Industrial Cloud Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

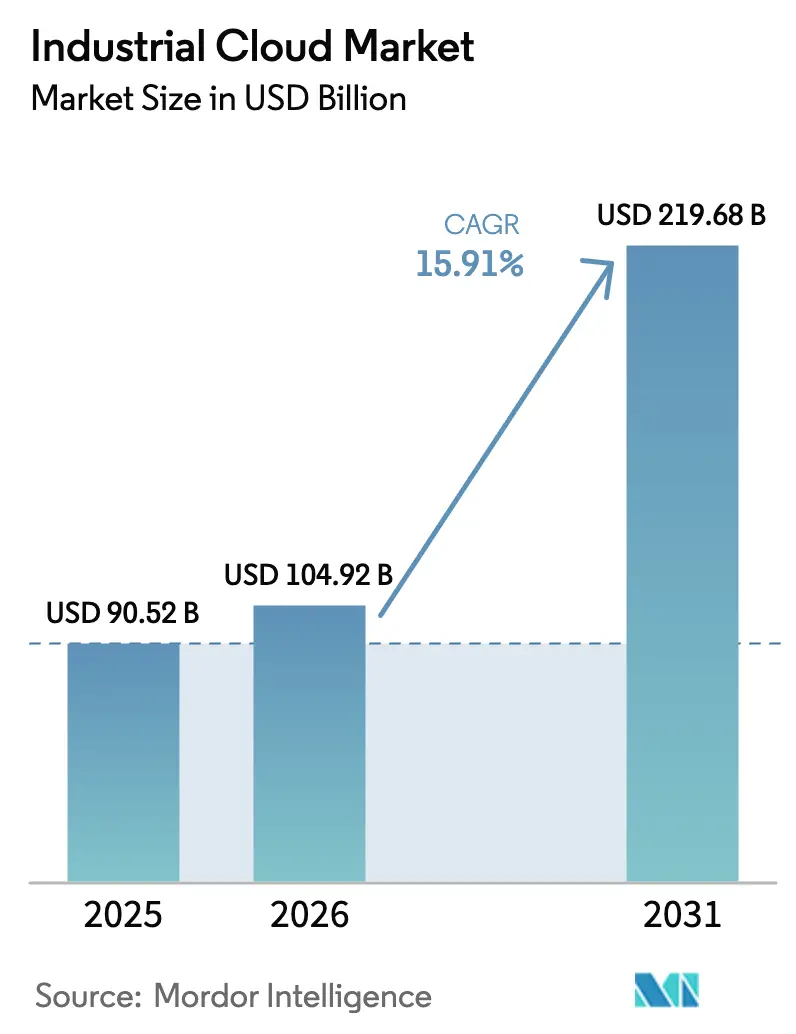

| Market Size (2026) | USD 104.92 Billion |

| Market Size (2031) | USD 219.68 Billion |

| Growth Rate (2026 - 2031) | 15.91% CAGR |

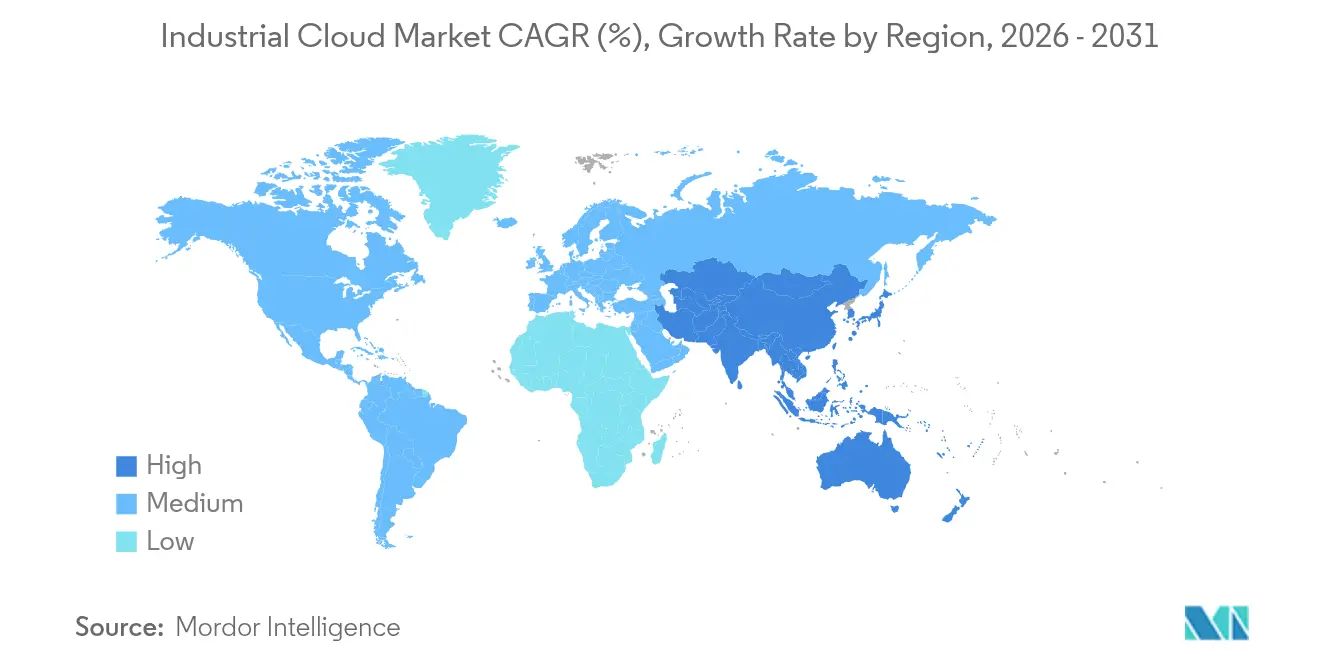

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Cloud Market Analysis by Mordor Intelligence

The industrial cloud market size was valued at USD 90.52 billion in 2025 and estimated to grow from USD 104.92 billion in 2026 to reach USD 219.68 billion by 2031, at a CAGR of 15.91% during the forecast period (2026-2031). Growth comes from manufacturers linking Industry 4.0 projects with post-pandemic operating resilience requirements, turning cloud infrastructure from a discretionary efficiency play into a core source of competitive edge. Sovereign cloud policies in the European Union, China and India are moving from concept to enforceable regulation, steering investment toward compliant architectures that still tap public-cloud economics. Simultaneously, edge-to-cloud convergence is bringing real-time analytics into brownfield plants, enabling uptime gains and energy savings that justify budget reallocations. On the supply side, hyperscalers and automation vendors are using acquisitions to embed operational-technology expertise into their platforms, while sustainability rules for data centers and multi-cloud procurement strategies temper the revenue concentration of any single provider.

Key Report Takeaways

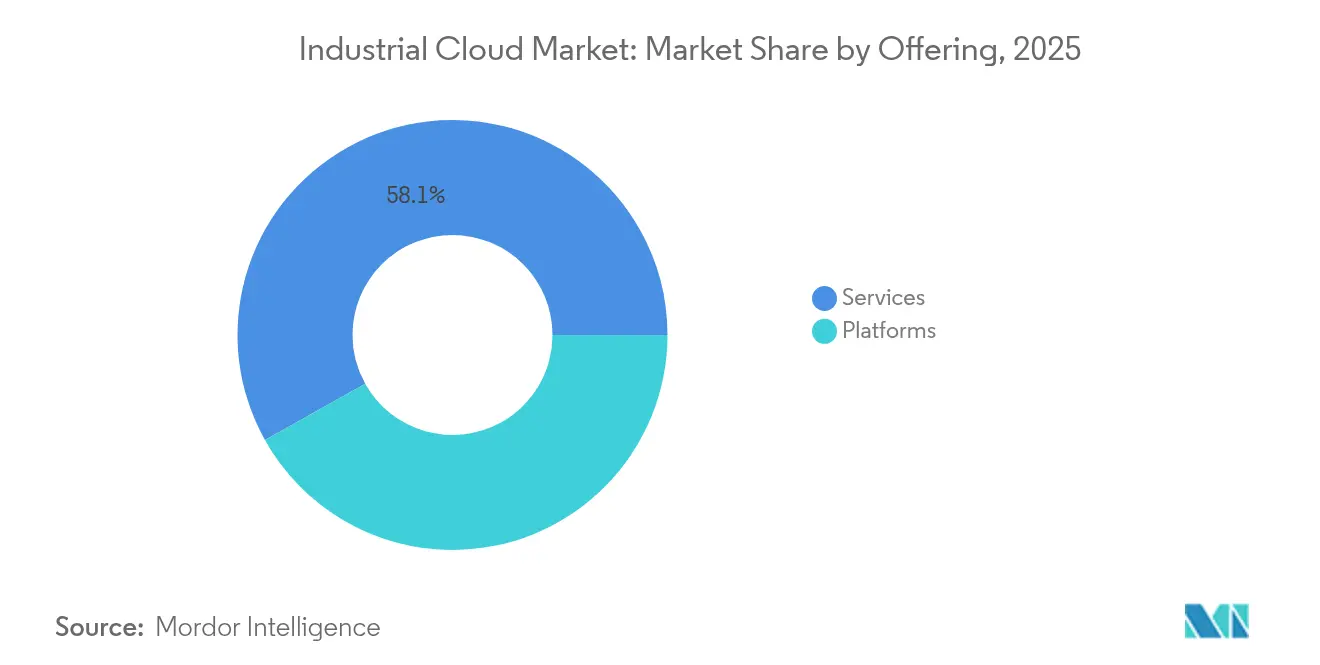

- By offering services, led with 58.12% of the industrial cloud market share in 2025, the segment is projected to climb at a 20.17% CAGR through 2031.

- By service model, PaaS is forecast to grow at 20.8% CAGR to 2031, while SaaS retained 46.55% revenue share of the industrial cloud market size in 2025.

- By deployment, the public cloud held 62.48% of the industrial cloud market in 2025, yet the private cloud is on course for a 18.54% CAGR through 2031.

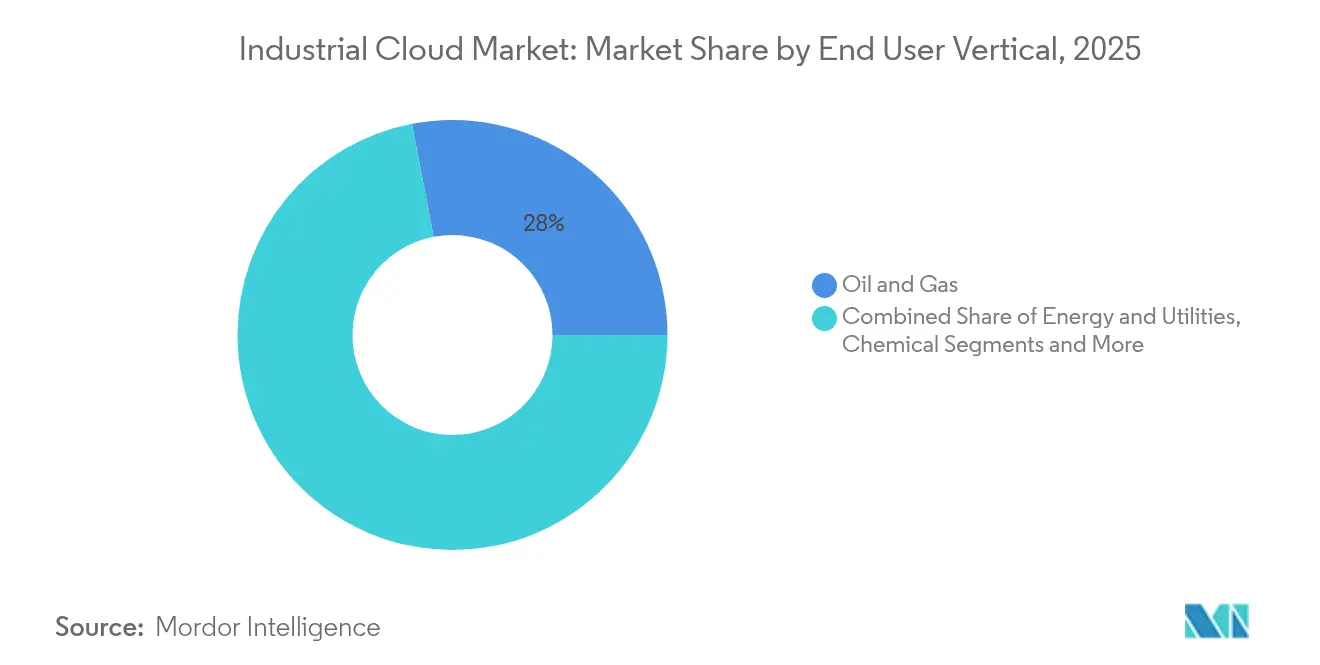

- By vertical, oil and gas commanded 28.02% of the industrial cloud market size in 2025, whereas pharmaceuticals are expected to expand at a 19.59% CAGR through 2031.

- By enterprise size, large enterprises accounted for 58.05% of adoption in 2025; SMEs are projected to grow at a 19.42% CAGR by 2031.

- By geography, North America held 48.35% revenue share in 2025, while Asia-Pacific is set to accelerate at 22.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of Industry 4.0 Initiatives | +3.2% | Global; early gains in Germany, Japan, South Korea | Medium term (2-4 years) |

| Cost-efficient Scalability of Cloud | +2.8% | Global, strong in North America and EU | Short term (≤ 2 years) |

| Remote Operations and Resilience Post-COVID-19 | +2.1% | Global; emphasis on APAC manufacturing hubs | Short term (≤ 2 years) |

| Sovereign/Regulated Industry-Cloud Frameworks | +1.9% | EU, China, India; spillover to MEA | Long term (≥ 4 years) |

| Vertical Cloud Marketplaces for OT Software | +1.5% | Core markets in North America and EU | Medium term (2-4 years) |

| Edge-to-Cloud Convergence in Brownfield Plants | +1.3% | APAC core; spill-over to Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of Industry 4.0 Initiatives

Manufacturing digitalization mandates are pushing enterprises to link cloud environments with shop-floor control systems, driving sustained demand for industrial-grade cloud platforms. Siemens generated EUR 75.9 billion revenue in 2024 with its Digital Industries division reporting accelerated orders for cloud-enabled manufacturing execution systems.[1]Siemens AG, “Annual Report 2024,” siemens.com Energy-efficiency directives in Germany and Japan now require digital twins that monitor resource consumption in real time, compelling plants to migrate operational data to the cloud. Early adopters are capturing productivity and quality gains that raise competitive thresholds and pressure lagging peers to fast-track migration. Automation vendors are lowering integration hurdles by shipping connector libraries that translate legacy PLC protocols into secure cloud APIs, opening brownfield footprints to cloud analytics without disruptive asset swaps.

Cost-efficient Scalability of Cloud

Economic volatility is pushing manufacturers toward variable-cost IT models. Oracle’s cloud-infrastructure revenue rose 52% in Q4 2024 to USD 15.9 billion, with a material share coming from industrial ERP migrations seeking elastic capacity for seasonal or launch-driven demand spikes.[2]Oracle Corporation, “Q4 2024 Earnings Press Release,” oracle.com Op-ex models avoid idle on-premises servers and leverage renewable-powered hyperscale data centers that cut both electricity bills and Scope 2 emissions. The value prop resonates with metals and mining firms that previously ran energy-intensive, batch-driven workloads on fixed infrastructure. SMEs gain proportionally more because cloud providers wrap best-practice security and HA configurations into pre-priced bundles that negate the need for in-house specialists.

Remote Operations and Resilience Post-COVID-19

Pandemic-era lockdowns revealed vulnerabilities in site-dependent operations and entrenched remote management as a core design principle. Hitachi committed more than USD 1.65 billion to AWS and Microsoft agreements that embed remote-monitoring capabilities into its industrial portfolio.[3]Hitachi Ltd., “Hitachi Expands Strategic Collaboration with AWS and Microsoft,” hitachi.com Manufacturers now deploy cloud-based video analytics and augmented reality support that let expert technicians diagnose equipment from thousands of miles away. The model protects revenue continuity during travel restrictions and reduces routine travel costs. For sectors such as oil and gas, where wells or pipelines are distributed across remote terrain, cloud connectivity pools scarce engineering talent and shortens mean time to resolution.

Sovereign/Regulated Industry-Cloud Frameworks

Data-sovereignty laws are reframing architecture choices. The European Union’s Digital Operational Resilience Act obliges critical infrastructure operators to prove that sensitive data stays inside approved jurisdictions. China’s Data Security Law mirrors the requirement and adds approval checkpoints for cross-border data transfers . Industrial cloud vendors are answering with sovereign regions that run under separate legal entities, paired with control planes that let customers anchor sensitive workloads on-premises while bursting non-critical analytics to public instances. Energy, telecom and defense contractors move first, but spill-over demand is already evident in pharmaceuticals seeking global batch-record visibility without breaching local storage mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and Compliance Concerns | -2.4% | Global; stringent in EU and China | Medium term (2-4 years) |

| Lack of IT Infrastructure in Developing Regions | -1.8% | Sub-Saharan Africa, parts of Latin America, rural Asia | Long term (≥ 4 years) |

| Carbon-Footprint Limits on Hyperscale DCs | -1.2% | EU, California; emerging in APAC | Long term (≥ 4 years) |

| Vendor Lock-in Fears for Proprietary Clouds | -1.6% | Global; amplified in enterprise segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-security and Compliance Concerns

Attackers are pivoting from IT systems to cloud-connected operational-technology assets, heightening risk awareness in boardrooms. IBM’s 2025 X-Force report highlights ransomware strikes that halted automotive and chemical production for multiple days, adding direct safety impacts to financial losses. Pharmaceutical and food-processing plants must prove that electronic records remain immutable throughout the product life-cycle, yet many cloud platforms still rely on shared-responsibility models that blur accountability. The skills gap compounds the issue because plant engineers seldom hold certifications in IAM or network segmentation. As a result, organizations delay certain migrations until reference architectures and managed services mature.

Vendor Lock-in Fears for Proprietary Clouds

Executives are wary of long-term dependencies on a single stack that may change terms mid-project. Google Cloud’s multi-cloud study cites 26-34% TCO savings when enterprises distribute workloads to the best-fit engine rather than commit exclusively to one provider. Beyond pricing, customers seek assurances that data schemas and APIs stay portable so that control systems with 20-year lifespans can outlive provider road-maps. Procurement teams now rank support for open standards and clear export tooling as top RFP criteria, slowing adoption of innovative but proprietary feature sets until exit strategies are clarified.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Drive Implementation Success

Services captured 58.12% of the industrial cloud market in 2025 as manufacturers turned to specialist partners to integrate cloud platforms with heterogeneous factory equipment. The segment is forecast to grow 20.17% annually to 2031, reinforcing how consulting, migration and managed services are prerequisites rather than optional add-ons. Service providers are building middleware that bridges 20-year-old PLCs with modern APIs, cutting deployment cycles from quarters to weeks and freeing plant staff for higher-value tasks. Platform revenue, although a smaller slice, carries better margins and funds RandD that pushes AI, digital twins and cybersecurity features deeper into the stack. Many vendors now bundle reference architectures that couple their platforms with certified services partners, reinforcing a flywheel where platform enhancements boost service revenue and vice versa.

By Service Model: PaaS Emerges as Growth Leader

Software-as-a-Service preserved 46.55% of 2025 revenue, yet Platform-as-a-Service is the fastest mover at 20.8% CAGR through 2031. Early wins in SaaS for ERP and CRM paved the runway for bespoke industrial apps built on low-code PaaS toolkits. Engineers can now configure predictive-maintenance dashboards or quality-inspection flows without deep coding skills, reducing backlog on corporate IT. Infrastructure-as-a-Service remains foundational, though margin pressure rises as hyperscalers battle on price. Differentiation shifts toward deterministic networking and time-sensitive workloads, traits that general-purpose clouds lack. The hierarchy shows maturation: once basic compute shifts are complete, value migrates to development platforms that host competitive IP.

By Deployment: Private Cloud Gains Momentum

Public instances still account for 62.48% of deployment, but private cloud is on a 18.54% growth trajectory through 2031 as compliance-heavy industries hedge sovereignty risk. Hybrid managers route telemetry and AI inference close to the line for latency reasons, then push aggregated insights to regional public zones for deep learning at scale. Edge appliances often carry built-in GPU acceleration, aligning with a trend where predictive control loops must close within milliseconds. The industrial cloud market benefits because hybrid orchestration increases overall consumption rather than cannibalizing one tier for another.

By End-user Vertical: Pharmaceuticals Accelerate Digital Transformation

Oil and gas maintained 28.02% share in 2025 due to the vast footprint of remote wells and pipelines that gain from cloud-based monitoring. Pharmaceutical plants, however, will grow 19.59% a year to 2031, lifted by electronic batch records, near-real-time quality analytics and collaborative RandD workspaces that handle sensitive clinical data. As regulators tighten serialization and traceability mandates, cloud platforms with pre-validated workflows reduce validation costs and accelerate time to market. Energy, chemicals and food processors keep steady momentum as they juggle efficiency gains with cyber-risk mitigation.

By Enterprise Size: SMEs Embrace Cloud Democratization

Large enterprises held 58.05% revenue in 2025 because they could fund multi-year, multi-platform transformations, yet SMEs are set to compound at 19.42% annually. Cloud vendors are releasing templated, pay-as-you-go blueprints that slot into common PLC brands and MES systems, removing the entry barrier of custom-coded connectors. For many SMEs, a single cloud-hosted quality module or inventory dashboard delivers immediate cash-flow impact, which then underwrites broader adoption.

Geography Analysis

North America led with 48.35% share owing to early Industry 4.0 rollouts and dense hyperscale regions. Asia-Pacific is forecast to grow 22.78% annually through 2031 as India and Vietnam commission new factories with cloud-native cells from day one. Governments in these markets link tax incentives to digital-twin adoption, locking in demand. Europe grows steadily under sustainability and sovereignty mandates, whereas Middle East and Africa and South America present upside tied to oil, mining and agriculture digitalization.

Competitive Landscape

The market sits in a moderate concentration zone. AWS, Microsoft Azure and Google Cloud hold material revenue shares, backed by global region counts, but face specialized competition from Siemens Industrial Edge, ABB Ability and Schneider Electric EcoStruxure that package domain know-how with cloud orchestration. Salesforce’s planned USD 8 billion acquisition of Informatica underscores the premium on integrating low-latency industrial data pipelines with enterprise applications. Nokia’s USD 2.3 billion purchase of Infinera brings coherent optical transport into its private-wireless and edge-cloud stack, vital for factory-to-cloud bandwidth.

Strategic moves cluster around three themes. First, sovereign cloud build-outs: hyperscalers are forming joint ventures with telecom incumbents to satisfy local-ownership rules. Second, AI accelerators: vendors bundle optimized silicon or managed model-training pipelines to lock in high-value workloads. Third, OT-IT fusion: automation providers acquire or partner with cloud teams to keep their installed bases from drifting to hyperscalers for analytics.

Industrial Cloud Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Alibaba Group Holding Limited

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce signed a definitive agreement to acquire Informatica for about USD 8 billion, adding data-integration and governance assets to its AI-centric CRM stack.

- January 2025: IBM acquired Applications Software Technology to deepen Oracle Cloud implementation skills for public-sector and regulated-industry clients.

- December 2024: Nokia closed its USD 2.3 billion purchase of Infinera, expanding optical-transport capacity for enterprise and webscale customers.

- July 2024: Nokia first announced the Infinera deal, targeting a 75% scale boost in optical networking and EUR 200 million(USD 471.16 million) in net operating-profit synergies by 2027.

Global Industrial Cloud Market Report Scope

Industrial cloud are cloud computing solutions specifically designed to meet the needs of a particular industry or sector. These are tailored to address specific industries' unique challenges, requirements, and regulatory constraints.

The industrial cloud market is segmented by component (platforms, services), by type (IaaS, PaaS, SaaS), by deployment (public cloud, private cloud, hybrid cloud), by end-user (oil and gas, energy and utilities, chemicals, food and beverages, pharmaceuticals, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Platforms |

| Services |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Public Cloud |

| Private Cloud |

| Oil and Gas |

| Energy and Utilities |

| Chemicals |

| Food and Beverages |

| Pharmaceuticals |

| Automotive and Transportation |

| Metals and Mining |

| Other Process and Discrete Industries |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Offering | Platforms | ||

| Services | |||

| By Service Model | Infrastructure-as-a-Service (IaaS) | ||

| Platform-as-a-Service (PaaS) | |||

| Software-as-a-Service (SaaS) | |||

| By Deployment | Public Cloud | ||

| Private Cloud | |||

| By End-user Vertical | Oil and Gas | ||

| Energy and Utilities | |||

| Chemicals | |||

| Food and Beverages | |||

| Pharmaceuticals | |||

| Automotive and Transportation | |||

| Metals and Mining | |||

| Other Process and Discrete Industries | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the industrial cloud market in 2026?

The industrial cloud market is valued at USD 104.92 billion in 2026 and is projected to reach USD 219.68 billion by 2031.

Which segment is growing the fastest in the industrial cloud market?

Platform-as-a-Service is expanding at a 20.8% CAGR through 2031, the highest among service models.

Why are pharmaceuticals adopting industrial cloud platforms quickly?

Regulatory mandates for electronic batch records and pressure to shorten drug-development cycles are driving a 19.59% CAGR in pharmaceutical cloud spending.

What role do sovereign cloud requirements play?

Data-sovereignty laws in the EU, China and India are accelerating hybrid and sovereign-cloud deployments that keep sensitive datasets within national borders while leveraging public-cloud elasticity.

Page last updated on: