Indonesia Artificial Intelligence (AI) Optimised Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

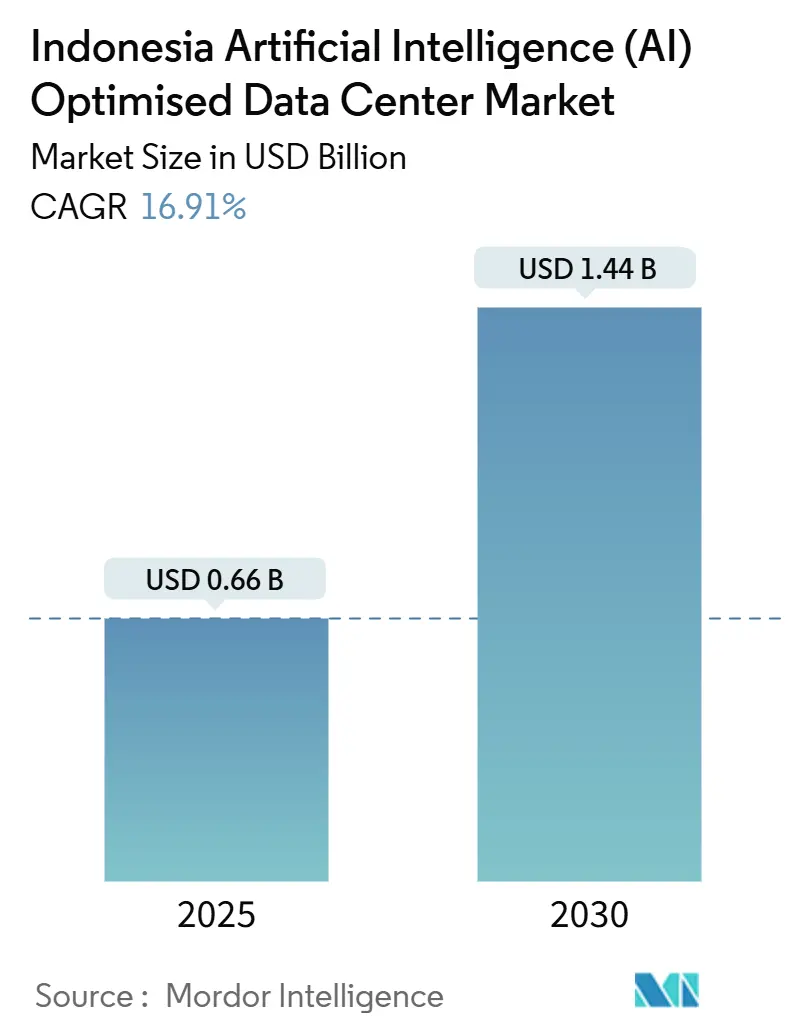

| Market Size (2025) | USD 0.66 Billion |

| Market Size (2030) | USD 1.44 Billion |

| Growth Rate (2025 - 2030) | 16.91% CAGR |

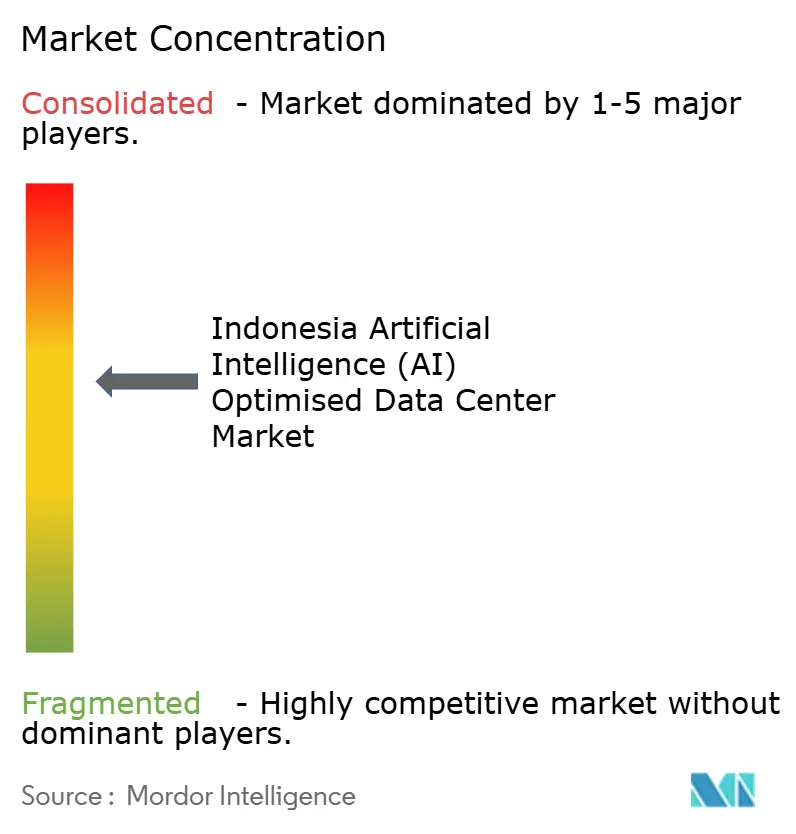

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Artificial Intelligence (AI) Optimised Data Center Market Analysis by Mordor Intelligence

The Indonesia Artificial Intelligence Data Center market size reached USD 0.66 billion in 2025 and is forecast to climb to USD 1.44 billion by 2030, advancing at a 16.91% CAGR. Strong sovereign AI policies, hyperscaler capital inflows, and strict data-localization rules combine to keep the Indonesia Artificial Intelligence Data Center market on a steep growth curve. Investment announcements from Microsoft, Sinarmas, and other players show confidence in local regulations, while the “Making Indonesia 4.0” roadmap pushes manufacturers, banks, and hospitals to shift workloads into domestic AI-ready facilities. Rapid 5G rollout and surging mobile data usage raise demand for low-latency processing. Competitive pressure is building as foreign cloud operators join local champions, yet persistent grid challenges favor operators able to secure their own resilient power and cooling. The mix of opportunity and constraint is setting the stage for accelerated consolidation during the outlook period.

Key Report Takeaways

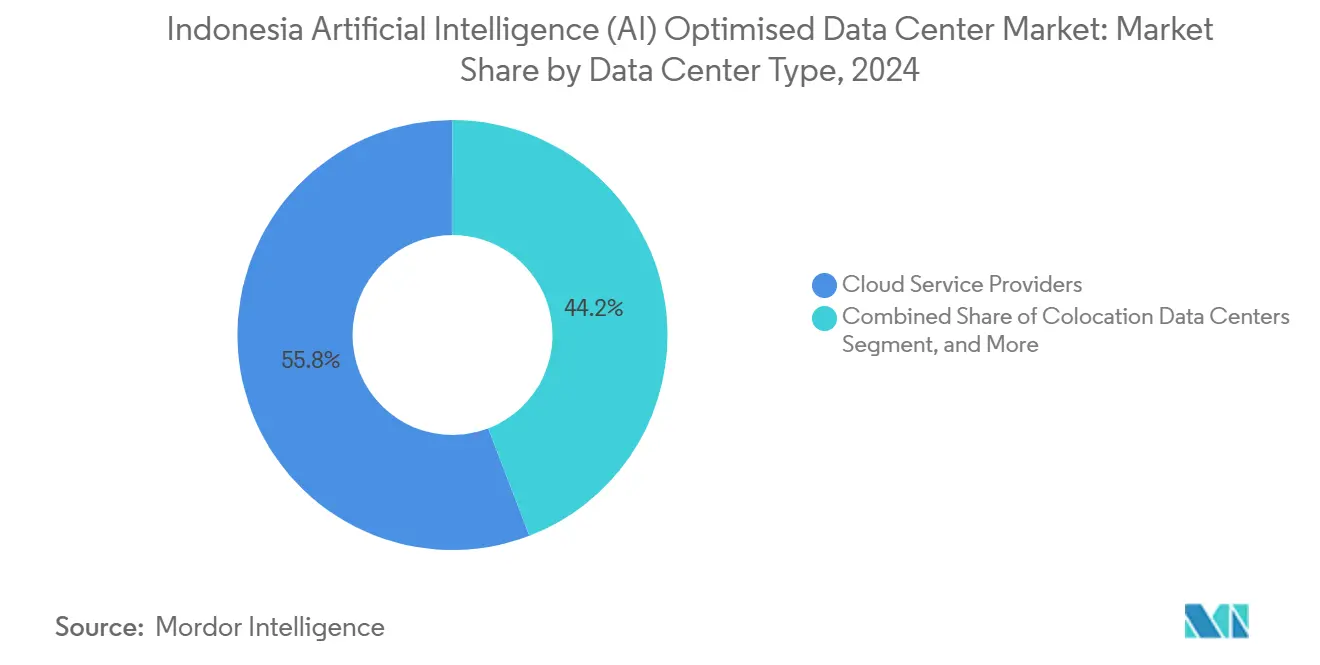

- By data-center type, Cloud Service Providers led with 55.82% of the Indonesia Artificial Intelligence Data Center market share in 2024, and colocation data centers are projected to post the highest 18.08% CAGR to 2030.

- By component, software held 45.83% share of the Indonesia Artificial Intelligence Data Center market size in 2024, and hardware is projected to post the highest 17.53% CAGR to 2030.

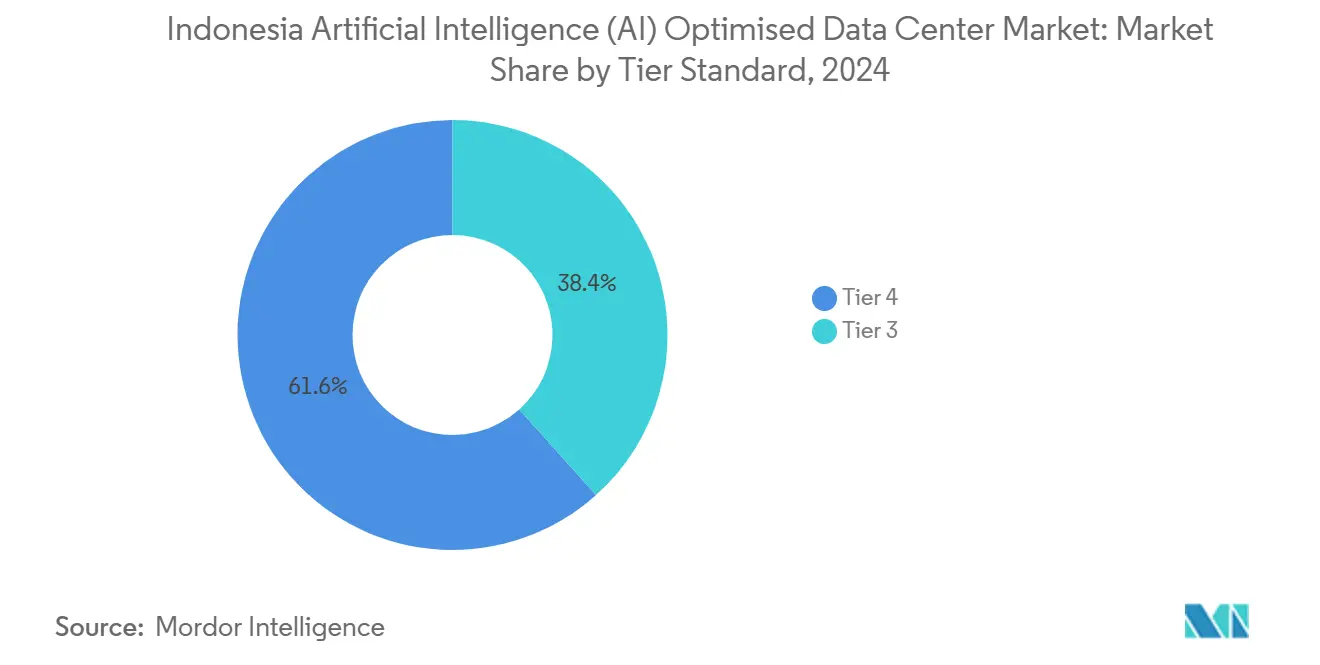

- By tier, Tier 4 held 61.63% share of the Indonesia Artificial Intelligence Data Center market size in 2024, and Tier III facilities are forecast to expand at 18.77% CAGR through 2030.

- By end-user industry, IT and ITES held 33.82% share of the Indonesia Artificial Intelligence Data Center market size in 2024, and internet and digital media workloads are advancing at the fastest 17.56% CAGR to 2030.

Competitive positioning in Indonesia includes both locally based firms and those operating across multiple regions. The market landscape in the global artificial intelligence (ai) data center industry research shows how these players are arranged internationally.

Indonesia Artificial Intelligence (AI) Optimised Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foreign direct hyperscale investments accelerate build-outs | +8.5% | Jakarta, Batam, tier-2 cities | Medium term (2-4 years) |

| Exploding mobile-first cloud usage fuels capacity demand | +7.2% | National, Java, Sumatra | Short term (≤ 2 years) |

| “Making Indonesia 4.0” policy incentivizes AI workloads | +6.8% | National | Long term (≥ 4 years) |

| Sub-sea cable landings enable low-latency AI fabrics | +4.1% | Jakarta, Batam, Surabaya | Medium term (2-4 years) |

| Data-localization mandate spurs local AI footprint | +5.9% | National | Short term (≤ 2 years) |

| Fintech and e-commerce edge nodes in tier-2 cities | +3.8% | Bandung, Yogyakarta, Medan, Makassar, Surabaya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Foreign Direct Hyperscale Investments Accelerate Build-outs

Every hyperscaler commitment sparks parallel spending on power lines, fiber, and skilled labor. Microsoft’s USD 1.7 billion pledge triggered vendor alliances and workforce programs that shorten build cycles.[1]Microsoft Indonesia, “Transforming Indonesian Businesses for an AI-Powered Future,” microsoft.com Similar moves by Korean and Singaporean investors broaden the Indonesia Artificial Intelligence Data Center market beyond Jakarta, with Batam emerging as a low-latency overflow site. Nvidia’s USD 200 million venture in Solo signals that foreign capital now targets secondary cities where land is cheaper and demand is rising. These flows help Indonesia capture a larger share of Southeast Asian AI infrastructure spending than its digital economy size alone would imply.

Exploding Mobile-First Cloud Usage Fuels Capacity Demand

Smartphone penetration and social-media adoption are reshaping traffic patterns. Heavy video streaming and real-time commerce drive operators to deploy edge racks nearer to users to avoid backhaul delays.[2]Grahanusa Mediatama, “Perkembangan Ekonomi Stabil, Ekspansi Data Center Indonesia Ikut Tumbuh,” kontan.co.id Enterprises therefore look for facilities in Bandung, Yogyakarta, and Medan that pair high-density GPU clusters with carrier-neutral interconnection. Telkom’s plan to boost capacity from 42 MW to 400 MW rests mainly on this mobile-driven requirement. The surge in user traffic has already lifted enterprise inquiries for rack space, confirming that mobile culture is a direct catalyst for new AI-ready builds.

"Making Indonesia 4.0” Policy Incentivizes AI Workloads

Tax breaks, fast permitting, and sector-specific AI programs combine to push manufacturers, banks, and public agencies to upgrade local compute. The national AI strategy defines roadmaps through 2045, giving operators a clear demand horizon. Production plants now specify on-premises inferencing for quality control, and banks expand conversational AI tied to compliance rules. Because the policy favors domestic hosting, operators that guarantee data residency gain a winning edge. The multi-decade scope of the initiative keeps the Indonesia Artificial Intelligence Data Center market on a visible expansion path, enabling long-tenor financing.

Sub-Sea Cable Landings Enable Low-Latency AI Fabrics

New Singapore-Batam and Bifrost cables slash transit times and widen international bandwidth. Landing sites near Jakarta and Batam now support 480 Tbps capacity, making these zones attractive for distributed AI training that taps global datasets. Redundant routes lower the risk of outages and justify premium colocation rates. Operators that cluster around cable landing stations can promote single-digit-millisecond latency to Singapore and onward to global cloud nodes, a critical selling point for real-time inference workloads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of AI-ready engineering talent | −4.2% | National, acute in tier-2 cities | Long term (≥ 4 years) |

| High power and cooling OPEX pressures margins | −3.8% | Jakarta and major hubs | Short term (≤ 2 years) |

| Grid instability across islands threatens uptime | −5.1% | Eastern Indonesia, rural Java, Sumatra | Medium term (2-4 years) |

| Water-stress limits liquid-cooling expansion | −2.9% | Jakarta, Surabaya, industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of AI-Ready Engineering Talent

Graduates skilled in GPU orchestration, model training, and data-center automation remain too few for the pace of build-outs. Operators pay premium wages or fly in foreign staff, eroding EBITDA margins. The gap is widest in secondary cities where universities focus on general IT. Government scholarships and vendor boot camps are growing, but most programs will not release enough specialists before 2028. Until then, staffing limits could stall commissioning schedules, especially for facilities that promise rapid ramp-ups to hyperscaler clients.

High Power and Cooling OPEX Pressures Margins

AI racks draw 3-5 times more power than typical enterprise loads. Jakarta’s industrial tariffs stay above regional peers, pushing operators to negotiate long-term deals or invest in on-site generation. Liquid cooling beats air systems for dense GPU farms yet raises capital and water bills.[3]Alan Smith and Vamsi Alla, “AMD Instinct MI300X Accelerator,” hc2024.hotchips.org These costs tighten the payback window and may deter smaller entrants without scale economics. Early movers with renewable power contracts or waste-heat reuse technologies hold a clear cost advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Providers Lead, Colocation Surges

Cloud Service Providers held 55.82% of the Indonesia Artificial Intelligence Data Center market share in 2024, benefiting from early hyperscale campuses and enterprise SaaS migration. Growing foreign investment keeps their footprint large, yet the Indonesia Artificial Intelligence Data Center market size shows a pivot toward colocation, forecast at 18.08% CAGR to 2030. Enterprises want mix-and-match setups that pair owned GPU clusters with on-demand cloud scaling. This hybrid logic explains why Princeton Digital Group and EdgeConneX each plan campuses above 90 MW in Batam and Jakarta, targeting tenants that need sovereign hosting with cross-connects to global clouds.

In the second half of the decade, local operators are expected to close the gap by bundling managed AI services. DCI Indonesia markets sovereign compliance and Tier IV uptime to banks, while Telkom offers cloud adjacency and direct fiber to its mobile core network. The surge of edge nodes in tier-2 cities broadens addressable demand for smaller colocation halls optimized for regional e-commerce and fintech. As a result, hyperscale and colocation models increasingly converge, with providers offering both to secure multiyear contracts from large tenants.

By Component: Software Dominates, Hardware Accelerates

Software captured 45.83% share in 2024 because enterprises spend first on AI models, MLOps, and security layers before upgrading racks. Spending on GPUs, high-memory servers, and power gear, however, is growing at 17.53% CAGR, lifting the hardware slice of the Indonesia Artificial Intelligence Data Center market size. Computer-vision modules in manufacturing and NLP chatbots in banking represent quick-win use cases driving license revenues, yet training LLMs now demands local NVIDIA H100 clusters, pushing operators to higher density designs.

Power and cooling systems thus shift toward liquid loops and rear-door heat exchangers. Operators that integrate these features can charge premium rates and attract tenants obliged to keep data onshore. Services spending also rises, as firms lacking internal ML skills outsource cluster management and model tuning. The combined trend expands value pools beyond physical racks into full-stack AI enablement, lifting overall monetization per megawatt within the Indonesia Artificial Intelligence Data Center industry.

By Tier Standard: Tier IV Commands Trust, Tier III Gains Momentum

Risk-averse banks, health networks, and government agencies favored Tier IV, giving it a 61.63% share in 2024. Certification reassures customers that uptime meets global benchmarks, and domestic insurers often demand the same. Yet Tier III is forecast to grow 18.77% CAGR as mid-sized firms seek balanced cost and reliability, nudged by improved grid power quality in Jakarta and Batam. Operators now offer modular Tier III halls inside larger campuses, letting clients pick service levels by workload type.

Longer term, more enterprises will classify applications by resilience needs instead of defaulting to maximal redundancy. That shift frees budget for GPU hardware and software innovation. The ongoing mix change therefore broadens the Indonesia Artificial Intelligence Data Center market by adding a mid-price tier attractive to exporters, SaaS firms, and digital media platforms.

By End-User Industry: IT Rules, Digital Media Races Ahead

IT and ITES firms generated 33.82% of 2024 revenue by building, integrating, and managing AI solutions for clients. They also act as anchor tenants for new facilities, booking multi-megawatt blocks early in construction. Internet and Digital Media players, however, will post the fastest 17.56% CAGR to 2030, lifted by streaming, gaming, and creator platforms that require edge caching and GPU inference near users. Banks ramp fraud analytics and chatbots, while hospitals deploy AI imaging to serve remote islands.

Manufacturing plants roll out predictive maintenance and quality control on local clusters to avoid latency and connectivity risks inside factories. Public agencies embrace AI for tax, benefits, and permit workflows, a trend strengthened by regulations that prevent hosting citizen data abroad. The widening sector mix protects the Indonesia Artificial Intelligence Data Center market from downturns in any single vertical and supports multiyear, multi-tier demand across the value chain.

Geography Analysis

Jakarta holds most capacity because of submarine cables, government proximity, and enterprise headquarters concentration. Batam follows as a Singapore overflow site offering tax incentives and sub-10 millisecond round-trips to the island-state. Together they represent more than 70% of installed megawatts in the Indonesia Artificial Intelligence Data Center market.

Java’s industrial corridor underpins many AI workloads tied to automotive, electronics, and consumer-goods manufacturing. Sumatra presents rising needs from resource and agribusiness activities seeking predictive analytics for logistics and safety. Eastern Indonesia lags due to weaker grid stability, yet pilot edge nodes in Makassar and Balikpapan prove localized demand for public-service and mining applications.

The planned new capital, IKN Nusantara, will include a dedicated government cloud zone. Telkom has pledged initial backbone, while private operators lobby for land concessions around the site. Over the outlook horizon, improved renewable generation and fresh cable landings should let operators reduce Jakarta dependency, spreading growth to tier-2 cities and lowering latency nationwide.

Mordor Intelligence tracks the artificial intelligence (ai) data center market across other major regions such as Europe, Asia, and Middle East and Africa, with additional country-level coverage spanning Thailand, Australia, United Kingdom, South Africa, Saudi Arabia, and Mexico, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Around 68 operators contest the Indonesia Artificial Intelligence Data Center market, but scale economics are tilting power toward a handful of well-funded players. DCI Indonesia leads with 83 MW and a solid Tier IV track record. Telkom Indonesia bundles network and mobile assets to attract both government and enterprise tenants, planning to reach 400 MW by 2030. International entrants such as EdgeConneX, Princeton Digital Group, and NTT deliver hyperscale design, liquid cooling, and global cross-connects.

Mergers, joint ventures, and minority stake sales accelerate as smaller firms seek capital for GPU-ready retrofits. Korean and Singaporean funds have taken positions in local specialists to gain early exposure. Hyperscaler partnerships also reshape the field: Telkom teams with Microsoft Azure, while Indosat markets NVIDIA H100 clusters under the “GPU Merdeka” brand. Operators differentiate with energy sourcing strategies, from geothermal PPAs to on-site solar, aiming to hedge rising power tariffs.

Barriers to entry are rising as land near cables tightens and permitting gets stricter. Yet niches remain in edge hubs where local knowledge beats pure capital heft. Companies able to offer turnkey AI stacks, hardware, MLOps, plus compliance services, stand to lock in stickier contracts and fend off price-only competition.

Indonesia Artificial Intelligence (AI) Optimised Data Center Industry Leaders

DCI Indonesia

Princeton Digital Group Indonesia

ST Telemedia GDC Indonesia

Telkomsigma / NeuCentrIX

NTT Global Data Centers Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Microsoft announced plans to launch its first data center in Indonesia, named the Indonesia Central Cloud Region, by Q2 2025. This facility, under construction since 2021, will become part of Microsoft’s extensive global network of over 60 cloud regions. The data center is expected to play a pivotal role in supporting AI-driven innovations and services in Indonesia, catering to the growing demand for advanced cloud and AI solutions. Additionally, the project is anticipated to generate significant economic benefits, including the creation of over 106,000 jobs across key sectors such as manufacturing, finance, government, and communications. The initiative highlights Microsoft’s commitment to advancing cloud and AI technologies in Indonesia, aligning with its broader strategy to support digital transformation in the region.

- March 2025: LG Sinar Mas broke ground on a data center in Jakarta, Indonesia. The company is a joint venture between LG CNS, a South Korean data center service provider, and PT SMPlus Digital Investment, a digital infrastructure platform backed by Indonesian conglomerate Sinar Mas.

- February 2024: Telin and Citra Connect broke ground on a Nongsa cable landing station serving four subsea systems to boost Batam connectivity.

- December 2024: Indonesia opened talks with xAI on potential local facilities, signaling top-level ambition to host frontier model training.

Indonesia Artificial Intelligence (AI) Optimised Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, a nd forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How large is the Indonesia Artificial Intelligence Data Center market in 2025?

The market stands at USD 0.49 billion in 2025 and is projected to reach USD 1.76 billion by 2030.

What is the expected CAGR for Indonesian AI-centric data centers through 2030?

The forecast CAGR is 16.91% for the 2025-2030 period.

Which data-center type is growing fastest in Indonesia?

Colocation Data Centers are forecast to expand at 18.08% CAGR as firms adopt hybrid AI architectures.

Why are Tier III facilities gaining traction despite Tier IV dominance?

Many enterprises now balance uptime needs with cost, making Tier III an attractive middle ground that is growing at 18.77% CAGR.

How are data-localization rules affecting foreign cloud firms?

The Personal Data Protection Law forces global providers to place AI processing inside Indonesia, driving new builds and joint ventures with local operators.

Page last updated on: