educational on-demand titles. Labels, a high-margin subset, transition fastest to digital as variable artwork and regional compliance data proliferate. Textile and functional print niches contribute incremental volume via pigment-inkjet and conductive circuitry, linking the United States printing inks market share gains to wearable electronics and smart-packaging rollouts.

Geography Analysis

The United States printing inks market is nationwide, yet regional dynamics shape demand profiles. In the first cluster, California, Texas, and Illinois, large fulfillment centers and consumer-goods hubs drive corrugated packaging tonnage that favors water-based flexography for rapid dry-back on recycled linerboard. The Midwest and Northeast serve as academic publishing nuclei, and their print-on-demand rebound has buoyed aqueous inkjet sales for short-run textbooks and scholarly monographs. Gulf-Coast chemical corridors, meanwhile, anchor raw-material supply for resin and pigment intermediates, giving local ink makers an edge in lead times and Buy American compliance.

West Coast sustainability statutes add complexity. California’s Senate Bill 1053 and South Coast AQMD (Air Quality Management District) Rule 1171 impose some of the nation’s most stringent microplastic and VOC limits, steering converters toward UV LED and bio-based formulations sooner than in other regions. Oregon and Washington are evaluating parallel rules that could extend the regulatory corridor northward. Across the Southeast, flexible-packaging converters leverage proximity to food-processing plants, stimulating trials of electron-beam ink that withstands retort while avoiding photoinitiators.

Finally, government procurement hotspots in Washington DC and Virginia influence domestic-content adoption. Federal contract print shops prioritize United States printing inks market size products that clear 55% local-value thresholds, increasingly specified in infrastructure program tenders. As domestic-content minima ratchet up to 65% in 2029, suppliers with US pigment and resin capacity should capture incremental share, especially for security documents and regulatory manuals.

Competitive Landscape

The United States Printing Inks market is moderately fragmented. Strategic themes converge on sustainability, supply-chain security, and advanced functionality. Patent filings in photoinitiator-free UV systems and conductive polymers are rising, while joint ventures between ink makers and printed-electronics firms accelerate roll-to-roll sensor commercialization. With regulatory pressures and technology transitions unfolding concurrently, competitive intensity is expected to persist, rewarding suppliers that validate performance and compliance in tandem.

United States Printing Inks Industry Leaders

Flint Group

Siegwerk Druckfarben AG & Co. KGaA

DIC Corporation

hubergroup

INX International Ink Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Fujifilm Corporation collaborated with ImpactWest to strengthen its United States presence. The partnership brought Fujifilm’s production print technology to businesses on the West Coast, leveraging ImpactWest’s regional service and support capabilities.

- January 2026: Canon U.S.A. introduced the Texas LT3 Series UV LED true flatbed printers. The Texas LT3 Series, available in LT3/X2 and LT3/X3 models, featured print speeds of up to 7,489 square feet per hour, advanced LED UV curing technology, and enhanced color options, including orange, gray, white, and varnish.

United States Printing Inks Market Report Scope

Printing inks consist of pigments or pigments of the required color mixed with oil or varnish, mainly a black ink made from carbon blacks and thick linseed oil added.

The United States Printing Inks market for printing inks is segmented by type, printing process, and application. By type, the market is segmented into solvent-based, water-based, oil-based, UV, UV-LED, and other types (EB inks, screen printing inks, and conductive inks). By printing process, the market is segmented into lithographic web printing, lithographic sheetfed printing, flexographic printing, gravure printing, digital printing, and other processes. By application, the market is segmented into packaging, commercial and publication, textiles, and others. The report offers market size and forecasts for printing ink in the United States in value (USD) for all the above segments.

By Type

| Solvent-based |

| Water-based |

| Oil-based |

| UV |

| UV LED |

| Other Types (EB Inks, and Screen Printing Inks and Conductive Inks) |

By Printing Process

| Lithographic Web Printing |

| Lithographic Sheetfed Printing |

| Flexographic Printing |

| Gravure Printing |

| Digital Printing |

| Other Process |

By Application

| Packaging | Rigid Packaging | Paperboard Containers |

| Corrugated Boxes | ||

| Rigid Plastic Containers | ||

| Metal Cans | ||

| Others | ||

| Flexible Packaging | ||

| Labels | ||

| Other Packaging | ||

| Commercial and Publication | ||

| Textiles | ||

| Others |

| By Type | Solvent-based | ||

| Water-based | |||

| Oil-based | |||

| UV | |||

| UV LED | |||

| Other Types (EB Inks, and Screen Printing Inks and Conductive Inks) | |||

| By Printing Process | Lithographic Web Printing | ||

| Lithographic Sheetfed Printing | |||

| Flexographic Printing | |||

| Gravure Printing | |||

| Digital Printing | |||

| Other Process | |||

| By Application | Packaging | Rigid Packaging | Paperboard Containers |

| Corrugated Boxes | |||

| Rigid Plastic Containers | |||

| Metal Cans | |||

| Others | |||

| Flexible Packaging | |||

| Labels | |||

| Other Packaging | |||

| Commercial and Publication | |||

| Textiles | |||

| Others | |||

Key Questions Answered in the Report

How large is the United States printing inks market in 2026?

It is estimated at USD 4.84 billion, advancing toward USD 5.64 billion by 2031 at a 3.11% CAGR.

Which ink type holds the biggest share today?

Oil-based lithographic inks led with 41.12% of 2025 volume thanks to their entrenched role on sheetfed offset presses.

What is the fastest-growing ink category?

The Other Types cluster, electron-beam, screen, and conductive formulations, is projected to expand at 5.11% CAGR through 2031.

Why are UV LED inks gaining traction?

They cure at low temperatures, eliminate photoinitiator migration, cut energy use up to 70%, and comply with food-contact rules.

How do Buy American rules affect ink sourcing?

Federal thresholds rising to 55% domestic content in 2026 and 75% by 2030 are pushing formulators to localize pigment and resin supply chains.

Page last updated on: