Knowledge Process Outsourcing (KPO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 104.47 Billion |

| Market Size (2031) | USD 246.77 Billion |

| Growth Rate (2026 - 2031) | 18.76% CAGR |

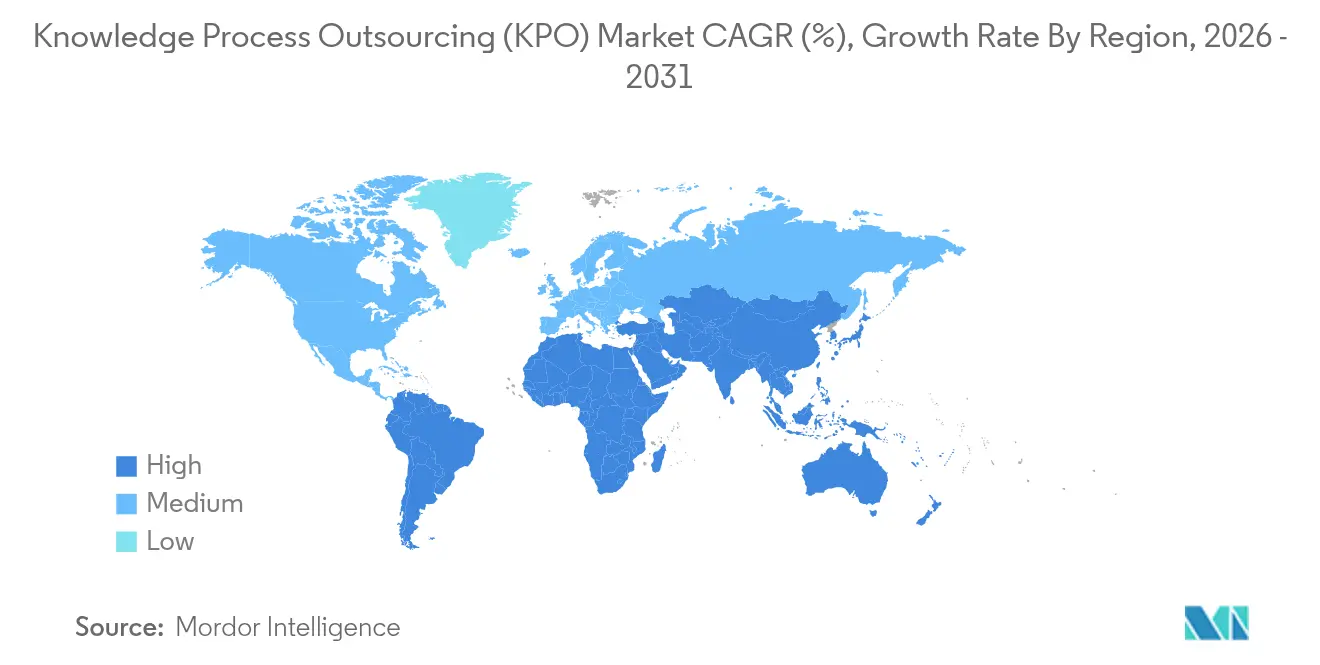

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

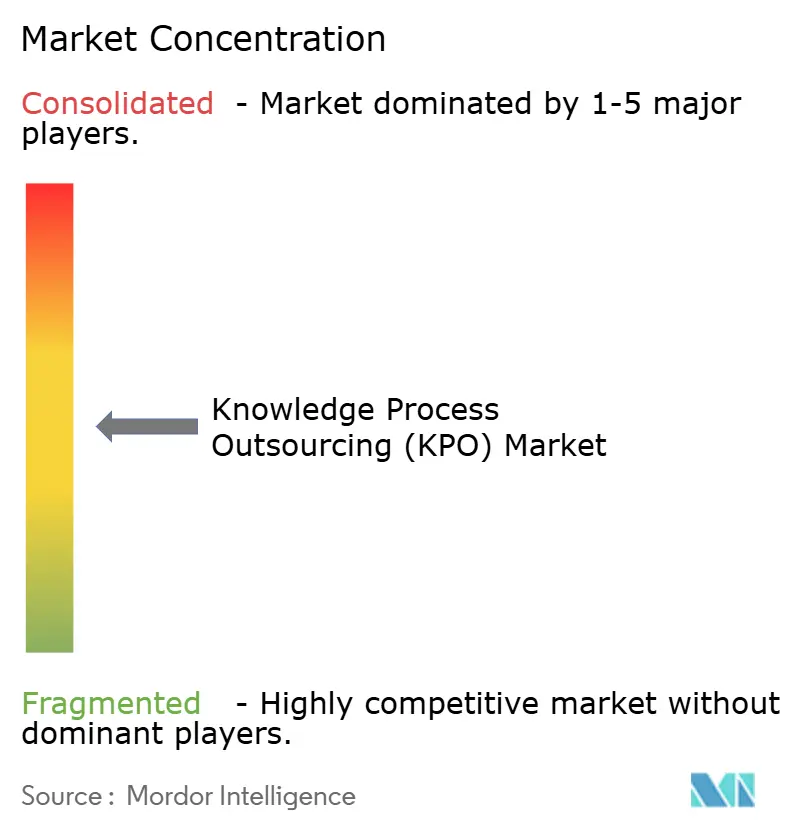

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Knowledge Process Outsourcing (KPO) Market Analysis by Mordor Intelligence

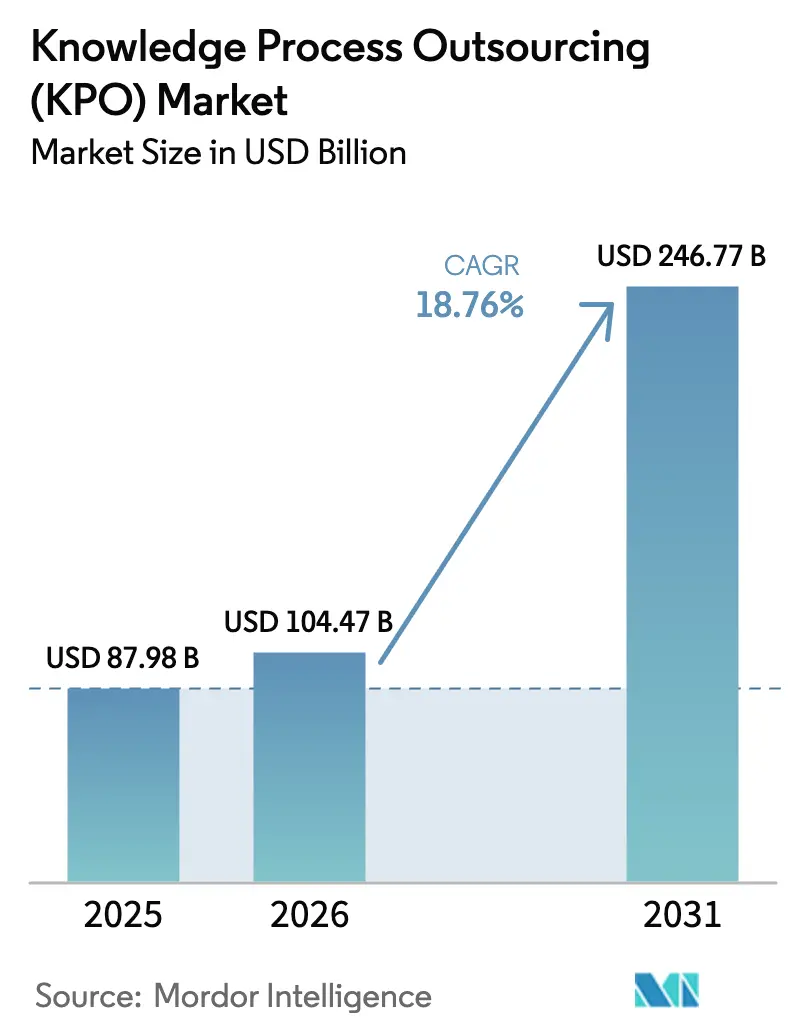

The knowledge process outsourcing market size in 2026 is estimated at USD 104.47 billion, growing from 2025 value of USD 87.98 billion with 2031 projections showing USD 246.77 billion, growing at 18.76% CAGR over 2026-2031. Surging demand for high-value analytics, heightened regulatory scrutiny, and the need to bridge global talent gaps are shifting outsourcing from a cost-savings tactic to a strategic partnership model. Enterprises now insist on domain expertise and real-time insight generation, encouraging providers to combine data science, industry knowledge, and regulatory fluency. Technology adoption—especially generative AI, robotic process automation, and low-code orchestration—raises service speed and breadth, while geopolitical risk and data-sovereignty rules push clients toward more diversified delivery footprints within the knowledge process outsourcing market. Competitive differentiation hinges on proprietary AI tools, outcome-based pricing, and the ability to safeguard sensitive data in complex regulatory environments.

Key Report Takeaways

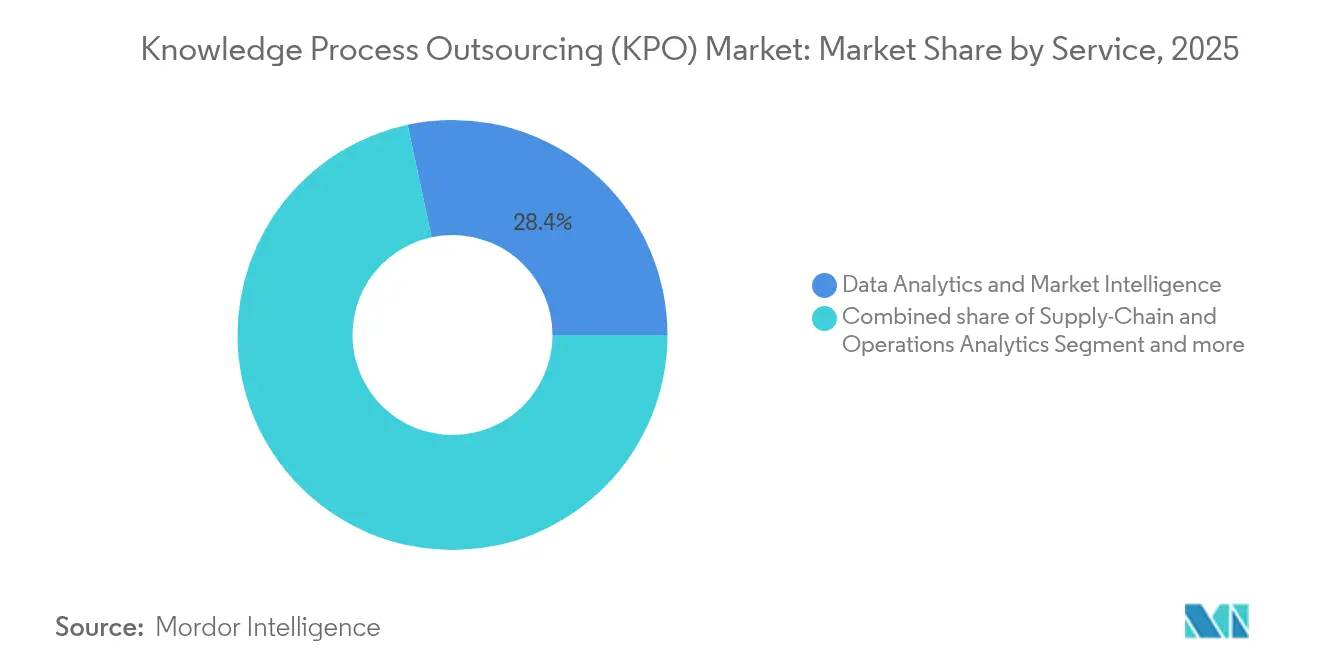

- By service type, Data Analytics and Market Intelligence held 28.35% of the knowledge process outsourcing market share in 2025, whereas Supply-Chain and Operations Analytics is projected to expand at a 19.05% CAGR through 2031.

- By end-user industry, BFSI commanded 31.78% of the knowledge process outsourcing market share in 2025, while Manufacturing and Industrial applications are set to grow the fastest at a 19.22% CAGR to 2031.

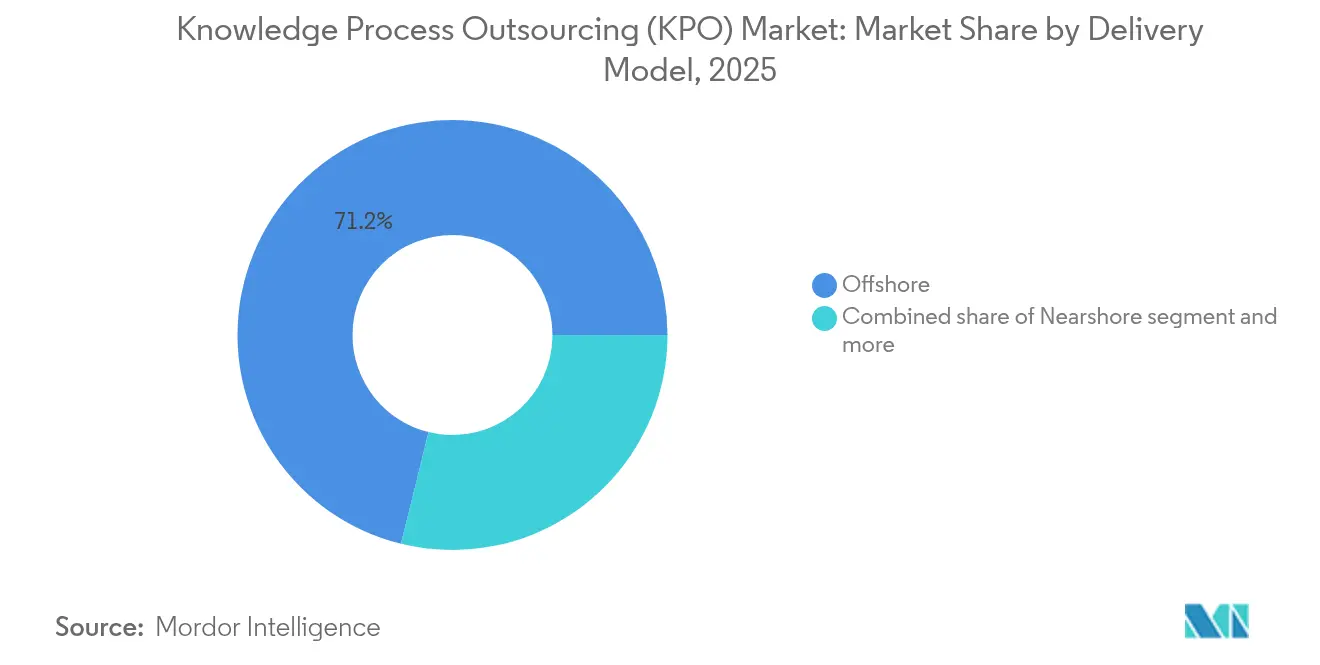

- By delivery model, offshore centers retained 71.15% revenue share in 2025; nearshore operations record the strongest momentum with a 19.63% CAGR expected through 2031.

- By organization size, large enterprises captured 60.42% of 2025 revenues, yet SME adoption is expanding at a 19.78% CAGR to 2031, supported by AI-enabled service platforms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Knowledge Process Outsourcing (KPO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for data-driven decision-making | +4.2% | Global, centered in North America and Europe | Medium term (2-4 years) |

| Cost optimisation via offshore specialised talent | +3.8% | Global, with APAC delivery hubs | Short term (≤ 2 years) |

| Digital transformation and AI/RPA enablement | +3.5% | Global, led by developed markets | Medium term (2-4 years) |

| Regulatory-driven outsourcing (ESG, AML, Basel IV) | +2.9% | North America and Europe, spreading to APAC | Long term (≥ 4 years) |

| Talent shortages in niche domains in OECD | +2.4% | OECD markets | Long term (≥ 4 years) |

| Rise of decentralised gig-based knowledge platforms | +1.8% | Global tech-forward economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Data-Driven Decision-Making

Enterprises see advanced analytics as vital to competitive positioning, driving sustained expansion of the knowledge process outsourcing market. Internal teams often lack capacity to manage streaming IoT feeds, social-media sentiment, and unstructured enterprise content. KPO partners now supply predictive modelling, algorithm governance, and scenario planning expertise, meeting rising oversight expectations from regulators that require data-backed risk assessments[1]Central Bank of Ireland, “Regulatory & Supervisory Outlook Report 2025,” centralbank.ie. Generative AI supplements, rather than replaces, human analysts, who are needed to validate models, fine-tune prompts, and curate training data.

Cost Optimisation via Offshore Specialised Talent

Labor-arbitrage remains relevant, yet has evolved to emphasize access to hard-to-find talent in quantitative finance, actuarial science, and advanced analytics. Mature hubs in India and the Philippines provide large pools of credentialed professionals, while emerging Eastern European centers add language proximity for EU clients. Value is now proven through solution quality and speed, not merely wage gaps, prompting hybrid pricing that rewards outcome delivery[2]Asia Business Council, “India’s Path Forward,” asiabusinesscouncil.org.

Digital Transformation and AI/RPA Enablement

Generative AI, natural-language search, and task-orchestrating bots allow providers to process larger datasets while freeing analysts for interpretive work. New service lines include model-prompt engineering, bias detection, and AI governance audits. Leaders embed proprietary co-pilot tools into workflows to lift analyst productivity while maintaining human oversight.

Regulatory-Driven Outsourcing (ESG, AML, Basel IV)

Heightened enforcement and expanding disclosure mandates encourage banks, insurers, and corporates to seek domain specialists who can capture, cleanse, and interpret granular risk and ESG data. ESG attestation, AML network analytics, and Basel IV capital modelling create sticky, high-margin engagements that anchor long-term provider revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and IP-protection concerns | -2.8% | Global, acute in regulated sectors | Short term (≤ 2 years) |

| Margin pressure from intense competition | -2.1% | Global, in commoditised tasks | Medium term (2-4 years) |

| On-shoring push due to data-sovereignty laws | -1.9% | Europe and North America | Long term (≥ 4 years) |

| Automation cannibalising low-end KPO revenues | -1.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Security and IP-Protection Concerns

High-profile breaches elevate board-level scrutiny of third-party analytics partners. GDPR, CCPA, and emerging localisation statutes add contractual complexity and require on-premises or private-cloud deployment models. Providers invest in zero-trust architectures and industry-specific certifications to reassure clients.

Margin Pressure from Intense Competition

Commoditisation in basic research and reporting squeezes pricing. AI-native start-ups push rapid-turnaround offerings, forcing incumbents to reposition around deeper domain expertise and outcome-linked contracts that protect margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Analytics Dominance Shifts Toward Operations Intelligence

Supply-chain visibility demands and omnichannel fulfilment complexity are driving the fastest growth in operations analytics, which is projected to rise at a 19.05% CAGR and thereby expand its weight within the knowledge process outsourcing market. Data Analytics and Market Intelligence remains the largest slice at 28.35% of 2025 revenue, reflecting entrenched enterprise dependence on external market sensing and BI platforms.

Providers are layering generative AI onto existing research workflows to speed insight generation while pushing up the value curve to simulation, digital-twin modelling, and prescriptive optimisation. Engineering design services also gain traction as manufacturers co-create products with globally distributed research and development hubs. Meanwhile, content outsourcing faces low-end displacement from automated text generators, reinforcing a pivot toward specialised editorial and thought-leadership roles that require nuanced domain interpretation within the knowledge process outsourcing market.

By End-User Industry: Manufacturing Acceleration Challenges BFSI Leadership

BFSI leads with 31.78% of 2025 revenue, anchored by risk analytics and regulatory reporting that clients seldom bring fully in-house. Yet manufacturing-sector engagements are expanding at a 19.22% CAGR as factories digitise production, adopt predictive maintenance, and pursue resilient sourcing. This momentum increases the sector’s contribution to the knowledge process outsourcing market size while balancing industry concentration.

Retailers and e-commerce firms outsource customer-journey analytics and demand forecasting to refine merchandising and reduce stockouts. Healthcare and life-sciences companies rely on specialist providers for pharmacovigilance and real-world-evidence studies that inform value-based care models. Collectively, these verticals diversify the knowledge process outsourcing industry and lessen dependence on financial-services spending.

By Delivery Model: Nearshore Momentum Challenges Offshore Dominance

Although offshore hubs still captured 71.15% of 2025 spend, nearshore locations in Latin America and Eastern Europe are growing at 19.63% CAGR as clients seek time-zone overlap and improved data-sovereignty alignment. Hybrid models mix offshore cost advantages with nearshore collaboration and onshore oversight, letting clients assign workloads by sensitivity and required responsiveness.

Providers continue upgrading physical and cyber-security controls across multi-shore campuses, ensuring that proximity benefits do not undermine the cost-efficiency that historically defined the knowledge process outsourcing market. Those capable of orchestrating seamless multi-site delivery earn premium positioning with highly regulated clients.

By Organization Size: SME Adoption Accelerates Through AI-Enabled Platforms

Large enterprises contributed 60.42% of 2025 revenue, but AI-driven, self-service portals are lowering entry thresholds, allowing SMEs to tap modular analytics and compliance services at a 19.78% CAGR. Flexible subscription terms and outcome-based pricing resonate with mid-market CFOs looking to convert fixed analytics headcount into variable costs within the knowledge process outsourcing market.

Providers that productise repeatable service modules, such as sales-pipeline diagnostics or ESG data reconciliation, secure scale without excessive customisation. This evolution expands addressable demand and underscores how automation democratises sophisticated knowledge work beyond the enterprise tier of the knowledge process outsourcing industry.

Geography Analysis

North America held 40.65% of worldwide revenue in 2025, with United States banks, insurers, and healthcare networks relying on third-party specialists for model risk management, clinical analytics, and real-time fraud detection. Canada complements demand with energy-sector outsourcing for asset-integrity assessment and carbon accounting. Mexico rises as a nearshore delivery hub, benefiting from USMCA provisions and cultural affinity.

Asia-Pacific is the fastest-growing region at a 19.54% CAGR, underpinned by India’s mature talent pools and policy support for AI-enabled services. The region not only supplies cost-efficient capacity but also generates rising domestic demand from Chinese conglomerates and ASEAN manufacturers pursuing sophisticated analytics. Governments in Vietnam and Malaysia invest in STEM training and 5G infrastructure, further propelling the knowledge process outsourcing market.

Europe expands steadily as GDPR compliance, ESG reporting, and Basel IV readiness steer clients toward regional providers. Germany and the United Kingdom generate sizeable engagements, while Poland and Romania scale delivery centres for actuarial and multi-lingual analytics. In the Middle East, UAE and Saudi Arabia channel sovereign funds into AI research zones that double as regional KPO hubs, whereas South Africa frames itself as a springboard for Anglophone Africa, adding geographic diversity to the knowledge process outsourcing market.

Competitive Landscape

The knowledge process outsourcing market shows moderate concentration. Global IT-services majors such as Accenture, TCS, and Infosys accelerate deal activity, acquiring AI boutiques that boost domain depth in climate-risk modelling, drug discovery analytics, and marketing science. Private-equity interest rises as recurring, compliance-driven revenue streams promise stable cash flows; there were 857 KPO-related merger and acquisition transactions worth USD 32.2 billion in 2024[3]Siemens AG, “Siemens Expands U.S. Manufacturing Footprint with USD 10 Billion Investment,” siemens.com.

Strategic differentiation rests on proprietary AI co-pilots, sector-specific data models, and value-sharing contracts that link provider income to business outcomes. Smaller specialists defend niches through deep expertise—for example, ESG scoring frameworks or anti-fraud graph analytics—often partnering with cloud hyperscalers for scale.

Investment priorities include zero-trust security, prompt-engineering academies, and certifications covering AML, pharmacovigilance, and aerospace compliance. As automation absorbs routine tasks, human analysts focus on storytelling, causal inference, and regulator engagement, reinforcing the symbiotic AI-plus-expertise model that defines leadership in the knowledge process outsourcing market.

Knowledge Process Outsourcing (KPO) Industry Leaders

WNS Global Services

Genpact Limited

International Business Machines Corporation

Wipro Limited

Infosys Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Siemens announced USD 10 billion of US manufacturing investments to expand AI-powered design and simulation services following its Altair acquisition.

- May 2025: Siemens introduced Industrial Copilot AI agents that demonstrated 50% productivity gains across automation tasks.

- March 2025: India’s TCS, Infosys, Wipro, and HCLTech disclosed plans to hire 70,000 graduates in FY26 to meet escalating AI and digital-transformation demand.

- February 2025: The Central Bank of Ireland’s Supervisory Outlook underscored stricter oversight of AI use and third-party dependencies in financial services.

- January 2025: Baker McKenzie outlined 2025 compliance milestones, including the Designated Activities Regime and tighter third-party risk governance that affect KPO contracts.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the knowledge process outsourcing (KPO) market as revenue from contracts where domain specialists deliver analytics-heavy services such as data analytics, business and financial research, legal support, and engineering design. According to Mordor Intelligence, on-site, near-shore, and offshore delivery all fall within scope.

For clarity, we exclude routine contact-center, transaction processing, and generic IT help-desk work.

Segmentation Overview

- By Service

- Data Analytics and Market Intelligence

- Supply-Chain and Operations Analytics

- Engineering and Product Design

- Equity, Investment and Risk Research

- Content and Publishing Outsourcing

- Research and Development Outsourcing

- Other Niche Services (IP, Legal, Actuarial)

- By End-user Industry

- IT and Telecom

- BFSI

- Retail and E-commerce

- Manufacturing and Industrial

- Healthcare and Life Sciences

- Others (Energy, Media, Education)

- By Delivery Model

- Offshore

- Nearshore

- Onshore

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed procurement heads in BFSI, life sciences, and tech firms, plus leaders at tier-1 KPO vendors across North America, Europe, India, and the Philippines. Dialogues verified rates, contract terms, GenAI uptake, and how data-sovereignty rules shape delivery.

Desk Research

We mapped the service pool using UNCTAD commercial-services trade, World Bank digital indicators, WTO TiVA, and national filings like US BLS and India RBI data. These datasets anchor regional export value and talent.

Next, Mordor analysts parsed SEC 10-Ks, NASSCOM sheets, and provider releases, cross-checking news via Factiva and financials on Hoovers. Patent counts from Questel and rulings by FCA or MAS flagged demand. Sources listed are illustrative, not exhaustive.

Market-Sizing & Forecasting

Our model starts top-down: export receipts, payroll surveys, and provider disclosures rebuild global spend, then split by service, industry, and region. Selective bottom-up roll-ups of listed suppliers and sampled ASP × FTE counts act as a reasonableness check.

We track variables like offshore wage spreads, analytics share in CFO budgets, e-discovery caseloads, engineering R&D outsourcing, and GenAI productivity lift. A multivariate regression projects each driver through 2030, while scenario analysis cushions currency shifts. Missing supplier splits are imputed from three-year contract awards in Factiva.

Data Validation & Update Cycle

Outputs undergo dual analyst review, variance alerts flag shifts over five percent, and anomalies prompt follow-up interviews. Reports refresh yearly, and big deals or regulations trigger interim updates before we release findings.

Why Mordor Intelligence's Knowledge Process Outsourcing Baseline Commands Reliability

Clients often notice that published KPO values rarely match because each study tweaks what gets counted and which year's exchange rate underpins the math.

Most gaps appear when studies bundle routine BPO revenue into KPO or stretch one historic growth rate without fresh provider filings or trade data. Mordor narrows scope to knowledge-centric contracts, converts inputs to constant 2025 dollars, and updates drivers yearly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 87.98 B (2025) | Mordor Intelligence | - |

| USD 141.0 B (2024) | Global Consultancy A | Folds routine BPO |

| USD 68.9 B (2024) | Industry Research B | No filing check |

| USD 56.73 B (2023) | Research Boutique C | Press releases only |

The comparison shows Mordor's disciplined scope, driver-based modeling, and tight update cycle deliver a balanced, transparent baseline managers can rely on.

Key Questions Answered in the Report

What is the current size of the knowledge process outsourcing market?

The knowledge process outsourcing market size reached USD 104.47 billion in 2026 and is projected to hit USD 246.77 billion by 2031.

Which service segment is growing the fastest?

Supply-Chain and Operations Analytics is the fastest-growing service line, expected to expand at a 19.05% CAGR through 2031.

Why is nearshore delivery gaining traction?

Nearshoring offers time-zone alignment, stronger data-sovereignty compliance, and geopolitical risk mitigation while retaining many cost benefits of traditional offshore models.

How is AI affecting KPO providers?

Generative AI and RPA automate low-complexity tasks, boost analyst productivity, and create new service categories such as model governance and prompt engineering.

Which industries contribute most to KPO demand?

BFSI leads with 31.78% of 2025 revenue, followed by fast-rising Manufacturing & Industrial clients that require supply-chain and operational analytics.

What security measures do top KPO providers adopt?

Market leaders implement zero-trust architectures, secure private-cloud environments, and obtain sector-specific certifications to meet stringent data-protection requirements.

Page last updated on: