Indonesia Digital Software Solutions Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

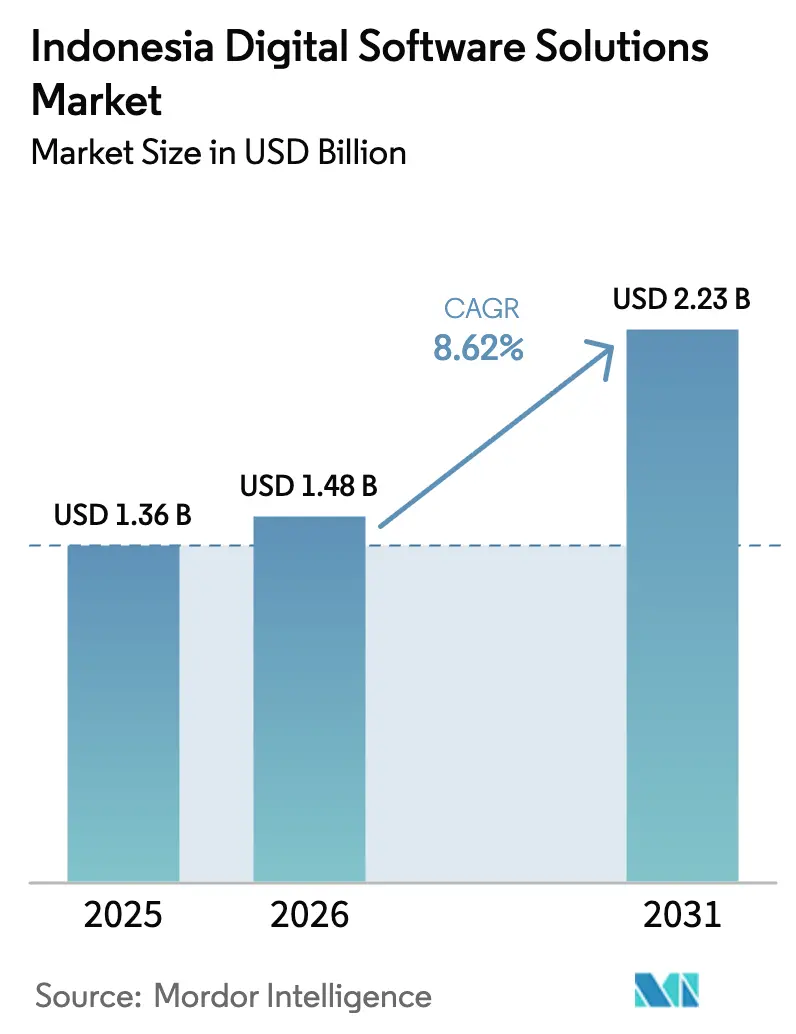

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 2.23 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

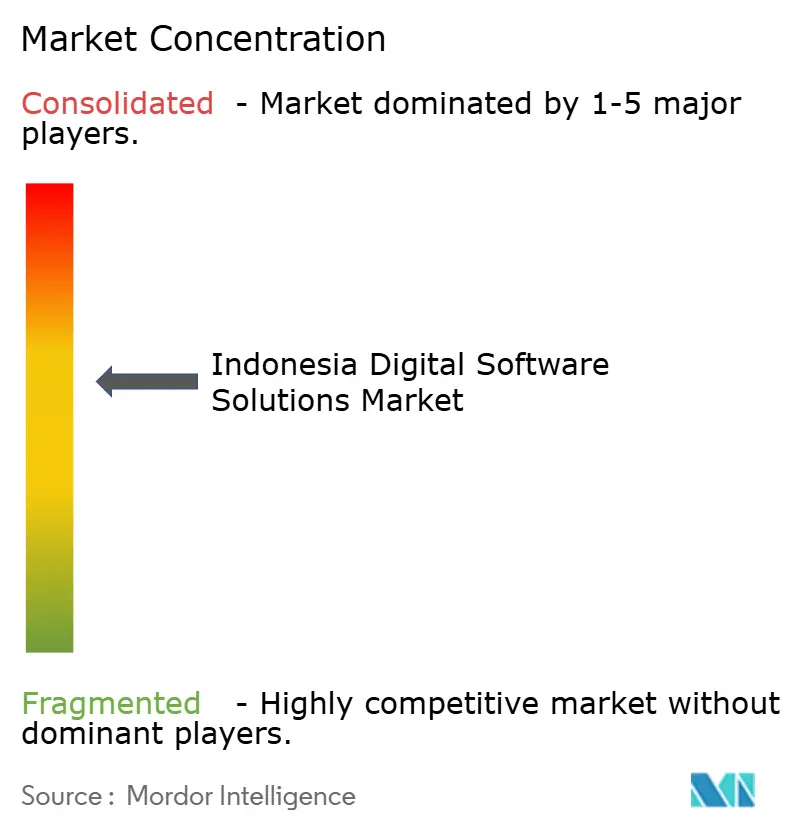

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Digital Software Solutions Market Analysis by Mordor Intelligence

Indonesia digital software solutions market size in 2026 is estimated at USD 1.48 billion, growing from 2025 value of USD 1.36 billion with 2031 projections showing USD 2.23 billion, growing at 8.62% CAGR over 2026-2031. Demand is accelerating as public-sector cloud mandates, hyperscale data-center incentives, and rapid e-commerce growth reinforce corporate investment priorities. Government directives, such as the nationwide e-invoice requirement and cloud-first procurement roadmap, are shortening decision cycles, while Microsoft’s USD 1.7 billion infrastructure commitment signals long-term support for local workloads.[1]Microsoft, "Microsoft announces US$1.7 billion investment to advance Indonesia's cloud and AI ambitions", microsoft.com/apacEnterprise buyers are rationalizing application portfolios around cloud-native suites; meanwhile, digital-native SMEs are adopting “ERP-lite” bundles that integrate payments, logistics, and tax compliance on a single subscription. Competitive intensity is rising: global vendors are deepening channel alliances, and local independents are packaging industry-specific add-ons that address regulatory nuances and language localization.

Key Report Takeaways

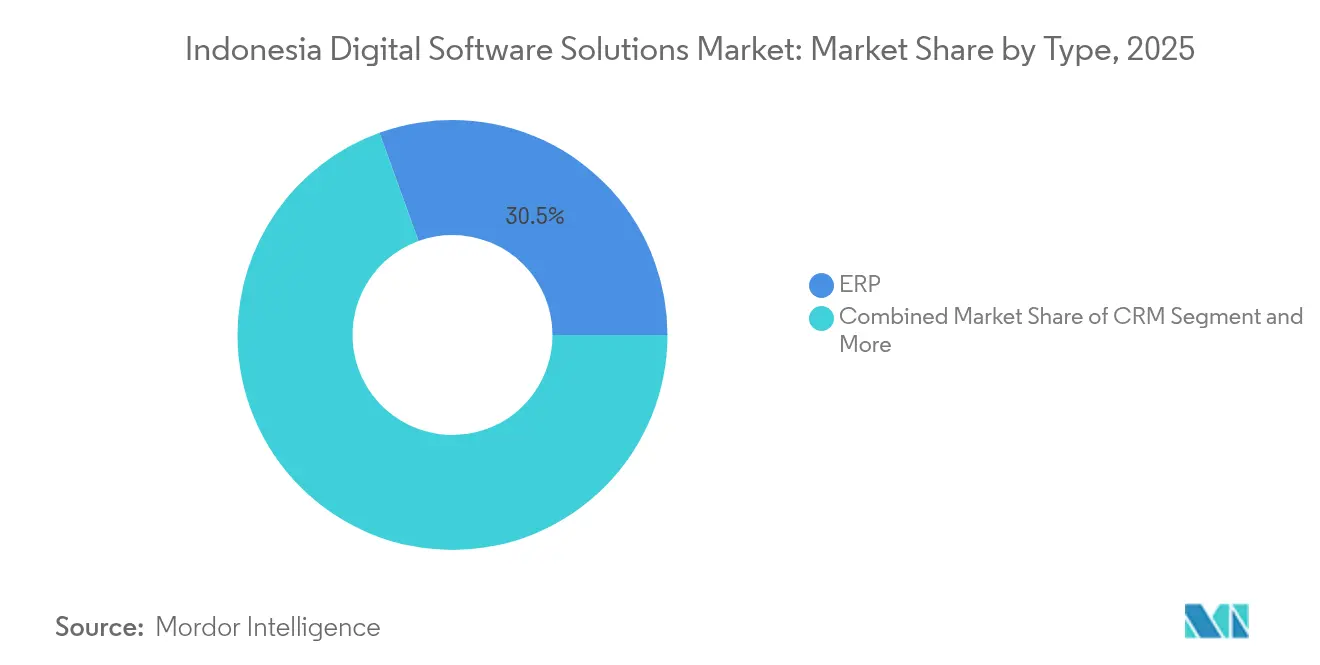

- By type, ERP captured 30.52% of Indonesia digital software solutions market share in 2025; customer communication management is forecast to grow at a 14.58% CAGR to 2031.

- By deployment mode, Cloud held 65.23% of the Indonesia digital software solutions market size in 2025, while cloud solutions are projected to expand at a 15.93% CAGR between 2026-2031.

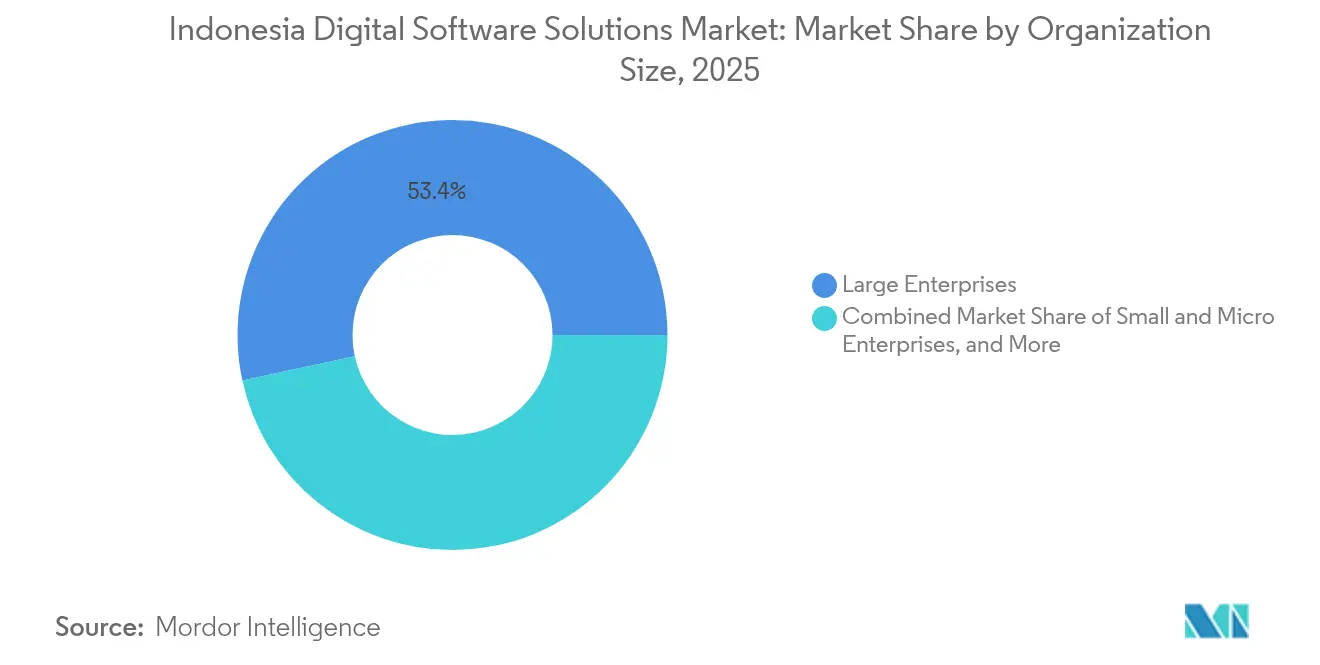

- By organization size, large enterprises commanded a 53.40% share of the Indonesia digital software solutions market in 2025; SMEs are advancing at a 16.28% CAGR through 2031.

- By industry vertical, BFSI led with 22.12% revenue share in 2025; retail and e-commerce are forecast to post a 16.44% CAGR to 2031.

- By geography, Java accounted for 57.36% of Indonesia digital software solutions market size in 2025; Sulawesi represents the fastest regional CAGR at 15.58% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Digital Software Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first procurement roadmap | +2.10% | National (Java centric) | Medium term (2-4 years) |

| Data-center tax holidays | +1.80% | Java, Sumatra | Long term (≥ 4 years) |

| Digital-native SME ERP-lite onboarding | +1.50% | Java, Bali & Nusa Tenggara | Short term (≤ 2 years) |

| National e-invoice mandate | +1.30% | National | Short term (≤ 2 years) |

| Talent repatriation fuelling ISV ecosystem | +0.90% | Java | Medium term (2-4 years) |

| Real-time payment APIs | +0.70% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-first Government Procurement Roadmap Stimulates SaaS Demand

Regulation 95/2018 prioritizes cloud procurement across ministries and agencies, eliminating lengthy CAPEX approval cycles and standardizing interoperability requirements. Since its rollout, public entities have lifted SaaS penetration by 30%, primarily in document management, citizen-service portals, and financial reporting. The policy’s technical guidelines are being mirrored by state-owned enterprises and private suppliers that transact with government, broadening addressable demand. Vendors that secure Perpres-compliant certifications become preferred partners, winning multi-year renewal contracts that bundle infrastructure, platform, and application layers. Integration blueprints created for public workflows are now reused in healthcare and utility deployments, lowering delivery costs and improving margin profiles.

Data-center Tax Holidays Attracting Hyperscale IaaS Partners

Corporate income-tax waivers of up to 20 years have positioned Indonesia as Southeast Asia’s next hyperscale hub. Fresh capacity from Microsoft, along with build-out announcements from AWS and regional telcos, is resolving data-sovereignty concerns and reducing latency for mission-critical SaaS. Cloud providers are cross-selling marketplace applications that embed local language packs and regulatory logic, accelerating time-to-value for end-users. Lower hosting costs are flowing through to subscription pricing, prompting price-sensitive retailers and provincial banks to shift workloads that were previously retained on-premise. GDP impact models suggest an incremental USD 10.7 billion contribution over five years as higher-order application adoption takes hold.

Surge in Digital-Native SMEs Onboarding ERP-lite Platforms

Mobile-first merchants that formed during the e-commerce boom are sidestepping legacy accounting packages and adopting modular suites delivered via app stores. Marketplace channels now influence 77% of micro-enterprise software purchases, and uptake is highest in foodservice, fashion, and creative crafts.[2]DAI Global, LLC, "MSMEs and Digital Tool Use amidst the COVID-19 Pandemic", dai.com Low-code configurability allows owners to stitch together inventory, storefront, and tax-filing functions without hiring in-house IT staff. Vendors are winning share by offering transparent per-transaction pricing and local payment-gateway integrations. Government targets to connect 30 million MSMEs are expected to widen the funnel, especially as regional development banks bundle software licenses with working-capital loans.

National e-Invoice Mandate Driving Accounting & CCM Upgrades

The e-Faktur 3.2 requirement obliges every business to generate standardized digital invoices with embedded signatures and XML payloads, pushing firms to retire manual spreadsheets. Mid-market manufacturers and distributors are accelerating platform refreshes to avoid compliance penalties, often opting for cloud upgrades that also deliver real-time analytics and automated reconciliations. Early adopters report cycle-time reductions of up to 40% in month-end closing, freeing finance teams to focus on cash-flow optimization. CCM vendors are embedding invoice templates alongside personalized marketing content, opening upsell pathways once core compliance is completed.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented broadband outside Java | −1.2% | Sumatra, Kalimantan, Sulawesi, Papua & Maluku | Medium term (2-4 years) |

| Informal SME bookkeeping | −0.9% | National (rural bias) | Long term (≥ 4 years) |

| Data-sovereignty clauses for cross-border SaaS | −0.7% | National | Short term (≤ 2 years) |

| Shortage of bilingual support engineers | −0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Broadband Outside Java Limits Cloud QoS

Sub-10 Mbps speeds in outer islands undermine real-time application performance, forcing vendors to maintain offline-sync logic that increases development cost. Enterprises in mining and agro-processing delay full SaaS migration, sustaining demand for hybrid or edge appliances. Government fiber-optic projects will narrow the gap, yet last-mile constraints persist, and some firms budget additional satellite links to guarantee uptime.

Persistent Informality of SME Bookkeeping Curbs Paid Adoption

Many micro-businesses still operate on cash-basis ledgers or paper notes, limiting the perceived value of premium accounting solutions. Vendors that tie offerings to working-capital financing or marketplace disbursement requirements are gradually shifting behavior, but cultural change remains gradual. Integration of POS data and simplified mobile onboarding are proving most effective in converting informal operators to subscription tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: ERP Retains Scale Advantage; CCM Breaks Out

ERP anchored the Indonesia digital software solutions market in 2025, holding a 30.52% share and serving as the digital core for enterprise resource planning, procurement, and manufacturing execution. Multinationals favor global templates from SAP and Oracle, whereas mid-tier corporates lean toward localized configurations delivered by PT Soltius Indonesia and similar partners.

Demand is strengthening in process industries that require lot-traceability and multi-plant consolidation. CCM, though smaller today, is gaining momentum at a 14.58% forecast CAGR as invoicing mandates converge with heightened customer-experience ambitions. Vendors bundle omni-channel templates, AI-based personalization, and analytics dashboards, turning compliance upgrades into revenue-generating projects. Business intelligence and CRM solutions continue steady double-digit growth, benefiting from the same cloud and API catalysts.

By Deployment Mode: Cloud Clips Legacy Footprint

Cloud workloads already influence more than 66% of new-license decisions and are scaling at a 15.93% CAGR, driven by subscription economics and lower maintenance overhead. SMBs have leapfrogged straight to public cloud, attracted by pay-as-you-grow tiers and local data centers that mitigate latency. Large enterprises still split budgets between private-cloud migrations and selective on-premise retention for regulated workloads, but hybrid architectures increasingly dominate RFPs.

Edge computing nodes located in manufacturing plants and hospital campuses are bridging inconsistent connectivity by processing data locally while syncing summary records to central repositories. On-premise implementations hold relevance in banking, defense, and regions where network reliability remains spotty, yet their relative contribution to Indonesia digital software solutions market size is eroding each year.

By Organization Size: Large Enterprise Budgets Dominate; SME Velocity Accelerates

Large enetrprises command 53.40% revenue in 2025. Corporates employing ≥500 staff, reflecting complex multi-module deployments and multi-year rollout programs. Chief information officers prioritize integrated roadmaps that combine ERP, analytics, and robotic process automation, frequently adopting a “platform of platforms” strategy to simplify vendor management.

Small and micro enterprises, however, are the fastest-growing cohort, expanding at 16.28% CAGR as low-entry SaaS nullifies historic capital barriers. Micro-enterprises are onboarding single-function apps—often invoicing or point-of-sale—before expanding into inventory and HR. Medium-sized firms favour suites that consolidate finance, inventory, and CRM under one contract, accelerating cross-sell potential for vendors that prove early value. This bottom-up dynamism is rebalancing Indonesia digital software solutions market share toward broader, price-sensitive segments.

By Industry Vertical: BFSI Deepens Core Upgrades; Retail Spurs Omnichannel Race

BFSI accounts for 22.12% of spending in 2025, driven by regulatory compliance, anti-fraud analytics, and omnichannel engagement initiatives that connect core banking systems to mobile apps. Cloud readiness statements from the central bank have unlocked migration of tier-two workloads, spurring demand for native security layers and automated testing.

Retail and e-commerce are scaling at 16.44% CAGR as omnichannel order-management, last-mile logistics, and personalized loyalty programs become competitive necessities. Manufacturing investments focus on supply-chain visibility and predictive maintenance, while healthcare moves toward electronic health records and telemedicine portals. Verticals reliant on extractive industries are piloting workflow automation tied to environmental and safety reporting, expanding the functional breadth of Indonesia digital software solutions market.

Geography Analysis

Java anchors 57.36% of Indonesia digital software solutions market size owing to dense enterprise headquarters, superior fiber coverage, and a robust talent pipeline. Jakarta’s banking cluster drives core-system overhauls, Bandung’s engineering schools feed the ISV ecosystem, and Surabaya’s manufacturing corridor accelerates adoption of plant-level analytics. Sumatra follows with a 15.32% share, leveraging Medan’s agro-industrial base and Palembang’s petrochemical complex to justify ERP and maintenance-planning deployments. Kalimantan contributes 8.41%, primarily from mining majors requiring asset-integrity platforms and regulatory reporting automation.

Sulawesi represents 18.91%, yet growth trajectories outpace national averages as connectivity programs narrow the digital divide. Makassar is positioning itself as an eastern logistics hub, stoking demand for transport-management systems. Tourism-driven Bali consumes guest-experience platforms and property-management software, while remote Papua projects experiment with satellite-enabled cloud instances to support hospital information systems. Hyperscale points-of-presence scheduled for 2026 are expected to reduce regional latency by up to 40 milliseconds, further broadening the practical reach of cloud services. The evolving spread underscores the multi-regional potential of Indonesia digital software solutions market beyond its Java stronghold.

Competitive Landscape

Indonesia digital software solutions market remains semi-consolidated: three global vendors dominate core applications, but local specialists sustain meaningful share through customization and segment focus. Oracle, SAP, and Microsoft maintain entrenched enterprise bases, leveraging reference architectures and certified partners to win repeatable deals. PT Soltius Indonesia, PT Abyor International, and Telkomsigma differentiate via Bahasa-first support, flexible payment schedules, and deep localization of tax and payroll modules. Strategic alliances are proliferating; IBM’s purchase of Equine Global added 500+ project references and fortified service depth, illustrating the premium placed on local delivery capability.

Cloud adoption has tilted competitive dynamics: hyperscalers curate marketplaces featuring fintech, agritech, and healthtech micro-ISVs, offering them instant national distribution. Start-ups exploit this channel to undercut incumbents on price while focusing on vertical depth. The infusion of AI capabilities—predictive maintenance, credit scoring, conversational analytics—is raising switching costs and embedding software deeper into operational workflows. Overall, pricing remains rational, but implementation services are the battleground as clients demand quicker time-to-value and agile change management.

Indonesia Digital Software Solutions Industry Leaders

-

Oracle Corporation

-

SAP SE

-

Microsoft Corporation

-

Salesforce Inc.

-

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Microsoft opened its first Indonesian cloud region, enabling in-country data residency and sub-50 ms latency, a foundation for real-time ERP and analytics workloads.

- April 2025: Microsoft committed USD 1.7 billion to Indonesian cloud and AI capacity, including skilling programs that aim to certify 2.5 million professionals by 2030.

- November 2023: IBM acquired ERP consultancy Equine Global, integrating 225 enterprise customers and reinforcing hybrid-cloud delivery expertise.

- October 2023: Fifteen Australian tech firms signalled Indonesia expansion plans during the Southeast Asia Tech Immersion Mission, broadening inbound competition.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Indonesia's digital software solutions market as all packaged or subscription-based enterprise applications, ERP, CRM, workflow, and customer communication platforms, delivered on-premise or through public and private clouds to Indonesian end-users. According to Mordor Intelligence, revenue reflects license, implementation, and annual service fees booked locally for new deployments as well as major upgrades.

Scope Exclusions: Pure custom software development, outsourced IT services, and stand-alone cybersecurity hardware are excluded.

Segmentation Overview

-

By Type

- Enterprise Resource Planning (ERP)

- Customer Relationship Management (CRM)

- Business Intelligence and Analytics (BI)

- Human Capital Management (HCM)

- Supply-Chain Management (SCM)

- Customer Communication Management (CCM)

- Workflow and Process Automation

- Other Packaged Software (EAM, PLM, etc.)

-

By Deployment Mode

- Cloud

- On-premise

-

By Organization Size

- Small and Micro Enterprises (≤100 FTE)

- Medium Enterprises (101-499 FTE)

- Large Enterprises (≥500 FTE)

-

By Industry Vertical

- BFSI

- Telecom and IT Services

- Manufacturing

- Healthcare and Life Sciences

- Retail and E-commerce

- Energy, Mining and Utilities

- Public Sector and Education

- Transportation and Logistics

- Other Industries

-

By Region

- Java

- Sumatra

- Kalimantan

- Sulawesi

- Papua and Maluku

- Bali and Nusa Tenggara

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed software vendors, channel partners, and CIOs across the archipelago to test volume assumptions, discount structures, and cloud-migration velocity. Follow-up surveys with finance heads of mid-market manufacturers validated average seat-expansion budgets and upgrade cycles.

Desk Research

We began with open datasets such as Statistics Indonesia's ICT expenditure tables, Bank Indonesia's quarterly capex index, Kominfo e-invoice adoption bulletins, and customs records for packaged-software imports. Company filings and press releases benchmarked large rollouts, while paid feeds from D&B Hoovers and Dow Jones Factiva supplied audited revenue splits.

Further context came from APJII broadband surveys and the Indonesian Employers Association's SME digital-maturity polls, which clarified user pools and typical price points across Java, Sumatra, and emerging eastern provinces. The sources mentioned are illustrative; many others informed data collection and validation.

Market-Sizing & Forecasting

A top-down build starts with national enterprise IT spend and software import duties, which are then filtered through application-penetration ratios, SaaS seat-growth rates, average selling-price trends, e-invoice compliance adoption, and data-center capacity additions. Supplier roll-ups and sampled ASP x volume checks provide selective bottom-up cross-checks.

Multivariate regression, using GDP at factor cost, cloud-MW additions, Regulation 95/2018 licensure filings, and APJII broadband coverage, drives the 2025-2030 forecast. Where bottom-up evidence lags, gaps are imputed through scenario averages agreed with interviewed experts.

Data Validation & Update Cycle

Variance scans, anomaly flags, and multi-level analyst reviews precede release. The model refreshes yearly, with interim updates triggered by material policy or exchange-rate shifts.

Why Mordor's Indonesia Digital Software Solutions Baseline Earns Trust

Published estimates often diverge because providers mix services with software, apply dissimilar cloud mark-ups, or lock exchange rates months ahead.

One public analysis pegs 2025 revenue at USD 1.25 billion. Another, built around an IT-services umbrella, assigns a far higher USD 6.32 billion value for 2024.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.36 bn (2025) | Mordor Intelligence | - |

| USD 1.25 bn (2025) | Regional Consultancy A | Omits low-ticket SaaS add-ons and updates currency at 2022 rates |

| USD 6.32 bn (2024) | Global Consultancy B | Bundles consulting and infrastructure with packaged software, inflating base |

These contrasts show that when scope clarity, live currency factors, and dual-check modeling converge, Mordor's baseline offers a balanced, transparent yardstick that executives can rely on for strategic planning.

Key Questions Answered in the Report

What is the size of the Indonesia digital software solutions market in 2026?

It stands at USD 1.48 billion and is forecast to grow at 8.62% CAGR to reach USD 2.23 billion by 2031.

Which segment currently generates the largest revenue?

ERP applications hold 30.52% share, reflecting their role as the transactional backbone for enterprises.

How fast is cloud deployment growing compared with on-premise?

Cloud solutions are projected to expand at a 15.93% CAGR, while on-premise footprints are slowly contracting.

Why is the BFSI sector a leading buyer of software in Indonesia?

BFSI invest heavily in compliance, analytics, and omnichannel systems, accounting for 22.12% of total spend.

Page last updated on: