Market Overview

| Study Period | 2020 - 2031 |

|---|---|

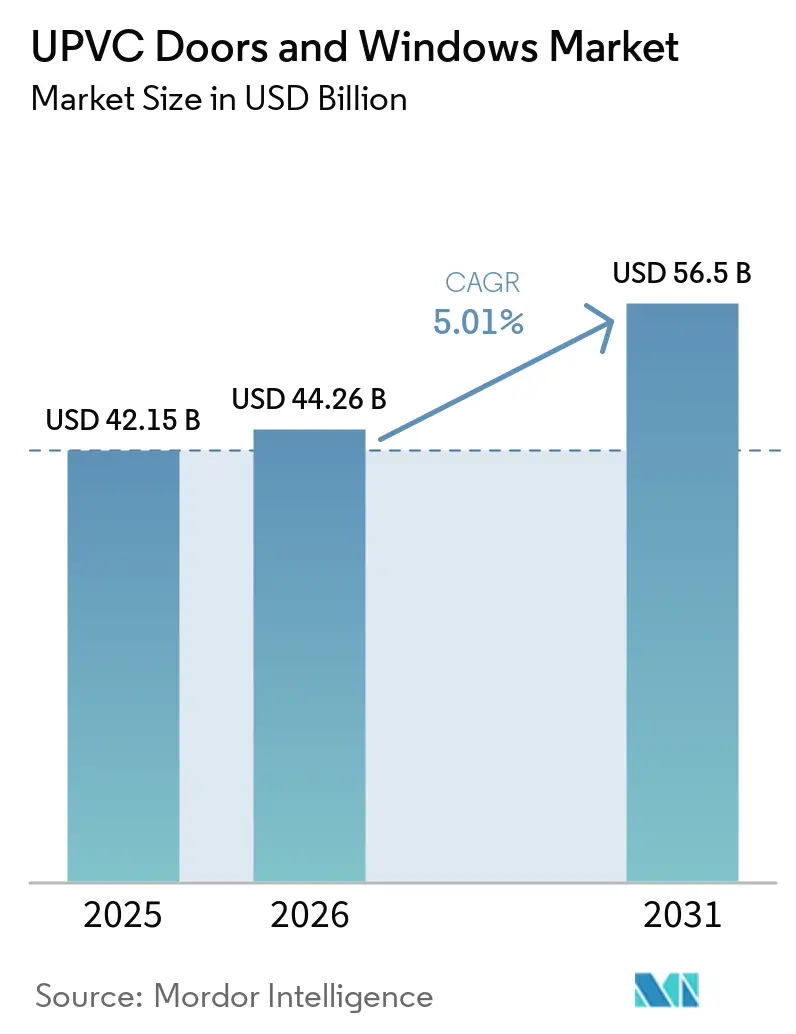

| Market Size (2026) | USD 44.26 Billion |

| Market Size (2031) | USD 56.5 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

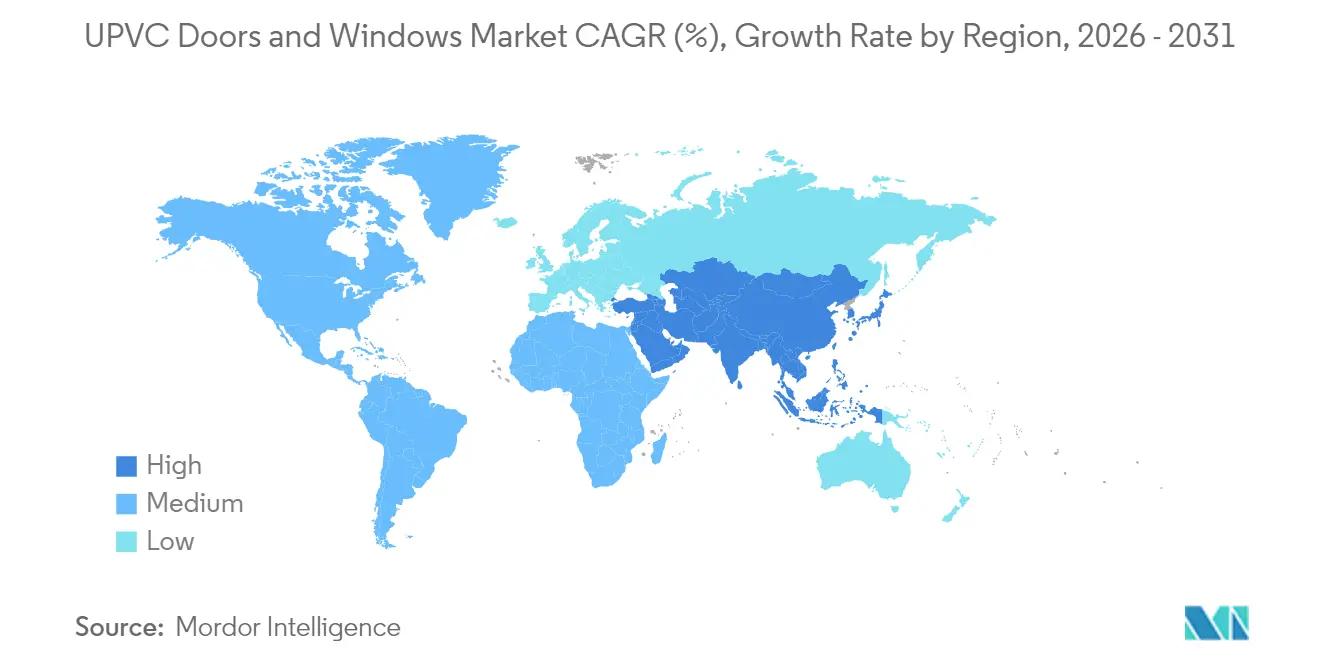

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UPVC Doors and Windows Market Analysis by Mordor Intelligence

The UPVC doors and windows market size was valued at USD 42.15 billion in 2025 and estimated to grow from USD 44.26 billion in 2026 to reach USD 56.5 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031). Heightened energy-efficiency codes, synchronized across large economies, position UPVC profiles as a mainstream choice rather than a regional alternative. Regulatory convergence, from the European Union’s zero-emission requirement for new buildings by 2030 to California’s Title 24 revisions, yields a global baseline for thermal performance that favors multi-chamber UPVC systems. Construction digitalization is reinforcing that pull by making performance data transparent to architects who increasingly specify products proven to lower operating costs. Supply chains are adapting, with localized extrusion capacity rising in high-growth regions to shield margins from resin price swings tied to petroleum markets. Meanwhile, sustained renovation cycles in mature economies and robust greenfield activity in emerging markets combined to give the UPVC doors and windows market a diversified demand base that reduces cyclicality.

Key Report Takeaways

- By product type, UPVC windows captured 61.10% of the UPVC doors and windows market share in 2025; UPVC doors are forecast to post a 6.82% CAGR between 2026 and 2031.

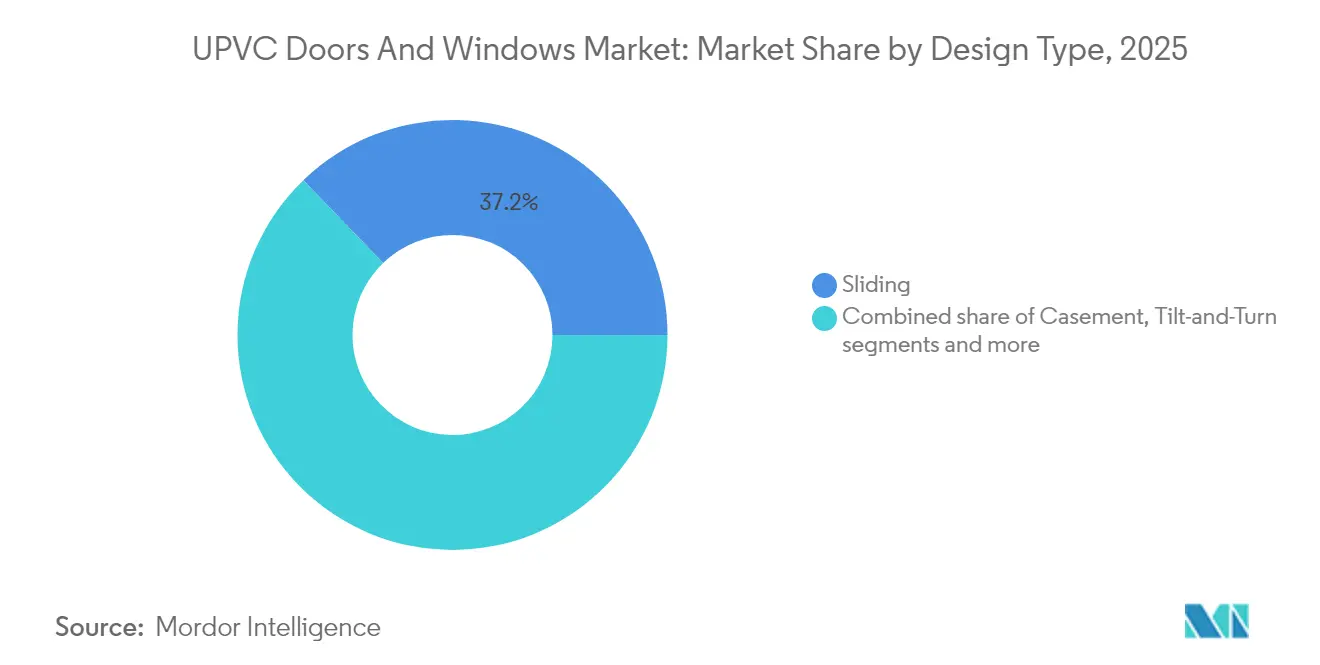

- By design, sliding configurations accounted for 37.20% revenue in 2025, while tilt-and-turn systems are projected to expand at a 6.05% CAGR through 2031.

- By installation, replacement, and renovation, represented 55.20% of the UPVC doors and windows market size in 2025; new construction is set for a 5.21% CAGR to 2031.

- By end-user, the residential segment held 68.12% revenue in 2025, whereas commercial installations are expected to grow at a 5.74% CAGR over the same horizon.

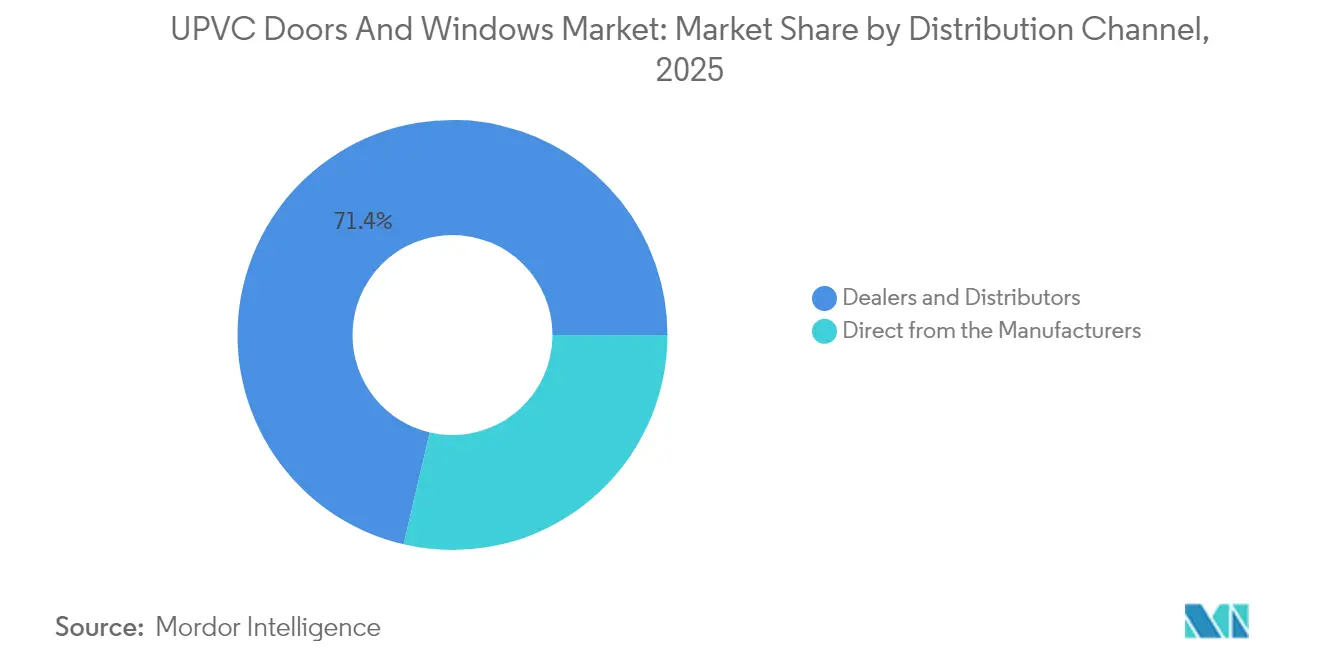

- By distribution channel, dealers and distributors commanded 71.35% of 2025 revenue and are on course for a 6.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UPVC Doors and Windows Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Energy-efficiency Codes in New-build Housing | +1.2% | Global, with EU and North America leading adoption | Medium term (2-4 years) |

| Rising Mid-income Urban Renovation Spend in APAC | +0.8% | APAC core, spill-over to emerging markets | Long term (≥ 4 years) |

| Post-pandemic Home-office Conversions in North America | +0.6% | North America, with secondary impact in Europe | Short term (≤ 2 years) |

| Insurance Incentives for High-impact-resistant Fenestration | +0.4% | Coastal regions globally, concentrated in North America | Medium term (2-4 years) |

| AI-driven Mass-customisation Platforms for Dealers | +0.3% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Emerging Carbon-credit Schemes Rewarding High-recycled-content UPVC | +0.2% | Europe leading, expanding to North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Energy-efficiency Codes in New-build Housing

Global building regulations are converging on performance benchmarks that can only be met by multi-chambered, thermally-broken UPVC profiles. The United Kingdom’s Future Homes Standard, effective 2025, lowers the maximum window U-value to 1.2 W/m²K, a shift that compels builders to select advanced UPVC systems over commodity double-glazed frames[1]REHAU, “Future Homes Standard and Window U-Values,” rehau.com. Comparable performance thresholds are being tabled in several United States, Canada, and the European Union’s revision of the Energy Performance of Buildings Directive, all of which collectively convert compliance budgets into predictable, high-margin volume for the UPVC doors and windows market. Suppliers that can validate profile thermal simulation data and secure early certification stand to gain price premiums, while fabricators failing to retool face margin compression as code cycles shorten.

Rising Mid-income Urban Renovation Spend in APAC

The demographic surge in the Asia-Pacific’s middle class is reshaping renovation demand. Households in China, India, and five major ASEAN economies allocate a rising share of income to existing-home upgrades, and windows top the energy-efficiency priority list because air-conditioning costs account for up to 40% of household electricity bills in tropical regions. UPVC’s low-maintenance surfaces and resistance to termite damage resonate with homeowners accustomed to humid climates, creating a durable pull-through for the UPVC doors and windows market. Dealers that bundle project financing see higher close rates, underscoring the importance of consumer credit ecosystems in unlocking deferred renovation demand across APAC.

Post-pandemic Home-office Conversions in North America

Hybrid work is now a structural labor pattern, not a stopgap arrangement, and this permanence is being monetized through home-office retrofits focused on daylighting, acoustic comfort, and insulation. UPVC profiles integrated with triple-pane IGUs reduce HVAC energy load and cut exterior noise by 45 dB, performance gains that align with worker productivity metrics cited by employers offering home-office stipends[2]Home Improvement Research Institute, “North American Renovation Outlook 2025,” homeimprovementresearchinstitute.org. The effect is a renovation upswing that compensates for lower single-family housing starts, cushioning North American volume. Given the regional preference for do-it-yourself channels, manufacturers are ramping supply of pre-glazed units sized to pass through standard doorways to facilitate single-trip installation.

Insurance Incentives for High-impact-resistant Fenestration

Wind-borne debris accounts for 70% of residential hurricane claims in the United States Gulf Coast, pushing insurers to subsidize resilient fenestration. Programs in Louisiana and Florida offer premium credits ranging from 35% to 55% for windows certified to the FORTIFIED Gold standard. Because UPVC frames can integrate laminated IGUs without galvanic corrosion, a risk for aluminum, they dominate the coastal specification lists. This alignment of risk-transfer economics and material science places the UPVC doors and windows market in a virtuous subsidy loop: as more households install compliant systems, aggregate losses drop, reinforcing the underwriting logic behind the incentive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UPVC Price Volatility Linked to Oil-derived Resin | -0.6% | Global, with particular impact on price-sensitive markets | Short term (≤ 2 years) |

| Stringent Fire-safety Codes in High-rise Construction | -0.4% | Global urban centers, with stricter enforcement in developed markets | Medium term (2-4 years) |

| Growing ESG Pushback Against Chlorinated Polymers | -0.5% | Europe and North America leading, spreading globally | Long term (≥ 4 years) |

| Waste-management & Recycling Constraints for End-of-Life UPVC | -0.3% | Europe leading regulatory requirements, expanding to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

UPVC Price Volatility Linked to Oil-derived Resin

UPVC resin prices track ethylene and chlorine inputs derived from petroleum, leading to quarterly swings exceeding 20% whenever crude futures spike. Fabricators with forward contracts absorb some volatility yet still pass through cost increments that make project budgeting unpredictable in price-sensitive emerging markets. The volatility dampens bidding competitiveness for large public tenders that lock prices 9-12 months ahead, temporarily steering demand toward aluminum, where alloy surcharges are more transparent.

Growing ESG Pushback Against Chlorinated Polymers

Corporate buyers active in green-bond financing increasingly screen out chlorinated polymers from their material palettes. Nordic Swan Ecolabel requirements limit allowable additives and demand documented end-of-life pathways, placing compliance burdens on UPVC suppliers[3]Nordic Swan Ecolabel, “Window and Door Material Criteria,” nordicswanecolabel.org. Although recycling initiatives like VinylPlus mitigate the perception, ESG committees remain cautious, slowing specification approvals in commercial projects financed through sustainability-linked loans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Doors Accelerate as Windows Retain Scale

UPVC windows held a commanding 61.10% share of the UPVC doors windows market in 2025, a leadership position rooted in decades of code-driven thermal upgrades and homeowner familiarity with tilt, casement, and sliding variants. Segment revenue climbed steadily as multi-glazed configurations raised average selling prices faster than extrusion costs, allowing fabricators to widen gross margins while preserving price accessibility versus wood-clad composites. The UPVC doors and windows market size for windows is forecast to expand at a steady clip as urban mid-rise housing retrofits specify triple-pane units to meet post-2025 energy benchmarks.

UPVC doors, though smaller in volume, are set for a 6.82% CAGR through 2031, led by commercial storefronts and residential patio expansions that demand large, thermally stable panels. Security glazing compliance with EN 1627 burglar-resistance grades boosted the perceived value of polymer doors in multifamily lobbies, where dwell time of occupants requires higher acoustic and thermal comfort. Door fabricators are cross-leveraging window profile platforms to achieve scale economies, enabling bundled quoting that erodes historical price premiums of competing aluminum systems. As architects in North America adopt European-style lift-and-slide and tilt-and-turn entrance systems, door volumes are converting from niche to mainstream, extending the value ladder within the UPVC doors and windows market.

By End-use Sector: Commercial Growth Outpaces Residential Base

Residential buyers contributed 68.12% of 2025 sales. Awareness campaigns and smart-home bundling raise acceptance, especially among first-time homeowners value low maintenance.. Long replacement intervals, historically 25 years, are shortening to 18–20 years as consumers trade older double-glazed frames for triple-pane, low-E upgrades eligible for utility rebates. That cadence keeps residential demand resilient, even during mortgage-rate spikes that temporarily suppress housing starts. Builders in high-latitudes Canada and Scandinavia increasingly pre-install UPVC fenestration to lower building energy intensity, extending the baseline for the UPVC doors and windows market.

Commercial demand, although smaller in absolute terms, is projected to grow faster at a 5.74% CAGR. Growth engines include mixed-use high-rise developments in the Middle East and data centers in North America that demand tight thermal envelopes to optimize HVAC loads. Facility managers are recalibrating total-cost-of-ownership models by assigning a higher weight to maintenance savings; UPVC’s resistance to salt spray and airborne pollutants delivers lifecycle cost advantages of up to 30% versus anodized aluminum. This recalibration reinforces a structural shift that places commercial buyers at the vanguard of premium feature adoption, impact-graded glass, integrated motorized blinds, and smart-lock-ready door systems, thereby enhancing value density per square foot.

By Design Type: Tilt-and-Turn Systems Challenge Sliding Dominance

Sliding windows, entrenched in space-constrained apartment design, retained 37.20% revenue share in 2025, reflecting their cost efficiency and minimal projection into rooms or balconies. Manufacturers have improved their air-and-water infiltration performance via dual weather seals, preserving relevance in regions with moderate climate loads. Strong condominium pipelines in Southeast Asia and South America assure a healthy baseline for slide configurations within the UPVC doors and windows market.

Tilt-and-turn profiles, expanding at 6.05% CAGR, offer dual-function ventilation and full egress, features that resonate in post-pandemic building layouts emphasizing air quality. Tilt for secure night ventilation and turn for full egress. Fabricators are engineering deeper sash profiles, 3.25 inches, to accommodate North American wall assemblies and adding nail fins that match local installation practices. Smart-home integration further propels adoption, as tilt sensors pair easily with building management systems to regulate ventilation based on CO₂ levels. Sliding’s volume advantage will persist, yet the design mix is tilting toward tilt-and-turn for value-oriented performance upgrades, reinforcing diversification within the UPVC doors windows market.

By Installation Type: Replacement Market Provides Stability

Replacement and renovation work represented 55.20% of 2025 demand, a testament to the aging housing stock in North America and Western Europe, where more than 65% of homes were built before 2000. Rising energy tariffs, coupled with the availability of on-bill financing, encourage homeowners to prioritize window upgrades that can cut heating and cooling costs by up to 22%. Insurance premium deductions for impact-rated glazing provide an additional monetary lever in coastal states, further embedding replacement volumes as an all-weather pillar of the UPVC doors and windows market.

New construction, though inherently more cyclical, is positioned for a 5.21% CAGR through 2031. Urbanization in India and Nigeria, as well as large mixed-use projects aligned with Saudi Arabia’s Vision 2030, generate greenfield demand pockets with long planning horizons. In these projects, UPVC’s light weight simplifies logistics in high-rise construction, where crane time is a cost driver. Because new-build codes in emerging markets rapidly align with International Energy Conservation Code standards, builders are leapfrogging directly to thermally enhanced UPVC systems, ensuring that the technology is not merely a replacement choice but also the default new-build option in several geographies.

By Distribution Channel: Dealer Networks Sustain Reach

In 2025, dealers and distributors accounted for 71.35% of the revenue, underscoring the importance of site measurement, code knowledge, and after-sales support in fenestration projects. These channels play a pivotal role in ensuring seamless project execution, as they bridge the gap between manufacturers and end-users. Due to AI-enhanced portals, dealers now access real-time inventory and configuration tools, allowing them to generate customized quotes in hours instead of days. This newfound efficiency strengthens their outlook, projecting a 6.38% CAGR. Additionally, the integration of advanced technologies has enabled dealers to better manage customer expectations and streamline operations, further solidifying their dominance in the market.

Channels purchasing directly from manufacturers prioritize volume contracts, particularly in public-housing rollouts. Here, buying decisions hinge on standardized SKUs and long-term warranties. While this channel represents a minority share, it plays a crucial role in ensuring baseline factory utilization during sluggish retail cycles. Moreover, it adds a layer of diversification to the go-to-market strategies of the UPVC doors and windows industry. By focusing on large-scale contracts, manufacturers can maintain consistent production levels and mitigate risks associated with fluctuating retail demand. This approach not only supports operational stability but also enhances the industry's ability to cater to diverse customer segments.

Geography Analysis

Asia-Pacific dominated the UPVC doors and windows market with 44.10% revenue share in 2025, and its trajectory remains robust as urban populations concentrate in megacities that pursue aggressive energy-efficiency targets. China’s retrofit subsidies and India’s Pradhan Mantri Awas Yojana housing mission collectively underpin multi-year project pipelines, amplifying base volumes. Mature markets such as Japan and Australia add stability through stringent building codes that favor low-maintenance fenestration. Regional climatic diversity, typhoon-prone coasts, and alpine interiors demand profile versatility, a requirement that encourages global suppliers to localize extrusion plants and co-develop tropicalized gasket materials with petrochemical partners.

Middle East & Africa is forecast to clock the fastest 5.67% CAGR, riding on a USD 3.7 trillion project pipeline that includes NEOM, Red Sea Global, wealth fund-backed, and multiple LNG hubs. Harsh desert temperatures and dust storms accentuate the performance gap between powder-coated aluminum and UV-stabilized UPVC, prompting specification shifts in hospitality and high-end residential towers. The region’s sovereign wealth fund-backed developers also articulate net-zero ambitions, pushing for thermally superior glazing that reduces mechanical cooling loads. Local extruders partnering under technology-transfer agreements can tap import-substitution demand, accelerating the localization of the uPVC doors and windows market supply chain.

Europe remains a volume-dense yet mature territory where regulation, rather than sheer construction growth, dictates market direction. The Future Homes Standard in the United Kingdom creates a near-term spike in profile demand, while Nordic Ecolabel compliance requirements steer procurement toward recycled-content UPVC. Germany’s Building Energy Act drives triple-pane adoption, keeping replacement cycles active despite flat housing starts. North America’s growth is steadier, fueled by coastal replacement projects and tilt-and-turn migration. South America, though smaller, shows upside as public-sector housing programs in Brazil integrate energy-efficiency targets that align naturally with UPVC’s cost-performance profile.

Competitive Landscape

Global UPVC doors windows market structure is moderately consolidated, with the top five suppliers controlling just under half of installed capacity. These leaders integrate resin polymerization, profile extrusion, takeover, and hardware fabrication, thus insulating gross margins from commodity feedstock swings. Strategic acquisitions, MITER Brands’ USD 3.1 billion purchase of PGT Innovations in 2024 and Pella’s Weather Shield take-over in 2025, signal a pivot toward platforms capable of serving every performance tier from entry-level vinyl to impact-resistant, high-design-pressure systems.

Technology is the critical battleground. Factories equipped with robotic welder-cleaners achieve cycle-time cuts that unlock same-day order fulfillment for dealer pick-ups. AI-enabled design portals deliver instant pricing, and early adopters report dealer conversion rates rising by 15 percentage points. Firms lagging on automation struggle with labor shortages and are increasingly attractive targets for roll-ups. Product innovation is equally intense. Triple-gasket co-extrusion, color-fast PMMA capstocks, and welded-corner look-alike mechanical joins answer architectural aesthetics without compromising weld integrity, expanding addressable premium segments within the UPVC doors and windows market.

Sustainability credentials are turning into formal tender prerequisites, especially in Europe. Manufacturers with take-back programs that guarantee cradle-to-cradle certification gain a bidding advantage, while smaller extruders lack the scale to invest in closed-loop logistics. This divide is likely to widen as the European Commission moves ahead with product environmental footprint labeling. Overall, the competitive landscape rewards vertical integration, digital fluency, and verifiable ESG compliance, giving well-capitalized incumbents a defensible moat yet leaving space for specialized entrants focused on circular-economy niches.

UPVC Doors and Windows Industry Leaders

VEKA AG

Deceuninck NV

Rehau Group

LIXIL Group (Tostem)

Profine GmbH (Kömmerling)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Pella acquired Weather Shield and expanded its distribution network through strategic partnerships, strengthening its position in premium fenestration markets.

- March 2025: MITER Brands completed its USD 3.1 billion acquisition of PGT Innovations, creating a comprehensive fenestration platform that combines MITER’s operational footprint with PGT’s impact-resistant technologies.

- February 2025: VEKA Germany, a global leader in the UPVC profile industry, successfully acquired 100% ownership of the Company, marking VEKA’s unwavering commitment to the Indian market and its confidence in India’s rapidly expanding construction, real estate, and infrastructure sectors.

- January 2025: Andersen Corporation divested its Silver Line and American Craftsman vinyl window brands to Ply Gem for USD 190 million, including four manufacturing plants and over 4,000 employees.

Global UPVC Doors and Windows Market Report Scope

UPVC, or unplasticized polyvinyl chloride, is a low-maintenance and cost-effective material used in building and construction, especially in pipework and window frames. The report covers a complete background analysis of the UPVC doors and windows market. It includes an assessment of the UPVC doors and windows markets worldwide, emerging trends by segments and regional markets, and significant changes in market dynamics and market overview. The report also features qualitative and quantitative assessments that analyze the data gathered from industry analysts and market participants across key points in the industry's value chain.

The UPVC doors and windows market is segmented by product type, end-user, distribution channel, and geography. By product type, the market is sub-segmented into UPVC doors and UPVC windows. By end user, the market is sub-segmented into residential, commercial, industrial, construction, and other end users. By distribution channel, the market is sub-segmented into offline stores and online stores, and by geography, the market is sub-segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. The report offers market size and values in (USD) during the forecast years for the above segments.

By Product Type

| UPVC Windows |

| UPVC Doors |

By Design Type

| Sliding |

| Casement |

| Tilt-and-Turn |

| Others (French, Awning, etc.) |

By Installation Type

| New Construction |

| Replacement & Renovation |

By End-user

| Residential |

| Commercial |

| Industrial & Infrastructure |

By Distribution Channel

| Direct from the Manufacturers |

| Dealers and Distributors |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | UPVC Windows | |

| UPVC Doors | ||

| By Design Type | Sliding | |

| Casement | ||

| Tilt-and-Turn | ||

| Others (French, Awning, etc.) | ||

| By Installation Type | New Construction | |

| Replacement & Renovation | ||

| By End-user | Residential | |

| Commercial | ||

| Industrial & Infrastructure | ||

| By Distribution Channel | Direct from the Manufacturers | |

| Dealers and Distributors | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the forecast value of the UPVC doors and windows market by 2031?

The UPVC doors and windows market size to reach USD 56.5 billion, supported by a 5.01% CAGR.

Which region will grow the fastest through 2031?

The Middle East & Africa is expected to register the highest 5.67% CAGR, propelled by mega-projects and net-zero building codes.

Why do builders prefer UPVC over aluminum in new energy-code projects?

UPVC meets strict U-value targets without costly thermal breaks, lowering life-cycle energy consumption and installed cost.

How large was the residential share in 2025?

Residential applications accounted for 68.12% of global revenue, driven by renovation programs and smart-home upgrades.

What incentives support impact-resistant UPVC windows?

Insurance premium reductions of up to 30% in hurricane-prone regions shorten payback periods and stimulate adoption.

Page last updated on: