South Korea AI Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

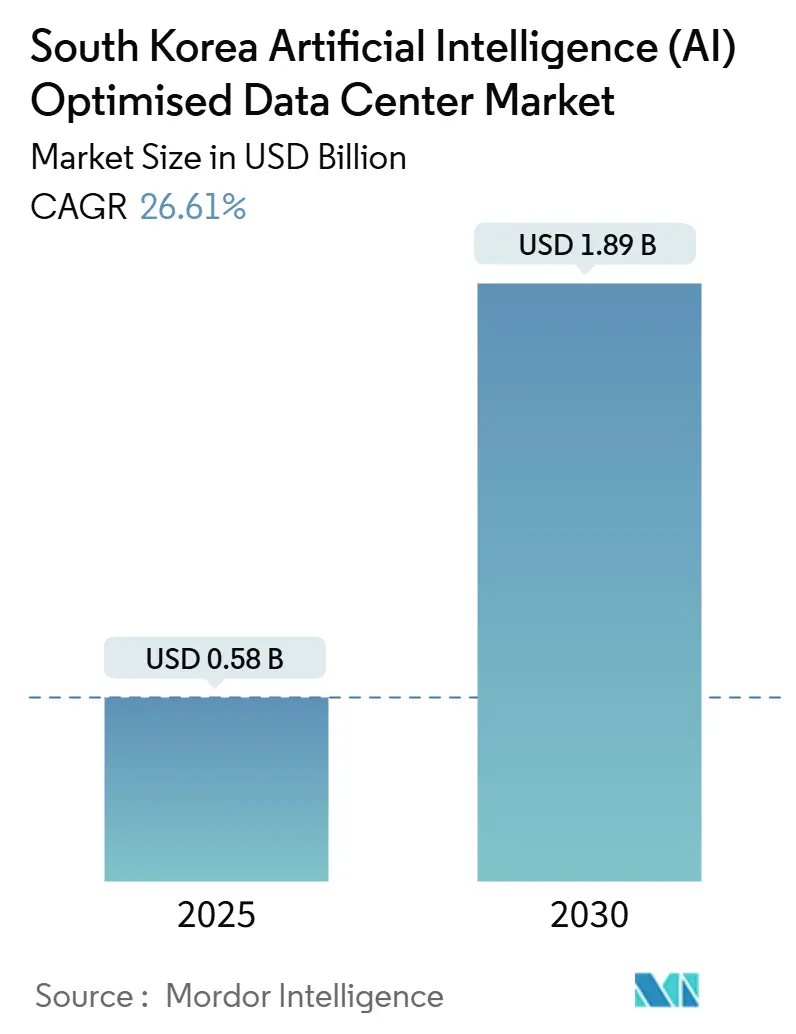

| Market Size (2025) | USD 0.58 Billion |

| Market Size (2030) | USD 1.89 Billion |

| Growth Rate (2025 - 2030) | 26.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea AI Data Center Market Analysis by Mordor Intelligence

The South Korea artificial intelligence data center market size stands at USD 0.58 billion in 2025 and is projected to reach USD 1.89 billion by 2030, reflecting a 26.61% CAGR. Surging public-sector funding, hyperscale cloud expansion, and nationwide 5G adoption converge to accelerate capacity additions. Rapid traffic growth from streaming video, online gaming, and generative-AI services keeps utilization rates high while encouraging operators to deploy edge nodes in secondary cities for latency-sensitive applications. Government incentives under the Digital New Deal lower financing costs for new-build facilities that incorporate high-density liquid cooling and renewable energy procurement. Competitive pressure centers on securing power allocations in the Seoul-Incheon corridor, prompting creative site-selection, such as repurposing idle industrial plants and colocating with green-energy projects. Operators that bundle managed AI platforms with colocated GPU clusters gain revenue diversity and deepen customer stickiness.

Key Report Takeaways

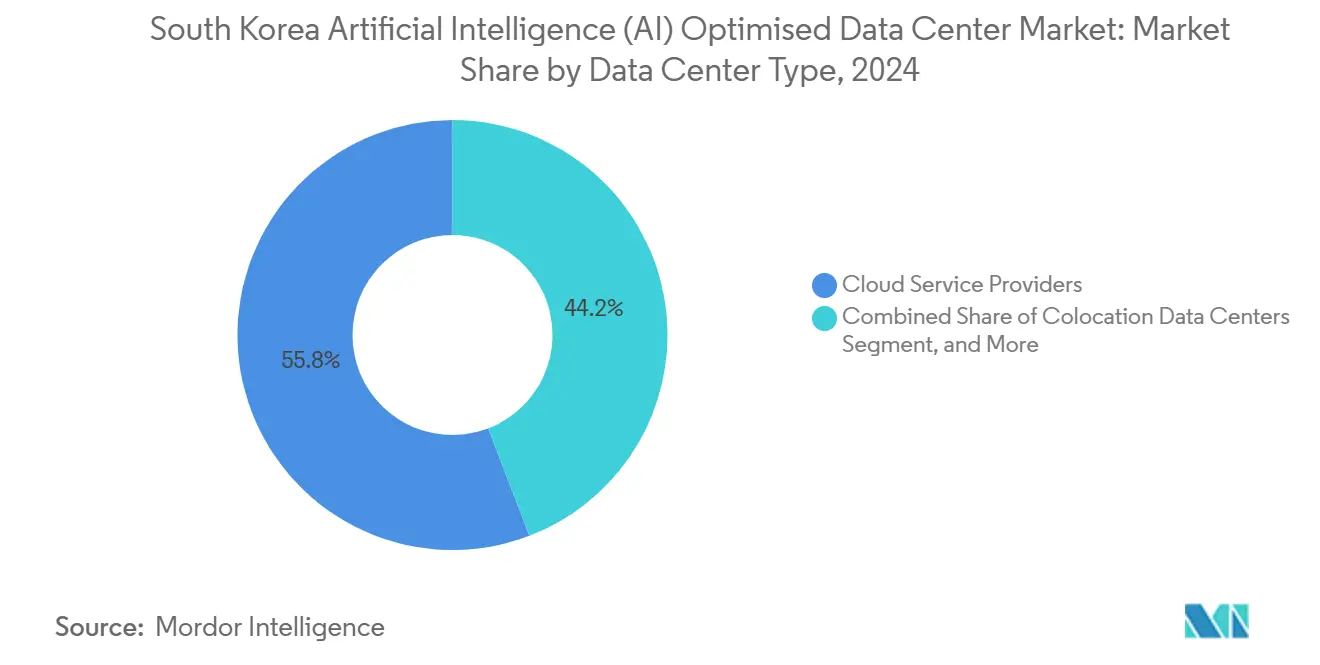

- By data center type, cloud service providers led with 55.82% of the South Korea artificial intelligence data center market share in 2024, while colocation data centers are advancing at a 28.23% CAGR through 2030.

- By component, software accounted for 45.83% of the South Korea artificial intelligence data center market size in 2024; hardware is growing fastest at 27.67% CAGR to 2030.

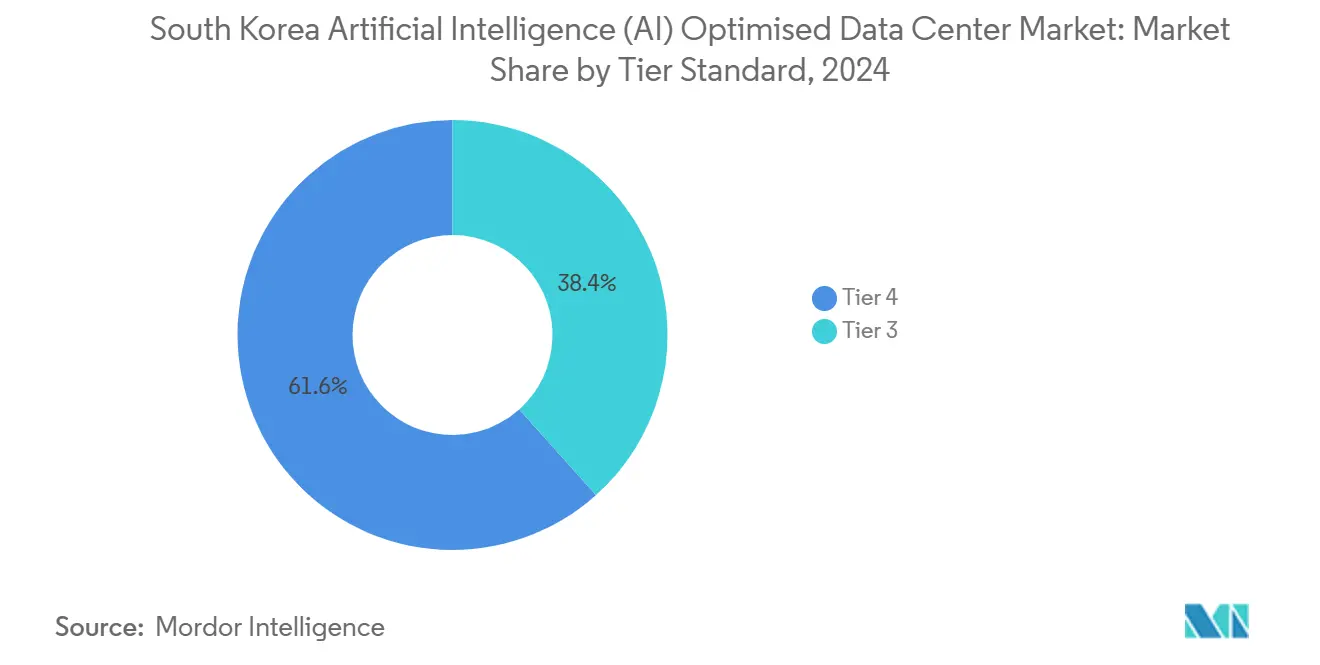

- By tier standard, Tier IV facilities captured 61.63% revenue share in 2024 in the South Korea artificial intelligence data center market, yet Tier III facilities are forecast to expand at a 28.77% CAGR over 2025-2030.

- By end-user, IT and ITES held 33.82% of spending in 2024 in the South Korea artificial intelligence data center market, while internet and digital media is projected to rise at a 27.45% CAGR to 2030

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea AI Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of cloud computing and edge computing services | +6.8% | National, concentrated in Seoul-Incheon corridor | Medium term (2-4 years) |

| Government incentives under "Digital New Deal" for AI infrastructure | +5.4% | National, with priority zones in Busan, Gwangju, Daegu | Long term (≥ 4 years) |

| Surge in 5G-driven data consumption and streaming traffic | +4.2% | National, early deployment in metropolitan areas | Short term (≤ 2 years) |

| Growing low-latency demand from autonomous vehicles and smart factories | +3.7% | Industrial clusters in Ulsan, Pohang, Changwon | Medium term (2-4 years) |

| Repurposing idle industrial sites for modular AI data centres | +2.9% | Rust belt regions, particularly Gyeonggi Province | Short term (≤ 2 years) |

| Corporate green-energy PPAs accelerating AI compute hubs | +3.6% | Coastal regions with renewable energy access | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Cloud Computing and Edge Computing Services

Enterprises are shifting legacy workloads into hyperscale cloud environments even as they deploy micro data centers at factories and retail sites for real-time inference. Average cloud migration rates rose 34% year-over-year, yet 41% of those same firms launched edge nodes in 2024 to keep latency below 10 ms for mission-critical processes.[1]Samsung SDS, “Sustainability Report 2024,” samsungsds.com SK Telecom and AWS integrated a 50 MW facility in Ulsan that hosts GPU clusters for training while distributing inference workloads to local edge cabinets, illustrating the hybrid architectures shaping the South Korea artificial intelligence data center market. The Personal Information Protection Act further sustains sovereign-cloud spending, ensuring sensitive datasets remain onshore even when models are globally orchestrated.

Government Incentives Under “Digital New Deal” for AI Infrastructure

The KRW 160 trillion stimulus reserves 23% for AI compute and connectivity, creating tax breaks, low-interest loans, and accelerated permitting for compliant projects. Public sector anchor tenants, such as the National AI Computing Center, pre-book capacity and de-risk greenfield builds in provincial cities. Operators meeting prescribed Power Usage Effectiveness targets qualify for incremental subsidies that can lower lifetime capex by 6-8%.[2]Korea Development Bank, “Technology Finance Report,” kdb.co.kr The resulting project pipeline positions the South Korea artificial intelligence data center market for sustained double-digit expansion through 2030.

Surge in 5G-Driven Data Consumption and Streaming Traffic

With 48% 5G penetration, video and gaming traffic climbed 3.8× in 2024, overwhelming first-generation metro data centers. Content providers turned to AI-powered caching and adaptive-bitrate algorithms that require GPU resources close to users. Esports platforms demand sub-20 ms round-trip latency, steering investments toward metro-edge facilities that blend content delivery and inference accelerators. Regulators maintain strict net-neutrality rules, forcing operators to over-provision backbone capacity rather than throttling peak loads.

Growing Low-Latency Demand from Autonomous Vehicles and Smart Factories

Hyundai Motor’s autonomous fleets generate 4 TB of sensor data per vehicle-hour, necessitating roadside or factory-level inference for obstacle detection within 5 ms. Samsung’s smart-factory AI deployments rely on embedded racks that flag defects in real time to avoid line stoppages. Compliance with ISO 27001 and IEC 62443 promotes air-gapped edge architectures that sync processed data back to hyperscale clusters for retraining, uplifting demand for both central and distributed capacity in the South Korea artificial intelligence data center market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating expenditure requirements | -4.2% | National, acute in Seoul metropolitan area | Short term (≤ 2 years) |

| Stringent environmental regulations on energy and water use | -2.8% | National, stricter enforcement in urban areas | Medium term (2-4 years) |

| Power-grid constraints in Seoul metropolitan area | -3.1% | Seoul-Incheon corridor, spillover to Gyeonggi | Short term (≤ 2 years) |

| Talent shortage for AI-optimised DC operations engineers | -2.6% | National, concentrated in technical roles | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Expenditure Requirements

AI-grade halls cost USD 12 million per MW in Seoul, 50% above conventional facilities, driven by liquid cooling loops, redundant 400 Gbps fabrics, and GPU procurement premiums. Operating costs escalate as dense racks push energy intensity 40% higher than legacy systems while specialist engineers command 30% salary uplifts. Import dependencies on GPU silicon expose operators to exchange-rate swings that inflate bill-of-materials by up to 20% in weak-won periods.

Stringent Environmental Regulations on Energy and Water Use

Cooling water consumption caps at 1.2 L per kWh compel adoption of dry coolers and immersion tanks that raise upfront costs by 25%. From 2026, Seoul’s carbon limits require PUE under 1.3, forcing retrofits or risk operational penalties. Environmental impact assessments add 6-12 months to project schedules and USD 2-3 million in consulting outlays, tempering new entrant enthusiasm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Providers Lead Hybrid Transformation

Cloud Service Providers continued to dominate, retaining 55.82% revenue in 2024, while the colocation segment is accelerating with a 28.23% CAGR. This mix shows enterprises blending hyperscale training clusters with rentable edge racks to balance sovereignty and scalability. In 2024, 67% of new AI workloads adopted hybrid deployment spanning at least two facility types.[3]SK Telecom, “Cloud Strategy Report 2024,” sktelecom.com Colocation operators now pre-install liquid-ready risers and 400 Gbps leaf-spine fabrics to attract latency-sensitive AI inference contracts. The South Korea artificial intelligence data center market keeps evolving as enterprises prefer seamless workload portability between on-premises GPU pods and cloud VMs.

Managed hosting remains essential for regulated sectors that cannot fully outsource data, sustaining moderate growth in enterprise-class halls. Edge micro-data centers situated inside manufacturing parks underscore the market’s geographic dispersion. The Korea Internet and Security Agency’s zero-trust guidelines also heighten demand for secure inter-facility links, reinforcing the relevance of multi-type strategies in the South Korea artificial intelligence data center industry.

By Component: Hardware Acceleration Drives Infrastructure Refresh

Software retained 45.83% of spending in 2024, reflecting license fees for orchestration platforms and AI frameworks, yet Hardware posted the fastest 27.67% CAGR as every new hall pivots to GPU racks drawing 700 W per chip.[4]NVIDIA, “H100 GPU Partnership Report,” nvidia.com The South Korea artificial intelligence data center market size for hardware surpassed USD 0.2 billion in 2024 and is projected to triple by 2030 on the back of high-bandwidth memory GPUs and 800 Gbps optical interconnects. Liquid cooling rollouts shift CAPEX allocations toward infrastructure subsystems instead of traditional chiller plants.

Professional services rise as firms seek workload tuning and capacity-planning expertise. Consulting contracts now bundle energy-optimization, model-partitioning, and compliance assessments, underscoring how software and services monetize beyond one-off hardware purchases. Sovereign-cloud mandates drive proprietary accelerator development, a trend likely to diversify the supply chain within the South Korea artificial intelligence data center market.

By Tier Standard: Edge Demands Drive Tier III Acceleration

Tier IV commanded 61.63% revenue in 2024 because banks and SaaS giants still favor “five-nines” uptime. Yet Tier III capacity is expanding at 28.77% CAGR, chiefly for edge and industrial deployments where 2N power redundancy suffices and latency trumps absolute resiliency. Tier III’s lower capex profile, roughly 40% below Tier IV, frees budgets for GPU density upgrades rather than diesel backup arrays.

The Korea Data Center Association now drafts AI-centric guidelines evaluating cooling adequacy and rack-level power densities instead of traditional tier nomenclature. This evolution ensures that both Tier III and Tier IV facilities will coexist as complementary rather than competing options within the South Korea artificial intelligence data center market.

By End-User Industry: Media Streaming Accelerates AI Adoption

IT and ITES maintained their leadership at 33.82% due to continual platform-development demand. Internet and Digital Media stands out with a 27.45% CAGR, amplified by streaming services that employ AI for content recommendation and video upscaling. In 2024, Naver processed 2.3 billion queries a day, driving its hardware refresh cycles every 18 months.

BFSI interest climbs as anti-fraud and algorithmic trading workloads intensify. Health-care deployments, such as Samsung Medical Center’s imaging AI, require localized processing to comply with patient-data rules. Manufacturing integration of predictive maintenance illustrates industrial AI’s shift from pilot to production, further diversifying consumption patterns in the South Korea artificial intelligence data center market.

Geography Analysis

Seoul-Incheon hosts roughly 65% of national capacity due to unmatched fiber density and proximity to enterprise headquarters. Land scarcity and 50 MW grid caps, however, spur a wave of expansion into Busan, Daejeon, and Daegu. Busan’s submarine cable gateway offers latency advantages for international traffic and has earmarked 200 MW parcels in its AI cluster zone. Government tax holidays and accelerated depreciation make provincial builds financially appealing.

Gwangju’s government-backed National AI Data Center anchors a regional ecosystem, incentivizing hyperscalers to colocate satellite halls nearby. Daegu and Ulsan draw automotive and electronics tenants requiring on-site inference for factory automation. Jeju Island’s green-power surplus positions it as a training-job destination where workloads can tolerate longer response times but benefit from 100% renewable electricity. The resulting dispersal relieves pressure on Seoul’s constrained grid and shapes a multi-node topology for the South Korea artificial intelligence data center market.

Competitive Landscape

Domestic telecom giants SK, KT, and LG combine carrier-grade networks with deep government ties, giving them first-mover advantage in obtaining permits and power. International specialists Equinix and Digital Realty import hyperscale design templates and global interconnection fabrics valued by multinationals. Land prices above USD 2,000 per m² in Seoul encourage joint ventures that spread risk and share scarce utility quotas.

Innovation focal points include liquid-immersion and direct-to-chip cooling, 800 Gbps optical fabrics, and automated energy-management software. Patent filings related to AI-adaptive thermal controls surged 340% in 2024, indicating a technology race that may reshape share positions. Edge computing remains a white-space segment where no single operator holds more than 15% capacity, presenting expansion headroom for new entrants in the South Korea artificial intelligence data center market.

South Korea AI Data Center Industry Leaders

KT Corporation (IDC Business Unit)

SK Broadband Co., Ltd.

LG CNS Co., Ltd.

Naver Cloud Corp.

Kakao Enterprise Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: KT Cloud is set to establish an AI Data Center Demonstration Center in Seoul, South Korea. Scheduled to launch in November 2025, the center will be located at KT's Mok-dong DC 2 Center in the Yangcheon District. It will focus on implementing AI-based automated data center operation technologies, optimizing power consumption, cooling, and network operations, and incorporating renewable energy and liquid cooling systems.

- March 2025: Fir Hills Inc., a new venture, plans to develop a 3GW AI data center in South Korea, with an estimated investment ranging from USD 10 billion to USD 35 billion. The company has signed a Memorandum of Understanding (MoU) with Governor Kim of Jeollanam-do Province for the project, which is expected to include advanced cooling infrastructure to manage energy load variations typical of AI workloads. Construction is expected to begin in winter 2025, with completion targeted for 2028. The project aligns with South Korea's broader efforts to expand its data center capacity, following similar announcements in Jeollanam-do and Gangwon Provinces in recent years.

- January 2025: KT announced a USD 250 million retrofit of its Mok-dong campus to add 20 MW of immersion-cooled AI capacity.

- December 2024: SK Telecom and AWS completed Phase 1 of their 50 MW Ulsan AI data center, deploying H100 clusters for regional model training.

South Korea AI Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How fast is capacity in the South Korea artificial intelligence data center market expected to expand?

Installed capacity is forecast to climb from USD 0.58 billion in 2025 to USD 1.89 billion by 2030, implying a robust 26.61% CAGR.

Which facility tier is growing the quickest?

Tier III sites are projected to post a 28.77% CAGR as edge computing takes hold in industrial clusters outside Seoul.

What fuels the surge in colocation demand?

Hybrid cloud strategies and sovereign-data regulations push enterprises to rent high-density GPU racks that complement public cloud resources while maintaining control over sensitive AI workloads.

How are operators addressing Seoul’s power constraints?

Strategies include migrating builds to Busan and Gwangju, signing renewable PPAs for guaranteed supply, and deploying immersion cooling to reduce total power draw.

Which end-user segment shows the strongest growth momentum?

Internet and Digital Media is advancing at 27.45% CAGR through 2030 as streaming, gaming, and generative-AI platforms ramp up GPU consumption.

Page last updated on: