Industrial Furnace Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.54 Billion |

| Market Size (2031) | USD 17.01 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

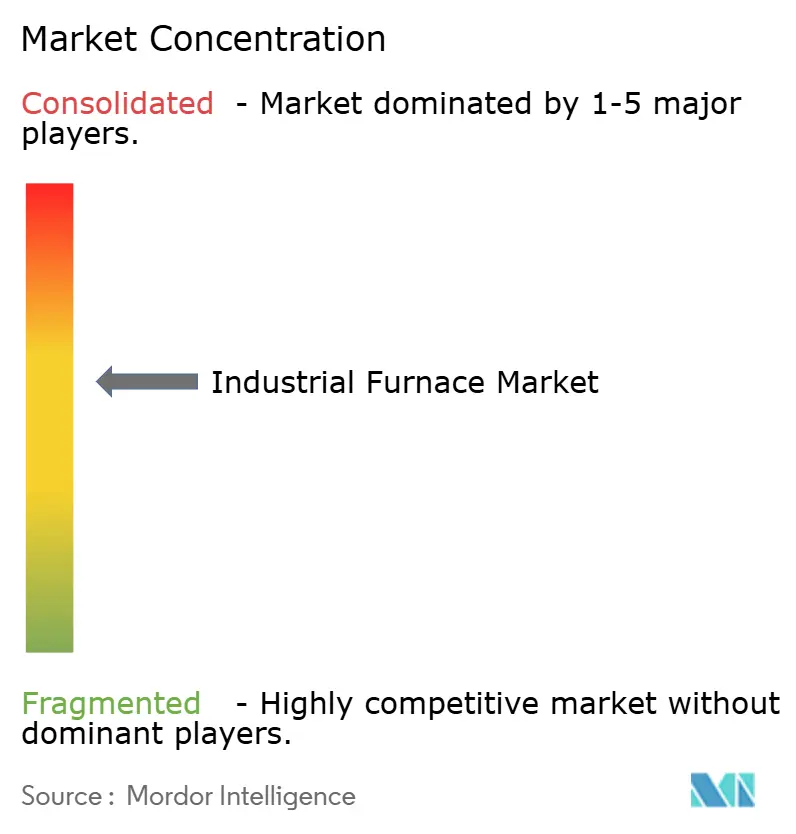

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Furnace Market Analysis by Mordor Intelligence

The industrial furnace market size is expected to grow from USD 12.93 billion in 2025 to USD 13.54 billion in 2026 and is forecast to reach USD 17.01 billion by 2031 at 4.68% CAGR over 2026-2031. Growth rests on steady demand for precision heat-treatment in automotive and aerospace manufacturing, accelerated adoption of hydrogen-ready and electric furnace technologies, and ongoing regulatory pressure to curb industrial emissions.[1]Primetals Technologies, “Hydrogen-Based Steel Production Technologies,” primetalstechnologies.com Manufacturers are investing in modular designs that lower installation time and enable distributed production, while digital control systems equipped with predictive maintenance reduce downtime and energy waste. Energy-efficiency retrofits in North America and decarbonization programs in Europe and Japan underpin short-term momentum, whereas large-scale capacity additions in the Asia-Pacific sustain long-term expansion. Competitive intensity is shaped by mid-sized engineering firms vying with global conglomerates for projects that bundle equipment, services, and software.

Key Report Takeaways

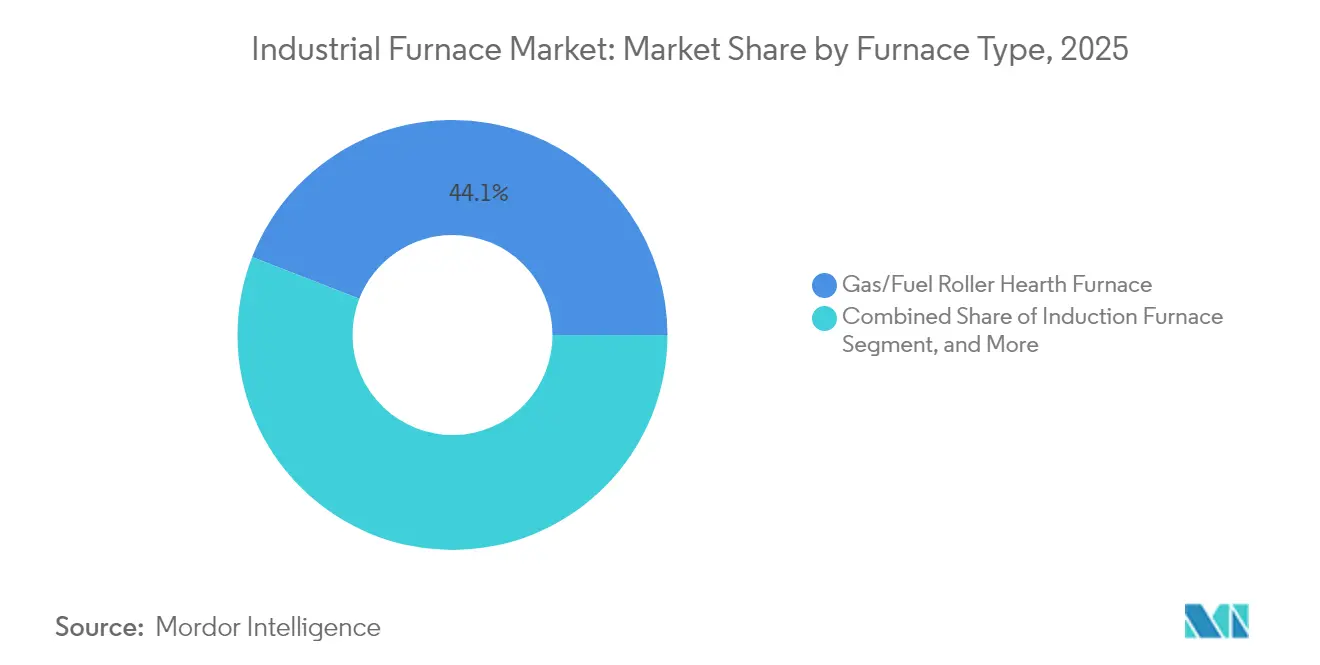

- By furnace type, gas/fuel roller hearth systems led with 44.10% of the industrial furnace market share in 2025; hydrogen-ready designs are forecast to expand at a 6.59% CAGR through 2031.

- By arrangement, box/chamber/muffle formats accounted for 37.45% of the industrial furnace market size in 2025, while tube/clamshell units posted the fastest 6.51% CAGR to 2031.

- By heating method, combustion-fired units held 51.10% of the industrial furnace market size in 2025; hybrid gas-electric solutions are set to grow at a 5.98% CAGR during the same period.

- By temperature range, operations between 1,000-1,500 °C dominated with 52.94% industrial furnace market share in 2025; installations rated above 1,500 °C are advancing at 5.58% CAGR.

- By end-user, metal and mining applications captured 33.72% of the industrial furnace market size in 2025; aerospace uses are progressing at a 6.55% CAGR through 2031.

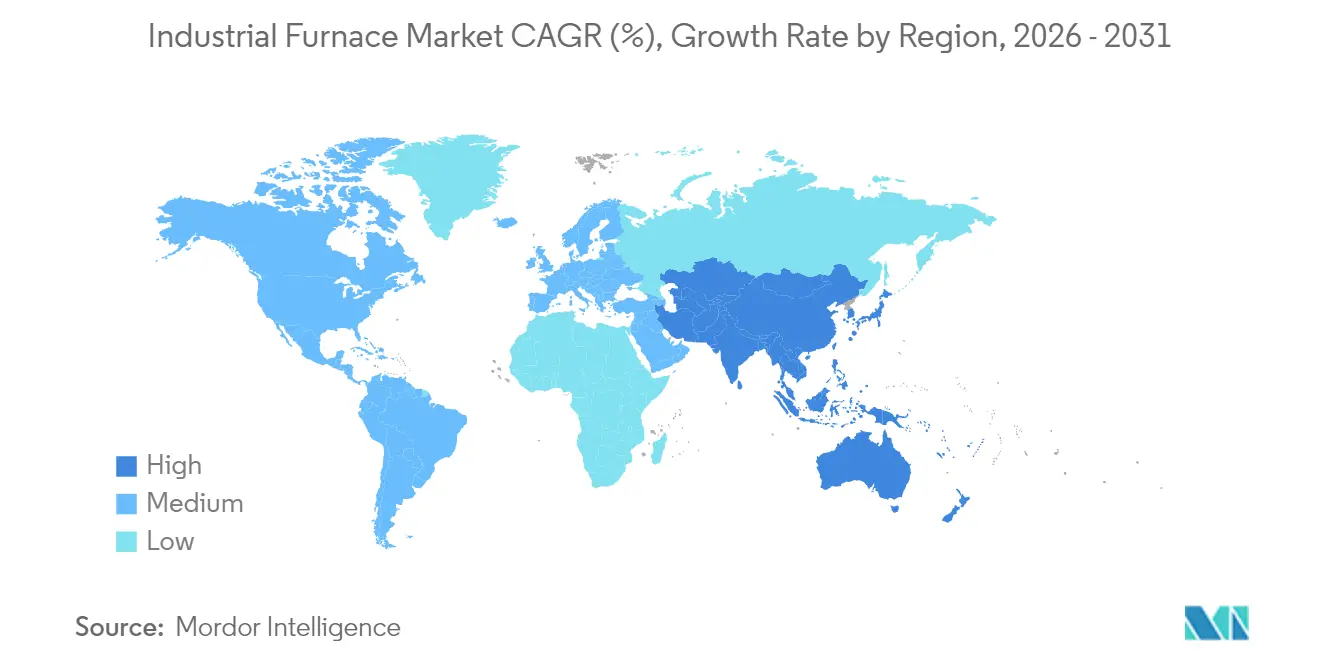

- By geography, North America commanded 35.10% of the industrial furnace market size in 2025, whereas Asia-Pacific recorded the quickest 6.24% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Furnace Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for heat-treatment in automotive | +0.8% | North America and Europe | Medium term (2-4 years) |

| Investments in metal and mining capacity expansion | +0.9% | Asia-Pacific and Middle East-Africa | Long term (≥ 4 years) |

| Rapid adoption of electric furnaces | +0.7% | Europe and Japan; expanding to North America | Medium term (2-4 years) |

| Stringent energy-efficiency norms | +0.6% | North America and European Union | Short term (≤ 2 years) |

| Shift toward hydrogen-ready designs | +0.5% | Europe and Japan | Long term (≥ 4 years) |

| Growth of micro-scale modular furnaces | +0.4% | Global industrial clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Heat-Treatment in Automotive Manufacturing

The pivot to electric vehicle production is reshaping thermal-processing requirements across global assembly plants. Battery housings, traction-motor cores, and lightweight body structures need heat-treatment profiles that minimize distortion and support tighter tolerances. Automakers therefore specify furnaces with rapid quench rates, inert atmospheres, and closed-loop controls that document every cycle for ISO 26262 compliance.[2]Tesla, “Manufacturing and Technology Updates,” tesla.com Suppliers integrating predictive-maintenance analytics achieve higher uptime, reducing total cost of ownership and strengthening competitive bids for long-term sourcing contracts.

Rising Investments in Metal and Mining Capacity Expansion

Steel and non-ferrous producers in China, India, and the Gulf Cooperation Council are building or revamping assets to meet infrastructure and energy-transition spending. Policies encouraging electric-arc furnaces (EAFs) over legacy blast furnaces drive replacement demand, while lower-grade ore processing boosts the need for furnaces with advanced refractory linings and oxygen-rich atmospheres that preserve throughput yet cut energy use.[3]China Iron and Steel Association, “Steel Industry Consolidation Policy,” chinaisa.org.cn Modular plants allow operators to stagger capital outlays and match future commodity cycles.

Accelerated Adoption of Electric Furnaces for Decarbonization Mandates

Carbon-pricing schemes, such as the European Union’s Carbon Border Adjustment Mechanism, elevate the cost advantage of low-emission manufacturing pathways. Steelmakers and foundries respond by deploying EAFs powered by renewable electricity, achieving up to 66% emission cuts relative to coke-fired routes. Government grants and tax credits in the United States further compress payback periods for electric retrofits, strengthening order pipelines for furnace OEMs specialized in high-current power supplies and off-gas capture systems.

Stringent Energy-Efficiency Norms Driving Furnace Retrofits

Minimum efficiency requirements enacted by the U.S. Department of Energy in 2024 oblige industrial facilities to upgrade burners, recuperators, and control software. The regulation accelerates replacement cycles for units reaching the end of service life and propels demand for real-time monitoring that verifies compliance. Vendors offering turnkey retrofit packages, including engineering, installation, and post-start-up training, secure multi-year service contracts that stabilize revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and running costs for >1500°C installations | -0.6% | Global, particularly affecting specialty metals and advanced materials sectors | Medium term (2-4 years) |

| Volatility in natural gas and electricity prices | -0.4% | Europe and North America, with spillover effects in energy-intensive regions | Short term (≤ 2 years) |

| Skilled-operator shortage for complex heat-treat processes | -0.3% | Global, with acute shortages in North America and Europe | Long term (≥ 4 years) |

| Regulatory uncertainty on future carbon-pricing schemes | -0.2% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Running Costs for > 1,500 °C Installations

Extreme-temperature furnaces cost upward of USD 10 million to install and consume 15-20% of plant operating budgets. Advanced refractories, custom alloys, and enhanced safety systems inflate upfront investment, while a global shortage of technicians specialized in ultra-high-temperature operations raises labor costs. Insurance premiums and stringent permitting add further overhead, extending payback periods and deterring adoption in smaller firms.

Volatility in Natural Gas and Electricity Prices

Geopolitical disruptions and supply-demand imbalances have lifted energy price variance beyond historical norms. For gas-fired furnaces in Europe, feedstock swings account for 40% of production cost uncertainty, complicating long-range budgeting.[4]Powernext, “European Natural Gas Price Volatility,” powernext.com Electric-furnace operators face similar volatility in regions with intermittent renewable penetration and capacity-market redesigns. Complex hedging raises financial overhead and dampens capital commitment to greenfield projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Furnace Type: Hydrogen Integration Reshapes Technology Landscape

Hydrogen-ready designs form the fastest-moving segment with a 6.59% CAGR to 2031 as policy frameworks in Europe and Japan stipulate carbon-neutral process heat. Gas/fuel roller hearth equipment nonetheless retained 44.10% of the industrial furnace market share in 2025, favored for reliability and existing infrastructure. Hybrid burners allowing incremental hydrogen substitution widen user options, ensuring legacy assets remain productive throughout the transition.

Wider adoption of electric roller hearth furnaces in renewable-rich regions encourages OEMs to co-develop high-power transformers and sophisticated magnetic-field controls that reduce energy loss. Induction units remain the tool of choice for niche metallurgical applications requiring rapid heating and fine temperature gradients, whereas solar furnaces occupy a nascent but promising niche in high-irradiance zones willing to leverage concentrated solar power for specialty ceramics.

By Arrangement / Format: Modular Designs Drive Operational Flexibility

Box/chamber/muffle configurations delivered 37.45% of the industrial furnace market size in 2025 by serving batch processes across metals, machinery, and ceramics. Tube/clamshell systems are recording a 6.51% CAGR as producers switch to continuous-flow layouts that minimize dwell time and energy consumption. Car-bottom and bottom-loading designs retain importance in heavy-equipment production where oversized castings demand robust material-handling solutions.

Vacuum and controlled-atmosphere units capture rising share in aerospace and semiconductor back-end processing, reflecting chain-of-custody requirements for contamination-free surfaces. The industrial furnace industry now emphasizes plug-and-play skids that scale production without lengthy site work, aligning with lean manufacturing philosophies and reduced capital-risk appetites among mid-tier suppliers.

By Heating Method: Hybrid Systems Gain Strategic Importance

Combustion-based furnaces comprised 51.10% of the industrial furnace market size in 2025, yet face flat growth as emission caps tighten. Hybrid gas-electric solutions show 5.98% CAGR because they switch energy sources in real time, balancing grid charges against pipeline fuel prices. Resistance electric technology thrives in clean-environment sectors such as electronics, while induction electric units dominate specialty steels requiring fast, uniform heat penetration.

Heat-recovery and regenerative-burner upgrades boost the efficiency of existing combustion assets, extending their economic life and smoothing the pathway to low-carbon heat. OEMs bundle energy-management dashboards that guide operators toward the least-cost heat-source mix, reducing exposure to volatile spot markets.

By Temperature Range: Ultra-High-Temperature Applications Drive Innovation

Processes between 1,000-1,500 °C commanded 52.94% of the industrial furnace market share in 2025, integral to standard steel tempering, aluminum billet homogenization, and kiln-fired advanced ceramics. Demand for above-1,500 °C capabilities is rising 5.58% CAGR as aerospace engines and hypersonic systems need ultra-refractory alloys. Research programs at institutions such as Tohoku University spark supplier interest in next-generation insulation and cooling schemes that lengthen refractory life while trimming energy draw.

Below-1,000 °C furnaces serve food, pharmaceutical, and composites curing, where thermal uniformity rather than peak temperature dictates quality outcomes. Innovations in low-mass insulation reduce heat-up time by 25% and contribute incremental savings that multiply across continuous-flow lines running multiple shifts.

By End-User Industry: Aerospace Leads Growth Acceleration

Metal and mining held 33.72% of the industrial furnace market size in 2025, underpinned by primary steel, copper, and aluminum throughput. Aerospace registers the swiftest 6.55% CAGR to 2031 as manufacturers qualify advanced nickel-based superalloys and ceramic matrix composites necessitating precision temperature-soak profiles. Automotive OEMs and tier suppliers sustain steady spend on furnaces tailored to electric-vehicle components, while electronics and semiconductor producers adopt vacuum furnaces with sub-ppm contamination control for advanced node production.

Chemical and construction-machinery sectors represent durable demand pools, especially where national infrastructure programs boost cement, glass, and heavy-equipment volumes. Rising adoption of continuous-annealing lines and galvanizing furnaces in coated-steel markets further broadens end-user diversity and insulates suppliers from cyclical swings in any single vertical.

Geography Analysis

North America contributed 35.10% of the industrial furnace market size in 2025, driven by strong heat-treatment orders from U.S. automotive and aerospace hubs and compliance with updated Department of Energy standards. Expansion projects such as Nucor’s USD 3.0 billion EAF program and Canadian mining investments elevate baseline demand for high-capacity units. Skilled technical labor supports after-sales service revenue, though price volatility in natural gas and electricity remains a management priority.

Asia-Pacific records the quickest 6.24% CAGR, thanks to China’s steel sector modernization that replaces outdated blast furnaces with EAFs and India’s Production-Linked Incentive scheme that pulls forward capital spending on machinery and electronics capacity. Japan pioneers hydrogen-ready metallurgy, allocating JPY 329.4 billion to furnace upgrades that align with 2035 climate goals. South Korea, Singapore, and Australia round out regional growth by boosting semiconductor back-end and mineral-processing lines.

Europe sustains mid-single-digit growth anchored in climate policy compliance. Germany funnels public research grants toward hydrogen burners, while Italy modernizes heat-treatment fleets for specialty steel and automotive supply chains. The Carbon Border Adjustment Mechanism incentivizes furnace retrofits that cut Scope-1 emissions, and the Industrial Emissions Directive mandates best-available-technology upgrades in refractory, control systems, and waste-heat recovery. Eastern European markets, particularly Poland and Czechia, attract green-field investments in battery-component plants equipped with low-carbon furnaces.

Competitive Landscape

The industrial furnace industry remains moderately fragmented, with the top five suppliers holding roughly 28% combined revenue. Global conglomerates such as Andritz AG, Tenova, and Inductotherm compete with niche engineering firms, including Ipsen International and SECO/WARWICK. Players differentiate through proprietary burner designs, digital twins, and tailored after-market service contracts that lock in recurring revenue.

Strategic moves center on digitalization and decarbonization. Ipsen retrofitted its global installed base with an IoT suite that trims unplanned downtime by 15%, whereas SECO/WARWICK introduced a cloud-based energy optimizer leveraging machine learning to cut cycle-fuel usage by up to 8%. RHI Magnesita acquired Resco Products for USD 340 million, gaining refractory technology vital for > 1,500 °C operations and strengthening supply security.

Emerging entrants target niche gaps: modular solar furnaces for specialty ceramics, skid-mounted induction units for additive-manufacturing post-processing, and hydrogen burner retrofits for existing batch lines. Incumbents respond through minority stakes or outright acquisitions to secure technology roadmaps while retaining scale economies in fabrication and global field-service teams.

Industrial Furnace Industry Leaders

Andritz AG

Carbolite Gero Limited

Epcon Industrial Systems LP

Gasbarre Products Inc.

International Thermal Systems LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nucor Corporation posted USD 603 million net earnings and advanced USD 1.8 billion in EAF capacity projects, underscoring continued spending on low-carbon steel.

- June 2025: Commercial Metals Company generated USD 204.1 million core EBITDA as its TAG program improved EAF efficiency.

- May 2025: Thermon Group Holdings closed the F.A.T.I. acquisition and reported USD 498.2 million annual revenue, enlarging its industrial heating portfolio.

- April 2025: Lincoln Electric recorded USD 1.004 billion in Q1 sales, reflecting robust welding-equipment demand that supports furnace fabrication.

- March 2025: Mueller Industries achieved USD 1.0 billion in Q1 revenue, benefiting furnace supply chains through copper-based components.

- February 2025: RHI Magnesita finalized the USD 340 million acquisition of Resco Products, bolstering ultra-high-temperature refractory supply.

- January 2025: Atlas Holdings acquired EVRAZ North America’s steel assets, including multiple EAFs, signaling continued consolidation.

Global Industrial Furnace Market Report Scope

An industrial furnace is used for the heat treatment of metals/glass and other materials for tempering, annealing, carburizing, and pre-treatment for forging and shaping. An industrial furnace's basic function includes superheating materials to extreme temperatures using a variety of formats and fuels.

industrial furnace market is segmented by type (gas/fuel roller hearth furnace and electric boller hearth furnace), by arrangement (box furnace/chamber furnace/muffle furnace, tube/clam shell furnace, bottom loading/car bottom loading furnace, top loading furnace, and others (vaccum furnace, heat treatment furnace, atmosphere furnaces, others)), by end-user industry (chemicals, metal & mining, manufacturing (automotive manufacturers, construction machinery manufacturers, aircraft-related manufacturers, and other end-user industries), and by geography (North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America). The report offers market forecasts and size in value (USD) for all the above segments.

| Gas/Fuel Roller Hearth Furnace |

| Electric Roller Hearth Furnace |

| Induction Furnace |

| Hydrogen-ready Furnace |

| Solar Furnace |

| Box/Chamber/Muffle Furnace |

| Tube/Clamshell Furnace |

| Bottom Loading/Car Bottom Loading Furnace |

| Top Loading Furnace |

| Vacuum/Atmosphere/Heat-Treatment Furnace |

| Combustion-Fired |

| Resistance Electric |

| Induction Electric |

| Hybrid (Gas plus Electric) |

| Below 1 000 °C |

| 1 000 – 1 500 °C |

| Above 1 500 °C |

| Chemicals |

| Metal and Mining |

| Automotive Manufacturing |

| Construction Machinery |

| Aerospace |

| Electronics and Semiconductors |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Furnace Type | Gas/Fuel Roller Hearth Furnace | ||

| Electric Roller Hearth Furnace | |||

| Induction Furnace | |||

| Hydrogen-ready Furnace | |||

| Solar Furnace | |||

| By Arrangement / Format | Box/Chamber/Muffle Furnace | ||

| Tube/Clamshell Furnace | |||

| Bottom Loading/Car Bottom Loading Furnace | |||

| Top Loading Furnace | |||

| Vacuum/Atmosphere/Heat-Treatment Furnace | |||

| By Heating Method | Combustion-Fired | ||

| Resistance Electric | |||

| Induction Electric | |||

| Hybrid (Gas plus Electric) | |||

| By Temperature Range | Below 1 000 °C | ||

| 1 000 – 1 500 °C | |||

| Above 1 500 °C | |||

| By End-user Industry | Chemicals | ||

| Metal and Mining | |||

| Automotive Manufacturing | |||

| Construction Machinery | |||

| Aerospace | |||

| Electronics and Semiconductors | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the industrial furnace market in 2031?

The industrial furnace market is projected to reach USD 17.01 billion by 2031.

How fast is demand for hydrogen-ready furnaces growing?

Hydrogen-ready designs are expected to expand at a 6.59% CAGR through 2031 as decarbonization policies tighten.

Which region is growing the quickest for new furnace installations?

Asia-Pacific records the fastest 6.24% CAGR, propelled by Chinese steel upgrades and Indian manufacturing incentives.

Why are hybrid gas-electric furnaces gaining popularity?

They let operators switch energy sources in response to real-time fuel and electricity prices, improving cost control and emission compliance.

Which end-user sector shows the highest growth in furnace demand?

Aerospace leads with a 6.55% CAGR due to advanced materials that require precise, high-temperature processing.

How fragmented is the competitive landscape?

The market concentration score is 6, indicating moderate consolidation, with the top five firms holding roughly 60-70% combined revenue.

Page last updated on: