Indonesia Communication Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

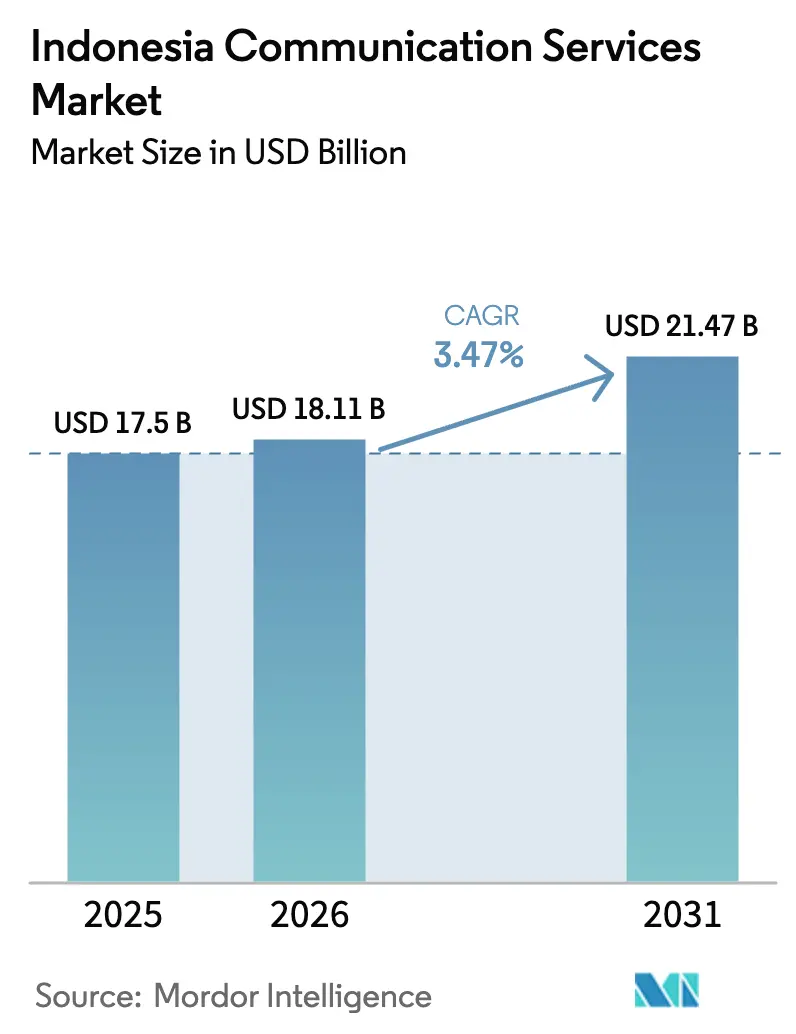

| Base Year Market Size (2025) | USD 17.5 Billion |

| Market Size (2026) | USD 18.11 Billion |

| Market Size (2031) | USD 21.47 Billion |

| Growth Rate (2026 - 2031) | 3.47% CAGR |

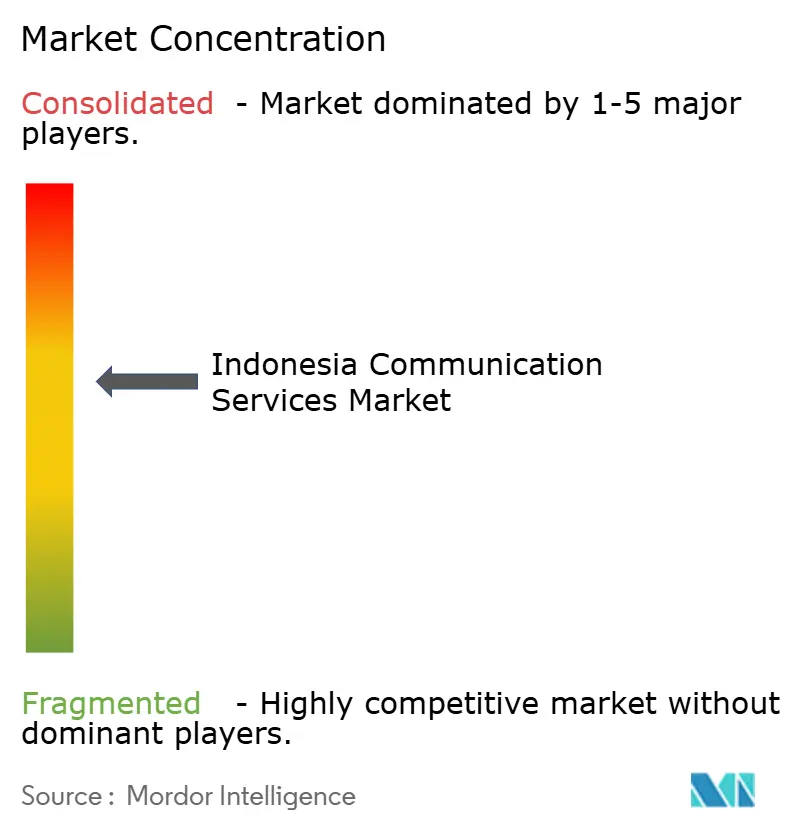

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Communication Services Market Analysis by Mordor Intelligence

The Indonesian Communication Services Market size is expected to grow from USD 17.5 billion in 2025 to USD 18.11 billion in 2026 and is forecast to reach USD 21.47 billion by 2031 at 3.47% CAGR over 2026-2031. Consolidation is accelerating after the USD 6.5 billion XL Axiata-Smartfren merger combined 94.5 million subscribers and redirected USD 300 million to USD 400 million in annual synergies to 5G densification and enterprise cloud bundles. Mobile data contributed 44.79% of 2024 service revenue, while IT-managed and cloud services are expanding at a rate of 6.14% annually, as operators shift away from pure connectivity. Government programs added 6,672 base transceiver stations in 3T regions by December 2024, narrowing the rural coverage gap, even as the average revenue per user (ARPU) outside Java remains 40% lower than the urban average. Tower sharing, which now covers more than 95% of cell sites, lowers per-site capital expenditure by up to 50% and frees up cash for spectrum and software-defined networking.

Key Report Takeaways

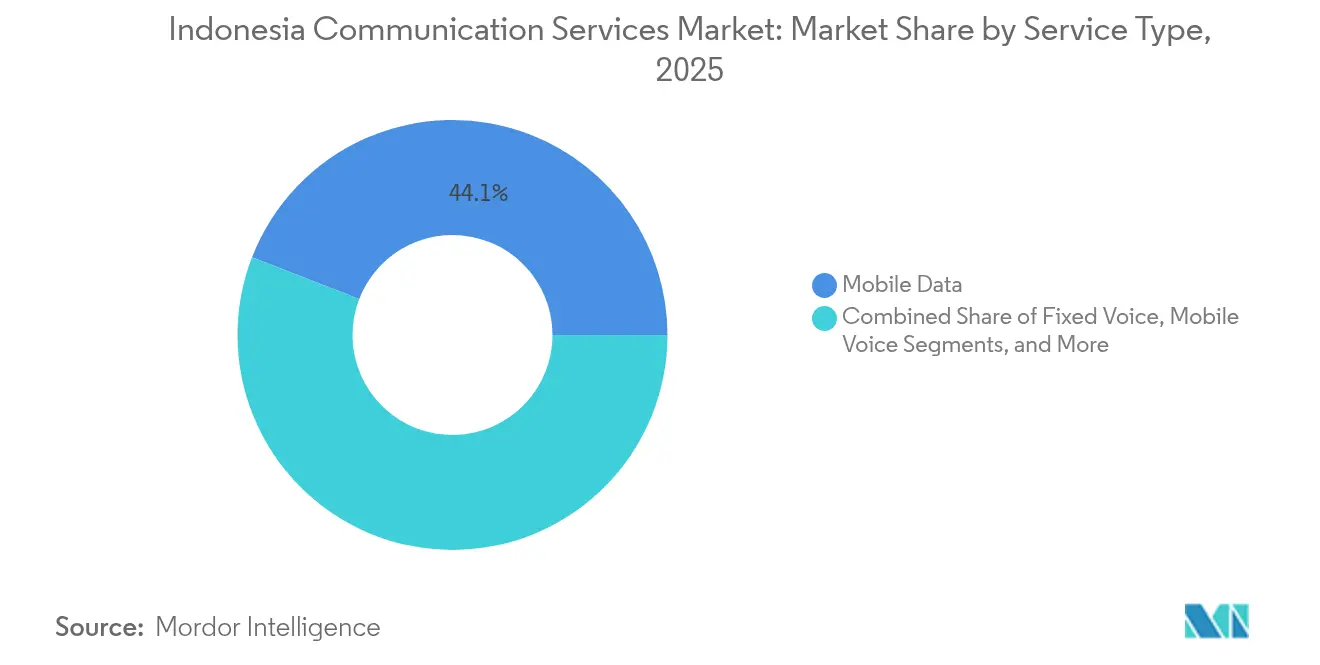

- By service type, mobile data held 44.12% revenue share in the Indonesian communication services market 2025, while IT-managed and cloud services are forecast to expand at a 6.05% CAGR through 2031.

- By connectivity technology, 4G/LTE commanded 51.74% of the Indonesian communication services market share in 2025, whereas 5G NR is projected to grow at a 6.87% CAGR to 2031.

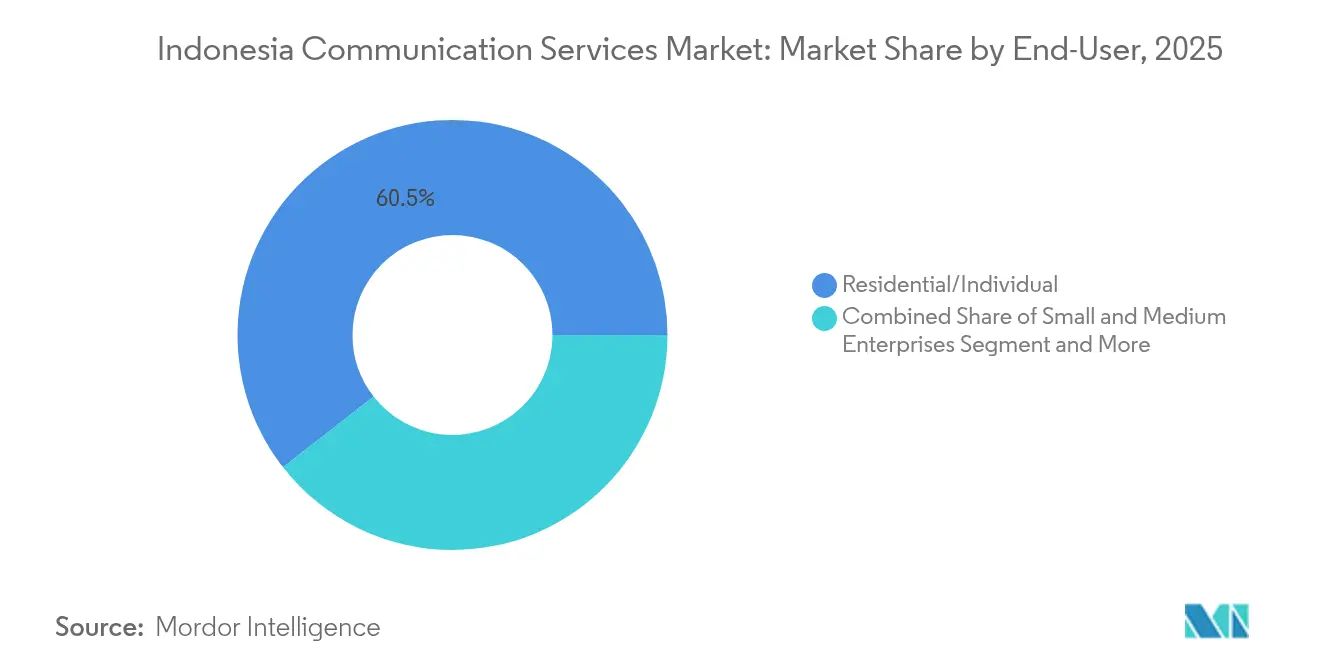

- By end-user, residential and individual subscribers generated 60.55% of 2025 revenue; small and medium enterprises are advancing at a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Communication Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile–Data Traffic Boom Post-5G Launch | +0.9% | National, with concentration in Java, Bali, and Sumatra urban corridors | Medium term (2-4 years) |

| Growing SME Digitization Demand for Bundled Cloud–Connectivity | +0.7% | Java dominance, expanding to Sumatra and Kalimantan industrial zones | Medium term (2-4 years) |

| Government “Indonesia Digital 2025” Broadband Targets | +0.6% | National, prioritizing 3T regions in Papua, Maluku, and eastern Kalimantan | Long term (≥4 years) |

| Tower-Sharing Economics Lowering Service Costs | +0.5% | National, accelerating deployment in Sulawesi and Nusa Tenggara | Short term (≤2 years) |

| Sub-1 GHz Spectrum Refarming for Rural Coverage | +0.4% | 3T regions, eastern Indonesia islands, remote Sumatra highlands | Long term (≥4 years) |

| Rising Demand from Submarine-Cable Back-Haul Consortia | +0.3% | Coastal hubs in Java, Sumatra, Sulawesi; international gateway concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mobile–Data Traffic Boom Post-5G Launch

Monthly data usage increased from 13 GB in early 2024 to 15 GB by year-end and is expected to reach 25-59 GB by 2028 as 5G device penetration surpasses 20%. [1]Indonesia Mobile Market Data, GSMA Intelligence, gsmaintelligence.com Telkomsel’s standalone 5G network at Tanjung Priok seaport enables real-time container tracking, which cuts dwell time by 18%, proving its enterprise value before mass consumer adoption. Indosat Ooredoo Hutchison and XL Axiata activated 5G in Jakarta, Surabaya, and Bandung, achieving 26% population coverage by December 2024, yet hitting the 32% 2030 target demands faster spectrum refarming. [2]Indonesia Targets 32% 5G Coverage by 2030, OpenGov Asia, opengovasia.com Video streaming and gaming generate 65% of peak traffic, prompting network slicing and edge nodes to protect user experience without proportional backhaul spend. Monetization is gradually shifting from volume pricing to tiered service-level agreements that bundle latency and reliability guarantees.

Growing SME Digitization Demand for Bundled Cloud-Connectivity

Indonesia’s 64.2 million SMEs, which employ 97% of the labor force, accelerated cloud adoption in 2024 as e-commerce and e-payment regulations made always-on connectivity essential. Telkom Indonesia’s IndiHome-Microsoft 365-cybersecurity bundle, priced at IDR 500,000 (USD 32) per month, captured 120,000 SME subscribers in six months, showing 30% ARPU uplift versus connectivity alone. Indosat is linked with Amazon Web Services to sell virtual private clouds with guaranteed uplinks to West Java manufacturers that need real-time inventory synchronization. A talent pool of fewer than 8,000 certified cloud-security specialists inflates operating costs 15-20% and underpins demand for managed services. Despite 8-12% managed-service margins, lifetime value triples that of pure connectivity, solidifying SME digitization as a strategic thrust.

Government “Indonesia Digital 2025” Broadband Targets

The Ministry of Communication and Informatics allocated universal-service funds to deploy 6,672 base stations in 3T regions by December 2024, thereby increasing national population coverage to 96%. [3]Universal Service Obligation Program, Ministry of Communication and Informatics, kominfo.go.id The 100 Gbps-upgraded Palapa Ring backbone now touches 440 regencies, yet municipal right-of-way fees add 10-15% to construction costs, slowing last-mile builds. Starlink pilot links in Bali and the Aru Islands show 150 Mbps download speeds for rural clinics, illustrating satellite as a temporary solution for fiber gaps. The USD 860 million Satria-2 satellite, launching in 2027 with a 300 Gbps capacity, will prioritize eastern provinces where terrestrial backhaul remains uneconomical. Coverage obligations embedded in operating licenses ensure continued investment, even when near-term returns are limited.

Tower-Sharing Economics Lowering Service Costs

Independent tower firms Mitratel, Tower Bersama, and Protelindo manage more than 70,000 sites, enabling tenants to reduce per-site capex by 40-50% compared to single-tenant builds. The XL Axiata–Smartfren merger plans to retire 15% of duplicate towers and redirect USD 120 million annually into 5G densification. Regulation DGPPI 6/2024 now mandates sharing for new 5G sites, compressing differentiation on physical build-outs and shifting rivalry toward spectrum and software. Tower companies are retrofitting urban poles with micro-data centers that keep latency under 10 ms, opening new colocation income streams. CPI-linked lease escalators preserve tower margins while providing operators with elastic capacity to adapt to unpredictable traffic patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Spectrum-Auction Reserve Prices | -0.6% | Nationwide, small-operator impact | Short term (≤2 years) |

| Persistent Rural ARPU Gap | -0.5% | 3T regions Papua, Maluku, Kalimantan, Sumatra | Long term (≥4 years) |

| Municipal Fiber-Right-of-Way Delays | -0.4% | Tier-two and tier-three cities | Medium term (2-4 years) |

| Shortage of Cloud-Security Specialists Inflating OPEX | -0.3% | National, Java and Bali hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Spectrum-Auction Reserve Prices

Mid-band reserve prices topping USD 0.50 per MHz-pop deterred smaller bidders and pushed back the planned 3.5 GHz sale, squeezing operator budgets needed for rural coverage. The big three already hold more than 80% of sub-6 GHz spectrum, limiting the entry of newcomers that could spur price competition. Spectrum spend absorbs 12–15% of capex, and high reserves weaken the rural business case where density falls below 50 users per km². The ministry is piloting the dynamic sharing of underutilized government bands, yet the interference rules remain incomplete. Until reserve levels drop, 5G expansion outside Java risks slowing.

Persistent Rural ARPU Gap

ARPU in Papua and Maluku averages USD 2.50-3.00 versus USD 5.00-6.00 in Jakarta, a 40% gap driven by lower income and prepaid voice-centric usage. Although 6,672 universal-service base stations pushed coverage above 96%, traffic per rural cell is still 60% below the national mean, keeping opex coverage challenging. Satellite backhaul can cost USD 800-1,200 monthly per site, eroding margins further. Starlink pricing of around USD 100 a month suits clinics and enterprises, but remains unaffordable for households. Satria-2 will reduce backhaul costs by 30-40% after 2027; however, a meaningful ARPU uplift hinges on broader economic development in the 3T regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Integration Reshapes Revenue Mix

IT-managed and cloud services are growing at a rate of 6.05% annually, outpacing every other line of business as enterprises adopt hybrid architectures that combine private links with public-cloud workloads. Mobile data still accounts for 44.12% of revenue, yet falling revenue per gigabyte forces operators to upsell security and software bundles. Telkom Indonesia’s bundled offer added 120,000 SME customers within six months, demonstrating that integrated packages increase ARPU by 30%. Fixed voice slipped into a single-digit share while fixed broadband stabilizes in the mid-teens, fueled by IndiHome’s urban fiber and pilots of Nokia’s FastMile fixed-wireless access that bypass long permit queues. The Indonesian communication services market size for cloud-centric solutions is expected to accelerate as operators transition from being pipe-centric to platform-centric.

Operators are countering the cloud-security talent shortage, which has fewer than 8,000 certified professionals nationwide, by embedding managed detection and response into connectivity contracts, thereby securing margins at even 8-12% levels. Indosat’s AWS tie-up provides pre-configured virtual private clouds to West Java manufacturers that require sub-second ERP replication, underscoring the emerging vertical playbooks. XL Axiata’s managed SD-WAN reached 450 enterprise sign-ups within one quarter, aided by a 20% price discount to DIY procurement. As commoditization squeezes simple connectivity, the Indonesian communication services industry is monetizing integration expertise.

By Connectivity Technology: 5G Acceleration Meets 4G Maturity

4G/LTE still accounts for 51.74% of the Indonesian communication services market share, thanks to 96% population coverage, but 5G NR is accelerating with a 6.87% CAGR to satisfy the 32% coverage mandate by 2030. Telkomsel’s 5G standalone node at Tanjung Priok cut container dwell times by 18%, validating industrial use cases before consumer streaming overloads capacity. Indosat’s Nokia contract combines 4G upgrades with new 5G gear across three islands, maximizing tower-lease ROI. The Indonesian communication services market size tied to 5G is expanding as XL Axiata and Smartfren redeploy overlapping 4G spectrum and funnel USD 300 million into densifying Jakarta and Surabaya. Open RAN feasibility work, led by NEC and Japan, could reduce equipment outlays by 20–30%, broadening vendor choice.

Fiber-to-the-home penetration remains under 15% nationwide because 514 local governments control permits that can add 12–18 months to the build process. Satellite and VSAT bridge the gap in Papua and Maluku, where Starlink’s early deployments have clocked speeds of 150 Mbps for clinics. Satria-2 will deliver 300 Gbps of Ka-band capacity in 2027, reducing backhaul costs by 30-40% and creating headroom for fiber extensions. The technology mix shows a measured shift toward software-driven, spectrum-efficient architectures.

By End-User: SME Growth Outpaces Residential Maturity

SMEs are expanding at 5.24% annually, faster than residential segments that already exceed 130% mobile penetration and suffer ARPU stagnation under USD 5. IndiHome’s SME bundle achieved a 30% ARPU lift over connectivity-only contracts and reached 120,000 lines in just half a year. Indosat’s AWS partnership sells guaranteed-uplink virtual clouds to manufacturers in Karawang and Bekasi, securing long-term revenue. Large enterprises and government agencies value dedicated capacity and SLAs, yielding margins above 20% but requiring 12-18 month sales cycles.

Residential demand is primarily driven by video and social media, accounting for 65% of peak load. However, unlimited plans reduced unit pricing by 12% in 2024, negatively impacting margins. Rural ARPU remains 40% below that of Java, despite 96% population coverage, which delays fiber-to-the-home deployment in low-density areas. XL Axiata’s managed SD-WAN, offering last-mile plus 24/7 NOC, attracted 450 multi-site retailers in its first quarter. The Indonesian communication services market size attributed to SMEs will therefore grow faster than the saturated household base, as digital commerce mandates always-on, secure links.

Geography Analysis

Java generated 55-60% of 2025 revenue, primarily due to dense populations and fiber penetration rates of nearly 20% in Jakarta and Surabaya. Telkomsel secures more than 60% of the fixed-broadband share on the island through IndiHome bundles, while the XL Axiata-Smartfren union is funneling USD 300 million in synergy savings into 5G densification across Java’s top cities. Indosat’s Huawei core upgrade achieved sub-20 ms latency for 100 million users in Greater Jakarta, solidifying the quality of mobile gaming. The upcoming Nusantara capital in East Kalimantan opens a greenfield chance to install software-defined networks from scratch.

Sumatra contributes roughly 18-20% of revenue, with 90% 4G coverage in Medan and Palembang, but a sub-10% fiber penetration rate, making fixed-wireless access via Nokia FastMile an attractive option. Kalimantan, Sulawesi, and Bali collectively account for 15-18% of turnover; Bali’s tourism sector drives smartphone penetration above 80%, whereas Kalimantan’s mines require private LTE for remote sites. The Palapa Ring 100 Gbps uplift links 440 regencies, but municipal fees inflate extension costs 10-15%. Starlink trials in Bali clinics confirmed satellite as a viable stopgap at 150 Mbps. Papua and Maluku account for less than 5% of the revenue, despite covering 22% of the landmass, with an ARPU 40% below that of Java and a density of under 10 persons per km². Universal-service deployments increased population coverage to 96%, yet traffic per tower remains 60% lighter than the national average. Satria-2’s 2027 launch will reduce site backhaul costs by 30-40%, improving fiber economics. Nusa Tenggara stays at sub-8% fixed-broadband penetration, leaning on 4G fixed-wireless access that incurs USD 800-1,200 monthly satellite backhaul fees. Makassar’s emerging edge-data center cluster is positioning Sulawesi as the low-latency gateway for content delivery in eastern Indonesia.

Competitive Landscape

The Indonesian communication services market, following the merger, is a triopoly in the mobile arena, comprising Telkomsel, Indosat, and XL Axiata-Smartfren. This is steering rivalry toward 5G quality, cloud bundles, and device financing rather than headline tariffs. Fixed broadband is less consolidated, with IndiHome’s 60% Java share challenged by Biznet, MyRepublic, First Media, and CBN Fiber that undercut long-term contracts by up to 20%. Independent tower ownership above 95% levels compresses capex advantages, shifting focus to spectrum holdings and software automation.

Emerging disruptor Starlink received its Indonesian license in May 2024 and offers 150 Mbps satellite internet at USD 100 per month, serving government clinics and enterprises rather than mass households. Hyperscalers, including AWS, Microsoft Azure, and Google Cloud, added Jakarta data centers in 2024 and sell direct-connect links, creating coopetition with telcos. A Japan-Indonesia Open RAN study seeks to trim 5G gear costs by 20-30%, potentially lowering rural build prices. Indosat’s patent-pending AI algorithm reallocates spectrum in real-time, cutting congestion without the need for extra radios, exemplifying the pivot from iron to intelligence.

White-space prospects include enterprise cloud integration, which is currently constrained by the 8,000-person cloud-security talent pool. Eastern Indonesia remains under-connected but will benefit once Satria-2 lowers backhaul costs. Vertical integration surfaces as Telkomsel bundles fixed and mobile services, while horizontal alliances, such as Indosat-AWS, combine network reach with global cloud scale.

Indonesia Communication Services Industry Leaders

Telkomsel (PT Telekomunikasi Selular)

Indosat Ooredoo Hutchison Tbk

PT XLSMART Telecom Sejahtera Tbk (XLSMART)

Biznet Networks (PT. Supra Primatama Nusantara)

CBN Fiber

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: XL Axiata and Smartfren closed their USD 6.5 billion merger, pooling 94.5 million subscribers and targeting 40% 5G population coverage by 2027.

- December 2024: Nokia landed a multi-year deal with Indosat to deploy AirScale RAN and FastMile FWA across Java, Sumatra, and Bali.

- August 2024: Indosat Ooredoo Hutchison and Huawei finished a 26-site cloud-native core upgrade delivering sub-20 ms latency to 100 million users.

- August 2024: Telkomsel activated Indonesia’s first 5G standalone network at Jakarta’s Tanjung Priok port, reducing container dwell time by 18%.

Indonesia Communication Services Market Report Scope

The Indonesia Communication Services Market Report is Segmented by Service Type (Fixed Voice, Fixed Data/Broadband, Mobile Voice, Mobile Data, IT-Managed and Cloud Services), Connectivity Technology (Fiber-To-The-Home [FTTH], 4G/LTE, 5G NR, Satellite and VSAT), and End-User (Residential/Individual, Small and Medium Enterprises, Large Enterprise and Government). The Market Forecasts are Provided in Terms of Value (USD).

| Fixed Voice |

| Fixed Data/Broadband |

| Mobile Voice |

| Mobile Data |

| IT-Managed and Cloud Services |

| Fiber-to-the-Home (FTTH) |

| 4G/LTE |

| 5G NR |

| Satellite and VSAT |

| Residential/Individual |

| Small and Medium Enterprises |

| Large Enterprise and Government |

| By Service Type | Fixed Voice |

| Fixed Data/Broadband | |

| Mobile Voice | |

| Mobile Data | |

| IT-Managed and Cloud Services | |

| By Connectivity Technology | Fiber-to-the-Home (FTTH) |

| 4G/LTE | |

| 5G NR | |

| Satellite and VSAT | |

| By End-User | Residential/Individual |

| Small and Medium Enterprises | |

| Large Enterprise and Government |

Key Questions Answered in the Report

What is the projected value of the Indonesia communication services market in 2031?

The market is expected to reach USD 21.47 billion by 2031.

How fast is the shift from 4G to 5G happening in Indonesia?

5G NR is growing at a 6.87% CAGR and aims for 32% population coverage by 2030.

Which service type is expanding the quickest among Indonesian telecom operators?

IT-managed and cloud services are advancing at 6.05% per year through 2031.

Why are SMEs strategic for Indonesian telcos?

Bundled connectivity-plus-cloud packages lift SME ARPU by about 30% and triple lifetime value compared with connectivity alone.

How will the Satria-2 satellite affect eastern Indonesia connectivity?

When operational in 2027, Satria-2 is expected to cut rural backhaul costs by up to 40%, improving the economics of fiber and 5G rollouts.

What role do independent tower companies play in Indonesia?

They own more than 95% of macro-cell infrastructure, lowering per-site capex for operators by up to 50% and accelerating nationwide 5G deployment.

Page last updated on: