Digital Inks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

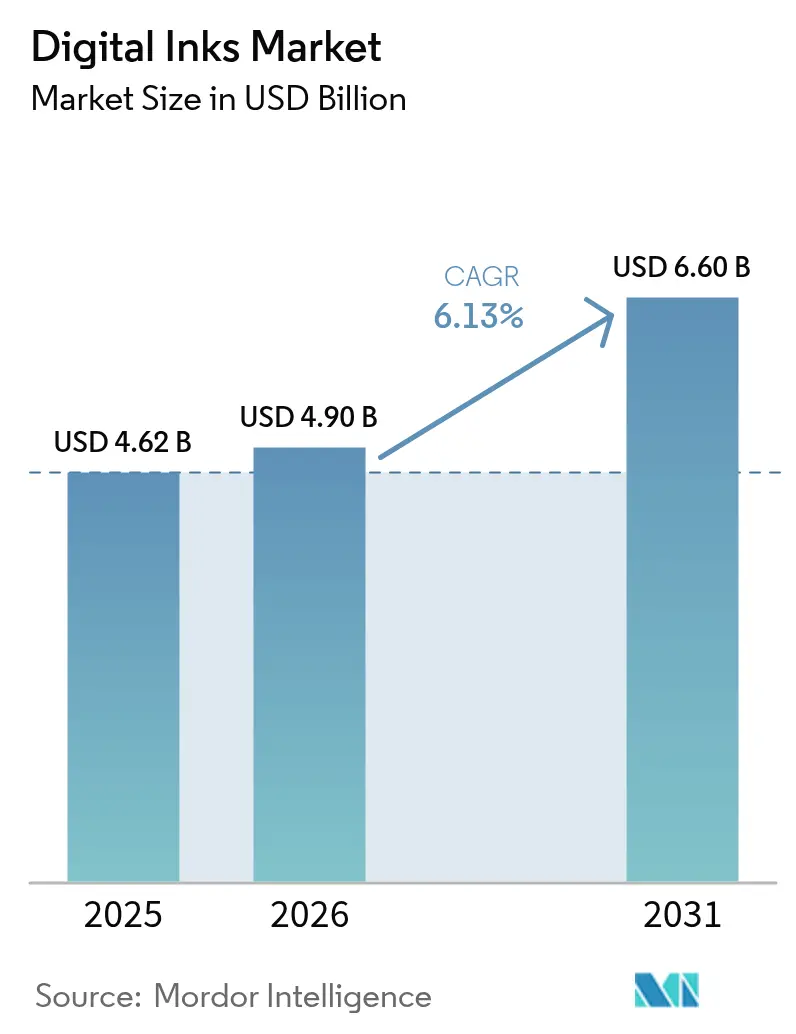

| Market Size (2026) | USD 4.9 Billion |

| Market Size (2031) | USD 6.6 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

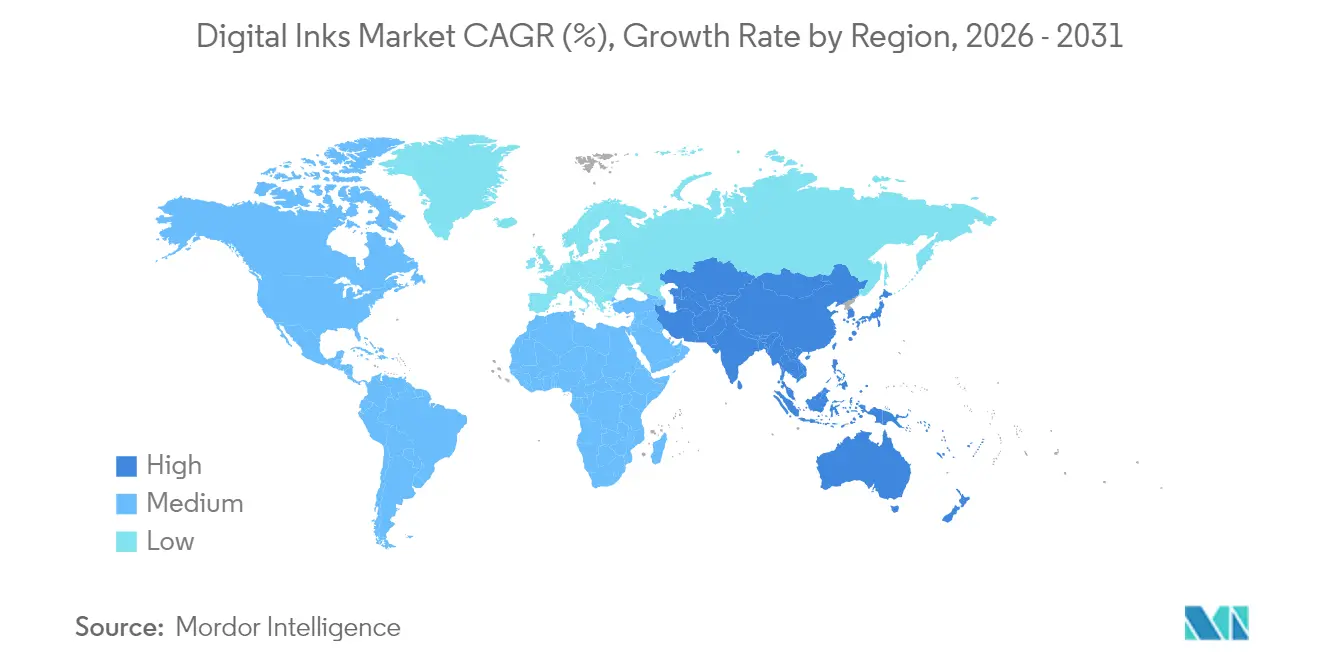

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Inks Market Analysis by Mordor Intelligence

Digital Inks market size in 2026 is estimated at USD 4.9 billion, growing from 2025 value of USD 4.62 billion with 2031 projections showing USD 6.6 billion, growing at 6.13% CAGR over 2026-2031. This sustained expansion reflects the rapid shift from analog to digital printing workflows that favor on-demand customization, resource efficiency, and compliance with tightening environmental regulations. Demand growth gathers pace around UV-curable formulations that cure instantly, nano-scale conductive materials that enable printed electronics, and substrate-specific adhesion chemistries that open new industrial use-cases. Continuous gains in printhead precision, fluid viscosity control, and inline quality inspection create productivity benefits that validate capital spending on next-generation presses. Simultaneously, stricter global standards on volatile organic compound (VOC) emissions accelerate the pivot toward low-solvent or solvent-free ink chemistries, reinforcing technological differentiation among suppliers. Applications such as packaging, textiles, and flexible electronics translate these technical improvements into shorter production runs, rapid design iteration, and lower inventories, strengthening the overall digital inks market trajectory.

Key Report Takeaways

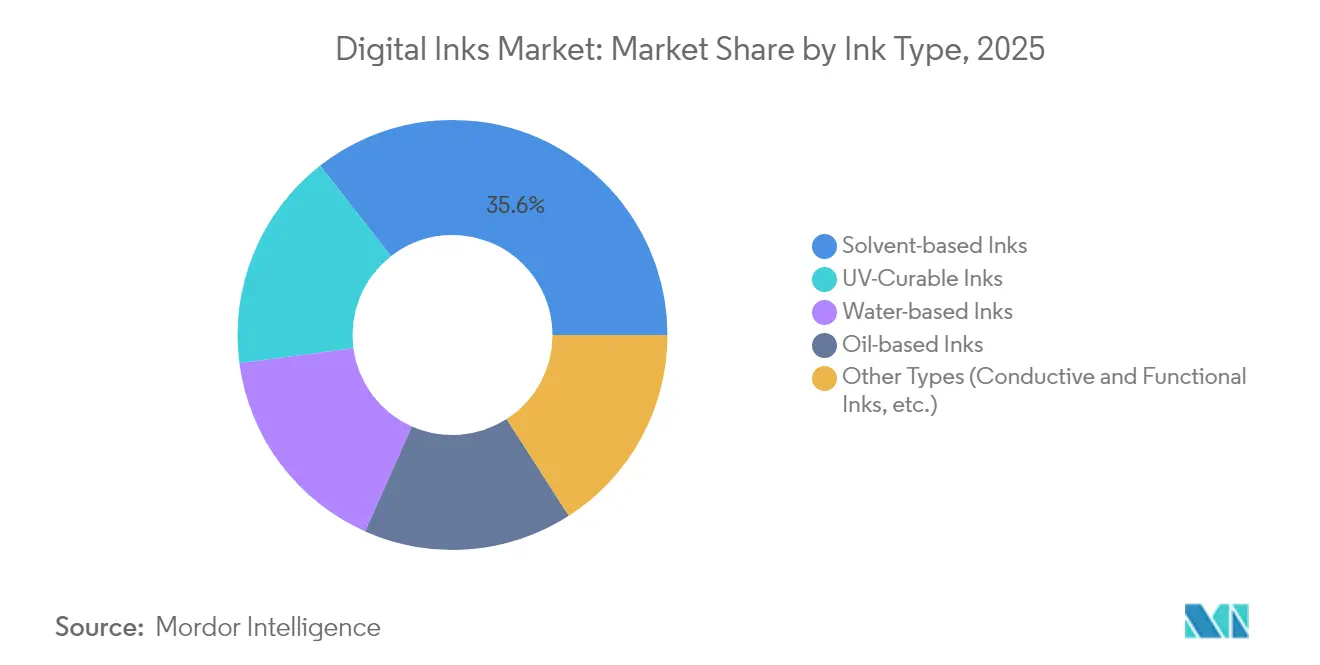

- By ink type, solvent-based systems retained 35.55% of the digital inks market share in 2025, whereas UV-curable inks are forecast to expand at a 6.86% CAGR through 2031.

- By printing technology, drop-on-demand inkjet held 54.60% share of the digital inks market size in 2025, while continuous inkjet is projected to log a 7.18% CAGR between 2026 and 2031.

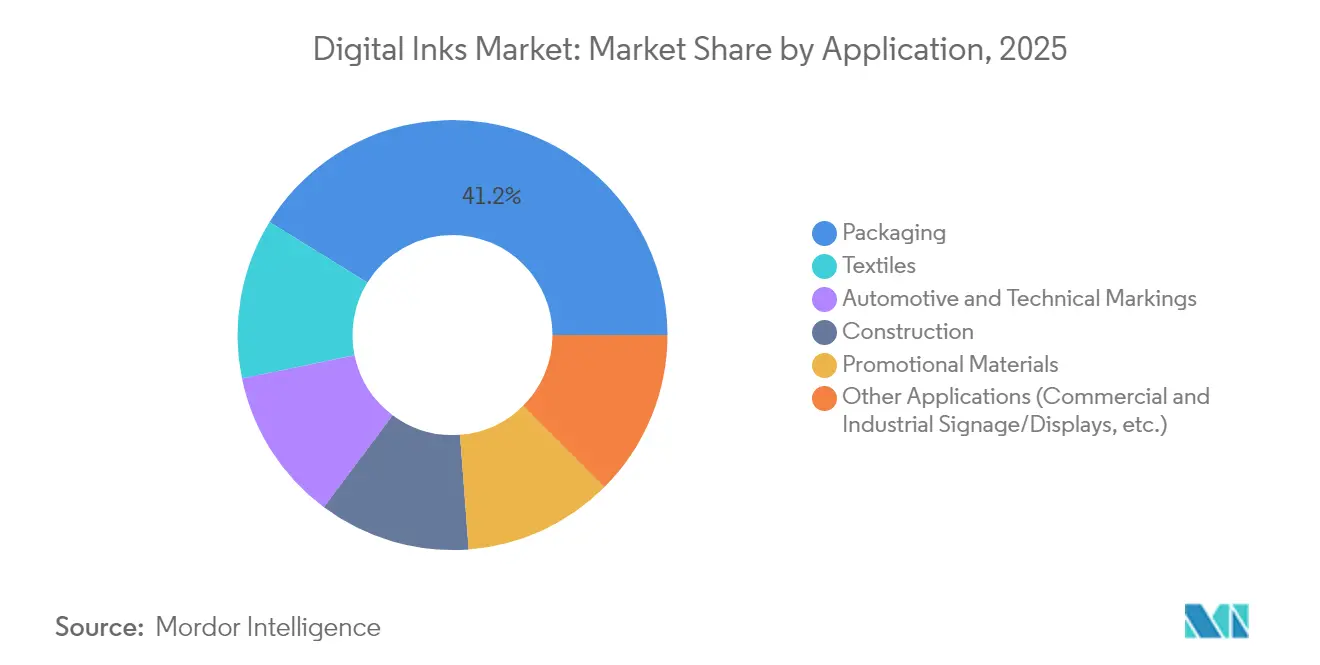

- By application, packaging captured 41.20% revenue share in 2025; while other applications represent the fastest growing segment with a 7.22% CAGR to 2031.

- By geography, Asia-Pacific led with 48.10% of the digital inks market share in 2025 and is advancing at a 6.95% CAGR through the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Inks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Demand for UV-Curable Inks in Packaging and Signage | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rapid Adoption of Inkjet Printing for Textile Digitalization | +1.8% | APAC core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Rising Uptake of Eco-Solvent Inks on Sustainability Grounds | +0.9% | Europe leading, followed by North America | Short term (≤ 2 years) |

| Emergence of Conductive Nano-Inks for Flexible Electronics | +0.7% | APAC manufacturing hubs, R&D in North America | Long term (≥ 4 years) |

| Expansion of E‑Commerce and On‑Demand Packaging | +1.1% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for UV-Curable Inks in Packaging and Signage

Instant polymerization under ultraviolet light eliminates drying bottlenecks, enabling higher throughput and energy savings compared with solvent systems. Minimal VOC emissions make UV-curable inks an effective route to regulatory compliance, and producers such as DuPont have commercialized water-based pigment series that meet food-contact norms without sacrificing color density[1]DuPont, “Artistri PN1000 Water-Based Inkjet Inks,” dupont.com. Packaging converters value the ability to decorate glass, metal, and multilayer polymer films while maintaining barrier integrity, whereas outdoor signage installers rely on the inks’ superior weather fastness and color retention. Accelerated adoption is further supported by lower maintenance costs and the growing availability of mid-radiant LED curing modules that reduce press heat loads. These combined benefits place UV-curable systems on a steady adoption path across both developed and emerging printing hubs.

Rapid Adoption of Inkjet Printing for Textile Digitalization

Digital inkjet technology replaces water-intensive dyeing lines with precision deposition that cuts water use by up to 95% on certain cotton and polyester substrates. Equipment makers such as Kyocera and Epson have scaled print bars capable of 2 m web widths, allowing roll-to-roll fabric printing at industrial speeds. Capacity expansions, including Epson’s new Akita and Tohoku facilities, signal confidence in long-run demand linked to fashion mass customization. Artificial intelligence embedded in RIP software accelerates workflow setup and enables algorithmic pattern generation, trimming design-to-sample cycles. Buyers gain smaller minimum-order quantities and serialized garment identification, benefits that reinforce sourcing shifts toward on-shore or near-shore micro-factories.

Rising Uptake of Eco-Solvent Inks on Sustainability Grounds

Revisions to the United States National Volatile Organic Compound Emission Standards announced in January 2025 push converters toward lower-reactivity solvents, while the European Union’s Green Deal accelerates phase-outs of mineral-based carriers. German and French legislation frame strict reporting thresholds that effectively force substitution to plant-derived alternatives with comparable dry-time and rub resistance. Suppliers such as INX International actively market natural-origin solvents and reclaimed material content to capture early-compliance premiums. Improved odor profiles and indoor-air quality performance broaden the addressable market into interior décor and wallpaper, further extending the eco-solvent growth runway.

Emergence of Conductive Nano-Inks for Flexible Electronics

Silver nanoparticle, graphene, and carbon-nanotube formulations enable printed traces that retain conductivity under repeated bending, unlocking sensor-rich wearables and intelligent packaging. Academic breakthroughs, such as Seoul National University’s laser lift-off process that cuts carbon residue by 92.8%, reduce defect rates in ultrathin circuitry. The printed sensor sub-market is valued at USD 12.1 billion in 2025 and is projected to reach USD 16.84 billion by 2030, providing a sizeable opportunity for ink makers that master dispersion stability and low-temperature sintering. Consumer-electronics OEMs increasingly specify ink-based antennas and force-sensing resistors, paving a path for high-margin specialty grades within the broader digital inks market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Pigment and Raw-Material Prices | -0.8% | Global, with highest impact in price-sensitive markets | Short term (≤ 2 years) |

| Stringent Global VOC-Emission Regulations on Solvent Inks | -0.6% | Europe and North America leading, expanding globally | Medium term (2-4 years) |

| Durability Issues on Polyester and Blended Substrates | -0.4% | APAC textile manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Pigment and Raw-Material Prices

Titanium dioxide and specialty organic pigments account for a high proportion of ink-making costs, and price swings driven by tariffs on Chinese and Mexican imports compress profit margins throughout the value chain. Specialty chemicals suppliers face geopolitical disruptions that ripple into inconsistent lead times and hedging difficulties, compelling ink formulators to consider dual-sourcing and index-linked contracts. Print service providers (PSPs) add cost surcharges or adopt lighter coverage designs to protect margins, though these tactics face resistance in price-sensitive advertising and textile segments. Working-capital intensity rises as firms hold safety stock to buffer uncertainty, raising barriers for smaller market entrants.

Stringent Global VOC-Emission Regulations on Solvent Inks

North American states such as Washington are proposing outright bans on specific solvent-based formulations, while Europe advances the Circular Economy Action Plan that elevates consumer-safety thresholds on potential carcinogens. Material registries under the Toxic Substances Control Act introduce additional paperwork and pre-notification cycles that stretch time-to-market. India’s toluene prohibition for food-contact inks and China’s GB 4806.14-2023 framework echo similar constraints in Asia, underscoring the global scope of compliance pressure. Investments in solvent-free pilot lines and analytical validation labs temper smaller firms’ competitiveness, reinforcing market consolidation tendencies in the digital inks market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ink Type: Solvent Systems Face Regulatory Headwinds

Solvent-based inks commanded 35.55% of 2025 revenue, yet the digital inks market size attached to UV-curable grades is forecast to outpace at a 6.86% CAGR through 2031. Performance advantages include on-press curing within seconds and negligible VOC content, which align with packaging converters’ push for leaner workflows and food-safety assurance. Water-based pigments accelerate in label and flexible-pouch formats as low-odor characteristics allow presses to run inside populated production halls without extraction upgrades. Niche oil-based systems remain relevant for thermoplastic substrates that demand elevated film-forming temperatures and lubricant functionality, though volume prospects stay limited.

A separate opportunity unfolds in conductive and other functional inks, where graphene-rich formulations achieve conductivities approaching 7.3 × 10⁵ S/m while retaining 800% stretchability, making them attractive for medical patches and bendable circuitry. European directives phasing out mineral oils amplify strategic urgency for greener alternatives, prompting suppliers to test bio-sourced diluents that match drying speeds and color vibrancy. As compliance deadlines tighten, solvent lines risk market share attrition, whereas UV-curable and water-based chemistries advance toward mainstream status inside the digital inks market.

By Printing Technology: Drop-on-Demand Dominance Faces CIJ Challenge

Drop-on-demand (DOD) architecture held 54.60% share in 2025 and continues to define the digital inks market through nozzle refinement that yields native 2-picolitre droplets and resolutions surpassing 1,200 dpi. Reliability improvements such as recirculating head manifolds cut downtime and support low-viscosity aqueous chemistries, broadening addressable substrates from uncoated paper to rigid plastics. Continuous inkjet (CIJ) systems, historically rooted in coding and marking, now integrate dual-frequency deflection to print variable data at line speeds above 400 m/min, giving the segment a projected 7.18% CAGR. UV inkjet bridges high-opacity white under-printing on metals and glass, thereby encroaching on screen-printing share in industrial décor.

Recent investments underline future momentum. Epson’s 5.1 billion-yen Tohoku facility, scheduled to come online by September 2025, will quadruple annual PrecisionCore printhead output, ensuring secure supply for expanding OEM partnerships. Hybrid platforms that marry flexographic priming stations with inline inkjet modules cater to converters balancing cost-per-square-meter efficiency and SKU proliferation. Collectively these dynamics ensure printing-technology innovation remains a decisive factor in sustaining the digital inks market expansion.

By Application: Packaging Dominance Amid Textile Acceleration

Packaging accounted for 41.20% of 2025 consumption thanks to e-commerce fulfillment models and brand mandates for serialized anti-counterfeiting codes. Variable-data capabilities lower plate costs, making digital attractive for run lengths below 10,000-linear-meters in corrugated and folding carton formats. Automotive and aerospace markets specify high-temperature-resistant inks for under-hood and cabin trim, yet remain niche by volume. Construction material branding requires UV-stable pigments for exterior cladding and vinyl siding.

The other applications segment—which spans commercial signage, industrial displays, décor panels, and emerging interactive surfaces—expanded at a 7.22% CAGR from 2025 and is projected to retain the fastest trajectory among all verticals through 2031, lifting its slice of the digital inks market size as converters shift short-run graphics from solvent screen presses to high-speed UV inkjet systems. Performance gains stem from ultra-adhesive formulations that bond to glass, metal, and polycarbonate without primers, enabling durable storefront graphics, transit wraps, and factory safety placards that weather UV exposure and chemical washdowns. Variable-data capabilities also allow quick revisions for seasonal promotions and regulatory signage, trimming waste and inventory.

Geography Analysis

Asia-Pacific controlled 48.10% of the digital inks market in 2025 and is projected to advance at 6.95% CAGR through 2031. China anchors regional momentum with expansive corrugated and electronics production, while Japan delivers high-precision components and growing installation bases for textile and industrial printers. India accelerates capacity investments, illustrated by DIC India’s INR 1.1 billion facility in Gujarat producing toluene-free liquid inks . South Korea and Taiwan leverage electronics manufacturing know-how to expand conductive ink adoption in display and sensor applications. ASEAN economies such as Vietnam benefit from garment export booms that trigger demand for low-water textile printing.

North America remains an innovation hub where regulatory leadership nudges rapid uptake of UV-curable and eco-solvent chemistries. The United States’ vibrant e-commerce sector stimulates on-demand packaging growth, fostering press installations around omnichannel fulfillment centers. Canada and Mexico supply resins and pigments but face tariff-driven cost variability, prompting contingency sourcing and localized blending strategies. INX International’s USD 1.6 billion annual sales underscore the region’s industrial depth and R&D commitment in the digital inks market

Europe shapes global standards through early adoption of circular-economy policies that mandate recyclable materials and low-toxicity formulas. Germany’s engineering heritage underpins equipment advances, while France channels policy instruments to eliminate mineral-oil-based inks in food packaging. Nordic innovation focuses on biodegradable binders derived from lignin and tall oil, aligning with forestry-rich economies. Italy reinforces leadership in fashion print applications, and the United Kingdom sustains strength in label and specialty graphics. Although Russia faces trade constraints, domestic demand persists for industrial marking inks, while Eastern Europe grows as a near-shore production base. South America and Middle East and Africa, though smaller by value, reveal double-digit local growth where infrastructure modernizes and foreign direct investment funds flexible packaging and textile print clusters.

Competitive Landscape

Digital ink manufacturing displays moderate concentration, with leading players pursuing vertical integration to secure pigment supply, formulate bespoke chemistries, and embed analytics across production lines. INX International exemplifies this strategy, channeling USD 68.5 million during 2024-2025 into AI analytics firm Oden Technologies and predictive-maintenance specialist AssetWatch to lift plant availability and cut changeover times by 71%[2]INX International, “Corporate Investment Highlights 2024-2025,” inxinternational.com . Technology-oriented entrants exploit white-space in conductive nano-inks, with E Ink unveiling low-power electrophoretic modules that function from –20 °C to 65 °C and target outdoor digital signage.

Mergers and acquisitions remain a lever for scale and portfolio breadth: Xerox’s USD 1.5 billion purchase of Lexmark repositions the combined entity among the top five print-solution providers while increasing exposure to the Asia-Pacific region. Patent depth grows in importance as companies license printhead architectures and rheology modifiers; Wacom’s library of 3,000+ filings offers defensible linkage between digital pen ecosystems and ink rende. Technology-oriented entrants exploit white-space in conductive nano-inks, with E Ink unveiling low-power electrophoretic modules that function from –20 °C to 65 °C and target outdoor digital signage

Pricing discipline tightens under raw-material inflation, pushing top suppliers to negotiate volume-based rebates with pigment makers and to rationalize SKUs toward high-margin specialty lines. Service models evolve toward subscription-based ink delivery, remote diagnostics, and color management expertise, creating annuity revenues beyond the initial press sale. Collectively, these maneuvers sustain moderate rivalry while yielding incremental consolidation within the digital inks market.

Digital Inks Industry Leaders

Sun Chemical (DIC Corporation)

FUJIFILM Speciality Ink Systems Limited

Siegwerk Druckfarben AG & Co. KGaA

Flint Group

INX International Ink Co

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: INX launched INXJet MDLM UV Curable Inkjet digital ink at Cannex Fillex for metal can printing. The ink is engineered for metal decorating applications and works with multiple printhead technologies.

- September 2024: DuPont introduced the Artistri PN1000 digital ink series at the PRINTING United Expo 2024. The water-based pigment inkjet ink features low viscosity for commercial printing applications. The ink series incorporates DuPont's proprietary technology and works with standard industry drying systems.

Global Digital Inks Market Report Scope

The digital ink market is segmented by type water-based inks, oil-based inks, solvent-based inks, UV curing inks, and other types. The market is segmented by application into automotive and technical markings, construction, packaging, promotional materials, textiles, and other applications. The report also covers the market size of and forecasts for the digital ink market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Solvent-based Inks |

| Water-based Inks |

| UV-Curable Inks |

| Oil-based Inks |

| Other Types (Conductive and Functional Inks, etc.) |

| Drop-on-Demand Inkjet |

| Continuous Inkjet (CIJ) |

| UV Inkjet |

| Digital Screen Printing |

| Other Technologies (Hybride inkjets, etc.) |

| Packaging |

| Automotive and Technical Markings |

| Construction |

| Promotional Materials |

| Textiles |

| Other Applications (Commercial and Industrial Signage/Displays, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Ink Type | Solvent-based Inks | |

| Water-based Inks | ||

| UV-Curable Inks | ||

| Oil-based Inks | ||

| Other Types (Conductive and Functional Inks, etc.) | ||

| By Printing Technology | Drop-on-Demand Inkjet | |

| Continuous Inkjet (CIJ) | ||

| UV Inkjet | ||

| Digital Screen Printing | ||

| Other Technologies (Hybride inkjets, etc.) | ||

| By Application | Packaging | |

| Automotive and Technical Markings | ||

| Construction | ||

| Promotional Materials | ||

| Textiles | ||

| Other Applications (Commercial and Industrial Signage/Displays, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the digital inks market?

The digital inks market size is valued at USD 4.9 billion in 2026, reflecting steady adoption across packaging, textiles, and industrial printing.

Which segment is growing fastest in the digital inks market?

UV-curable inks register the highest forecast growth at a 6.86% CAGR through 2031, propelled by instant curing and low-VOC benefits.

Why are conductive nano-inks important?

Conductive nano-inks enable printed electronics such as wearable sensors and smart packaging, creating a USD 2.31 billion sub-market opportunity by 2031.

How does regulation affect solvent-based inks?

Stricter VOC-emission standards in North America and Europe force suppliers to reformulate or shift to eco-solvent and water-based systems, reducing solvent ink share.

Which region leads the digital inks market?

Asia-Pacific holds 48.10% of market revenue thanks to manufacturing scale in China, precision engineering in Japan, and textile digitalization in India.

Page last updated on: