Cross-Domain Solution Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.24 Billion |

| Market Size (2031) | USD 7.29 Billion |

| Growth Rate (2026 - 2031) | 11.45% CAGR |

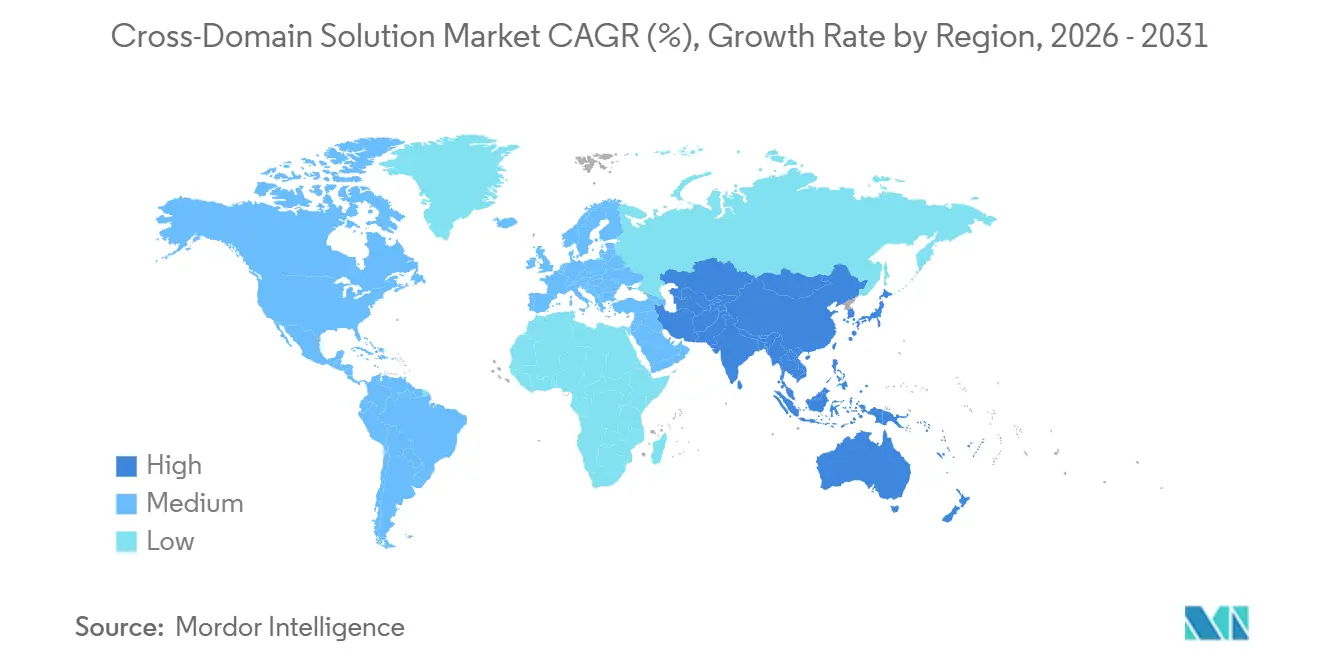

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

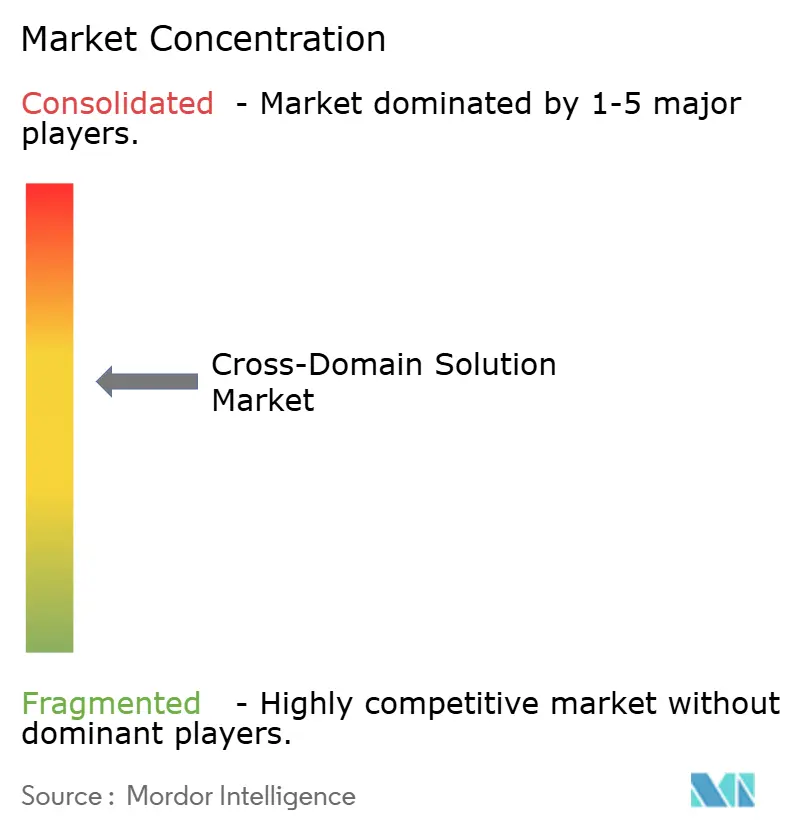

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cross-Domain Solution Market Analysis by Mordor Intelligence

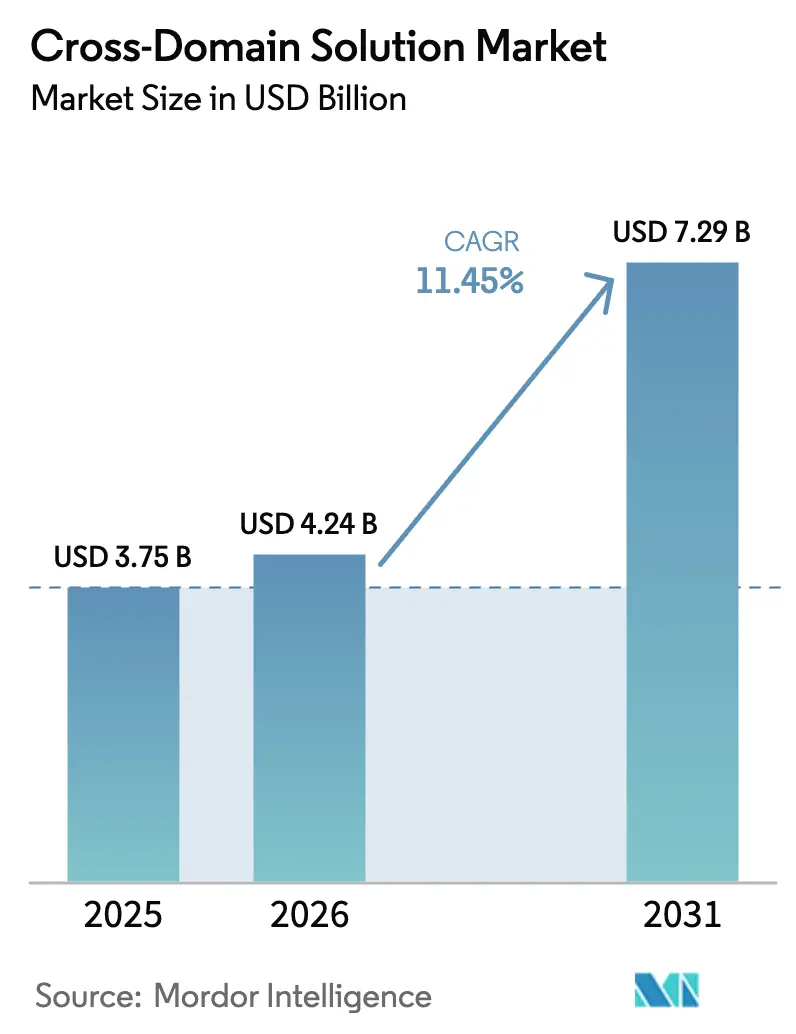

The Cross-Domain Solution market size is projected to be USD 3.75 billion in 2025, USD 4.24 billion in 2026, and reach USD 7.29 billion by 2031, growing at a CAGR of 11.45% from 2026 to 2031. Demand is pivoting from isolated air-gapped appliances toward software-defined guards that compress decision cycles from hours to seconds, a shift powered by zero-trust policies, AI-driven targeting loops, and hyperscale cloud enclaves. Program offices now weight contracts toward integration skill sets because continuous compliance, automated policy orchestration, and 24/7 monitoring outstrip the value of hardware alone. Cloud-hosted secret regions have converted budget-constrained agencies into subscription buyers, while satellite constellations and unmanned systems fuel need for low-SWaP edge nodes. Competitive intensity remains moderate as the top five vendors hold a collective 55% revenue share, leaving fertile ground for niche specialists that can clear multi-authority certifications within 18 months or less.

Key Report Takeaways

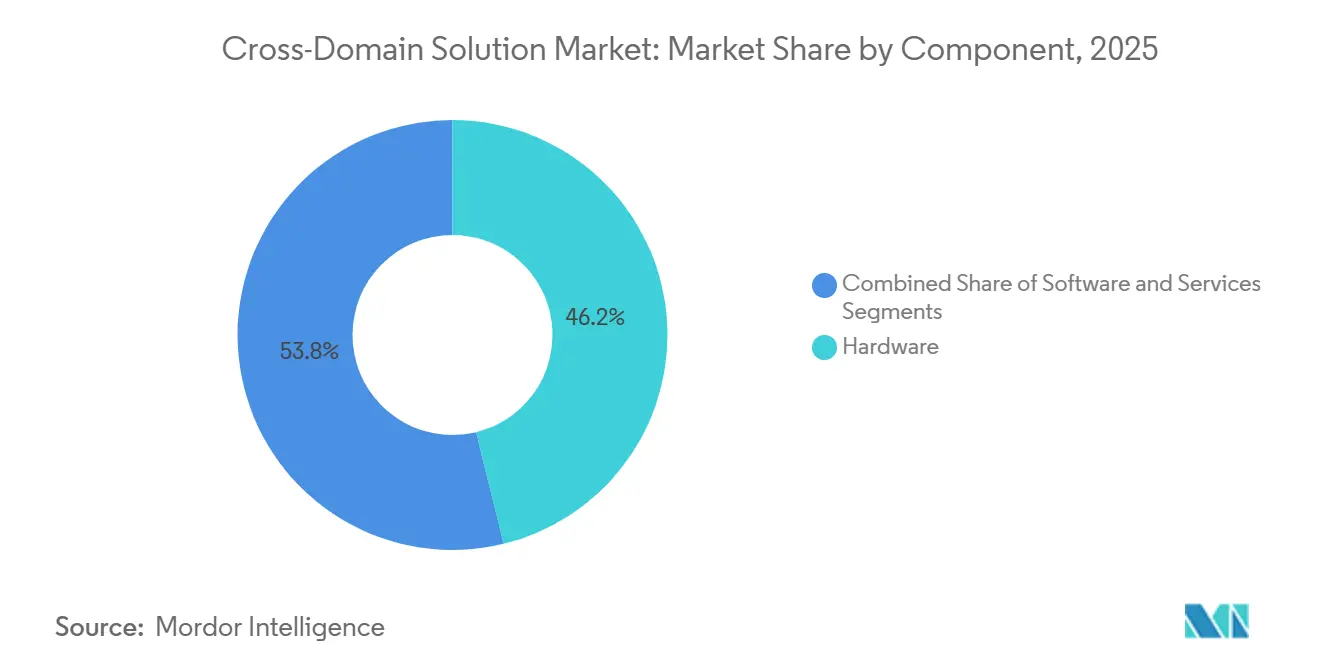

- By component, hardware commanded 46.19% of revenue in 2025, while services is projected to advance at an 11.84% CAGR through 2031.

- By solution type, transfer solutions accounted for 41.27% of revenue in 2025, whereas multi-level solutions are forecast to grow at a 12.22% CAGR through 2031.

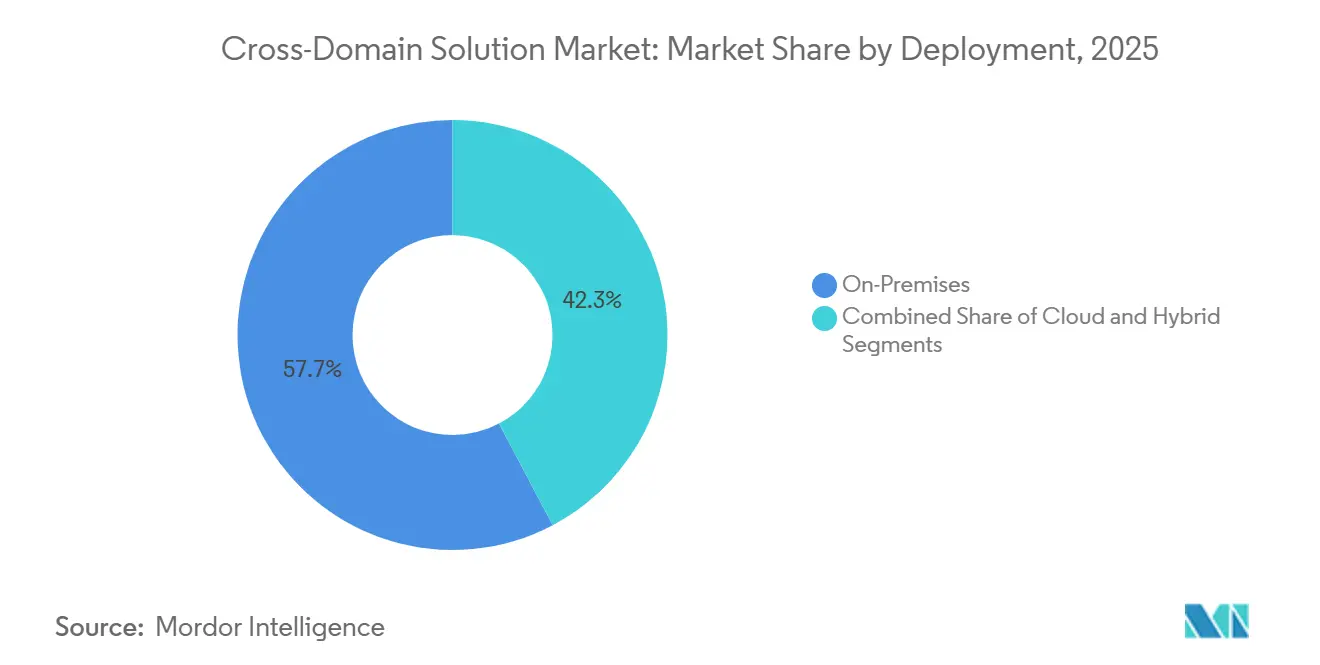

- By deployment, on-premises captured 57.71% share in 2025, yet cloud deployment is expected to expand at a 12.55% CAGR over the forecast period.

- By end-user, aerospace and defense held 49.64% of spending in 2025, while critical infrastructure operators are anticipated to rise at an 11.98% CAGR through 2031.

- By geography, North America led with 43.53% of global revenue in 2025, whereas Asia-Pacific is projected to be the fastest-growing region at a 12.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cross-Domain Solution Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Volume of Multi-Domain Classified Data Flows | +2.80% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Stringent Zero Trust Mandates in U.S. DoD and NATO | +2.30% | North America and Europe | Short term (≤ 2 years) |

| Rapid Proliferation of AI/ML Decision-Support Systems Requiring Air-Gapped Feeds | +2.00% | Global, early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing Use of Commercial Cloud Enclaves for Secret Workloads | +1.60% | North America, expanding to Europe and Asia-Pacific | Medium term (2-4 years) |

| Space-to-Ground Telemetry Security Gaps in New Satellite Constellations | +1.20% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Surge in OT-IT Convergence Across Critical Infrastructure | +1.00% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Volume of Multi-Domain Classified Data Flows

Joint all-domain command and control architectures funnel imagery, signals intelligence, and edge-sensor feeds across security levels in real time, eclipsing human-mediated review capacity.[1]United States Space Force, “Proliferated Low Earth Orbit Constellation Factsheet,” spaceforce.mil High-throughput cross-domain gateways now process petabytes daily, with NATO targeting 2028 for full interoperability between national secret networks and NATO Secret.[2]NATO Allied Command Transformation, “Multi-Domain Operations Concept,” act.nato.int Velocity adds further strain because targeting loops in contested theaters compress to minutes. As constellations reach full orbit density by 2027, automated guards capable of line-rate Deep Content Inspection become non-negotiable. These dynamic supplies the single largest uplift to the Cross-Domain Solution market by widening every procurement’s scope and budget envelope.

Stringent Zero Trust Mandates in U.S. DoD and NATO

The U.S. Department of Defense’s 2024 Zero Trust Strategy obliges every enclave boundary to verify user, device, and data attributes continuously, a stance that invalidates static one-way diodes.[3]U.S. Department of Defense, “Zero Trust Strategy and Roadmap,” defense.gov NATO mirrored the posture through its Secure Digital Infrastructure Programme in 2025, earmarking EUR 1.2 billion (USD 1.3 billion) for cross-domain-ready zero-trust stacks.[4]NATO, “Secure Digital Infrastructure Programme Overview,” nato.int Allied defense ministries from the United Kingdom to Germany have aligned funding lines, creating synchronized, near-term demand. Vendors with plug-and-play identity-provider connectors and policy-as-code toolkits see shortened sales cycles because compliance timelines are fixed for 2027. The mandate’s immediacy converts policy into capex, bolstering near-term revenue certainty.

Rapid Proliferation of AI/ML Decision-Support Systems Requiring Air-Gapped Feeds

Classified AI models mix top-secret satellite imagery with lower-classification sensor tracks, forcing bidirectional transfers of model weights and inference outputs under immutable provenance tags. Commercial providers such as Google Cloud support Impact Level 5 containers, but only after cross-domain guards scrub payloads for embedded malicious code. Policy engines now inspect not just files but tensors, validating training data lineage before elevation. As more agencies embed machine learning in every mission thread, the need for GPU-optimized, low-latency guards scales with inference frequency. This factor secures long-tail momentum for the Cross-Domain Solution market through 2031.

Growing Use of Commercial Cloud Enclaves for Secret Workloads

AWS Secret Region, Azure Government Secret, and similar offerings have lowered the entry barrier for agencies lacking high-side data centers. However, every burst from on-premises to cloud requires encrypted inspection at the guard tier, introducing measurable latency and sparking a mini-arms race for throughput. FedRAMP’s High Baseline Plus of 2024 expanded coverage to container orchestration and supply-chain attestation, prompting a wave of re-architecture that includes guard modernization. Providers that certify virtual guards for cloud marketplace deployment capitalize on consumption-based revenue streams, anchoring mid-term growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Multi-Authority Certification Cycles | -1.80% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Scarcity of Cross-Domain-Aware DevSecOps Talent | -1.30% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Lack of Interoperability Standards for Data-Diode Protocols | -0.90% | Global | Long term (≥ 4 years) |

| High Total Cost of Ownership for Small-Footprint Deployments | -0.70% | Global, disproportionate impact on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Multi-Authority Certification Cycles

Guards destined for coalition operations must clear NATO, NSA, and often national cyber authorities, a gauntlet that can stretch beyond 36 months. With only 14 products on the NSA’s Commercial Solutions for Classified list as of 2026, evaluation queues lengthen, inflating non-recurring engineering costs. Small vendors lose critical runway as certification outlays absorb over one-fifth of annual R&D budgets. The result is slower feature cadence and delayed revenue recognition, shaving 1.8 percentage points off expected market growth.

Scarcity of Cross-Domain-Aware DevSecOps Talent

Clearance-holding engineers versed in policy-as-code remain rare, with 68% of federal cybersecurity teams reporting vacancies exceeding nine months to fill. University pipelines lag, showing only seven accredited programs worldwide. Salary premiums of 35% over conventional cybersecurity roles pressure program budgets and extend deployment timelines. Talent constraints manifest as slower integration, higher operating costs, and increased reliance on service wrappers that distort total cost of ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Command Growth Momentum

Services secured an expanding revenue footprint because agencies now prize continuous certification documentation, threat-hunting, and policy tuning over device acquisition. A 2025 Air Force rollout allocated 58% of contract value to managed services, underscoring that the Cross-Domain Solution market is morphing into an outcomes-oriented business model. Software follows close behind as container-native guards integrate into DevSecOps pipelines, enabling blue-green updates without physical swaps. Hardware revenues remain positive, yet their relative weight shrinks as budgets earmark refresh cycles for compute-accelerated inspection blades rather than complete chassis replacement.

Hardware still anchors brownfield sites because rack-mounted appliances deliver predictable performance in electromagnetically shielded vaults. Yet certification-ready, cloud-portable code bases help the Services line item outpace boxed units at an 11.84% CAGR. Vendors that bundle compliance automation with 24/7 monitoring earn sticky multi-year renewals, reinforcing a recurring-revenue mix that elevates valuation multiples across the Cross-Domain Solution market.

By Solution Type: Multi-Level Architectures Outstrip Point Transfers

Users with mixed clearance badges now access shared data lakes where attribute-based guards enforce granular policy, cutting procurement duplication. NATO’s Multilevel Security Gateway standard galvanized 12 member states to converge on interoperable platforms by 2027. Transfer Solutions survive by modernizing with dynamic labelling engines, yet their 41.27% legacy share is tapering. Access Solutions provide cavity-free read-only interfaces for law enforcement, protecting chain-of-custody requirements while feeding nationwide threat portals.

Multi-Level Solutions register the fastest expansion because they dovetail with zero-trust doctrine that favours context-rich session handling over bulk exports. The trajectory suggests the Cross-Domain Solution market size for multi-level deployments could rival Transfer Solutions before 2031 if procurement preferences continue shifting at the present pace.

By Deployment: Cloud Traction Outpaces Air-Gap Orthodoxy

FedRAMP High Plus accreditation opened the door for secret workloads on commercial hyperscale’s, yielding a 12.55% CAGR for cloud deployment models. agencies stagger workloads, hosting tactical logistics in the cloud while reserving on-premises nodes for highly sensitive war-planning data. Hybrid architectures flourish, with brigade headquarters using rack-mounted guards for last-mile radio ingest while bursting analytic tasks to GovCloud regions.

On-premises installations keep their 57.71% hold because some nations still lack sovereign cloud certifications, and air-gap policies remain embedded in doctrinal checklists. Yet every cloud migration wave embeds a guard-modernization budget line, lifting aggregate Cross-Domain Solution market demand irrespective of physical location.

By End-User: Critical Infrastructure Operators Rapidly Scale Adoption

Aerospace and Defense, with almost half of 2025 spending, remains the bellwether client class, but regulatory shockwaves have vaulted pipelines, rail, and electric utilities into the fastest-growing slot. Updated TSA directives compel over 300 asset owners to erect segmentation gateways by end-2025. Utilities bound by NERC-CIP now budget multi-year refreshes, elevating service revenues through 2029.

Law-Enforcement and Security Agencies deploy read-only access guards to feed fusion centers without leaking investigative sources, while Government Civilian Agencies lag due to fiscal caps. Still, federal grant programs ensure a baseline of momentum, confirming that mission-critical adoption will continue diffusing beyond defense and intelligence, enlarging the Cross-Domain Solution market.

Geography Analysis

North America maintained 43.53% of global turnover in 2025 as the U.S. defense budget set aside USD 13.2 billion for cybersecurity line items that envelope cross-domain infrastructure. Canada injected CAD 2.1 billion (USD 1.5 billion) into network interoperability upgrades to remain plug-and-play with classified U.S. systems. Mexico entered the arena by piloting guards at joint task-force headquarters combating organized crime, underscoring regional vertical expansion. Certification bottlenecks, however, temper the growth rate because the NSA cleared only two new products in 2025, producing queue spillover into 2026. Coordination projects such as CISA’s Joint Cyber Defense Collaborative are expected to widen civilian use cases, but progress hinges on workforce onboarding and budget adjudication.

Asia-Pacific outruns every other region at 12.16% CAGR as military-modernization budgets accelerate. Australia’s Integrated Investment Program earmarked AUD 330 billion (USD 220 billion) through 2034, explicitly listing cross-domain hardware for naval radar networks. Japan’s JPY 128 billion (USD 870 million) allocation covers gateway co-development with United States allies, while India’s tri-service Defence Communication Network uses domestic vendors to align with self-reliance mandates. South Korea’s KRW 315.2 trillion (USD 235 billion) Defense Reform 2.0 embeds guards into missile-defense nodes, pushing local integrators to achieve NSA and NATO parity certifications. Although China’s Military-Civil Fusion program lacks transparency, regional procurement data indicates home-grown guard deployments within strategic support units, foreshadowing stronger indigenous competition.

Europe, Middle East, and Africa collectively contribute roughly 35% of global revenue. Europe’s Permanent Structured Cooperation initiative bankrolled 60 digital defense projects by 2025, accelerating gateway adoption in multinational formations. The United Kingdom allocated GBP 800 million (USD 1.0 billion) for multi-level security infrastructure underpinning the Tempest fighter program, and Germany awarded EUR 95 million (USD 103 million) to Rohde and Schwarz for BSI-compliant guards. Middle East modernization programs blend defense-localization goals with cyber-sovereignty, illustrated by Saudi Arabia’s SAMI-Thales joint venture for domestic data-diode production. South American adoption remains niche outside Brazil, where Embraer integrated guards into Link-BR2 tactical data links, signalling early but material interest.

Competitive Landscape

The Cross-Domain Solution market features a moderate concentration profile: BAE Systems, Lockheed Martin, General Dynamics, Forcepoint, and Owl Cyber Defense capture an estimated 55% share. BAE Systems deepened its moat by absorbing Bohemia Interactive Simulations, seeding secure synthetic environments that demand embedded cross-domain pipelines. Lockheed Martin cross-sells guards inside end-to-end command-and-control suites, leveraging trust accrued over decades of prime contracting. Owl Cyber Defense cultivates credibility with hardware-enforced one-way diodes that resonate in critical-infrastructure risk assessments, winning sizable multi-utility deals in late 2025.

Second-tier specialists thrive by attacking certification velocity and edge form-factor pain points. Waterfall Security focuses on industrial niches where bidirectional flow is prohibited, while Advenica rides its freshly minted NATO SDIP badge to penetrate European ministries. Patent filings hint at looming disruption from Cisco Systems, whose intent-based networking patents could automate classification labelling, squeezing the professional-services revenue pool. Still, the high cost and 18-24-month runway of Common Criteria evaluations discourage aggressive start-up entry, anchoring incumbent market positions.

White-space prospects circle unmanned platforms and soldier-borne devices where size, weight, and power are at a premium. The U.S. Army’s Integrated Visual Augmentation System, for example, necessitates sub-2 kg form factors, forcing miniaturization leaps. Vendors able to containerize guards into virtual network functions gain cloud marketplace traction, pulling subscription fees that diversify margin mixes. Certification bottlenecks remain the largest gating factor, so integrators investing in automated evidence-generation pipelines stand to truncate time-to-market and clinch first-mover advantage.

Cross-Domain Solution Industry Leaders

BAE Systems plc

Lockheed Martin Corporation

General Dynamics Corporation

Forcepoint LLC

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Waterfall Security Solutions received Common Criteria EAL4+ certification for its Unidirectional Security Gateway.

- January 2025: Thales Group partnered with Google Cloud to develop quantum-resistant security solutions for government and enterprise customers.

- December 2024: Everfox announced a strategic partnership with Palantir Technologies to integrate cross-domain data-analytics capabilities.

- January 2024: Saab AB teamed with Maxar Technologies to build secure satellite-communication solutions for defense customers.

Global Cross-Domain Solution Market Report Scope

The Cross-Domain Solution Market Report is Segmented by Component (Hardware, Software, Services), Solution Type (Access Solutions, Transfer Solutions, Multi-Level Solutions), Deployment (Cloud, On-Premises, Hybrid), End-User (Aerospace and Defense, Law-Enforcement and Security Agencies, Critical Infrastructure Operators, Government Civilian Agencies), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Access Solutions |

| Transfer Solutions |

| Multi-Level Solutions |

| Cloud |

| On-Premises |

| Hybrid |

| Aerospace and Defense |

| Law-Enforcement and Security Agencies |

| Critical Infrastructure Operators |

| Government Civilian Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Solution Type | Access Solutions | |

| Transfer Solutions | ||

| Multi-Level Solutions | ||

| By Deployment | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By End-User | Aerospace and Defense | |

| Law-Enforcement and Security Agencies | ||

| Critical Infrastructure Operators | ||

| Government Civilian Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is spending on cross-domain guards in Asia-Pacific expected to grow through 2031?

Asia-Pacific spending is projected to rise at a 12.16% CAGR as Australia, Japan, India, and South Korea modernize joint command networks.

Which component earns the steepest growth rate between 2026 and 2031?

Services outpace all other components with an 11.84% CAGR because agencies now value integration, continuous compliance, and managed monitoring.

Why are Multi-Level Solutions gaining momentum over Transfer Solutions?

Multi-Level architectures support mixed-clearance user groups and align with zero-trust mandates, driving them to the fastest 12.22% CAGR among solution types.

What drives cloud deployment of cross-domain solutions despite air-gap preferences?

FedRAMP High Plus accreditation for secret workloads and hyperscale cost efficiencies push cloud deployments to a 12.55% CAGR, even as mission-critical assets stay on-premises.

What is the primary headwind slowing new product launches?

Certification cycles across NSA, NATO, and national agencies can exceed 36 months and absorb over 20% of R&D budgets, delaying time-to-market.

Which end-user segment is expanding most rapidly outside traditional defense?

Critical Infrastructure Operators lead non-defense growth at an 11.98% CAGR due to regulatory mandates in pipeline, rail, and electric utility sectors.

Page last updated on: