Chemical Indicator Inks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 89.74 Million |

| Market Size (2031) | USD 131.44 Million |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

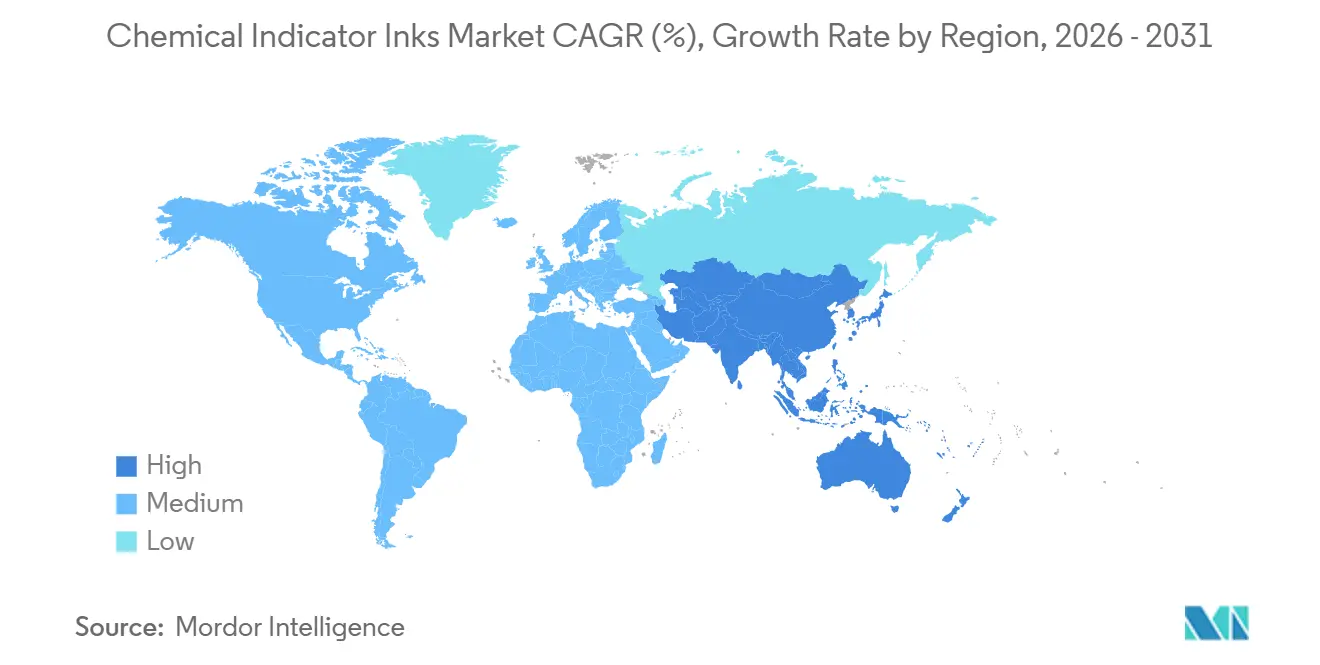

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

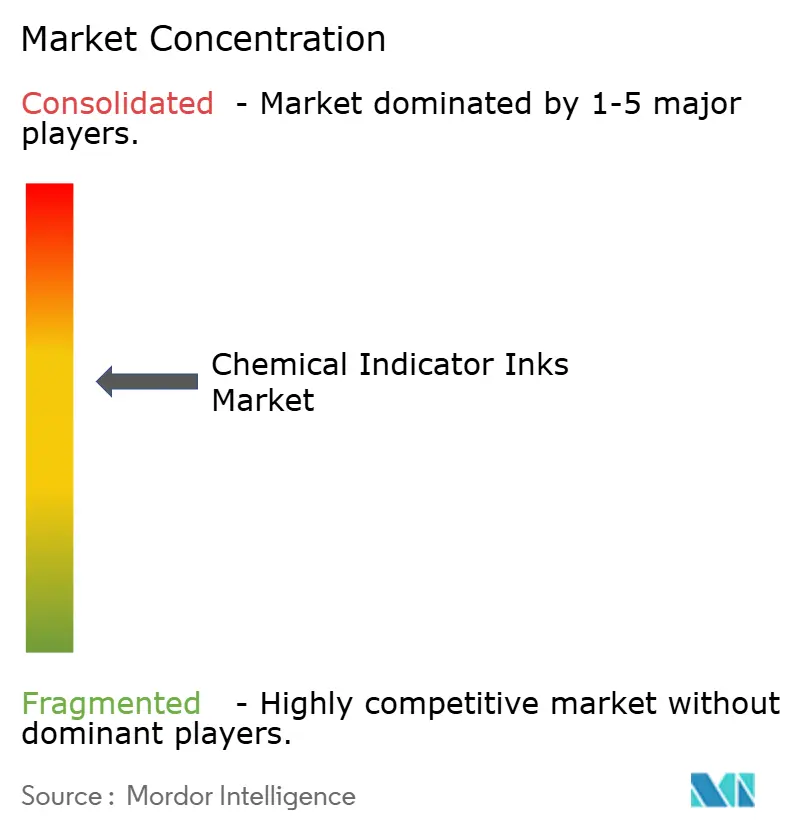

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chemical Indicator Inks Market Analysis by Mordor Intelligence

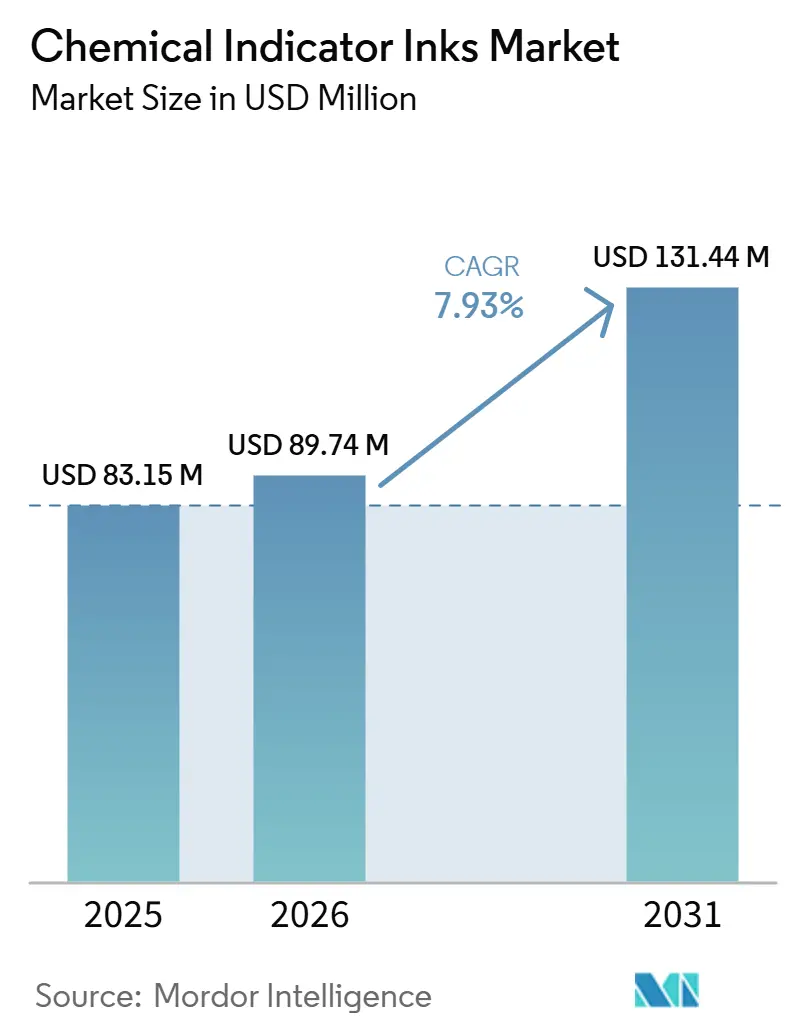

The Chemical Indicator Inks Market size was valued at USD 83.15 million in 2025 and is estimated to grow from USD 89.74 million in 2026 to reach USD 131.44 million by 2031, at a CAGR of 7.93% during the forecast period (2026-2031). As global regulators tighten validation rules, hospitals, pharmaceutical manufacturers, and contract sterilizers are transitioning from visual-only checks to multi-parameter chemical indicators. Water-based formulations continue to dominate production volumes due to their compatibility with existing flexographic lines and compliance with volatile organic compound (VOC) limits. However, UV-curable systems are capturing new capacities as converters aim for faster curing times and lower energy costs. Demand is further supported by radio-frequency identification (RFID)-integrated smart labels. These labels combine color-change chemistry with asset-tracking tags, creating additional revenue opportunities for inks capable of embedding memory chips without compromising sterility. At the same time, pigment-supply constraints and sustainability mandates are driving suppliers to secure long-term contracts with compliant pigment manufacturers, enhance backward integration, or accelerate the adoption of low-carbon chemistries. This approach also helps avoid the European Union’s 12% Carbon Border Adjustment tariff on non-low-carbon inks.

Key Report Takeaways

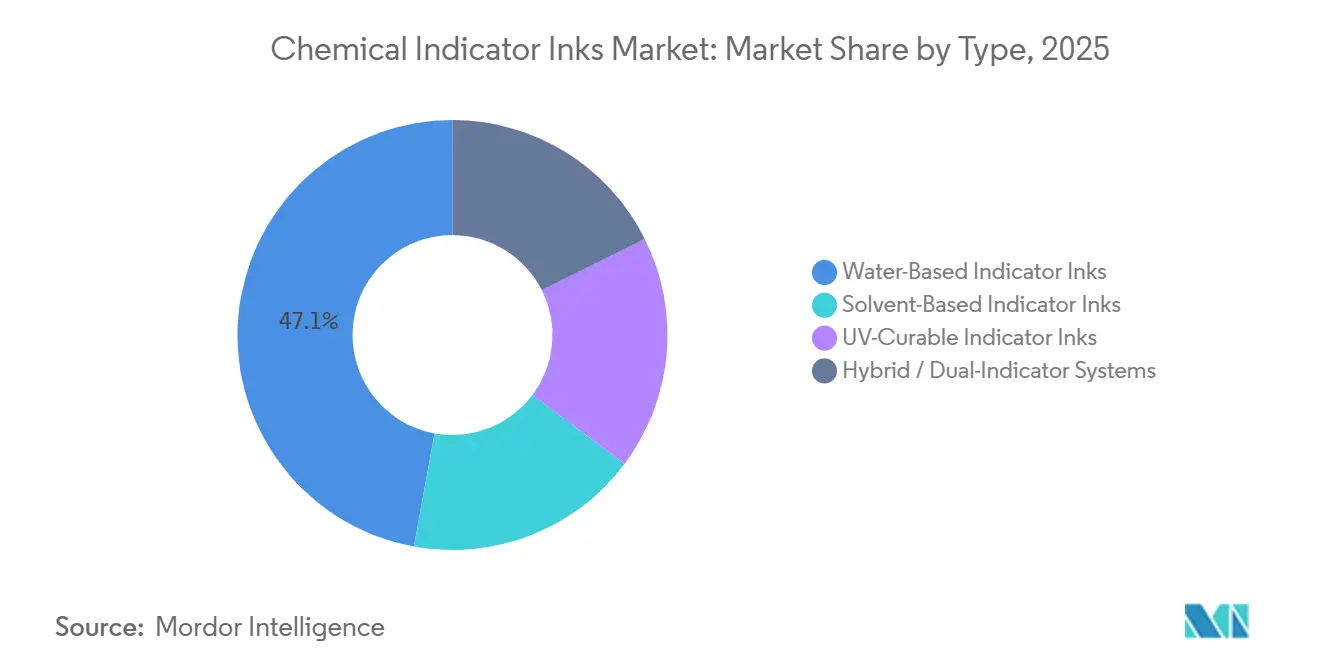

- By type, water-based indicator inks held 47.12% of the chemical indicator inks market share in 2025, while UV-curable indicator inks are advancing at an 8.36% CAGR through 2031.

- By process type, steam sterilization indicators led with 36.98% revenue share in 2025; plasma/H₂O₂ Gas Sterilization Indicators are the fastest-growing segment at an 8.14% CAGR to 2031.

- By application, packaging products such as pouches, wraps, and tapes commanded 43.11% of the chemical indicator inks market size in 2025, whereas labels and tags are projected to expand at an 8.78% CAGR to 2031.

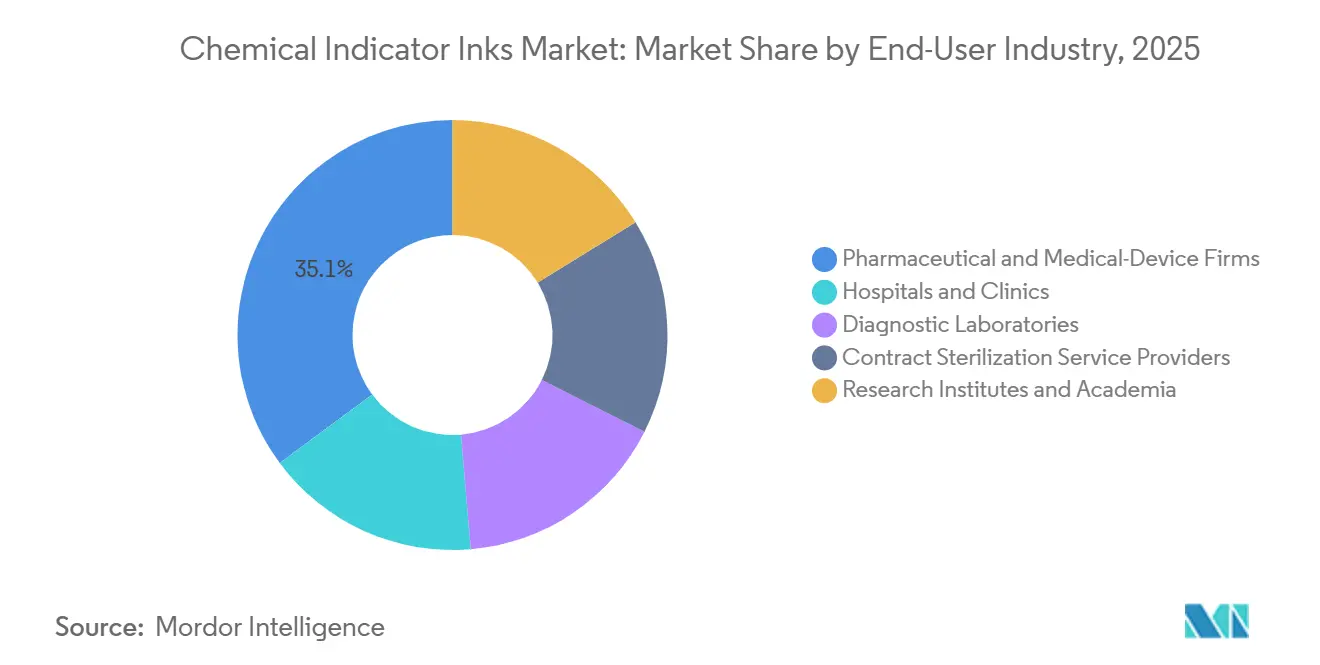

- By end user, pharmaceutical and medical-device companies captured 35.14% revenue share in 2025, and contract sterilization service providers exhibit the highest projected growth at an 8.11% CAGR to 2031.

- By geography, North America dominated with 37.88% revenue share in 2025; Asia-Pacific is advancing at the fastest 8.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chemical Indicator Inks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased awareness about infection-control regulations | +1.8% | Global, with peak intensity in North America & EU | Medium term (2-4 years) |

| Rising surgical and outpatient procedure volumes | +2.1% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Stricter validation norms in pharma and med-device manufacturing | +1.6% | North America, EU, APAC core markets | Long term (≥ 4 years) |

| RFID-integrated smart indicator labels for asset tracking | +0.9% | North America & EU early adopters, spill-over to APAC | Medium term (2-4 years) |

| Rapid adoption of on-pack smart inks for cold-chain biologics | +1.2% | Global, concentrated in pharma hubs (US, EU, India, China) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased Awareness About Infection-Control Regulations

Regulators now recommend the use of multi-parameter Type 4 indicators instead of single-parameter strips, addressing a compliance gap. In March 2025, the U.S. Food and Drug Administration (FDA) recognition of ANSI/AAMI ST58:2024 requires U.S. hospitals to document each sterilization cycle with a traceable chemical indicator that verifies time, temperature, and sterilant concentration[1]U.S. Food and Drug Administration, “Recognized Consensus Standards –Sterilization and Reprocessing,” FDA.gov . Updates from the Joint Commission in July 2024 and July 2025 incorporate these requirements into accreditation audits, necessitating product upgrades. Canada's GUI-0074 and Europe's EN 556-1:2024 align regional regulations with ISO 11140, expanding the number of compliant facilities. These regulatory changes drive the growth of the chemical indicator inks market by making advanced chromogenic systems a necessary business investment.

Rising Surgical and Outpatient Procedure Volumes

Ambulatory and robotic-assisted surgeries are growing faster than inpatient procedures, driving the need for low-temperature sterilizers that cannot rely solely on steam indicators. In 2025, Intuitive Surgical reported approximately 3.15 million da Vinci procedures, reflecting an 18% year-over-year increase, with expectations of double-digit growth in 2026. The United States Centers for Medicare and Medicaid Services (CMS) introduced 573 new outpatient codes for 2026, distributing sterilization workloads across numerous smaller centers that often lack centralized sterile-processing departments[2]Centers for Medicare & Medicaid Services, “CY 2026 Outpatient Prospective Payment System Final Rule,” cms.gov . Each new site is required to stock validated indicators, ensuring consistent demand for suppliers and increasing the market potential for chemical indicator inks.

Stricter Validation Norms in Pharma and Med-Device Manufacturing

In January 2024, the Food and Drug Administration (FDA) mandated that 510(k) applicants validate their processes using ISO-11140-compliant indicators. This requirement effectively excludes legacy Class 1 strips from new filings. Simultaneously, major pharmaceutical companies are investing significant amounts in new biologics and active pharmaceutical ingredient (API) plants. For instance, Novartis is allocating USD 23 billion from 2025 to 2030, while AbbVie has committed USD 380 million for 2026. Both companies are designing their facilities around multi-parameter chemical indicators integrated into batch records. With long construction timelines, these investments ensure a sustained demand for consumables, driving consistent growth in the chemical indicator inks market.

RFID-Integrated Smart Indicator Labels for Asset Tracking

The integration of Radio-Frequency Identification (RFID) tags with chromogenic inks is transforming compliance documentation. Getinge’s Poladus 150 VH₂O₂ sterilizer, equipped with an RFID reader, scans indicator labels, uploads cycle data to FleetView software, and identifies out-of-spec loads without requiring manual checks. Xerafy and GA International have introduced autoclave-resistant RFID tags that withstand over 600 steam cycles. This advancement enables the pairing of reusable trays with disposable color-change strips. As tag prices decrease to below USD 0.50, hospitals in the Asia-Pacific region are anticipated to adopt this technology, driving growth in the chemical indicator inks market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited market awareness in low-income regions | -0.7% | Sub-Saharan Africa, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Volatile supply of specialty chromogenic pigments | -1.1% | Global, acute in EU and North America | Short term (≤ 2 years) |

| Sustainability pressure on solvent-based ink carriers | -0.9% | EU, North America, with spillover to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Market Awareness in Low-Income Regions

Surgical-site infection rates in sub-Saharan Africa are 11.8%, compared to 1.9% in high-income countries. Many medical facilities in these regions, constrained by financial limitations, rely on basic Class 1 strips that monitor only a single variable instead of using multi-parameter indicators. Donor programs often fund sterilizers but exclude consumables, leaving technicians without the necessary tools to validate sterilization cycles. Additionally, a significant portion of staff lacks formal training in interpreting International Organization for Standardization (ISO)-compliant indicators. Without the inclusion of chemical-indicator funding in procurement guidelines by multilateral agencies, the adoption of these indicators is expected to remain inconsistent. This inconsistency could impact the growth potential of the chemical indicator inks market in these regions.

Volatile Supply of Specialty Chromogenic Pigments

Following Heubach's insolvency and Sudarshan Chemical's acquisition in October 2024, the pigment supply became constrained, consolidating two major producers into one entity. In January 2025, the European Union (EU) implemented anti-dumping duties on Chinese titanium dioxide, increasing input costs. Concurrently, the United States Environmental Protection Agency's (U.S. EPA) ongoing review of Pigment Violet 29 introduces regulatory uncertainty. Smaller ink manufacturers without long-term contracts face cost increases and delivery delays, impacting revenue and raising entry barriers in the chemical indicator inks market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Water-Based Formulations Dominate, UV-Curable Systems Gain on Energy Economics

In 2025, water-based formulations accounted for 47.12% of the type segment, reflecting their compatibility with modern presses and compliance with volatile organic compound (VOC) limits outlined in China's 14th Five-Year Plan. As hospitals and medical device companies increasingly align their purchases with corporate net-zero objectives, the market for water-based chemical indicator inks is expected to grow steadily. Suppliers such as Fujifilm, with its AQUAFUZE hybrid water-based ultraviolet (UV) line, and Sun Chemical, with its bio-renewable SunCure Advance ECO, are improving performance while reducing carbon footprints.

Among the type segments, UV-curable systems are growing at a compound annual growth rate (CAGR) of 8.36%, the fastest in the market. This growth is driven by instant curing technology, which reduces energy costs by up to 60% and increases throughput for contract sterilizers handling high-volume labels. The industry is seeing increased adoption, with companies like Mimaki introducing Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH)-compliant ELH inks and StarColor offering low-migration flexographic (flexo) sets, both gaining traction in pharmaceutical packaging. Additionally, suppliers proficient in developing dual-indicator chemistries, combining sterilization proof with cold-chain time-temperature response, can access premium market segments and support the growth of the chemical indicator inks market.

By Process Type: Steam Holds Installed Base, Plasma and VH₂O₂ Capture Innovation Spend

In 2025, steam indicators accounted for 36.98% of the process-type revenue, primarily driven by the extensive use of hospital autoclaves worldwide. The updated ANSI (American National Standards Institute)/AAMI (Association for the Advancement of Medical Instrumentation) ST58:2024 standard requires Type 4 internal monitors, leading to increased replacement sales and supporting steam's market share.

Plasma and vaporized hydrogen peroxide indicators are projected to grow at a CAGR (Compound Annual Growth Rate) of 8.14%. This growth is attributed to advancements in robotics, the adoption of heat-sensitive implants, and the FDA's (Food and Drug Administration) 2024 Category A reclassification, which simplified validation processes. Getinge’s Poladus 150 bundle and Mesa Labs’ ExpoSure kits illustrate equipment-consumable ecosystems designed to retain customers through proprietary inks, contributing to the chemical indicator inks market share held by leading technology providers.

By Application: Packaging Leads Volume, Labels and Tags Capture Smart-Indicator Premium

In 2025, packaging bags, wraps, and tapes accounted for 43.11% of the application revenue. High-volume sterile pouches primarily used cost-effective water-based inks; however, the shift in substrate to all-plastic Tyvek required reformulation for polyethylene surfaces.

Labels and tags, despite their smaller tons, are advancing at a Compound Annual Growth Rate (CAGR) of 8.78%. Radio-Frequency Identification (RFID)-enabled smart labels now combine color-change chemistry with electronic serialization, achieving higher market prices. Additionally, the market for chemical indicator inks associated with smart labels is projected to surpass commodity packaging as adopters transition from pilot trials to enterprise-level implementations.

By End-User Industry: Pharma and Device Firms Lead Spend, Contract Sterilizers Drive Volume Growth

In 2025, pharmaceutical and medical-device manufacturers accounted for 35.14% of the revenue share. Companies such as Novartis, AbbVie, and Novo Nordisk are incorporating sterilization validation into every filling line and isolator through their multi-billion-dollar greenfield projects, ensuring the consumption of multi-parameter indicators for years to come.

Contract sterilization providers are projected to grow at a compound annual growth rate (CAGR) of 8.11% through 2031, marking the fastest growth among end users. The outsourcing trend by original equipment manufacturers (OEMs) has increased indicator demand, benefiting companies like STERIS and Sterigenics. These firms specify validated inks in client agreements, creating consistent demand for suppliers in the chemical indicator inks market.

Geography Analysis

In 2025, North America accounted for 37.88% of the revenue. The adoption of ANSI/AAMI ST58:2024 (American National Standards Institute/Association for the Advancement of Medical Instrumentation) by hospitals in the United States, along with significant capital expenditures in the pharmaceutical industry, supported demand. Additionally, the Centers for Medicare & Medicaid Services (CMS) expanded reimbursement for outpatient procedures, increasing the customer base. RFID (Radio-Frequency Identification) trials are progressing from university hospitals to major Integrated Delivery Networks (IDNs), enhancing the market presence of chemical indicator inks.

Europe follows, driven by EU MDR (European Union Medical Device Regulation) audits, the harmonization of EN 556:2024, and the implementation of a 12% Carbon Border Adjustment tariff, which supports water-based and UV (ultraviolet) sets. Rising pigment costs due to duties on titanium dioxide (TiO₂) are prompting converters to pursue long-term supply agreements or backward integration, reshaping the competitive landscape.

Asia-Pacific is the fastest-growing region, with an 8.32% CAGR (Compound Annual Growth Rate) projected through 2031. India's plan to add 2 million hospital beds by 2030 and China's 30% reduction mandate on volatile organic compounds (VOCs) are driving both volume growth and technology shifts. Private-equity investments in Asian Contract Development and Manufacturing Organizations (CDMOs) and hospitals are further increasing demand for validated indicators, accelerating the market expansion for chemical indicator inks.

Competitive Landscape

The chemical indicator inks market is moderately concentrated. Top suppliers such as 3M, STERIS, Getinge AB, Crosstex International, Inc., and Terragene collectively account for 55-60% of global revenue, indicating moderate market concentration. Getinge's bundled offerings of sterilizers and consumables, STERIS's 9.6% organic revenue growth in Fiscal Year (FY) 2025, and Ecolab's USD 828 million contribution from its Healthcare segment reflect a strategic shift from price competition to ecosystem-based approaches. Regional players, including Inkmaker SRL and NiGK Corporation, achieve success through customized shades and effective navigation of local regulations. Additionally, companies such as Xerafy, GA International, and SEIKO Tags, focusing on Radio Frequency Identification (RFID)-integrated labels, and Fujifilm and Sun Chemical, with their UV-curable bio-based chemistries, are gradually capturing market share from established players, particularly in regions where sustainability mandates are driving faster technological adoption. Larger firms, leveraging vertical pigment integration and strategic stockpiling, are better positioned to mitigate supply risks, a significant advantage amid ongoing pigment volatility, which smaller converters may find challenging to manage.

Chemical Indicator Inks Industry Leaders

3M

Getinge AB

STERIS

Terragene

Crosstex International, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AbbVie plans to invest USD 380 million to expand its Active Pharmaceutical Ingredient (API) production capacity in North Chicago, with operations expected to begin in 2029. This expansion aligns with the growing demand for APIs, which are critical components in the production of pharmaceuticals, including applications in Chemical Indicator Inks used for sterilization monitoring and other healthcare processes.

- April 2025: Novartis announced a USD 23 billion plan to establish seven manufacturing plants in the United States from 2025 to 2030. The initiative includes the integration of multi-parameter indicator validation, a critical component in chemical indicator inks, across all new production lines. Chemical indicator inks are essential in monitoring sterilization processes, ensuring compliance with stringent quality standards in manufacturing.

Global Chemical Indicator Inks Market Report Scope

Chemical indicator inks are color-changing inks that provide visual confirmation of exposure to sterilization processes, such as steam, ethylene oxide (EtO), or irradiation. These inks undergo an irreversible chemical reaction due to heat, pressure, or chemical exposure, changing color to verify that a medical device, for example, has been processed.

The chemical indicator inks market is segmented by type, process, application, end-user industry, and geography. By type, the market is segmented into water-based indicator inks, solvent-based indicator inks, uv-curable indicator inks, hybrid / dual-indicator systemswater-based indicator inks, solvent-based indicator inks, uv-curable indicator inks, and hybrid/dual-indicator systems. By process, the market is segmented into steam sterilization indicators, ethylene oxide (EO) sterilization indicators, dry-heat sterilization indicators, plasma/h₂o₂ gas sterilization indicators, radiation (gamma / e-beam) indicators, and formaldehyde sterilization indicators. By application, the market is segmented into packaging (bags, wraps, tapes), labels and tags, and test strips and pouches. By end-use industry, the market is segmented into hospitals and clinics, pharmaceutical and medical-device firms, diagnostic laboratories, contract sterilization service providers, and research institutes and academia. The report also covers the market size and forecasts for chemical indicator inks in 15 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Water-Based Indicator Inks |

| Solvent-Based Indicator Inks |

| UV-Curable Indicator Inks |

| Hybrid / Dual-Indicator Systems |

| Steam Sterilization Indicators |

| Ethylene Oxide (EO) Sterilization Indicators |

| Dry-Heat Sterilization Indicators |

| Plasma / H₂O₂ Gas Sterilization Indicators |

| Radiation (Gamma / E-Beam) Indicators |

| Formaldehyde Sterilization Indicators |

| Packaging (Bags, Wraps, Tapes) |

| Labels and Tags |

| Test Strips and Pouches |

| Hospitals and Clinics |

| Pharmaceutical and Medical-Device Firms |

| Diagnostic Laboratories |

| Contract Sterilization Service Providers |

| Research Institutes and Academia |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Water-Based Indicator Inks | |

| Solvent-Based Indicator Inks | ||

| UV-Curable Indicator Inks | ||

| Hybrid / Dual-Indicator Systems | ||

| By Process Type | Steam Sterilization Indicators | |

| Ethylene Oxide (EO) Sterilization Indicators | ||

| Dry-Heat Sterilization Indicators | ||

| Plasma / H₂O₂ Gas Sterilization Indicators | ||

| Radiation (Gamma / E-Beam) Indicators | ||

| Formaldehyde Sterilization Indicators | ||

| By Application | Packaging (Bags, Wraps, Tapes) | |

| Labels and Tags | ||

| Test Strips and Pouches | ||

| By End-user Industry | Hospitals and Clinics | |

| Pharmaceutical and Medical-Device Firms | ||

| Diagnostic Laboratories | ||

| Contract Sterilization Service Providers | ||

| Research Institutes and Academia | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Chemical Indicator Inks Market?

The Chemical Indicator Inks Market size was valued at USD 83.15 million in 2025 and is estimated to grow from USD 89.74 million in 2026 to reach USD 131.44 million by 2031, at a CAGR of 7.93% during the forecast period (2026-2031).

Which formulation type is gaining the most share from sustainability mandates?

UV-curable systems are expanding at an 8.36% CAGR because instant curing reduces energy use and avoids VOC emissions targeted by new EU and China rules.

Why are RFID-enabled indicator labels attracting investment?

They merge sterilization verification with asset tracking, automate record-keeping, and cut labor costs, driving premium pricing in hospitals and contract sterilizers.

What limits adoption of advanced indicators in low-income regions?

Budget constraints, training gaps, and donor focus on equipment over consumables keep many facilities dependent on single-parameter strips.

Page last updated on: