Indoor Plants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.61 Billion |

| Market Size (2031) | USD 16.36 Billion |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

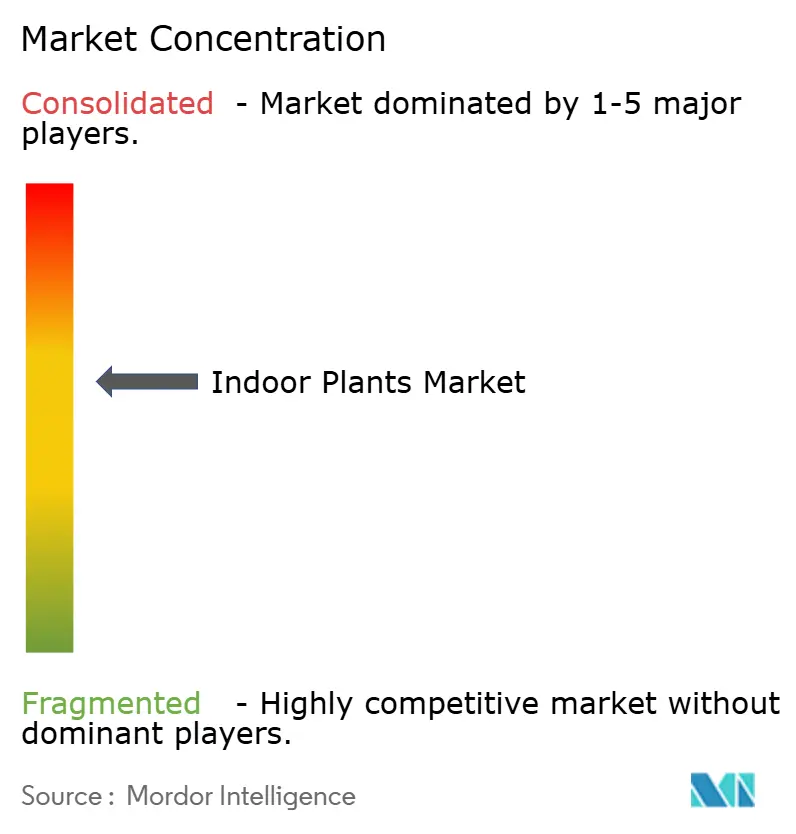

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indoor Plants Market Analysis by Mordor Intelligence

The Indoor Plants market size is expected to grow from USD 13.12 billion in 2025 to USD 13.61 billion in 2026 and is forecast to reach USD 16.36 billion by 2031 at 3.75% CAGR over 2026-2031.

Corporate wellness programs, WELL and LEED certification targets, and the mainstreaming of biophilic design are pushing the indoor plants market beyond its traditional decorative role into a functional workplace and wellness investment. Technology-driven care solutions, social-media-enabled trends, and sustained urbanization in Asia-Pacific continue to enlarge the customer base and lift premium product penetration. Supply-side factors, especially tissue-culture propagation, peat-free substrates, and smart-planter innovations, are lowering production costs, broadening varietal availability, and reshaping channel economics. Competitive intensity remains moderate as no single grower or retailer holds a decisive lead, leaving room for nimble specialists to monetize niche cultivars, IoT-enabled formats, and commercial maintenance services.

Key Report Takeaways

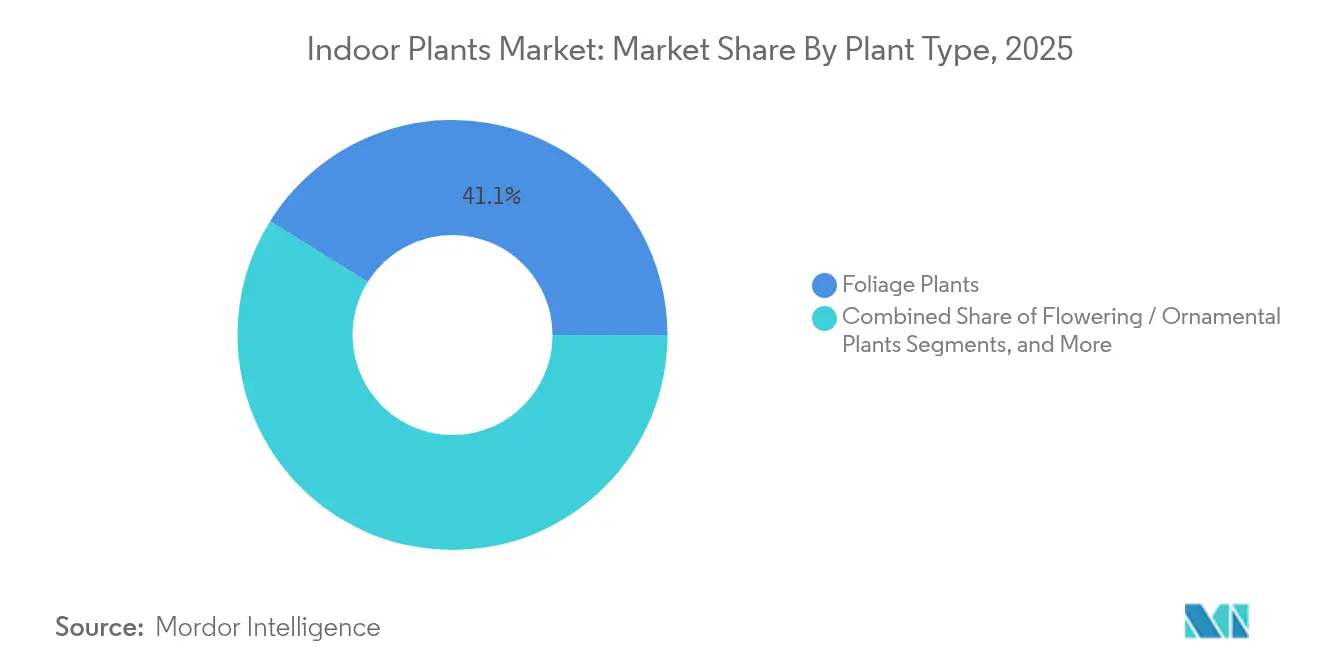

- By plant type, foliage plants led with 41.12% revenue share in 2025; succulents and cacti are projected to expand at a 6.88% CAGR through 2031 in the indoor plants market.

- By light requirement, low-light tolerant species held 46.05% of the indoor plants market share in 2025, while medium-light plants are poised for a 6.51% CAGR to 2031.

- By product form, conventional potted plants captured 67.10% of the indoor plants market size in 2025; smart potted and IoT-enabled formats will rise at an 11.20% CAGR to 2031.

- By application, home decoration accounted for a 54.05% share of the indoor plants market size in 2025; air-purification and wellness installations are growing at an 7.92% CAGR through 2031.

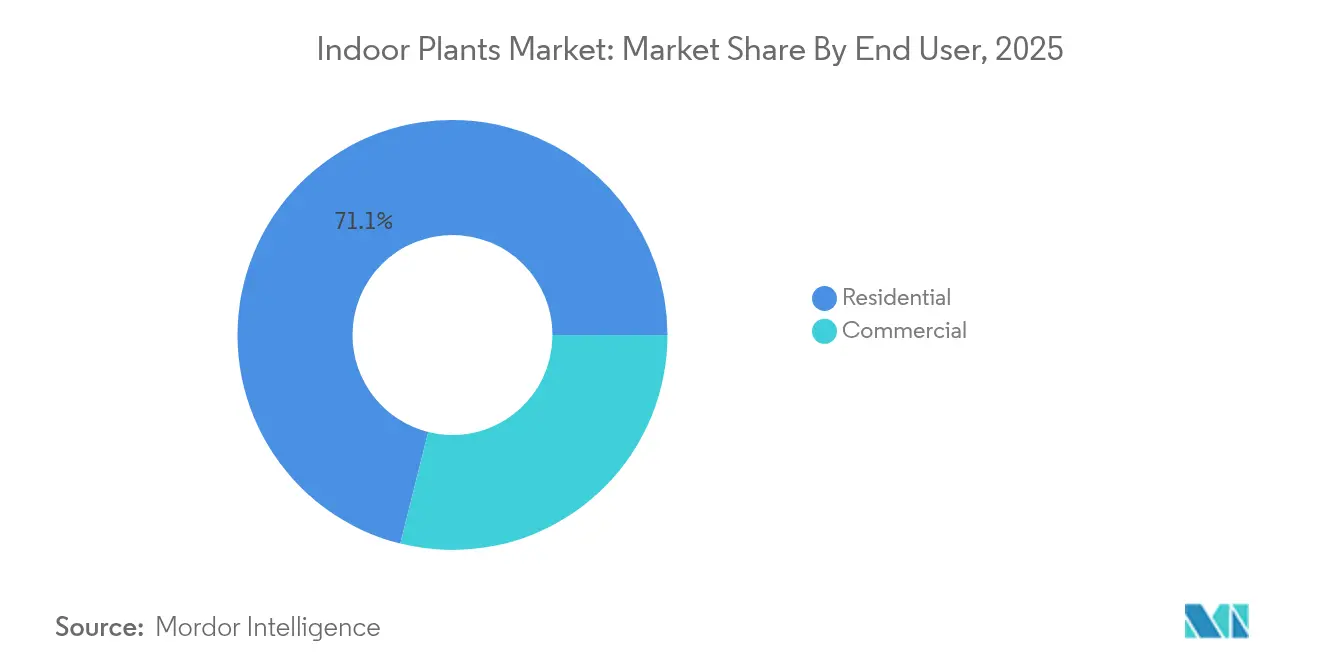

- By end user, residential consumers held 71.10% revenue share in 2025, whereas commercial users are advancing at a 6.05% CAGR in the indoor plants market.

- By distribution channel, garden centers and nurseries retained 50.10% share in 2025, yet online platforms will accelerate at a 10.05% CAGR to 2031 in the indoor plants market.

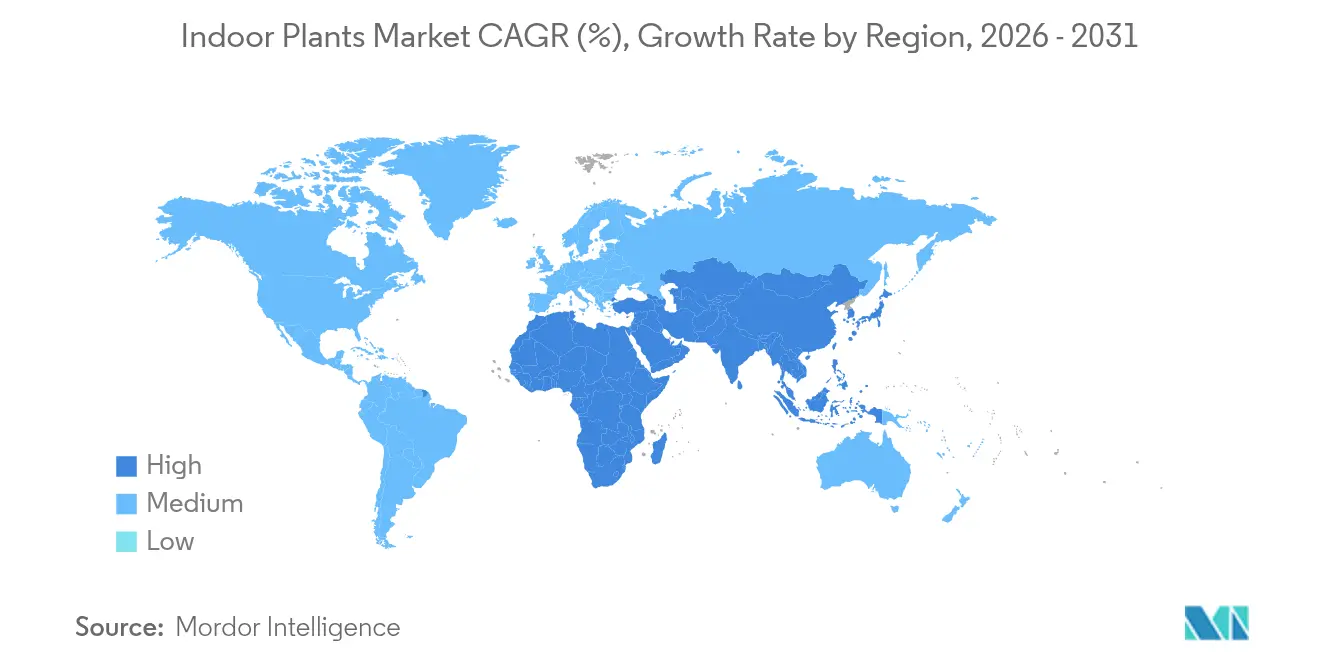

- By region, Asia-Pacific commanded 35.40% of global revenue in 2025 and is forecast to post a 6.65% CAGR to 2031 in the indoor plants market.

- The competitive landscape remains moderately concentrated with Costa Farms, Dummen Orange, Syngenta Flowers, LiveTrends Design Group, and IKEA collectively holds significant market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Indoor Plants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social-media-fueled biophilic interior design trend among Millennials and Gen-Z | +0.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Corporate WELL and LEED certification push integrating greenery in workspaces | +0.6% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Rapid adoption of IoT self-watering and smart planter technologies | +0.5% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Rising consumer focus on indoor air-quality and wellness benefits of plants | +0.4% | Global, with early gains in urban centers | Long term (≥ 4 years) |

| Availability of rare variegated cultivars as aspirational lifestyle assets | +0.3% | North America and Europe, premium segments | Short term (≤ 2 years) |

| Declining price-points through tissue-culture mass propagation | +0.2% | Global, led by Thailand and Indonesia production | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Social-Media-Fueled Biophilic Interior Design Trend Among Millennials and Gen-Z

Social platforms have turned plants into lifestyle signifiers as short-form videos and curated feeds elevate rare foliage and creative planters to viral status. The resulting peer-to-peer influence migrates from homes into co-working hubs, cafes, and boutique hotels, where younger employees and customers expect greenery that mirrors their online aesthetics. Field studies link biophilic interiors to up to 15% productivity gains and 200% higher well-being metrics, offering employers a quantifiable return on greening budgets. Rapid content cycles, however, can create demand spikes followed by sharp price corrections, as seen when tissue-cultured aroids flooded listings after their social-media peak.

Corporate WELL and LEED Certification Push Integrating Greenery in Workspaces

Employers pursuing WELL and LEED credits now view plant installations as baseline infrastructure that signals a commitment to employee wellness and environmental stewardship. Bulk orders, maintenance contracts, and performance guarantees shift purchasing clout toward professional interior-landscaping firms capable of servicing large footprints. Mid-market companies are adopting similar standards to attract talent in competitive labor markets, widening the indoor plants market beyond Fortune 500 budgets. Yet standardized, low-maintenance species often eclipse niche cultivars, tempering upside for specialty growers within corporate supply chains.

Rapid Adoption of IoT Self-Watering and Smart Planter Technologies

Smart planters embed sensors, micro-pumps, and mobile apps that automate watering, nutrient dosing, and micro-climate alerts, lowering the knowledge barrier that once constrained household plant success. Controlled-environment studies show up to 80% yield increases and 80-90% resource savings versus manual care. Subscription refills for nutrients and firmware updates convert one-off product sales into annuity revenue streams. Data harvested from connected devices feeds cultivar-performance analytics, informing future product design. High price points limit the uptake to affluent early adopters for now, but component costs continue to fall.

Rising Consumer Focus on Indoor Air-Quality and Wellness Benefits of Plants

Longer hours spent indoors have amplified awareness of volatile organic compounds and particulate matter. Peer-reviewed trials found that certain foliage combinations can remove up to 87% of micro-pollutants within 24 hours [1]Source: American Society of Landscape Architects, “Plants as Bio-Filters,” asla.org. . Supports premium pricing and larger installations, particularly in healthcare, senior-living, and education facilities where wellness metrics carry budgetary weight. Marketing teams must substantiate claims with lab data to avoid regulatory pushback, raising compliance costs for growers who lack in-house research capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tissue-culture oversupply leading to price compression for growers | -0.4% | Global, strongest impact in Thailand and Indonesia | Short term (≤ 2 years) |

| CITES and phytosanitary regulations restricting trade in exotic species | -0.3% | Global, with complex compliance in EU and North America | Long term (≥ 4 years) |

| High e-commerce return rates due to transit damage and cold-chain gaps | -0.2% | Global, acute in regions with extreme climates | Medium term (2-4 years) |

| Transition to peat-free substrates increasing production costs | -0.2% | Europe-led, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tissue-Culture Oversupply Leading to Price Compression for Growers

High-throughput tissue-culture labs can replicate tens of thousands of clones from scarce mother stock, eroding scarcity premiums on once-exclusive foliage. Rare aroid prices, for instance, fell more than 70% in some markets after large nurseries scaled production. Growers pivot toward volume production or hyper-niche species that resist in-vitro propagation, but lower unit margins strain working-capital cycles and elevate consolidation risk among small operators. Discounted prices nevertheless democratize access, broadening the total addressable base for the indoor plants market.

CITES and Phytosanitary Regulations Restricting Trade in Exotic Species

Permitting, inspection, and documentation demands under CITES add weeks and significant costs to cross-border shipments of protected orchids, cycads, and succulents [2]Source: CITES Secretariat, “Trade Regulations for Endangered Flora,” cites.org. . Legitimate traders invest in compliance specialists and captive tissue-culture facilities to secure legal supply, while inconsistent enforcement allows grey-market channels to persist, skewing price dynamics. Domestic producers able to navigate bureaucratic hurdles gain share, yet smaller boutiques often exit the exotic category, narrowing consumer choice and potentially slowing the indoor plants market, where novelty drives repeat purchasing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plant Type: Foliage Plants Lead Despite Succulent Surge

Foliage plants retained a 41.12% revenue share in 2025, underscoring their versatility across décor, wellness, and corporate installations. The indoor plants market continues to prize broad-leaf species such as monstera and philodendron for their lush visual impact, with tissue-culture advances stabilizing supply and pricing. Succulents and cacti, propelled by low-maintenance appeal, are climbing at a 6.88% CAGR through 2031 as first-time buyers seek hardy options that tolerate irregular care schedules. Flowering varieties, herbs, and aquatics provide seasonal or experiential diversification, yet none threaten the foliage core. Tissue-culture democratization has shifted rare foliage from elite collector circles into mainstream retail, flattening price hierarchies while inflating unit volumes. Specialty breeders respond by launching variegated cultivars and micro-foliage formats aimed at space-constrained urban dwellers. Consumer interest in edible micro-herbs and aromatics adds a functional twist that supports premium tiering, especially when positioned alongside smart countertop hydroponics. The indoor plants market size for foliage categories is forecast to reach USD 6.89 billion by 2031, reflecting both residential replenishment cycles and institutional renovations. Conversely, the succulent’s cohort is expected to command 17.60% of incremental revenue gains, indicating its sustained momentum despite slowing novelty peaks.

By Light Requirement: Low-Light Dominance Reflects Urban Reality

Low-light tolerant species captured 46.05% of the indoor plants market share in 2025, mirroring apartment layouts and deep-plan offices where direct sunlight is scarce. Snake plants, ZZ plants, and pothos anchor this category, thriving under ambient LEDs and sporadic natural light. Demand for medium-light varieties rises alongside cost-effective full-spectrum fixtures, which now retail at price points palatable to mainstream consumers. These LED systems widen viable plant selections, pushing medium-light sales toward a projected 6.51% CAGR. High-light plants remain niche, often restricted to conservatories and sunbelt regions with ample glazing. Breeding programs target chlorophyll efficiency and chloroplast density to enhance shade performance, while smart-lighting algorithms tailor spectrum and intensity to specific cultivars for corporate clients. Urban planners increasingly incorporate vertically mounted low-light greenery in co-living spaces, generating steady replacement orders as tenancy cycles reset. The indoor plants market size for medium-light species is forecast to surpass USD 4.27 billion by 2031, yet the low-light segment will still account for the lion’s share of revenue due to its compatibility with dense city real estate.

By Product Form: Smart Technology Disrupts Traditional Potting

Conventional soil-based pots retained 67.10% revenue in 2025, benefiting from established distribution, low unit costs, and consumer familiarity. However, IoT-enabled and self-watering planters are scaling fast, with an 11.20% CAGR signaling a structural shift in the indoor plants market. Sensor-equipped pots transmit moisture, pH, and temperature data to smartphone dashboards, automating reminders or triggering autonomous watering pumps. Subscription businesses bundle fertilizer pods and firmware updates, stretching customer lifetime value far beyond the initial sale. Hydroponic countertop gardens, once confined to hobbyists, have penetrated big-box retail and online marketplaces, attracting urban renters eager for soil-free freshness. Terrariums and moss-walls continue to flourish in boutique hospitality venues, though growth there is design-project driven rather than volume-led. As component costs decline, smart formats could secure more than 20.00% of the indoor plants market size by 2031, cannibalizing legacy pot sales unless incumbents pivot to hybrid offerings.

By Application Purpose: Wellness Applications Outpace Decoration

Home decor still accounted for 54.05% of 2025 revenue, yet the air-purification and wellness segment is expanding at an 7.92% CAGR as consumers seek tangible health benefits. Scientific endorsements elevating plants as biofilters support higher average selling prices and multi-plant arrays designed around pollutant-removal thresholds. Retail merchandising now groups species by functional claims—stress relief, VOC removal, humidity control—to aid purchase decisions. Commercial interiors integrate large-scale living walls and mandated greenery zones to meet WELL and LEED scoring, stabilizing project pipelines for professional installers. Event planners increasingly rent purpose-grown greenery for temporary installations that enhance attendee well-being metrics. Research and biotech demand rare genotypes for pharmaceutical assays and gene-editing trials, yet they remain a niche contributor to the overall indoor plants market revenue. Decoration-only use cases are expected to relinquish 4.10 percentage points of share by 2031 as wellness-centric messaging captures mindshare and budgets.

By End User: Commercial Segment Accelerates Despite Residential Dominance

Residential buyers preserved 71.10% of sales in 2025, sustained by replenishment cycles, gifting occasions, and the ongoing urban gardening movement. Nevertheless, corporate occupiers, healthcare facilities, and educational institutions are driving the fastest growth at a 6.05% CAGR. Absenteeism cost analyses show ROI horizons under 18 months for plant-based workplace interventions, prompting C-suites to allocate green budgets within human-capital spending. Hospitality brands incorporate lobby jungles and guest-room micro-gardens as differentiators, while retail flagships deploy statement greenery to amplify experiential shopping. Government offices adopt plants to meet carbon-sequestration targets and boost public-space aesthetics. This structural shift redistributes bargaining power toward facility-management firms that bundle plants, maintenance, and reporting into multi-year contracts, gradually professionalizing the demand side of the indoor plants market.

By Distribution Channel: Digital Transformation Accelerates Traditional Retail

Garden centers and nurseries still command a 50.10% share owing to their advisory role and immediate plant quality assurance. E-commerce climbs at 10.05% CAGR, propelled by marketplace platforms, direct-to-consumer brands, and subscription models that simplify care routines. Cold-chain packaging innovations—recyclable honeycomb wraps, phase-change gel packs, shock-absorbent inserts—have reduced transit losses by up to 40%, mitigating the historically high return rates that plagued online plant deliveries. Click-and-collect programs allow customers to inspect specimens before finalizing the purchase, blending digital convenience with tactile reassurance. Brick-and-mortar retailers are responding with livestream advice sessions, augmented-reality placement previews, and loyalty apps offering personalized care prompts. As omnichannel ecosystems mature, the indoor plants market size sold through online channels could approach USD 5.21 billion by 2031, while physical outlets focus on experiential merchandising, workshops, and on-site maintenance services.

Geography Analysis

Asia-Pacific remains the growth engine for the indoor plants market, holding 35.40% of 2025 global revenue and expanding at a 6.65% CAGR to 2031. Rapid urban migration in India, Indonesia, and Vietnam compresses living spaces, cultivating demand for compact, low-light foliage and tabletop hydroponics. India’s domestic sector was valued at USD 11 billion in FY24, with online plant orders projected to rise 30% annually through FY29. China’s Tier-1 cities show an uptick in bulk corporate orders tied to occupational-health directives, while Japanese retailers emphasize smart-planter bundles for senior consumers seeking low-maintenance wellness solutions.

North America exhibits a mature yet evolving profile. Corporate wellness mandates, combined with steady disposable incomes, are tilting demand toward premium IoT-enabled devices and rare collector cultivars. U.S. horticultural clusters in California and Florida supply year-round production, but rising labor costs accelerate automation investments in propagation and fulfillment. Strict phytosanitary regimes favor domestic propagation and tissue-culture labs, indirectly boosting local employment and shortening lead times.

Europe commands sophisticated consumer expectations around sustainability. Imports of ceramic planters climbed from EUR 2.7 billion in 2018 to EUR 3.9 billion in 2022 . The Netherlands leverages advanced greenhouse infrastructure and logistics to serve as the continent’s distribution nerve-center, exporting finished plants across the EU within 24 hours of harvest. Germany tops consumption volumes, although France and the Nordics display faster corporate uptake linked to strict indoor-air-quality legislation. Peat-free regulations increase production costs but also unlock premium “eco-substrate” positioning. Eastern European markets remain under-penetrated, representing a medium-term expansion frontier as disposable incomes climb.

Competitive Landscape

The indoor plants market remains moderately fragmented, with Costa Farms, Dümmen Orange, Syngenta Flowers, LiveTrends Design Group, and IKEA leading yet collectively holding well under 40% of global revenue. Scale advantages in propagation, greenhouse automation, and nationwide distribution give these incumbents a head start, but barriers to entry stay low for niche specialists leveraging direct-to-consumer channels or proprietary breeding IP. The USDA’s relaxed genomic-editing rule—allowing up to 12 simultaneous trait modifications when achieved through conventional breeding methodologies—slashes R&D timelines for pest resistance, compact growth habits, and enhanced leaf coloration.

Technology serves as the new competitive divider. Start-ups integrating capacitive soil sensors, Bluetooth Low-Energy modules, and AI-driven care algorithms capture tech-savvy buyers and corporate facilities demanding measurable performance. Established growers counterbalance by rolling out in-house smart lines or partnering with electronics firms for co-branded devices. Meanwhile, logistics innovators supplying shock-absorbent biodegradable packaging see accelerated uptake from both pure-play e-tailers and legacy nurseries pivoting online.

Strategic moves underscore the sector’s dynamism. Cibus Capital injected over USD 600 million into sustainable agriculture and controlled-environment robotics in 2024, including a majority stake in Dutch robotic arm maker ISO Group. Proven Winners expanded U.S. greenhouse capacity and unveiled the leafjoy houseplant range with 100 new SKUs for 2025, bundling plants with bio-based support structures to target eco-conscious consumers. These initiatives reflect a broader shift toward vertically integrated models that link propagation, automation, branding, and data analytics in one consolidated value chain.

Indoor Plants Industry Leaders

Costa Farms

Dümmen Orange

Syngenta Flowers

LiveTrends Design Group

IKEA (Indoor Greenery Line)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Cibus Capital closed USD 600 million across its agriculture funds and acquired Dutch robotics firm ISO Group to accelerate automation for indoor vegetable and flower growers.

- March 2024: Proven Winners boosted greenhouse capacity and introduced 100 leafjoy houseplant varieties for 2025, pairing them with natural-material support systems to meet eco-friendly consumer demand.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the indoor-plants market as the sale value of live, rooted plants purpose-grown to thrive inside homes, offices, and public buildings where temperature, light, and humidity are actively managed. This spans foliage, flowering, succulents, cacti, herbs, aquatic, and smart-potted variants sold through offline nurseries, home-improvement retailers, supermarkets, and online channels.

Scope exclusion: Landscaping trees, cut flowers, and artificial or preserved arrangements sit outside Mordor's definition.

Segmentation Overview

- By Plant Type

- Foliage Plants

- Flowering / Ornamental Plants

- Succulents & Cacti

- Herbs & Edible Indoor Plants

- Aquatic Indoor Plants

- Artificial & Preserved Indoor Plants

- By Light Requirement

- Low Light (Shade-loving)

- Medium / Indirect Light

- High / Direct Light

- By Product Form

- Potted Soil-based

- Hydroponic / Water-based

- Terrariums & Miniature Landscapes

- Smart Potted / IoT-enabled

- By Application Purpose

- Air Purification & Wellness

- Home & Interior Decoration

- Commercial & Corporate Landscaping

- Gifting & Events

- Research & Biotechnology

- By End User

- Residential

- Commercial

- Offices & Co-working Spaces

- Hospitality

- Healthcare Facilities

- Educational Institutions

- Retail & Shopping Malls

- Government & Public Infrastructure

- By Distribution Channel

- Offline

- Garden Centers & Nurseries

- Home Improvement & DIY Stores

- Supermarkets / Hypermarkets

- Specialty Boutiques & Concept Stores

- Online

- E-commerce Marketplaces

- Direct-to-Consumer Brand Websites

- Subscription Services

- B2B Horticulture Platforms

- Offline

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed nursery managers, online plant-store founders, facility designers, and horticulture-extension officers across North America, Europe, and Asia-Pacific. These conversations clarified average selling prices, wastage rates, and seasonality, and they validated early model outputs drawn from desk work.

Desk Research

We began with publicly available horticulture statistics from FAO, USDA, Eurostat, and national customs portals, which trace cross-border plant trade and nursery receipts. Reports from the World Bank on urbanization and disposable income trends, EPA indoor-air guidelines, and trade-association updates (e.g., National Garden Bureau) enriched context. Company filings and retailer presentations helped us map channel margins, while D&B Hoovers and Dow Jones Factiva supplied financial clues on leading growers and e-commerce specialists. Questel patent pulls signaled cultivar innovation. The sources listed illustrate key inputs; many more were reviewed before numbers were finalized.

Market-Sizing & Forecasting

A top-down build started with horticulture production and import data, reconstructed into an indoor-only demand pool through penetration ratios for residential units and commercial floor space. Select bottom-up checks sampled supplier revenue roll-ups and channel ASP × volume tests tempered the totals. Key variables include new urban housing completions, disposable income per capita, office fit-out spending, e-commerce share of plant sales, and average plant replacement cycles. Multivariate regression underpins the 2025-2030 forecast, with coefficient bands tuned to consensus gathered during expert calls. Where retailer roll-ups were thin, we filled gaps by applying region-specific ASP corridors derived from transaction scans.

Data Validation & Update Cycle

Outputs pass three layers of analyst review; anomaly screens flag swings above preset thresholds, and any material variance triggers a call-back to respondents. Every study refreshes annually; interim updates follow major policy changes, pest outbreaks, or supply-chain shocks.

Why Mordor's Indoor Plants Baseline Earns Trust

Published figures often diverge because firms choose unlike scopes, price points, and refresh cadences. Our team sets a narrower lens: live potted plants only, measured at retail value in 2025 dollars, before any modeling starts.

Key gap drivers versus other publishers include: some fold artificial décor into totals, others mix greenhouse wholesale with retail mark-ups, a few apply aggressive inflation escalators, and many carry forward pre-pandemic patterns without new channel checks. Mordor's yearly update and dual-track validation dilute those risks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.12 B (2025) | Mordor Intelligence | - |

| USD 20.68 B (2024) | Regional Consultancy A | Includes artificial décor and gardening accessories |

| USD 22.60 B (2025) | Global Consultancy A | Uses farm-gate output plus vertical-farming crops |

| USD 19.43 B (2023) | Industry Association B | Older base year and simple currency deflator, no channel split |

In sum, our disciplined scoping, frequent refresh, and blended top-down/bottom-up testing give decision-makers a balanced, traceable baseline that aligns more closely with purchase realities than the broader, occasionally inflated values published elsewhere.

Key Questions Answered in the Report

What is the current value of the indoor plants market?

The indoor plants market generated USD 13.61 billion in 2026 and is forecast to reach USD 16.36 billion by 2031 at a 3.75% CAGR.

Which region leads the indoor plants market?

Asia-Pacific held 35.40% of global revenue in 2025 and is also the fastest-growing region, advancing at a 6.65% CAGR through 2031.

Who are the key players in Indoor Plants Market?

Dümmen Orange (U.S.), Syngenta Crop Protection AG (Switzerland), Beekenkamp Group (Netherlands), Hofland Flowering Plants (Netherlands) and Sakata Seed America (U.S.) are the major companies operating in the Indoor Plants Market.

Why are smart planters gaining popularity?

IoT-enabled planters automate watering and nutrient delivery, reduce care errors, and come with subscription models that extend product support, resulting in an 11.20% CAGR for the segment.

How are corporate wellness programs influencing demand?

WELL and LEED certification criteria include greenery requirements, prompting bulk purchases and maintenance contracts that expand commercial installations at a 6.05% CAGR.

What challenges does online plant retail face?

High return rates from transit damage have historically impeded growth, but advances in shock-absorbing, temperature-regulated packaging are cutting losses and supporting a 10.05% CAGR for e-commerce channels.

How are regulations affecting the trade in exotic plants?

CITES permits, phytosanitary inspections, and compliance costs lengthen lead times and raise expenses, particularly for rare orchids and cycads, dampening growth for specialty importers while favoring domestic propagation.

Page last updated on: