Cloud API Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

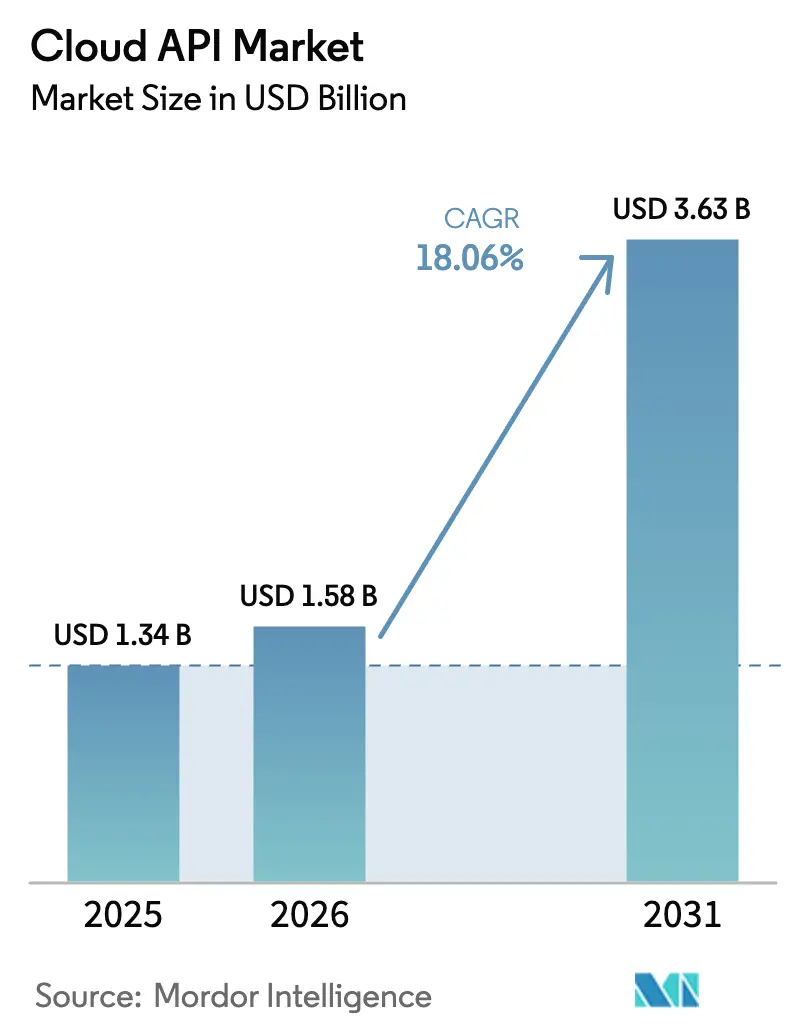

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 18.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud API Market Analysis by Mordor Intelligence

Cloud API market size in 2026 is estimated at USD 1.58 billion, growing from 2025 value of USD 1.34 billion with 2031 projections showing USD 3.63 billion, growing at 18.06% CAGR over 2026-2031. This sustained growth stems from corporate moves toward API-first architecture, the shift to serverless computing, and the monetisation of developer ecosystems. Enterprises now treat APIs as revenue drivers rather than integration utilities, so investment focuses on governance, low-latency performance, and data-sharing compliance. The Cloud API market also benefits from the spread of industry-specific standards such as PSD2 and FHIR, which formalise data interchange and open new service opportunities. At the same time, spending on API security, observability, and AI-enabled traffic management mitigates the rising breach costs tied to multi-vector attacks.

Key Report Takeaways

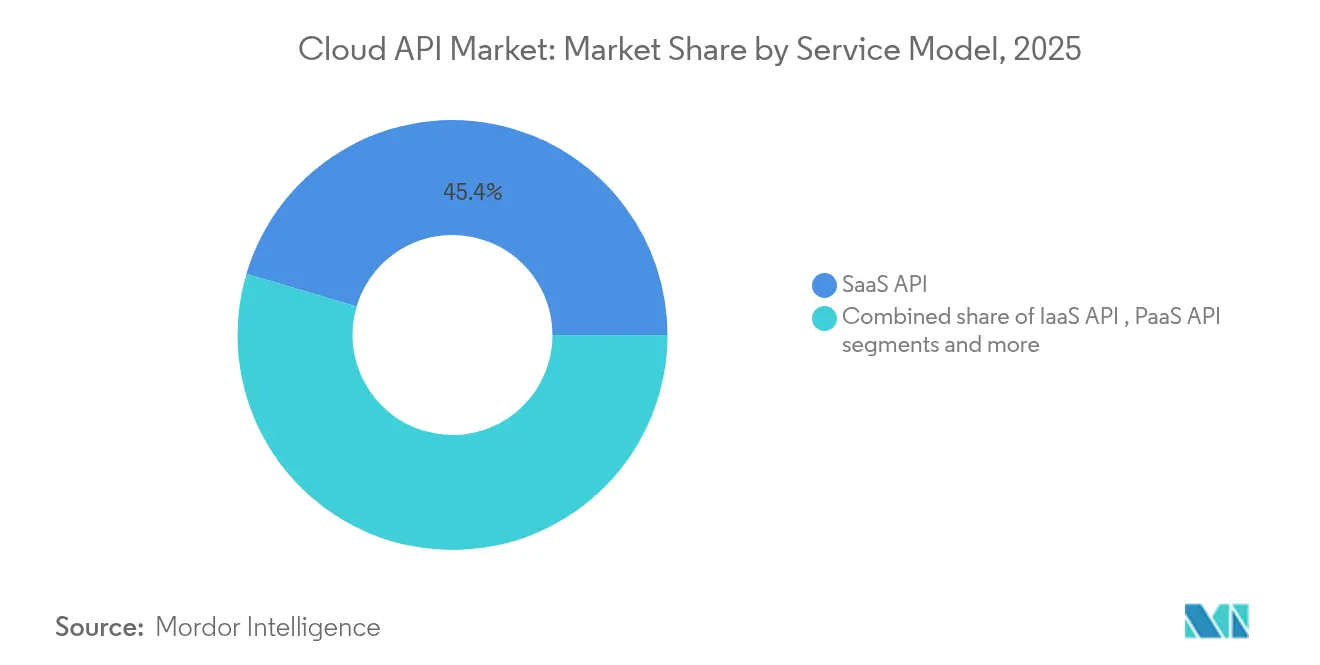

- By service model, SaaS APIs led with a 45.40% revenue share of the Cloud API market in 2025; Function-as-a-Service APIs are projected to expand at a 25.7% CAGR to 2031.

- By deployment model, public cloud retained 62.20% of the Cloud API market share in 2025, while hybrid and multicloud are advancing at a 22.9% CAGR through 2031.

- By enterprise size, large enterprises held 57.30% of the Cloud API market in 2025; small and medium-sized businesses record the fastest growth at 21.4% CAGR to 2031.

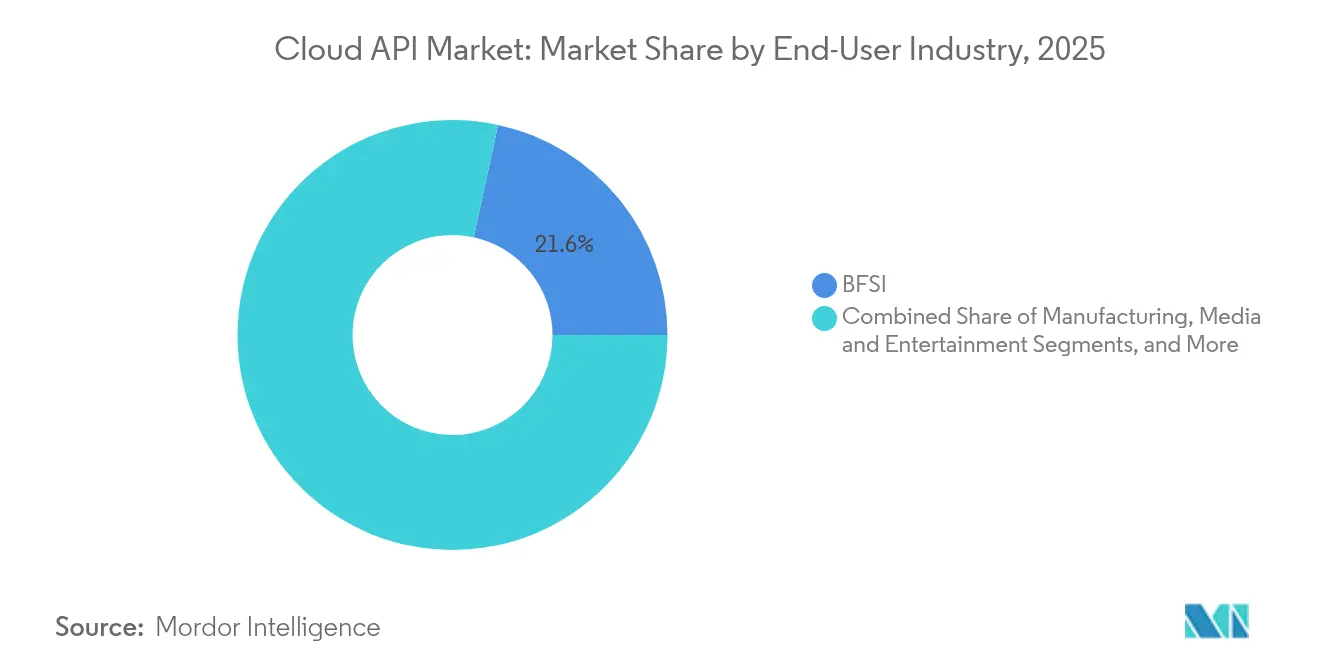

- By end-user industry, BFSI captured 21.60% of the Cloud API market size in 2025; healthcare and life sciences is rising at a 23.1% CAGR between 2026-2031.

- By API architecture, REST commanded 71.20% of the Cloud API market in 2025; GraphQL shows the highest projected CAGR at 26.8% through 2031.

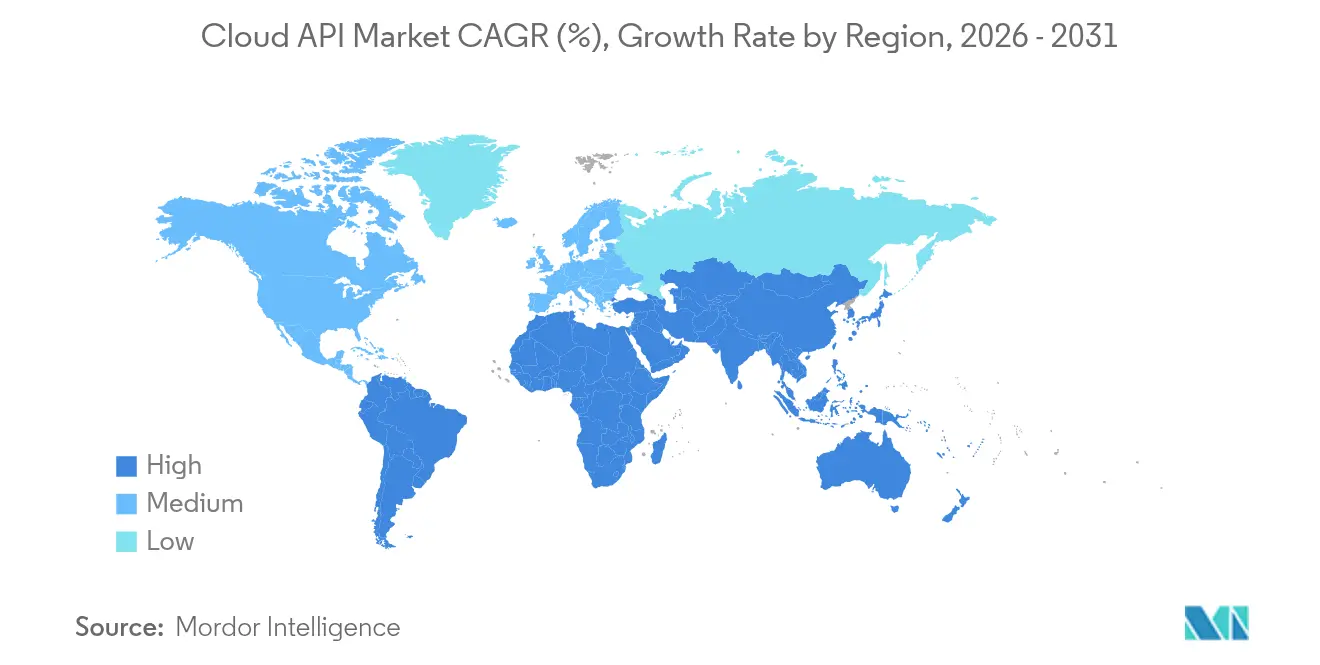

- By geography, North America led with 37.60% of the Cloud API market share in 2025; Asia-Pacific is set to post a 21.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud API Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native application boom among Global 2000 enterprises | 4.20% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid API-first adoption to accelerate DevOps velocity | 3.80% | Global, led by North America & APAC | Short term (≤ 2 years) |

| Serverless & event-driven architectures driving API call volumes | 3.10% | Global, with early adoption in North America | Medium term (2-4 years) |

| Rise of industry-specific data-sharing mandates (e.g., PSD2, FHIR) | 2.90% | Europe (PSD2), Global (FHIR), North America (healthcare) | Long term (≥ 4 years) |

| Monetisation of third-party developer ecosystems | 2.40% | Global, with focus on North America & Europe | Medium term (2-4 years) |

| Edge computing integration driving low-latency API requirements | 2.10% | Global, with early adoption in APAC & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-native Application Boom Among Global 2000 Enterprises

Modernisation now prioritises microservices, containers, and managed Kubernetes. Large corporations rebuild billing, risk, and supply-chain systems as composable services that expose well-governed APIs. Banks report plans to double external API exposure within three years, fuelling demand for high-throughput management gateways. Dedicated platform-engineering teams, combined with top-down governance boards, keep versioning discipline while maintaining developer autonomy. As a result, the Cloud API market gains predictable, subscription-based revenue from enterprises moving away from one-off integration projects. [1]5G Americas, “The Programmable 5G Network and API Ecosystem,” 5gamericas.org

Rapid API-first Adoption to Accelerate DevOps Velocity

API-first design locks interface contracts before coding starts, allowing front-end and back-end teams to work in parallel. This approach raises deployment frequency, reduces defect rates, and creates a single source of truth. Developer portals with automated documentation cut onboarding time, and low-code tooling extends participation to citizen developers. A growing portfolio of reference blueprints from hyperscale providers further institutionalises the practice, reinforcing the Cloud API market trajectory toward standardised, scalable pipelines. [2]CrowdStrike Holdings, “Strategic Partnership with Google Cloud for AI-Native Cybersecurity,” ir.crowdstrike.com

Serverless & Event-driven Architectures Driving API Call Volumes

Serverless functions spin up on demand, so applications issue many short-lived calls instead of fewer long-running sessions. Bursty traffic stresses rate-limiting policies and observability layers, driving sales of AI-assisted auto-scaling gateways. Mid-market firms pursuing hybrid AI strategies integrate on-prem inference with cloud training through APIs, raising traffic elasticity requirements. The result is a direct uplift in Cloud API market revenues tied to consumption-based billing models.

PSD2 obliges European banks to open payment data, while FHIR shapes healthcare interoperability worldwide. These mandates turn compliance into an innovation catalyst, prompting providers to launch new premium endpoints for partners. Standardisation also lowers integration costs, which accelerates pilot projects in emerging economies. Compliance deadlines extend into the next decade, offering a long-tail revenue stream for specialised vendors within the Cloud API market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-vector API security vulnerabilities & breach costs | -2.80% | Global, with heightened concern in North America & Europe | Short term (≤ 2 years) |

| Latency-sensitive workloads avoiding public clouds | -1.90% | Global, with particular impact in APAC manufacturing | Medium term (2-4 years) |

| Hidden egress fees & unpredictable cost governance | -1.60% | Global, with focus on North America & Europe | Short term (≤ 2 years) |

| Skills gap in multi-cloud API lifecycle management | -1.40% | Global, with acute shortages in APAC & MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Multi-vector API Security Vulnerabilities & Breach Costs

Attackers exploit token misconfiguration, business logic flaws, and third-party dependencies. Average breach costs now exceed USD 4.5 million, and insurers are tightening coverage terms. Platform providers respond with inline machine-learning threat detection and zero-trust token rotation. Yet the talent deficit in cloud security remains a constraint, especially for small teams. Persistent incidents temper adoption speed in highly regulated sectors and reduce near-term Cloud API market expansion.

Latency-sensitive Workloads Avoiding Public Clouds

Manufacturing control loops and high-frequency trading require sub-millisecond response times. Edge and private-5G roll-outs address part of the problem, but integration complexity rises as data spans core, edge, and device. Customers delay migration of ultra-critical workloads, limiting the immediate revenue pool for public endpoints. Vendors mitigate by distributing API gateways closer to the user and by adding QoS-aware routing. Still, performance concerns slow the broader Cloud API market adoption curve, particularly in APAC factories where wide-area network latency remains higher than in mature regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Model: FaaS APIs Accelerate Serverless Adoption

The Cloud API market size for SaaS integrations equalled USD 0.61 billion in 2025, equating to a 45.40% share. Enterprises rely on SaaS APIs to connect CRM, ERP, and collaboration suites. The Function-as-a-Service cluster increases at a 25.7% CAGR, the fastest within the Cloud API market. Developers value on-demand execution and granular billing, so serverless endpoints now underpin chatbots, streaming analytics, and AI inference. FaaS also reinforces event-driven patterns that decouple modules and shrink time-to-launch. IaaS and PaaS APIs remain essential for provisioning, but growth is slower because most infrastructure automation is already in place.

Serverless adoption changes cost models; teams pay for invocations, not idle capacity. Business leaders view this as financial agility, aligning opex with revenue cycles. Yet the operational shift to stateless design challenges legacy monitoring tools. Vendors answer with integrated observability, offering trace visualisation that scales to billions of calls. The competitive field thus tilts toward platforms bundling compute, storage, and API lifecycle management, which locks in customers and sustains the Cloud API market revenue stream.

By Deployment Model: Hybrid Strategies Balance Performance and Sovereignty

Public endpoints captured 62.20% of the Cloud API market share in 2025, thanks to hyperscale reach and mature ecosystems. Cost-effective regional PoPs support global rollouts, and pay-as-you-go models suit unpredictable traffic. Hybrid deployments rise 22.9% CAGR through 2031 as firms unite on-prem nodes with multiple clouds to satisfy latency targets and data-residency laws. Policy-driven routing tools and service meshes provide uniform security, so teams avoid rewriting business logic.

Private clouds remain critical for classified workloads and industrial automation. Telecom operators also house APIs within network cores to monetise 5G slices. Multicloud control planes, delivered as managed services, synchronise policy enforcement across domains. The Cloud API market therefore pivots to federation features such as unified discovery and cross-cloud quotas, enabling businesses to exploit best-of-breed components without vendor lock-in.

By Enterprise Size: SMBs Drive Democratization Through Low-code Platforms

Large corporations continued to dominate spending, accounting for 57.30% of the Cloud API market size in 2025. They possess complex legacy estates and regulatory obligations that demand robust, audit-ready gateways. However, low-code and no-code tools now lower adoption barriers, so SMBs expand at a 21.4% CAGR. Component marketplaces with drag-and-drop connectors reduce the need for deep development skills. Consumption-based pricing aligns with variable revenues, supporting use cases from digital retail to regional logistics.

As SMB adoption grows, platform vendors craft tiered offerings: self-serve portals for startups, guided onboarding for medium firms, and enterprise editions with SOC 2 certifications. This segmentation allows providers to capture the full value curve while keeping acquisition costs low. The influx of smaller customers diversifies the Cloud API market user base and drives community-led innovation.

By End-user Industry: Healthcare Transformation Accelerates FHIR Adoption

BFSI retained the top position with 21.60% of the Cloud API market share in 2025. Banks deploy open banking endpoints for account aggregation and real-time payments. Fintech partnerships rely on these APIs to differentiate through instant credit decisions. Healthcare and life sciences exhibit a 23.1% CAGR, the highest among industries, as providers roll out patient-facing apps, e-prescription services, and remote monitoring feeds. Standardised FHIR resources simplify cross-vendor data exchange, opening revenue opportunities for specialist integrators.

Manufacturers integrate digital twins and predictive maintenance analytics through edge-optimised APIs. Media firms embrace GraphQL to tailor content bundles and reduce mobile payload sizes. Telcos expose network APIs for SMS, location, and quality-on-demand, turning infrastructure into a service. In every vertical, compliance dictates architecture, so domain-specific accelerators gain traction and further enlarge the Cloud API market.

By API Architecture: GraphQL Gains Momentum in Data-intensive Applications

REST remained dominant with a 71.20% share in 2025 due to its simplicity and broad tooling. GraphQL, however, rises at a 26.8% CAGR, appealing to mobile and IoT developers who want precise data queries. Reduced round-trips lower battery consumption, a key advantage in endpoint-rich environments. gRPC serves internal microservice communication where binary protocols improve throughput. SOAP still underpins some legacy ERP links, particularly in heavily regulated industries.

Major commerce platforms migrating from REST to GraphQL report double-digit latency reductions and cleaner version control. Toolchains now auto-generate GraphQL schemas from domain models, boosting productivity. As a result, architecture choice becomes a competitive lever; firms that modernise quickly deliver richer experiences and capture customer loyalty, strengthening their position in the Cloud API market.

Geography Analysis

North America remained the largest regional contributor to the Cloud API market, posting a 37.60% revenue share in 2025. Enterprise maturity, vibrant startup ecosystems, and strong venture funding sustain demand. Legislative directives such as the US interoperability rule promote API-centric data flows in healthcare. Hyperscale providers maintain expansive partner networks, which reduces integration friction.

Europe follows, supported by PSD2 and consistent privacy enforcement. Financial institutions rolled out open banking endpoints ahead of schedule, and regulators now explore energy-sector data access. Digital-sovereignty discussions encourage in-region hosting, stimulating local-cloud partnerships. Vendors add region-locking features that comply with Schrems II, improving adoption among risk-averse corporates.

Asia-Pacific is the fastest-growing theatre, advancing at a 21.9% CAGR. China’s tech giants scale super-app ecosystems while India’s fintech scene embraces unified payment interface (UPI) APIs. Southeast Asian start-ups deploy lightweight gateways on regional cloud zones to serve cross-border e-commerce. Governments sponsor smart-city pilots that embed APIs into traffic, healthcare, and utility platforms, broadening the Cloud API market footprint.

The Middle East and Africa accelerate as 5G roll-outs create new monetisation routes from network APIs. UAE and Saudi Arabia anchor investments with national digital agendas. Latin America records steady expansion driven by Brazil’s open finance mandate and Argentina’s e-invoice requirements. Multinational providers often partner with in-country data-centre operators to navigate localisation laws. Collectively, these dynamics underline the global breadth of the Cloud API market and signal sustained multi-regional revenue streams.

Competitive Landscape

The Cloud API market shows moderate concentration. Amazon Web Services, Microsoft Azure, and Google Cloud Platform bundle compute, storage, and full-lifecycle API services within integrated consoles. Their scale advantages include multi-region latency control, embedded AI accelerators, and marketplace reach. Strategic acquisitions, such as Google’s Apigee and Microsoft’s GitHub, broaden developer engagement and lock in workloads.

Specialist vendors maintain defensible niches. MuleSoft excels at enterprise integration for complex hybrid estates. Kong focuses on lightweight, open-source gateways suited to cloud-native deployments. Postman dominates collaborative design and testing, embedding itself early in the development cycle. New entrants such as Zuplo target edge-optimised gateways for latency-critical use cases.

AI infusion defines recent differentiation. Platforms now incorporate machine-learning models to predict traffic spikes, recommend caching policies, and flag anomalous behaviour. Edge distribution also reshapes competition. Vendors place gateways on POPs and carrier networks, reducing round-trip times and enabling 5G-dependent applications. Nokia’s acquisition of Rapid demonstrates telecom ambition to monetise network exposure through standardised APIs, blending infrastructure and software competencies.

Consolidation continues as broader software suites seek API capabilities. Observability providers acquire gateway start-ups to add transaction visibility, while security firms embed runtime protection into design workflows. Although hyperscale clouds still command the largest share, the rich mix of specialists and open-source alternatives sustains innovation and prevents outright dominance in the Cloud API market.

Cloud API Industry Leaders

Amazon Web Services Inc.

Microsoft Corporation

Alphabet Inc.

Oracle Corporation

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cloudflare announced strategic partnerships with Asana, Atlassian, and PayPal to integrate Claude AI assistant capabilities through Cloudflare Workers and the Managed Component Protocol.

- March 2025: ServiceNow and Google Cloud expanded their partnership to deliver AI-powered tools to millions of users.

- February 2025: Nokia completed its acquisition of Rapid, the world’s largest API center, to strengthen software capabilities for 5G and 4G networks.

- January 2025: Dynatrace signed a new strategic collaboration agreement with Amazon Web Services to optimise digital enterprise operations.

Global Cloud API Market Report Scope

A cloud API (Application Programming Interface) comprises protocols, tools, and definitions that facilitate interaction between software applications and cloud services. By leveraging Cloud APIs, developers can seamlessly integrate a myriad of cloud-based services ranging from computing power and storage to machine learning and networking into their applications or systems.

The study tracks the revenue accrued through the sale of cloud APIs by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The cloud API Market is segmented by type (IaaS API, PaaS API, and SaaS API), enterprise size(small & medium enterprises, and large enterprises), end-user (BFSI, education, IT & telecom, manufacturing, media & entertainment, healthcare, and others), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| IaaS API |

| PaaS API |

| SaaS API |

| Function-as-a-Service (FaaS) API |

| Public Cloud |

| Private Cloud |

| Hybrid/Multicloud |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecommunications |

| Manufacturing |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Education |

| Others |

| REST |

| GraphQL |

| gRPC |

| SOAP and Legacy |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Service Model | IaaS API | |

| PaaS API | ||

| SaaS API | ||

| Function-as-a-Service (FaaS) API | ||

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid/Multicloud | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | |

| Information Technology and Telecommunications | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Education | ||

| Others | ||

| By API Architecture | REST | |

| GraphQL | ||

| gRPC | ||

| SOAP and Legacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Cloud API market?

The Cloud API market size is USD 1.58 billion in 2026 and is forecast to grow to USD 3.63 billion by 2031.

Which service model is expanding the fastest?

Function-as-a-Service APIs record a 25.7% CAGR because serverless execution aligns compute costs with bursty event traffic.

Why is Asia-Pacific the fastest-growing region?

Massive cloud infrastructure investment, fintech expansion, and government smart-city projects drive a 21.9% CAGR in the region.

How do regulatory mandates influence adoption?

Frameworks such as PSD2 and FHIR require standardised APIs, creating compliance demand while opening new revenue streams for data services.

What security challenges threaten growth?

Multi-vector attacks on poorly secured endpoints raise breach costs and necessitate AI-based runtime protection and zero-trust token governance.

Page last updated on: