Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

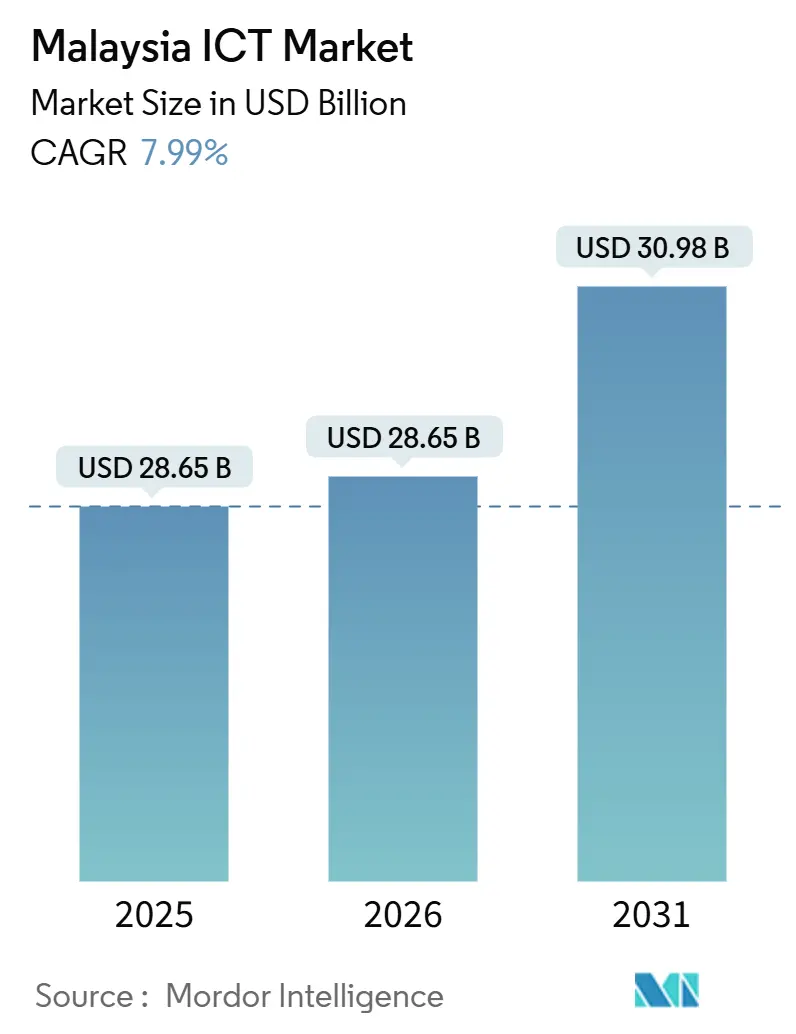

| Base Year Market Size (2025) | USD 28.65 Billion |

| Market Size (2026) | USD 28.65 Billion |

| Market Size (2031) | USD 30.98 Billion |

| Growth Rate (2026 - 2031) | 7.99% CAGR |

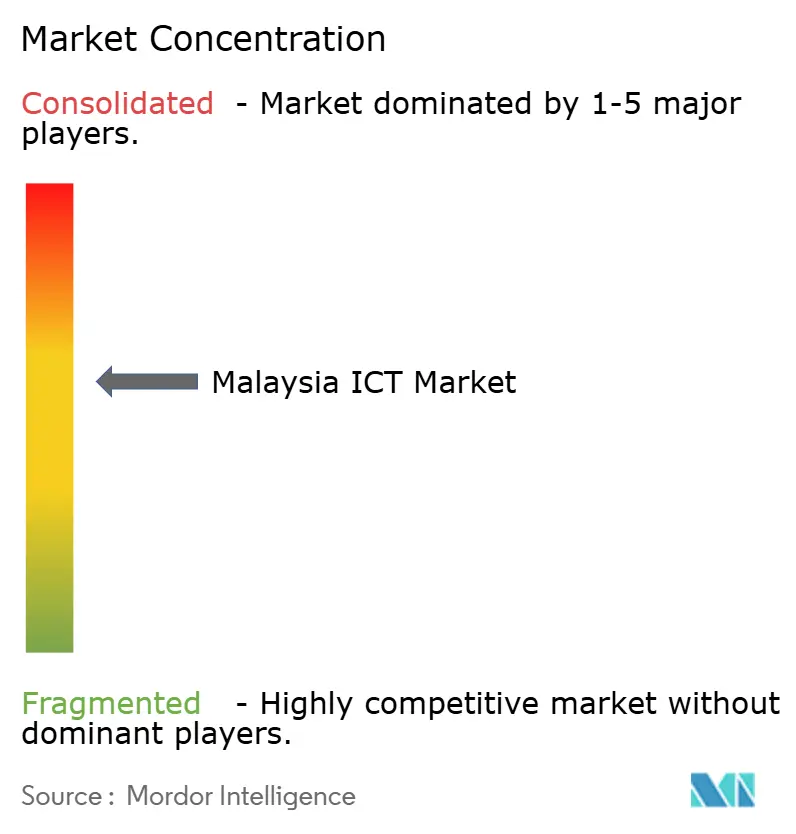

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia ICT Market Analysis by Mordor Intelligence

The Malaysia ICT Market size is projected to expand from USD 28.65 billion in 2025 and USD 28.65 billion in 2026 to USD 30.98 billion by 2031, registering a CAGR of 7.99% between 2026 to 2031.

Robust public-sector funding under MyDIGITAL and the 12th Malaysia Plan, a dual-network 5G architecture, and USD 9.2 billion in hyperscale data-center commitments collectively sustain double-digit demand for cloud platforms, cybersecurity, and edge connectivity. Enterprise buyers continue to replace legacy MPLS links with 5G private networks, while the government’s cloud-first mandate compresses procurement cycles for infrastructure-as-a-service and platform-as-a-service offerings. Large enterprises drive near-term revenue through modern ERP conversions, yet small and medium enterprises accelerate their spending trajectory as grants, tax deductions, and subscription pricing narrow the digital divide. Despite power-supply constraints in Johor and a national cybersecurity skills shortage, sustained foreign direct investment and competitive carrier dynamics keep the growth outlook intact for the Malaysia ICT market.

Key Report Takeaways

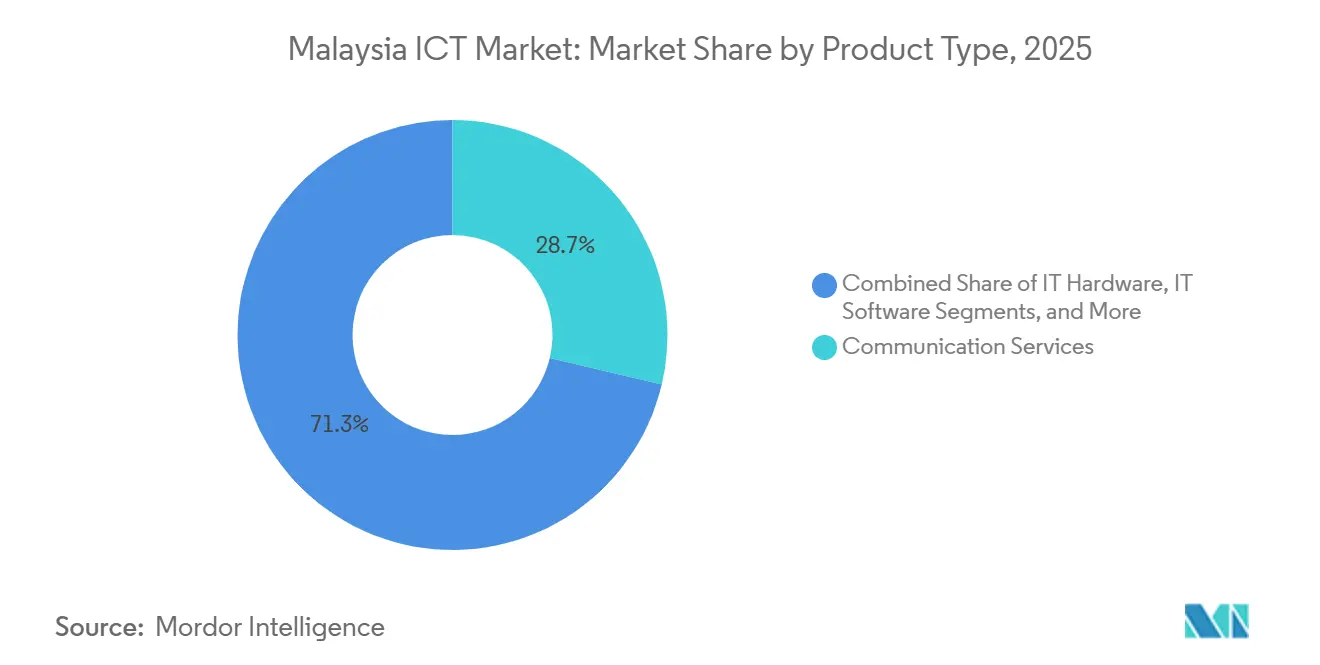

- By product type, Communication Services led with 28.70% of the Malaysia ICT market share in 2025, while IT Security is advancing at a 10.99% CAGR to 2031.

- By enterprise size, Large Enterprises held 58.20% spending in 2025, whereas Small and Medium Enterprises are projected to grow at an 8.10% CAGR through 2031.

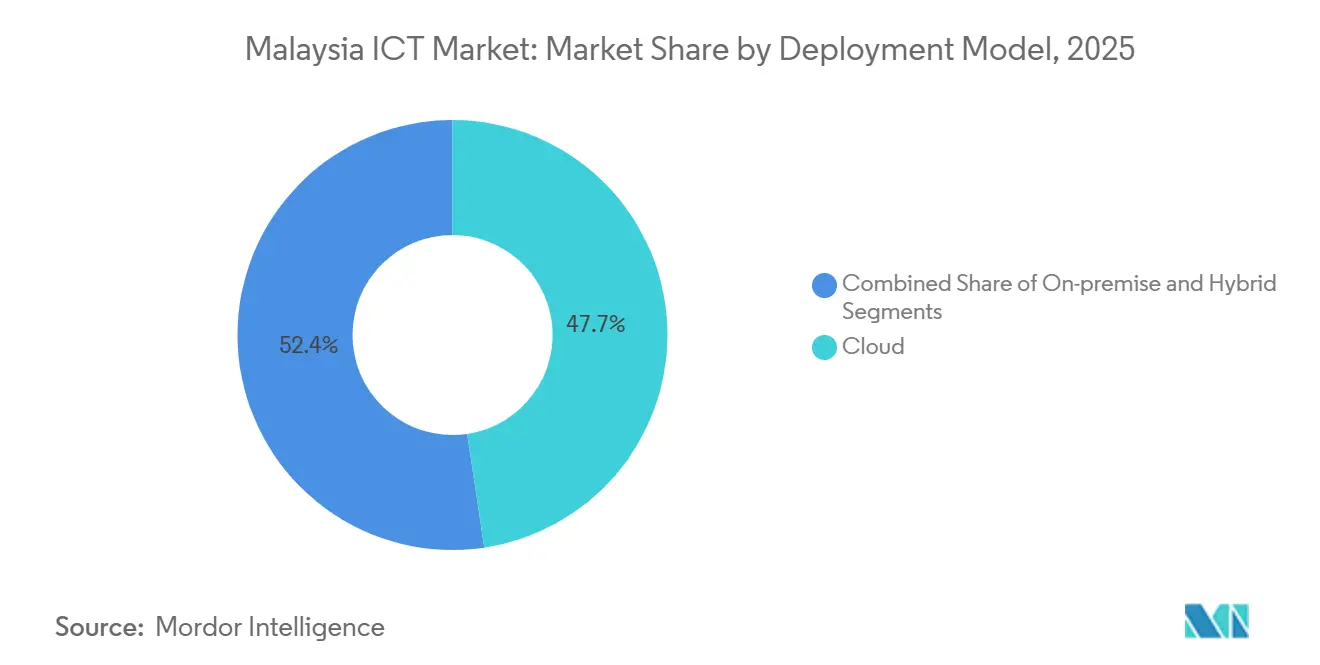

- By deployment model, cloud deployment accounted for 47.65% of the Malaysia ICT market size in 2025 and is set to expand at an 8.40% CAGR between 2026 and 2031.

- By industry vertical, Manufacturing and Industry 4.0 captured 19.30% of 2025 spending, while Gaming and Esports posts the fastest 11.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MyDIGITAL and 12th Malaysia Plan execution push | +2.1% | National, early gains in Klang Valley, Johor, Penang | Medium term (2-4 years) |

| National 5G roll-out under dual-network model | +1.8% | National, urban-first rollout with rural coverage by 2027 | Short term (≤ 2 years) |

| Cloud-first policy catalyzing hyperscale data-center builds | +1.5% | National, concentrated in Selangor, Johor, Penang | Long term (≥ 4 years) |

| SME digital-tax incentives and matching grants | +0.9% | National, higher uptake in Selangor, Penang, Johor | Medium term (2-4 years) |

| PADU national registry unlocking analytics demand | +0.7% | National, government and BFSI sectors lead adoption | Short term (≤ 2 years) |

| AI-optimized electricity tariff for Kedah GPU clusters | +0.4% | Regional, Kedah with potential replication in Sarawak | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MyDIGITAL and 12th Malaysia Plan Execution Push

Federal allocations totaling RM 3.5 billion across the 2025–2026 budgets keep ministries on pace to deliver 80% end-to-end digital public services. Forty-seven agencies migrated legacy workloads in 2024, signaling a steady pipeline for cloud migration, SaaS procurement, and managed services. The forthcoming 13th Malaysia Plan extends the agenda and formalizes a 50% digital-economy GDP target by 2030, further anchoring enterprise confidence in long-term ICT demand. Vendor lock-in clauses are being rewritten, leveling the field for mid-tier Malaysian integrators. Procurement standardization also trims integration costs, prompting wider experimentation with open-source stacks and micro-services architectures.

National 5G Roll-Out Under Dual-Network Model

Malaysia’s November 2024 decision to license U Mobile as a second 5G operator introduces sustained price competition and service differentiation. Digital Nasional Berhad’s 81.6% population coverage pairs with U Mobile’s industrial-zone focus, giving enterprises multi-carrier choice and stronger service-level negotiations. CelcomDigi’s March 2025 standalone 5G core reached sub-10-millisecond latency, an essential threshold for automated guided vehicles and real-time visual inspection lines.[1]Source: CelcomDigi Annual Report 2024, celcomdigi.comTower-sharing reduces capital intensity, while fiber backhaul contracts funnel incremental revenue to infrastructure vendors. Regulatory mandates for 90% population coverage by 2027 compress the deployment timeline, pulling forward equipment orders and systems-integration projects.

Cloud-First Policy Catalyzing Hyperscale Data-Center Builds

The Malaysia Cloud Policy 2.0 classifies data by sensitivity, permitting public-sector workloads in compliant local regions. AWS, Google Cloud, Microsoft, and Oracle collectively add 450 megawatts of IT load, positioning Malaysia as Southeast Asia’s third-largest data-center hub.[2]Source: AWS Press Release, “Amazon Web Services Announces USD 6 Billion Investment in Malaysia Through 2038,” press.aboutamazon.com Sovereign-data residency rules guarantee local tenancy for sensitive applications, boosting take-up of object storage, GPU instances, and managed AI pipelines. Competitive entry of three hyperscalers trimmed compute pricing by 15% in 2025, widening addressable demand among mid-market firms. A 10-year tax holiday on data-center income for sites above 20 megawatts further secures future build phases.

SME Digital-Tax Incentives and Matching Grants

SMEs, representing 97.4% of businesses, grapple with upfront ICT costs yet benefit from matching grants up to RM 5,000, a 200% tax deduction on qualified spend, and six-month cloud-credit pilots from Microsoft. Collectively, these incentives cut net digital-transformation outlays by almost one-quarter. As subscription models spread, monthly price points below RM 500 enable micro-enterprises to onboard e-commerce platforms, accounting suites, and CRM tools. Uptake concentrates in Selangor, Penang, and Johor, where broadband penetration and digital-payment adoption outpace the national mean. Increased SME participation broadens the total contract value pool for SaaS vendors and managed service providers.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High SME digitalization costs | -0.8% | National, acute in Sabah, Sarawak, rural Peninsular states | Medium term (2-4 years) |

| Acute cyber-security skills shortage | -0.6% | National, most severe in Klang Valley, Penang, Johor | Long term (≥ 4 years) |

| Proposed USP-Fund levy on cloud providers | -0.3% | National, impacts enterprises using public cloud | Short term (≤ 2 years) |

| Power and water-supply limits in Johor | -0.4% | Regional, Johor with spillover to Selangor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High SME Digitalization Costs

Average upfront investment of RM 80,000 for a basic ERP, e-commerce, and cybersecurity bundle surpasses the annual IT budget of 62% of micro-enterprises. Matching grants reached fewer than 1% of eligible firms in 2025 because of complex applications and co-funding obligations. While subscription pricing eases capital strain, recurring fees still weigh on cash flow in sectors with razor-thin margins. Limited collateral restricts bank lending, forcing entrepreneurs to rely on retained earnings. The 200% tax deduction unveiled in Budget 2026 should improve affordability, yet bureaucratic processing may delay the tangible impact to 2027.

Acute Cyber-Security Skills Shortage

Malaysia lacked 15,000–20,000 qualified cybersecurity professionals in 2025, equivalent to 40% of demand. Median salaries of RM 120,000–RM 180,000 price out many mid-sized enterprises and public agencies. Universities graduated only 2,500 specialists in 2025, leaving a persistent gap that on-the-job training cannot quickly close. High certification costs and limited training seats constrain pipeline growth, although a new subsidized talent program targets 5,000 participants over three years. Outsourcing to managed security-service providers partly offsets staffing deficits but shifts spending patterns toward services rather than security products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Security Spending Outpaces Legacy Infrastructure

The IT Security segment accounted for the fastest expansion, logging a 10.99% CAGR through 2031, while Communication Services retained the largest 28.70% slice of 2025 revenue. This surge arises from 1,200 ransomware incidents recorded in 2024, which compelled enterprises to roll out zero-trust frameworks and endpoint detection suites. Malaysian telcos monetized 5G by bundling managed SD-WAN, driving cross-sell of network-access control appliances. Simultaneously, the Malaysia ICT market size for traditional on-premise servers contracted as hyperscale cloud options became cost-competitive, a pivot evidenced by declining x86 shipments.

Over the outlook period, firewall refreshes, identity governance, and security information and event management platforms capture incremental share, while voice and data traffic shift from 4G to 5G stand-alone cores. Vendors focused on artificial-intelligence-driven threat detection benefit from government breach-notification rules that fine tardy disclosures. Managed detection and response providers win deals from mid-market banks that cannot afford in-house security operations centers. Consequently, IT Services revenue rises in tandem, supporting a broader Malaysia ICT market expansion trajectory.

By End-User Enterprise Size: SMEs Narrow the Digital Divide

Large Enterprises comprised 58.20% of outlays in 2025, yet their growth moderates to 7.80% as digital-maturity plateaus. Conversely, SME spending tracks an 8.10% CAGR, reflecting strong policy support and subscription affordability. Hardware refresh delays within corporate data centers also redirect budgets toward managed services and application modernization.

Grants, cloud credits, and fiscal deductions shrink onboarding costs, encouraging micro-retailers to deploy online storefronts and cloud POS modules. Financial institutions align product bundles—such as embedded financing—around digitalized SMEs, further broadening ICT demand. As a result, the Malaysia ICT market share held by SMEs inches upward each year, signaling a gradual rebalancing of customer concentration.

By Deployment Model: Hybrid Architectures Balance Sovereignty and Agility

Cloud deployment captured 47.65% spending in 2025 and expands at an 8.40% CAGR as compliant local regions come online. Sensitive government and BFSI workloads migrate once providers prove ISO 27001 adherence and local data residency. Hybrid configurations remain crucial for factories requiring sub-10-millisecond response times, thus edge nodes coexist with centralized analytics hosted in the cloud.

On-premise investments focus on refresh cycles and regulatory mandates, but their share slips as software publishers discontinue perpetual licenses. Kubernetes orchestration underpins workload portability, reducing vendor lock-in. Collectively, these trends sustain persistent double-digit growth in cloud consumption, anchoring the broader Malaysia ICT market.

By End-User Industry Vertical: Gaming Disrupts Traditional Hierarchies

Manufacturing and Industry 4.0 retained the largest 19.30% slice in 2025, fueled by smart-factory incentives and private 5G pilots. BFSI modernization projects, including core-banking overhauls valued at more than RM 450 million, keep financial services the second-largest buyer group.

Gaming and Esports, however, posts the fastest 11.30% CAGR, underwritten by government tournament funding and Kuala Lumpur’s emergence as an event hub. Retail logistics rollouts of AI robots and demand-forecasting engines accelerate warehouse automation budgets. Healthcare spends aggressively on electronic health records ahead of a 2026 compliance deadline, while oil and gas outfits deploy digital twins on offshore rigs. These combined dynamics diversify revenue streams and reinforce the resilience of the Malaysia ICT market.

Geography Analysis

The Klang Valley cluster, embracing Kuala Lumpur, Selangor, and Putrajaya, generated roughly 55% to 60% of 2025 outlays, buoyed by federal agencies and hyperscale zones in Cyberjaya. Johor followed with 12% to 15%, leveraging Iskandar Malaysia’s incentives and cross-border proximity to Singapore. Penang contributed close to 10%, where semiconductor plants upgraded to private 5G and edge compute for real-time quality control.

Sabah and Sarawak collectively supplied another 8% to 10% yet posted the swiftest 9.5%–10.5% growth rates, thanks to fiber rollouts aimed at doubling penetration by 2027. Kedah’s preferential RM 0.28 per-kilowatt-hour tariff attracted GPU cluster operators into its technology park, spawning an AI micro-ecosystem. Power constraints in Johor risk pushing some builds to Selangor, which maintains a 500-megawatt surplus.

Mid-tier cities such as Ipoh, Kuching, and Kota Kinabalu offer untapped bandwidth, prompting state digital kiosk pilots to close last-mile gaps. Rural districts in Perlis, Pahang, and Terengganu lag with 25%–30% fiber coverage, but public Wi-Fi kiosks deployed in 2025 begin to bridge the divide, creating incremental pockets of Malaysia ICT market demand.

Competitive Landscape

Moderate fragmentation defines the competitive topology: the five largest players together control near 40% revenue, leaving meaningful white space for specialist integrators and SaaS disruptors. Telekom Malaysia’s March 2025 purchase of a 30% cybersecurity stake strengthens its managed-security bundling, countering CelcomDigi’s aggressive 5G enterprise push. Microsoft Malaysia’s USD 2.2 billion data-center campus secures a five-year Azure deal with the Ministry of Finance, highlighting hyperscalers’ ability to convert capex into anchor contracts.

AWS, Google Cloud, Oracle, and Huawei Cloud compete on sovereign-residency assurances, while TIME dotCom’s 10-gigabit symmetric broadband undercuts incumbents by up to 25%, capturing media-production studios and fintech startups. Ericsson’s multi-access edge compute nodes, deployed with CelcomDigi in Penang and Johor, illustrate vendor-led ecosystem creation around latency-sensitive manufacturing workloads[3]Source: Ericsson Malaysia, “Multi-Access Edge Compute Deployment,” ericsson.com.

Original Intelligence, financed with RM 120 million in January 2025, builds Bahasa Malaysia large-language models, aiming to embed local context into government and education applications. Managed service providers such as Accenture, TCS, Wipro, and IBM scale domestic headcount to accommodate cloud migrations, cybersecurity outsourcing, and AI data-labeling contracts. Compliance with ISO 27001 and the Personal Data Protection Act’s 72-hour breach rule remains a table-stakes differentiator across BFSI and public-sector tenders.

Malaysia ICT Industry Leaders

Accenture plc

Amazon Web Services Malaysia Sdn Bhd

CelcomDigi Berhad

Cisco Systems (Malaysia) Sdn Bhd

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Google Cloud Malaysia commenced commercial operations of its Kuala Lumpur region, adding Vertex AI and BigQuery to the local catalog.

- December 2025: U Mobile reached 2,000 5G base stations six months ahead of schedule, attaining 42% population coverage.

- October 2025: Microsoft Malaysia expanded its Cyberjaya campus with a third data-center building, introducing Azure OpenAI Service and Azure Quantum.

- September 2025: Oracle announced a USD 1.0 billion Johor cloud region slated for Q3 2027 commissioning.

Malaysia ICT Market Report Scope

The market is defined by the revenue accrued through the sale of ICT offerings, including IT hardware, IT software, IT services, IT infrastructure/data centers, IT security/cybersecurity, and communication services that are being used in various end-user industries across Malaysia.

The Malaysia ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security, and Communication Services), End-User Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Deployment Model (On-premise, Cloud, and Hybrid), and End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, and Gaming and Esports). Market Forecasts are Provided in Terms of Value (USD).

By Products Type

| IT Hardware |

| IT Software |

| IT Services |

| IT Infrastructure |

| IT Security |

| Communication Services |

By End-User Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By Deployment Model

| On-premise |

| Cloud |

| Hybrid |

By End-User Industry Vertical

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Other Verticals |

| By Products Type | IT Hardware |

| IT Software | |

| IT Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services | |

| By End-User Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Deployment Model | On-premise |

| Cloud | |

| Hybrid | |

| By End-User Industry Vertical | Government and Public Administration |

| BFSI | |

| Energy and Utilities | |

| Retail, E-commerce and Logistics | |

| Manufacturing and Industry 4.0 | |

| Healthcare and Life Sciences | |

| Oil and Gas (Up-, Mid-, Down-stream) | |

| Gaming and Esports | |

| Other Verticals |

Key Questions Answered in the Report

What is the projected value of the Malaysia ICT market by 2031?

The market is forecast to reach USD 45.50 billion by 2031.

How fast is cloud deployment growing in Malaysia’s ICT sector?

Cloud spending is expanding at an 8.40% CAGR between 2026 and 2031.

Which product category is growing the quickest?

IT Security records the fastest growth, advancing at a 10.99% CAGR to 2031.

Why is Gaming and Esports considered a high-growth vertical?

Government funding, national tournament hosting, and a large online audience drive an 11.30% CAGR for Gaming and Esports.

Page last updated on: