Industrial Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

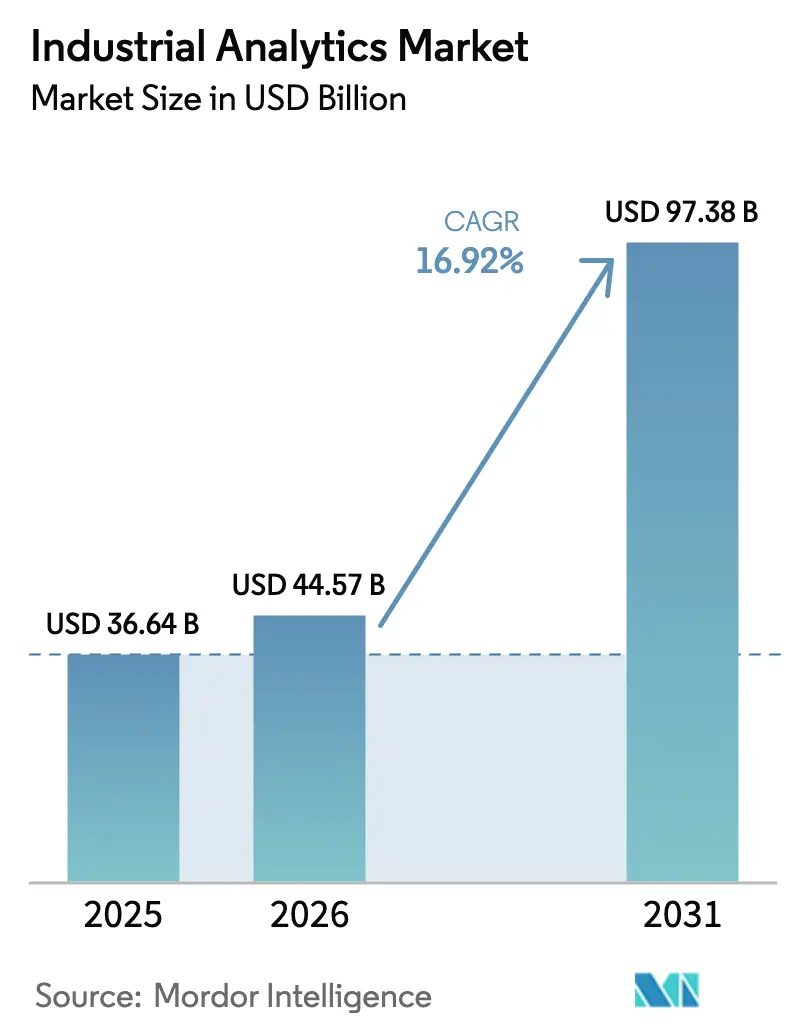

| Market Size (2026) | USD 44.57 Billion |

| Market Size (2031) | USD 97.38 Billion |

| Growth Rate (2026 - 2031) | 16.92% CAGR |

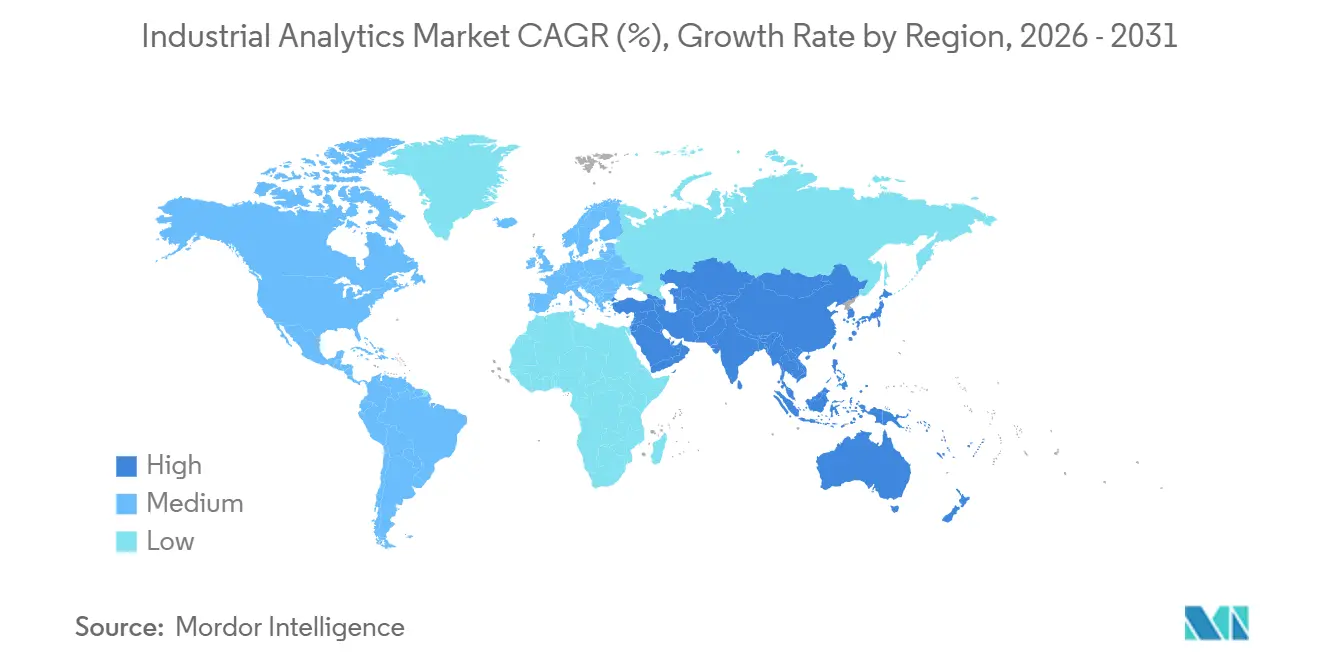

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

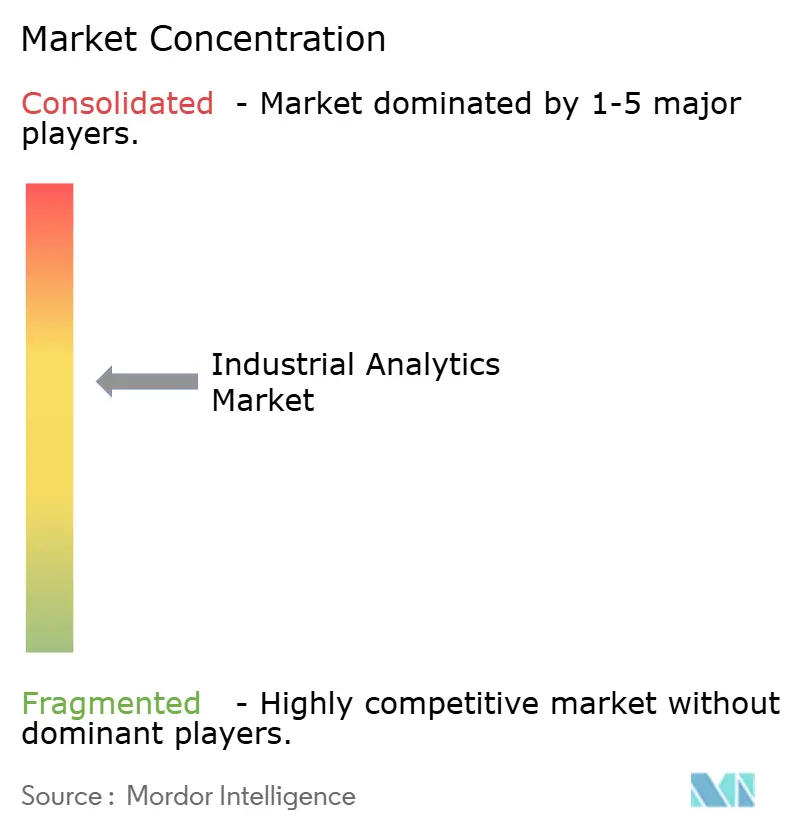

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Analytics Market Analysis by Mordor Intelligence

The industrial analytics market size was valued at USD 36.64 billion in 2025 and is estimated to grow from USD 44.57 billion in 2026 to reach USD 97.38 billion by 2031, at a CAGR of 16.92% during the forecast period (2026-2031). The rising demand for real-time optimization, growing edge-to-cloud connectivity, and escalating sustainability regulations are the primary drivers behind this expansion. Vendors are embedding prescriptive intelligence directly into automation layers, allowing operators to act on insights within milliseconds. A steady migration toward hybrid architectures, where low-latency workloads run on-site and model retraining occurs in the cloud, underpins long-term growth. Heightened cyber-physical threats, talent shortages, and data-sovereignty mandates temper the outlook but do not alter the upward trajectory of the industrial analytics market.

Key Report Takeaways

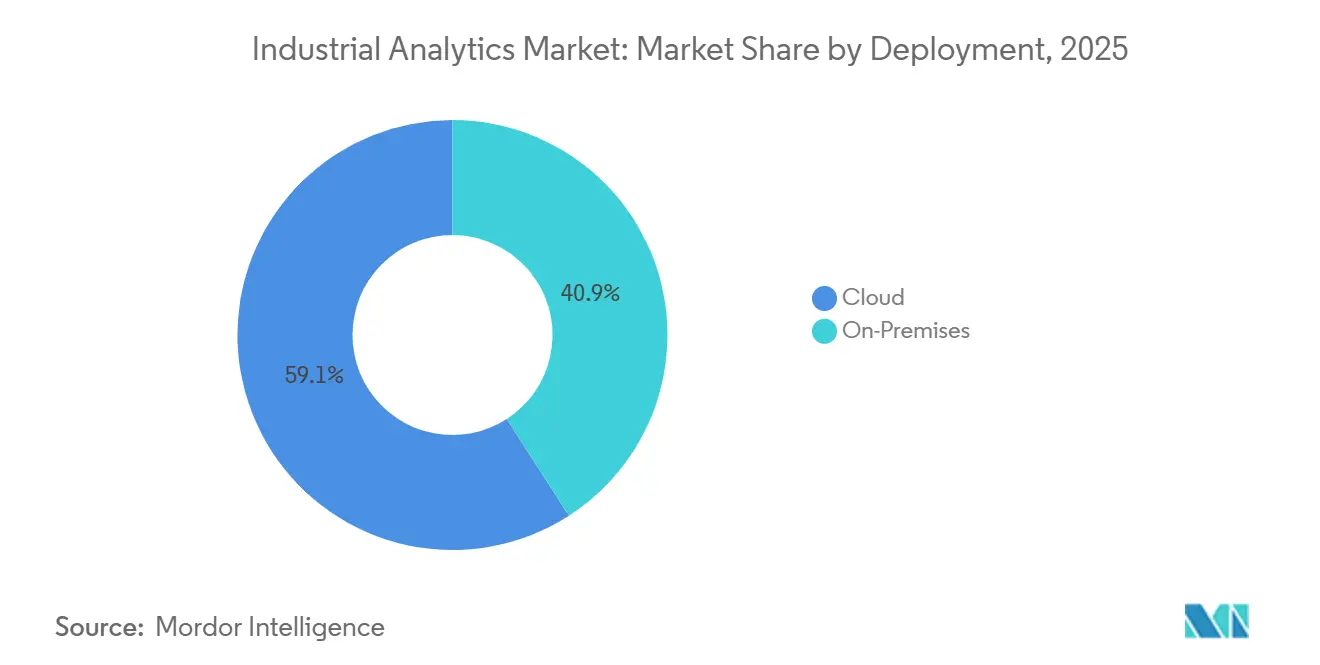

- By deployment, cloud led with 59.12% revenue share in 2025 and is projected to advance at a 17.09% CAGR through 2031.

- By component, software captured 62.34% share in 2025, whereas services are forecast to expand at a 17.21% CAGR to 2031.

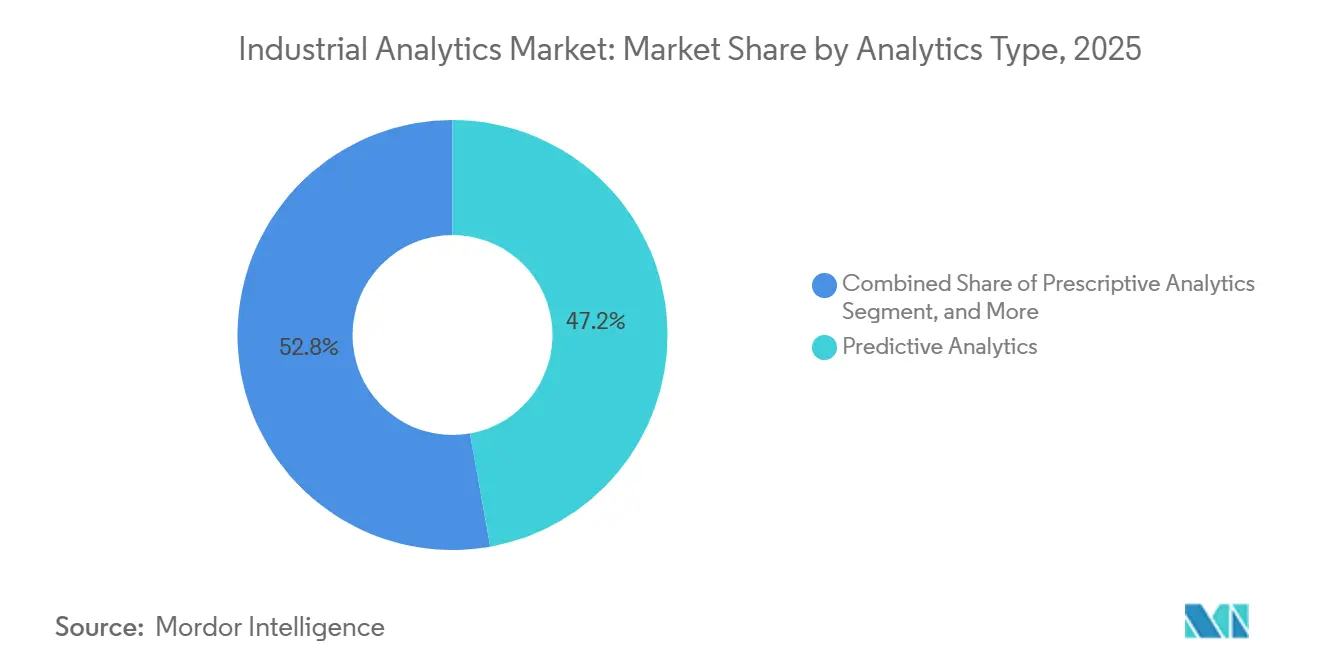

- By analytics type, predictive analytics accounted for 47.19% revenue in 2025, while prescriptive analytics is poised to grow at a 17.36% CAGR through 2031.

- By end-user industry, manufacturing commanded 29.36% share in 2025, whereas utilities are set to register an 18.23% CAGR to 2031.

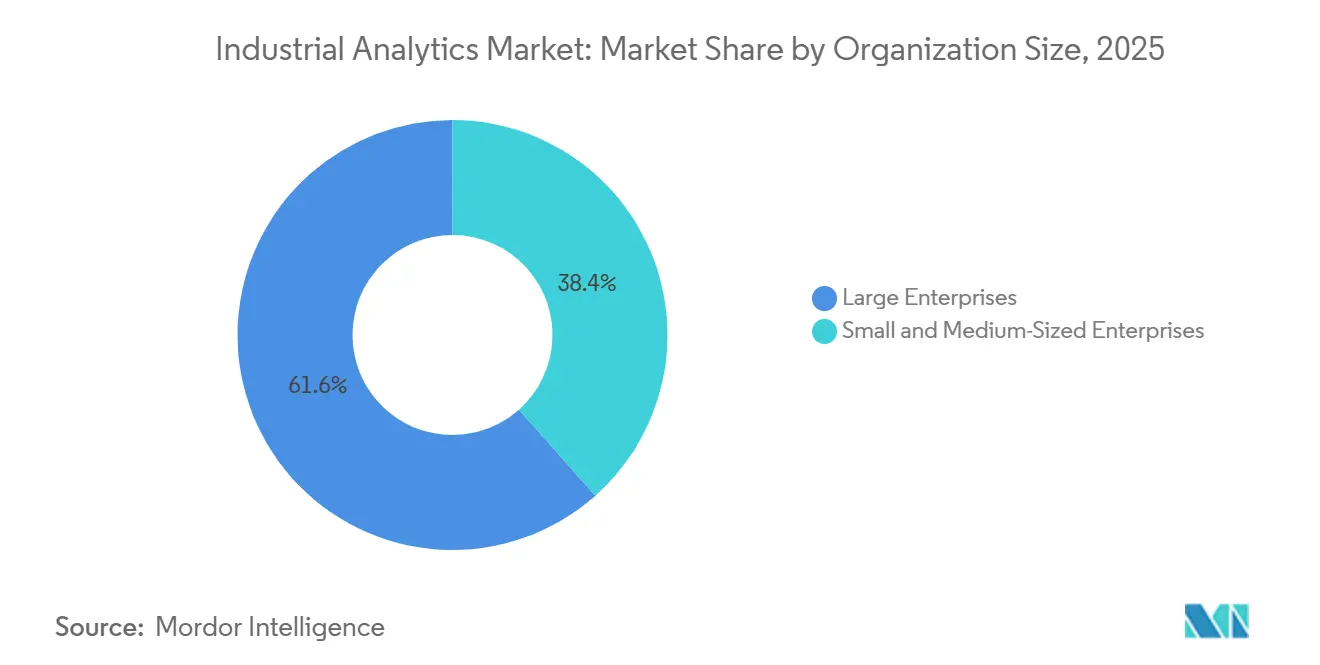

- By organization size, large enterprises held 61.57% share in 2025, while small and medium-sized enterprises are projected to increase at a 17.14% CAGR through 2031.

- By application, asset performance management led with 33.48% share in 2025, whereas energy management is anticipated to rise at a 17.89% CAGR to 2031.

- By geography, North America retained 38.29% market share in 2025, while Asia-Pacific is forecast to expand at a 17.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Edge Computing Capabilities | +3.2% | Global, with concentration in North America and Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Integration of Industrial AI in Low-Code Platforms | +2.8% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Proliferation of 5G-Enabled Industrial IoT Networks | +3.5% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Regulatory Push for Energy-Efficient Operations | +2.4% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Standardization of Digital Twins Across Asset-Intensive Sectors | +2.1% | Global, led by manufacturing and utilities in developed markets | Long term (≥ 4 years) |

| Mainstream Adoption of Pay-per-Use Analytics Models | +1.9% | Global, accelerated uptake in emerging markets and SME segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Edge Computing Capabilities

Edge-localized inference eliminates network bottlenecks for latency-sensitive tasks such as robotic path planning, vision-based quality checks, and substation fault isolation. Honeywell and Google Cloud deployed micro-nodes that process sensor streams on-site, reducing bandwidth costs by 30%.[1]Source: Honeywell, “Honeywell and Google Cloud Collaborate on Industrial AI,” honeywell.com IBM shipped 15-watt edge devices that run predictive models on offshore platforms where connectivity is sporadic. Microsoft Azure Stack integrates seamlessly with Siemens Industrial Edge, allowing manufacturers to train centrally and then push compressed weights to shop-floor gateways. Such architectures ensure uninterrupted operations when networks fail and allow real-time control loops to operate within single-digit millisecond windows. Resulting productivity gains make edge computing one of the highest-impact catalysts for the industrial analytics market.

Integration of Industrial AI in Low-Code Platforms

Drag-and-drop workflows seamlessly embed analytics into maintenance, quality, and logistics processes, eliminating the need for Python or SQL skills. Bain research showed a 60% reduction in deployment time when plants used low-code tools versus traditional programming. Microsoft Power Platform now ships with anomaly-detection models tuned for pumps, motors, and compressors.[2]Honeywell, “Honeywell and Google Cloud Collaborate on Industrial AI,” honeywell.com IFS and ServiceNow link sensor events to work-order generation, allowing technicians to receive prescriptive actions instantly. McKinsey’s 2025 Lighthouse Network found that factories that embraced low-code recorded 25% faster root-cause analyses. The ease of configuration lowers barriers for small plants and accelerates the diffusion of industrial analytics market best practices.

Proliferation of 5G-Enabled Industrial IoT Networks

Private 5G networks deliver sub-10-millisecond latency, enabling mobile robots and AR-assisted maintenance to function safely. Nokia rolled out private 5G across 12 European factories, improving AGV collision avoidance metrics by 40%.[3]Microsoft, “Microsoft and Siemens Deepen Partnership,” news.microsoft.com Verizon streamed HD video to cloud vision models in a U.S. auto plant, increasing defect detection rates by 23%. Cisco and Ericsson added TSN support, letting OT and IT traffic converge on a single backbone. Standardized slicing from Deutsche Telekom guarantees throughput for analytics even in congested environments. As spectrum fees fall, 5G becomes an essential enabler for the industrial analytics market, especially in high-density plants.

Regulatory Push for Energy-Efficient Operations

The European Union’s Corporate Sustainability Reporting Directive requires approximately 50,000 firms to disclose asset-level energy data, driving demand for embedded metering analytics. The U.S. EPA proposed continuous emissions monitoring rules, nudging utilities toward the use of real-time dashboards. China’s dual-control policy requires hourly energy consumption reporting through provincial portals. ISO 50001 certification became a prerequisite for public procurement bids in several EU states. These policies lift long-run demand for the industrial analytics market because compliance requires granular insights that spreadsheets cannot deliver.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Sovereignty Concerns in Cross-Border Cloud Deployments | -1.8% | Europe, China, and emerging markets with localization mandates | Medium term (2-4 years) |

| Shortage of Industrial-Domain-Specific Data Scientists | -1.5% | Global, acute in emerging markets and SME segments | Long term (≥ 4 years) |

| Cyber-physical Security Vulnerabilities in OT Networks | -1.2% | Global, heightened in critical infrastructure sectors | Short term (≤ 2 years) |

| Legacy Equipment Integration Costs | -1.4% | North America and Europe brownfield sites, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty Concerns in Cross-Border Cloud Deployments

China’s Data Security Law forces multinationals to store operational data on domestic servers, preventing global data-lake consolidation. The EU’s GDPR restricts the exporting of employee biometrics used in access control, driving vendors to set up regional inference clusters. India’s draft Digital Personal Data Protection Act may adopt similar localization clauses. Each silo raises infrastructure costs, fragments model training, and slows feature rollouts. For the industrial analytics market, this introduces friction that vendors can only mitigate with edge or hybrid architectures.

Shortage of Industrial-Domain-Specific Data Scientists

A World Economic Forum survey revealed that 63% of manufacturers cite talent scarcity as the primary barrier to scaling AI. Few university programs teach both data science and programmable logic controllers, forcing employers to invest up to 18 months in upskilling. McKinsey projects a 40% supply gap for industrial data scientists through 2030. SMEs are hit hardest because they cannot match the salaries of large enterprises. Vendors are embedding more domain logic into templates; however, highly customized processes, such as underground mining or continuous-batch pharmaceuticals, still rely on scarce human expertise, thereby diluting the growth rate of the industrial analytics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Architectures Bridge Cloud and Edge

Cloud-based implementations accounted for 59.12% of the industrial analytics market share in 2025, as manufacturers adopted consumption pricing and pre-trained models. The industrial analytics market size for cloud deployments is projected to expand at a 17.09% CAGR, driven by integrations with Microsoft Azure, AWS IoT SiteWise, and Google Cloud Vertex AI. On-premises systems continue to serve latency-critical workflows in defense and pharmaceutical industries, accounting for 40.88% of demand. Hybrid use cases are multiplying. Schneider Electric’s EcoStruxure synchronizes models bi-directionally, allowing regulatory data to remain on-site while benefiting from cloud-based retraining. ABB’s Ability Genix offers similar advantages, demonstrating how federated architectures can satisfy sovereignty, uptime, and scalability within a single stack.

The growing mesh of local gateways and centralized MLOps pipelines enables firms to retain sensitive data while benchmarking performance against anonymized peer metrics in the cloud. This blended approach resonates with multinational manufacturers juggling multiple jurisdictions. As orchestration tooling matures, hybrid architectures are expected to dominate new deployments, cementing their role at the core of future industrial analytics market growth.

By Component: Service Revenues Rise With Complexity

Software represented 62.34% revenue in 2025, but services are catching up fast with a 17.21% CAGR through 2031. Enterprises outsource sensor integration, feature engineering, and continuous model tuning to partners such as Accenture, Deloitte, and PwC. As a result, the industrial analytics market size for services is expanding faster than the software layer. Vendors, ranging from SAP and IBM to Siemens, bundle managed offerings that include equipment profile libraries, anomaly threshold calibration, and security patching.

Because industrial assets age and process variables drift, analytics initiatives require perpetual recalibration. Customers rely on system integrators to embed change management and domain expertise. This service-centric model transforms analytics from a capital purchase into an operational expenditure, deepening vendor-client relationships and fostering recurring revenue streams that will shape the industrial analytics market through 2031.

By Analytics Type: Prescriptive Engines Close the Loop

Predictive analytics held a 47.19% share in 2025; however, prescriptive tools are advancing at a 17.36% CAGR, as operators demand automated set-point adjustments rather than dashboard alerts. The industrial analytics market size for prescriptive solutions is poised to grow rapidly, as they free human experts from routine decision-making cycles. GE Digital’s turbines now self-calibrate combustion parameters, while Rockwell’s FactoryTalk dispatches technician-specific work orders based on parts availability. Reinforcement learning in PTC ThingWorx adds autonomous optimization loops that improve over time.

While descriptive dashboards are crucial for regulatory reporting, they offer only modest operational savings. Consequently, there's a swift shift in budget allocations towards prescriptive engines, which leverage advanced analytics to provide actionable insights and optimize decision-making processes. This transition is significantly reducing payback periods from years to mere months, enabling organizations to achieve faster returns on investment. Vendors emphasizing closed-loop control and integrated workflow automation are well-positioned to capture a substantial portion of the growing industrial analytics market, as these capabilities address the increasing demand for efficiency and streamlined operations.

By End-User Industry: Utilities Outpace Manufacturing

Manufacturing controlled 29.36% of demand in 2025, leveraging analytics for yield improvement and downtime reduction. However, utilities are forecast to post an 18.23% CAGR as renewable intermittency forces grid operators to implement real-time balancing algorithms. National Grid ESO reduced balancing costs by integrating wind and solar forecasts into its dispatch models, and Duke Energy reduced transformer failures by 30% through the use of predictive maintenance. These successes make utilities the fastest-expanding cohort in the industrial analytics market.

Other sectors, including mining and logistics, are also advancing adoption. Rio Tinto uses route-optimizing analytics for autonomous haulage, while Maersk applies shipboard sensors to schedule engine servicing during port calls. Each vertical adds nuanced requirements, such as safety compliance in mines and cold-chain integrity in logistics, fueling a broad-based rise in industrial analytics market penetration across asset-intensive industries.

By Organization Size: SMEs Benefit From Pay-Per-Use

Large enterprises commanded a 61.57% share in 2025, but small and medium-sized firms are registering a 17.14% CAGR, thanks to pay-as-you-go tiers that eliminate capital barriers. The adoption of industrial analytics among SMEs accelerates when suppliers, such as Siemens and AWS, offer free or low-volume starter packages. Vertical templates shorten deployment cycles, and consumption pricing keeps monthly outlays aligned with production volumes. Challenges persist, especially in areas such as cybersecurity staffing and governance; however, managed services and cloud-native security controls are helping to lower these hurdles.

As the SME segment continues to grow, it broadens the total addressable market for industrial analytics. This shift indicates a rising demand trend, prioritizing affordability and simplicity over extensive customization. Driven by the pursuit of operational efficiency, cost reduction, and competitive edge, SMEs are increasingly adopting industrial analytics solutions. These solutions enable businesses to optimize processes, improve decision-making, and identify growth opportunities, thereby fueling the market's growth.

By Application: Energy Management Surges

Asset performance management retained a 33.48% share in 2025, but energy-management solutions are expanding at a 17.89% CAGR, driven by carbon-pricing schemes and volatile electricity rates. Schneider Electric’s Resource Advisor and ABB’s Energy Manager target multi-site enterprises that need load-shifting and demand-response insights. Because energy costs often account for 10-40% of operating expenses in heavy industry, even marginal efficiency gains can pay for analytics subscriptions within a quarter. Consequently, energy-focused modules are poised to capture a growing share of the industrial analytics market by 2031.

Quality optimization, supply-chain visibility, and safety analytics round out application demand. Each draws on the same sensor and time-series foundations, reinforcing the platform approach that vendors favor. Cross-application synergies enhance customer loyalty by enabling seamless integration and functionality across multiple modules. This reduces churn rates among multi-module users, as they are more likely to remain engaged with the platform. Consequently, these synergies drive sustained revenue growth in the industrial analytics market over the long term.

Geography Analysis

North America contributed 38.29% of the industrial analytics market share in 2025, driven by investments in the semiconductor, automotive, and oil and gas sectors, linked to the CHIPS and Science Act. Federal incentives stipulate digital-twin capabilities, catalyzing analytics deployments across greenfield fabs. Canada’s Strategic Innovation Fund backed aerospace and EV battery pilots, while Mexican nearshoring projects embraced cloud-edge hybrids to accelerate plant commissioning. Fragmented state privacy laws raise compliance overhead but also spur demand for governance modules, indirectly benefiting software vendors.

Asia-Pacific is forecast to record a 17.96% CAGR through 2031. China ties subsidies to smart-manufacturing metrics, pushing factories to retrofit lines with digital twins. India’s Production-Linked Incentive scheme requires real-time quality analytics for reimbursement eligibility, creating a multiplier effect for the industrial analytics market. Japan’s Society 5.0 promotes human-robot collaboration powered by fatigue-prediction models, while South Korea’s smart-factory program subsidizes the adoption of SME analytics. Australia’s mining sites utilize edge analytics to enhance haul-truck efficiency, while Southeast Asian exporters implement compliance dashboards to meet EU due diligence requirements.

Europe’s growth story revolves around sustainability compliance. The Corporate Sustainability Reporting Directive promotes equipment-level energy audits, while Germany’s Industrie 4.0 grants encourage mid-size manufacturers to adopt digital twins. France’s Industry of the Future tax incentives and the United Kingdom’s Made Smarter grants further expand demand. Eastern markets remain nascent, but local vendors in Russia tailor offerings to national standards to circumvent import restrictions, adding regional flavor to the industrial analytics market.

The Middle East and Africa, along with South America, represent emerging growth pockets. Saudi Arabia’s Vision 2030 drives analytics for petrochemicals and utilities, and South Africa’s mines deploy safety analytics to detect gas leaks. Brazil’s agribusiness chains integrate precision agriculture with food-processing analytics, and Argentina’s lithium producers utilize models to reduce water usage. Although absolute spend is lower than in developed regions, pilot projects are accelerating across these territories, widening the global footprint of the industrial analytics market.

Competitive Landscape

Incumbent automation firms, such as Siemens, ABB, Schneider Electric, Rockwell Automation, and Honeywell, bundle analytics with control hardware, leveraging their installed bases to deepen lock-in. Cloud hyperscalers, including Microsoft Azure, AWS, Google Cloud, IBM, and Oracle, compete on scalable MLOps, pre-trained models, and pay-as-you-go economics. Specialized software providers such as PTC, SAP, SAS Institute, and Splunk target vertical niches: PTC for discrete manufacturing, SAP for process industries, and Splunk for log analytics tied to OT cybersecurity.

Strategic partnerships abound. Siemens and Microsoft co-developed industrial-metaverse applications that merge CAD, simulation, and live sensor data. Honeywell and Accenture formed a joint venture to deliver analytics-as-a-service to mid-sized factories, while SAP and NVIDIA integrated physics-accurate digital twins into their supply-chain suites. Investment in R&D remains robust: ABB expanded its Bangalore analytics lab by USD 150 million, filing patents on reinforcement learning for industrial control.

Competition now revolves around platform completeness, cybersecurity certification, and domain-specific model libraries. Vendors scoring IEC 62443 compliance gain an edge with risk-averse customers. As platforms converge, differentiation shifts to the speed of deployment, breadth of templates, and ecosystem openness. Despite intense rivalry, the top 10 suppliers control roughly 45-50% of the revenue, indicating a moderately concentrated industrial analytics market where both scale and domain depth are important factors.

Industrial Analytics Industry Leaders

Cisco Systems

IBM Corporation

General Electric Company

Oracle Corporation

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Siemens acquired Altair Engineering for USD 10.6 billion, strengthening simulation-to-operations digital-twin capabilities.

- September 2025: Microsoft and Kawasaki Heavy Industries created a Kobe innovation center to deploy Azure AI across robotics and aerospace divisions.

- August 2025: Schneider Electric launched EcoStruxure Automation Expert 2.0, decoupling control logic from hardware for analytics-ready architectures.

- July 2025: Honeywell and Accenture formed Honeywell Accenture Digital Solutions to deliver analytics-as-a-service for mid-size manufacturers.

Global Industrial Analytics Market Report Scope

The Industrial Analytics Market Report is Segmented by Deployment (On-Premises, and Cloud), Component (Software, and Services), Analytics Type (Descriptive Analytics, Predictive Analytics, Prescriptive Analytics), End-User Industry (Manufacturing, Construction, Mining, Transportation and Logistics, Utilities, Other End-User Industry), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Application (Asset Performance Management, Quality and Process Optimization, Supply-Chain and Inventory Analytics, Energy Management, Safety and Risk Analytics), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud |

| Software |

| Services |

| Descriptive Analytics |

| Predictive Analytics |

| Prescriptive Analytics |

| Manufacturing |

| Construction |

| Mining |

| Transportation and Logistics |

| Utilities |

| Other End-User Industry |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Asset Performance Management |

| Quality and Process Optimization |

| Supply-Chain and Inventory Analytics |

| Energy Management |

| Safety and Risk Analytics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment | On-Premises | ||

| Cloud | |||

| By Component | Software | ||

| Services | |||

| By Analytics Type | Descriptive Analytics | ||

| Predictive Analytics | |||

| Prescriptive Analytics | |||

| By End-User Industry | Manufacturing | ||

| Construction | |||

| Mining | |||

| Transportation and Logistics | |||

| Utilities | |||

| Other End-User Industry | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises | |||

| By Application | Asset Performance Management | ||

| Quality and Process Optimization | |||

| Supply-Chain and Inventory Analytics | |||

| Energy Management | |||

| Safety and Risk Analytics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the industrial analytics market?

It stands at USD 44.57 billion in 2026 and is projected to reach USD 97.38 billion by 2031.

Which deployment model is growing fastest?

Cloud deployments are forecast to expand at a 17.09% CAGR through 2031.

Why are utilities investing heavily in analytics?

Integrating intermittent renewables demands real-time load balancing, driving an 18.23% CAGR for analytics adoption in the sector.

How do low-code platforms help manufacturers?

They cut analytics application deployment time by 60%, letting process engineers build models without coding expertise.

What is the biggest restraint on market growth?

Data-sovereignty regulation forces regional data silos, increasing infrastructure costs and complicating global rollouts.

Which application segment offers the fastest growth?

Energy-management analytics, advancing at a 17.89% CAGR, leads due to carbon-pricing and volatile electricity costs.

Page last updated on: