North America Siding And Decking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

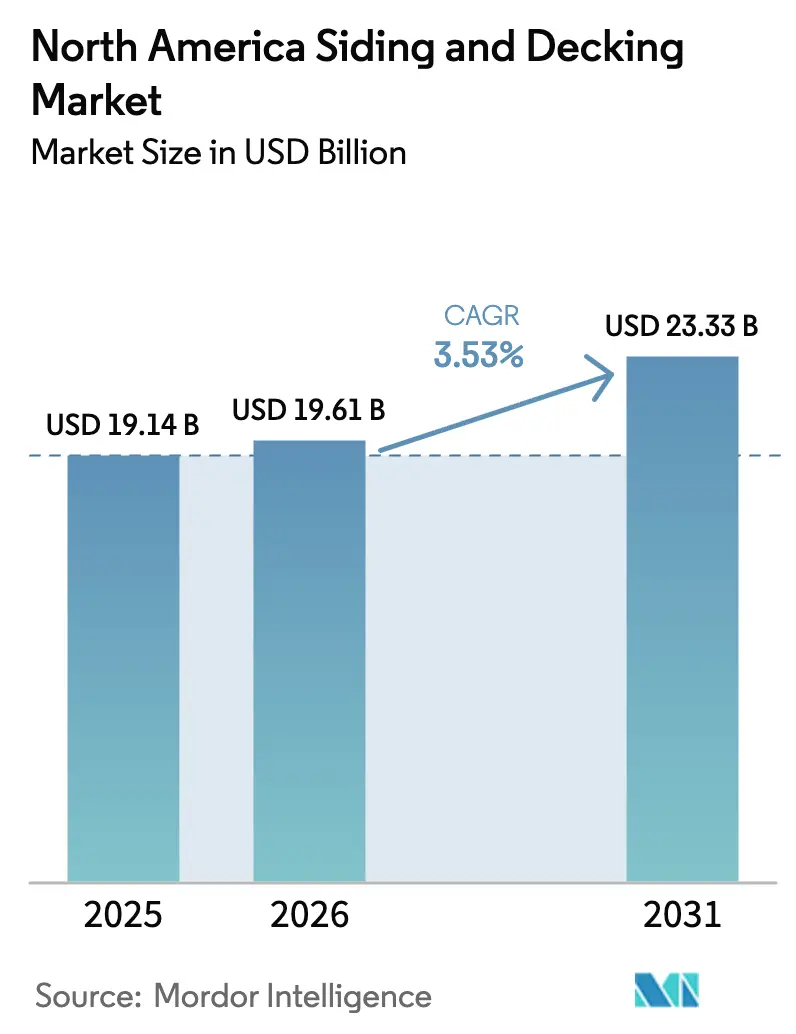

| Base Year Market Size (2025) | USD 19.14 Billion |

| Market Size (2026) | USD 19.61 Billion |

| Market Size (2031) | USD 23.33 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

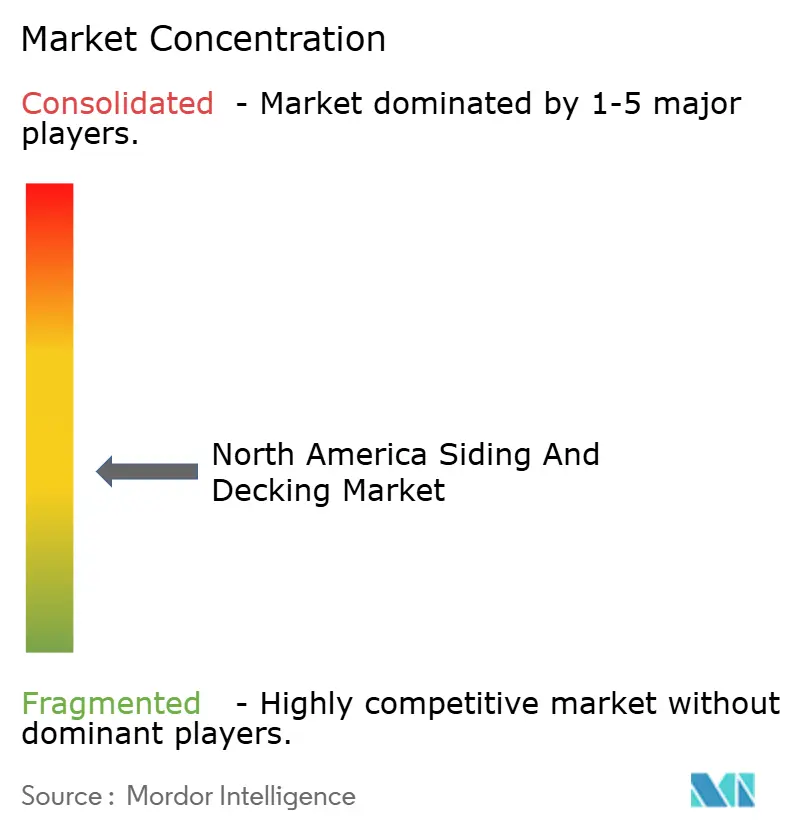

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Siding And Decking Market Analysis by Mordor Intelligence

The North America Siding And Decking Market size is projected to be USD 19.14 billion in 2025, USD 19.61 billion in 2026, and reach USD 23.33 billion by 2031, growing at a CAGR of 3.53% from 2026 to 2031.

Vinyl regained the lead in United States new-home exteriors in 2024, climbing to a 26% share of principal wall materials, while fiber cement reached 23%, signaling sustained conversion toward low-maintenance cladding[1]National Association of Home Builders, “Stucco No Longer Most-Used Exterior Wall Material,” NAHB, nahb.org. Energy-efficiency requirements under the 2024 International Energy Conservation Code and California’s 2025 standards, effective in 2026, are elevating demand for insulated and higher-performance building envelopes. Wildfire-resilience guidance that prioritizes noncombustible cladding is influencing material selection in risk-exposed regions, with insurers increasingly tying coverage to hardened assemblies. Labor constraints and installation cost inflation continue to push factory-fabricated, panelized siding and modular deck systems that reduce skilled labor hours and compress construction timelines.

Key Report Takeaways

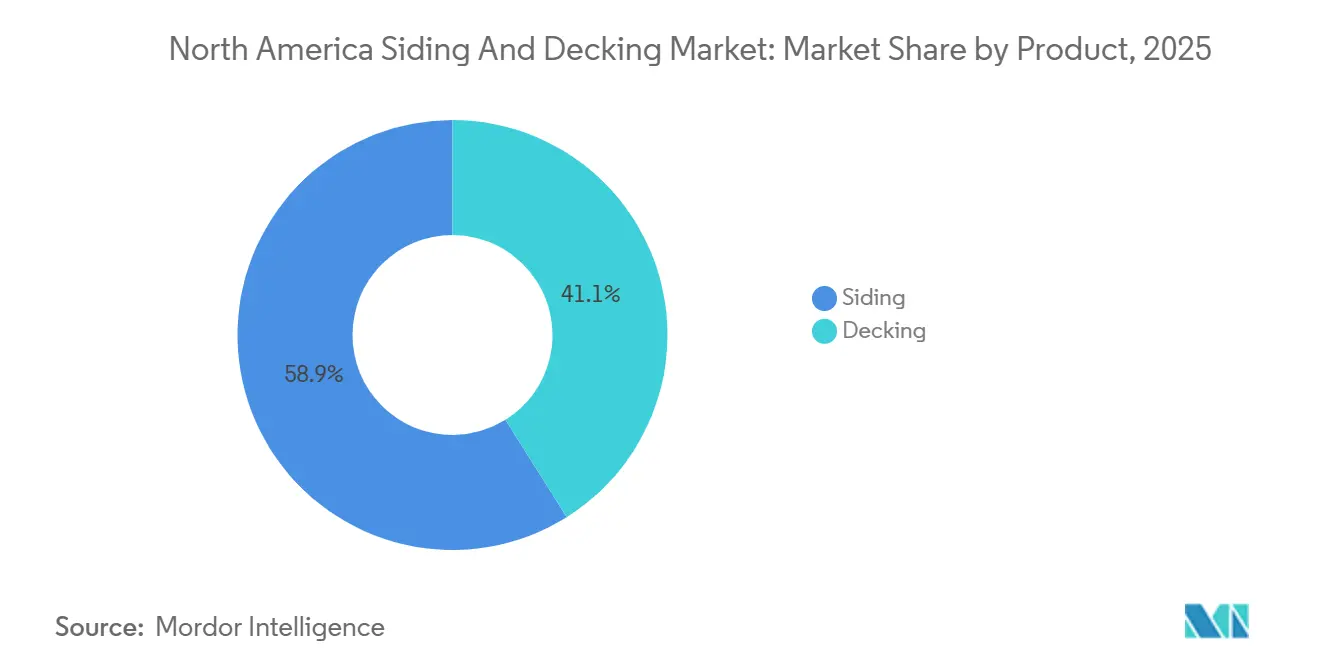

- By product, siding accounted for 58.91% of 2025 revenue, while decking is the fastest growing with a 3.98% CAGR through 2031.

- By material, vinyl held the largest 2025 share at 43.63%, and composite/WPC/PVC posted the highest forecast growth at a 4.56% CAGR.

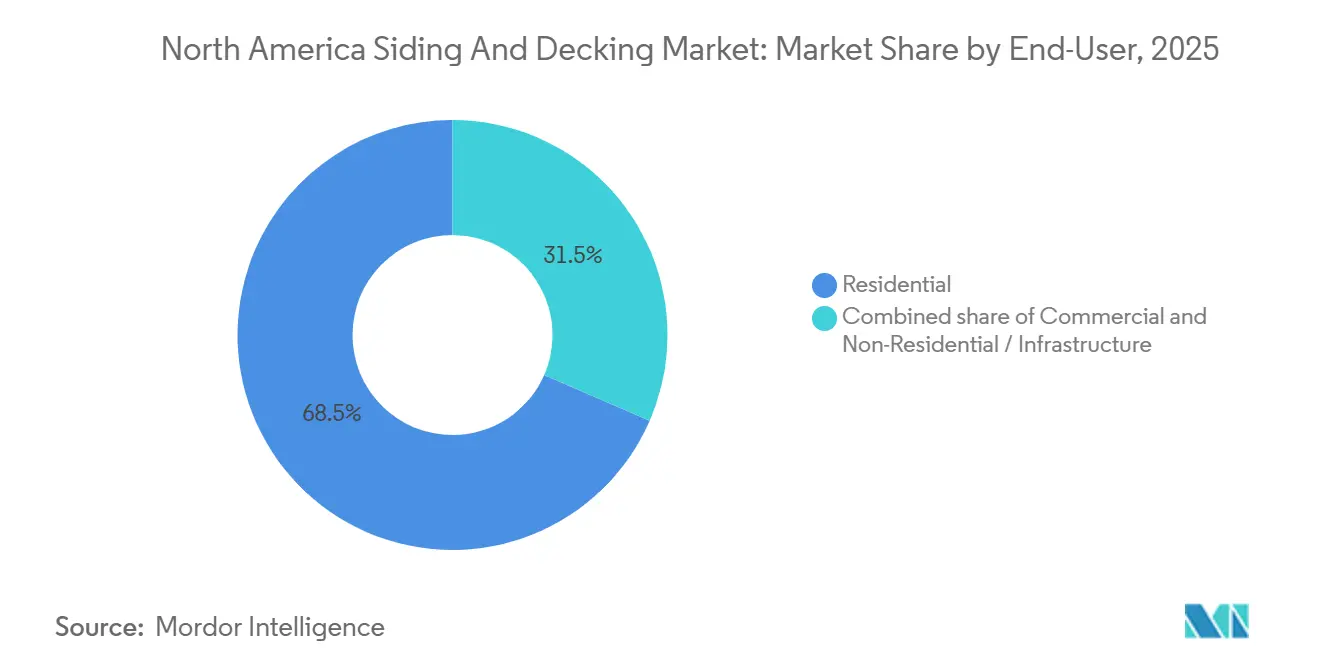

- By end-user, residential captured 68.47% in 2025, while commercial is set to expand the fastest at a 4.16% CAGR.

- By installation method, on-site stick-built represented 75.36% of 2025 installs, and prefabricated/modular panels and deck modules are growing the quickest at a 4.72% CAGR.

- By geography, the United States accounted for 81.61% of 2025 regional sales, and Mexico is the fastest-growing country at a 4.93% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Siding And Decking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Architectural shift toward large openings and indoor-outdoor living designs | +0.7% | Strongest in Sunbelt states (TX, FL, AZ), Pacific Northwest | Medium term (2-4 years) |

| Rising preference for low-maintenance composite & vinyl materials | +0.9% | North America core, spill-over to Mexico | Long term (≥ 4 years) |

| Energy-efficiency codes boosting insulated siding demand | +0.5% | United States (IECC 2024 adopters: Nevada, Rhode Island), California (2025 Code effective 2026) | Medium term (2-4 years) |

| Outdoor-living culture driving deck installations post-pandemic | +0.8% | National, with early gains in the western United States, distributor/dealer conversions | Short term (≤ 2 years) |

| Wildfire-zone building codes are accelerating ignition-resistant cladding | +0.4% | California, Oregon, Pacific & Mountain regions, TX WUI areas | Short term (≤ 2 years) |

| Prefab light-steel framing fueling panelized siding/deck modules | +0.6% | North America (United States ICC-ES certified projects, Mexico nearshoring) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Architectural Shift Toward Large Openings and Indoor–Outdoor Living Designs

Large glass openings, expansive patio doors, and seamless transitions to decks are influencing exterior choices, color palettes, and accessory systems in the North America siding and decking market. Trex reported resilient consumer demand through 2025, with double-digit railing momentum that complements larger deck footprints and higher-value outdoor layouts[2]Trex Company, Inc., “Trex Company Reports Third Quarter 2025 Results,” Trex, trexcompanyinc.gcs-web.com. James Hardie’s Iron Gray 2026 Color of the Year aligns with modern elevations that frame wide openings and exterior focal points with deeper, neutral hues. Commercial and multifamily projects are also prioritizing outdoor amenity spaces and standardized deck modules to accelerate occupancy, a pattern that supports factory-finished cladding and engineered railing packages. Turnkey prefab cabin shells that assemble within days illustrate how an indoor–outdoor design brief pairs with off-site production for predictable timelines in short-term rental and resort applications.

Rising Preference for Low-Maintenance Composite & Vinyl Materials

Material conversion continues to steer share gains as homeowners and builders choose durability, long warranties, and low maintenance, a shift that supports long-run growth in the North America siding and decking market. Trex manufactures high recycled-content decking and expanded in 2025 with an Arkansas plastic processing facility to secure cost-effective recycled inputs and support capacity in Virginia and Nevada. Vinyl’s 26% share of principal exterior wall materials in 2024 underscores the appeal of cost, minimal upkeep, and robust North American supply chains. Fiber cement’s 2024 share at 23% reflects rising preference for ignition-resistant cladding that maintains aesthetics without the rot or insect risks of wood[3]National Association of Home Builders, “Stucco No Longer Most-Used Exterior Wall Material,” NAHB, nahb.org. Noncombustible or ignition-resistant options receive added support from FEMA best practices for wildfire-prone zones, strengthening conversion tailwinds in the West.

Energy-Efficiency Codes Boosting Insulated Siding Demand

IECC 2024 tightened performance thresholds and is in force in select United States jurisdictions, which encourages continuous insulation and higher R-values in exterior wall assemblies when re-siding or building new. California’s 2025 Building Energy Efficiency Standards take effect for permit applications on or after January 1, 2026, adding momentum to envelope upgrades that pair insulated cladding with efficient HVAC and electric-ready provisions. Insulated vinyl siding can be counted in prescriptive compliance pathways when labeled for R-value, which integrates well with siding replacement scopes that expose wall sheathing. The Energy Efficient Home Improvement Credit provides a 30% credit for eligible insulation and air-sealing improvements through 2025, supporting homeowner payback in retrofit markets where immediate comprehensive re-siding is not feasible. DOE guidance reinforces that the most practical time to add continuous insulation is during re-siding, when installers have direct access to the wall assembly and can deliver comfort and noise-reduction benefits with incremental cost.

Outdoor-Living Culture Driving Deck Installations Post-Pandemic

Decking demand continues to be supported by outdoor living, with railing and accessory sales demonstrating resilience even during periods of slower new-home starts. Trex guided to USD 1.15 billion to USD 1.16 billion in 2025 net sales and noted performance in western United States markets tied to distributor and dealer conversions, which boost the North America siding and decking market in remodeling-heavy channels. Standardized prefab deck shells with rapid assembly timelines are gaining traction in hospitality and short-term rental settings, where fixed-price offerings reduce schedule risk. Attractive warranties, low maintenance, and design flexibility reinforce composite and PVC adoption for long-term use scenarios. As distribution consolidates and specification tools improve, homeowners encounter clear upgrade paths to composite decking and color-coordinated railing systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (lumber, resins, metals) | -0.5% | Global, acute pressure in North America lumber markets post-Section 232 tariffs. | Short term (≤ 2 years) |

| Skilled-labor shortage is inflating installation costs | -0.4% | National, the highest wage inflation in framing/drywall (15-18%) and millwork (15-25%) | Medium term (2-4 years) |

| High up-front cost of composites vs. traditional wood | -0.2% | National dampens first-cost-sensitive R&R segments | Medium term (2-4 years) |

| End-of-life recycling gap for multi-material composites | -0.1% | North America, Europe; circular infrastructure development is nascent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Lumber, Resins, Metals)

Commodity swings are pressuring margins and forcing shorter price locks, complicating bids and forecasts across distributors and contractors. Tariff and duty regimes continue to influence delivered lumber costs, with producers highlighting shipment adjustments and demand moderation in the second half of 2025. Resin inputs for vinyl and composite have eased at points, yet many suppliers limit price holds to 30 days or less for insulation and related materials, reflecting ongoing uncertainty. Freight costs rose through mid-2025, adding to project totals in a market where sticker prices tend to be locked months ahead for homeowners. Vertically integrated recyclers and manufacturers mitigate spot volatility by sourcing in-house or through dedicated networks, which supports more stable pricing for premium decking lines.

Skilled-Labor Shortage Inflating Installation Costs

Wage inflation in framing and drywall, and premiums for millwork installers, are redefining project economics and magnifying the need for labor-saving systems. Panelized and prefinished cladding, along with modular railing and hidden-fastener platforms, reduce the time on site, which is attractive where crews are booked out and overtime drives costs. Manufacturers are ramping up product education and consumer marketing to strengthen pull-through for higher-value systems that tolerate elevated labor rates without suppressing demand. The North America siding and decking market benefits from installation aids and standardized details because these reduce callbacks and improve productivity in tight labor markets. Over the medium term, easier-to-install assemblies are poised to gain share from traditional stick-built workflows that require specialized trades and longer schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Decking’s Margin Architecture Outpaces Siding Volume

Siding captured 58.91% of 2025 revenue, the largest share of the North America siding and decking market for the period, while decking is projected to grow at a 3.98% CAGR through 2031 as outdoor-living preferences reinforce demand for premium railing and accessories. The mix shift into low-maintenance designs supports upselling opportunities in both new construction and remodeling, with homeowners favoring coordinated systems that carry strong warranties and reduce upkeep. The North America siding and decking market continues to see dealers convert to composite-oriented assortments where value propositions are clear on durability and lifecycle cost. In siding, factory-finished options and performance attributes such as ignition resistance are strengthening specification positions across production builders and multifamily owners.

Decking’s growth tilt is evident in company results and product roadmap choices, with railing and fasteners complementing boards to lift average order values. Siding remains the installed-base workhorse, but rising code and insurance scrutiny in wildfire zones is gradually steering selections toward noncombustible and ignition-resistant materials. Producer guidance in 2025 pointed to solid profitability in siding, supported by prefinished lines that deliver mix benefits and faster cycle times for builders. In aggregate, the North America siding and decking market reflects steady siding volume with a premiumization drift in decking that favors branded systems.

By Material: Composite/WPC/PVC’s Circular-Economy Credentials Fuel 4.56% CAGR

Vinyl held a 43.63% share in 2025, reflecting affordability and low maintenance, while composite/WPC/PVC leads growth with a 4.56% CAGR as sustainability and durability drive conversion in the North America siding and decking market. The North America siding and decking market size for composite/WPC/PVC is projected to expand at a 4.56% CAGR through the forecast as manufacturers integrate more recycled content and demonstrate consistent performance in harsh climates. Trex’s 2025 activation of a plastic-processing facility in Arkansas deepens access to cost-efficient recycled feedstock, helping stabilize input costs and support volume growth. AZEK expanded circular capabilities with the acquisition of Northwest Polymers in 2025, signaling an industry-wide push to scale recycling infrastructure in core markets.

Fiber cement continues to gain preference due to fire performance and stability, supported by design flexibility that mimics wood without its maintenance and pest exposure. Vinyl remains embedded in value segments and regions where installed cost and supply availability drive choices for new starts and re-siding. Metal cladding, including aluminum and steel, is finding greater use in fire-prone geographies and commercial applications where noncombustibility and energy performance are prioritized. Across categories, standardized accessories and finish systems are enabling cohesive exterior packages that are easier to install, which supports conversion across price tiers in the North America siding and decking market.

By End-User: Commercial’s 4.16% CAGR Reflects National-Builder Consolidation.

Residential commanded 68.47% of 2025 demand, while commercial end-users are projected to grow the fastest at a 4.16% CAGR as large builders and owner-developers pursue long-term durability and code compliance. The North America siding and decking market is increasingly influenced by multi-year supply and specification agreements that standardize higher-performance envelopes in production neighborhoods and multifamily communities. Fiber cement, insulated metal panels, and advanced PVC decking align with insurance and code requirements in large projects, allowing owners to manage lifecycle cost while improving resilience.

Commercial and institutional projects are also advancing higher energy performance and embodied carbon considerations, which encourage the use of high-efficiency panels and factory-finished products. Company guidance in 2025 anticipated margin expansion from product mix in siding while positioning for recovery in select construction segments. The North America siding and decking industry is also converging around turnkey exterior packages that accelerate schedules and reduce weather risk for commercial timelines. As specification consolidates around code-compliant assemblies, commercial demand is positioned to sustain faster growth through the forecast.

By Installation Method: Prefabricated Modules Capture Labor-Inflation Alpha

On-site stick-built methods accounted for 75.36% of 2025 installations, while prefabricated and modular panels and deck modules are projected to expand at a 4.72% CAGR, the fastest rate among installation categories in the North America siding and decking market. The North America siding and decking market size for prefabricated and modular systems is projected to expand at a 4.72% CAGR as schedule control, weather resilience, and labor savings become decisive benefits for developers and homeowners. Rapid-assembly exterior shells and deck modules allow consistent factory quality and predictable setup windows of days rather than weeks. Code-ready, panelized cladding is also aligning with evolving energy standards that reward continuous insulation and controlled interfaces.

Public-sector initiatives in Canada highlight a growing role for prefabrication to scale housing output, with qualification programs supporting standardized, factory-built solutions. Manufacturers of cladding systems continue to emphasize easier installation and panelized alternatives that shorten time on site and reduce reliance on scarce specialized trades. The trend complements ongoing wage pressures in framing and drywall, making factory fabrication an effective hedge against project delays. With performance, speed, and labor advantages, prefabricated systems are positioned to take incremental share across both repair and remodel and new construction in the North America siding and decking market.

Geography Analysis

The United States held 81.61% of regional sales in 2025, while Mexico recorded the fastest growth at a 4.93% CAGR, indicating divergent baselines and distinct demand catalysts across the North America siding and decking market. In the United States, wildfire resilience and stricter energy codes are influencing exterior material choices and installation approaches in both new builds and re-siding projects[4]Federal Emergency Management Agency, “Builder’s Guide to Construction in Wildfire Zones, FEMA P-737,” FEMA, fema.gov. Insurers increasingly prioritize hardened assemblies and noncombustible materials in high-risk regions, which supports ignition-resistant cladding selections. Builder partnerships and product standardization are also advancing, reinforcing specification consistency across national communities. Ongoing investments in capacity and manufacturing automation for insulated panels reflect intensifying commercial demand for energy-efficient, code-compliant envelopes.

In Canada, provincial and local stakeholders are encouraging prefabrication and panelization to add housing supply at speed, which aligns with envelope systems that integrate insulation and cladding in the factory. Manufacturers emphasize material choices that perform in cold climates, including composite decking designed for freeze-thaw durability and better traction in wet and snowy conditions. Aluminum and steel profiles are also relevant in Canadian exterior packages due to fire performance and low maintenance, and suppliers are broadening finishes for residential design flexibility. The North America siding and decking market benefits from Canadian demand for standardized, code-ready facade systems that reduce labor needs and deliver predictable schedules.

Mexico’s 4.93% CAGR reflects nearshoring-related construction, expanding housing demand, and growing use of modular and prefabricated assemblies that simplify onsite labor. High-efficiency insulated concrete panels that combine structure and insulation are gaining use in exterior walls to improve resilience and speed. Prefabricated facade specialists provide factory-finished elements with thermal and acoustic layers to shorten installation and reduce waste at the job site. Industrial constructors in the Bajío region highlight hybrid solutions that balance fire performance, assembly speed, and sustainability outcomes for build-to-suit projects. Specialty mortars, coatings, and adhesives designed to reduce fire propagation are also part of the toolkit in residential and commercial buildings. With greater emphasis on speed-to-market and resilience, Mexico is positioned to remain the region’s fastest-growing segment of the North America siding and decking market.

Competitive Landscape

The North America siding and decking market features diversified competitors across materials, with leaders strengthening positions through capacity additions, sustainability platforms, and portfolio integration. A pivotal 2025 transaction combined siding, decking, trim, railing, and pergola assets under one parent, enhancing go-to-market and specification breadth. Composite decking manufacturers invested in recycling and processing infrastructure to improve input availability and costs while supporting brand sustainability messages in consumer channels. Premium insulated panel producers expanded North American manufacturing footprints to meet commercial energy-performance demands.

Strategic moves in 2024 and 2025 bolstered metal building and components coverage, reinforced distribution, and diversified exposure to residential and commercial end-markets. Siding producers highlighted the mix and margin benefits of prefinished lines and noted steady share gains in new construction and recovering accessory categories. Composite decking leaders reported resilient sell-through and double-digit railing growth, pointing to outdoor projects as a durable category even during periods of higher mortgage rates. Builders and insurers are signaling a long-term tilt toward ignition-resistant exteriors, which favors fiber cement, metals, and advanced PVC profiles in risk-prone regions.

Competitive differentiation increasingly centers on compliance evidence, installer-friendly systems, and digital tools that guide selections across colors, profiles, and accessories. With code changes and insurer criteria tightening, documentation for fire performance and energy outcomes has become a decisive factor in specifications. Capacity expansions and regional manufacturing are helping reduce lead times and logistics costs, supporting consistent service levels for large builders and commercial contractors. As sustainability targets proliferate across the value chain, circular-content claims and third-party validations are reinforcing brand positions in the North America siding and decking market.

North America Siding And Decking Industry Leaders

Trex Company, Inc.

The AZEK Company (TimberTech)

James Hardie Industries plc

Cornerstone Building Brands

Westlake Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: James Hardie announced Iron Gray as its 2026 Color of the Year within the Statement Collection, highlighting ongoing demand for deep, neutral exterior palettes.

- September 2025: Cornerstone Building Brands acquired Metal Sales Manufacturing Corporation, expanding its presence in metal building systems and components across North America.

- July 2025: Kingspan Insulated Panels North America opened a new USD 50 million, 135,000 sq ft facility in Mattoon, Illinois, designed to LEED Gold standards and powered by a 1MW solar array.

- July 2025: James Hardie completed the acquisition of The AZEK Company, integrating siding, decking, trim, railing, and pergola offerings under a combined exterior solutions platform.

North America Siding And Decking Market Report Scope

Siding and decking products are essential exterior building components used to protect structures, enhance durability, and improve the visual appeal of residential, commercial, and infrastructure buildings across North America. The North America siding and decking market is segmented by product, material, end-user, installation method, and country. By product, the market is segmented into siding and decking. By material, the market is segmented into vinyl, fiber cement, wood (treated wood, cedar, and redwood), composite/WPC/PVC, and metal (aluminum and steel). By end-user, the market is segmented into residential, commercial, and non-residential/infrastructure. By installation method, the market is segmented into on-site stick-built and prefabricated/modular panels and deck modules. By country, the market is segmented into the United States, Canada, and Mexico. The report offers the market size in value terms in USD for all the above-mentioned segments.

| Siding |

| Decking |

| Vinyl |

| Fiber Cement |

| Wood (Treated, Cedar, Redwood) |

| Composite / WPC / PVC |

| Metal / Aluminum / Steel |

| Residential |

| Commercial |

| Non-Residential / Infrastructure |

| On-Site Stick-Built |

| Prefabricated / Modular Panels & Deck Modules |

| United States |

| Canada |

| Mexico |

| By Product | Siding |

| Decking | |

| By Material | Vinyl |

| Fiber Cement | |

| Wood (Treated, Cedar, Redwood) | |

| Composite / WPC / PVC | |

| Metal / Aluminum / Steel | |

| By End-User | Residential |

| Commercial | |

| Non-Residential / Infrastructure | |

| By Installation Method | On-Site Stick-Built |

| Prefabricated / Modular Panels & Deck Modules | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size and growth outlook of the North America siding and decking market?

The North America siding and decking market size is USD 19.61 billion in 2026 and is projected to reach USD 23.33 billion by 2031 at a 3.53% CAGR.

Which product segment is growing the fastest in this market?

Decking is the fastest-growing product with a 3.98% CAGR through 2031, while siding remains the largest by revenue.

What materials are gaining share in North America’s siding and decking market?

Composite/WPC/PVC is leading growth at a 4.56% CAGR, while vinyl holds the largest 2025 share and fiber cement advances on ignition-resistant performance.

Which installation methods are gaining traction and why?

Prefabricated and modular panels and deck modules are the fastest-growing installation methods at a 4.72% CAGR due to labor savings, faster assembly, and factory quality.

Page last updated on: