Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

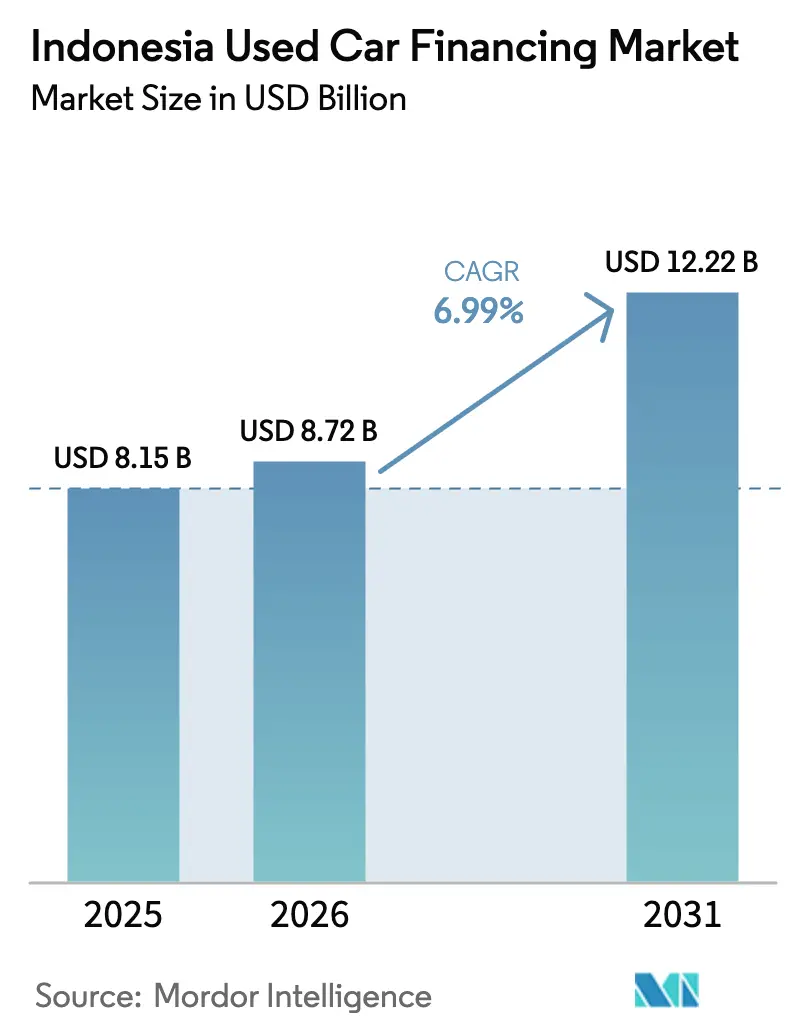

| Base Year Market Size (2025) | USD 8.15 Billion |

| Market Size (2026) | USD 8.72 Billion |

| Market Size (2031) | USD 12.22 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Used Car Financing Market Analysis by Mordor Intelligence

The Indonesian used car financing market size is projected to expand from USD 8.15 billion in 2025, USD 8.72 billion in 2026, to USD 12.22 billion by 2031, registering a 6.99% CAGR from 2026 to 2031. Surging household price sensitivity, a widening gap between new-car sticker prices and disposable income, and Bank Indonesia’s still-elevated lending rates have pushed many first-time and repeat buyers toward previously owned vehicles. Digital marketplaces that embed instant approvals shorten decision times from several days to less than 24 hours, attracting tech-savvy borrowers while lowering origination costs for lenders. Sharia-compliant products are scaling as Islamic banks and multifinance units formalize murabahah and ijarah contracts, tapping a large faith-driven customer base and deepening the Indonesian used car financing market. Competitive dynamics are intensifying because fintech platforms leverage alternative data for thin-file borrowers, although tighter OJK capital and governance thresholds now temper their fee upside. At the same time, supportive vehicle-quality improvements, especially in three-to-seven-year-old stock, enlarge collateral pools and stimulate longer tenors.

Key Report Takeaways

- By vehicle type, multi-purpose vehicles accounted for 44.15% of the Indonesian used car financing market share in 2025, while sport utility vehicles registered the fastest 8.45% CAGR through 2031.

- By financing provider, commercial banks controlled 70.25% of the Indonesian used car financing market share in 2025; peer-to-peer and fintech lenders posted the highest 9.75% CAGR to 2031.

- By tenor, the 25-48 month bracket captured 49.10% of the Indonesian used car financing market size in 2025, whereas loans longer than 72 months are set to climb at an 8.93% CAGR.

- By vehicle age, cars 3 years or older held 58.36% of the Indonesian used car financing market size in 2025; vehicles aged 4 to 7 years are projected to expand at a 10.14% CAGR.

- By province, Jakarta represented 32.11% of 2025 originations, and Banten is forecast to advance at a 7.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Used Car Financing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from New to Used Cars | +2.1% | Jakarta, West Java, East Java | Medium term (2–4 years) |

| Expansion of Multi-Finance and Bank | +1.8% | Java provinces, Banten | Medium term (2–4 years) |

| Digital Marketplaces Loan Approvals | +1.4% | Jakarta, Surabaya, Medan, Bandung | Short term (≤ 2 years) |

| Sharia-Compliant Auto Finance | +0.9% | Aceh, West Sumatra, Jakarta | Long term (≥ 4 years) |

| Buy-Now-Pay-Later (BNPL) | +0.6% | Jakarta, Banten, West Java | Short term (≤ 2 years) |

| Second-Hand Vehicle Incentives | +0.3% | Jakarta, Banten, Surabaya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Demand Shift from New- to Used-Cars Amid High Interest Rates

Used-car sales hit 1.8 million units in 2024 versus 889,680 new-car registrations, reflecting cost-driven substitution as nominal wage growth lags vehicle inflation [1]“2024 National Sales Data,” Association of Indonesian Automotive Industries, gaikindo.or.id . In September 2024, Bank Indonesia held its policy rate steady. As a result, many families faced auto-loan coupons that remained high. This scenario has amplified the affordability edge of three-year-old multi-purpose vehicles (MPVs), with their monthly installments being significantly lower than their brand-new counterparts. Responding swiftly, multifinance companies adjusted their portfolios. Notably, BFI Finance experienced a notable rise in showroom-linked receivables in 2024, underscoring a strong demand in organized retail channels. To counteract the effects of diminished purchasing power and sustain loan origination flows, lenders have begun extending loan tenors beyond the typical duration, showing an annual increase. However, this strategy does come with an extended credit-risk exposure. Overall, these dynamics underscore that affordability challenges are the primary drivers steering flows into Indonesia's used car financing market.

Expansion of Multi-Finance and Bank Loan Portfolios into Used-Cars

By June 2024, total motor-vehicle disbursements saw significant growth as lenders shifted focus to higher-yield pre-owned segments, responding to a dip in new-car demand. Adira Finance's merger with Mandala Multifinance in October 2025 birthed a platform with a substantial user base and extensive service points, significantly broadening its geographic footprint. In a similar vein, BCA Finance, in September 2024, streamlined its used-car specialist arm, harmonizing risk systems and slashing loan processing costs. While used-car financing commands wider spreads due to heightened asset risk perceptions, this is balanced by swift repeat purchases, with owners upgrading to newer models every three to four years. As a result, the Indonesian used car financing market continues to attract robust institutional capital, even as lenders implement stricter valuation measures to mitigate default risks.

Digital Marketplaces Embedding Instant Loan Approvals

E-commerce platforms now preload conditional credit offers inside vehicle listings, compressing the buyer journey from multi-day branch visits to less than 24 hours, a step change that accelerates funnel conversion. OTO Multiartha taps e-wallet histories, telephony metadata, and in-app purchase trails to underwrite applicants with thin bureau files, supporting the Indonesian used car financing market’s previously underserved segments. OJK Regulation 40/2024 requires verified credit scoring and borrower documentation, raising compliance costs yet formalizing data standards to stabilize asset quality. Fintech lenders are advancing at a notable CAGR through 2031, but their fee caps and foreign-ownership limits amplify the need for balance-sheet partnerships with banks. Speed and frictionless UX remain their key competitive levers as time-sensitive sellers demand fast certainty.

Growth of Sharia-Compliant Auto Finance Products

By December 2023, BCA Syariah reported growth in vehicle financing (KKB iB), highlighting the strong demand for interest-free financing options among Indonesia's predominantly Muslim population. Islamic financing structures, like murabahah, offer fixed installments and clear mark-ups. This not only protects borrowers from the unpredictability of floating rates but also ensures compliance with Islamic law. Bank Syariah Indonesia is expanding its OTO division, and in response to POJK 46/2024, multifinance firms are launching dedicated Sharia windows. New regulations now allow Sharia peer-to-peer variants, extending their reach beyond traditional bank branches. However, challenges remain: limited product understanding and a shortage of Sharia-certified appraisers for used vehicles hinder widespread acceptance. Yet, with ambitious financial inclusion goals, Sharia assets are poised to gain a stronger foothold in Indonesia's used car financing landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trust and Odometer Fraud | –1.2% | Secondary cities, rural areas | Medium term (2–4 years) |

| Lending Rates and Macro Volatility | –0.9% | Low-income national segments | Short term (≤ 2 years) |

| Collateral Fraud and Stolen-Vehicle Risk | –0.7% | Jakarta, Surabaya, Medan | Medium term (2–4 years) |

| OJK Caps on Fintech Lending | –0.5% | Digital platforms countrywide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Trust and Odometer Fraud Issues

Industry surveys reveal mileage manipulation in roughly one quarter of traded units, inflating residual values and saddling both borrowers and lenders with unexpected repair bills that erode collateral cover. The absence of a nationwide vehicle-history ledger forces lenders to rely on manual inspections that extend approval times and increase operating expenditure. While POJK 46/2024 mandates stronger appraisal standards and borrower verification, uneven regional enforcement allows informal dealers to bypass scrutiny, perpetuating credibility gaps[2]“POJK 46/2024 and POJK 40/2024 Regulatory Text,” Financial Services Authority, ojk.go.id . Blockchain registries piloted by selected multifinance firms aim to stamp immutable service records yet require cross-ministerial data sharing. Until coverage becomes universal, trust deficits will curb first-time penetration and temper Indonesia used car financing market.

Elevated Lending Rates and Macro-Volatility

In 2024, Bank Indonesia reduced its policy rate. However, final borrower coupons still exceed acceptable levels. This discrepancy arises as lenders account for currency risks and elevated wholesale funding costs. In 2024, rising bond yields increased BFI Finance's funding costs, even with stable gearing. Meanwhile, Adira Finance experienced a decline in new disbursements. Due to rate inertia, subprime affordability is strained, leading to shorter tenors. This situation nudges lower-income buyers towards gray-market creditors, who impose steep charges. As a result, macroeconomic shocks, like rupiah depreciation, can strain household budgets and dampen momentum in Indonesia's used car financing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: MPVs Maintain Scale as SUVs Accelerate

Multi-purpose vehicles held 44.15% of 2025 financing originations, underscoring their suitability for extended families that dominate Indonesian demographics. Compact SUVs are outpacing all other categories at an 8.45% CAGR as aspirational middle-class buyers gravitate toward higher ground clearance and premium perception, often paying resale premiums above same-age sedans. Lenders typically extend up to 80% loan-to-value on three-year-old MPVs or SUVs because of strong liquidity and predictable collateral curves, ensuring that the Indonesia used car financing market size tied to these segments remains robust through the forecast window.

Sedans and hatchbacks account for a dwindling slice as OEMs phase out low-margin small cars. Ride-hailing fleets still sustain sedan demand, but private owners pivot to crossover designs with more perceived status and safer cabin structure. Loan products now differentiate tenor ceilings: SUVs can qualify for 72-month terms, whereas older hatchbacks often cap at 48 months due to steeper depreciation. These underwriting nuances reinforce segmental divergence within the Indonesian used car financing market.

By Financing Provider: Banks Retain Scale, Fintechs Gain Pace

Due to low-cost deposits and the ability to cross-sell, commercial banks secured a commanding 70.25% share of the 2025 origination, solidifying their dominance in Indonesia's used car financing market. Yet peer-to-peer and fintech platforms are growing at 9.75% CAGR by offering real-time decisions and alternative credit analytics that onboard applicants sidelined by legacy scorecards. Non-bank multifinance firms sit between these poles, blending deep vehicle knowledge with moderate digital enablement, although their funding spreads face a squeeze from both ends.

Partnership models are proliferating: BCA Finance’s app now embeds inside leading marketplaces, closing the convenience gap with pure fintechs while preserving deposit-funded pricing. Regulation 40/2024 obliges peer-to-peer lenders to maintain a minimum composite rating of 3 and equity equivalent to 50% of paid-up capital, which raises thresholds and triggers consolidation. Joint ventures between digital lenders and mid-tier banks, therefore, become a critical route to scale inside the Indonesian used car financing market.

By Financing Tenor: Mid-Term Prevails, Ultra-Long Tenors Emerge

Loans of 25-48 months captured 49.10% of the 2025 pool, balancing monthly affordability with manageable credit exposure. However, loans longer than 72 months are expanding 8.93% annually as stretched households need smaller installments to absorb higher rate environments, especially for 4-to-7-year-old vehicles where ticket sizes are smaller but maintenance risk is higher. Lenders compensate through stepped-up pricing and stricter reserve buffers, aligning with POJK 46/2024’s risk-based provisioning model. Shorter tenors below two years now cater mainly to cash-rich buyers, optimizing interest payments, and a shrinking profile within the Indonesian used car financing market size matrix.

Dynamic pricing engines reward shorter contracts with lower coupons, yet competitive pressure to preserve volumes often overrides these signals. Average portfolio tenor at Adira Finance remained stable in 2024 as management prioritized credit quality, proving that policies toward tenor segmentation differ across institutions but still converge on meeting affordability thresholds for the broad borrower base.

By Vehicle Age: Younger Stock Leads, Mid-Age Grows Fastest

Cars up to three years old held 58.36% of financed units in 2025, reflecting lenders’ comfort with residual values and active resale channels supported by OEM warranties. The 4-to-7-year bracket is the fastest-growing at 10.14% CAGR as consumers accept higher mileage to curb upfront cost and as analytics tools sharpen valuation accuracy. Loans secured by cars older than seven years remain marginal because accelerated depreciation necessitates significant LTV caps and 36-month tenor limits, deterring many formal lenders and keeping this tier lightly penetrated by the Indonesian used car financing industry.

Supply dynamics also steer preferences. New-car sales slumped to 889,680 units in 2024, reducing future inflows of sub-three-year stock, so lenders are preparing collateral strategies for mid-age vehicles, including telematics-based condition monitoring to ensure asset integrity over longer repayment horizons.

Geography Analysis

Jakarta delivered 32.11% of 2025 volumes via dense branch footprints, higher per-capita income, and concentrated digital-lender marketing spend. The city’s regulatory scrutiny and traffic curbs, such as broader odd-even plate controls, now moderate incremental demand, nudging growth toward satellite regions. Banten, adjacent to the capital, is set to climb 7.28% CAGR through 2031, leveraging rapid industrial expansion in Tangerang and Serang that elevates middle-income commuter populations.

The three Javanese heartland provinces—West, Central, and East Java—benefit from sprawling manufacturing corridors that sustain steady vehicle demand among factory workforces. Still, household motorization often begins with two-wheelers; hence, per-capita four-wheeler penetration remains below that of Jakarta. Multifinance players such as Mandiri Tunas Finance therefore tailor underwriting to variable income patterns, adopting flexible payment schedules and mid-age collateral to deepen reach [3]“Branch Network Profile,” PT Mandiri Tunas Finance, mtf.co.id .

Banten’s proximity to Jakarta unlocks access to the capital’s vast used-car inventory while offering residents lower housing costs and lighter traffic, stimulating purchase intent. Its industrial parks drive formal employment, raising credit eligibility. In contrast, North Sumatra’s plantation economy and sparse lender branches hinder financing uptake, though mobile underwriting initiatives are making inroads. Nationwide, OJK mandates risk-governance parity across provinces, pushing lenders to invest in branch diversification and digital KYC to sustain compliance as they scale the Indonesian used car financing market.

Competitive Landscape

Indonesia’s used-car credit arena is moderately concentrated: the top three groups—Astra Credit Companies, BFI Finance, and Adira Finance—control a notable share of receivables, while commercial banks and their multifinance arms together exceed the majority of originations, leaving a long tail of smaller non-banks and fintechs. Digital challengers accelerate approval speed and target underbanked borrower pools using real-time data, but OJK’s tougher capital and governance ratios temper aggressive scaling, prompting partnerships with mid-tier banks for balance-sheet strength.

Strategic consolidation is prominent. BCA Finance absorbed BCA Multi Finance in September 2024, integrating risk systems and lowering operational duplication. Adira Finance merged with Mandala Multifinance in October 2025, lifting active users above 2.6 million and expanding to 850 locations. Banks deepen vertical integration to capture margin through direct cross-sell, aided by deposit funding that lowers cost-of-capital relative to market-priced bonds.

Growth avenues now include used EV and hybrid niches—supported by second-hand battery warranties—and Sharia-compliant pools. Technology adoption is decisive: end-to-end mobile workflows cut disbursement times to under a single day, and AI-driven valuation engines calibrate dynamic loan-to-value ratios by scanning marketplace price curves. Larger incumbents finance these upgrades through frequent bond programs; Adira’s Shelf Registration Bond VII attests to broad investor confidence despite higher rate environments [4]“Shelf Registration Bond VII Prospectus,” PT Adira Dinamika Multi Finance Tbk, adira.co.id . Compliance spending is climbing for all participants under POJK 46/2024, but scale players amortize that cost more efficiently, tilting competitive advantages toward larger balance sheets within the Indonesian used car financing market.

Indonesia Used Car Financing Industry Leaders

BFI Finance Indonesia

Astra Credit Companies (ACC)

Adira Dinamika Multi Finance

Mandiri Tunas Finance

Oto Multiartha

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Astra Group and Toyota Motor Asia (Singapore) Pte. Ltd. formed a strategic alliance, with Toyota taking a 40% stake in PT Astra Digital Mobil to broaden premium used-car access, financing, insurance, and aftersales services across Indonesia.

- August 2025: Carro, the largest and fastest-growing online used car platform in Asia Pacific, inked a Memorandum of Understanding with fintech platform SY Holdings. This strategic partnership aims to bolster Carro's expansion endeavors with tech-driven financing solutions. Carro boasts a dominant presence in key markets, including Singapore, Malaysia, Indonesia, Thailand, Japan, Taiwan, and Hong Kong SAR.

Indonesia Used Car Financing Market Report Scope

The scope includes segmentation by vehicle type (hatchback, sedan, sport utility vehicle, and multi-purpose vehicle), financing provider (captive OEM finance, commercial banks, non-bank finance companies, and peer-to-peer/fintech lenders), financing tenor (≤24 months, 25-48 months, 49-72 months, and above 72 months), and vehicle age (≤3 years old, 4-7 years old, and above 7 years old). The analysis also covers provincial-level segmentation, including Jakarta, West Java, East Java, Central Java, Banten, North Sumatra, and Other Provinces. Market size and growth forecasts are presented by value in USD.

By Vehicle Type

| Hatchback |

| Sedan |

| Sport Utility Vehicle (SUV) |

| Multi-Purpose Vehicle (MPV) |

By Financing Provider

| Captive OEM Finance |

| Commercial Banks |

| Non-Bank Finance Companies |

| Peer-to-Peer / Fintech Lenders |

By Financing Tenor

| Less than/Equals 24 Months |

| 25 - 48 Months |

| 49 - 72 Months |

| Above 72 Months |

By Vehicle Age

| Less than/Equals 3 Years Old |

| 4 -7 Years Old |

| Above 7 Years Old |

By Province

| Jakarta |

| West Java |

| East Java |

| Central Java |

| Banten |

| North Sumatra |

| Other Provinces |

| By Vehicle Type | Hatchback |

| Sedan | |

| Sport Utility Vehicle (SUV) | |

| Multi-Purpose Vehicle (MPV) | |

| By Financing Provider | Captive OEM Finance |

| Commercial Banks | |

| Non-Bank Finance Companies | |

| Peer-to-Peer / Fintech Lenders | |

| By Financing Tenor | Less than/Equals 24 Months |

| 25 - 48 Months | |

| 49 - 72 Months | |

| Above 72 Months | |

| By Vehicle Age | Less than/Equals 3 Years Old |

| 4 -7 Years Old | |

| Above 7 Years Old | |

| By Province | Jakarta |

| West Java | |

| East Java | |

| Central Java | |

| Banten | |

| North Sumatra | |

| Other Provinces |

Key Questions Answered in the Report

How fast will financing volumes grow between 2026 and 2031 in Indonesia’s used-car space?

Volumes are projected to rise at a 6.99% CAGR, lifting the Indonesia used car financing market size to USD 12.22 billion by 2031.

Which vehicle categories attract the most used-car loans?

Multi-purpose vehicles lead with 44.15% of 2025 originations, while sport utility vehicles are the fastest riser at an 8.45% CAGR.

Are digital lenders taking share from banks?

Yes, peer-to-peer and fintech platforms are expanding at 9.75% CAGR, though commercial banks still control 70.25% of 2025 volumes.

Which provinces will outpace national growth?

Banten is forecast to expand at a 7.28% CAGR through 2031, driven by industrialization in Tangerang and Serang that lifts middle-class car ownership.

Page last updated on: