Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

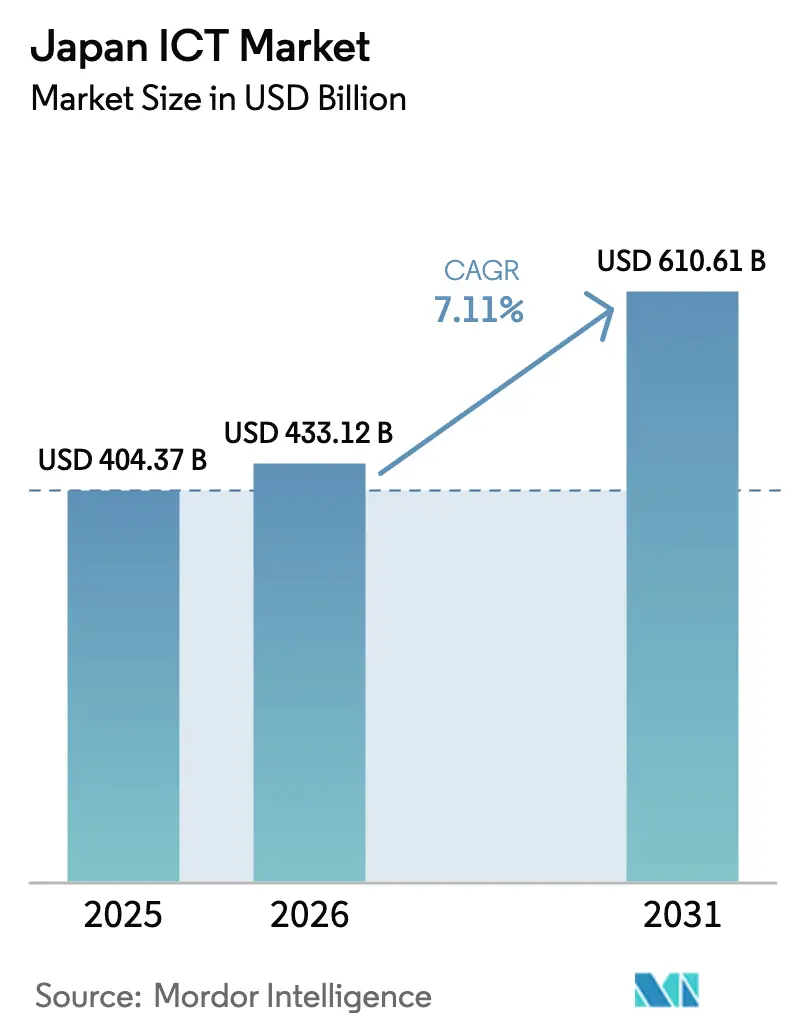

| Base Year Market Size (2025) | USD 404.37 Billion |

| Market Size (2026) | USD 433.12 Billion |

| Market Size (2031) | USD 610.61 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan ICT Market Analysis by Mordor Intelligence

Japan ICT market size in 2026 is estimated at USD 433.12 billion, growing from 2025 value of USD 404.37 billion with 2031 projections showing USD 610.61 billion, growing at 7.11% CAGR over 2026-2031.[1]Brad Smith, “Microsoft to Spend USD 2.9 Billion on Japanese Data Centers,” Data Center Dynamics, datacenterdynamics.com Enterprise commitments to modernize legacy mainframe estates before the “2025 cliff,” combined with Society 5.0 policy initiatives, are accelerating spending on hybrid cloud, AI infrastructure, and cybersecurity solutions.[2]IBM Japan Press Desk, “SCSK and IBM Japan Sign Strategic Partnership for Hybrid Cloud,” ibm.com Hyperscaler region build-outs exceeding USD 17.9 billion since 2024 are expanding domestic data-center capacity and creating multiplier effects for software, networking, and managed services demand Shrinking working-age population is intensifying automation investments, while ISMAP certification is reshaping procurement by favoring providers that meet more than 1,000 detailed security controls.[3] “List of ISMS Cloud Security Certified Organizations,” ISMS Accreditation Center, isms.jp Despite robust growth, the Japan ICT market faces structural challenges from an acute shortage of cloud and AI professionals, an expanding cyber-attack surface, and a widening digital trade deficit that highlights continued dependency on overseas platforms.

Key Report Takeaways

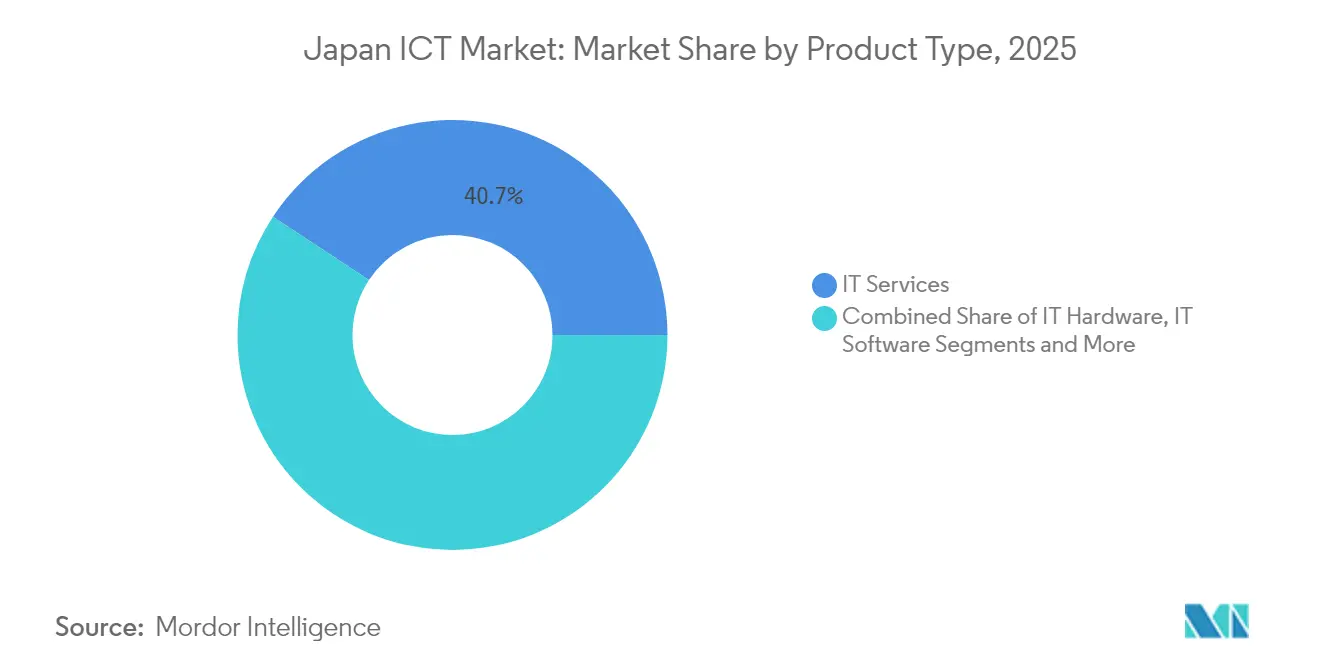

- By product type, IT Services captured 40.73% of Japan ICT market share in 2025, while Cloud Services is set to grow at a 7.78% CAGR through 2031.

- By enterprise size, large enterprises commanded 65.12% share of the Japan ICT market size in 2025; small and medium enterprises are advancing at a 7.51% CAGR through 2031.

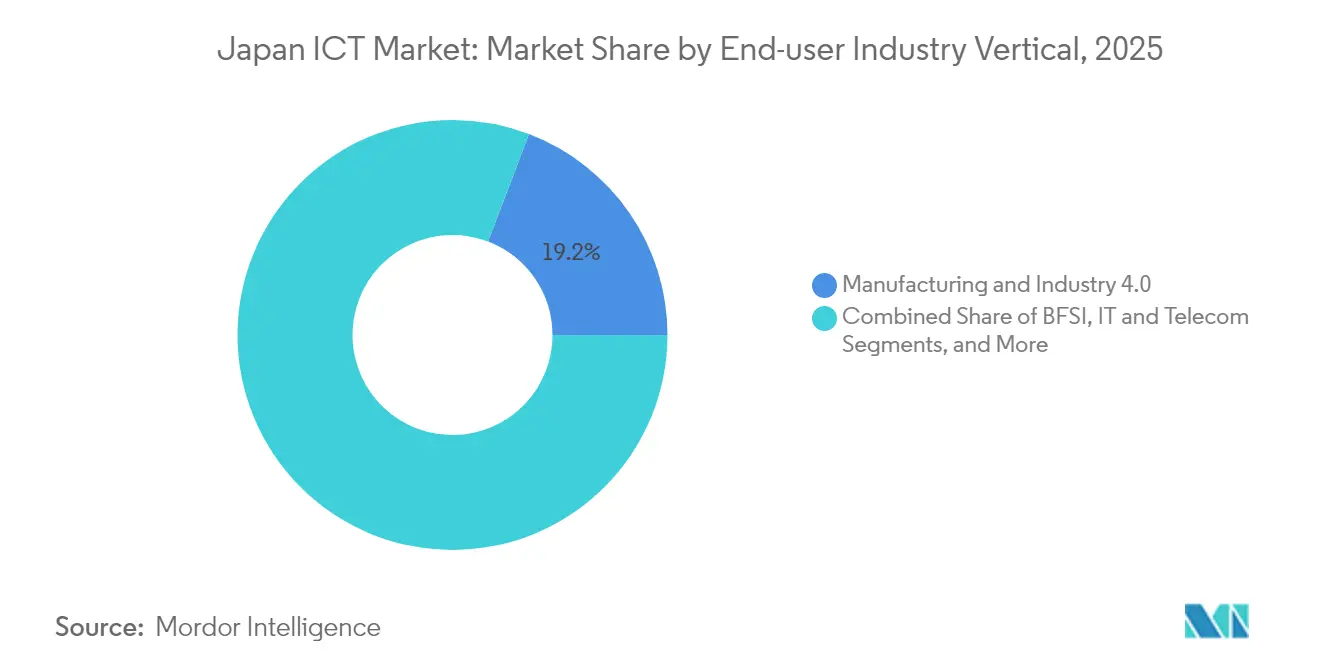

- By end-user vertical, manufacturing held 19.21% Japan ICT market share in 2025; healthcare and life sciences is forecast to grow at an 8.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating DX spending by large enterprises | +1.8% | Tokyo, Osaka, Nagoya metro areas | Medium term (2-4 years) |

| Hyperscaler CAPEX surge and local region build-outs | +1.5% | Kansai and Kyushu for new data-center clusters | Short term (≤ 2 years) |

| Government Cloud program boosting public-sector IT | +1.2% | Nationwide, central agencies and municipalities | Medium term (2-4 years) |

| AI-enabled SaaS adoption in underserved SMB segment | +0.9% | Urban centers with dense SME bases | Long term (≥ 4 years) |

| Semiconductor-equipment investments for AI infrastructure | +0.7% | Kumamoto, Hokkaido, broader APAC supply chain | Long term (≥ 4 years) |

| Workforce-automation demand amid aging demographics | +0.6% | Manufacturing regions and logistics corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating DX Spending by Large Enterprises

Large corporations are raising IT budgets to mitigate the “2025 cliff,” with 78% of major firms planning to double spend by 2026 as legacy systems reach end-of-life. METI estimates that economic losses could reach JPY 12 trillion (USD 0.08 trillion) per year if modernization lags, prompting rapid uptake of mainframe-to-cloud migration services. Panasonic’s COBOL-to-Java conversion has already saved tens of billions of yen in operating costs, demonstrating tangible ROI. Financial institutions lead demand, representing a JPY 500 billion (USD 3.38 billion) opportunity for legacy system transformation. Systems integrators and cloud providers alike are bundling assessment, re-platforming, and managed services into multi-year contracts that lock in recurring revenue.

Hyperscaler CAPEX Surge and Local Region Build-Outs

Microsoft, AWS, and Google Cloud have collectively earmarked more than USD 18 billion for new Japanese regions through 2025, adding power-dense campuses in Osaka, Fukuoka, and Hokkaido. SoftBank’s 400 MW AI facility and KDDI’s NVIDIA-powered center at the former Sharp Sakai site exemplify Japan’s push for local, low-latency compute that can train trillion-parameter models. These investments stimulate domestic supply chains for power, cooling, network interconnects, and professional services. Land-constrained metros are seeing creative brownfield conversions of idle industrial sites into tier-IV data centers, increasing region diversity and energy-efficiency standards.

Government Cloud Program Boosting Public-Sector IT

Japan’s Digital Agency mandates cloud-first procurement and enforces ISMAP accreditation, now totaling 702 certified services. Certification aligns more than 1,000 controls with ISO 27001 and NIST 800-53, setting a high security baseline. Local cloud provider Sakura Internet secured inclusion alongside global players, underscoring policy intent to balance sovereignty and innovation. Municipal DXSaaS platforms standardize back-office functions such as tax processing and resident services, shortening project lead-times. Private companies mirror ISMAP controls to streamline sales into public agencies, effectively expanding the compliant addressable market.

AI-Enabled SaaS Adoption in Underserved SMB Segment

SMEs benefit from SaaS platforms that embed GPT-based assistants for quoting, help-desk, and inventory tasks. TIS demonstrated 30% faster quotation cycles at Kyoei Sangyo after deploying its Generative AI Platform, reducing reliance on domain experts. No-code tools like CELF allow line-of-business staff to automate workflows without professional developers, slashing deployment timelines. Subscription pricing mitigates capex constraints typical of SMEs. Fintech startups exploit this accessibility to comply with FSA reporting rules, illustrating spillover effects into regulated verticals. Over time, SME cloud adoption is expected to narrow the productivity gap with large enterprises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of cloud/AI talent | -1.4% | Tokyo and Osaka tech corridors | Short term (≤ 2 years) |

| Intensifying cyber-attack surface and compliance costs | -0.8% | Nationwide, especially BFSI and critical infrastructure | Medium term (2-4 years) |

| Dependency on foreign software driving digital trade deficit | -0.6% | Nationwide, cross-industry | Medium term (2-4 years) |

| Legacy mainframe lock-in elevating modernization costs | -0.5% | Large enterprise hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Cloud/AI Talent

Japan may face a 400,000-to-800,000 engineer deficit by 2030, inflating salaries 40-60% above traditional IT roles and delaying project timelines. Legacy mainframe specialists over age 50 are in unprecedented demand for COBOL remediation, commanding multiple offers. Government reskilling grants and simplified “Specified Skilled Worker” visas aim to broaden the labor pool but will have limited near-term effect. Enterprises are offshoring niche tasks, yet language and security concerns restrict strategic workloads. This scarcity raises total cost of ownership and forces prioritization of high-ROI projects, tempering the overall Japan ICT market growth momentum.

Intensifying Cyber-Attack Surface and Compliance Costs

METI plans a corporate cybersecurity rating system that forces firms to report maturity metrics publicly, adding layers to ISO 27001 and sectoral mandates. Proliferation of IoT devices, 5G MEC nodes, and multicloud footprints widens threat exposure. BFSI and energy utilities must pursue zero-trust architectures and 24 × 7 SOC coverage, heightening operational expenses. Insurance premiums for cyber risk rose 34% year-over-year in 2024, eroding profit margins. While vendors gain revenue from defense spending, end-user capital is diverted from innovation to compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Maintain Scale While Cloud Accelerates

IT Services contributed 40.73% to Japan ICT market share in 2025, reflecting persistent reliance on systems integration and managed operations for mission-critical workloads. Cloud Services, powered by USD 17.9 billion hyperscaler CAPEX, is forecast to post an 7.78% CAGR, propelling the Japan ICT market size of this sub-segment from a 2025 base of USD 197.0 billion to USD 308.9 billion by 2031.

Systems integrators bundle application refactoring, data-center decommissioning, and ongoing governance, securing multi-year annuity revenue. Meanwhile, hardware demand clusters around AI-optimized GPUs and high-density rack power distribution. Domestic software publishers lag global peers, widening the digital trade deficit and reinforcing demand for SaaS imports. Communication Services leverage 5G Stand-Alone cores that enable network slicing, creating cross-sell opportunities for edge analytics. Cybersecurity vendors integrate zero-trust suites with observability platforms, delivering unified threat detection across hybrid estates.

By Enterprise Size: SMEs Pace Growth as Large Firms Lead Spend

Large enterprises held 65.12% of Japan ICT market share in 2025 and continue to fund large-scale DX programs designed to modernize COBOL estates and deploy AI governance tools. In contrast, SMEs are projected to grow at a 7.51% CAGR, adding USD 34.7 billion incremental spend by 2031 and lifting their contribution to 38.12% of incremental Japan ICT market size expansion.

The SME surge is catalyzed by subscription-based SaaS, governmental digital subsidies, and marketplaces that simplify procurement. Vendor go-to-market strategies include channel-first bundles pairing connectivity with productivity suites. Large enterprises centralize vendor panels to compress pricing and enforce ESG criteria. Both cohorts converge on managed security services to mitigate skills gaps, yet delivery models differ: SMEs leverage multi-tenant SOCs, while large firms fund dedicated fusion centers and red-team exercises.

By End-User Industry Vertical: Manufacturing Tops, Healthcare Accelerates

Manufacturing held 19.21% of Japan ICT market share in 2025, underwritten by Industry 4.0 upgrades such as AI-guided quality inspection and digital twins on advanced MES platforms. Healthcare and life sciences will register the highest 8.02% CAGR, supported by telemedicine reimbursement reforms and AI-assisted diagnostics for an aging population that will top 30% of citizens over 65 by 2030.

Government agencies expand adoption of municipality standard systems and digital resident ID platforms. BFSI institutions channel budgets to core banking modernization and open-API compliance, creating demand for microservices architectures. Gaming and esports, a nascent but fast-growing vertical, leverages edge compute and CDN optimization to deliver sub-50 ms latency for competitive play. Retail and logistics rely on AI-driven demand forecasting and autonomous last-mile delivery pilots, signalling multi-industry breadth of digitalization momentum.

Geography Analysis

Japan ICT market demand clusters in Tokyo’s Chiyoda, Minato, and Shibuya wards as well as Osaka’s Umeda district, where enterprise headquarters and carrier-neutral interconnect facilities concentrate network traffic. Regional governments aggressively court data-center investors with tax incentives, resulting in new campuses in Fukui, Mie, and Ibaraki Prefectures that diversify geographic risk and exploit renewable energy sources.

Rural revitalization programs harness 5G and satellite broadband to connect remote communities, allowing SMEs in Hokkaido dairy and Kyushu tourism to deploy cloud POS and AI chatbots. Hyperscaler edge zones in Sapporo, Hiroshima, and Sendai reduce round-trip latency for AI inference workloads to less than 20 ms, stimulating adoption of computer-vision-based smart-factory solutions.

National semiconductor hubs in Kumamoto and Hokkaido will attract ancillary ICT services from EDA software to clean-room automation. These technopoles create demand for high-performance computing clusters and secure OT-IT convergence solutions. Collectively, the geographic expansion ensures that the Japan ICT market continues to grow beyond the traditional Kanto–Kansai corridor, reinforcing nationwide digital resilience.

Competitive Landscape

Domestic systems integrators Fujitsu, NEC, and Hitachi command long-standing relationships with ministries and megabanks, yet face margin pressure as clients demand outcome-based pricing tied to KPI delivery. These incumbents forge alliances with AWS, Microsoft Azure, and Google Cloud to co-deliver hybrid solutions that protect legacy investments while offering cloud-native scalability. IBM Japan pivots to partner-centric sales, winning Oracle Cloud Applications Partner of the Year in 2024 and collaborating with SCSK to launch MF+ Hosting on IBM z16 mainframes.

Telecom operators NTT DATA, KDDI, and SoftBank leverage network footprints to bundle connectivity and edge services, vying for smart-factory and MEC contracts. SoftBank’s 750,000 m² Sakai AI data-center campus positions the firm as a domestic GPU cloud pioneer. Start-ups like FPT Smart Cloud Japan compete in niche GPU leasing, supported by SBI Holdings’ planned 35% stake that injects capital and enterprise channels.

Certification race under ISMAP governs public-sector eligibility; AvePoint, Google Cloud, and SAP achieved or renewed compliance in 2025. Vendors lacking accreditation face procurement barriers, intensifying rivalry to secure audits. The competitive arena values local data-sovereignty assurances, Japanese-language AI models, and long-term commitment to relationship management over pure pricing tactics.

Japan ICT Industry Leaders

Fujitsu Limited

Hitachi Ltd

IBM Japan Ltd

NEC Corporation

TIS Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: IBM and Tokyo Electron extended their semiconductor R&D collaboration for another five years, focusing on High-NA EUV and chiplet-based AI processors.

- March 2025: AvePoint Japan submitted ISMAP registration for its cloud management suite, positioning to serve local-government cloud migrations.

- March 2025: TIS signed an agreement with SCSK to resell CELF no-code tooling to financial-sector customers, advancing low-code automation adoption.

- January 2025: IBM Japan revamped its partner strategy to accelerate AI and hybrid-cloud deployments, prioritizing deeper co-creation with integrators.

Japan ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form.

The Japanese ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of the enterprise (small and medium enterprises and large enterprises), and industry vertical (BFSI, IT & telecom, government, retail, and e-commerce, manufacturing, and energy and utilities).

The market sizes and forecasts are provided in terms of value in USD million for all the above-mentioned segments.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Verticals | ||

Key Questions Answered in the Report

How large is the Japan ICT market in 2026?

It is valued at USD 433.12 billion in 2026 and is projected to grow at a 7.11% CAGR to USD 610.61 billion by 2031.

Which segment grows fastest inside Japan’s ICT sector?

Cloud Services shows the highest momentum, expanding at an 7.78% CAGR through 2031, propelled by hyperscaler investments and government cloud mandates.

What is driving SME technology adoption in Japan?

Affordable AI-enabled SaaS and no-code tools reduce entry barriers, allowing SMEs to automate processes and close productivity gaps.

What is ISMAP and why does it matter?

ISMAP is a government security certification that evaluates more than 1,000 controls; only certified cloud services can be procured by public agencies, influencing vendor selection across sectors.

How are talent shortages affecting ICT projects?

Limited availability of cloud and AI engineers inflates labor costs by up to 60% and forces companies to prioritize high-ROI initiatives or rely on managed services and offshore support.

Which region attracts the most data-center investments?

The Kansai region, particularly Osaka’s Sakai district, is emerging as a hotspot due to large brownfield sites, robust power infrastructure, and proximity to enterprise demand centers.

Page last updated on: