Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

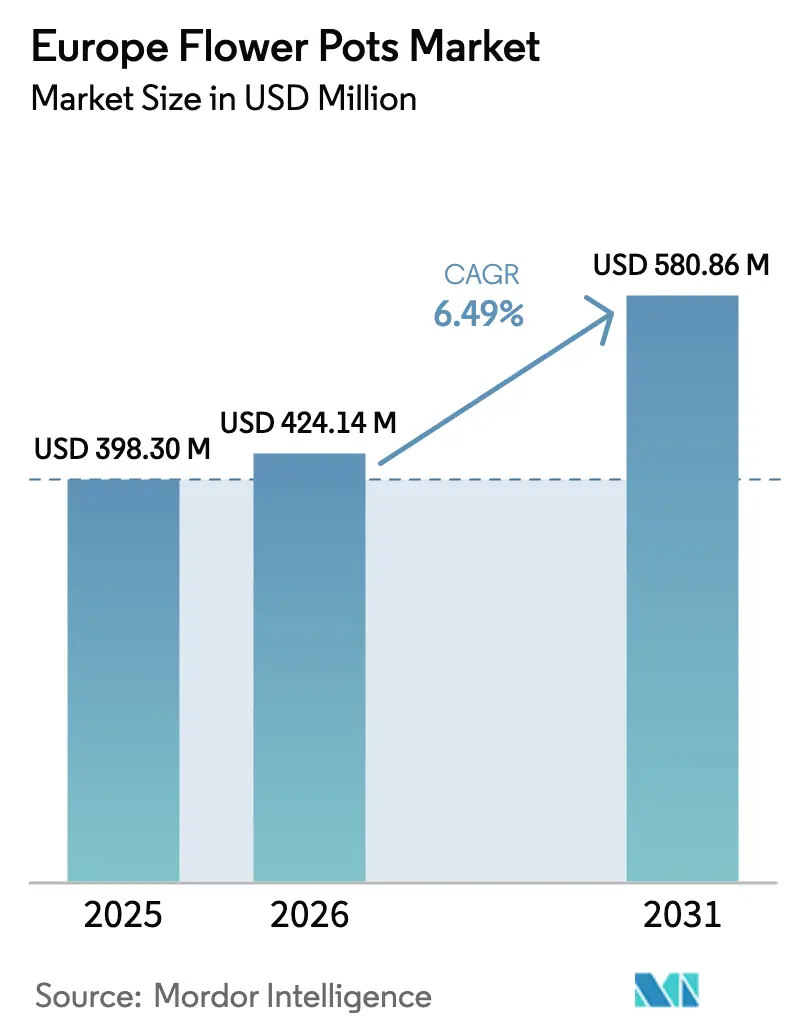

| Base Year Market Size (2025) | USD 398.30 Million |

| Market Size (2026) | USD 424.14 Million |

| Market Size (2031) | USD 580.86 Million |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Flower Pots Market Analysis by Mordor Intelligence

The Europe flower pots market size is projected to be USD 398.30 million in 2025, USD 424.14 million in 2026, and reach USD 580.86 million by 2031, growing at a CAGR of 6.49% from 2026 to 2031. The European flower pots market is shifting away from carbon-intensive ceramics toward circular, compliant plastics and bio-based designs as the European Union Packaging and Packaging Waste Regulation requires high recyclability and broader recycled content adoption by 2030. The United Kingdom’s March 31, 2026, curbside acceptance of non-black PP and PET plant pots removes a key end-of-life barrier and supports consumer confidence in recyclable options at the point of sale. EPR fee modulation in France is reinforcing this pivot, rewarding mono material, detachable label packaging, while penalizing carbon black pigments across horticulture formats. Persistently higher energy and carbon prices reduce ceramics’ cost competitiveness, which strengthens the business case for lightweight, NIR detectable PP and PET solutions under e-commerce and municipal procurement requirements [1]Cerame Unie, “EU ETS Impact on the Ceramic Industry,” European Ceramic Industry Association, cerameunie.eu. Competitive intensity is increasing as agile converters scale PCR sourcing and design innovations, illustrated by Elho’s product-level CO2e transparency and Keter’s Netherlands recycling hub that secures feedstock for recycled content pots.

Key Report Takeaways

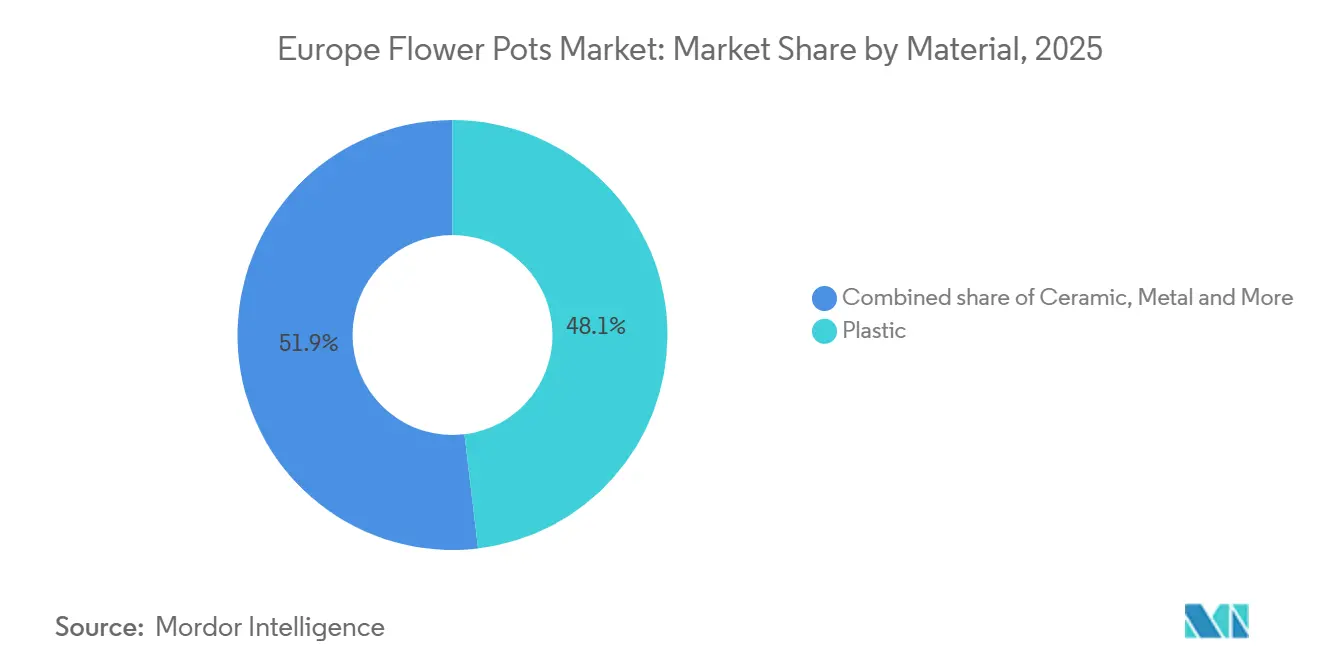

- By material, plastic led with 48.10% of the Europe flower pots market share in 2025, while biodegradable pots are projected to expand at a 7.27% CAGR through 2031.

- By usage location, outdoor applications held 63.05% of the Europe flower pots market share in 2025, whereas indoor pots are projected to grow at a 6.86% CAGR through 2031.

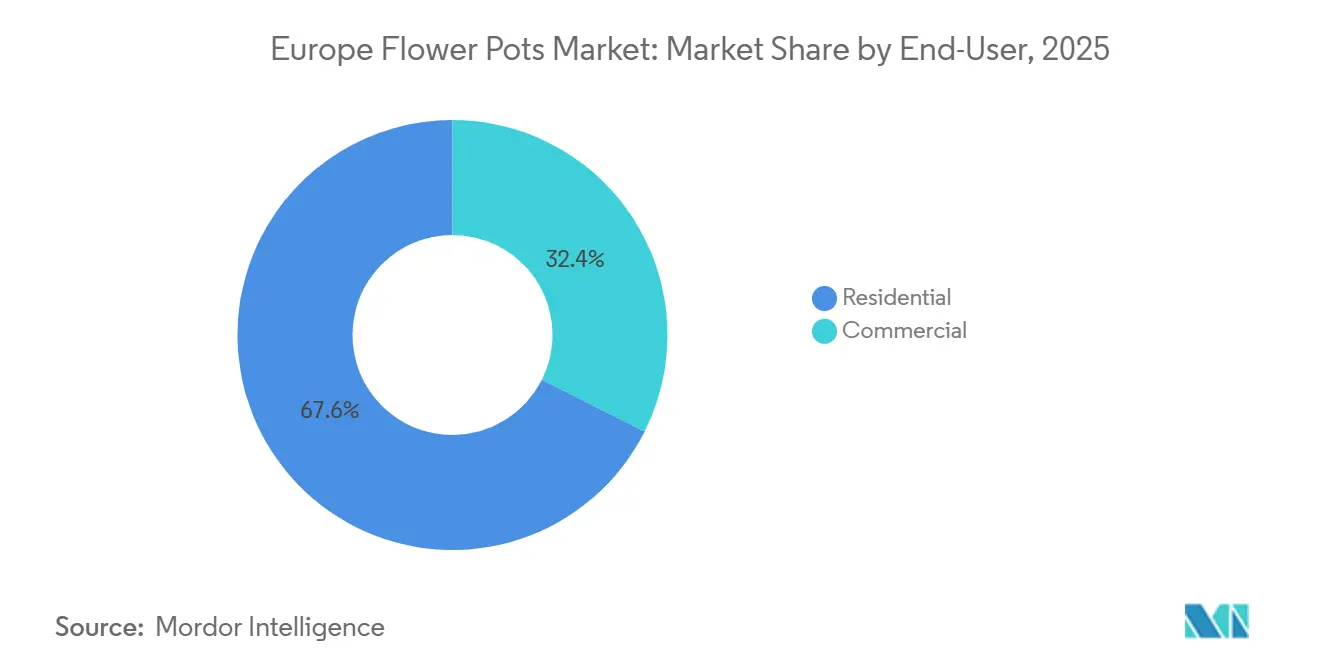

- By end user, residential buyers accounted for 67.60% of the Europe flower pots market share in 2025, while commercial customers are projected to expand at a 6.37% CAGR through 2031.

- By distribution channel, garden centers and DIY stores commanded 45.70% of the Europe flower pots market share in 2025, while online pure plays and marketplaces are projected to grow at a 7.62% CAGR through 2031.

- By geography, Germany led with 21.05% of the Europe flower pots market share in 2025, while Poland is projected to expand at a 7.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Flower Pots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PPWR recyclability and recycled‑content mandates push shift to mono-material and recycled‑plastic pots | +1.8% | Global, with early gains in France, Germany, the Netherlands, and Belgium | Medium term (2-4 years) |

| Urban greening targets in Europe increase municipal and commercial planter demand | +1.3% | European Union-wide, strongest in Germany, Poland, Nordic cities, and emerging Benelux markets | Long term (≥ 4 years) |

| Online DIY/home and garden expansion favors lightweight, shippable, self-watering planters | +1.1% | Germany, the United Kingdom, France, Netherlands; mature e-commerce infrastructure markets | Short term (≤ 2 years) |

| In the United Kingdom, in 2026, curbside acceptance of non‑black PP/PET pots accelerates NIR‑detectable designs | +0.9% | The United Kingdom primarily, with spillover to Ireland and Nordic adopters | Medium term (2-4 years) |

| EPR fee modulation by recyclability favors detachable labels and mono-material PP/PET pots | +0.7% | France, the United Kingdom, Germany, and expanding to Italy and Spain | Medium term (2-4 years) |

| Energy-intensive ceramics costs tilt the mix toward plastic and bio-based pots | +0.7% | Italy, Spain, Southern Europe ceramic hubs; impact spreads European Union-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PPWR Recyclability and Recycled Content Mandates Push Shift to Mono Material and Recycled Plastic Pots

The European Union Packaging and Packaging Waste Regulation requires that packaging placed on the market in 2026 be on a path to at least 70% recyclability by 2030, with recycling at scale targeted for the following decade, which redirects horticultural pots toward mono-material PP or PET formats and away from hard-to-sort composites[2]European Commission, “Packaging and Packaging Waste Regulation (PPWR),” EUR Lex, eur-lex.europa.eu . Carbon black pigments are being phased out because they disrupt NIR sorting, which accelerates the move to taupe and gray NIR detectable colors across the Europe flower pots market. The regulation also scales recycled content obligations, which raises the importance of reliable post-consumer feedstock and favors converters that can lock in PCR supply at consistent quality. EPR bonus and malus schemes, such as France’s fee modulation, give measurable cost advantages to lightweight, reusable, and clearly sortable pots while penalizing designs that hinder material recovery. Early adopters are commercializing compliant concepts, including Elho’s Winery Collection that partners with Adivalor and Healix to convert viticulture rope waste into 100% recycled and fully recyclable planters. United Kingdom recyclability frameworks and labeling guidance reinforce this transition by aligning sorting standards and consumer communication with NIR-compatible pigments and mono-material construction.

Urban Greening Targets in Europe Increase Municipal and Commercial Planter Demand

The European Union Nature Restoration Law sets a binding objective to restore 20% of European Union land and sea by 2030 and requires no net loss of urban green space and tree canopy over the same period, which strengthens demand for durable, modular planters across public spaces and commercial sites. All cities above 20,000 inhabitants are required to develop Urban Nature Plans, yet a small share of municipalities have deep experience with public-private partnerships for green infrastructure, which creates service opportunities for suppliers that bundle pots with installation and maintenance. Vilnius, the 2025 European Green Capital, planted 94,000 trees and one million bushes, underscoring the scale and cadence that urban greening programs can reach when supported by coordinated funding. Wrocław’s Nowy Targ Square transformation installed 170 trees with automatic irrigation in modular planters, offering a repeatable proof point for depaving constrained urban cores. Policy and funding recommendations at the European Union level continue to elevate nature-based solutions, which sustain procurement for large-format, self-watering designs that reduce maintenance and water use in high-traffic settings[3]Greening Cities Partnership, “Action Plan for Urban Greening,” EU Urban Agenda, greeningcitiespartnership.eu . This pull is also visible in premium commercial offerings such as LECHUZA’s modular planters with integrated irrigation and removable liners, which target facility managers who prioritize durability, circular inputs, and lower lifecycle costs.

Online DIY and Home Improvement Expansion Favors Lightweight, Shippable, Self-Watering Planters

DIY e-commerce penetration increased in 2024 and is projected to expand further by 2026 across the region’s largest markets, which helps brands that design lightweight, damage-resistant planters suited to parcel networks and cross-border fulfillment. Germany’s DIY and flowers segment outpaced overall online retail growth in 2025, signaling resilient demand for home and garden assortment despite macro headwinds. The PPWR rule capping space in transport packaging strengthens the economics of PP and PET formats that minimize dimensional weight and packing materials, especially for self-watering designs shipped directly from warehouses and third-party sellers. Marketplace concentration also shapes merchandising, with global platforms holding a sizable share of Europe’s DIY traffic and competing on price, convenience, and selection across planters and accessories [4]Cross Border Commerce Europe, “Top 50 DIY, Home & Garden Retail Europe,” CBCommerce.eu, cbcommerce.eu . Product innovation is adapting to online journeys, as shown by start-ups scaling flat pack self-watering planters and established brands adding IoT moisture monitoring to reduce care complexity for first-time indoor plant owners. These shifts raise the relative growth potential for circular compliant plastics within the European flower pots market as retailers favor SKUs that ship well, reduce returns, and meet recyclability guidelines.

United Kingdom 2026 Curbside Acceptance of Non Black PP and PET Pots Accelerates NIR Detectable Designs

England’s adoption of curbside acceptance for all non-black, recyclable PP and PET plant pots took effect March 31, 2026, which resolves a long-standing end-of-life barrier that limited consumer confidence at the point of purchase. The change complements the 2025 channel mix, where garden centers and DIY stores account for 45.70% of sales, by giving retailers a clear sustainability claim that aligns with local recycling systems. Because NIR sorters cannot see carbon black plastics, manufacturers are reformulating toward taupe and gray pigments that pass detection without compromising texture and finish. Design responses already include elho collections that use NIR-compliant recycled inputs, as well as LECHUZA planters offered in earth-tone palettes and modular forms that fit both indoor and outdoor placements. The policy reduces ambiguity for end users and simplifies messaging for retailers, which can accelerate the transition to mono-material, label-ready PP and PET across the European flower pots market. This shift reinforces the faster growth of bio-based and recycled content plastics as municipalities, retailers, and brands align around clear, system-ready designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polymer price/import volatility pressures plastic pot margins | -0.6% | European Union-wide, producers especially lack vertical integration or PCR contracts. | Short term (≤ 2 years) |

| Consumer spending headwinds slow premium upgrades and renovations | -0.5% | Germany, the United Kingdom, and France are mature markets with higher debt and inflation sensitivity. | Medium term (2-4 years) |

| NIR‑detectable color standards constrain dark aesthetics and branding | -0.3% | United Kingdom, Netherlands, Germany, with an advanced NIR sorting infrastructure | Medium term (2-4 years) |

| Decarbonization and energy costs constrain terracotta capacity and raise prices | -0.4% | Italy, Spain, Portugal, ceramic hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Polymer Price and Import Volatility Pressures Plastic Pot Margins

European polymer supply remains uneven, and import competition has reshaped operating rates since 2025, which reduces pricing power for converters as virgin resin benchmarks track global cycles more closely. Structural rationalization has been visible, including announced shutdowns and closures at large petrochemical complexes in the Netherlands and France, which signals supply rebalancing without guaranteeing margin relief for mid-downstream processors. Recycled polymers have not escaped these dynamics since weak virgin prices can compress PCR premiums and complicate the business case for collection and reprocessing capacity growth. At the same time, PPWR requirements on recycled content are tightening, which forces converters to secure consistent PCR quality and volumes under long-term contracts. Companies with vertical integration into recycling and regranulation, or with captive hubs near production plants, mitigate feedstock risk and blunt short-term volatility in the European flower pots market. The margin squeeze is sharper for smaller converters that rely on spot markets, which raises incentives to collaborate with retailers and municipalities to build closed-loop collection programs that stabilize inputs.

Decarbonization and Energy Costs Constrain Terracotta Capacity and Raise Prices

Industrial gas prices in Europe remain well above pre-crisis baselines in 2026, and this cost pressure filters directly into kiln-based manufacturing, where firing cycles are energy-intensive. European Union ETS costs add another structural burden for ceramics, with current carbon prices and forward expectations pointing to higher compliance outlays through 2030 that weigh on capital plans and unit economics. Italian ceramic investment declines in 2024 confirmed this trend as producers deferred kiln upgrades, which suggests a tighter terracotta supply over the forecast period, even as consumer demand for natural finishes persists in premium niches. The macro environment has already claimed high-profile casualties, illustrated by Royal Stafford’s liquidation following steep energy cost inflation, which highlights demand risk for energy-intensive formats in price-sensitive channels. Leading manufacturers are responding by modernizing assets and optimizing energy use, including initiatives under new leadership at global terracotta players to pursue efficiency and diversification, even as such moves lift capital intensity in the near term. Emerging hydrogen kiln pilots and efficiency retrofits remain strategically relevant but are unlikely to offset sustained energy and carbon costs in the short run, which keeps relative growth stronger for circular compliant plastics in the European flower pots market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Circular mandates fracture the traditional mix.

Plastic commanded 48.10% share of the European flower pots market size in 2025, while biodegradable pots are projected to lead growth with a 7.27% CAGR through 2031, as public realm installations favor decomposable formats where collection is difficult. PPWR elevates recyclability thresholds and recycled content targets, which concentrates demand in mono-material PP and PET that pass NIR sorting and qualify for EPR bonuses rather than maluses. NIR detection constraints are pushing brands to taupe and gray pigment systems to ensure accurate sorting and reprocessing at scale, which reinforces the appeal of standardized, label-ready designs. EPR fee modulation in France is already changing formulation choices and labelling strategies, and it is influencing retailer assortments that now emphasize sortable, recycled content SKUs. Leading converters are also investing in transparency, with ELHO publishing product-level CO2e via its Eco Passport, which supports procurement decisions that reward proven footprint reductions over time.

Energy and carbon costs weigh on terracotta and glazed ceramics since kiln firing magnifies fuel price and ETS exposure across every production run. Deferred investments in 2024 at major ceramic districts signal capacity tightening through the second half of the decade, which may sustain pricing in the premium terracotta niche while shifting mass market volumes toward recycled content plastics. The Europe flower pots industry is also consolidating recycled inputs, supported by integrated hubs that process household plastic into PCR suitable for horticultural pots at consistent quality. Brands that align pigments, detachable labels, and mono material construction to EPR rules secure a measurable cost advantage at scale, especially in France and the United Kingdom, where fee structures and curbside standards are clear. In this setting, biodegradable pots hold a distinct role in municipal greening and landscaping contracts where field composting and soil integration are preferred over collection, which complements rather than replaces the momentum in recycled content PP and PET.

By Usage Location: Indoor adoption rises with urban greening and biophilic design

Outdoor applications accounted for 63.05% of volume in 2025, while indoor pots are expanding at a 6.86% CAGR through 2031 as urban housing density and workplace biophilia increase demand for space-efficient, self-watering designs. The European Union Nature Restoration Law’s no net loss requirement for urban green space encourages balcony gardening, courtyard retrofits, and indoor planting programs in offices and public buildings, which channels steady replacement and upgrade cycles for planters that integrate irrigation and recycled inputs. The Europe flower pots market also benefits from e-commerce assortments that simplify indoor plant care, favoring modular pots and planters that fit shelves and window ledges and ship reliably in parcel networks.

Outdoor placements still demand frost resistance and UV stability, which pushes plastics toward improved stabilizers, while ceramics position on natural aesthetics and breathability in higher price tiers. Compliance-ready labeling and detachable tags are now standard in many indoor and outdoor SKUs, which helps consumers sort and recycle correctly under municipal systems. Indoor adoption strengthens as brands build features that reduce care complexity for first-time plant owners and facility managers, including integrated irrigation and removable liners that cut watering labor and improve plant health.

Product development now reflects these use cases, from LECHUZA’s solid wood planters with recycled liners for premium interiors to ELHO’s collections made with high PCR content and lifetime durability claims that fit compact, multi-room layouts. The Europe flower pots market is also diversifying indoor textures and finishes that maintain NIR compatibility, which protects recyclability while preserving design choice. Retailers curate indoor assortments with clear messaging on recyclability and PCR percentages to align with corporate sustainability commitments and EPR incentives. As more cities embed greening in building codes and workplace programs, indoor growth remains a structural pillar for value expansion across the forecast period.

By End User: Municipal and commercial demand complements a residential core

Residential buyers represented 67.60% of 2025 demand, while commercial customers are growing at a 6.37% CAGR through 2031 as municipalities, landscapers, and facilities teams scale urban greening programs under policy commitments. The public sector’s procurement gap in structuring PPPs for green infrastructure creates openings for suppliers that bundle planters with installation, irrigation, and maintenance, which helps cities accelerate project delivery. Municipal case studies such as Wrocław’s Nowy Targ Square show the practical uses of modular, self-watering planters to green hardscape plazas with minimal civil works and controlled water use.

Residential upgrades remain the volume anchor, but their material choices are increasingly shaped by recyclability claims and curbside acceptance standards that retailers and brands can now communicate clearly in the United Kingdom and several European Union markets. Commercial buyers continue to specify large-format pots and coordinated ranges for plazas and facades, which favors PCR-rich plastics that lighten installations and hold up under frequent cleaning cycles. Private and public end users are also aligning around proofs of circularity, from on-site take-back initiatives at retailers to published product-level footprints that simplify sustainability reporting for corporate buyers.

The European flower pots market benefits as brands document PCR percentages, renewable energy use, and EPR compliance status on product pages and labels, which reduces perceived risk in multi-site rollouts. In parallel, converters that integrate regranulation or secure long-term PCR contracts can offer price stability to city procurement and facility management, which improves win rates in competitive tenders. Where ceramic aesthetics are prioritized, buyers tend to segment them into premium zones while deploying recycled content plastics for higher traffic or weight-sensitive locations to control cost and installation complexity. This division of labor across end users sustains overall growth while allowing targeted innovation by material and feature set in the European flower pots market.

By Distribution Channel: Online and omnichannel models reshape discovery and fulfillment

Garden centers and DIY stores captured 45.70% of 2025 sales, while online pure plays and marketplaces are rising at a 7.62% CAGR through 2031 as assortments and logistics mature across key European Union markets. The PPWR 50% space rule for transport packaging is shifting economics toward compact, lightweight formats that reduce breakage and dimensional weight, which benefits NIR detectable PP and PET assortments for parcel networks. Cross-border DIY e-commerce continues to expand its share of orders, which enables Eastern and Central European converters to serve wider markets through marketplace storefronts. Retail circularity programs, including in-store take-back schemes, reinforce closed-loop supply and help brands secure consistent PCR inputs while enhancing customer loyalty through clear end-of-life solutions. Discovery now blends editorial content and compliance badges, with retailers highlighting EPR-aligned labels and NIR compliance, so shoppers can choose designs that fit local recycling systems.

The marketplace landscape in Europe remains competitive, with large platforms holding a prominent portion of DIY traffic and investing in selection and shipping speed for bulky and fragile items like planters. Brands respond by expanding D2C channels for curated collections while using omnichannel partners for depth and replenishment in mainstream sizes and colors across garden centers and home improvement chains. Assortment strategies prioritize compliance-ready labels and mono-material designs, which reduce reverse logistics friction by aligning with municipal collection rules. Retailers and brands also collaborate on storytelling around PCR content and durability guarantees to differentiate against entry-level imports, which improves conversion without eroding margin. As channel boundaries blur, the European flower pots market gains from better product discovery, transparent sustainability claims, and reliable returns handling that protect customer satisfaction.

Geography Analysis

Germany led with a 21.05% share in 2025, backed by national DIY chains and a mature online assortment, alongside retailer-led circularity moves such as take-back programs that align with local compliance regimes. Cross-border DIY e-commerce penetration allows German and neighboring brands to reach Austria, Switzerland, and Benelux more easily through marketplace channels and regional networks. The United Kingdom’s nationwide curbside acceptance of non-black PP and PET pots in 2026 clarifies recyclability messaging and is expected to boost compliant SKUs in garden centers and online retail. In France, EPR fee modulation has already reduced the use of carbon black pigments and steered packaging and labeling choices toward sortable, mono-material formats among leading suppliers. Together, these changes support a gradual mix shift across Western Europe toward circular compliant PP and PET, with visible merchandising emphasis in mainstream home improvement banners.

Italy and Spain face cost and compliance pressures on ceramics as energy and ETS expenses remain elevated, which constrains investments and tightens capacity outlooks into the late 2020s. Italian ceramic investment declines in 2024 and revenue softness in Iberia point to structural adjustments, even as demand for natural terracotta aesthetics remains resilient in premium niches. Strategic responses include modernization plans and leadership changes at top terracotta manufacturers to expand internationally and upgrade kiln technologies for a higher cost environment. Poland is forecast to grow at a 7.39% CAGR through 2031, helped by domestic injection molding capacity that reduces import reliance and serves Central European demand through cross-border marketplaces. Poland’s urban greening projects, including Wrocław’s planting of 170 trees with automatic irrigation in modular planters, illustrate how municipal procurement supports commercial planter demand.

The Netherlands and Belgium benefit from local PCR processing at scale, highlighted by integrated recycling capacity that supplies European factories and secures recycled input for PPWR-compliant planters. Nordic markets show strong receptivity to documented sustainability attributes such as product-level CO2e disclosures and recycled content claims, which align with public and private procurement standards. Municipal greening momentum is visible across Northern and Central Europe, with flagship city programs planting thousands of trees and expanding urban forests, which raises the need for durable, modular planters and self-watering systems that reduce maintenance costs. As PPWR and local EPR rules harmonize sorting and labeling over time, compliance-ready designs spread across the Rest of Europe markets, aided by marketplaces that accelerate the diffusion of best-selling SKUs. These geographic patterns support broad-based growth in the European flower pots market with faster expansion in Central and Eastern Europe and stable demand in the larger Western European economies.

Competitive Landscape

The European flower pots market is moderately fragmented, with leading brands scaling PCR inputs, design features, and transparency while regional converters and imports intensify price and assortment competition across channels. Elho introduced 125 new SKUs in 2026, launched biodiversity-supporting products from 100% recycled materials, and expanded product-level CO2e disclosures via its Eco Passport, supported by renewable energy and high PCR shares in core lines. Scheurich invested in hydrogen-compatible kiln capabilities and onsite photovoltaics to hedge decarbonization risk while building brand equity through environmental programs tied to each unit sold. Keter secured an integrated PCR supply by inaugurating a Netherlands recycling hub in 2024, which processes substantial volumes of household plastic and supplies European factories that already run high recycled input ratios. Deroma appointed a new CEO in 2024 to drive international expansion and efficiency upgrades in its terracotta portfolio as energy and ETS costs reshape kiln economics. LECHUZA extended its portfolio with solid wood planters featuring integrated irrigation and removable liners made from post-industrial recycled plastic, targeting commercial and premium residential buyers.

Strategy patterns converge on three themes that matter for growth and resilience in the European flower pots market. First, vertical integration into PCR processing or regranulation reduces feedstock risk and supports consistent product quality across high-volume SKUs. Second, design investments in self-watering features, modular formats, and NIR detectable finishes raise conversion in e-commerce and reduce returns for parcel shipment. Third, compliance-ready labeling and detachable tags unlock EPR bonuses and simplify curbside messaging, which helps retailers and municipalities expand take-back and on-site collection programs. Retailers are also piloting and scaling in-store pot take-back schemes that close the PCR loop locally and strengthen customer loyalty among sustainability-minded shoppers. These moves collectively improve operating leverage and support price realization for differentiated brands while preserving access to cost-sensitive segments through compliant entry-level ranges.

New entrants and regional specialists add competitive heat with e-commerce optimized SKUs and brand stories built around recycled inputs and functional design, including flat pack self-watering concepts that improve pallet density and shipping resilience. Polish and Central European manufacturers strengthen positions with domestic molding and toolmaking that compress lead times and enable private label programs for marketplace and retail partners. Leading incumbents respond with regional distribution deals, channel-specific collections, and more transparent impact reporting, which align with Northern European procurement norms and corporate sustainability reporting needs. Across the forecast period, competitive differentiation rests on verified circularity credentials, compliance-ready design, and reliable fulfillment that keeps pace with the channel mix shift in the European flower pots market. As fee modulation narrows the cost gap between compliant and non-compliant pots, scale in PCR sourcing and in-house color reformulation becomes a key hedge against regulatory and input volatility. This favors brands and converters that can execute quickly on pigment changes, detachable labels, and mono material formats without sacrificing aesthetics or durability.

Europe Flower Pots Industry Leaders

elho

Scheurich

Deroma

LECHUZA

Capi Europe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Elho's 2026 product catalogue introduced 125 new SKUs, including entry into the biodiversity category with "B's by elho" products (bird and insect habitats) made from 100% recycled, 100% recyclable materials using 100% renewable energy, co-designed with European experts and backed by a lifetime guarantee. The company also expanded its Grass Collection, featuring pots made from used artificial grass, suitable for indoor and outdoor use.

- December 2025: Nuova Deroma S.p.A. obtained ISO 45001 certification for its Occupational Health and Safety Management System, reinforcing its commitment to environmental, social, and governance objectives as the world's largest terracotta producer expands into the United Kingdom, Asia Pacific, and Eastern Europe markets.

- May 2025: Potr raised USD 670,000 in funding to scale production of flat-pack self-watering planters made from post-consumer waste, optimizing pallet density for cross-border e-commerce and targeting the EUR 78 billion European online DIY market projected for 2026.

- January 2025: LECHUZA launched the PALO Natural Wood Collection, marking the company's first use of a natural material, certified eucalyptus wood, with planters featuring integrated irrigation systems and removable liners made from 100% post-industrial recycled plastic, targeting commercial facility managers and premium residential buyers.

Europe Flower Pots Market Report Scope

Flower pots are items or containers used for growing or displaying plants like flowers, vegetables, and herbs. The market is filled with nursery planters and pots in a variety of sizes, styles, and designs.

The Europe Flower Pots Market Report is Segmented by Material (Plastic, Ceramic, Terracotta, Metal, Wood & Bamboo, Bio-degradable), Usage Location (Outdoor, Indoor), End-user (Residential, Commercial), Distribution Channel (Garden Centres, Online, D2C), and Geography (Germany, United Kingdom, France, Italy, Spain, Netherlands, Belgium, Nordics, Rest of Europe). Forecasts in Value (USD).

By Material

| Plastic |

| Ceramic |

| Terracotta |

| Metal |

| Wood & Bamboo |

| Bio-degradable (Coir, Paper, PLA, etc.) |

By Usage Location

| Outdoor |

| Indoor |

By End-user

| Residential |

| Commercial |

By Distribution Channel

| Garden Centres & DIY Stores |

| Supermarkets & Mass Merchandisers |

| Online Pure-plays & Marketplaces |

| Direct-to-Consumer Brands |

Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Nordics (Denmark, Sweden, Norway, Finland) |

| Rest of Europe (Poland, Czechia, etc.) |

| By Material | Plastic |

| Ceramic | |

| Terracotta | |

| Metal | |

| Wood & Bamboo | |

| Bio-degradable (Coir, Paper, PLA, etc.) | |

| By Usage Location | Outdoor |

| Indoor | |

| By End-user | Residential |

| Commercial | |

| By Distribution Channel | Garden Centres & DIY Stores |

| Supermarkets & Mass Merchandisers | |

| Online Pure-plays & Marketplaces | |

| Direct-to-Consumer Brands | |

| Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Belgium | |

| Nordics (Denmark, Sweden, Norway, Finland) | |

| Rest of Europe (Poland, Czechia, etc.) |

Key Questions Answered in the Report

What is the Europe flowerpots market size and growth outlook to 2031?

The Europe flower pots market size is projected at USD 424.14 million in 2026 and USD 580.86 million by 2031, reflecting a 6.49% CAGR from 2026 to 2031.

Which materials are leading and which are growing fastest in Europe?

Plastic led with a 48.10% share in 2025, while biodegradable pots are the fastest, projected at a 7.27% CAGR through 2031 as circular procurement expands.

How are European Union regulations shaping product design and materials?

PPWR requires high recyclability and rising recycled‑content thresholds, which favors mono-material PP and PET with NIR‑detectable pigments and detachable labels to qualify for EPR bonuses.

Which channels are gaining share across Europe?

Garden centers and DIY stores held 45.70% of 2025 sales, but online pure‑plays and marketplaces are rising at a 7.62% CAGR on the back of PPWR’s transport rules and better parcel economics for lightweight pots.

Which countries are leading or accelerating in Europe?

Germany led with a 21.05% share in 2025, and Poland is the fastest with a 7.39% CAGR through 2031 as domestic capacity and cross-border e-commerce expand.

What is the impact of the United Kingdom's curbside acceptance of PP and PET pots?

England’s March 31, 2026, curbside acceptance of non‑black PP and PET pots clarifies recycling and is expected to boost NIR‑detectable, mono-material designs at retail and online.

Page last updated on: