Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.87 Billion |

| Market Size (2031) | USD 6.54 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

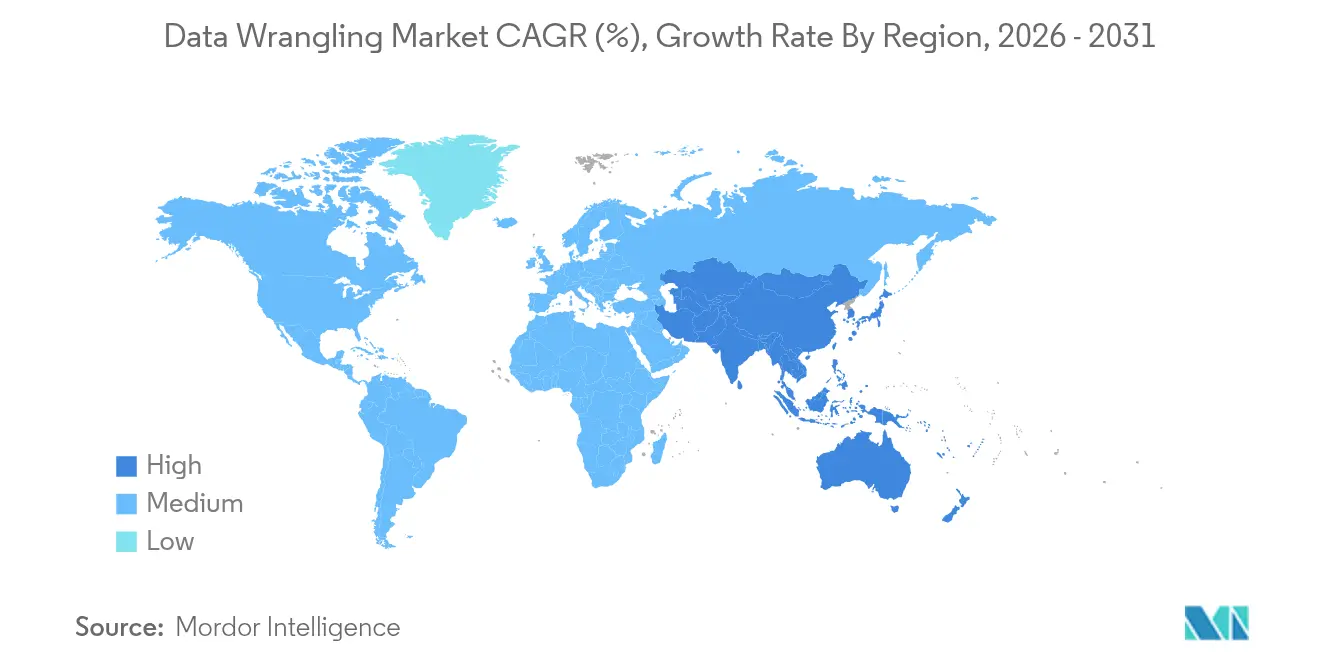

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

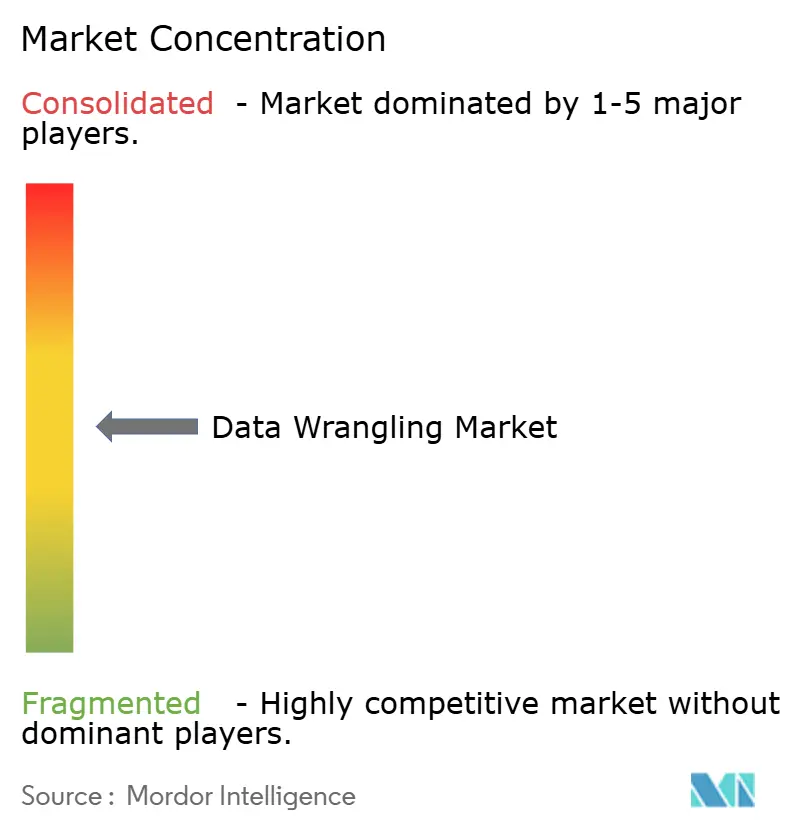

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Wrangling Market Analysis by Mordor Intelligence

The data wrangling market size is expected to grow from USD 3.48 billion in 2025 to USD 3.87 billion in 2026 and is forecast to reach USD 6.54 billion by 2031 at 11.08% CAGR over 2026-2031. Over the forecast period, the accelerating growth of enterprise data, mounting demand for real-time analytics, and the pivot from traditional ETL suites to AI-enabled preparation platforms will remain the principal growth engines. Vendors are embedding generative AI, low-code transformation flows, and lakehouse connectors to shorten time-to-insight and support self-service across finance, marketing, and operations teams. Competitive intensity is rising as hyperscale cloud providers integrate native wrangling features, forcing pure-play data preparation firms to differentiate through domain-specific automation and multimodal support. Emerging regulations that mandate strong governance frameworks and lineage reporting further reinforce adoption momentum, even as escalating compute costs push enterprises toward hybrid deployment models.

Key Report Takeaways

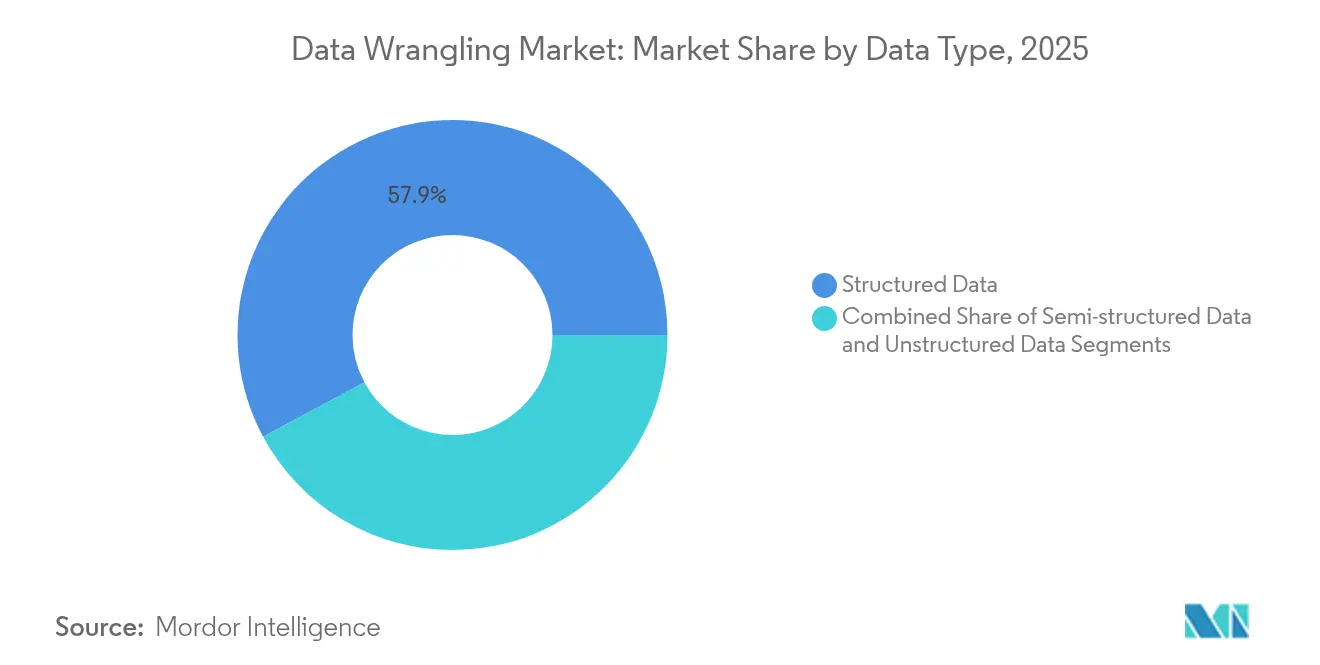

- By data type, structured formats retained 57.85% of data wrangling market share in 2025, while unstructured formats are forecast to expand at a 12.32% CAGR through 2031.

- By component, software captured 68.85% revenue in 2025; services represent the fastest-growing component at a 12.45% CAGR to 2031.

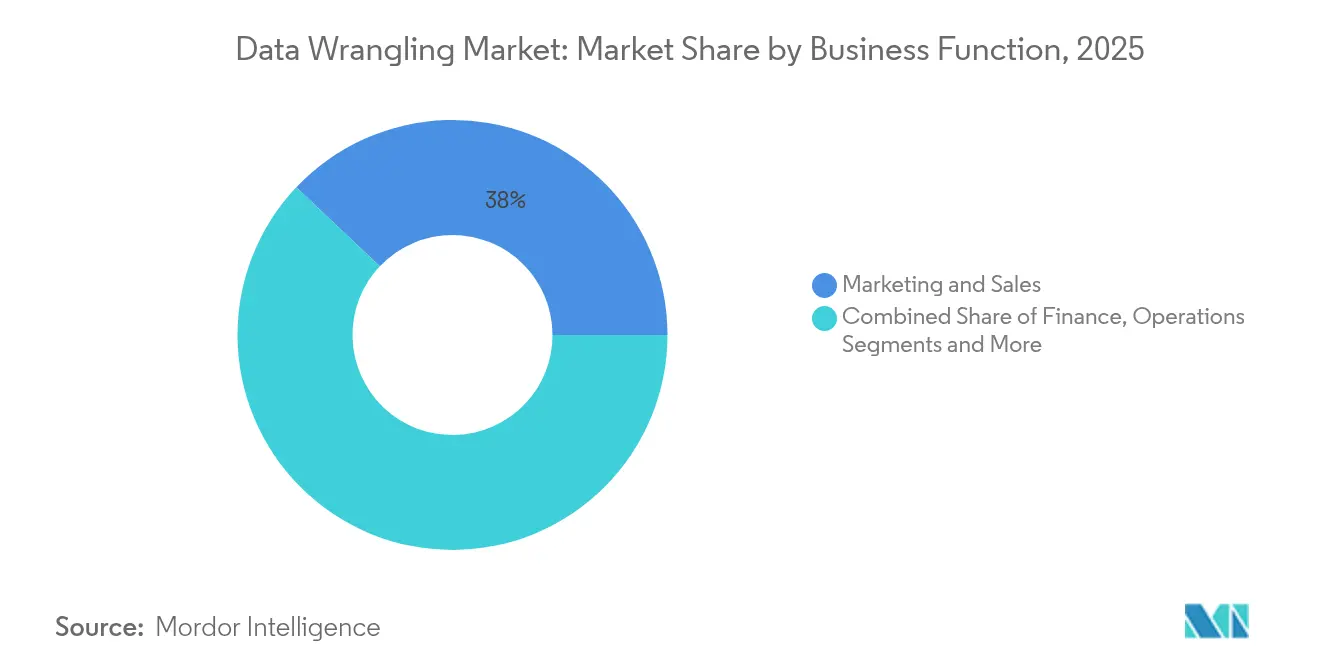

- By business function, marketing and sales led with 37.95% share of the data wrangling market in 2025, whereas finance is projected to grow at 11.98% CAGR.

- By end-user industry, IT and telecommunication held 27.35% share of the data wrangling market in 2025, and BFSI is advancing at an 11.42% CAGR.

- By geography, North America commanded 37.10% revenue share in 2025, while Asia-Pacific is set to register an 11.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Wrangling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global data volumes | +2.8% | Global | Long term (≥ 4 years) |

| Advances in AI-driven automation | +2.1% | North America, EU, APAC | Medium term (2-4 years) |

| Growing self-service analytics demand | +1.9% | Global | Short term (≤ 2 years) |

| Stricter quality and governance mandates | +1.7% | EU, North America | Medium term (2-4 years) |

| Lakehouse migration momentum | +1.4% | APAC, Middle East and Africa | Medium term (2-4 years) |

| Rise of no-code LLM copilots | +1.2% | North America, EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Volumes of Data Generated Across Industries

McKinsey estimates that global data-center outlays will reach USD 6.7 trillion by 2030, of which USD 5.2 trillion relates directly to AI workloads. Edge devices, 5G rollouts, and digitization of manufacturing lines are fueling data creation that outpaces legacy ETL capacity. Asia-Pacific exemplifies this trajectory with 12,206 MW of operational data-center power and 14,338 MW under development in 2024. Enterprises therefore pivot to platforms capable of processing diverse, high-frequency feeds in local jurisdictions that impose sovereignty guardrails.

Advancement in AI and Big-Data Technologies Enabling Automation

Vendors such as Alteryx have embedded generative assistants that recommend transformation steps and generate summaries in natural language. Gartner’s 2025 taxonomy of agentic analytics points to autonomous pipelines that self-correct for schema drift and optimize compute allocation. Databricks accelerated this trend by acquiring Lilac AI, adding LLM-based data-quality scoring to its lakehouse stack. While AI raises productivity, organizations temper adoption with hybrid deployment strategies that mitigate compute cost spikes.

Rising Demand for Self-Service Data Preparation Among Business Users

Retail case studies show that 54% of firms captured at least 10% profit gains from data analytics initiatives, yet still encounter fragmented silos that hinder self-service. Citizen data-scientist programs and embedded wrangling modules in BI suites equip finance and merchandising teams with point-and-click interfaces. Gartner forecasts over half of Chief Data and Analytics Officers will invest in data-literacy programs by 2027, highlighting that soft-skill enablement matters as much as tool selection.

Stricter Data-Quality and Governance Regulations

BCBS 239 and GDPR elevate the need for lineage, traceability, and audit-grade transformations. The European Central Bank’s latest RDARR reviews flagged persistent gaps in risk data aggregation, spurring banks to adopt enterprise-grade platforms that automate rule enforcement. Healthcare providers deploy de-identification routines to comply with HIPAA while preserving granular clinical attributes for research use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low SME awareness of data-wrangling tools | -1.8% | Emerging markets | Medium term (2-4 years) |

| Security-driven data-access restrictions | -1.2% | EU, APAC | Long term (≥ 4 years) |

| Shortage of cloud data-engineering talent | -1.1% | North America, EU | Medium term (2-4 years) |

| Escalating cloud compute expenses | -0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Awareness of Data-Wrangling Tools Among SMEs

MSMEs account for 98.9% of all businesses in Central and West Asia, yet scarce digital skills and budget constraints leave many reliant on spreadsheets[1]Asian Development Bank, “Asia SME Monitor 2022,” adb.org . Policy bodies advocate training subsidies and cloud vouchers to broaden adoption, while vendors pursue freemium tiers and local reseller partnerships to penetrate this price-sensitive segment.

Escalating Cloud-Compute Costs for Gen-AI-Enhanced Wrangling Workloads

IBM reported an 89% jump in compute outlays between 2023 and 2025, prompting 70% of executives to delay AI projects. Enterprises now benchmark total-cost-of-ownership across hyperscalers, adopt parameter-efficient models, and cache intermediate results to curb spend. These tactics temper but do not erase demand for AI-rich preparation pipelines, sustaining the long-term trajectory of the data wrangling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Type: Unstructured Volumes Open New Frontiers

Structured data contributed USD 2.01 billion to the data wrangling market size in 2025, equal to 57.85% revenue. Relational tables remain pivotal for transactional integrity and core reporting. Even so, modern pipelines must fuse logs, clickstreams, and sensor feeds into warehouse and lakehouse environments. SQL-centric visual builders that auto-generate lineage maps help enterprises maintain governance as row counts surge.

The unstructured segment is projected to add USD 1.19 billion in incremental revenue between 2026 and 2031 at a 12.32% CAGR, the highest pace among data types. LLM-powered classification and computer vision capabilities unlock insights within contracts, engineering drawings, and video frames. Providers differentiate by offering integrated vector indexing, multimodal metadata extraction, and privacy-aware redaction modules that comply with cross-border regulations.

By Component: Services Expand as Projects Grow Complex

Software tools held 68.85% of the data wrangling market in 2025, translating to USD 2.4 billion in license and subscription fees. Cloud-native suites weave preparation, cataloging, and governance into one workspace. Vendors cement stickiness by bundling prep functionality inside analytics or ML workloads, turning data wrangling into a workflow rather than a standalone task.

Services revenue, forecast to grow 12.45% annually, reflects demand for architecture design, migration, and managed operations. Deloitte’s collaboration with Databricks on Data as a Service for Banking underscores the lift that expert partners provide during modernization initiatives. As lakehouses and distributed fabrics mature, many firms outsource pipeline monitoring to specialists who deliver 24 × 7 support under outcome-based contracts.

By Business Function: Finance Accelerates Technology Spend

Marketing and sales captured 37.95% of data wrangling market share in 2025, equivalent to USD 1.32 billion, driven by omnichannel activation and personalization demands. Platform roadmaps add reverse-ETL connectors that push clean attributes back to campaign engines, enabling near real-time segmentation and A/B testing.

Finance workloads will rise at 11.98% CAGR to 2031 as regulators tighten reporting expectations and CFOs pursue continuous accounting. Rules-driven reconciliation templates, anomaly detection, and instant aggregation functions reduce month-end cycles from days to hours. Audit-ready lineage and immutable data-quality metrics position vendors for sustained growth within treasury, risk, and controllership teams.

By End-User Industry: BFSI Leads Compliance-Driven Uptake

IT and telecommunication contributed USD 0.95 billion to the data wrangling market in 2025. These firms run massive infrastructure footprints and act as early adopters of data governance frameworks. Their experience informs best practices later adopted by other verticals.

BFSI deployments will outpace all other sectors, growing 11.42% annually to 2031. Basel-aligned calculations such as liquidity and credit value adjustments require granular, high-frequency feeds that legacy ETL cannot accommodate. Banks turn to wrangling engines that parse nested XML trade files, enrich them with reference data, and surface lineage for supervisors. Insurance carriers use similar pipelines for solvency analytics, catastrophe modeling, and ESG disclosures.

Geography Analysis

North America held 37.10% of global revenue in 2025, reflecting deep cloud penetration, established hyperscale data-center networks, and sustained venture funding for AI-first platforms. United States enterprises drive the bulk of spend, illustrated by Microsoft’s USD 42.4 billion cloud revenue in Q1 2025 and Fabric’s 80% customer surge. Canada aligns with skills and regulatory frameworks, whereas Mexico’s manufacturing clusters embrace local lakehouse deployments to comply with data-residency laws. Cost pressures are pushing many firms toward workload-aware tiering that keeps frequently accessed datasets on fast object storage and archives cold data on-premises.

Asia-Pacific is forecast to log an 11.75% CAGR, making it the fastest-growing theater for the data wrangling market. Regional enterprises benefit from the 12,206 MW operational data-center footprint, an expanding 5G user base, and sovereign cloud offerings in China, India, and Indonesia. Local providers collaborate with global platforms to offer in-territory edges that satisfy latency and regulation constraints. Strong e-commerce and fintech ecosystems in Singapore and Hong Kong demand real-time customer 360 solutions, intensifying the call for scalable preparation engines.

Europe holds a mature but regulation-heavy environment where GDPR and operational risk mandates dictate procurement criteria. German automotive manufacturers deploy digital twins that blend plant telemetry with enterprise resource planning data. United Kingdom banks advance lineage automation to satisfy Prudential Regulation Authority expectations. Meanwhile, South America, and Middle East, and Africa remain nascent but promising. Brazil’s open banking initiative stimulates API traffic that must be standardized, and Saudi Arabia’s cloud-first directives increase demand for localized data fabrics that balance cultural and legal considerations.

Competitive Landscape

The data wrangling market features a mix of broad-based cloud suites and specialist vendors, leading to a moderate concentration of power. Microsoft, IBM, and Oracle bundle preparation with adjacent analytics and governance modules, capitalizing on existing enterprise agreements and global channel networks. Alteryx and Informatica compete through intuitive UIs and out-of-the-box connectors aimed at line-of-business analysts. Databricks and Snowflake position their lakehouse and cloud data platform ecosystems as the backbone for AI-native transformation flows, with Databricks reaching USD 3.7 billion in annualized revenue by July 2025 and 50% growth year over year.

Strategic deals underscore the race to embed AI and governance. ServiceNow acquired Data.world in May 2025 to integrate cataloging and workflow orchestration[3]ServiceNow Press Release, “ServiceNow completes acquisition of data.world,” servicenow.com. Databricks followed with Lilac AI to strengthen LLM-centric data-quality scoring. Partnerships also proliferate; Databricks joined forces with BladeBridge in April 2025 to streamline warehouse-to-lakehouse migrations. Vendor roadmaps now feature vector stores, fine-tuned language models, and cost-aware orchestration that automatically chooses between Spark, Photon, or SQL engines.

Price competition is rising as hyperscalers lower storage and compute tariffs for long-running analytics clusters, squeezing margins for standalone vendors. Nevertheless, differentiation around verticalized templates, data contracts, and instream quality checks keeps the field vibrant. The next arena of competition will likely center on autonomous agents that not only prepare but also continuously monitor and adapt pipelines based on business-rule changes.

Data Wrangling Industry Leaders

Alteryx, Inc.

Oracle Corporation

Teradata Corporation

SAS Institute Inc.

Altair Engineering Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Microsoft posted USD 70.1 billion total revenue and USD 42.4 billion cloud revenue, up 22% year over year, highlighting demand for AI and data services.

- May 2025: ServiceNow completed its acquisition of data.world, adding advanced catalog and governance capabilities to Workflow Data Fabric.

- April 2025: Databricks partnered with BladeBridge to migrate over 20 legacy warehouses to lakehouse architecture using AI-guided tooling.

- March 2025: Microsoft reported record quarterly cloud revenue exceeding USD 42 billion, with Microsoft Fabric adoption rising 80% year over year.

Global Data Wrangling Market Report Scope

Data wrangling is defined as the process of preparing raw data for analysis by cleaning, arranging, and converting it into the required format. Data wrangling, also known as data cleaning or data munging, helps organizations handle more complicated data in less time, create more accurate results, and make better decisions.

The data wrangling market is segmented by component (tool, service), deployment (cloud-based, on-premises), enterprise type (large, small, and medium-sized), end-user industry (IT and telecommunication, retail, government, BFSI, and healthcare), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Data Type

| Structured Data |

| Semi-structured Data |

| Unstructured Data |

By Component

| Software | Self-service data-preparation platforms |

| Embedded prep modules in BI/AI suites | |

| Services | Managed Services |

| Professional / Consulting Services |

By Business Function

| Finance |

| Marketing and Sales |

| Operations |

| Human Resources |

| Legal and Compliance |

By End-user Industry

| IT and Telecommunication |

| BFSI |

| Retail and E-commerce |

| Healthcare |

| Government and Public Sector |

| Other End-user Industries |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Data Type | Structured Data | ||

| Semi-structured Data | |||

| Unstructured Data | |||

| By Component | Software | Self-service data-preparation platforms | |

| Embedded prep modules in BI/AI suites | |||

| Services | Managed Services | ||

| Professional / Consulting Services | |||

| By Business Function | Finance | ||

| Marketing and Sales | |||

| Operations | |||

| Human Resources | |||

| Legal and Compliance | |||

| By End-user Industry | IT and Telecommunication | ||

| BFSI | |||

| Retail and E-commerce | |||

| Healthcare | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the data wrangling market?

The data wrangling market reached USD 3.87 billion in 2026 and is projected to grow to USD 6.54 billion by 2031 at an 11.08% CAGR.

Which region leads the data wrangling market?

North America led with 37.10% revenue share in 2025, supported by deep cloud adoption and a mature analytics ecosystem.

Which component is expanding fastest?

Services are the fastest-growing component, registering a 12.45% CAGR as enterprises seek expert support for complex transformation projects.

Why is the BFSI sector investing heavily in data wrangling?

Stricter regulations such as BCBS 239 require robust risk data aggregation and real-time reporting, driving rapid adoption in banking and insurance.

How are rising compute costs affecting adoption?

Escalating cloud expenses are pushing organizations toward hybrid deployments and parameter-efficient models, yet the long-term growth trajectory remains intact.

What competitive moves are shaping the market?

Recent acquisitions such as ServiceNow–data.world and Databricks–Lilac AI highlight a shift toward integrated governance and AI-powered quality analytics.

Page last updated on: