Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 44.59 Billion |

| Market Size (2031) | USD 61.19 Billion |

| Growth Rate (2026 - 2031) | 6.53% CAGR |

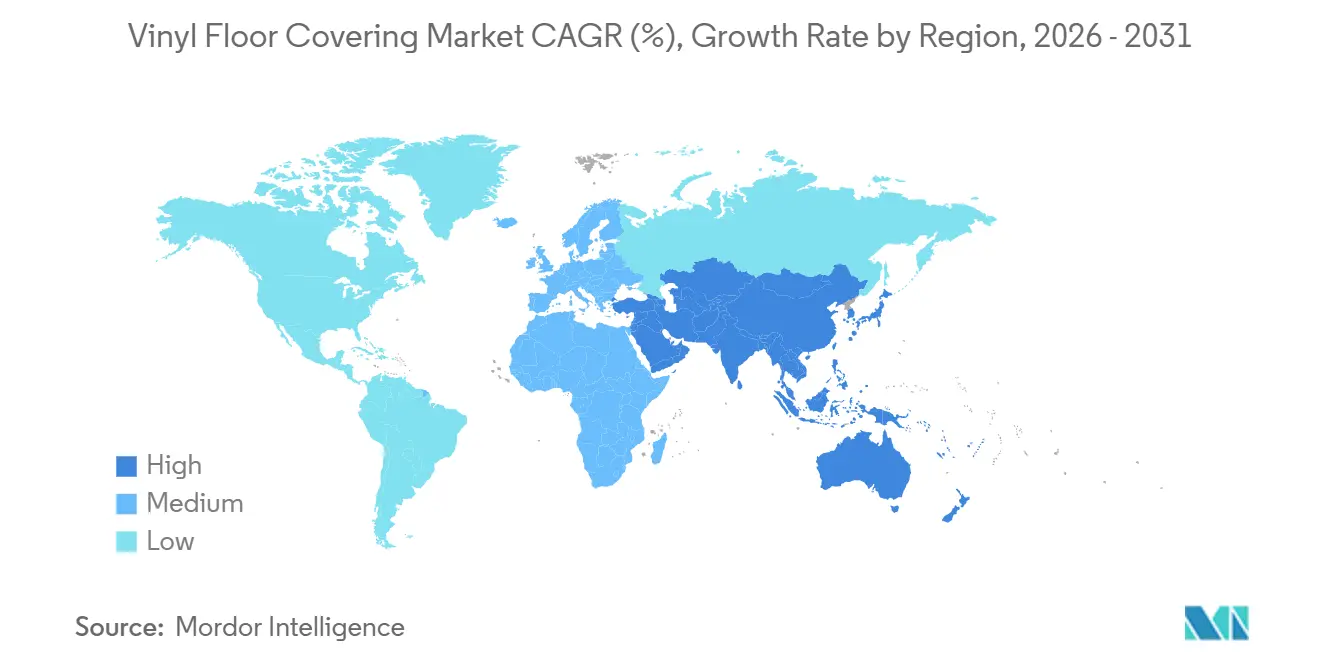

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vinyl Floor Covering Market Analysis by Mordor Intelligence

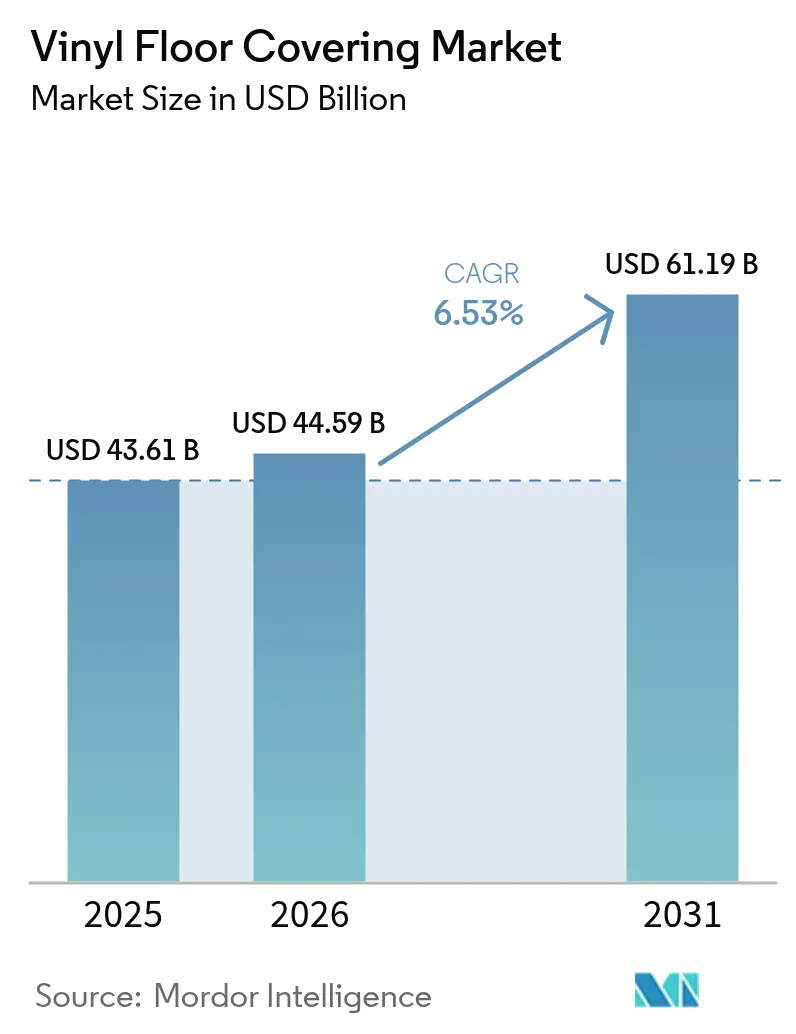

The global vinyl floor covering market size is expected to grow from USD 43.61 billion in 2025 to USD 44.59 billion in 2026 and is forecast to reach USD 61.19 billion by 2031 at 6.53% CAGR over 2026-2031. Growth is underpinned by steady replacement cycles in developed housing markets, faster urban development in the Asia-Pacific, and a decisive shift toward rigid-core formats that solve for waterproofing, design authenticity, and installed-cost performance in both residential and commercial settings. Procurement in healthcare, education, and public buildings is adopting PVC-free and low-VOC specifications, while domestic capacity additions in North America are designed to reduce tariff and logistics risk for time-sensitive projects. At the same time, input cost volatility for PVC resin and plasticizers keeps margin pressure elevated, which is pushing large brands to integrate upstream into compounding and to qualify alternative chemistries where performance permits. Overall, demand signals in 2026 reflect a balanced mix of remodeling-led volume and early-cycle new construction recovery, with rigid-core lines positioned as the anchor of the vinyl floor covering market across mid-price and premium segments.

Key Report Takeaways

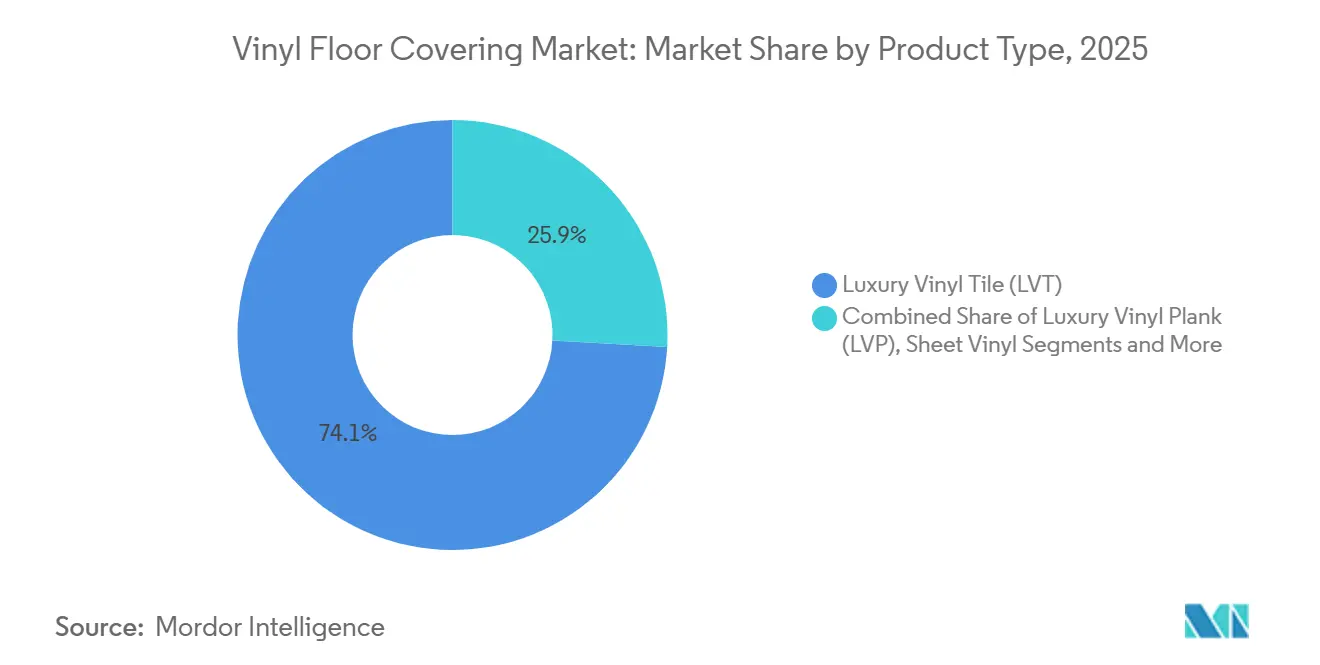

- By product type, luxury vinyl tile led with 74.12% revenue share in 2025; luxury vinyl plank is forecast to expand at a 6.72% CAGR through 2031.

- By installation method, interlocking formats held 56.20% share in 2025; glue-down is projected to grow at a 6.68% CAGR through 2031.

- By end-user, residential applications accounted for 64.90% of the 2025 volume; commercial applications are expected to grow at a 7.31% CAGR through 2031.

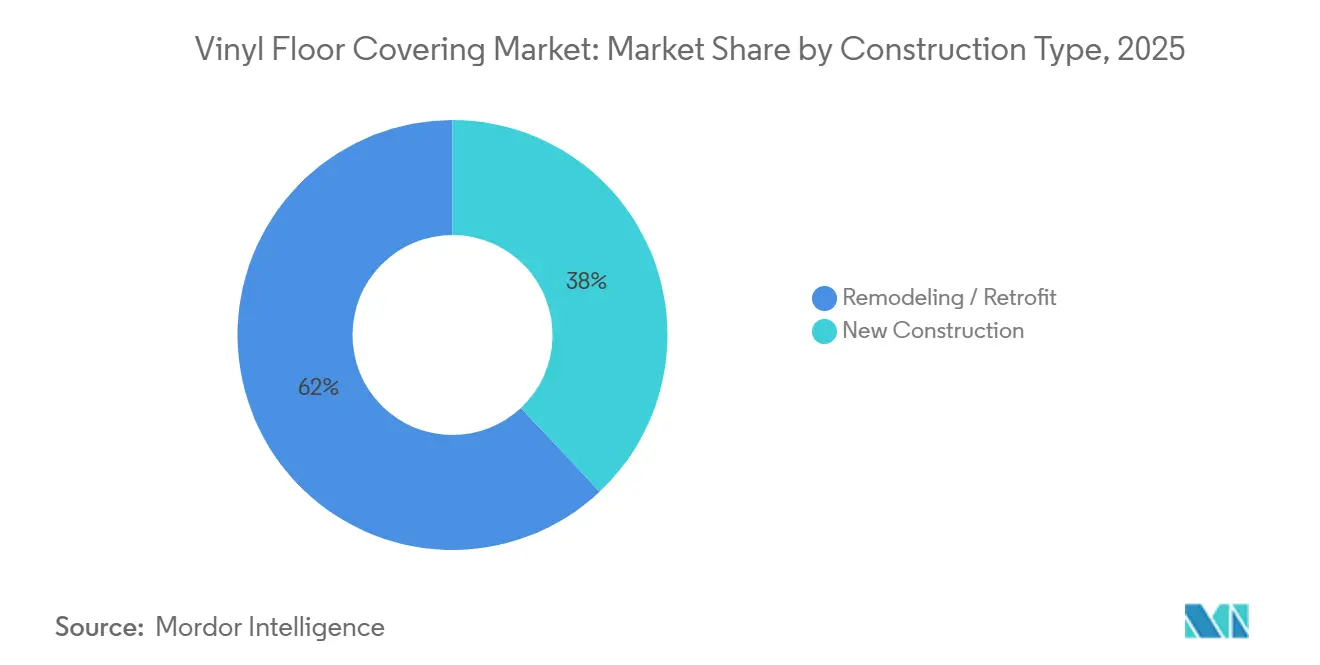

- By construction type, remodeling and retrofit projects commanded a 61.95% share in 2025; new construction is projected to grow at a 6.92% CAGR through 2031.

- By distribution channel, B2C retail captured 67.60% of 2025 sales; B2B contractor and builder channels are set to grow at a 6.78% CAGR through 2031.

- By geography, North America held 32.21% of 2025 revenue; Asia-Pacific is forecast to post the fastest growth at a 7.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vinyl Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LVT/SPC outcompetes wood/ceramic on waterproof durability, realistic designs, and installed cost | +1.8% | Global, with the highest penetration in North America and Western Europe | Medium term (2-4 years) |

| APAC construction and urbanization sustain multi-year vinyl demand | +1.5% | Asia-Pacific core, spillover to the Middle East & Africa | Long term (≥ 4 years) |

| Residential remodeling cycle and replacement favor easy, low-disruption vinyl upgrades | +1.2% | North America and Europe | Short term (≤ 2 years) |

| Omnichannel retail and click-and-lock DIY expand access and speed of adoption | +0.9% | Global, led by North America's online channels | Medium term (2-4 years) |

| ESG-driven specs accelerate PVC-free and circular resilient solutions in commercial bids | +0.7% | Europe and progressive U.S. municipalities (CA, NY, WA) | Long term (≥ 4 years) |

| Trade enforcement and tariffs catalyze nearshoring, improving lead times and reliability | +0.6% | North America, particularly the U.S. and Mexico, under the USMCA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

LVT/SPC Outcompete Wood/Ceramic on Waterproof Durability, Realistic Designs, and Installed Cost

Rigid-core vinyl formats address two common pain points in wood and ceramic, namely water exposure and subfloor preparation costs, which have allowed these lines to displace higher-cost categories without a visible downgrade in finish quality in many cases[1]National Wood Flooring Association, “Installation Guidelines and Best Practices,” National Wood Flooring Association, nwfa.org. Shaw Industries completed a USD 90 million expansion of its Ringgold, Georgia, plant in early 2026 to double SPC and LVT capacity, a move aimed at builders that need stable planks for basements and high-humidity coastal zones. Advances in synchronized embossing and digital print resolution now achieve realistic grain and stone veining while maintaining wear resistance that holds up to pets and wheeled traffic in mixed-use spaces. Installation labor requirements are lower because click systems avoid thin-set or multi-day acclimation, and industry cost references show installed totals that can undercut ceramic by a meaningful margin at scale in U.S. projects[2]National Association of Home Builders, “Remodeling and Labor Trends 2025,” National Association of Home Builders, nahb.org. These combined performance and cost characteristics have positioned rigid-core formats as standard options in many new and remodeled homes and in light-commercial spaces across the vinyl floor covering market.

APAC Construction and Urbanization Sustain Multi-Year Vinyl Demand

India’s building activity expanded in 2025 with 6.2% to 6.3% real growth, sustained by pipeline infrastructure outlays and state-backed housing programs that increase the use of durable, code-compliant finishes like vinyl in multi-tenant projects[3]Reserve Bank of India, “Economic Activity Index, January 2026,” Reserve Bank of India, rbi.org.in. China’s housing market showed signs of stabilization in 2025 and delivered 9.5 million urban housing units, while national urban renewal programs continue to prioritize occupied-building renovations where fast, low-disruption flooring is valued. Southeast Asia’s hospitality and retail development remains active, and project teams frequently select vinyl for tropical climates due to moisture tolerance and the ease of replacement during tenant turnover across franchise footprints. These conditions support a 2026 to 2031 regional growth rate that outpaces the global average for the vinyl floor covering market, reinforcing the strategic importance of local compounding and converting assets. Global brands continue to expand regional production and distribution to serve time-sensitive builds while avoiding transoceanic freight risks.

Residential Remodeling Cycle and Replacement Favor Easy, Low-Disruption Vinyl Upgrades

United States home-improvement outlays are projected to reach USD 522 billion by the end of 2026, with flooring among the top spend categories as owners replace aging surfaces during kitchen, bathroom, and basement projects. Homeowners with higher equity tend to prefer solutions installable in one to two days with limited furniture moving, and click-lock vinyl systems satisfy that requirement while avoiding adhesive off-gassing in occupied homes. Contractor backlogs for flooring work eased in 2025, helped by nearshore inventories and modular systems that raise daily install throughput and improve schedule predictability for remodelers. European renovation mandates tied to energy-performance certificates are also leading to floor replacements in older housing stock, where vinyl paired with approved Underlayments supports thermal and acoustic targets in cost-sensitive retrofits. These dynamics together reinforce a steady base of replacement-led demand for the vinyl floor covering market in mature economies through the forecast period.

Omnichannel Retail and Click-Lock DIY Expand Access and Speed of Adoption

Leading specialty retailers reported strong 2025 e-commerce gains as visualization tools helped consumers evaluate patterns, colors, and textures more confidently before purchase. Big-box home centers now synchronize storefront and distribution center stock status so customers and contractors can secure needed SKUs for pickup or delivery on compressed timelines, which shortens the gap between selection and installation starts for many vinyl jobs. Click-lock profiles continue to promote DIY adoption, supported by retailer workshops and rental tool programs that lower the barrier for first-time installers in kitchens and seasonal rooms. Product innovation is concentrating on locking geometry, integrated underlayment, and micro-bevel edges that improve perceived fit-and-finish for nonprofessional installs and reduce callbacks under satisfaction guarantees. The cumulative effect is broader access, faster conversion, and higher category velocity for the vinyl floor covering market in urban and suburban catchments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| End-of-life, VOC/IAQ concerns, and limited recycling infrastructure | -0.8% | Europe and progressive North American municipalities | Medium term (2-4 years) |

| PVC and plasticizer price volatility squeezes margins | -0.9% | Global, with acute pressure in Europe due to plant closures | Short term (≤ 2 years) |

| Installation labor shortages, subfloor and moisture prep failures drive callbacks | -0.6% | North America and Western Europe | Short term (≤ 2 years) |

| Quality issues in low-end SPC commoditization elevate warranty risk | -0.5% | Global, concentrated in import-heavy markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

End-of-Life, VOC/IAQ Concerns and Limited Recycling Infrastructure

California AB 863 places flooring containing ortho-phthalates under safer-consumer-products scrutiny and pushes brands toward take-back or safer-alternative pathways that meet procurement requirements for public projects[4]California Air Resources Board, “AB 863 Safer Consumer Products Program,” California Air Resources Board, arb.ca.gov. Third-party emissions certifications such as FloorScore and GREENGUARD Gold have become standard asks on school, healthcare, and LEED-oriented bids in the United States and Europe, channeling demand to validated low-emitting SKUs across resilient categories. Closed-loop recycling remains early, and while leading programs have diverted meaningful tonnage, post-consumer vinyl flooring is still landfilled or incinerated due to separation complexity at waste facilities. European regulatory updates under REACH are curbing certain phthalates in finished flooring, which increases reformulation costs but also expands the market for non-phthalate and biobased plasticizers over time. Together, these constraints encourage a shift toward circular designs and cleaner chemistries, with the vinyl floor covering market moving faster in jurisdictions that link green-building credits and procurement to emissions and take-back criteria.

PVC and Plasticizer Price Volatility Squeezes Margins

Raw-material volatility for PVC resin and plasticizers challenged planning and price commitments in 2025, and many distributors shortened buying horizons to manage risk, which lowered production visibility for fabricators. Brands with upstream capabilities in compounding and wear-layer formulation were better positioned to offset spikes through materials flexibility and cost averaging across lines. Biobased plasticizers derived from vegetable oils continue to gain interest for life-cycle and stability reasons, yet they still represent a small slice of overall plasticizer consumption due to performance and qualification needs in cold and UV-exposed environments. Pressure on gross margins led some manufacturers to rationalize slow-moving SKUs and streamline assortments to improve run lengths and reduce changeover waste during uncertain buying cycles. These adjustments help maintain service levels while the vinyl floor covering market waits for a more stable input-cost backdrop and improved contracting confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid Cores Claim Volume, Plank Aesthetics Drive Growth

Luxury Vinyl Tile captured 74.12% of the vinyl floor covering market share in 2025, anchored by rigid SPC and WPC cores that deliver stability and low-bounce performance in high-traffic settings. SPC has become the go-to choice for commercial zones with rolling loads due to its higher density and dent resistance, while WPC retains favor in senior living and hospitality areas for its softer underfoot feel. Luxury Vinyl Plank is projected to grow fastest at a CAGR of 6.72% through 2031, as residential remodelers and production builders replicate hardwood visuals in kitchens, living rooms, and basements without waterproofing or installation speed. Manufacturers continue to push synchronized embossing and matte finishes that elevate realism for oak, walnut, and stone designs, which keeps rigid-core offerings competitive against both wood and porcelain options in the vinyl floor covering market. Infection-control features such as antimicrobial wear layers are standardized in healthcare and education portfolios, which support specification in regulated environments.

In niche and value tiers, sheet vinyl retains a role in multifamily turnovers or large corridors where seam welding and continuous sheets lower first costs, and VCT serves specific institutional codes but continues to cede ground to LVT on design and maintenance performance. Within residential remodeling, planks in wider and longer formats favor open-concept spaces, and beveled edges that hide micro-gaps are improving DIY aesthetics. The vinyl floor covering industry is also coordinating with adhesive makers on reformulated systems for glue-down tiles and planks to meet tighter emissions thresholds in schools and healthcare. The vinyl floor covering market benefits from the breadth of formats that allow brands to match durability, acoustics, and cost targets at room-by-room granularity for large mixed-use developments.

By Installation Method: Interlocking Dominates DIY, Glue-Down Gains in Commercial

Interlocking formats accounted for 56.20% of the vinyl floor covering market share in 2025, reflecting homeowner preference for click systems that avoid adhesives and reduce install times without specialized tools. Angle-tap and drop-lock profiles allow single-crew installs to achieve high daily coverage, and the ability to remove and replace planks during future repairs supports life-cycle flexibility in occupied spaces. Glue-down is forecast to grow at 6.68% through 2031 as commercial specifiers in retail, hospitality, and healthcare settings require permanent anchorage and smooth transitions under wheeled traffic. Pressure-sensitive adhesives and system warranties tie installation practices to emissions and performance outcomes, which encourages closer alignment between flooring and adhesive engineering teams. Loose-lay and peel-and-stick retain roles for rapid retrofit and historic buildings where penetrations are restricted, rounding out a method mix that serves diverse job-site constraints in the vinyl floor covering market.

Capacity additions in domestic SPC lines are also tailored for glue-down commercial formats, signaling confidence that backlogged projects and retail refresh cycles will sustain demand for permanently anchored surfaces. Training and certification are increasingly tied to access in certain distributor networks, which raises the professional bar and helps reduce moisture-related callbacks in adhesive applications. The vinyl floor covering industry is responding with factory training modules and digital resources that segment best practices by subfloor and climate. This supports more predictable outcomes and aligns with a broader push for total-system warranties that integrate planks, Underlayments, and adhesives.

By End-User: Residential Volume Anchors Market, Commercial Specs Propel Growth

Residential applications made up 64.90% of 2025 revenue as ongoing remodels in kitchens, baths, and basements selected click-lock planks that balance moisture performance with attractive finishes. In the United States, a large cohort of homes built between 1980 and 2000 is entering peak remodeling age, which supports steady replacement volume for resilient surfaces within the vinyl floor covering market. Commercial applications are forecast to grow at 7.31% through 2031, with hospitality and retail leading as chains refresh interiors and align brand aesthetics across regional networks. Healthcare specifications center on weldable seams and antimicrobial surfaces that meet infection control expectations, while education bids focus on acoustics and durability for high-use spaces. Corporate offices are selecting vinyl in open-plan areas for reconfiguration flexibility, enabling space moves without demolition that disrupts business operations.

Public procurement increasingly embeds PVC-free and take-back language in RFPs, which is broadening evaluation criteria beyond first cost toward life-cycle metrics where qualified resilient systems can excel. Within multifamily rentals, thicker wear layers in commercial-grade LVT reduce turnover downtime and support lower total ownership cost models. The vinyl floor covering industry has responded with tiered lines that map durability and emissions profiles to use cases across residential and commercial verticals. This segmentation helps channel partners place the right product in the right setting and maintain performance confidence in both high-traffic and wet-area installations.

By Construction Type: Retrofit Leads Volume, New Construction Rebounds

Remodeling and retrofit projects commanded 61.95% of 2025 activity as existing stock volume far outweighs new completions in developed markets, keeping replacement-led demand central to the vinyl floor covering market. Retrofit economics favor click systems that can float over sound subfloors and avoid demolition, disposal, and extended drying windows. New construction is projected to grow at 6.92% from 2026 to 2031 as mortgage rates stabilize and household formation supports builder confidence in entry and move-up segments. U.S. single-family housing starts improved in late 2025, and builders continue to specify plank visuals to meet buyer expectations while keeping installed costs aligned to price points. Field codes in several states reference emissions criteria that increasingly limit compliant SKUs to low-VOC lines, which favors manufacturers invested in certified formulations.

The vinyl floor covering market size for new construction is projected to expand to a 6.92% CAGR between 2026 and 2031, which reverses the 2020 to 2023 pattern when higher rates slowed ground-up volumes and shifted focus to remodeling. Builder-standard LVP and LVT continue to move into higher price tiers as aesthetics and feel approach wood benchmarks, which supports broader adoption in primary living spaces. In parallel, retrofit remains a durable base as consumers prioritize projects that deliver quick results without disruptive tear-outs. Taken together, this split allows capacity to be balanced across floating and glue-down lines that align to each building phase and property type.

By Distribution Channel: B2C Retail Commands Share, B2B Contractor Networks Accelerate

B2C retail captured 67.60% of 2025 sales, led by home centers and specialty flooring chains that pair with broad SKU assortments with in-store design support and growing e-commerce capabilities for fast delivery. Online tools that visualize planks in actual rooms are improving conversion and reducing return friction across the vinyl floor covering market. B2B contractor and builder channels, while smaller, are projected to grow at a CAGR of 6.78% through 2031 as nearshored capacity and private-label programs shorten replenishment cycles for large projects. Trade actions that raised duties on certain imports have also realigned sourcing to domestic and regional partners in the United States and Mexico, which reinforces B2B velocity. Platform-style distribution that aggregates inventory access is gaining traction, which streamlines procurement and logistics for contractors that service multi-state accounts.

Domestic capacity moves, including acquisitions that add SPC lines, further support fast-turn B2B fulfillment and white-label flexibility for builders and regional distributors. Training and CE requirements in key states around moisture testing and adhesive selection for resilient floors raise practice standards in contractor channels, which benefits brands with comprehensive installer education. The vinyl floor covering industry is aligning assortment, service models, and digital tools to meet both consumer and professional expectations for speed and reliability. These steps sustain share in B2C while enabling share gains in B2B as project pipelines normalize.

Geography Analysis

North America held 32.21% of global revenue in 2025, supported by strong remodeling cycles and new nearshore capacity that reduces tariff exposure and freight risk for time-critical projects. The United States leads regional volume and continues to prioritize flooring within home improvement budgets, while Canadian provinces with tighter VOC rules tilt specifications to certified low-emitting lines. Shaw’s 2026 completion of a USD 90 million SPC and LVT expansion and AHF’s 2025 acquisition to add domestic SPC capacity reflect a shared strategy to anchor supply close to demand. Mexico is emerging as a converting hub under USMCA rules of origin, and the treaty review set for 2026 is expected to keep content requirements in focus for regional supply chains. The vinyl floor covering market size in North America, therefore, remains significant, with growth moderated by the pull-forward effect from 2020 to 2023 installations that created a temporary lull ahead of the next replacement wave.

Asia-Pacific is projected to post the fastest regional gains through 2031, with the vinyl floor covering market size in Asia-Pacific expanding at a 7.41% CAGR on the back of housing delivery and urban renewal programs that favor fast, low-disruption finishes. India’s 2025 construction growth near the mid-6% range and China’s 2025 delivery of 9.5 million urban housing units support sustained baseline demand across residential and mixed-use formats. Southeast Asian markets continue to add hotels and retail footprints where moisture-resistant flooring aligns with tropical conditions and rapid tenant turnovers, and regional production investments underscore the need to serve these pipelines without long ocean lead times. Japan and South Korea show steadier upgrades in healthcare and education specifications, where emissions and antimicrobial profiles hold outsized weight in product choice. Australia’s metro markets continue to blend new builds with retrofits that reference emissions certifications in local codes, providing steady avenues for certified resilient lines.

Europe’s 2026 to 2031 outlook is steady, supported by renovation mandates tied to energy-performance certificates and by procurement aligned to stricter indoor-air-quality thresholds under REACH for plasticizers. Germany, the United Kingdom, France, and Italy dominate spending, with BENELUX cities advancing pilots for circular product passports that open opportunities for PVC-free resilient systems. Nordics prioritize acoustics and emissions in healthcare and education, reinforcing use cases where certified LVT and sheet offerings can differentiate. In the Middle East, public and hospitality projects under national development plans emphasize rapid construction and low-VOC materials in government procurement, which aligns with certified resilient specifications and established take-back commitments. Across Africa, retail-format expansion in South Africa and urban growth corridors in select countries present incremental adoption pathways, with sourcing strategies responsive to tariff and logistics complexity that favor regionally held inventory within the vinyl floor covering market.

Competitive Landscape

The vinyl floor covering market features low market concentration, with multiple scaled manufacturers operating across regions and formats rather than a single dominant player, which maintains competitive intensity around service, assortment, and speed to market. Mohawk, Shaw, Tarkett, and Gerflor leverage vertical integration in compounding, wear layers, embossing, and branded networks, while also supporting private-label modules that expand reach in both B2C and B2B. Capacity additions and nearshoring remain a central playbook, as shown by Shaw’s 2026 capacity expansion and AHF’s 2025 SPC acquisition to support quick-turn replenishment and builder programs. Digital commerce and visualization tools help specialty retailers capture online momentum and guide shoppers to appropriate SKUs, which reinforces B2C leadership for category-focused chains. The resulting competitive dynamic rewards execution in quality control, installer education, and logistics agility across the vinyl floor covering market.

Sustainability and compliance are central to product roadmaps and to public procurement success. Tarkett’s take-back program has diverted substantial volumes of post-install and post-use materials since launch and continues to scale with clear reporting in 2025, while Interface has public targets to reduce operational emissions and expand biobased chemistries in selected portfolio lines. Manufacturers are aligning FloorScore and GREENGUARD Gold to meet third-party emissions validations that are table stakes in schools and healthcare. Patent activity reflects an emphasis on innovation in acoustic performance, thermal comfort, and antimicrobial protection, as well as on locking geometries and integrated Underlayments that streamline installation in the vinyl floor covering market. These features differentiate premium lines and support bids that equate better performance with lower long-term costs in high-use settings.

Trade policy and installer capacity influence go-to-market strategies. Antidumping and countervailing duty orders on certain vinyl flooring imports have reshaped sourcing toward North American and allied partners, reinforcing investments in U.S. and Mexican assets that enable 10-day or faster replenishment for national builders and large contractors. Training and certification are differentiators, with states requiring continuing education on moisture testing and correct adhesive selection for resilient floors, which benefits brands with end-to-end training and system warranties. Overall, the vinyl floor covering market rewards a balance of speed, consistent quality, verified emissions compliance, and clear sustainability progress that aligns with evolving procurement language in public and private sectors.

Vinyl Floor Covering Industry Leaders

Mohawk Industries

Tarkett SA

Shaw Industries Group

Gerflor Group

Mannington Mills

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tarkett published its 2025 sustainability report, disclosing that the ReStart take-back program diverted 124,000 tons of post-consumer flooring across 29 countries since inception, and reaffirmed a target to reach 30% recycled content by weight across resilient lines by 2030.

- November 2025: AHF Products completed the acquisition of Wellmade Performance Flooring, adding 200 million square feet of domestic SPC capacity in Dalton, Georgia, to serve production builders and distributors with sub-10-day lead times and private-label flexibility.

- October 2024: Shaw Industries announced completion of its USD 90 million expansion at Plant RP in Ringgold, Georgia, doubling Stone Plastic Composite and Luxury Vinyl Tile production capacity to serve North American residential and commercial markets, and adding advanced synchronized embossing lines for near-authentic wood and stone visuals.

Global Vinyl Floor Covering Market Report Scope

Vinyl flooring is a finished flooring material predominately made from a combination of limestone-based material mixed with composites of natural and synthetic polymer materials such as polyvinyl chloride and plasticizers.

The vinyl floor covering market is segmented by product, end-user, and geography. By product, the market is sub-segmented into vinyl sheet, vinyl composite tile, and luxury vinyl tile. By end-user, the market is sub-segmented into residential and commercial. By geography, the market is sub-segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| Luxury Vinyl Tile (LVT) | Stone Plastic Composite (SPC) |

| Wood Plastic Composite (WPC) | |

| Luxury Vinyl Plank (LVP) | |

| Sheet Vinyl | |

| Others (VCT, Resilient Vinyl-Backed Rubber Hybrid) |

By Installation Method

| Self-Adhesive Vinyl Tiles |

| Glue-Down |

| Interlocking Vinyl Tiles |

| Others |

By End-User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Remodeling / Retrofit |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Contractors / Builders |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Luxury Vinyl Tile (LVT) | Stone Plastic Composite (SPC) |

| Wood Plastic Composite (WPC) | ||

| Luxury Vinyl Plank (LVP) | ||

| Sheet Vinyl | ||

| Others (VCT, Resilient Vinyl-Backed Rubber Hybrid) | ||

| By Installation Method | Self-Adhesive Vinyl Tiles | |

| Glue-Down | ||

| Interlocking Vinyl Tiles | ||

| Others | ||

| By End-User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Remodeling / Retrofit | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Contractors / Builders | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the vinyl floor covering market?

The vinyl floor covering market size was USD 43.61 billion in 2025 and is projected to reach USD 61.19 billion by 2031 at a 6.53% CAGR from 2026 to 2031.

Which product formats are gaining the most traction in vinyl flooring?

Rigid-core LVT and LVP are leading due to waterproof performance, realistic designs, and easier installation, with LVP expected to grow fastest at 6.72% through 2031.

Where is regional growth strong for vinyl floor coverings?

Asia-Pacific leads the outlook with a 7.41% projected CAGR through 2031, supported by sustained construction and urban renewal pipelines in India, China, and Southeast Asia.

What installation methods are preferred across end markets?

Interlocking click systems dominate residential and DIY, while glue-down formats are gaining in commercial spaces for permanent anchorage and smoother transitions under wheeled traffic.

How are regulations shaping vinyl floor covering specifications?

Procurement and codes increasingly reference low-VOC certifications and phthalate restrictions, led by programs like FloorScore and GREENGUARD Gold and regulations such as California AB 863 and EU REACH Annex XVII.

What channels are sales on the vinyl floor covering market?

B2C retail holds the larger share of 2025 sales, while B2B contractor and builder channels are growing faster due to nearshore capacity and private-label programs that shorten replenishment cycles.

Page last updated on: